Market Overview

| Study Period | 2021 - 2031 |

|---|---|

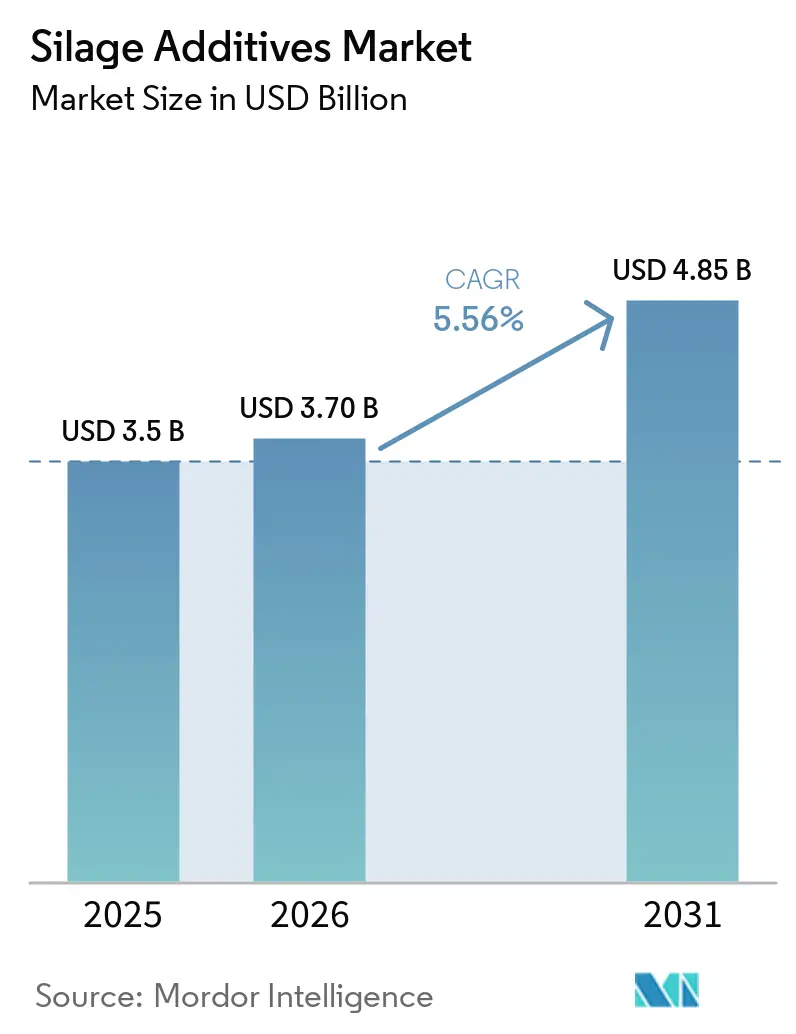

| Market Size (2026) | USD 3.70 Billion |

| Market Size (2031) | USD 4.85 Billion |

| Growth Rate (2026 - 2031) | 5.56% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Silage Additives Market Analysis by Mordor Intelligence

The silage additives market size was valued at USD 3.5 billion in 2025 and estimated to grow from USD 3.7 billion in 2026 to reach USD 4.85 billion by 2031, at a CAGR of 5.56% during the forecast period (2026-2031). The silage additives market is progressing as livestock producers increasingly view ensiled feed as a managed input that directly impacts feed efficiency, herd performance, and ration costs. According to projections by the Food and Agriculture Organization (FAO) and the Organization for Economic Cooperation and Development (OECD), global feed consumption is anticipated to increase by 15% by 2034, emphasizing the economic importance of forage preservation across livestock systems. This has driven demand for additives that minimize dry matter loss and enhance aerobic stability, offering operational advantages to livestock producers. Large dairies and feedlots are further reinforcing this demand by closely monitoring feed conversion rates, milk yields, and shrinkage, underscoring the critical role of consistent silage quality. Moreover, the European Union's 2024 ban on hexamine is accelerating product reformulation cycles, favoring suppliers with strong regulatory compliance and product development capabilities. These factors collectively underscore the growing importance of silage additives in enabling efficient, cost-effective livestock production.

Key Report Takeaways

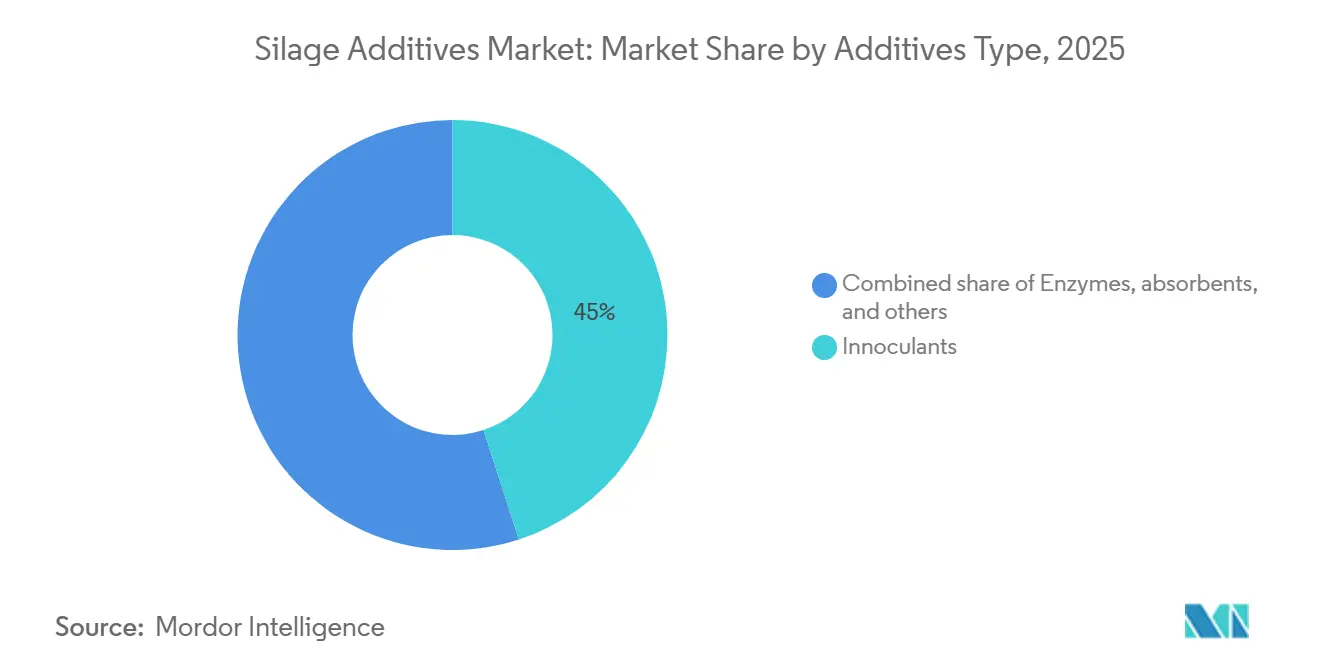

- By additive type, inoculants held 45.0% of the silage additives market share in 2025, while organic acids and salts recorded the fastest projected at 6.0% CAGR through 2031.

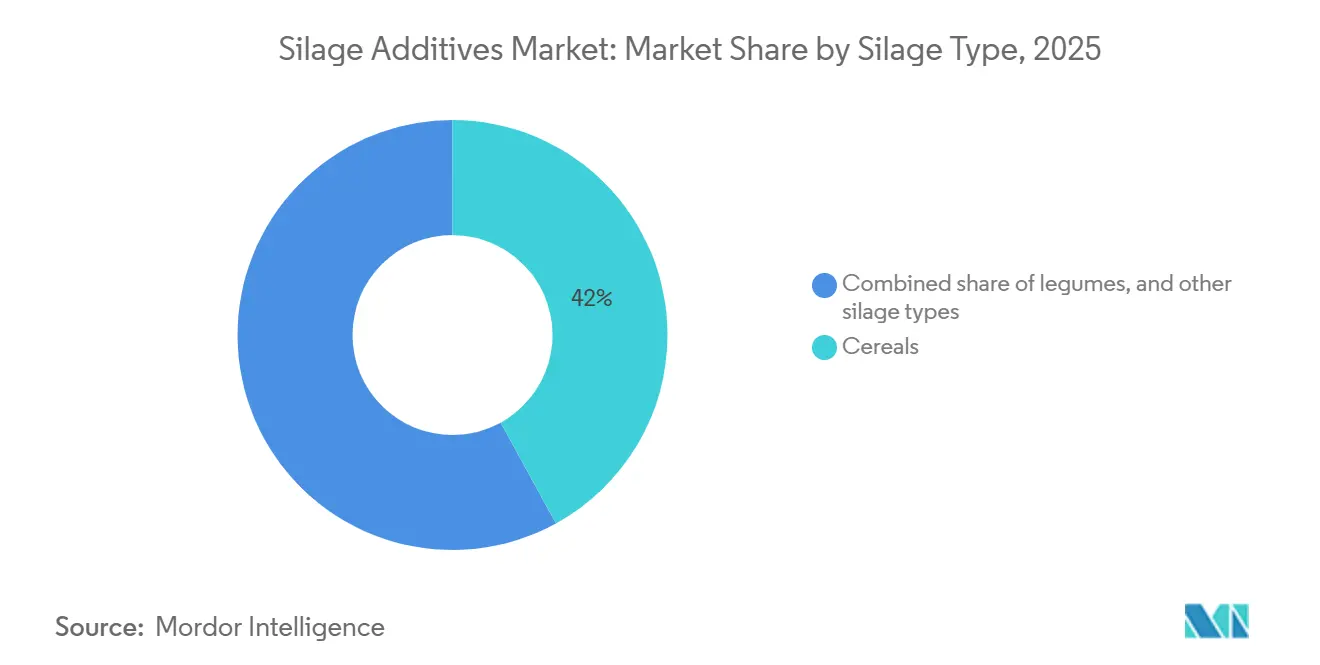

- By silage type, cereals led with 55% of the silage additives market size in 2025, while legumes remained the fastest-growing sub-segment with 6.10% CAGR through 2026-2031.

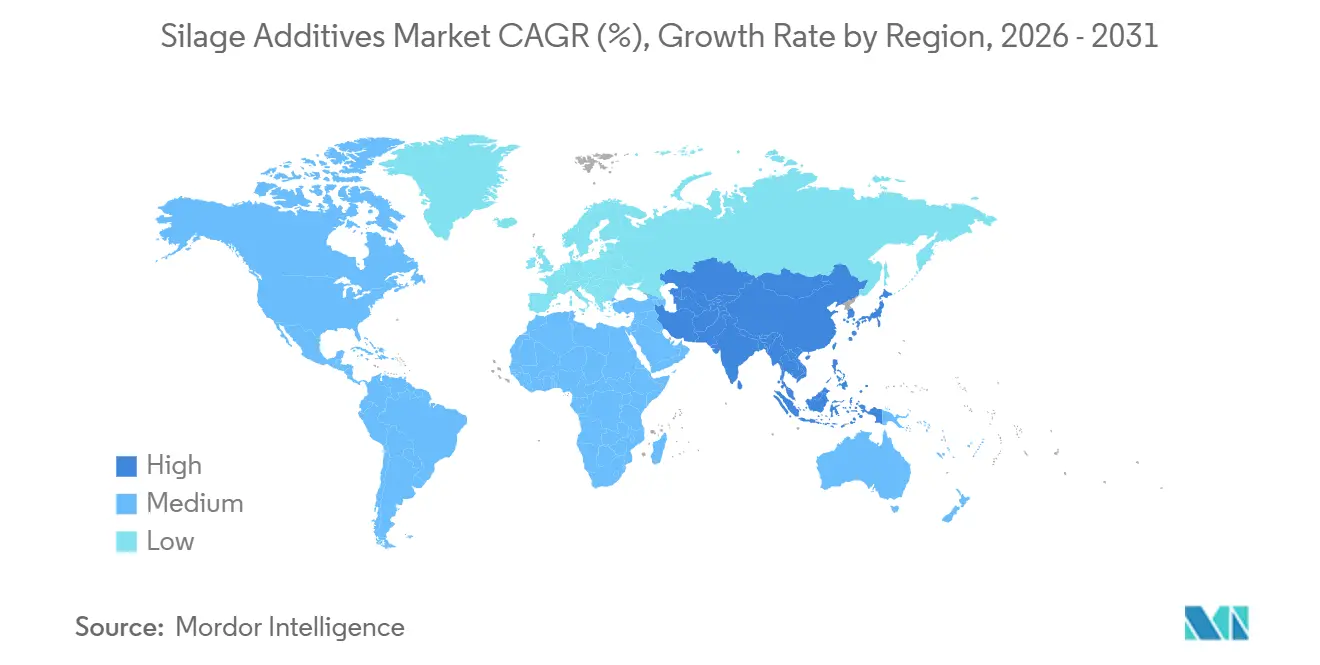

- By geography, North America accounted for 34.5% of the silage additives market size in 2025, while Asia-Pacific is advancing at the fastest 7.0% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Silage Additives Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying Dairy and Beef Productivity Targets | +1.2% | Global, with the highest intensity in North America, Europe, China, and Brazil | Medium term (2-4 years) |

| Scaling Industrial Livestock and Forage Systems | +0.9% | Global, strongest in China, the United States, Brazil, and India | Medium term (2-4 years) |

| Feed Shrink and Dry Matter Loss Reduction Focus | +0.8% | Global, particularly significant in North America, the United Kingdom, Brazil, and Argentina | Short term (≤ 2 years) |

| Shift Toward Biological Inoculants and Precision Fermentation | +0.7% | North America and Europe core, with spillover in the Asia-Pacific | Long term (≥ 4 years) |

| Mycotoxin Risk Control in High-Moisture Silage | +0.5% | Global, with elevated relevance in the United States, Italy, China, and Brazil | Medium term (2-4 years) |

| Faster Bunker Turnaround and Early Feedout Needs | +0.3% | North America, Germany, the United Kingdom, and Brazil | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Intensifying Dairy and Beef Productivity Targets

The increasing focus on maximizing milk and beef production per animal is driving the silage additives market, as these products are essential for improving ration efficiency and forage quality. The United States Department of Agriculture (USDA) projects that average milk production per cow will reach 11.07 metric tons by 2026, highlighting the need for high-quality silage to support such productivity[1]Source: United States Department of Agriculture, “Livestock, Dairy, and Poultry Outlook, September 2025,” Economic Research Service, ers.usda.gov. Supporting this, Lallemand reported in 2025 that its MAGNIVA Platinum grass silage inoculant improved neutral detergent fiber digestibility by 5.4 percentage points over 160 days, resulting in an additional 1.23 kg of daily milk yield per cow during the trials. These results emphasize the role of silage additives in enhancing livestock output, shifting purchasing decisions to focus on their contribution to milk and meat production rather than just treatment costs. In regions with limited forage acreage, this shift is even more critical, as operations must achieve higher productivity from the same land base. Consequently, the growing demand for silage additives reflects the increasing priority placed on efficiency and output in livestock management.

Scaling Industrial Livestock and Forage Systems

The silage additives market is also expanding as industrial livestock systems spread across China, India, and Brazil, increasing the use of standardized forage preservation inputs. In China, the Ministry of Agriculture and Rural Affairs' feed-saving plan released in 2025 promotes silage use to reduce grain dependence in feed rations[2]Source: Aihematijiang Rouzi, “Ministry Releases Feed-Saving Action Plan,” DCZ - Sino-German Agricultural Center, dcz-china.org. Xinhua reported in February 2026 that Tongliao in Inner Mongolia had 80.39 million hectares of silage corn in 2025, showing how quickly the forage base is being scaled for commercial livestock systems. The FAO and the OECD also project global livestock output to grow by 16.6% through 2034, with lower-middle-income countries driving proportionately stronger herd expansion. That trend broadens the customer base for entry-level inoculants, buffered acid blends, and region-specific preservation products in the silage additives market.

Feed Shrink and Dry Matter Loss Reduction Focus

Dry matter loss remains one of the clearest financial triggers for adoption in the silage additives market because it can be directly linked to replacement feed costs. Research published in Microorganisms in 2025 found that maize silage stored at 700 kg per cubic meter had dry matter losses of 3.37%, compared with 9.39% in low-density silos. The European Food Safety Authority reported in July 2024 that treated grass silage with Lactiplantibacillus plantarum DSM 34271 showed dry matter losses as low as 0.0% in official, standardized European Food Safety Authority (EFSA) registration efficacy trials conducted for the authorization of the feed additive, versus 4.0% and 1.7% in untreated controls[3]Source: European Food Safety Authority Panel on Additives and Products or Substances used in Animal Feed, “Safety and Efficacy of a Feed Additive Consisting of Lactiplantibacillus plantarum DSM 34271 as a Silage Additive for All Animal Species,” EFSA Journal, doi.org . In Germany, Landwirtschaftskammer Niedersachsen stated that medium fermentation quality losses can reach EUR 6,250 (USD 6,913) per season before additive costs are considered. As more farms use these loss calculations in ration planning, the silage additives market gains support from a straightforward economic case rather than from product promotion alone.

Shift Toward Biological Inoculants and Precision Fermentation

The silage additives market is shifting toward biological products with more targeted strain combinations and clearer forage-specific positioning. Lallemand’s MAGNIVA Platinum combines Lentilactobacillus hilgardii CNCM I-4785, Lactobacillus buchneri NCIMB 40788, and Pediococcus pentosaceus NCIMB 12455 to deliver both fermentation control and aerobic stability. Novonesis, formed in January 2024 through the merger of Chr. Hansen Holding A/S and Novozymes now markets its SiloSolve line through a broader biosolutions platform that uses deeper strain and fermentation knowledge. Biological formulations approved for organic use are also opening a premium channel that many conventional additive suppliers cannot access quickly. At the same time, the European Food Safety Authority's authorization process serves as a quality screen, giving science-backed inoculants a stronger competitive position in the silage additives market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw Material and Organic Acid Price Volatility | -0.8% | Global, most pronounced in Germany, the United States, India, and Brazil | Short term (≤ 2 years) |

| Regulatory Approval and Labeling Burden | -0.6% | Europe and Japan core, with growing relevance in North America and Asia-Pacific | Long term (≥ 4 years) |

| Live-Microbe Storage and Application Sensitivity | -0.5% | North America, Canada, Germany, and Australia are elevated in markets with variable cold-chain infrastructure | Medium term (2-4 years) |

| Performance Variability from Forage Heterogeneity | -0.4% | Global, most pronounced in the United States, France, India, and Brazil | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Raw Material and Organic Acid Price Volatility

Raw material price remain volatile in the silage additives market because organic acid products are exposed to volatile chemical feedstocks and energy costs. This pressure is strongest in the propionic acid and formic acid lines, where margins are thinner and customers are often more price-sensitive. Large commercial dairies can absorb these moves more easily through longer supply contracts, but smaller operators often cut application rates or shift to lower-specification products when prices rise. European feed additive rules also limit downward reformulation because product specifications and purity standards must still be maintained during cost spikes. That combination slows adoption in price-sensitive regions and puts mid-scale manufacturers under more pressure in the silage additives market.

Regulatory Approval and Labeling Burden

The silage additives market encounters significant challenges due to regulatory approval and labeling requirements, particularly for new microbial strains. The European Food Safety Authority (EFSA) mandates extensive evaluations, including multi-study efficacy assessments, antimicrobial resistance profiling, and comprehensive safety reviews, before granting authorization for many inoculant products. For instance, multiple EFSA opinions issued in 2025 for individual silage inoculant strains from Lactosan GmbH and BioCC OÜ demonstrate that each product line undergoes a separate, strain-specific review process. Additionally, the 2024 ban on hexamine in Europe necessitated reformulation and reauthorization efforts within a single commercial cycle, disrupting established preservative product lines. These stringent requirements tend to benefit larger suppliers with dedicated compliance resources, while limiting the ability of smaller specialists to scale operations within the silage additives market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Additive Type: Inoculants Remain Largest While Organic Acids and Salts Expand Fastest

Inoculants held the largest share, accounting for 45.0% of the silage additives market share in 2025. Their lead came from broad use across corn, grass, and legume silage, along with a clear return on investment in intensive dairy and beef systems. Organic acids and salts are the fastest-growing additive type, registering 6.0% CAGR through 2026-2031, with buffered and blended acid preservatives gaining traction as producers shift away from neat formic acid products. This growth is tied to demand for safer, less corrosive formulations and to the need for flexible preservation tools in regions where inoculant handling and cold-chain reliability are less consistent.

Within the remaining segments of the silage additives market, combination inoculants are gaining premium demand because they pair rapid pH reduction with stronger aerobic stability at feedout. Homofermentative inoculants continue to serve simpler ensiling conditions, while heterofermentative products are seeing greater use in high-dry-matter corn systems where heating risks are high. Enzymes, fermentation and spoilage control additives, and adsorbents are also expanding their role as farms place more emphasis on fiber digestibility, mold control, and mycotoxin management. Other additive types, including sugar-based and nutrient-based products, remain niche but relevant in wet forage and legume silage programs, especially in the Asia-Pacific and Africa.

By Silage Type: Corn Holds the Largest Position While Legumes Gain Speed

Cereals held the largest share, accounting for 42.0% of the silage additives market size in 2025. Their lead was supported by corn’s central role in high-energy dairy and beef rations and by its favorable carbohydrate profile, which supports reliable fermentation outcomes. Legumes are the fastest-growing silage type, registering a 6.10% CAGR through 2026-2031, driven by alfalfa area expansion in China and by tighter protein quality standards in commercial dairy nutrition. Demand has also been reinforced by trial results showing dry matter losses in ensiled alfalfa fell from 2.04% in untreated controls to 0.20% with additive use, which strengthens the case for premium inoculant programs.

Grass silage remains a major part of the silage additives market in the United Kingdom, Ireland, New Zealand, and Scandinavia, where producers rely on inoculants and organic acid blends to manage pH and feedout stability. Within cereals, sorghum is expanding in water-stressed regions, while oats and barley are gaining relevance in cooler temperate and high-altitude systems where early forage availability is important. Mixed forage silage is also becoming more important as multi-species swards spread, which is increasing demand for additives that can perform across variable botanical composition and dry matter levels. Other specialty silage, including cover crops, brassicas, and energy crops for biogas systems, remains a smaller segment but is creating targeted opportunities for niche formulations designed for wet and low-sugar feedstocks.

Geography Analysis

North America held 34.5% of the silage additives market share in 2025, making it the largest regional market. The United States maintains this lead because corn silage systems are highly mechanized, and large dairies closely monitor feed performance. The United States Department of Agriculture reported milk production at 222.6 billion pounds in 2025 in the United States and a milking herd of 9.06 million head, which keeps silage volumes and additive demand high. Regional growth is reflecting mature penetration but continued value expansion through multi-strain products. Canada and Mexico add incremental demand as intensive dairy and beef operations expand and suppliers widen access to premium formulations.

Asia-Pacific is projected to record the fastest 7.0% CAGR during 2026-2031 in the silage additives market, with China and India providing most of the new demand. China’s 2025 Feed-Saving Action Plan promotes the use of silage to reduce grain dependence, strengthening the case for preservation inputs across commercial livestock systems. South America is projected to grow, led by Brazil, while the Middle East and Africa are also seeing rising demand as commercial dairy operations expand in hot climates that increase the risk of aerobic spoilage.

Europe is set to grow at a descent CAGR during 2026-2031 in the silage additives market, with Germany, France, the United Kingdom, and the Netherlands leading the way. The region remains mature yet remains active because aerobic stability and certification standards shape buying decisions. Germany’s Deutsche Landwirtschafts-Gesellschaft testing framework acts as a quality filter, rewarding suppliers that can continue to demonstrate efficacy under defined silage protocols. The 2024 hexamine ban forced reformulation across part of the regional portfolio, and ADDCON completed the move to hexamine-free KOFASIL LP and KOFASIL Ultra by November 2024. Russia remains a sizable silage market, but import access and local production constraints slow the adoption of premium products.

Competitive Landscape

The silage additives market remains moderately concentrated, with the top 5 players, including Archer-Daniels-Midland Company, Lallemand Inc., BASF SE, Volac International Limited, and Novonesis A/S, forming the main global tier in the silage additives market. These companies compete more on strain quality, crop fit, and technical support than on price alone. In January 2024, Novonesis A/S was formed through the merger of Chr. Hansen Holding A/S and Novozymes, which combined 2 fermentation platforms under one biosolutions portfolio. That move raised the bar for research and scale for smaller suppliers that operate with narrower strain libraries.

Strategic expansion in the silage additives market is also coming through portfolio deals and targeted launches. In March 2024, EW Nutrition acquired the BIOSTABIL product line from dsm-firmenich, which gave it an established position in silage preservation. In March 2026, Lallemand launched MAGNIVA Platinum in Canada, extending a multi-strain product into a market where dairy and beef operators closely track forage performance. In April 2026, H. Wilhelm Schaumann GmbH launched FORTE 2.0 with new strains aimed at clostridial control in hard-to-ensile forages. These moves show that suppliers are using acquisitions and product releases to deepen product relevance.

Open space remains in organic-approved inoculants, precision application support, and products aimed at mycotoxin management. Specialist companies such as Agri-King, Inc. and H. Wilhelm Schaumann GmbH show that focused portfolios can still win premium positions in regional channels. Regulatory approval rules in Europe, North America, and Asia-Pacific continue to act as a moat, as obtaining strain authorization and labeling takes time and money. Companies that connect additives with digital feeding or fermentation monitoring tools are better placed to defend value, and Nutreco’s NutriOpt platform is one example of that broader service model. This structure leaves the silage additives market open to specialists, but it also favors players with strong science, distribution, and compliance capability.

Silage Additives Industry Leaders

Archer-Daniels-Midland Company

Lallemand Inc.

BASF SE

Volac International Limited

Novonesis A/S

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: H. Wilhelm Schaumann GmbH launched BONSILAGE FORTE 2.0, an upgraded homofermentative silage inoculant featuring the exclusive strain Lactobacillus huelsenbergensis to aggressively inhibit clostridia and stop butyric acid formation in hard-to-ensile, high-moisture crops like grass, alfalfa, and clover.

- March 2026: Lallemand Inc. launched MAGNIVA Platinum in Canada, expanding its most advanced forage inoculant to dairy and beef producers across the country. The product combines Lentilactobacillus hilgardii CNCM I-4785, Lactobacillus buchneri NCIMB 40788, and Pediococcus pentosaceus NCIMB 12455, and is supported by over 10 years of research at the Lethbridge Research and Development Centre among other institutions

- March 2026: H. Wilhelm Schaumann GmbH launched Silasil Energy.BG 2.0, a silage additive designed for wet, low-sugar energy crops and substrates with at least 20% dry matter, using 4 newly selected homofermentative lactic acid bacteria strains for rapid pH drop and stable fermentation in grass, clover-grass, alfalfa, green rye, and cover crops used in biogas systems.

Global Silage Additives Market Report Scope

Silage additives are used to improve the nutrient composition of silage, reduce storage losses by promoting rapid fermentation, reduce fermentation losses by limiting fermentation extent, and improve the bunk life of silage. The silage additives market is segmented by additive type (inoculants, organic acids and salts, enzymes, adsorbents, preservatives, and other types), silage type (cereals, legumes, and other silage types), and geography (North America, Europe, Asia-Pacific, South America, the Middle East, and Africa). The report provides market size and forecasts for value (USD) and volume (Metric Tons).

Additive Type

| Inoculants | Homofermentative |

| Heterofermentative | |

| Combination Inoculants | |

| Organic Acids and Salts | Formic Acid and Formates |

| Propionic Acid and Propionates | |

| Lactic Acid and Lactates | |

| Buffered/Blended Acid Preservatives | |

| Enzymes | Fiber-Digesting Enzymes |

| Starch-Digesting Enzymes | |

| Multi-enzyme Blends | |

| Adsorbents | Clay and Mineral Adsorbents |

| Fiber and Grain Carriers | |

| Fermentation & Spoilage Control Additives | Mold Inhibitors (Non-Acid Based) |

| Aerobic Stability Enhancers | |

| Other Types | Sugar-based Additives |

| Nutrient-based Additives |

Silage Type

| Grass Silage | |

| Cereals | Corn |

| Sorghum | |

| Oats | |

| Barley | |

| Other Cereal Silage | |

| Legumes | Alfalfa |

| Clover | |

| Other Legume Silage | |

| Mixed Forage Silage | |

| Other Specialty Silage |

Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| Turkey | |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| Additive Type | Inoculants | Homofermentative |

| Heterofermentative | ||

| Combination Inoculants | ||

| Organic Acids and Salts | Formic Acid and Formates | |

| Propionic Acid and Propionates | ||

| Lactic Acid and Lactates | ||

| Buffered/Blended Acid Preservatives | ||

| Enzymes | Fiber-Digesting Enzymes | |

| Starch-Digesting Enzymes | ||

| Multi-enzyme Blends | ||

| Adsorbents | Clay and Mineral Adsorbents | |

| Fiber and Grain Carriers | ||

| Fermentation & Spoilage Control Additives | Mold Inhibitors (Non-Acid Based) | |

| Aerobic Stability Enhancers | ||

| Other Types | Sugar-based Additives | |

| Nutrient-based Additives | ||

| Silage Type | Grass Silage | |

| Cereals | Corn | |

| Sorghum | ||

| Oats | ||

| Barley | ||

| Other Cereal Silage | ||

| Legumes | Alfalfa | |

| Clover | ||

| Other Legume Silage | ||

| Mixed Forage Silage | ||

| Other Specialty Silage | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| Turkey | ||

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size of the silage additives space?

The silage additives market was valued at USD 3.5 billion in 2025.

What is driving demand for silage additives through 2031?

Demand is being supported by feed efficiency pressure, rising global feed consumption, and the need to reduce dry matter loss and aerobic spoilage in commercial livestock systems.

Which additive type leads global revenue?

Inoculants are the largest segment, holding 45.0% in 2025, as producers prefer biological fermentation control for both preservation and feed out performance.

Which regional market is growing the fastest?

Asia-Pacific is the fastest-growing region, with a projected 7.0% CAGR during 2026-2031, led by China and India as forage systems modernize.

Why does corn silage create a strong demand for additives?

Corn is the largest silage type due to its yield and starch content, but it also poses aerobic stability and mycotoxin risks during feed out, underscoring the need for inoculants and preservatives.

Page last updated on: