Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 8.52 Billion |

| Market Size (2031) | USD 16.14 Billion |

| Growth Rate (2026 - 2031) | 13.62% CAGR |

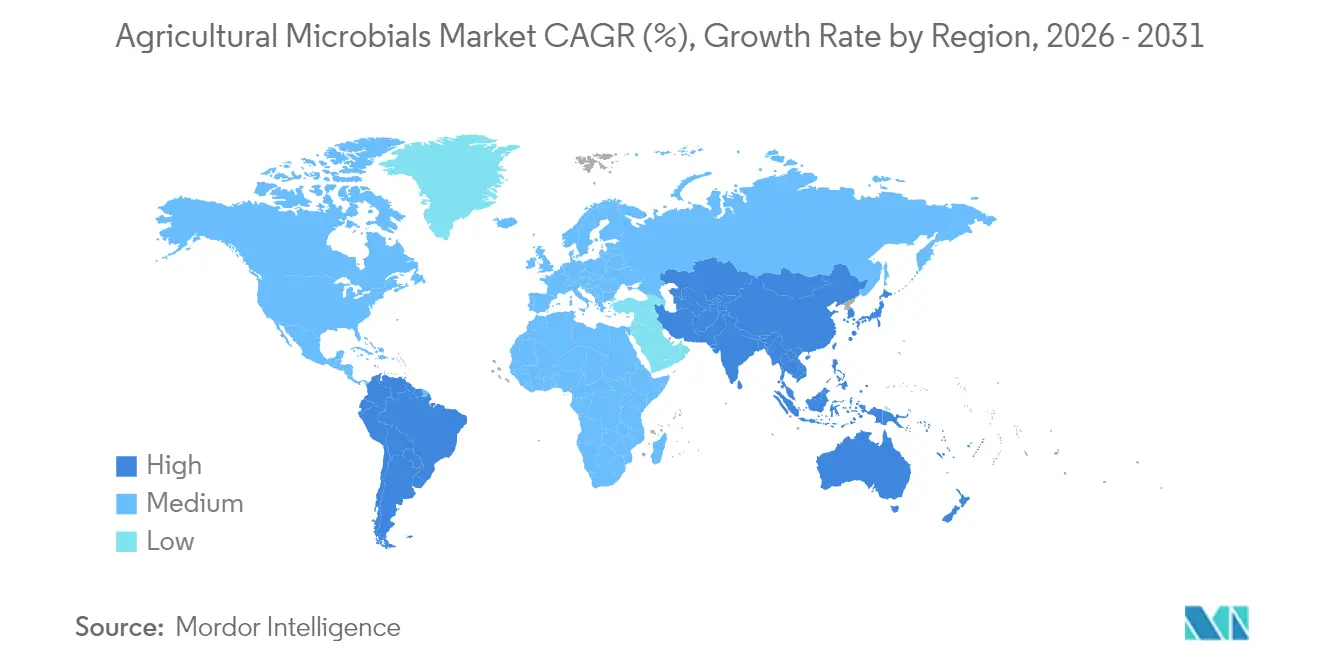

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

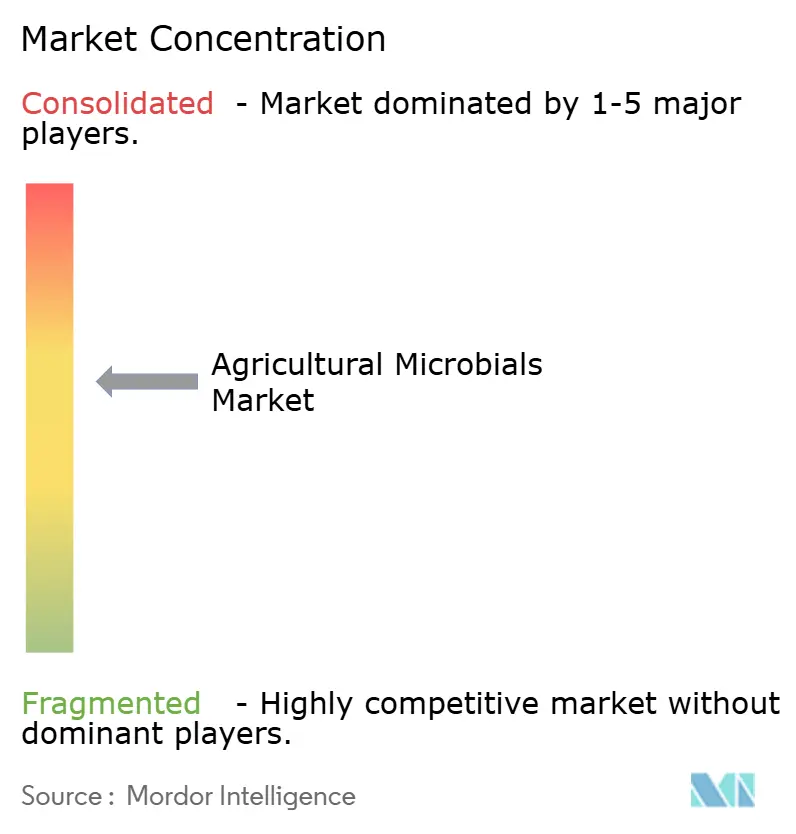

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Agricultural Microbials Market Analysis by Mordor Intelligence

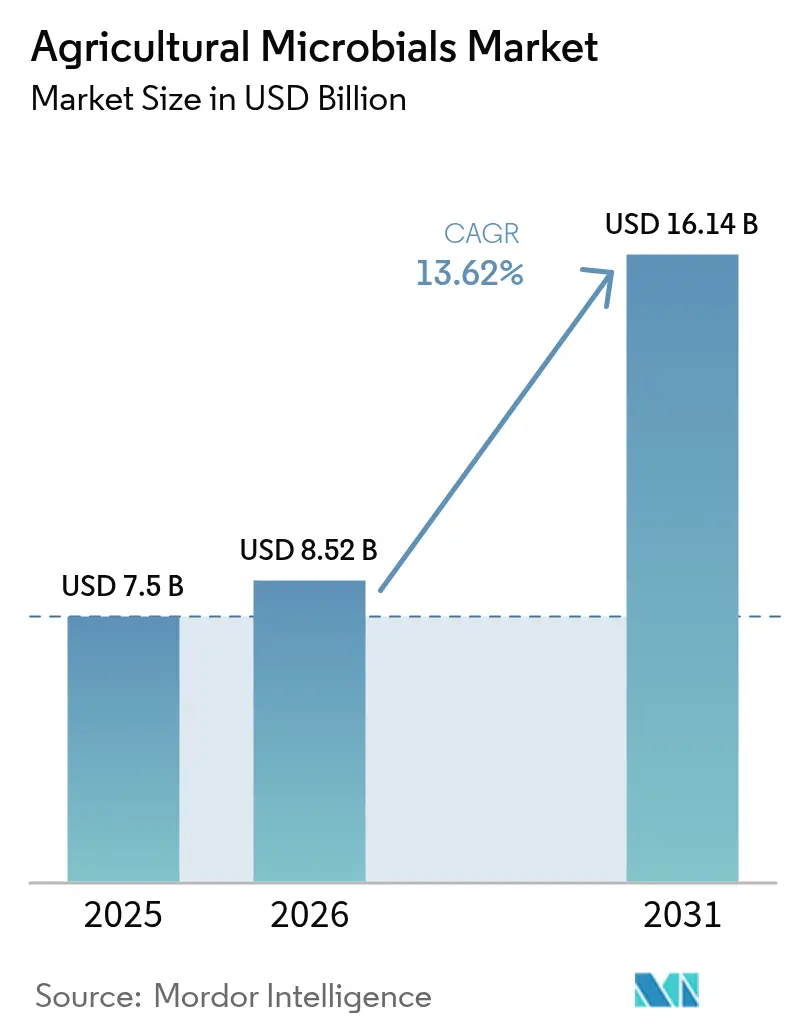

The agricultural microbials market size was valued at USD 7.50 billion in 2025 and estimated to grow from USD 8.52 billion in 2026 to reach USD 16.14 billion by 2031, at a CAGR of 13.62% during the forecast period (2026-2031). Input cost inflation for synthetic fertilizers, which rose sharply between 2022 and 2024, accelerates grower interest in biological replacements. Rapid growth reflects surging demand for residue-free food, mounting synthetic fertilizer costs, and global corporate sustainability mandates. AI-enabled strain discovery compresses product development cycles, allowing suppliers to refresh portfolios faster and address emerging pest resistance challenges.

Carbon-credit programs that pay USD 15-30 per metric ton of CO₂ equivalent for nitrogen reductions create an incremental income stream that makes microbial adoption cash-positive for many corn and soybean producers. Wider use of precision application tools lowers per-acre costs and improves field efficacy, encouraging adoption across large commercial farms and smallholder operations alike. Asia-Pacific remains the pivotal growth engine, supported by substantial government subsidies that lower farmer payback periods and by national fertilizer-reduction goals that favor biological inputs[1]Source: Ministry of Agriculture, Forestry and Fisheries Japan, “Green Food System Strategy,” maff.go.jp.

Key Report Takeaways

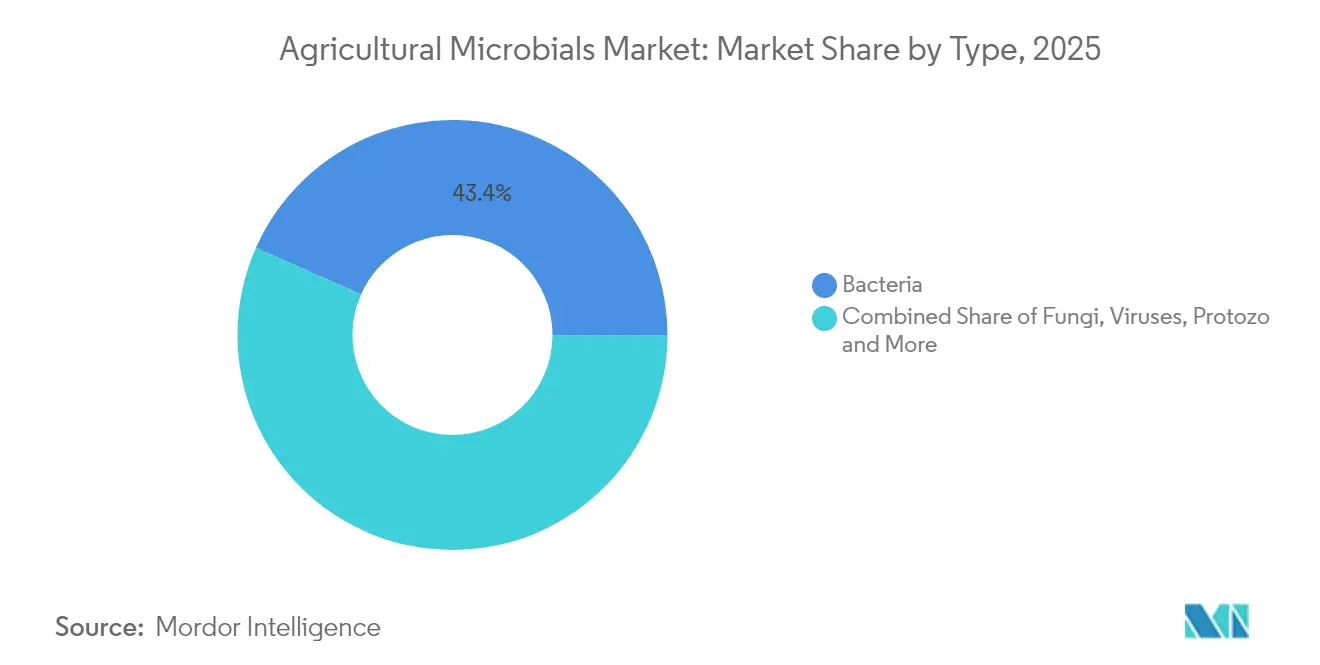

- By type, bacteria captured 43.35% of the agricultural microbial market share in 2025, while viruses are projected to expand at an 17.95% CAGR through 2031.

- By function, biopesticides led with a 48.10% revenue share in 2025, while biostimulants are forecasted to rise at a 15.05% CAGR through 2031.

- By application, fruits and vegetables commanded 28.70% of the agricultural microbials market size in 2025, while commercial crops are advancing at a 14.63% CAGR through 2031.

- By mode of application, seed treatment captured the largest share of the agricultural microbials market in 2025. Foliar spray is projected to expand at the fastest CAGR through 2031.

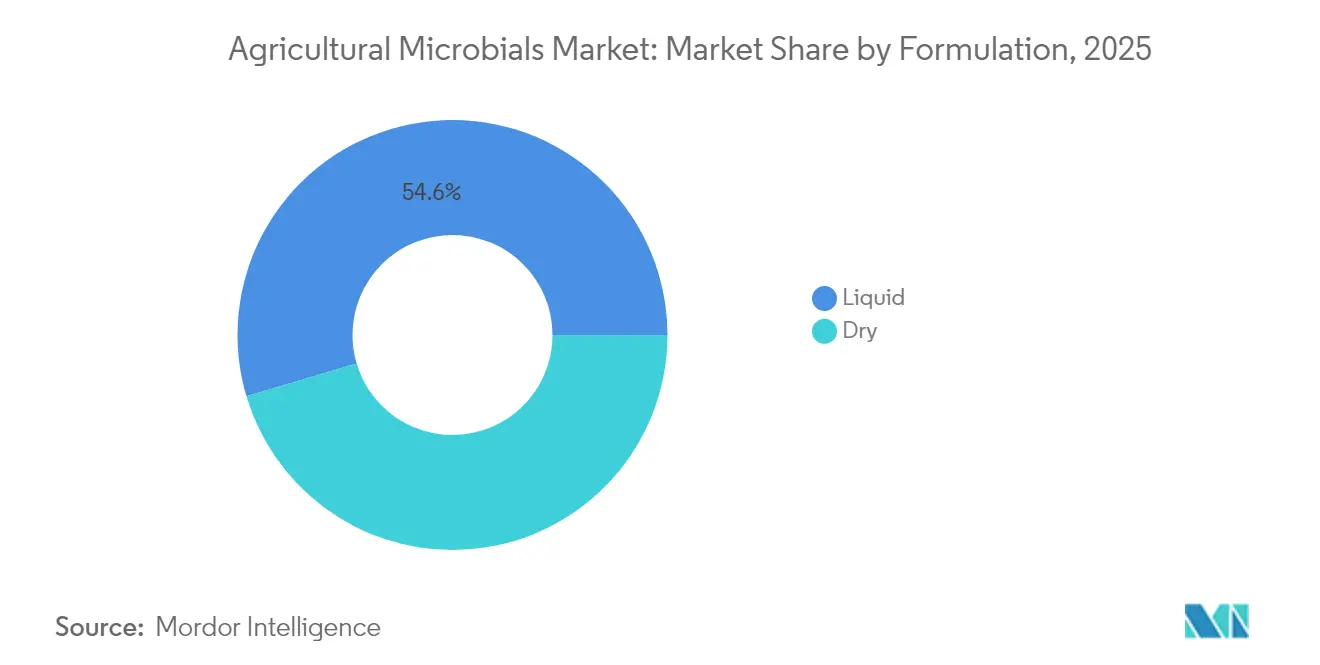

- By formulation, liquid products accounted for 54.60% of 2025 sales, while dry products are anticipated to expand at a 15.45% CAGR through 2031.

- North America held the largest share, accounting for 32.10% of the agricultural microbials market in 2025. Asia-Pacific is projected to register the fastest 16.83% CAGR through 2031.

- The top five suppliers including Bayer AG, BASF SE, Syngenta Group, Corteva Inc., and Novonesis A/S, held a majority share in the 2024 market revenue, confirming a moderately fragmented field with headroom for specialists.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Agricultural Microbials Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand for Residue-Free Food | +3.2% | Global premium produce markets | Medium term (2–4 years) |

| Expansion of Regenerative Agriculture Acreage | +2.8% | North and South America, expanding in the Asia-Pacific | Long term (≥4 years) |

| Government Subsidies for Bio-Inputs | +2.1% | Asia-Pacific core, European Union CAP zones, Brazil | Short term (≤2 years) |

| Rapid Strain Development Using AI and Omics | +1.9% | Biotech hubs in the United States, European Union, and Israel | Medium term (2–4 years) |

| Carbon-Credit Monetization for Reduced Chemical Use | +1.6% | Developed-market supply chains | Medium term (2–4 years) |

| Push from food majors’ Scope-3 emissions targets | +1.4% | North America and the European Union, scaling worldwide | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Residue-Free Food

Retailers’ zero-residue pledges pressure growers to adopt biological inputs, and Walmart now requires compliance across more than 2,000 suppliers. The European Union’s Farm to Fork Strategy seeks a 50% cut in chemical pesticide use by 2030[2]Source: European Commission, “Farm to Fork Strategy,” europa.eu. In high-value berries, leafy greens, and tree fruits, visible residue risks costly recalls, accelerating the agricultural microbials market shift toward biological crop protection. Export-oriented growers in South America and Asia follow these standards to secure market access. This retail-driven alignment between consumer expectations and regulation amplifies global demand for microbials.

Expansion of Regenerative Agriculture Acreage

Regenerative acres in the United States exceeded 15 million in 2024, a 35% yearly rise[3]Source: USDA Natural Resources Conservation Service, “Regenerative Agriculture Practices,” usda.gov. Commitments from Cargill, Incorporated, and Archer Daniels Midland Company to source from regenerative farms ensure durable demand for soil-enhancing microbes. University of Illinois research documented comparable yields and 12-18% lower input costs over three-year rotations, validating the value proposition. Brazil added 8 million hectares of soybean and corn under regenerative practices, stimulating sales of nitrogen-fixing bacteria and mycorrhizal fungi. These successes demonstrate how regenerative systems underpin long-term expansion of the agricultural microbials market.

Government Subsidies for Bio-inputs

India budgeted USD 2.1 billion in 2024 for the adoption of microbial inputs and layer state-level support, covering 50-75% of product costs. China’s 14th Five-Year Plan grants tax incentives that cut farmer expenses by 30-40% on biological pesticides. The European Union dedicates EUR 50 billion (USD 54 billion) through 2027 for eco-schemes that prioritize biological inputs. These programs remove cost barriers and accelerate smallholder purchases, directly bolstering the agricultural microbials market penetration.

Rapid Strain Development Using AI and Omics

Computational biology platforms are enhancing microbial strain development by predicting gene combinations prior to laboratory testing. The acquisition of Zymergen Inc. by Ginkgo Bioworks Holdings, Inc. for USD 300 million in 2024 highlighted the potential of AI-driven strain optimization platforms. Machine learning algorithms enable the screening of millions of genetic combinations in silico, reducing strain discovery timelines from 36 months to 12 months. CRISPR-Cas gene editing technologies enable precise modifications to microbial genomes, resulting in strains with enhanced survival rates in diverse soil conditions and improved pest control efficacy. The integration of synthetic biology and artificial intelligence attracted USD 1.8 billion in venture capital funding to agricultural biotechnology startups in 2024. Patent filings for genetically modified microbial strains increased by 340% between 2022 and 2024, indicating a rise in innovation in this field.

Restraints Impact Analysis*

| Restraint | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Inconsistent Field Efficacy Across Micro-Climates | -2.4% | Global, acute in tropical and arid zones | Short term (≤2 years) |

| Cold-Chain Requirements for Live Formulations | -1.8% | Developing regions with sparse refrigeration | Medium term (2–4 years) |

| Limited Shelf Life Versus Synthetic Chemicals | -1.6% | Global distribution networks | Short term (≤2 years) |

| Complex Regulatory Approval Timelines | -1.2% | Markets with evolving bio-input rules | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Inconsistent Field Efficacy Across Micro-climates

Microbial products show inconsistent performance across soil types, pH levels, and climatic conditions, which creates barriers to adoption among risk-averse growers. Field trials conducted by the University of California, Davis, United States, revealed efficacy variations of 30-70% for identical bacterial strains across different soil microbiomes within a single county. This inconsistency requires manufacturers to conduct extensive local testing before entering the market, which increases development costs and time-to-market. Growers who experience unreliable results often revert to synthetic alternatives, generating negative word-of-mouth that hinders market penetration in farming communities. Due to complex soil-microbe interactions, formulations that succeed in one region may fail in similar conditions elsewhere, necessitating region-specific product development. The absence of insurance coverage for crop losses related to biological input failures leaves growers fully exposed to the financial risks associated with adopting these inputs.

Cold-Chain Requirements for Live Formulations

Live microbial formulations require refrigerated storage and transportation, increasing distribution costs by 15-25% compared to synthetic alternatives that remain stable at room temperature. The insufficient cold-chain infrastructure in developing markets restricts market penetration, especially in sub-Saharan Africa and rural Asia, where temperature-controlled logistics are limited. Power disruptions and equipment malfunctions can damage entire shipments of live microbial products, creating supply chain risks that distributors transfer to manufacturers through strict contract terms. Rural retailers cannot support the investment in refrigeration equipment for low-volume microbial products, constraining last-mile distribution. The 2-8°C temperature requirement for many live formulations conflicts with conventional ambient storage in agricultural supply chains, necessitating significant changes to existing distribution networks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Bacteria Retain Leadership amid Viral Momentum

Bacteria held a 43.35% share of the agricultural microbial market in 2025, owing to their broad-spectrum efficacy and favorable regulatory status. Bacillus and Pseudomonas strains consistently deliver yields across various soils and are pre-approved for use in organic systems. Venture funding of USD 800 million flowed into bacterial innovation in 2024, including Pivot Bio, which alone raised USD 430 million to scale nitrogen-fixing inoculants. Virus-based solutions, although nascent, are projected to post an 17.95% CAGR by offering species-specific pest knockdown without harming pollinators.

Fungi anchor high-value crop niches, while protozoa and algae gain footholds in soil-health programs. Regulators grant bacteria an easier path, reinforcing their dominance. The Environmental Protection Agency (EPA) expedited track for naturally occurring strains speeds market entry, and CRISPR-enhanced variants move through the pipeline quickly.

By Function: Biopesticides Dominate but Biostimulants Surge

Biopesticides commanded 48.10% of the agricultural microbials market size in 2025. Bacillus thuringiensis insecticides established a majority share in global sales, underlining a mature value proposition against resistant caterpillars. Biofungicides post double-digit gains in grapes and tomatoes where synthetic options falter.

Biostimulants, expanding at a 15.05% CAGR, appeal to growers seeking yield lift without the regulations tied to pesticidal claims. Multi-strain consortia that enhance nutrient uptake gain share in high-value vegetables and controlled environment farms. Biofertilizers grow steadily at 13.95% CAGR in price-sensitive regions where spiking synthetic fertilizer costs increase the economic attractiveness of microbial alternatives.

By Application: Commercial Crops Accelerate, Fruits and Vegetables Sustain Premium Share

Fruits and vegetables accounted for 28.70% of 2025 sales, reflecting the premium residue-free requirements in export-oriented crops. Greenhouse operators appreciate the closed environment that maximizes microbial performance and worker safety. Row crops are expected to outpace the market at a 14.63% CAGR through 2031, driven by large-scale programs in Brazilian sugarcane and Indian cotton that seek biological solutions to persistent pest pressure.

Grains and cereals represent significant acreage but lighter revenue density, limiting their short-term contribution to the agricultural microbials market size. Pulses and oilseeds utilize nitrogen-fixing and phosphate-solubilizing inoculants to maintain protein content while reducing synthetic fertilizer expenditures.

By Mode of Application: Seed Treatment Retains Scale Advantage

Seed treatment captured 44.70% of the agricultural microbial market size in 2025, as it ensures direct delivery to the root zone at a per-acre cost of USD 5-15, which suits high-volume row crops. Foliar spray, powered by drones and variable-rate rigs, is expected to compound at a 15.72% CAGR as precision tools enable on-demand applications timed to pest life cycles.

Soil drenches remain essential in organic systems and perennial crops, where the long-term benefits to soil health justify the higher costs. Combined strategies that layer seed, soil, and foliar routes position growers to hit residue guarantees in premium markets while optimizing microbial survivability.

By Formulation: Liquid Products Still Rule but Dry Forms Gain

Liquid formulations accounted for 54.60% of 2025 revenues, rewarded for higher field efficacy and compatibility with common sprayers. Suppliers extend shelf life to 36 months through proprietary carriers, yet refrigeration demands restrict reach in emerging economies.

Dry forms, boosted by microencapsulation and freeze-drying, will grow 15.45% CAGR. Ambient-stable powders appeal to smallholders in tropical regions who lack cold storage and to distributors wary of spoilage. As efficacy gaps narrow, dry products may gain share in the agricultural microbials market where logistics hurdles remain.

Geography Analysis

North America held the largest share, accounting for 32.10% of the 2025 revenue base, and is anticipated to record moderate growth due to market maturity and stringent Environmental Protection Agency (EPA) protocols. However, Walmart’s zero-residue procurement policies and corporate Scope 3 commitments sustain volume demand in high-value produce and corn-soy rotations. Canada invests in microbial solutions for canola and wheat, supported by cost-sharing grants.

The Asia-Pacific is projected to post a 16.83% CAGR through 2031, the fastest worldwide, propelled by China’s significant demand for microbial products from more than 200 enterprises. Subsidies further contributed to the demand, as they reduced farmer costs by up to 40%. Additionally, India’s USD 2.1 billion support plan and Japan’s 30% reduction goal for fertilizer use reinforce the momentum. South America is expected to expand at a 14.33% CAGR. Brazil’s biological market benefits from 8 million hectares of soybeans and corn under biological pest management. Argentina lags due to economic headwinds, but shows pockets of adoption in wheat-belt districts. Europe advances at a significant CAGR under the Farm to Fork mandate, targeting a 50% pesticide cut by 2030. Direct payments tied to eco-schemes accelerate microbial uptake in France, Spain, and Germany. The Middle East and Africa trail in prominent growth, constrained by gaps in storage infrastructure, although South Africa’s citrus sector demonstrates strong adoption of microbial solutions.

Competitive Landscape

The agricultural microbials market remains moderately concentrated, with the top five suppliers holding the majority of the share. Bayer AG leads the market share, followed by BASF SE and Syngenta Group, which maintain aggressive research and development spending, as well as acquisitions, to expand their strain libraries. Strategic consolidation accelerated in 2024 and 2025. ICL Group Ltd. expanded local manufacturing in Brazil through the purchase of Nitro 1000, and venture rounds worth USD 160 million funded platform companies using AI to fast-track product launches.

Competitive intensity now centers on computational biology and rapid fermentation scale-up. Companies are licensing machine-learning platforms that predict field performance across soil types with 85% accuracy, cutting registration timelines by up to 18 months. Venture investors deployed USD 3.1 billion into agricultural biotech in 2024, and 60% of that capital funded companies with AI-driven strain-development pipelines, signaling sustained financial backing for disruptive entrants. Established agrochemical firms respond by co-locating digital agronomy teams with biological research and development units to speed proof-of-concept trials and integrate data analytics into product stewardship programs.

White-space opportunities persist in biostimulants, rhizosphere consortia, and climate-linked service models. Emerging suppliers bundle microbial inputs with soil microbiome diagnostics and carbon-credit facilitation, creating differentiated packages that drive longer customer contracts. Market entry barriers now rest less on core biology and more on access to precision-application data, validated ESG metrics, and regional cold-chain infrastructure. Companies that pair shelf-stable formulations with digital deployment tools are positioned to capture outsized share as sustainability mandates tighten.

Agricultural Microbials Industry Leaders

Bayer AG

BASF SE

Syngenta Group

Corteva Inc.

Novonesis A/S

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Japan’s Ministry of Agriculture issued biostimulant labeling guidance, providing growers and suppliers with transparent rules that streamline product registration and encourage national pilot programs for 69 crops.

- January 2025: India amended its Fertilizers Control Order, tightening quality rules for microbial products and covering more than 400 registrations. The move sets higher potency thresholds and mandates clearer labeling to reinforce farmer trust.

- May 2024: Bayer partnered with AlphaBio Control to co-develop microbial insecticides for corn and soybean pests across the Americas, advancing its pathway toward USD 1.62 billion biological sales by 2035.

Global Agricultural Microbials Market Report Scope

Crop Nutrition, Crop Protection are covered as segments by Function. Cash Crops, Horticultural Crops, Row Crops are covered as segments by Crop Type. Africa, Asia-Pacific, Europe, Middle East, North America, South America are covered as segments by Region.By Type

| Bacteria |

| Fungi |

| Viruses |

| Protozoa |

| Others |

By Function

| Biofertilizers |

| Biopesticides |

| Biostimulants |

By Application

| Grains and Cereals |

| Pulses and Oilseeds |

| Commercial Crops |

| Fruits and Vegetables |

| Other Crop Types |

By Mode of Application

| Soil Treatment |

| Foliar Spray |

| Seed Treatment |

By Formulation

| Liquid |

| Dry |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Type | Bacteria | |

| Fungi | ||

| Viruses | ||

| Protozoa | ||

| Others | ||

| By Function | Biofertilizers | |

| Biopesticides | ||

| Biostimulants | ||

| By Application | Grains and Cereals | |

| Pulses and Oilseeds | ||

| Commercial Crops | ||

| Fruits and Vegetables | ||

| Other Crop Types | ||

| By Mode of Application | Soil Treatment | |

| Foliar Spray | ||

| Seed Treatment | ||

| By Formulation | Liquid | |

| Dry | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Market Definition

- AVERAGE DOSAGE RATE - The average application rate is the average volume of agricultural biologicals applied per hectare of farmland in the respective region/country.

- CROP TYPE - Crop type includes Row crops (Cereals, Pulses, Oilseeds), Horticultural Crops (Fruits and vegetables) and Cash Crops (Plantation Crops, Fibre Crops and Other Industrial Crops)

- FUNCTION - Agricultural biological products provide crops with essential nutrients, prevent or control abiotic & biotic stresses, and enhance soil quality.

- TYPE - The Crop Nutrition function of agricultural biologicals includes organic fertilizer and Biofertilizer, whereas the Crop Protection function includes Biostimulants, Biopesticides and Biocontrol Agents.

| Keyword | Definition |

|---|---|

| Cash Crops | Cash crops are non-consumable crops sold as a whole or part of the crop to manufacture end-products to make a profit. |

| Integrated Pest Management (IPM) | IPM is an environment-friendly and sustainable approach to control pests in various crops. It involves a combination of methods, including biological controls, cultural practices, and selective use of pesticides. |

| Bacterial biocontrol agents | Bacteria used to control pests and diseases in crops. They work by producing toxins harmful to the target pests or competing with them for nutrients and space in the growing environment. Some examples of commonly used bacterial biocontrol agents include Bacillus thuringiensis (Bt), Pseudomonas fluorescens, and Streptomyces spp. |

| Plant Protection Product (PPP) | A plant protection product is a formulation applied to crops to protect from pests, such as weeds, diseases, or insects. They contain one or more active substances with other co-formulants such as solvents, carriers, inert material, wetting agents or adjuvants formulated to give optimum product efficacy. |

| Pathogen | A pathogen is an organism causing disease to its host, with the severity of the disease symptoms. |

| Parasitoids | Parasitoids are insects that lay their eggs on or within the host insect, with their larvae feeding on the host insect. In agriculture, parasitoids can be used as a form of biological pest control, as they help to control pest damage to crops and decrease the need for chemical pesticides. |

| Entomopathogenic Nematodes (EPN) | Entomopathogenic nematodes are parasitic roundworms that infect and kill pests by releasing bacteria from their gut. Entomopathogenic nematodes are a form of biocontrol agents used in agriculture. |

| Vesicular-arbuscular mycorrhiza (VAM) | VAM fungi are mycorrhizal species of fungus. They live in the roots of different higher-order plants. They develop a symbiotic relationship with the plants in the roots of these plants. |

| Fungal biocontrol agents | Fungal biocontrol agents are the beneficial fungi that control plant pests and diseases. They are an alternative to chemical pesticides. They infect and kill the pests or compete with pathogenic fungi for nutrients and space. |

| Biofertilizers | Biofertilizers contain beneficial microorganisms that enhance soil fertility and promote plant growth. |

| Biopesticides | Biopesticides are natural/bio-based compounds used to manage agricultural pests using specific biological effects. |

| Predators | Predators in agriculture are the organisms that feed on pests and help control pest damage to the crops. Some common predator species used in agriculture include ladybugs, lacewings, and predatory mites. |

| Biocontrol agents | Biocontrol agents are living organisms used to control pests and diseases in agriculture. They are alternatives to chemical pesticides and are known for their lesser impact on the environment and human health. |

| Organic Fertilizers | Organic fertilizer is composed of animal or vegetable matter used alone or in combination with one or more non-synthetically derived elements or compounds used for soil fertility and plant growth. |

| Protein hydrolysates (PHs) | Protein hydrolysate-based biostimulants contain free amino acids, oligopeptides, and polypeptides produced by enzymatic or chemical hydrolysis of proteins, primarily from vegetal or animal sources. |

| Biostimulants/Plant Growth Regulators (PGR) | Biostimulants/Plant Growth Regulators (PGR) are substances derived from natural resources to enhance plant growth and health by stimulating plant processes (metabolism). |

| Soil Amendments | Soil Amendments are substances applied to soil that improve soil health, such as soil fertility and soil structure. |

| Seaweed Extract | Seaweed extracts are rich in micro and macronutrients, proteins, polysaccharides, polyphenols, phytohormones, and osmolytes. These substances boost seed germination and crop establishment, total plant growth and productivity. |

| Compounds related to biocontrol and/or promoting growth (CRBPG) | Compounds related to biocontrol or promoting growth (CRBPG) are the ability of a bacteria to produce compounds for phytopathogen biocontrol and plant growth promotion. |

| Symbiotic Nitrogen-Fixing Bacteria | Symbiotic nitrogen-fixing bacteria such as Rhizobium obtain food and shelter from the host, and in return, they help by providing fixed nitrogen to the plants. |

| Nitrogen Fixation | Nitrogen fixation is a chemical process in soil which converts molecular nitrogen into ammonia or related nitrogenous compounds. |

| ARS (Agricultural Research Service) | ARS is the U.S. Department of Agriculture's chief scientific in-house research agency. It aims to find solutions to agricultural problems faced by the farmers in the country. |

| Phytosanitary Regulations | Phytosanitary regulations imposed by the respective government bodies check or prohibit the importation and marketing of certain insects, plant species, or products of these plants to prevent the introduction or spread of new plant pests or pathogens. |

| Ectomycorrhizae (ECM) | Ectomycorrhiza (ECM) is a symbiotic interaction of fungi with the feeder roots of higher plants in which both the plant and the fungi benefit through the association for survival. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms.