Sciatica Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 16.97 Billion |

| Market Size (2031) | USD 26.19 Billion |

| Growth Rate (2026 - 2031) | 9.08% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

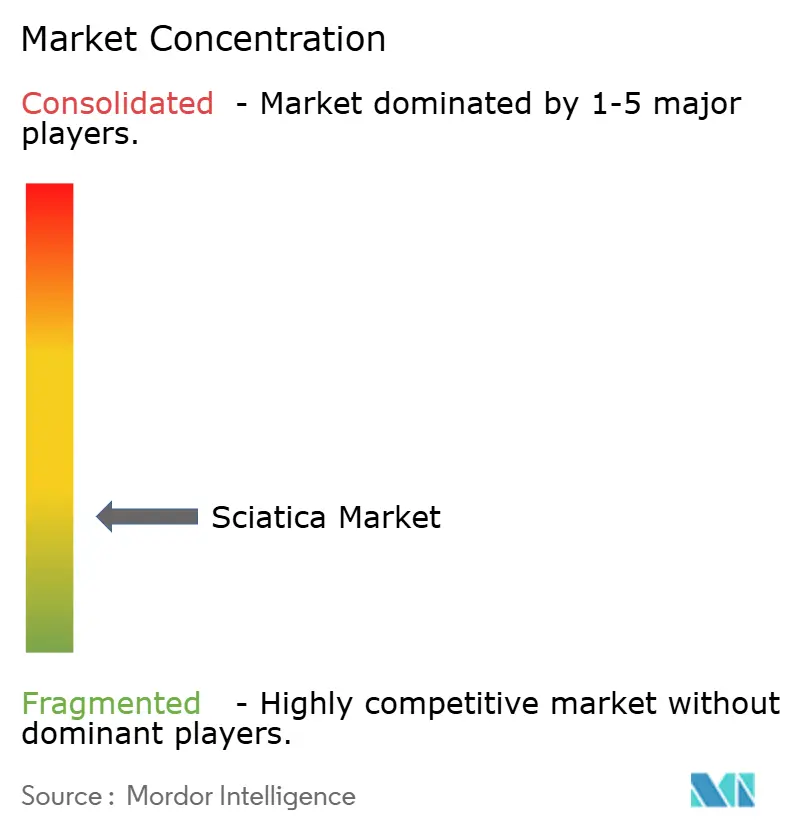

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sciatica Market Analysis by Mordor Intelligence

The sciatica market size is expected to grow from USD 15.56 billion in 2025 to USD 16.97 billion in 2026 and is forecast to reach USD 26.19 billion by 2031 at 9.08% CAGR over 2026-2031. Demand rises as aging populations experience higher rates of lumbar disc degeneration, while AI-assisted imaging shortens diagnostic pathways and supports earlier therapeutic intervention. Minimally invasive outpatient procedures now compete with hospital-based surgery, and expanding payor coverage for epidural steroid injections sustains interventional volumes. North America retains market leadership on the back of advanced reimbursement frameworks, yet Asia-Pacific is the fastest-growing region owing to widening healthcare access and rising incomes. Technology-led differentiation rather than scale now defines competition as illustrated by closed-loop neuromodulation approvals and targeted acquisitions.

Key Report Takeaways

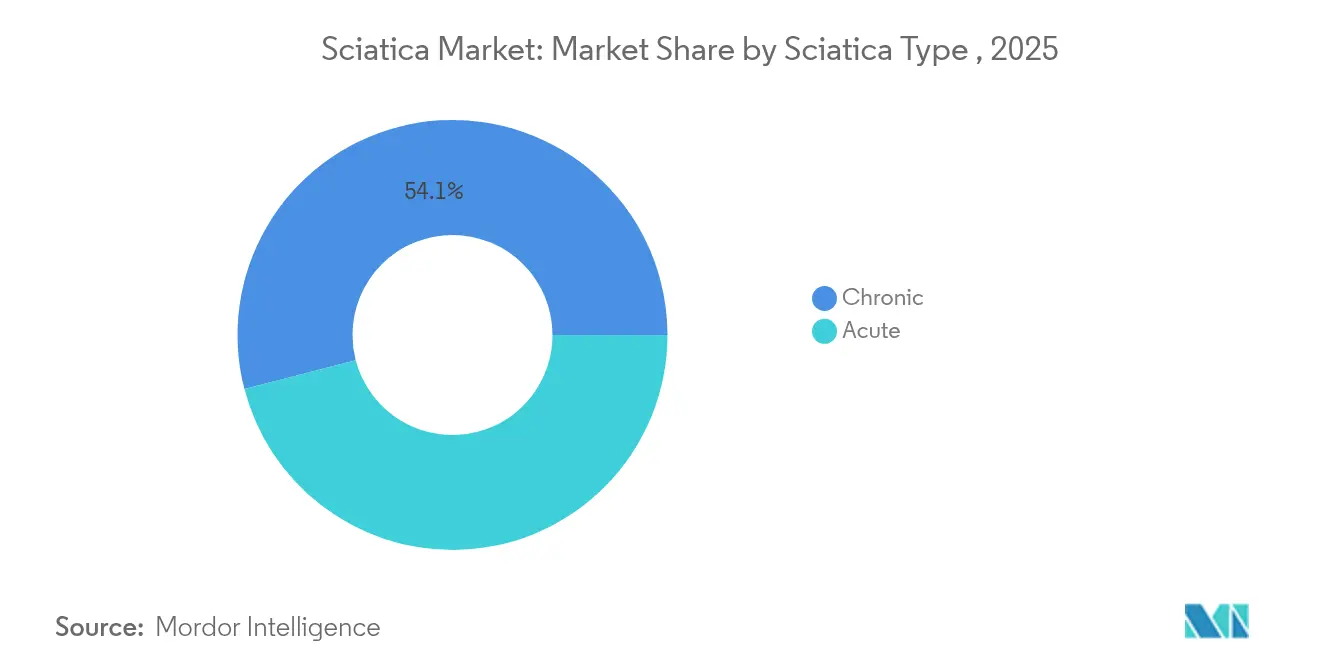

- By sciatica type, chronic cases held 54.05% of the sciatica market share in 2025, while acute cases are expanding at 9.92% CAGR to 2031.

- By pharmacological therapy, NSAIDs led with 39.05% revenue share in 2025; biologics and regenerative injectables are set to grow at 9.85% CAGR.

- By non-pharmacological modality, physical and exercise therapy accounted for 34.20% of the sciatica market size in 2025, whereas radiofrequency ablation is advancing at 10.6% CAGR.

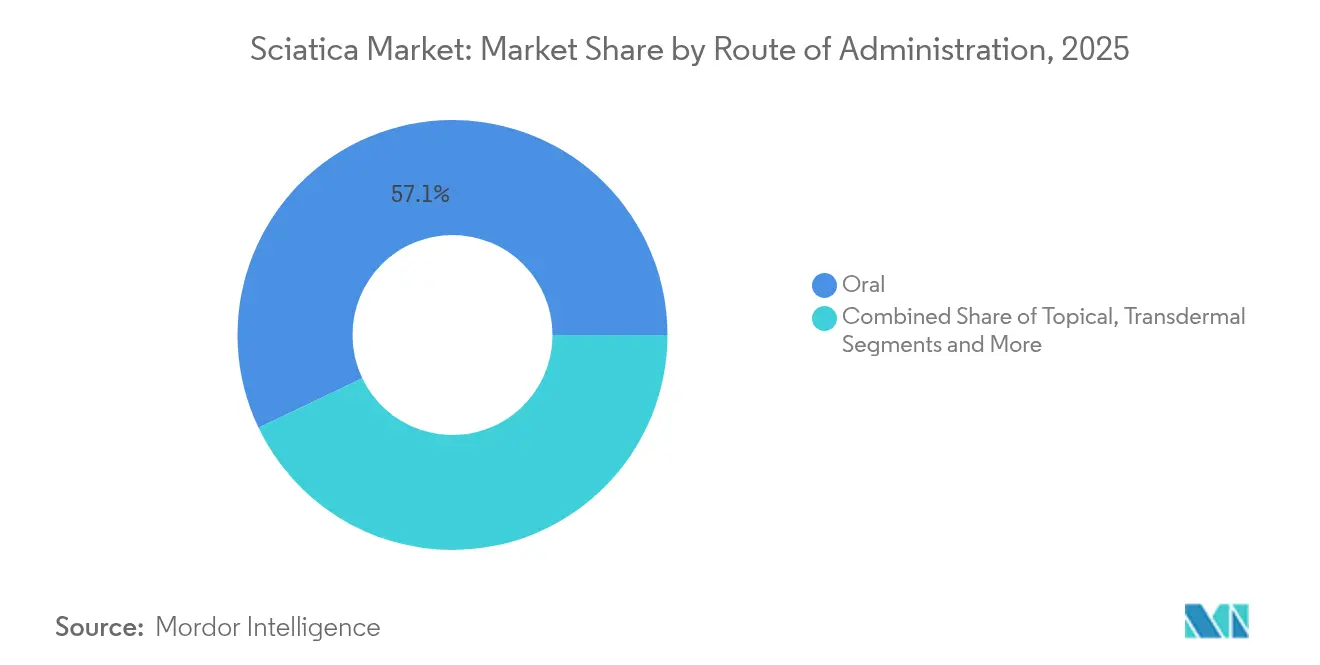

- By route of administration, oral delivery retained 57.10% share in 2025; transdermal systems are projected to rise at 9.9% CAGR.

- By end user, hospitals captured 39.10% of the market in 2025, yet home-care settings are progressing at 10.75% CAGR.

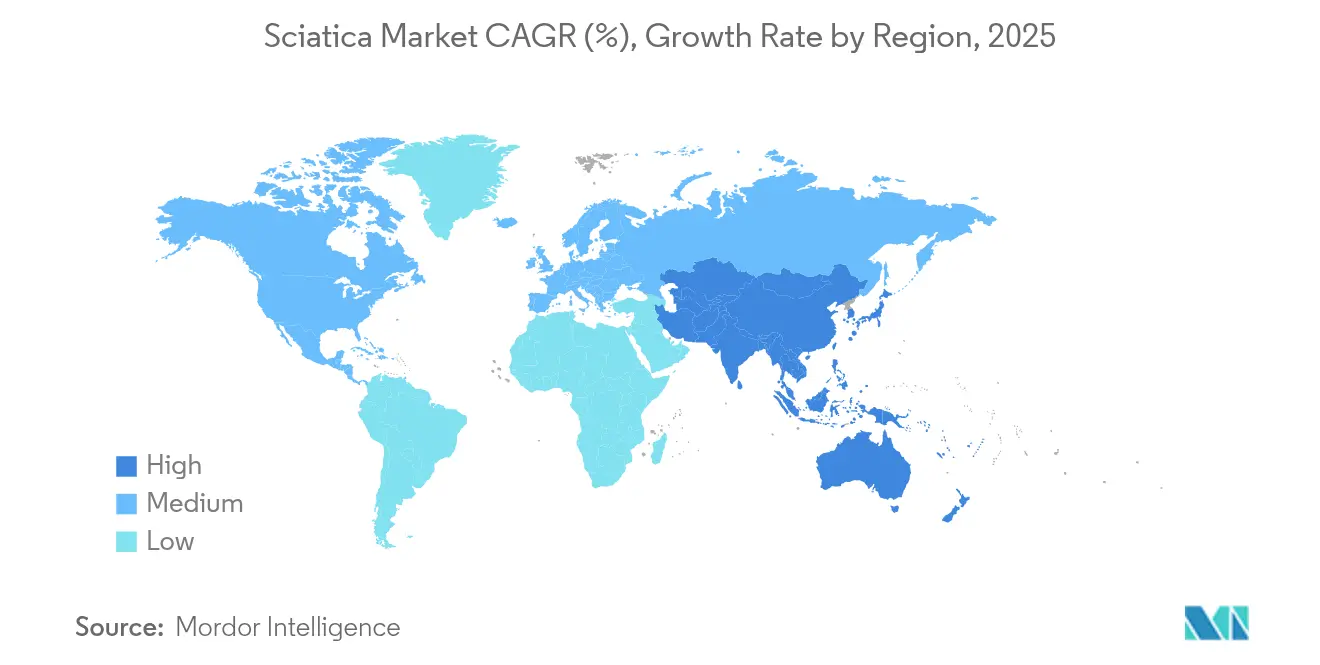

- By geography, North America commanded 39.20% share in 2025; Asia-Pacific is forecast to grow at 9.88% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Sciatica Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ageing populations & rising lumbar-disc degeneration rates | +2.1% | Global, highest in North America & Europe | Long term (≥4 years) |

| High diagnostic imaging penetration in OECD economies | +1.8% | North America & EU, spill-over to APAC | Medium term (2-4 years) |

| Shift toward minimally invasive outpatient pain procedures | +1.6% | Global, led by North America & Europe | Medium term (2-4 years) |

| Expanded payor coverage for epidural steroid injections | +1.3% | North America & EU | Short term (≤2 years) |

| AI-enabled MRI triage tools slash waiting times | +0.9% | OECD economies, early adoption in North America | Short term (≤2 years) |

| Growing direct-to-consumer nutraceutical bundles for sciatica | +0.7% | Global, strongest in North America & APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Ageing Populations & Rising Lumbar-Disc Degeneration Rates

Demographic transition is raising chronic pain prevalence as the ≥65-year cohort expands and 27.5 million elderly individuals live with spinal deformities. Degenerative disc disease already affects 266 million people worldwide, translating into steady demand for conservative and interventional care. Payers are broadening coverage for minimally invasive techniques that reduce surgical risk in comorbid seniors, and device makers are tailoring implants for osteoporotic bone quality. Together these factors underpin a durable growth base for the sciatica market.

High Diagnostic Imaging Penetration in OECD Economies

AI-reconstructed lumbar MRI can cut scan time by 45% without sacrificing accuracy. Automated image analysis improves early detection of disc herniation and stenosis, steering patients toward preventive therapies rather than delayed surgery. Hospitals report MRI throughput gains that ease bottlenecks in elective care, and reimbursement policies reward evidence-based triage[1]Centers for Medicare & Medicaid Services, “Facet Joint Interventions for Pain Management (DL38803),” cms.gov. Faster diagnosis strengthens clinical outcomes and accelerates revenue cycles, reinforcing imaging as a catalyst for the sciatica market.

Shift Toward Minimally-Invasive, Outpatient Pain Procedures

Endoscopic spine surgery yields 92% patient satisfaction with shortened stays, supporting migration to ambulatory centers. Basivertebral nerve ablation delivers clinically meaningful pain reduction in 77.4% of real-world patients at 12 months. Lower facility costs and quicker recovery appeal to payers and patients alike, prompting hospitals to open dedicated outpatient suites. These shifts intensify competition yet enlarge the addressable sciatica industry.

Expanded Payor Coverage for Epidural Steroid Injections

Medicare and major U.S. insurers continue to cover transforaminal injections when conservative therapy fails, though injection frequency is capped to curb steroid exposure. Policies require imaging guidance and strict documentation, fostering uptake of integrated radiology-anesthesia workflows. Stable reimbursement ensures volumes but pressures providers to demonstrate value through outcome tracking, underpinning procedural revenues within the sciatica market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack Of Universally Accepted Diagnostic Criteria | -1.4% | Global, most pronounced in developing markets | Long term (≥ 4 years) |

| Abundant Low-Cost Off-Label NSAID Usage | -1.1% | Global, highest impact in price-sensitive markets | Medium term (2-4 years) |

| Procedure Reimbursement Cuts In Europe | -0.8% | Europe, with spill-over effects to other regions | Short term (≤ 2 years) |

| Post-Opioid-Crisis Caution Limiting Prescription Renewals | -0.6% | North America, expanding to other regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Abundant Low-Cost Off-Label NSAID Usage

NSAIDs account for 39.53% of pharmacological sciatica therapies and remain inexpensive first-line options despite safety issues. High-risk prescribing consumes USD 31 million annually in the NHS and leads to 6,000 lost QALYs over 10 years. Long-term NSAID users face elevated knee-replacement risk, yet prescribers still favor these drugs where budgets are tight. As specialized biologics must prove superior value, cheap generics dampen near-term growth of the sciatica market.

Post-Opioid-Crisis Caution Limiting Prescription Renewals

Outpatient spine programs cut narcotic scripts by 37% through opioid-reduction protocols without harming outcomes. Policymakers encourage non-opioid modalities, boosting demand for neuromodulation and regenerative injections. Still, heightened oversight complicates access for appropriate candidates, tempering prescription-driven revenues in the sciatica market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sciatica Type: Chronic Dominance Drives Innovation

Chronic cases held 54.05% of the sciatica market share in 2025, underpinning steady demand for long-term management solutions. Acute presentations expand at 9.92% CAGR as prompt AI-assisted imaging redirects patients to early intervention. Emerging biologics, including NF-kappa B decoy oligonucleotides, are delivering 12-month pain relief and disc height restoration, highlighting disease-modifying potential. Acute episodes benefit from proactive epidural injections and guided exercise that prevent degeneration. Combined, these trends reinforce segmentation-specific investment across the sciatica market.

A growing body of evidence positions intradiscal stem-cell therapy as a viable option for refractory chronic pain, with trials demonstrating improved disc volume and function. Health insurers are piloting value-based payment bundles that differentiate reimbursement for acute versus chronic pathways. As clinical guidelines mature, stakeholders expect clearer coding and accelerated coverage decisions—a dynamic that enlarges overall sciatica market size at the segment level.

By Pharmacological Therapies: NSAIDs Face Emerging Competition

Traditional NSAIDs led revenue with 39.05% share in 2025, yet safety-driven prescribing curbs sustained use. Biologics and regenerative injectables are growing 9.85% annually, reflecting payer readiness to reimburse interventions that delay surgery. Corticosteroids remain central for flare management, while anticonvulsants treat neuropathic components.

Innovations target disc pathology directly: allogeneic disc progenitor cells have improved pain and disability scores in randomized trials, with regulators reviewing fast-track designations. Novel COX-2 inhibitors aim to mitigate GI toxicity, though cardiovascular risk surveillance persists. The segment’s shift from symptomatic relief to regenerative repair supports premium pricing and lifts the sciatica market size for advanced pharmacology.

By Non-Pharmacological Treatment Modality: Technology Transforms Traditional Approaches

Physical and exercise therapy captured 34.20% of 2025 revenues, underscoring its role as first-line care. Radiofrequency ablation leads growth at 10.6% CAGR thanks to refined patient selection and outcome data. Epidural steroid injections persist despite debate, while closed-loop spinal cord stimulation systems such as Medtronic’s Inceptiv adjust therapy in real time to maintain analgesia.

Complementary approaches gain legitimacy through randomized trials demonstrating phytochemical efficacy in neuropathic pain. Chemonucleolysis with condoliase is emerging as a minimally invasive disc-dissolution method, attracting surgeons seeking alternatives to open discectomy. These hybrid modalities broaden choice and reinforce technology-centric competition in the sciatica market.

By Route of Administration: Oral Dominance Challenged by Innovation

Oral delivery retained 57.10% share in 2025, owing to convenience and established prescribing habits. Transdermal systems are growing 9.9% CAGR as patches reduce systemic exposure; buprenorphine patches show favorable dosing economics in chronic low-back pain. Parenteral and epidural routes serve interventional needs, while topical diclofenac matches oral NSAID efficacy with fewer systemic events.

Direct-to-consumer nutraceutical sales via e-commerce deliver convenience but challenge clinicians to integrate self-selected supplements into evidence-based care. The convergence of novel delivery technologies and patient preference continues to diversify revenue sources across the sciatica market.

By End User: Home-Care Surge Reshapes Delivery

Hospitals generated 39.10% of 2025 revenues, reflecting their dominance in acute imaging and complex interventions. Home-care settings are advancing 10.75% CAGR, powered by telemedicine follow-up that reliably monitors post-operative recovery. Portable devices such as the FDA-cleared Kizu Spine Belt enable non-pharmacological therapy at home, supporting patient autonomy.

Ambulatory surgical centers and specialized pain clinics gain share as payers incentivize site-of-service shifts that lower costs while maintaining quality. Enhanced recovery after surgery protocols shorten stays for elderly fusion patients, illustrating system-wide adoption of efficiency best practices. These distributed models underpin sustained expansion of the sciatica market.

Geography Analysis

North America commanded 39.20% of global revenue in 2025, underpinned by comprehensive insurance coverage and rapid adoption of closed-loop spinal cord stimulators cleared by the FDA in 2024 and 2025. Medicare continues to reimburse epidural injections and selective nerve-root blocks under strict indications, supporting procedure volumes. An aging, sedentary population and high obesity prevalence sustain long-term demand, while robust research funding accelerates translational innovation.

Europe remains sizeable but faces reimbursement cuts that temper procedure growth; nonetheless, cost-effective minimally invasive techniques align with EU health-system objectives. Adoption of AI-enabled MRI triage mitigates waiting-list pressures and improves early treatment access. Germany, the United Kingdom, and France prioritize evidence-based pathways, creating a stable environment for clinically validated devices and biologics.

Asia-Pacific is the fastest-growing region at 9.88% CAGR as healthcare investments rise and aging demographics resemble Western patterns. Japan and South Korea lead technological uptake, while India expands access through insurance schemes and public-private partnerships. Multinational device makers localize production to meet regulatory requirements and tap cost-sensitive segments. Collectively these dynamics enlarge regional contributions to the sciatica market size.

Competitive Landscape

The market is fragmented: Medtronic, Boston Scientific, and Abbott hold entrenched channel relationships, yet smaller innovators secure share through differentiated technology. Globus Medical’s USD 250 million acquisition of Nevro in 2025 bolstered its neuromodulation portfolio and signaled accelerating consolidation. Closed-loop stimulators such as Inceptiv and HFX redefine performance benchmarks, narrowing the gap between incumbents and upstarts.

Vertical integration emerges as a strategic theme; firms bundle imaging AI, therapy devices, and remote-monitoring software to control the full continuum of care. Biotechnology entrants develop regenerative disc therapies, targeting disease modification rather than symptom relief, and partner with device firms for combined delivery platforms.

White-space opportunities arise in personalized medicine: genetic markers and predictive analytics guide therapy choice, promising stronger outcomes and payer acceptance. Market participants that align with evidence-based reimbursement and demonstrate cost utility will likely gain share across the sciatica market.

Sciatica Industry Leaders

Scilex Holding

SpineThera

Medtronic plc

Boston Scientific Corporation

Teva Pharmaceutical Industries

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Globus Medical completed its acquisition of Nevro Corp for USD 250 million, expanding its neuromodulation platform.

- September 2024: Nevro received FDA clearance for AI-driven spinal cord stimulation that adjusts output via machine-learning algorithms.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines the global sciatica market as all revenues earned worldwide from products and services that diagnose, manage, or cure pain caused by compression or irritation of the sciatic nerve. Our study covers oral and injectable drugs, regenerative biologics, image-guided pain procedures, physical rehabilitation programs, and implantable neuromodulation devices.

Scope Exclusion: General wellness apps, off-the-shelf back supports, and spinal fusion hardware are excluded to avoid double counting.

Segmentation Overview

- By Sciatica Type

- Acute Sciatica

- Chronic Sciatica

- By Pharmacological Therapies

- Non-steroidal Anti-inflammatory Drugs (NSAIDs)

- Corticosteroids

- Antidepressants

- Anticonvulsants

- Opioids

- Emerging Biologics & Regenerative Injectables

- By Non-Pharmacological Treatment Modality

- Physical & Exercise Therapy

- Epidural Steroid Injection

- Radio-frequency Ablation

- Spinal Cord Stimulation

- Chemonucleolysis (Condoliase etc.)

- Complementary & Alternative (Acupuncture, Herbal)

- By Route of Administration

- Oral

- Topical

- Parenteral / Epidural

- Transdermal

- By End User

- Hospitals

- Specialty Pain Clinics

- Ambulatory Surgical Centers

- Home-care

- Rehabilitation Centers

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

We held structured conversations with pain physicians, physiotherapists, interventional radiologists, and payor reviewers across North America, Europe, and Asia. Their inputs helped us confirm prevalence multipliers, realistic selling prices, and likely adoption curves for emerging biologic injectables, closing critical gaps.

Desk Research

During desk work, we pulled incidence and treatment-seeking ratios from WHO Global Health Observatory, CDC National Center for Health Statistics, Eurostat hospital discharge files, and UN Population Prospects, giving us a robust patient pool.

Our team then layered therapy penetration and spend patterns taken from Pain Society guidelines, customs trade data for steroid injectables, WSTS shipment logs for spinal stimulators, plus revenue splits in 10-Ks and investor decks, supported by D&B Hoovers and Dow Jones Factiva. The sources named here are illustrative; many additional public records were reviewed for data validation.

Market-Sizing & Forecasting

Our model blends top-down and bottom-up checks. It starts with a prevalence-to-treated-patient cascade tied to prescription volumes, procedure rates, and average therapy spend, then validates totals with sampled supplier roll-ups and channel checks. Six fingerprints, age-adjusted incidence, imaging utilization per capita, share of chronic cases, steroid injection frequency, NSAID course cost, and neuromodulator uptake, anchor assumptions. Multivariate regression against GDP per capita and the 65-plus share drives the 2025-2030 outlook; where local data were thin, regional price corridors verified in interviews bridged gaps.

Data Validation & Update Cycle

We run variance scans, peer reviews, and expert re-contacts before release. Models refresh each year and reopen mid-cycle if events such as landmark FDA approvals materially change demand.

Why Mordor's Sciatica Baseline Earns Solid Decision-Maker Trust

Published sciatica numbers often differ because firms vary scope, patient funnels, and data-refresh cadence, whereas our inclusion of both drug and non-drug spend plus annual reviews delivers a steadier view.

Key divergence drivers are competitor models that limit revenue to pharmacy drugs, drop secondary Asian markets, or fold generic low-back-pain therapies into totals, creating wide swings versus our disciplined universe.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 15.56 B (2025) | Mordor Intelligence | - |

| USD 5.92 B (2025) | Regional Consultancy A | Counts only pharmacy-dispensed drugs, excludes procedure fees |

| USD 5.62 B (2025) | Industry Tracker B | Omits several Asian markets and hospital channel sales |

| USD 17.34 B (2024) | Analytics Firm C | Bundles sciatica with general low-back-pain therapies and equipment |

The comparison shows that Mordor's clearly defined scope, transparent variables, and disciplined annual reconciliation provide a dependable baseline executives can trace and replicate with confidence.

Key Questions Answered in the Report

What is the current size of the sciatica market?

The sciatica market is valued at USD 16.97 billion in 2026 and is projected to reach USD 26.19 billion by 2031.

Which region leads the global sciatica market?

North America holds 39.20% of global revenue, supported by robust reimbursement policies and rapid adoption of advanced pain technologies.

Which treatment modality is growing fastest?

Radiofrequency ablation records the highest growth at 10.6% CAGR because minimally invasive techniques are increasingly preferred for durable pain relief.

How fast is the Asia-Pacific market expanding?

The Asia-Pacific sciatica market is forecast to grow at a 9.88% CAGR through 2031 due to expanding healthcare access and rising disposable incomes.

What role do biologics play in future therapy?

Biologics and regenerative injectables are forecast to grow 9.85% annually as clinical trials demonstrate durability and payers recognize disease-modifying value.

Page last updated on: