Market Overview

| Study Period | 2019 - 2030 |

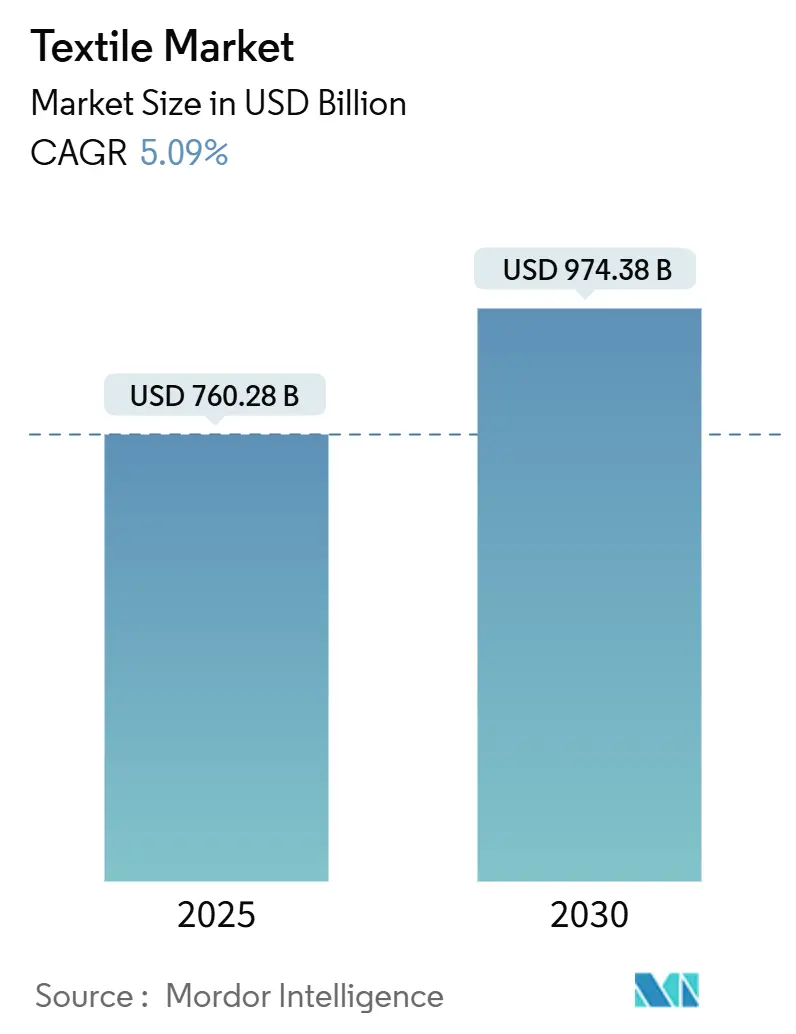

| Market Size (2025) | USD 760.28 Billion |

| Market Size (2030) | USD 974.38 Billion |

| Growth Rate (2025 - 2030) | 5.09% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Textile Market Analysis by Mordor Intelligence

The Textile Market is valued at USD 760.28 billion in 2025 and is projected to reach USD 974.38 billion by 2030, advancing at a 5.09% CAGR. Tightening sustainability regulations in Europe, near-shoring strategies such as “China + 1,” and expanding demand for high-performance technical fabrics set the growth tone for the global textile market. Polyester recycling lines, the rapid rise of e-commerce brands that want custom designs, and government incentive programs in India and Vietnam all reinforce investment momentum. Feedstock cost swings and climate-driven water restrictions on cotton create volatility, yet they also hasten the pivot toward recycled synthetics and new fiber blends. Overall, competitive advantage now hinges on traceability, low-impact production, and the ability to deliver small runs quickly for fast-fashion and direct-to-consumer labels[1]European Commission, “Ecodesign for Sustainable Products Regulation Working Plan 2025-2030,” European Commission, ec.europa.eu.

Key Report Takeaways

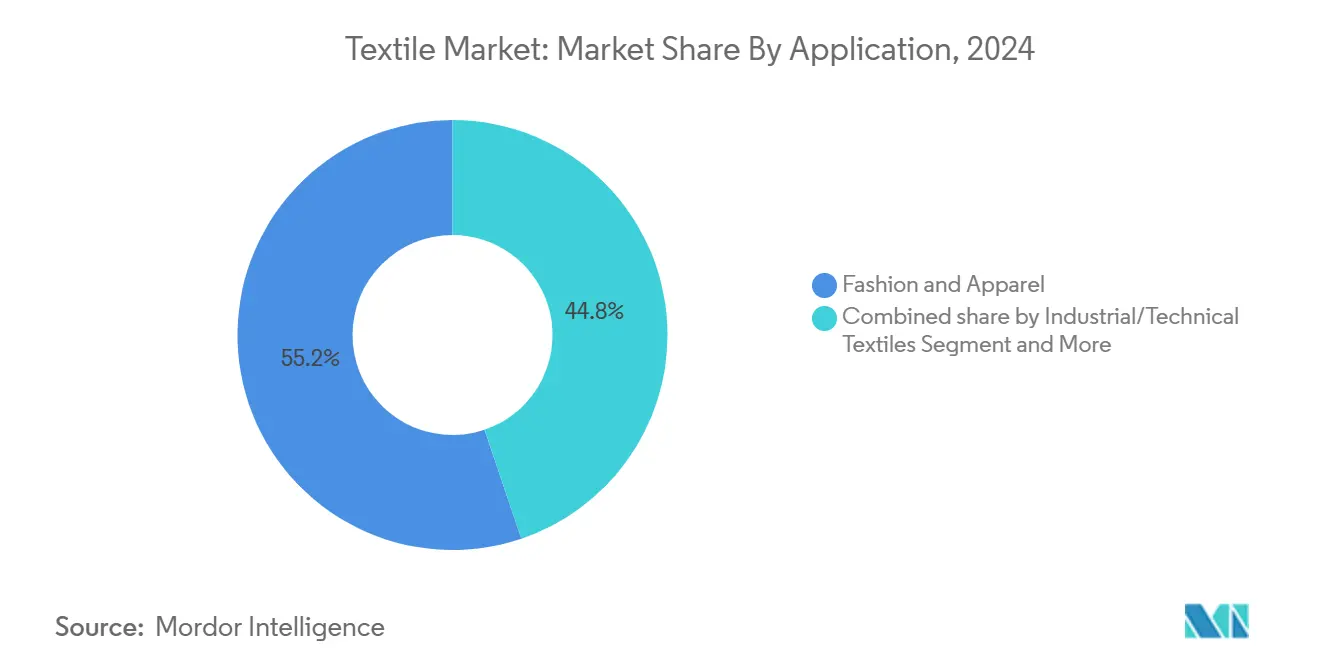

- By application, fashion and apparel held 55.2% of the textile market share in 2024, while industrial and technical textiles are forecast to expand at a 5.91% CAGR through 2030.

- By raw material, synthetic fibers dominated with 53.1% revenue share in 2024; polyester is the fastest-growing fiber at a 6.32% CAGR to 2030.

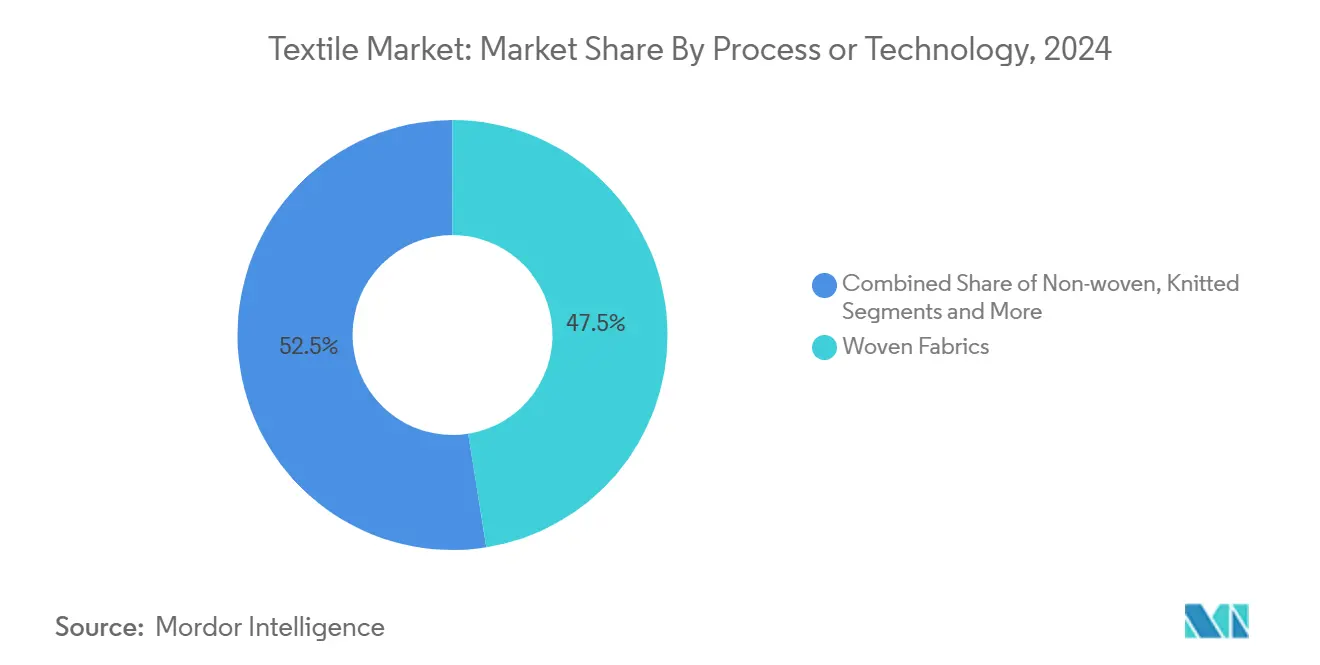

- By process, woven textiles led with a 47.5% share in 2024, yet non-wovens are projected to grow at a 5.81% CAGR.

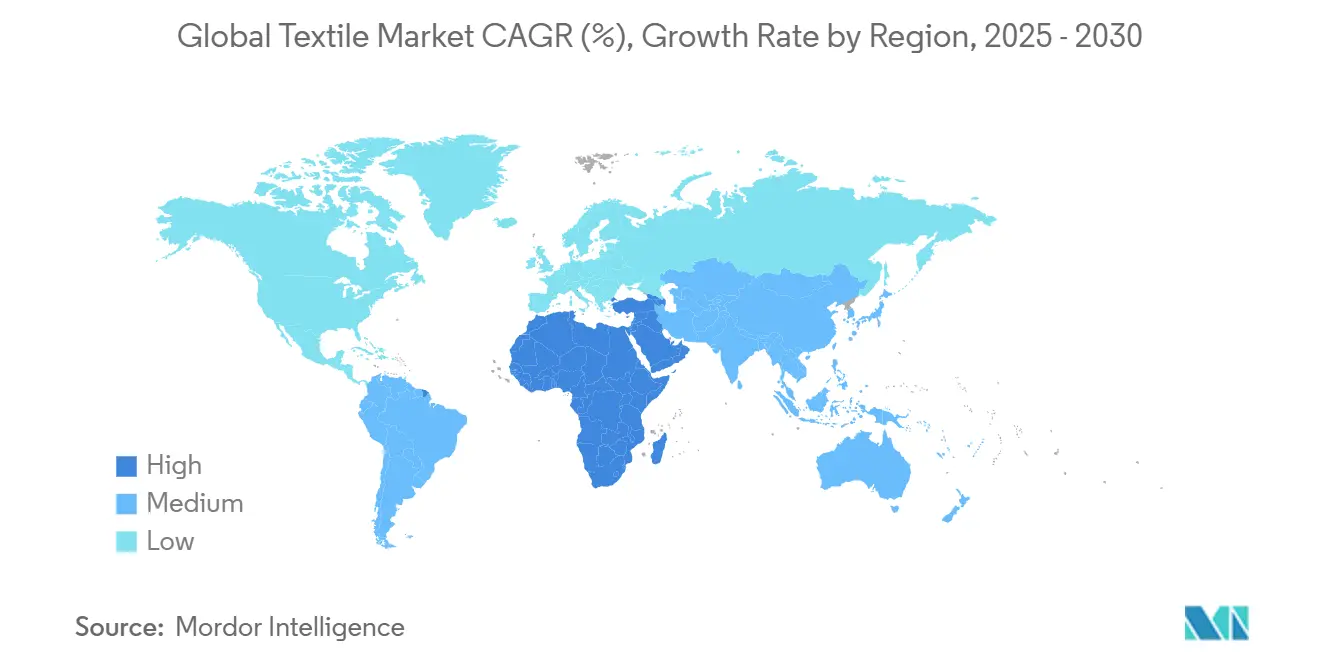

- By geography, Asia-Pacific controlled 53.2% of the textile market share in 2024, whereas the Middle East and Africa region is set to post the quickest growth at a 5.56% CAGR to 2030.

Global Textile Market Trends and Insights

Drivers Impact Analysis

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sustainable and circular textiles under the EU Green Deal | +0.8% | Europe with global spillover | Medium term (2-4 years) |

| Indian PLI and MITRA incentives | +0.7% | India with export reach | Medium term (2-4 years) |

| “China + 1” diversification lifting South Asian mill orders | +0.6% | South Asia, Turkey, Morocco | Medium term (2-4 years) |

| Automotive lightweighting mandates | +0.5% | Global, led by Europe, North America, China | Long term (≥ 4 years) |

| Ultra-short lead-time demand from Turkey and Morocco hubs | +0.4% | Europe, North America | Short term (≤ 2 years) |

| D-to-C e-commerce brands scaling customisation | +0.3% | Developed markets | Medium term (2-4 years) |

Source: Mordor Intelligence

Accelerating Shift to Sustainable & Circular Textiles Driven by the EU Green Deal

Extended Producer Responsibility came into force across the EU on January 1, 2025, prohibiting the household disposal of textiles and requiring separate collection streams. Digital product passports that disclose carbon footprints and recycling routes will accompany every garment by 2027. Brands, therefore, redesign for durability, invest in traceability, and secure recycled feedstocks to avoid punitive eco-modulation fees. Early adopters already win shelf space and can charge premium prices in eco-conscious retail chains. Compliance costs discourage laggards, yet they open expansion opportunities for suppliers that master low-impact chemistry and closed-loop supply chains.

Near-shoring & “China + 1” Supply-Chain Realignment Boosting South-Asian Mill Orders

Vietnam, Pakistan, Indonesia, Bangladesh, and Turkey are projected to absorb 47% of world cotton imports by 2030, while China’s share falls to 24%. Turkish producers have stepped into Egypt after its currency devaluation reduced labor costs to about 30% of Turkey’s, and free-trade deals provide duty-free access to the US market. Morocco secured a USD 230 million Chinese investment that will create 7,000 direct textile jobs. Pan-Euro-Med rule changes let European brands source yarn in one nation, cut-and-sew in another, and still ship duty-free, an option that trims lead times against Asian sourcing. Capacity constraints in new hubs remain a hurdle, yet quick-response orders continue to shift west of the Suez Canal.

Fast-Fashion Refresh Rates Fueling Ultra-Short Lead-Time Demand from Turkey & Morocco Hubs

Fashion labels now drop collections in under two weeks instead of the former six-month cycle. Turkey ranks seventh in global clothing exports and can truck finished goods into the EU within 72 hours. Morocco’s free-trade status with both the EU and the US means sweaters sewn near Tangier hit Paris stores within ten days. Egypt’s Qualified Industrial Zones enable US duty-free entry for garments that blend Israeli input, integrating with Turkish know-how to cut cycle times further. McKinsey cites 12% landed-cost savings for jeans made in Mexico or Turkey versus China, while shrinking lead times to two weeks. Specialized trims still come from Asia, which adds complexity but does not offset the speed edge.

E-Commerce Native D-to-C Labels Scaling Customisation, Raising Technical Fabric Uptake

Direct-to-consumer brands deploy generative AI tools to recommend styles and allow shoppers to tweak fit in real time. Global online apparel sales could top USD 1.39 trillion by 2033, growing at 8.7% CAGR. Rental fashion in China is expected to hit USD 1.08 billion by 2026, driving the need for abrasion-resistant fabrics that endure many laundering cycles. WRAP reports repair services displace 82.2% of new garment purchases, pushing mills to boost fiber strength and colorfastness. The intersection of mass customisation and sustainability enlarges profit pools for premium technical textiles with verified low environmental impacts.

Restraints Impact Analysis

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Apparel rental and re-commerce platforms | -0.30% | OECD economies | Medium term (2-4 years) |

| Water-scarcity regulations on conventional cotton in MENA | -0.40% | Middle East and North Africa | Long term (≥ 4 years) |

Source: Mordor Intelligence

Rise of Apparel Rental & Re-Commerce Platforms Slowing Virgin Textile Volumes in OECD

Preloved purchases offset 64.6% of new garment demand, and repair services replace 82.2% of foregone sales, according to WRAP. EU strategy bans destruction of unsold stock, which historically ran near 21% of output. Second-hand trade hit USD 9.3 billion in 2021 and continues to climb as platforms curate higher-quality assortments. Rental fashion widens consumer reach in China and Western Europe, further cutting virgin yarn orders. Brands that overproduce face markdowns and higher waste-handling fees, accelerating the adoption of on-demand manufacturing[2]United Nations Economic Commission for Europe, “Global Trade in Second-Hand Clothing,” UNECE, unece.org.

Growing Water-Scarcity Regulations Curbing Conventional Cotton Cultivation in MENA

Agriculture accounts for 70% of total water withdrawals across the Middle East and North Africa, a region that sees freshwater availability fall every year. Regulators are limiting cotton acreage and demanding deficit-irrigation practices. Satellite data show high-yield plots can still achieve stable output with 30% less water when growers switch to precision drip systems. Mills therefore hedge supply risk through polyester recycling contracts and viscose blends. Lower cotton volumes combine with volatile spot prices to challenge margin planning for spinning operations reliant on imported fiber.

Segment Analysis

By Application: Technical Textiles Expand Beyond Fashion Leadership

Fashion and apparel claimed 55.2% of the textile market share in 2024, yet industrial and technical textiles are projected to record the fastest 5.91% CAGR to 2030. Automotive lightweighting rules elevate demand for seatbelt webbings, airbag fabrics, and natural fiber composites that help manufacturers trim vehicle mass. Medical and hygiene categories hold steady as aging populations and procedural backlogs raise consumption of disposable gowns and wound-care wraps. The technical textiles surge highlights a structural pivot where performance and compliance trump seasonal aesthetics in shaping mill orders.

Technical textiles also lift margins because buyers value strength, fire resistance, and chemical durability. Electric vehicle battery insulation relies on aramid and glass fabrics that command double-digit premiums over commodity cloth. Sportswear brands blend high-tenacity polyamide yarns to improve abrasion life for rental models. Infrastructure spending on geotextiles supports drainage projects across Southeast Asia, locking in multi-year contracts. As technical specifications grow stringent, integrated producers with in-house testing labs secure preferred-supplier status with aerospace and defense clients.

Note: Segment shares of all individual segments available upon report purchase

By Raw Material: Synthetic Leadership Faces Circular Pressures

Synthetic fibers held a 53.1% revenue share in 2024, and recycled polyester is on track to be the fastest-growing fiber at 6.32% CAGR through 2030. Selenis and Syre have built textile-to-textile recycling plants capable of producing 10,000 metric tons of circular polyester yearly while cutting CO2 emissions by 85% versus virgin production. Natural fibers face constraints from water regulations in cotton-growing regions, especially across the Middle East and North Africa, where agricultural water use accounts for 70% of total withdrawals. Wool and silk maintain stable but small shares in luxury segments where synthetic alternatives cannot match hand feel or drape.

Cotton cultivation adapts through high-density planting and precision irrigation that maintains yields with 30% less water. UNIFI launched globally available recycled polyester yarns made from textile waste in August 2024. Specialty fibers like aramid, carbon, and ultra-high molecular weight polyethylene serve technical applications where extreme performance justifies premium pricing. The textile market size for recycled content grows fastest in Europe, where Extended Producer Responsibility fees penalize virgin materials, yet Asian mills also invest in chemical recycling to prepare for export market compliance.

By Process/Technology: Non-woven Growth Challenges Traditional Weaving

Woven fabrics maintained 47.5% textile market share in 2024, while non-woven segments are projected to grow at 5.81% CAGR through 2030. The Techtextil trade fair drew 38,000 visitors from over 100 countries, highlighting innovations in spunlaid and wet-laid processes that enable cost-efficient technical applications. Knitted fabrics serve markets requiring stretch and comfort, while 3D weaving addresses complex shapes for automotive and aerospace components. The process technology evolution reflects a broader shift toward performance-driven applications where traditional aesthetics yield to functional requirements.

Spunlaid processes, including spunbond and melt-blown technologies, drive non-woven growth through filtration, medical, and hygiene products. Dry-laid hydroentangled and wet-laid processes serve specialized applications requiring specific fiber orientation and bonding characteristics. Needle-punched methods provide cost-effective solutions for industrial and geotextile applications. Automation and digitalization investments enhance production efficiency while reducing labor dependency, especially important as nearshoring brings capacity back to higher-wage regions. The textile market size for non-wovens expands fastest in medical applications, where single-use items require consistent quality and sterility assurance.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Asia-Pacific dominated the textile market with 53.2% share in 2024, while the Middle East and Africa are set to grow fastest at 5.56% CAGR through 2030. China faces rising labor costs and geopolitical tensions that drive supply chain diversification toward Vietnam, Pakistan, Indonesia, Bangladesh, and Turkey. These five nations are projected to absorb 47% of global cotton imports by 2030, while China's share falls to 24%. India raised its Production Linked Incentive budget from INR 45 crore (USD 5.4 million) to INR 1,148 crore (USD 138.3 million) for 2025-26 to support seven new mega-parks that target USD 350 billion in industry size by 2030. Japan and South Korea focus on high-value technical textiles and advanced materials, while ASEAN countries benefit from "China + 1" strategies as manufacturers seek supply chain resilience[3]International Cotton Advisory Committee, “Cotton: World Statistics Update 2025,” ICAC, icac.org.

Europe shapes global textile practices through sustainability regulations, with Extended Producer Responsibility schemes and Digital Product Passports that influence manufacturing worldwide. Germany strengthens ties with Morocco in automotive supply chains, while Turkey's strategic position enables rapid order fulfillment for European brands requiring ultra-short lead times. The UK's post-Brexit trade agreements may limit access to pan-Euro-Med preferential treatment, potentially disadvantaging British textile firms compared to EU competitors. Nordic countries emphasize sustainable innovation and circular economy principles, creating premium market segments for environmentally certified products that command higher margins despite smaller volumes.

North America pursues nearshoring and technical textile applications, with Mexico emerging as a strategic manufacturing hub offering 12% cost advantages versus China for certain products while providing shorter lead times for US brands. The US textile industry faced challenges in 2024 but shows optimism for 2025 driven by administration changes and consumer preferences for domestically manufactured products. Canada benefits from USMCA trade agreements while maintaining focus on technical and specialty textiles. South America, led by Brazil and Argentina, serves regional markets while exploring export opportunities, though infrastructure limitations constrain global competitiveness compared to Asian manufacturing hubs that benefit from integrated supply chains and established logistics networks.

Note: Segment shares of all individual segments available upon report purchase

Competitive Landscape

The Global Textile Market shows moderate fragmentation with established players leveraging vertical integration and technological innovation to maintain competitive advantages amid sustainability pressures and supply chain diversification. Technical textiles demonstrate higher consolidation due to specialized knowledge requirements, while fashion and apparel segments remain fragmented across numerous regional and global players. Strategic patterns emphasize sustainability investments, circular economy integration, and geographic diversification to mitigate regulatory compliance costs and supply chain risks that threaten margins across all segments.

Technology adoption accelerates as companies integrate IoT, AI, and blockchain solutions to enhance supply chain transparency and operational efficiency. Lectra generated USD 520 million in 2023 revenues through Industry 4.0 solutions, including acquisitions of TextileGenesis and Launchmetrics for enhanced traceability capabilities. White-space opportunities emerge in textile-to-textile recycling, technical textiles for automotive applications, and digital product passport implementation. Emerging disruptors focus on circular business models and direct-to-consumer customization platforms that bypass traditional wholesale channels. Competitive dynamics intensify as regulatory compliance becomes a differentiating factor, with early adopters of EU sustainability standards gaining market access advantages.

Mergers and acquisitions reshape the landscape as companies seek scale and technical capabilities. Lone Star Funds announced an agreement to acquire RadiciGroup's Specialty Chemicals and High Performance Polymers Business Areas in February 2025. Freudenberg Performance Materials acquired the core business of Heytex to enhance its technology platform and market presence in technical textiles. Milliken & Company announced acquisition of Polartec from Versa Capital Management, expected to close June 2025, adding outdoor and fleece textiles capabilities to enhance its performance textile portfolio. These transactions highlight consolidation trends in specialized segments where technical expertise and intellectual property create defensible market positions.

Textile Industry Leaders

-

Toray Industries Inc.

-

Weiqiao Pioneering Group Co. Ltd.

-

Texhong Textile Group Ltd.

-

Inditex S.A.

-

Aditya Birla Fashion & Retail Ltd.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- March 2025: Chinese textile group Sunrise invested USD 230 million in Morocco to construct two industrial units in Skhirat and Fez, creating 7,000 direct jobs and 1,500 indirect jobs while establishing integrated supply chains for international orders.

- March 2025: Indian government scaled up PLI budget for textiles from INR 45 crore (USD 5.4 million) to INR 1,148 crore (USD 138.3 million) for 2025-26, targeting enhanced manufacturing capabilities and global competitiveness as part of self-reliance strategy.

- February 2025: Lone Star Funds announced agreement to acquire RadiciGroup's Specialty Chemicals and High Performance Polymers Business Areas, while the Radici family retains control of Advanced Textiles Solutions, with transaction expected to close in second half of 2025 .

- February 2025: Freudenberg Performance Materials acquired core business of Heytex to enhance technology platform and market presence in technical textiles, strengthening consolidation trends in specialized segments.

Global Textile Market Report Scope

The report aims to provide a detailed analysis of the global textile industry. It focuses on market dynamics, technological trends, and insights on the geographical segments and the process, material, and application types. Also, it analyses the major players and the competitive landscape in the global textile industry. The Textile Industry is Segmented by Application Type (Clothing, Industrial/Technical Applications, and Household Applications), By Material (Cotton, Jute, Silk, Synthetics, and Wool), by Process ( Woven and Non-woven), and by Geography (North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa). The report offers market size and forecasts for the textile industry in Value (USD billion) for all the above segments.

| By Application | Fashion & Apparel | ||

| Industrial/Technical Textiles | |||

| Household & Home Textiles | |||

| Medical & Healthcare Textiles | |||

| Automotive & Transport Textiles | |||

| Others (Protective, Sports Textiles, etc.) | |||

| By Raw Material | Natural Fibers | Cotton | |

| Wool | |||

| Silk | |||

| Synthetic Fibers | Polyester | ||

| Nylon | |||

| Rayon / Viscose | |||

| Acrylic | |||

| Polypropylene | |||

| Recycled Fibers | |||

| Others (Speciality High-Performance Fibers (Aramid, Carbon, UHMWPE)) | |||

| By Process / Technology | Woven | ||

| Knitted | |||

| Non-woven | Spunlaid (Spunbond / Melt-blown) | ||

| Dry-laid Hydro-entangled | |||

| Wet-Laid | |||

| Needle-punched | |||

| 3-D Weaving & Spacer Fabrics | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Peru | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| BENELUX (Belgium, Netherlands, and Luxembourg) | |||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| Australia | |||

| South Korea | |||

| ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam) | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Saudi Arabia | ||

| United Arab Emirates | |||

| Qatar | |||

| Kuwait | |||

| Turkey | |||

| Egypt | |||

| South Africa | |||

| Nigeria | |||

| Rest of Middle East and Africa | |||

By Application

| Fashion & Apparel |

| Industrial/Technical Textiles |

| Household & Home Textiles |

| Medical & Healthcare Textiles |

| Automotive & Transport Textiles |

| Others (Protective, Sports Textiles, etc.) |

By Raw Material

| Natural Fibers | Cotton |

| Wool | |

| Silk | |

| Synthetic Fibers | Polyester |

| Nylon | |

| Rayon / Viscose | |

| Acrylic | |

| Polypropylene | |

| Recycled Fibers | |

| Others (Speciality High-Performance Fibers (Aramid, Carbon, UHMWPE)) |

By Process / Technology

| Woven | |

| Knitted | |

| Non-woven | Spunlaid (Spunbond / Melt-blown) |

| Dry-laid Hydro-entangled | |

| Wet-Laid | |

| Needle-punched | |

| 3-D Weaving & Spacer Fabrics |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Peru | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam) | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Kuwait | |

| Turkey | |

| Egypt | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current size of the global textile market?

The global textile market is valued at USD 760.28 billion in 2025 and is projected to reach USD 974.38 billion by 2030, growing at a 5.09% CAGR.

Which region dominates the global textile market?

Asia-Pacific dominates with 53.2% market share in 2024, with China as the leading producer despite facing challenges from rising labor costs and supply chain diversification toward countries like Vietnam, Bangladesh, and India.

How is sustainability affecting the textile industry?

Sustainability regulations, particularly the EU's Extended Producer Responsibility schemes launched in January 2025, are forcing manufacturers to redesign products for durability and recyclability while investing in traceability systems, creating both compliance costs and premium pricing opportunities.

What are the fastest-growing segments in the textile market?

Industrial and technical textiles are growing fastest at 5.91% CAGR through 2030, driven by automotive lightweighting mandates and infrastructure modernization, while polyester leads fiber growth at 6.32% CAGR as manufacturers pivot toward recycled content.

How is the "China + 1" strategy reshaping textile manufacturing?

The "China + 1" strategy is diversifying supply chains toward Vietnam, Pakistan, Indonesia, Bangladesh, and Turkey, which are projected to account for 47% of global cotton imports by 2030 while China's share contracts to 24%, creating manufacturing opportunities in these emerging hubs.

What impact do circular business models have on textile demand?

Circular fashion models like rental platforms and second-hand marketplaces are slowing virgin textile demand, with preloved clothing purchases displacing 64.6% of new acquisitions and repair services reaching 82.2% displacement rates, pushing manufacturers toward more durable, recyclable materials.