Specialty Paper Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 34.39 Billion |

| Market Size (2031) | USD 42.38 Billion |

| Growth Rate (2026 - 2031) | 4.27% CAGR |

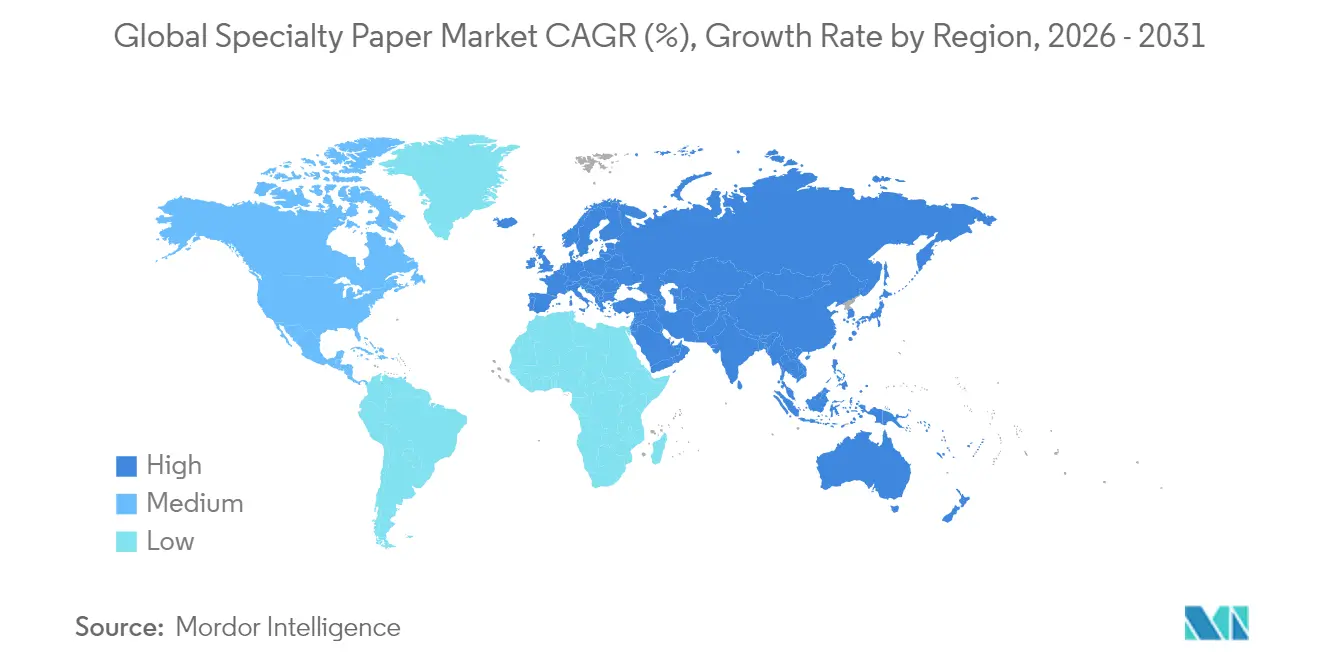

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

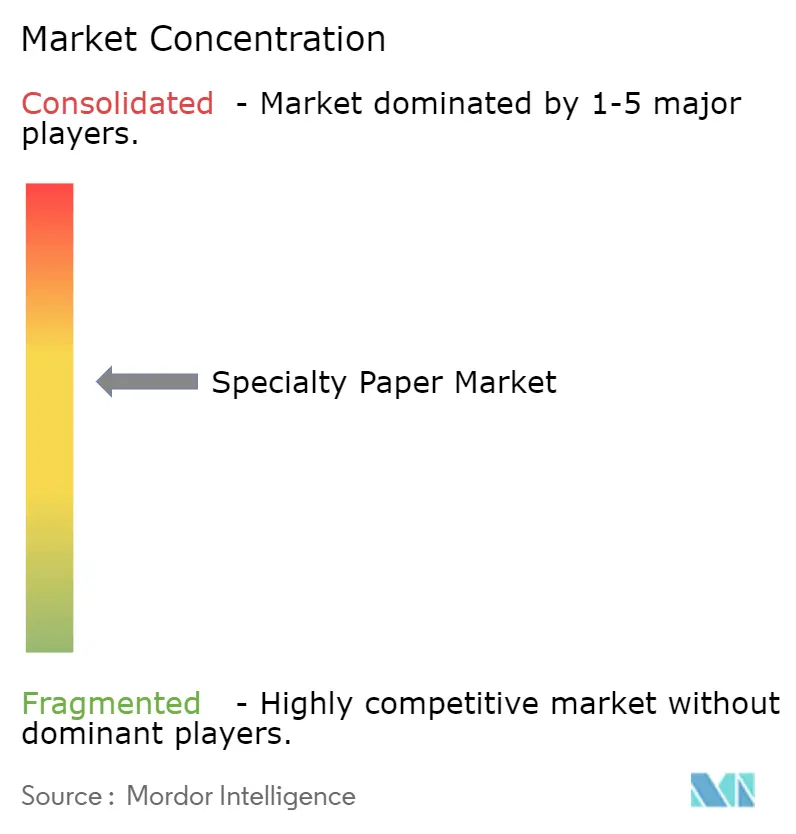

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Specialty Paper Market Analysis by Mordor Intelligence

The specialty paper market size was valued at USD 32.98 billion in 2025 and estimated to grow from USD 34.39 billion in 2026 to reach USD 42.38 billion by 2031, at a CAGR of 4.27% during the forecast period (2026-2031). This trajectory mirrors the global shift toward fiber-based packaging, heightened regulatory scrutiny of single-use plastics, and the rise of smart functionality requirements in labels and electronics. Consolidation among leading producers, exemplified by multibillion-dollar packaging mergers, is generating scale efficiencies while unlocking wider geographic reach. Europe presently leads demand, yet Asia-Pacific is expanding faster on the back of e-commerce penetration, capacity additions, and electronics manufacturing growth. Raw-material volatility and chemical-additive rules remain key risks, putting a premium on integrated pulp ownership and agile coating technologies.

Key Report Takeaways

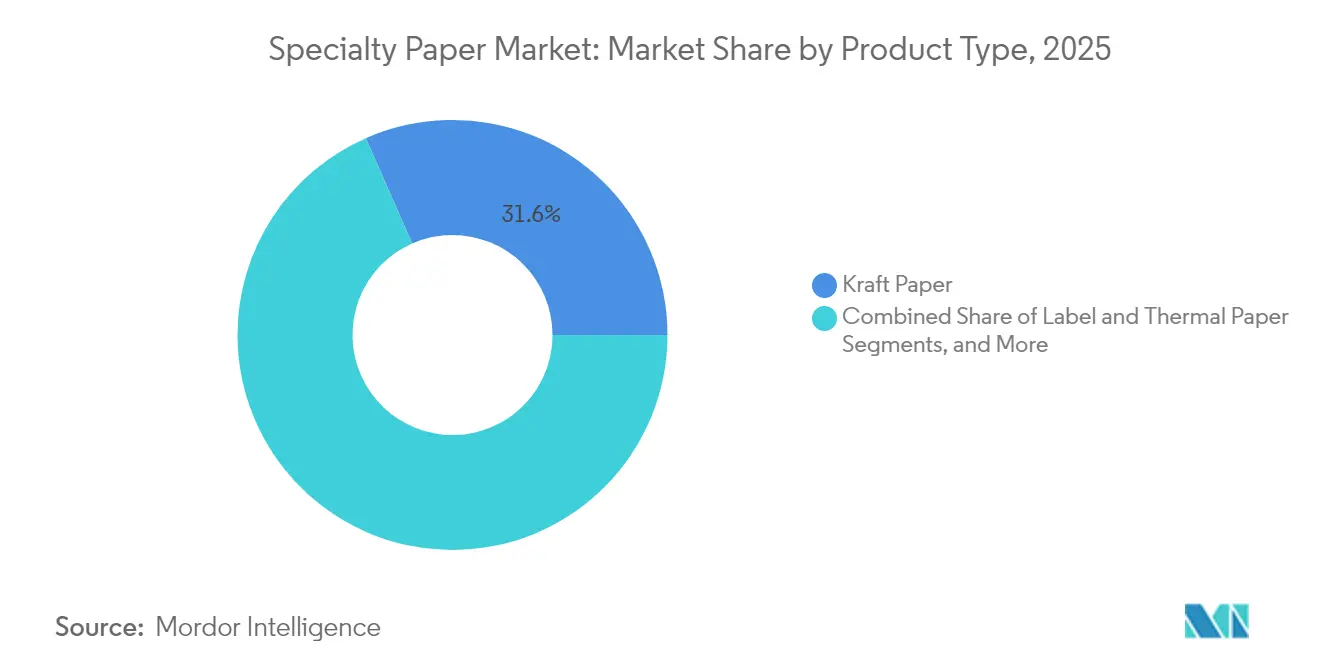

- By product type, kraft paper accounted for 31.60% of the Specialty Paper market share in 2025, while release-liner paper is set to grow at a 6.18% CAGR to 2031.

- By raw material, virgin fiber commanded 48.40% share of the Specialty Paper market size in 2025; recycled fiber is forecast to advance at 5.15% CAGR through 2031.

- By functionality, barrier and grease-proof grades held 58.10% revenue share in 2025, whereas anti-microbial papers are projected to expand at a 5.10% CAGR to 2031.

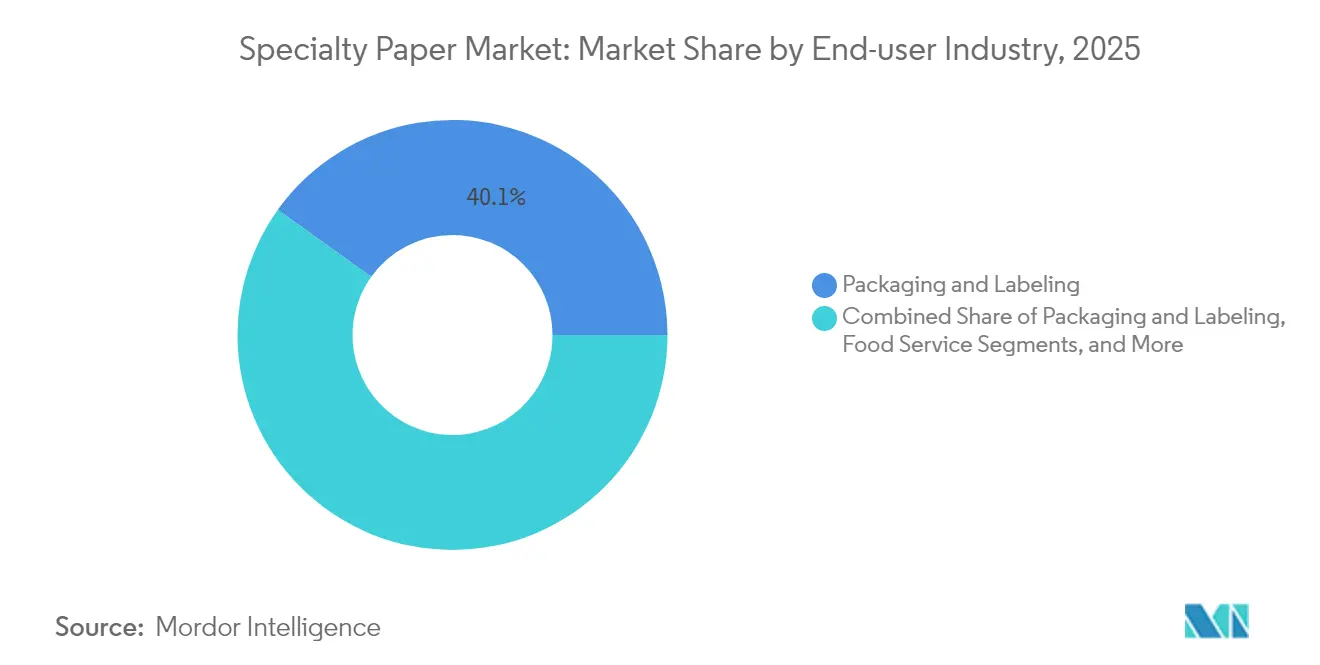

- By end-user industry, packaging and labeling led with a 40.10% share in 2025, while medical and healthcare is the fastest-growing segment at 5.45% CAGR.

- By form, sheets dominated with 52.70% share of the Specialty Paper market size in 2025; rolls are projected to post a 5.55% CAGR over the forecast period.

- By geography, Europe captured 32.70% of the Specialty Paper market share in 2025; Asia-Pacific is advancing at a 6.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Specialty Paper Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce push for sustainable packaging | +0.8% | North America and Europe | Medium term (2-4 years) |

| Food-service shift to fiber disposables | +0.6% | Developed market worldwide | Short term (≤ 2 years) |

| Smart-label release-liner demand | +0.4% | North America and Europe | Medium term (2-4 years) |

| Flexible printed-electronics substrates | +0.3% | Asia-Pacific primary | Long term (≥ 4 years) |

| Security papers for pharma | +0.2% | Global hubs | Medium term (2-4 years) |

| PFAS-free grease-proof coatings | +0.5% | North America and EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

E-commerce Push for Sustainable Packaging

Rapid online retail growth is accelerating the “paperization” of secondary and tertiary packaging as brands phase out plastics to meet Extended Producer Responsibility mandates[1] International Paper, “2025 Sustainability Report,” internationalpaper.com. Retailers now specify certified fiber, recyclable formats, and lower basis-weight kraft grades that reduce freight costs without compromising load integrity. Continuous order fulfillment drives demand for printable kraft mailers and molded-fiber cushioning, anchoring stable volume gains across shipping categories. Producers with integrated kraft assets capture margin upside because they can flex pulp streams toward high-growth e-commerce variants while mitigating raw-material shocks.

Food-Service Shift to Fiber-Based Disposables

Legislated single-use plastic bans in Europe, North America, and key Asian cities have triggered a swift migration to fiber utensils, cups, and clamshells. Advances in grease-proof barrier chemistries now enable paper containers to tolerate hot oils and sauces, allowing quick-service restaurants to meet compostability targets. Chain-level contracts prioritize post-consumer recycled content, supporting wider collection and re-pulping infrastructure. Volume visibility in food-service channels encourages multi-machine retrofits at mills specializing in cupstock and lightweight MG papers, boosting asset utilization.

Smart-Label Release-Liner Demand Surge

Connected-packaging programs in retail and logistics integrate RFID and NFC labels to automate inventory tracking and enhance shopper engagement. New plastic-free inlays, such as Trimco’s PaperMark platform, rely on FSC-certified release-liner paper that offers dimensional stability for precise die-cutting. Digital press penetration toward 10% of label volume by 2029 raises quality requirements for release substrates, driving specification upgrades that favor specialty grades over commodity glassine. As omnichannel fulfillment scales, liner recycling initiatives gain traction, extending circular-economy credentials for converters and brand owners alike.

Flexible Printed-Electronics Substrates

Printing advances now deposit conductive polymers and graphene onto coated paper, enabling cost-effective sensors, batteries, and antennas for wearables and packaging. Pilot trials in South Korea and Japan demonstrate roll-to-roll throughput compatibility with legacy flexographic lines, lowering adoption barriers. Performance parity with polymer films on bend radius and moisture resistance is within reach through multilayer coatings, opening a new addressable frontier for high-margin grades tailored to electronics supply chains.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Pulp-price volatility and supply shocks | -0.7% | Global, with acute impact in Europe and North America | Short term (≤ 2 years) |

| Chemical-additive regulatory tightening | -0.4% | Europe and North America primarily | Medium term (2-4 years) |

| High-clarity mono-material plastic films | -0.3% | Global, strongest in Asia-Pacific and North America | Medium term (2-4 years) |

| Slow ink-jet press adoption in EMs | -0.2% | Emerging markets, particularly Latin America & Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Pulp-Price Volatility and Supply Shocks

Benchmark Northern Bleached Softwood Kraft touched EUR 1,380 per metric ton in April 2024 after labor actions in Finland and mill incidents curtailed supply, squeezing specialty margins. Spot price spikes force non-integrated converters to adjust pricing quarterly, risking customer churn. Climate-related fiber disruptions and limited greenfield capacity suggest enduring volatility, reinforcing the strategic value of captive pulp or long-term chip contracts.

Chemical-Additive Regulatory Tightening

EU and US agencies are phasing out PFAS, mineral-oil inks, and select biocides, compelling mills to accelerate R&D pipelines for compliant barrier systems. Compliance validation and line-scale trials add cost and slow commercial rollouts, burdening smaller players that lack formulation capacity. The resulting squeeze may accelerate consolidation yet also elevate switching costs, fortifying incumbent relationships with brand owners that demand assured regulatory continuity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Kraft Paper Holds Scale While Release-Liner Gains Pace

Kraft grades generated the largest revenue contribution at 31.60% Specialty Paper market share in 2025, buoyed by industrial sacks, carrier bags, and burgeoning e-commerce mailers. The Karlsborg mill in Sweden alone produces 335,000 tons of sack kraft per year, underscoring the scale economics backing this position. Growth now tilts toward release-liner paper, which is forecast at a 6.18% CAGR through 2031 on the strength of RFID-enabled labels and rising digital press adoption. Smart labels require ultra-smooth calipers and calibrated density, steering converters toward engineered liner substrates and away from commodity options. Décor and laminating papers remain sizeable yet see share pressure from digital décor films, while filter and security papers preserve niche relevance through exacting performance criteria and embedded anti-counterfeit features.

Structural demand for high-purity fiber and tighter moisture control anchors long-term kraft capacity commitments even as liner innovations capture incremental value. Producers diversify grade slates to hedge against cyclical swings, but capital allocations now prioritize coating flexibility to address the liner opportunity. This bifurcation within the Specialty Paper Market fosters a portfolio mix where heritage kraft volumes finance next-wave liner technology upgrades.

By Raw Material: Recycled Fiber Momentum Builds Despite Virgin Dominance

Virgin fiber held 48.40% of the Specialty Paper market size in 2025 owing to tensile and porosity thresholds demanded by premium labels, security stock, and medical wraps. Yet recycled fiber is charting a 5.15% CAGR to 2031 as circular-economy mandates normalize recovered-content ratios and as brown recycled pulp grades reach specifications suitable for barrier-coated packaging. The Specialty Paper market size attached to synthetic and hybrid compositions remains modest, but these materials enable unique properties such as solvent resistance for automotive gaskets.

Non-wood pulps drawn from bamboo and agricultural residue are advancing through new enzymatic processes that mitigate silica contamination. Cost parity with hardwood chips remains elusive, constraining scale, yet brand-owner carbon disclosures are incentivizing trial volumes. Mills armed with dual-fiber systems can toggle furnish recipes to offset pulp pricing spikes, enhancing resilience during volatile cycles.

By Functionality/Coating: Barrier Grades Lead; Anti-Microbial Rises Fast

Barrier and grease-proof papers captured 58.10% Specialty Paper market share in 2025, reflecting pervasive uptake across quick-service packaging and frozen foods. PFAS withdrawal deadlines have catalyzed investment in algae-based and mineral-oil-free barriers certified for fatty and acidic contact. Anti-microbial papers, though smaller in volume, are expanding at a 5.10% CAGR as hospitals adopt germ-inhibiting wraps amid heightened infection-control protocols.

Conductive and antistatic coatings are garnering pilot orders from electronics assemblers, signaling a fusion of paper with functional chemistries once exclusive to polymers. Water-resistant and fire-retardant segments sustain moderate growth linked to outdoor signage and industrial gasketing. Suppliers differentiate through modular coating stations that accommodate quick chemistry swaps, enabling agile compliance with divergent regional safety codes.

By End-User Industry: Packaging Dominates; Medical Accelerates

Packaging and labeling applications retained 40.10% market share in 2025 as e-commerce, shelf-ready formats, and personalization lifted volumes in corrugated liner, folding carton, and label laminate. The medical and healthcare segment is projected to outpace at 5.45% CAGR, fueled by rising biologic drug launches that require high-barrier, tamper-evident paper-foil structures. Food-service outlets boost specialty demand through compostable cupstock and grease-proof wraps, while printing and publication volumes continue to migrate to digital media.

Building and construction demand persists in décor laminates and overlay papers for engineered wood, though economic slowdowns may temper near-term uptake. Industrial filtration media for transportation and energy maintain defensible niches, with emerging traction in hydrogen fuel-cell separator prototypes. This end-user diversification anchors the Specialty Paper Market against sector-specific shocks.

By Form: Sheets Prevail; Rolls Outpace Growth

Sheets constituted 52.70% revenue in 2025, integral to offset printing and specialty converter workflows that favor cut-size efficiency. Rolls, however, are on course for a 5.55% CAGR as high-speed label, masking-tape, and RFID inlay lines optimize continuous web throughput. Converters cite lower trim waste and faster job changeovers when sourcing master rolls, spurring mills to upgrade winding and reel diameters.

Converted products such as retail bags, tapes, and cups continue to capture downstream value, with machine manufacturers reporting steady order pipelines for nested-forming and pleating equipment. The shift to rolls mirrors the automation imperative within the Specialty Paper Market, pushing upstream producers to guarantee tight CD moisture profiles that safeguard web stability under elevated line speeds.

Geography Analysis

Europe remained the largest regional contributor at 32.70% Specialty Paper market share in 2025, underpinned by strict environmental statutes that accelerate conversion from plastics to fiber. Monthly paper and board output rebounded from the 2023 energy shock as mills optimized CHP configurations and locked in renewable electricity contracts. Germany and France lead eco-ink adoption and mineral-oil phase-outs, directing order flow toward low-migration label stock. Yet energy cost inflation has precipitated selective capacity closures, including UPM’s Ettringen site slated to cease operations in July 2025. Consolidation, such as Heinzel Group’s acquisition of Steyrermühl, signals a tightening asset base geared toward higher-margin grades.

Asia-Pacific is the fastest-growing territory at a 6.05% CAGR to 2031. China’s rebound in containerboard demand and Nine Dragons Paper’s Malaysian expansion illustrate a southward capacity realignment that taps proximate ASEAN markets, predicting 4% cardboard growth per year. Electronics supply chains in Japan and South Korea spur demand for conductive and antistatic papers, while India’s rising disposable-income levels lift specialty food-service grades. Regional governments channel stimulus into waste-paper collection infrastructure, broadening recycled-fiber availability that fuels local specialty conversions.

North America records steady mid-single-digit growth as nearshoring and packaging automation offset mature publishing segments. Investment programs such as Kimberly-Clark’s USD 2 billion expansion underscore confidence in long-run tissue and specialty capacity economics. Simultaneously, mega-mergers like Smurfit WestRock consolidate corrugated integration, enabling cost synergies and wider customer reach. The US South attracts greenfield pulp projects due to forest proximity and competitive energy tariffs, supporting integrated models better positioned to weather pulp price gyrations.

Competitive Landscape

Moderate concentration defines the Specialty Paper Market as top producers continue to merge, seeking scale and fiber security. International Paper’s USD 7.2 billion purchase of DS Smith and the Smurfit Kappa-WestRock tie-up worth USD 11.2 billion exemplify this wave of consolidation that pivots portfolios toward packaging growth and away from declining graphic papers. Vertical integration-from timberland to converting-protects margins via captive pulp and secures supply continuity for global brand owners.

Technology capability is emerging as a sharper differentiator than sheer tonnage. Avery Dennison’s Materials Group reports outperformance by focusing on premium pressure-sensitive and intelligent labels, showcasing how adhesive science and liner innovation create resiliency despite broader market pressures. Mills retrofit coaters for multi-chemistry flexibility, enabling quick shifts among grease-proof, anti-microbial, and conductive runs without extended downtime.

Smaller specialists defend share by targeting high-barrier niches such as security banknote stock or flame-retardant laminates where entry hurdles deter commoditization. However, escalating compliance costs and volatile inputs may prompt further consolidation or strategic alliances aimed at joint RandD and mill-level debottlenecking.

Specialty Paper Industry Leaders

Stora Enso Oyj

Mondi plc

Nippon Paper Industries Co., Ltd.

SAPPI Limited

International Paper Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: International Paper exited the molded-fiber packaging and closed two North American sites following DS Smith acquisition.

- May 2025: Valmet landed a major machine rebuild order from Sylvamo to modernize North American specialty capacity.

- May 2025: Smurfit WestRock posted USD 7,656 million Q1 2025 sales and announces 500,000-ton paper capacity closures while commissioning new converting plants.

- May 2025: Stora Enso acquired Junnikkala Oy sawmills for up to EUR 137 million to bolster wood supply at Oulu packaging board site.

Global Specialty Paper Market Report Scope

Specialty papers are superior-quality papers that are designed for specific purposes. They possess specific features and properties, along with proficiency in print technologies and design. The specialty paper market is segmented by application (packaging and labeling, food service, printing and publication, building and construction) and geography (North America [United States, Canada], Europe [Germany, United Kingdom, France, rest of Europe], Asia-Pacific [China, India, Japan, rest of Asia-Pacific], Latin America, Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Kraft Paper |

| Release-Liner Paper |

| Label and Thermal Paper |

| Décor and Laminating Paper |

| Filter and Security Paper |

| Others |

| Virgin Fiber |

| Recycled Fiber |

| Synthetic Fiber |

| Hybrid Composites |

| Barrier and Grease-Proof |

| Water-Resistant |

| Anti-microbial |

| Conductive and Antistatic |

| Fire-Retardant |

| Other functionality/Coating |

| Packaging and Labeling |

| Food Service |

| Printing and Publication |

| Building and Construction |

| Industrial and Automotive |

| Medical and Healthcare |

| Other End-user Industries |

| Rolls |

| Sheets |

| Converted Products (Bags, Tapes, Cups, and More) |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Nordics | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

| By Product Type | Kraft Paper | ||

| Release-Liner Paper | |||

| Label and Thermal Paper | |||

| Décor and Laminating Paper | |||

| Filter and Security Paper | |||

| Others | |||

| By Raw Material | Virgin Fiber | ||

| Recycled Fiber | |||

| Synthetic Fiber | |||

| Hybrid Composites | |||

| By Functionality/Coating | Barrier and Grease-Proof | ||

| Water-Resistant | |||

| Anti-microbial | |||

| Conductive and Antistatic | |||

| Fire-Retardant | |||

| Other functionality/Coating | |||

| By End-user Industry | Packaging and Labeling | ||

| Food Service | |||

| Printing and Publication | |||

| Building and Construction | |||

| Industrial and Automotive | |||

| Medical and Healthcare | |||

| Other End-user Industries | |||

| By Form | Rolls | ||

| Sheets | |||

| Converted Products (Bags, Tapes, Cups, and More) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Nordics | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| ASEAN | |||

| Australia | |||

| New Zealand | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the Specialty Paper Market?

The market stands at USD 34.39 billion in 2026 and is forecast to reach USD 42.38 billion by 2031.

Which region is growing the fastest?

Asia-Pacific records the highest growth, advancing at a 6.05% CAGR through 2031.

Which product type leads revenue?

Kraft paper remains the largest product segment, holding 31.60% of 2025 market share.

Why are PFAS-free coatings important?

Regulatory bans effective in 2025 compel food-service and packaging companies to adopt alternative grease-proof chemistries, boosting demand for new barrier papers.

Page last updated on: