Turf And Ornamental Inputs Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 5.38 Billion |

| Market Size (2031) | USD 7.05 Billion |

| Growth Rate (2026 - 2031) | 5.55% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Turf And Ornamental Inputs Market Analysis by Mordor Intelligence

The turf and ornamental inputs market size is expected to grow from USD 5.1 billion in 2025 to USD 5.38 billion in 2026 and is forecast to reach USD 7.05 billion by 2031 at 5.55% CAGR over 2026-2031. Growth stems from accelerating adoption of precision-spray systems, stricter environmental regulations that favor bio-based inputs, and renovation cycles triggered by climate stress. Demand is concentrated in professional sports venues and golf courses that require uniform playing surfaces, yet residential landscapes contribute a steady volume due to water-efficient turf conversions. Input manufacturers are reshaping portfolios toward low-toxicity chemistries, while equipment suppliers bundle software analytics with autonomous sprayers to maintain efficacy at lower use rates. The turf and ornamental inputs market is also benefiting from insurance-mandated integrated pest management documentation, which stimulates demand for digital record-keeping and certified applicator services.

Key Report Takeaways

- By input type, pesticides accounted for 45.30% of the turf and ornamental inputs market share in 2025, whereas bio-stimulants are advancing at a 9.25% CAGR through 2031.

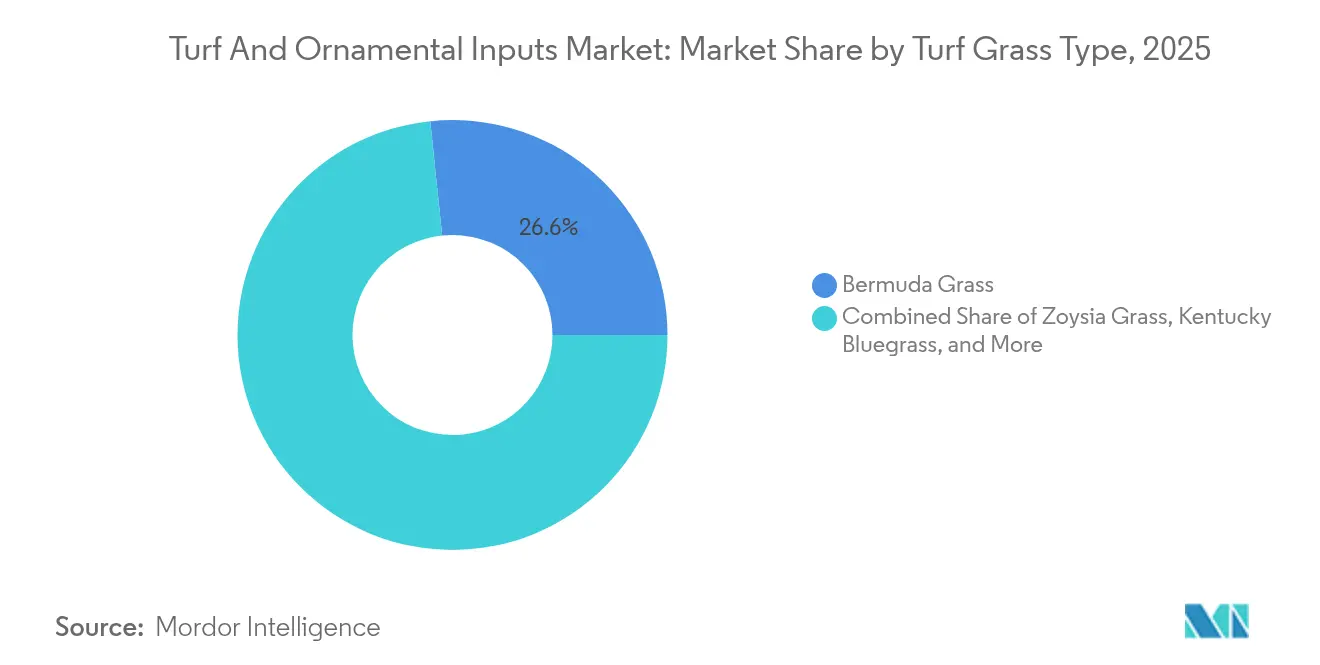

- By turf grass type, Bermuda grass led with 26.65% of the turf and ornamental inputs market size in 2025, and Zoysia grass is forecast to post a 7.45% CAGR to 2031.

- By ornamental grass type, feather reed grass captured 22.20% revenue share in 2025, while fiber optic grass is projected to register an 8.15% CAGR through 2031.

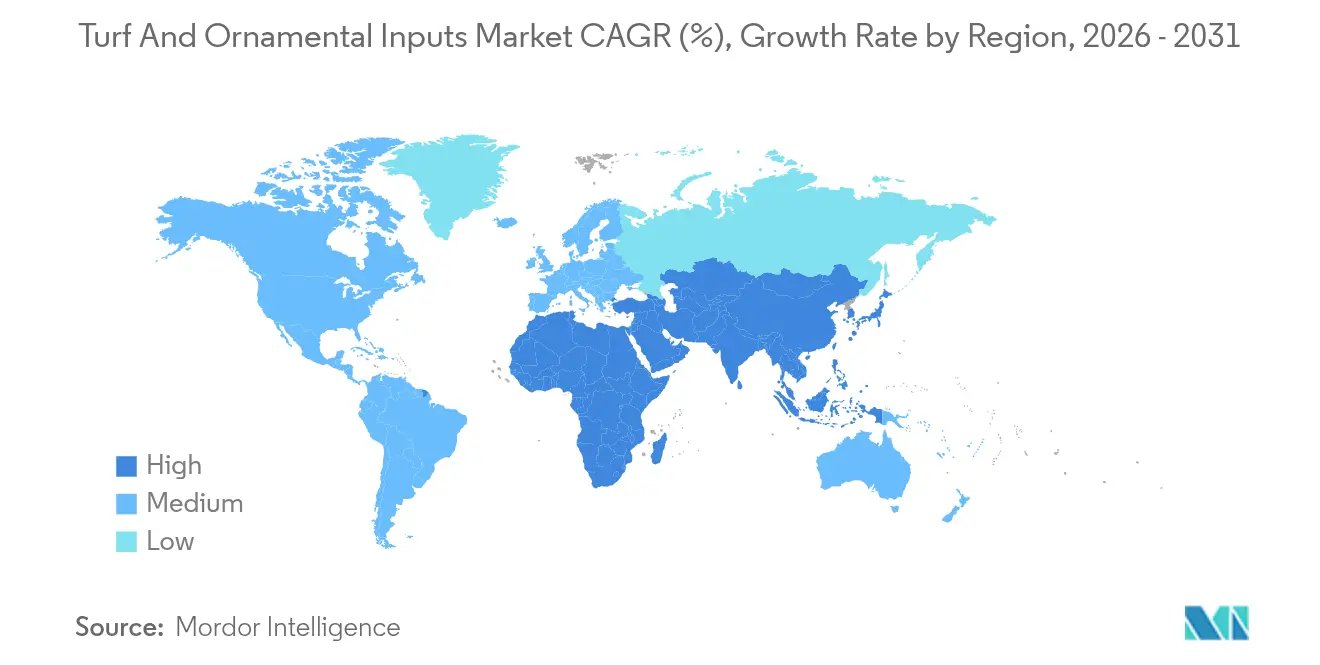

- By geography, North America held 34.60% of the turf and ornamental inputs market share in 2025, and Asia-Pacific is growing the fastest at a 6.55% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Turf And Ornamental Inputs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Precision-spray technologies reduce chemical over-application | +1.2% | North America and Europe core, expanding to Asia-Pacific | Medium term (2-4 years) |

| Shift toward low-toxicity bio-based formulations | +0.9% | Global, with strongest adoption in Europe and North America | Long term (≥ 4 years) |

| Turf rebuild after 2024-2026 El Niño damage | +0.8% | Asia-Pacific and South America primary, secondary effects in North America | Short term (≤ 2 years) |

| Climate-linked insurance requiring IPM compliance | +0.6% | North America and Europe, expanding to developed Asia-Pacific markets | Medium term (2-4 years) |

| Outsourced sports-turf management contracts | +0.5% | Global, concentrated in urban markets with professional sports infrastructure | Long term (≥ 4 years) |

| Golf-course renovations ahead of PGA/LPGA calendar expansion | +0.4% | North America and Europe primary, selective Asia-Pacific venues | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Precision-spray Technologies Reduce Chemical Over-application

Autonomous sprayers equipped with computer vision identify individual weeds and apply herbicide only where needed, slashing use rates by as much as 90% while preserving control levels. Drone-based spot applications verified by Texas A&M University and USDA research replicated full-coverage weed control yet used 67% less chemical, lowering both cost and environmental load.[1]Source: USDA Agricultural Research Service, “Drone-Based Spot Spraying Research,” USDA.GOV Equipment costs continue to decline, and university extension services now offer operator training that accelerates adoption. Municipal restrictions near waterways further incentivize the use of precision equipment, as it documents compliance. For buyers, return on investment occurs within three seasons owing to input savings and reduced re-spray labor. As a result, the turf and ornamental inputs market increasingly ties product sales to hardware and software ecosystems that optimize timing and placement.

Shift Toward Low-toxicity Bio-based Formulations

Municipal bans on certain synthetics have prompted distributors to expand their lines of bio-stimulants and organic-certified pesticides, now the fastest-growing segment within the turf and ornamental inputs market. BASF’s 2024 launch of the Aramax fungicide illustrates how legacy producers are reformulating active ingredients to lower persistence while preserving spectrum. End-users report that bio-based products often require shorter re-application intervals, creating steady demand for service contractors who can manage tighter schedules. Corporate campuses and homeowner associations are increasingly stipulating low-impact programs in bid documents, thereby broadening the customer base. While price premiums persist, controlled-release coatings and microbial carriers are improving longevity, which narrows total-cost gaps with conventional chemistries. The trend is long-lived because it is supported by regulation, client preference, and supplier innovation.

Turf Rebuild After 2024-2026 El Niño Damage

Heat spikes and erratic rainfall led to widespread turf loss across the Asia-Pacific and parts of South America, forcing courses and sports fields to reseed with drought-tolerant cultivars. Research indicates that nighttime temperatures are increasing at a faster rate than daytime highs, thereby reducing the recovery windows for cool-season species.[2]Source: BIGGA Editorial Team, “Five Ways Climate Change Is Affecting Golf Courses,” BIGGA.ORG.UK Renovation projects, including root-zone reconstruction and drainage retrofits, increase demand for soil amendments and wetting agents. Insurance payouts for damage frequently cover the cost of replacement seeds and specialty fertilizers, thereby accelerating sales cycles. Suppliers that bundle seed genetics with bio-stimulant starter packs have gained share because they streamline procurement for time-sensitive restorations. The turf and ornamental inputs market is therefore experiencing temporary volume spikes in regions hardest hit by weather anomalies.

Climate-linked Insurance Requiring IPM Compliance

Insurers now require integrated pest management documentation for liability coverage at golf facilities and commercial landscapes, compelling owners to invest in monitoring software, calibrated spray equipment, and certified applicators. Policies emphasize safe storage, audited application logs, and adherence to buffer zones to curb runoff litigation risk. The mandate steers purchasing toward digital record-keeping tools bundled with sprayers, creating recurring revenue for equipment vendors. Service providers that can deliver turnkey compliance are winning multi-year contracts, reinforcing consolidation in the professional turf care industry. As documentation becomes standard, the turf and ornamental inputs market benefits through higher-value service packages linked to chemistry sales.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening PFAS and neonicotinoid bans | -1.1% | Europe and North America primary, expanding globally | Medium term (2-4 years) |

| Labor shortages limiting professional turf service frequency | -0.8% | Global, most severe in developed markets | Long term (≥ 4 years) |

| Micro-dosing robotics delaying bulk chemical demand | -0.6% | North America and Europe early adoption, Asia-Pacific following | Long term (≥ 4 years) |

| Public pushback on fertilizer runoff in urban lakes | -0.5% | North America and Europe urban areas, expanding to Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Tightening PFAS and Neonicotinoid Bans

California’s 2024 PFAS restrictions eliminated several legacy turf products, and the European Commission is preparing similar measures that will further shrink chemical portfolios. Replacement formulas often carry higher per-unit costs and different application windows, which can disrupt established programs. Stringent buffer-zone rules add scheduling complexity and may require specialized nozzle sets, raising capital outlays for smaller contractors. Manufacturers are racing to reformulate, but development timelines compress margins. Until compliant alternatives scale, the turf and ornamental inputs market will face friction in product availability and user confidence.

Micro-dosing Robotics Delaying Bulk Chemical Demand

Robotic spot sprayers achieve up to 79% reduction in herbicide use compared with blanket applications, while retaining efficacy, and shift demand toward concentrated formulations rather than bulk drums.[3]Source: Frontiers Editorial Board, “Reduction of Chemical Inputs by Smart Spot Sprayer Technology,” FRONTIERSIN.ORG Early adopters often sign multi-year software subscriptions with equipment vendors, redirecting budget from chemicals to data services. Although high-value adjuvants continue to sell, the overall volume per acre declines. As unit economics improve, broader adoption could cap total market volumes despite rising installed turf area.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Turf Grass Type: Warm-Season Cultivars Sustain High-Traffic Performance

Bermuda grass held 26.65% of the turf and ornamental inputs market size in 2025, underscoring its status as the workhorse for warm-season sports venues and commercial landscapes. Its aggressive growth habit demands consistent nitrogen and targeted pre-emergent herbicides, creating a steady pull-through for input suppliers. Zoysia grass is gaining momentum at a 7.45% CAGR because improved cold tolerance expands its viable zone into transition regions. Kentucky bluegrass still commands a 24.25% share due to its visual appeal in northern climates, yet its water and disease needs remain high, making it a reliable consumer of fungicides and wetting agents.

Tall fescue adoption increases in drought-prone municipal parks, as its deep roots reduce irrigation bills. Ryegrass retains importance as an overseed during winter, supporting seed and fertilizer sales outside the main growing season. Ongoing cultivar development at Oregon State University targets traits such as salt tolerance and reduced clipping yield, which can reduce mowing labor. For suppliers, aligning agronomic packages with region-specific cultivars becomes essential to capture the next wave of growth in the turf and ornamental inputs market.

By Ornamental Grass Type: Design-Driven Demand for Low-Input Aesthetics

Feather reed grass accounted for 22.20% of ornamental revenue in 2025, reflecting landscaper preference for species that maintain form with minimal pruning and irrigation. Fountain grass is followed by its plume-like texture, which extends the seasonal interest. Fiber optic grass is the fastest growing segment, with an 8.15% projected CAGR, as designers seek novelty and adaptability to variable moisture conditions. Purple millet and Ravenna grass fill niches in naturalistic plantings and large-scale commercial sites, respectively, each benefiting from movement toward native and climate-resilient palettes.

Maintenance profiles of these species lean on controlled-release fertilizers and periodic fungicide programs rather than intensive weekly treatments. That pattern broadens the customer base beyond golf to municipalities and corporate campuses that value sustainability credentials. As urban planners integrate bioswales and rain gardens, demand emerges for grasses that stabilize soil and tolerate fluctuating water tables, creating crossover opportunities for wetting agents and bio-stimulants. The ornamental category, therefore, keeps the turf and ornamental inputs market diversified across end-use sectors.

By Input Type: Chemistry Transitions Reshape Revenue Mix

The pesticides segment contributed 45.30% of 2025 sales by delivering reliable control of weeds, insects, and pathogens that can jeopardize playability and aesthetics. Regulatory scrutiny, especially toward PFAS and neonicotinoids, caps volume growth and encourages migration to low-toxicity alternates. Fertilizers remain foundational, yet slow-release granules and variable-rate application tech temper total tonnage. Plant growth regulators grow annually as courses aim to reduce mowing frequency and conserve fuel.

Bio-stimulants represent the fastest-growing line within the turf and ornamental inputs market, with an estimated 9.25% CAGR, as they enhance stress tolerance without introducing regulated residues. Wetting agents and surfactants, though smaller in value, gain relevance as water scarcity makes uniform infiltration vital. Equipment-linked platforms now bundle adjuvant recommendations with sensor data, ensuring optimal uptake and reinforcing brand loyalty. Altogether, the input mix is shifting toward integrated programs that balance chemistry, biology, and data.

Geography Analysis

North America commanded 34.60% of global revenue in 2025, driven by its extensive golf course network and professional sports footprint. The United States alone hosts more than 1,250 courses in Florida, each requiring high-intensity fertility and protection programs that drive steady demand. Precision-spray adoption and insurance-driven IPM documentation are expected to sustain a significant CAGR through 2030, even as the installed base matures. Canada and Mexico add incremental volume through growing sports tourism and urban greening projects that mirror the best practices of the United States.

The Asia-Pacific region is the fastest-growing region, with a 6.55% CAGR through 2031, driven by rapid urbanization, increasing middle-class spending, and national initiatives to expand recreational spaces. China invests in public golf despite earlier course caps, while Japan upgrades aging sports infrastructure ahead of international events. India’s metropolitan parks are embracing drought-tolerant turf varieties, which stimulate seed and bio-stimulant imports. Equipment suppliers partner with local dealers to introduce autonomous mowing fleets, which offset labor shortages and accelerate the penetration of precision inputs across the region.

Europe grows annually as environmental mandates shift spending toward compliant chemistries and data-driven application systems. Germany and the United Kingdom lead in the adoption of buffer-zone mapping tools that minimize drift. Southern Europe, prone to water stress, invests in wetting agents and low-input warm-season grasses. South America, the Middle East, and Africa post impressive CAGRs, reflecting tourism investments and mega-sporting events that require elite playing surfaces. In these emerging regions, distributors that offer technical training capture early loyalty, positioning themselves favorably as regulatory frameworks become more stringent.

Regulatory Landscape

Regulation is tightening around active ingredients and formulation components used in turf and ornamental programs, which is increasing portfolio turnover toward lower-toxicity and bio-based options. In the United States, state-level actions on neonicotinoids are already affecting outdoor ornamental and turf use. New York State DEC implemented Phase 1 of its Birds and Bees Protection Act in December 2024, banning outdoor ornamental and turf use of clothianidin and dinotefuran, and scheduled Phase 2 for December 2026 to expand restrictions to additional neonicotinoids, including imidacloprid, thiamethoxam, and acetamiprid. At the federal level, the US EPA continues to process registrations and new-use applications, including notices published in the Federal Register in June 2026 that include turf-related use patterns.

In Europe, EU-level plant protection rules are shaping label content and permissible formulation ingredients. In May 2026, Regulation (EU) 2026/1120 updated the list of unacceptable co-formulants by adding substances to Annex III of Regulation (EC) No 1107/2009, with Member States required to withdraw authorizations for affected products by 16 June 2028, setting a defined reformulation and relabeling timeline for suppliers. Also in May 2026, Regulation (EU) 2026/1123 introduced new labeling requirements for plant protection products, replacing Regulation (EU) No 547/2011, with compliance tied to authorizations granted on or after 1 January 2028. Approval extensions such as Implementing Regulation (EU) 2025/2316 (November 2025) provide temporary continuity for certain turf-relevant actives while the overall compliance burden rises.

Competitive Landscape

The turf and ornamental inputs industry exhibits moderate concentration. Bayer AG leads with its broad fungicide and herbicide lineup paired with agronomic advisory teams. Syngenta Group is leveraging proprietary seed treatments and supportive research stations. The top five players are Bayer AG, Syngenta Group, Corteva Agriscience, BASF SE, and SiteOne Landscape Supply Inc.

Recent consolidation underscores the strategic importance of distribution reach. W.S. Connelly’s March 2025 acquisition of AmeriTurf extends logistics coverage and adds proprietary blends that cater to course superintendents. AstroTurf Corporation’s early-2025 purchases of General Acrylics and Atlantic Sports Group broaden its construction arm, enabling bundled installation and maintenance contracts. Equipment makers capitalize on proprietary sensor suites and cloud platforms, capturing subscription revenue that supplements traditional sales of units.

Competitive advantage increasingly hinges on the ability to integrate inputs with hardware and data. Firms that combine bio-stimulants with drone analytics or offer app-based compliance logs build stickier client relationships. Customer service and local agronomic expertise remain critical differentiators, especially when navigating rapidly shifting regulatory landscapes. Niche opportunities persist for suppliers of climate-adaptive seed genetics and ultra-low-volume formulations that align with micro-dosing robotics.

Turf And Ornamental Inputs Industry Leaders

BASF SE

FMC Corporation

SiteOne Landscape Supply Inc

Bayer AG

Syngenta Group

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

The most immediate opportunity is in biological and IPM-adjacent solutions that help end users operate within tighter ingredient and runoff constraints while maintaining playability and aesthetics. BASF Agricultural Solutions completed its acquisition of AgBiTech in March 2026, strengthening access to biological insect control platforms designed for low-residue programs used by golf facilities, sports venues, and commercial landscapes. Portfolio refresh cycles for fungicides, insecticides, and herbicides in professional turf channels also continue, as indicated by Nufarm introducing new solutions for the golf turf industry at the GCSAA Conference and Trade Show in January 2026.

A second opportunity lies in the commercialization layer that connects chemistry and biologicals to precision-spray workflows and compliance documentation demanded by insurers and municipalities. As autonomous and spot-application systems reduce use rates, suppliers that package ultra-low-volume formulations, adjuvants, and decision-support tools, including digital application logs aligned with IPM requirements, can defend revenue per treated acre even as blanket applications decline. Distribution-scale players and specialized turf distributors can expand bundled programs across irrigation, agronomics, and plant protection to support a one-stop procurement model for contractors and course superintendents operating under stricter buffer-zone and ingredient constraints.

Recent Industry Developments

- July 2026: BASF launched Apthena, a biological insect attractant positioned to support Integrated Pest Management programs in professional turf and ornamental settings. The launch broadens BASFs biological toolset alongside conventional crop protection, aligning with end-user demand for lower-toxicity approaches and tighter documentation requirements.

- March 2026: SiteOne Landscape Supply completed the acquisition of Reinders, adding 12 locations across the US Midwest and expanding reach in irrigation and agronomics distribution. The deal strengthens SiteOnes ability to bundle turf inputs with irrigation and service-focused categories, improving availability and contractor coverage in core turf markets.

- December 2025: Syngenta announced federal registration by the US Environmental Protection Agency for Atexzo insecticide/miticide for use on golf courses and sod farms. The approval adds a new tool for managing insect and mite pressure in high-value turf, supporting rotation strategies as ingredient scrutiny and resistance management needs intensify.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers crop input products that are applied to turfgrass and ornamental grasses to maintain quality, manage pests, and support growth in professional and residential landscapes, reported as market value in USD at the global level.

Scope exclusions: We exclude turf equipment, irrigation hardware, and landscaping services because they are not input products consumed on turf or ornamental grass.

Segmentation Overview

- By Turf Grass Type

- Bermuda Grass

- Zoysia Grass

- Kentucky Bluegrass

- Ryegrass

- Tall Fescue

- Other Turf Grasses

- By Ornamental Grass Type

- Feather Reed Grass

- Fountain Grass

- Purple Millet

- Ravenna Grass

- Fiber Optic Grass

- Other Ornamental Grasses

- By Input Type

- Pesticides

- Fertilizers

- Plant Growth Regulators

- Wetting Agents and Surfactants

- Bio-stimulants

- Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- Europe

- Germany

- United Kingdom

- France

- Spain

- Italy

- Denmark

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- Thailand

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Kenya

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the fact base for the model and to keep assumptions consistent across regions. We relied on public sources such as USDA and other national agriculture departments, FAO datasets, customs and trade statistics portals, and EPA and EU regulatory publications that clarify active ingredient approvals and use restrictions. Where needed, patent databases and peer reviewed agronomy or turf management journals were checked to understand formulation shifts and adoption patterns.

In parallel, we reviewed company filings, investor presentations, annual reports, association websites, and reputable press coverage to map product positioning and regional exposure. A paid subscription focused on company financials and another subscription focused on news and financials were used selectively to speed up fact checks and capture corporate changes that can affect supply or pricing. The sources listed above are illustrative and not exhaustive, and many other public references were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary interviews and surveys were completed with a mix of input suppliers, distributors, and professional buyers such as golf course and sports turf managers, along with landscaping decision makers. Because this is a global market, perspectives were collected across Americas, EMEA, and APAC so regional seasonality, regulations, and product preferences could be reflected. Respondent input helped close gaps from the desk work and test the pricing and penetration assumptions used in the forecast.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 14% | APAC: 41% |

| Mid tier: 44% | Functional/Unit leaders: 36% | EMEA: 37% |

| Smaller Players: 21% | Managers: 50% | Americas: 22% |

Market-Sizing & Forecasting

Sizing started with a top-down build where the addressable demand pool was reconstructed using region level turf and ornamental activity indicators, then filtered through input intensity and product mix assumptions. To keep the numbers grounded, we corroborated totals using selective bottom-up approximations, such as sampled price per unit x treated area proxies, channel checks on distributor throughput, and supplier revenue exposure where disclosures allowed it.

Key inputs used in the model included (as illustrative examples) managed turf area trends tied to golf and sports facilities, residential lawn and landscape care intensity, pest and disease pressure by climate zone, regulatory tightening that shifts chemistry choices, and average selling price movement for fertilizers, pesticides, and plant growth regulators. Forecasting relied on scenario analysis supported by expert views on adoption of bio-based solutions, application frequency changes, and pricing pass-through behavior, which helped us keep the trajectory realistic when weather or policy shifts occur. When bottom-up signals were incomplete for smaller countries, gaps were handled using proxy ratios from similar climates and income levels, and then rechecked with primary feedback before finalizing regional totals.

Data Validation & Update Cycle

Outputs were validated through triangulation across independent signals, including regional demand indicators, product mix logic, and supplier and channel feedback, then variance checks were run to spot unusual jumps in volume or pricing. Where an outlier appeared, assumptions were revisited, and follow-up calls were triggered if the change could not be explained by seasonality, regulation, or one-time stocking patterns.

Before sign-off, the model and narrative go through multi-step analyst reviews so definitions, conversions, and year alignment stay consistent. Reports are refreshed annually, with interim updates when material events occur, and a final pre-delivery pass is done so clients receive the most current view available at the time of publishing.

Mordor Intelligence's Global Turf and Ornamental Inputs Market Market Estimate Compared With Other Published Estimates

Published market sizes for turf and ornamental inputs often vary because the market can be defined in multiple ways, and because some publishers lock assumptions earlier than others. Differences usually come from what is counted as an input, how pricing is converted into USD across regions, and whether the estimate is built from treated area logic or from broader landscaping spend proxies.

The biggest gap drivers in this market tend to be whether studies include only synthetic chemical inputs or also add adjacent items like seeds, soil amendments, or turf protection services, which can inflate totals. Another common driver is the way average selling prices are projected, where some estimates apply uniform inflation, while others adjust for regulation-driven chemistry shifts and changing application frequency by use case and climate.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 5.38 B (2026) | |

| Industry Publisher A | USD 7.36 B (2025) | This estimate is higher mainly because the scope is framed around broader synthetic chemical input baskets and is anchored to a different base year, which can pull in pricing and mix assumptions that do not align with treated turf and ornamental demand intensity. |

| Industry Publisher B | USD 8.04 B (2025) | The reported total likely reflects wider inclusion of input categories and a separate year alignment, and it can also be sensitive to how ASP progression is applied across regions with different regulatory constraints and application patterns. |

Overall, the spread in published values is largely explained by scope packing and year alignment, followed by how price and usage intensity are carried into the forecast. Keeping the model tied to treated area signals and input type coverage, rather than broader landscape spending, is what makes the market total more traceable in our approach, including the way turf and ornamental inputs are counted in Mordor Intelligence.

Key Questions Answered in the Report

What is the current value of the turf and ornamental inputs market?

The turf and ornamental inputs market size reached USD 5.38 billion in 2026 and is set to rise to USD 7.05 billion by 2031.

Which region is expanding the fastest?

Asia-Pacific is registering the highest regional CAGR at 6.55% due to rapid urbanization and new recreational facilities.

Which input category is growing at the quickest pace?

Bio-stimulants are the fastest-growing category, projected to climb at a 9.25% CAGR through 2031 because of regulatory and sustainability preferences.

Who are the leading companies?

The top five players are Bayer AG, Syngenta Group, Corteva Agriscience, BASF SE, and SiteOne Landscape Supply Inc.

Page last updated on: