Recloser Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

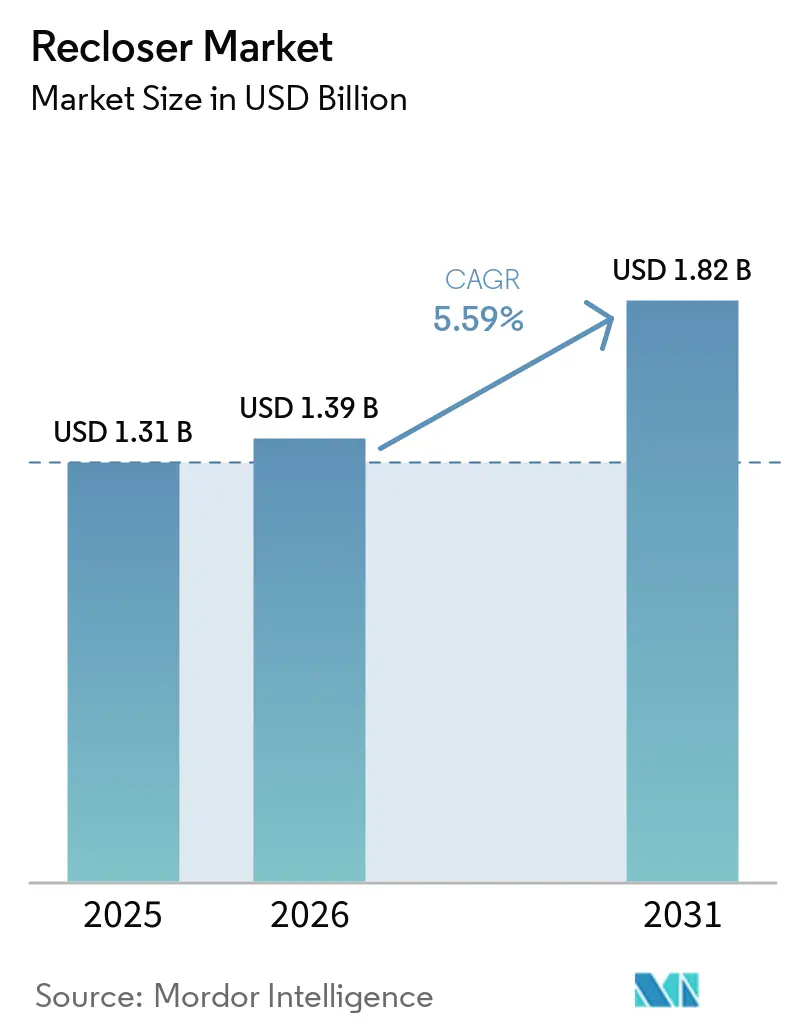

| Market Size (2026) | USD 1.39 Billion |

| Market Size (2031) | USD 1.82 Billion |

| Growth Rate (2026 - 2031) | 5.59% CAGR |

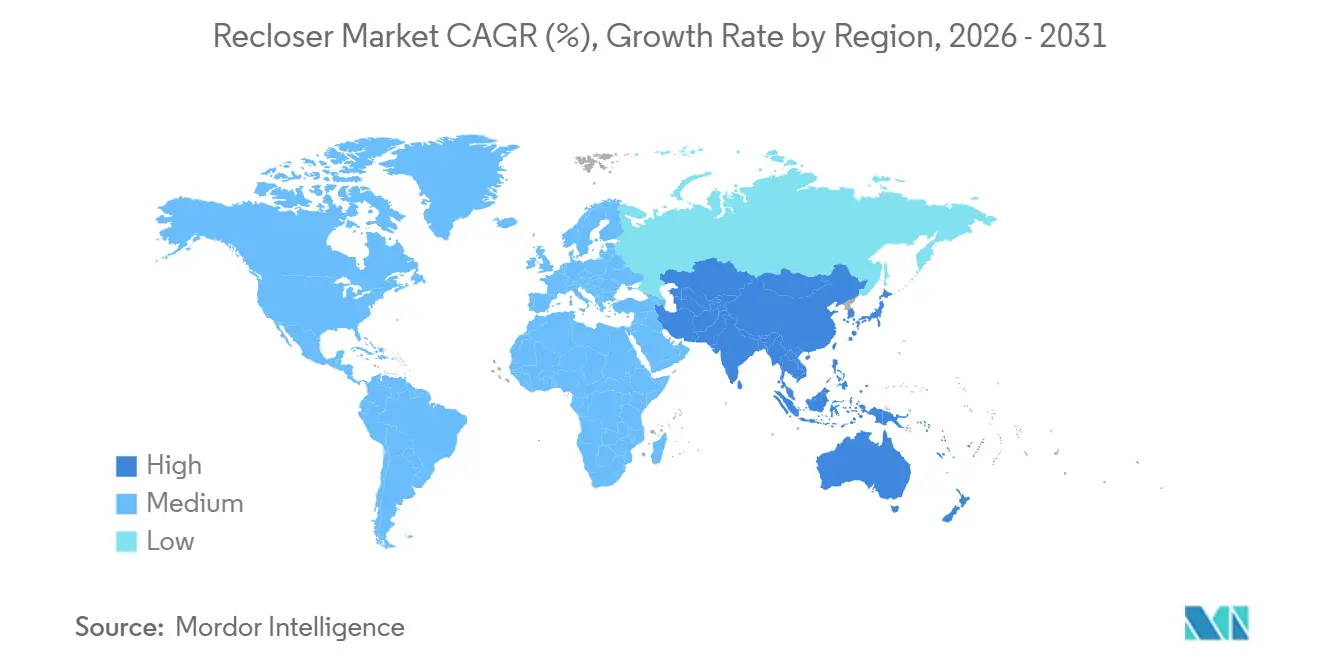

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

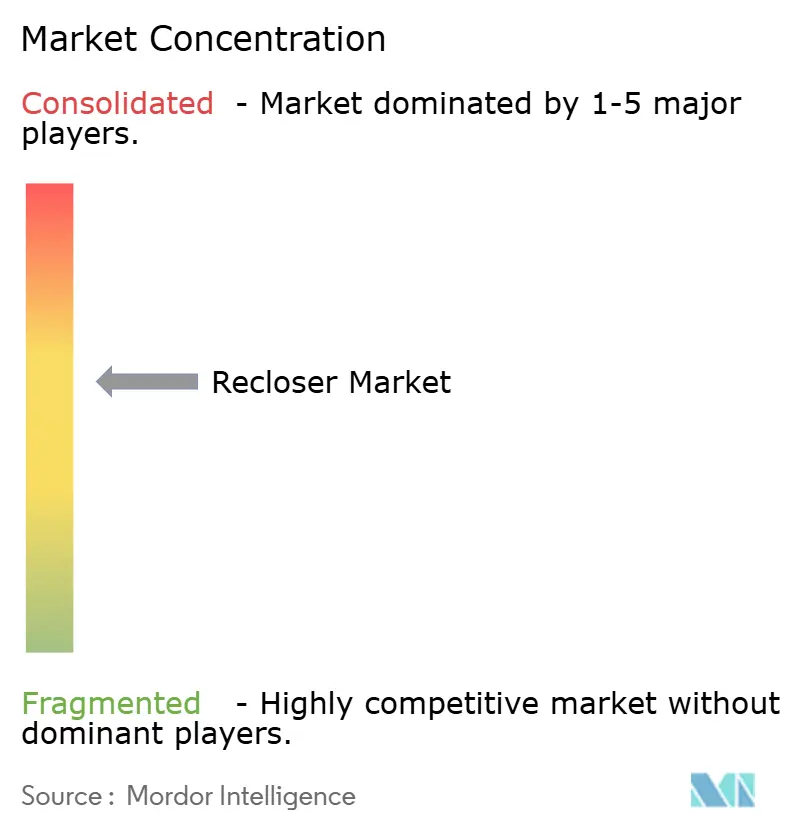

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Recloser Market Analysis by Mordor Intelligence

The Recloser Market size is projected to expand from USD 1.31 billion in 2025 and USD 1.39 billion in 2026 to USD 1.82 billion by 2031, registering a CAGR of 5.59% between 2026 to 2031. Utilities are accelerating replacements of SF₆-insulated equipment ahead of the European Union’s January 2026 F-gas deadline, while China State Grid’s five-year USD 574 billion plan and the United States’ 2,600 GW renewable interconnection backlog are pulling micro-processor-based reclosers into standard specifications. Power distribution automation now claims roughly one-third of grid-modernization outlays, placing reclosers at the nexus of reliability mandates and decarbonization timelines. Competition remains moderately fragmented, yet new entrants are capitalizing on AI-enabled fault diagnostics that cut SAIDI up to 80% versus legacy hydraulic designs.

Key Report Takeaways

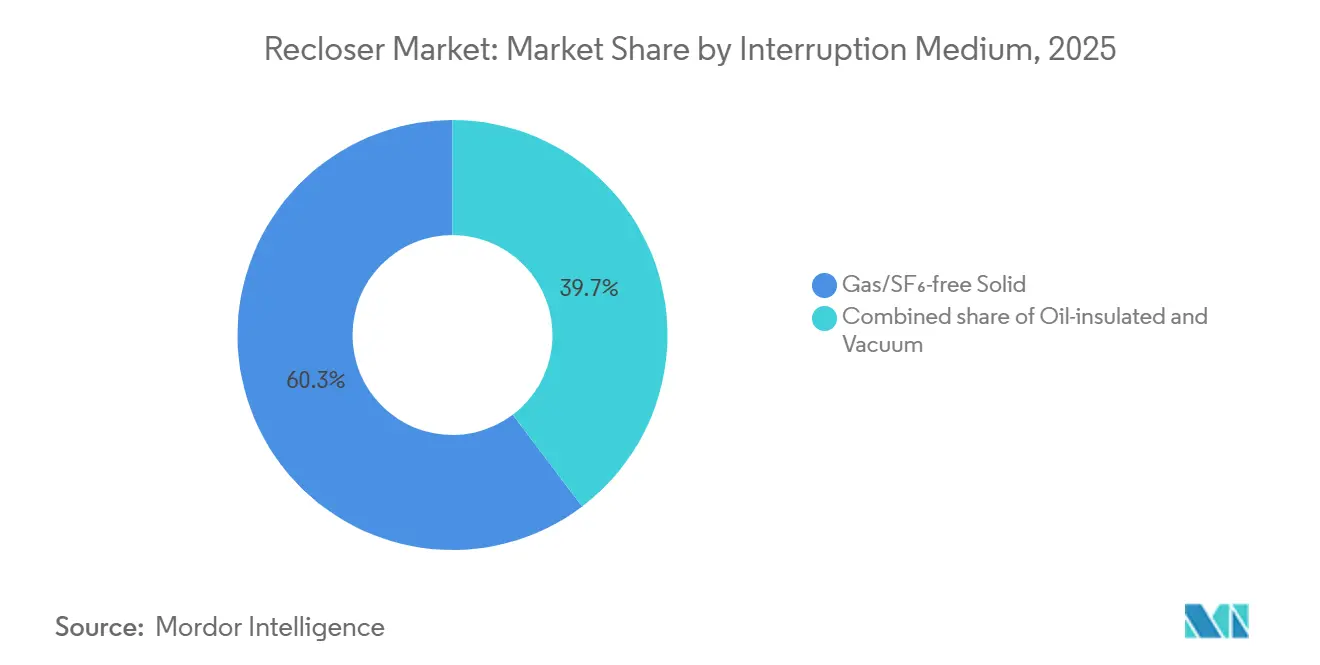

- By interruption medium, gas and SF₆-free solid insulation led with 60.3% 2025 recloser market share, while vacuum interrupters are advancing at an 8.0% CAGR to 2031.

- By phase configuration, three-phase units commanded 48.9% share in 2025, and triple-single configurations are set to grow 6.5% through 2031.

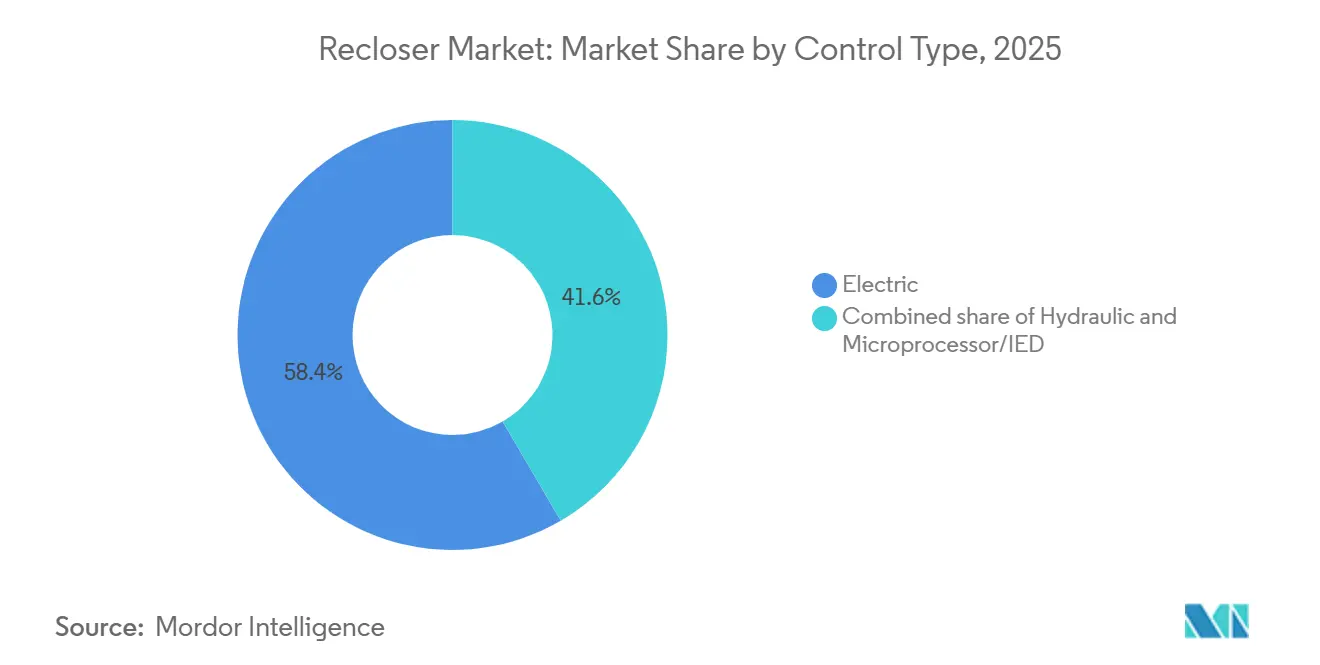

- By control type, electric actuation captured 58.4% of 2025 demand, but micro-processor and IED controls are rising at a 6.3% CAGR during 2026-2031.

- By voltage class, the 16-27 kV class accounted for 44.7% of 2025 volume, whereas 28-38 kV units will accelerate at 6.1% through 2031.

- By installation location, pole-mounted overhead installations represented 72.0% of shipments in 2025, yet pad-mounted designs are forecast to climb 7.3% over the period.

- By end-user, utility T&D buyers held 61.5% share in 2025, while commercial and institutional users will expand at 6.8% through 2031.

- By geography, Asia-Pacific dominated with 42.8% revenue share in 2025 and is projected to maintain the fastest 6.2% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of Recloser Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid-modernization programs & T&D automation spending surge | +1.8% | Global, with concentration in North America, China, India, EU | Medium term (2-4 years) |

| Accelerated renewable energy interconnections at medium-voltage levels | +1.5% | Global, strongest in APAC (China, India, ASEAN), North America, Europe | Medium term (2-4 years) |

| Reliability mandates under IEEE 1366 SAIDI/SAIFI tightening (North America) | +0.9% | North America (United States, Canada), spill-over to Latin America | Short term (≤ 2 years) |

| AI-enabled predictive maintenance lowering total asset lifecycle cost | +0.7% | Global, early adoption in North America, Europe, Australia | Long term (≥ 4 years) |

| Fast-rising micro-grid deployments in islanded & remote grids | +0.6% | APAC (Pacific islands, remote mining), Africa, Middle East | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Grid-Modernization Programs and T&D Automation Spending Surge

Utilities allocated USD 480 billion to grid upgrades in 2025 and plan to invest USD 5.8 trillion through 2035, funneling roughly one-third toward distribution automation that includes high-speed reclosers [1]U.S. Department of Energy, “Grid Resilience and Innovation Partnerships Program,” energy.gov. Eversource earmarked USD 16.2 billion of its 2025-2029 capital plan for smart-grid overlays across New England circuits serving 1.4 million customers [2]Eversource Energy, “2025–2029 Capital Investment Plan,” eversource.com. China State Grid is funding 137,500 circuit-kilometers of feeders in western provinces, creating landmark orders for vacuum units rated at 27 kV and 38 kV. Alberta’s 20-year USD 5.1 billion blueprint dedicates two-thirds of spending to renewable-driven feeder automation, while the U.S. GRIP program has awarded USD 7.6 billion to wildfire-hardening projects that specify pad-mounted reclosers in coastal flood zones.

Accelerated Renewable Energy Interconnections at Medium-Voltage Levels

Interconnection queues held 2,600 GW of solar, wind, and storage in early 2026, stretching median wait times beyond 36 months and pushing utilities to adopt IEEE 1547-2018-compliant reclosers able to manage bidirectional flows. India’s 450 GW renewables target demands USD 21 billion in transmission upgrades, much at 33 kV and 11 kV, where reclosers form the first protection layer. Duke Energy Florida cites 17 GW of queued data-center load that now dictates accelerated deployment of intelligent reclosers across 24 kV loops. ASEAN nations face USD 300 billion in grid investment by 2040 to support cross-border power trade, reinforcing sustained demand for 15-38 kV devices. Massachusetts utilities cut fault-restoration times 60% in 2025 by pairing reclosers with ADMS software that reroutes power within 30 seconds.

Reliability Mandates Under IEEE 1366 SAIDI/SAIFI Tightening (North America)

New York, California, and Massachusetts toughened outage metrics in 2024-2025, imposing penalties that make sub-second recloser operation financially attractive. NYSEG forecasts a 40% customer-interruption reduction by installing triple-single units on poor-performing rural feeders. Eversource’s underground Kendall Square substation integrates SF₆-free switchgear with reclosers to meet urban reliability targets. The 2024 IEEE 1366 revision introduced momentary metrics, driving utilities toward reclosers that separate temporary from permanent faults. SaskPower’s CAD 1.15 billion rural program adds reclosers on 2,400 km of agricultural circuits to arrest SAIDI drift.

AI-Enabled Predictive Maintenance Lowering Total Asset Lifecycle Cost

Machine-learning models applied to recloser telemetry predicted insulator or bushing failures up to two weeks in advance with 85-95% accuracy, halving unplanned outages and extending asset life 20%. NOJA Power’s RC-20 controller streams 1 GB/day of synchrophasor data, enabling utilities to detect ferroresonance and conductor galloping long before protective trips. ARENA-backed Australian pilots cut arc-flash energy 40%, while SEL’s Arc Sense Technology now flags high-impedance faults that spark wildfires in drought-stricken California and Australia. Metropolitan Water District replaced legacy breakers on its 830-mile aqueduct with IEC 61850-enabled reclosers, reducing SCADA polling latency from 4 seconds to 10 milliseconds.

Restraints Impact Analysis of Recloser Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Capital-intensive retrofit of legacy hydraulic fleets | −0.4% | Mature markets with aging infrastructure | Medium term (2-4 years) |

| Lengthy utility qualification cycles and type-test backlogs | −0.3% | Global | Short term (≤ 2 years) |

| Cyber-security compliance costs for IEC 61850-based controls | −0.5% | Developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Capital-Intensive Retrofit of Legacy Hydraulic Fleets

Hydraulic devices need oil changes every 3-5 years and cost USD 600-1,000 per repair, yet new vacuum units range USD 15,000-40,000, stretching payback to a decade. Eaton’s Form 7 retrofit kit slashes install cost 40% by re-using the pole structure, but European projects bear extra USD 2,000-5,000 PCB disposal fees that extend timelines [3]Eaton Corporation, “Form 7 Recloser Retrofit Program,” eaton.com. ABB’s battery-free Eagle single-phase model targets one-to-one hydraulic swaps and encrypts Wi-Fi commissioning traffic for field crews.

Lengthy Utility Qualification Cycles and Type-Test Backlogs

Full IEC 62271-111 testing costs up to USD 500,000, and queues stretch 18 months, deterring small vendors [4]International Electrotechnical Commission, “IEC 62271-111 Type-Test Requirements,” iec.ch. G&W’s Viper-ST finished tests in March 2025 but still endured six additional months of utility-specific acceptance, delaying revenue capture. EU CE-mark audits add another half-year, and North American buyers often repeat impulse and EMI tests under IEEE C37.60, driving duplicate expenses.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Recloser Market Segment Analysis

By Interruption Medium:

Vacuum Units Take Share as SF₆ Ban LoomsVacuum interrupters dominated growth with an 8.0% CAGR, while gas and SF₆-free solids retained the largest 60.3% 2025 recloser market share. The recloser market size for vacuum technology is set to expand rapidly as utilities in Europe replace banned SF₆ equipment starting January 2026.

Utilities that migrated to vacuum report maintenance savings because the design delivers 10,000 operations without gas top-ups. ABB’s SafePlus Air and Schneider’s GM AirSeT illustrate retrofits that fit existing footprints, easing regulatory approval. Oil-filled units persist in arctic and seismic vaults, but new hermetic vacuum bottles rated –50 °C are narrowing that niche.

By Phase:

Triple-Single Architecture Accelerates on Rural FeedersThree-phase devices held 48.9% of the 2025 recloser market share, yet triple-single models will outpace at a 6.5% CAGR through 2031. Rural circuits carrying irrigation and oil-field loads gain 30-40% fewer customer interruptions when only the faulted phase is opened.

Hubbell’s LineDefender and ABB’s Eagle demonstrate visible fault indication and self-powered operation that linemen can install without cranes. As micro-processor logic synchronizes independent poles, utilities foresee triple-single adoption even on 27 kV backbone laterals to optimize DER hosting capacity.

By Control Type:

IED Platforms Embed Synchrophasors and CybersecurityElectric actuation still represented 58.4% of shipments in 2025, but micro-processor and IED platforms are growing 6.3% on rising IEEE 1547-2018 and IEC 61850 requirements. The recloser market size for intelligent controllers is projected to widen as embedded PMUs stream 1 GB/day of high-resolution data.

SEL’s 651R adds MACsec encryption, meeting IEC 62351 extensions that many U.S. and EU utilities now stipulate. NOJA’s RC-20 won an engineering excellence award for using sampled-values messaging that hits sub-10 ms tripping, halving arc-flash energy on critical feeders.

By Voltage Class:

28-38 kV Band Gains on Renewable Backbone UpgradesThe 16-27 kV class controlled 44.7% of demand in 2025, but 28-38 kV units are forecast at 6.1% CAGR, driven by data centers and renewable hubs. Recloser market size in this higher band will benefit from China State Grid’s 35 kV feeders and U.S. 34.5 kV conversions that cut I²R losses on long rural spans.

G&W’s Viper-ST now spans up to 170 kV BIL, letting a single frame standardize spares across voltage tiers. India’s USD 93 billion substation plan channels disproportionate capital to 33 kV lines, reinforcing demand for vacuum interrupters suited to 40.5 kV insulation.

By Installation Location:

Pad-Mounted Growth Follows Undergrounding WavePole-mounted gear still dominates at 72.0% of 2025 shipments, yet pad-mounted configurations will rise 7.3% as wildfire-prone states and urban cores bury circuits. The recloser market size for pad-mounted units receives impetus from San Francisco’s USD 1.63 billion undergrounding initiative and California Energy Commission grants.

S&C’s Vista Green uses SF₆-free CO₂-mix insulation and survives full submersion, winning orders from coastal utilities. Underground vault standards in Boston and Seattle now stipulate arc-resistant pad-mounted reclosers with remote racking, catalyzing uptake despite 40-60% price premiums.

By End-User:

Commercial & Institutional Campuses Accelerate ProcurementUtility T&D customers remained the largest buyers at 61.5% of revenue, while commercial and institutional users will grow 6.8% as data-center clusters build N+1 micro-grids. The recloser market size for these campuses is expanding alongside 17 GW of queued U.S. data-center load in early 2026.

Hospitals in California and Texas installed more than 200 MW of CHP and solar + storage during 2025, each relying on 2-4 reclosers to segment emergency circuits. Mining and heavy-industry buyers in Chile and Zambia are increasingly opting for pad-mounted devices designed to withstand severe dust exposure and high-altitude operating conditions. This trend supports stable demand, even as growth slows in more mature regions.

Geography Analysis

APAC Recloser Market

Asia-Pacific secured 42.8% of 2025 revenue and is forecast to grow at 6.2% CAGR, buoyed by China's USD 574 billion distribution expansion and India's USD 93 billion substation program targeting 500 GW of non-fossil power. State Grid aims to wire 137,500 circuit-kilometers of new lines, most at 35 kV, directly lifting the regional recloser market. Pacific Islands funded 5 MW of mini-grids under the REnew Pacific scheme, validating single-phase units that enable seamless islanding during cyclones.

North America Recloser Market

In North America, the U.S. GRIP program injects USD 7.6 billion into wildfire mitigation and undergrounding across 50 states. Eversource's USD 16.2 billion distribution plan and Canada's NRCan grants underscore stable utility spending. Data-center clusters in Virginia, Florida, and Texas are specifying 34.5 kV pad-mounted reclosers with IEC 61850 Edition 2.1 cybersecurity, pushing suppliers to add MACsec and role-based access control.

Europe Recloser Market

In Europe, the SF₆ ban forces the retrofit of 50,000-70,000 medium-voltage devices. ABB shipped SafeRing Air switchgear to E.ON Germany ahead of the deadline, and Schneider invested USD 9.6 million in its Leeds plant for Ringmaster AirSeT production. Nordic DSOs such as Landsnet pioneered fully digital substations that integrate recloser PMUs over fiber, a blueprint spreading to the Baltics and Central Europe.

South America Recloser Market

Growth in South America is driven by ANEEL-mandated loss reduction initiatives in Brazil and increased mining capital expenditure in Chile's Atacama region. Pad-mounted reclosers, designed for altitudes of up to 4,500 meters, are now being utilized in pit-rim networks to support electric haul trucks.

MEA Recloser Market

The Middle East and Africa will grow as Saudi Electricity Company orders 5,000-7,000 vacuum units for NEOM and Red Sea renewables, and DEWA deploys automated reclosers across the Mohammed bin Rashid Al Maktoum solar park. South Africa's Eskom backlog of 20,000 aging units remains a latent replacement pool, contingent on fiscal reform.

Competitive Landscape

The Recloser Market is semi consolidated. Regional challengers NOJA Power, G&W Electric, S&C Electric, and Tavrida Electric exploit voltage or geography niches where incumbents face longer lead times. GE Vernova’s USD 5.275 billion February 2026 purchase of Prolec GE adds seven transformer plants, enabling bundled bids that package reclosers with medium-power transformers and cut utility vendor count.

MacLean Power Systems merged with Power Grid Components in March 2026, assembling a portfolio spanning Allied Bolt to Vizimax and giving cooperatives a one-stop catalog of reclosers, insulators, and connectors. Smaller players gain traction by inserting AI algorithms that forecast wildlife-caused faults with up to 95% accuracy, a feature utilities see as crucial under wildfire liability statutes in California and Australia.

Compliance with IEC 62351 drives differentiation: SEL’s MACsec-enabled 651R, NOJA’s RC-20, and Schneider’s EcoCare-monitored GM AirSeT offer secure firmware updates, winning bids where utilities report hundreds of monthly cyberattacks. Meanwhile, rapid triple-single innovations are chipping at three-phase incumbency; Hubbell’s LineDefender and S&C’s Vista Green now command price premiums yet deliver measurable SAIDI savings on rural feeders.

Recloser Industry Leaders

ABB Ltd

Eaton Corp

Siemens Energy AG

Schneider Electric SE

Hubbell Power Systems

- *Disclaimer: Major Players sorted in no particular order

Recloser Market Companies Covered in this Report

- ABB Ltd

- Eaton Corporation plc

- Siemens Energy AG

- Schneider Electric SE

- Hubbell Power Systems

- S&C Electric Company

- NOJA Power Switchgear

- G&W Electric Company

- Tavrida Electric

- GE Grid Solutions

- Schweitzer Engineering Laboratories (SEL)

- Arteche Group

- ERMCO Inc.

- Ningbo Tianan (Group) Co.

- Zhejiang Zhegui Electric

- CG Power & Industrial Solutions

- Myers Power Products

- Brush Group

- Mitsubishi Electric Power Products

- Powell Industries

Recent Industry Developments in Recloser Market

- March 2025: ABB confirmed a USD 120 million commitment for a 320,000 square-foot Selmer, Tennessee facility that will elevate U.S. capacity for low-voltage electrification products by over 50%.

- March 2025: Schneider Electric earmarked USD 140 million for new U.S. manufacturing, including an 85 million Mt. Juliet, Tennessee plant producing medium-voltage switchgear.

- March 2025: Siemens launched SENTRON ECPD, an electronic protection device switching up to 1,000 times faster than thermal-magnetic products and freeing up 80% panelboard space.

- October 2024: S&C Electric signed a framework deal with National Grid Electricity Distribution to supply TripSaver II reclosers, reducing UK customer interruptions substantially.

Global Recloser Market Report Scope

A recloser is an automatic electrical protection device used in power distribution systems. It detects faults such as short circuits or overloads, temporarily interrupts the power supply, and restores it after a brief interval to determine if the fault has cleared. By repeating this process a few times before permanently disconnecting the line if the issue persists, reclosers help minimize outage duration, improve system reliability, and reduce the need for manual intervention. This is particularly effective in addressing transient faults caused by environmental factors such as lightning or tree contact.

The global recloser market is segmented by interruption medium, phase, control type, voltage class, installation location, end-user, and geography. By interruption medium, the market is segmented into oil-insulated, vacuum, and gas/SF₆-free solid reclosers. By phase, the market is segmented into single-phase, three-phase, and triple-single. By control type, the market is segmented into hydraulic, electric, and microprocessor/IED-based controls. By voltage class, the market is segmented into up to 15 kV, 16–27 kV, and 28–38 kV. By installation location, the market is segmented into pole-mounted overhead, pad-mounted, and underground vault installations. By end-user, the market is segmented into utilities (transmission and distribution), industrial, and commercial & institutional sectors. The report also covers market size and forecasts for the global recloser market across major countries and regions, including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. For each segment, the market sizing and forecasts have been carried out on the basis of value (USD).

Segmentation Overview

| Oil-insulated |

| Vacuum |

| Gas/SF₆-free Solid |

| Single-Phase |

| Three-Phase |

| Triple-Single |

| Hydraulic |

| Electric |

| Microprocessor/IED |

| Up to 15 kV |

| 16 to 27 kV |

| 28 to 38 kV |

| Pole-Mounted Overhead |

| Pad-Mounted |

| Underground Vault |

| Utilities (T&D) |

| Industrial (Manufacturing, Mining, Oil & Gas) |

| Commercial and Institutional |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Interruption Medium | Oil-insulated | |

| Vacuum | ||

| Gas/SF₆-free Solid | ||

| By Phase | Single-Phase | |

| Three-Phase | ||

| Triple-Single | ||

| By Control Type | Hydraulic | |

| Electric | ||

| Microprocessor/IED | ||

| By Voltage Class | Up to 15 kV | |

| 16 to 27 kV | ||

| 28 to 38 kV | ||

| By Installation Location | Pole-Mounted Overhead | |

| Pad-Mounted | ||

| Underground Vault | ||

| By End-User | Utilities (T&D) | |

| Industrial (Manufacturing, Mining, Oil & Gas) | ||

| Commercial and Institutional | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the recloser market by 2031?

The recloser market is forecast to reach USD 1.82 billion by 2031, expanding at a 5.59% CAGR from 2026 to 2031.

How will the European SF₆ ban affect future demand?

The January 2026 EU ban on SF₆ in ≤24 kV switchgear is accelerating vacuum and dry-air retrofits, boosting replacement volumes over the next five years.

Which segment is expected to grow fastest within the recloser product mix?

Vacuum interrupter units lead growth with an anticipated 8.0% CAGR thanks to maintenance-free operation and compliance with greenhouse-gas regulations.

Why are triple-single reclosers gaining popularity?

Utilities operating rural or unbalanced feeders adopt triple-single designs to isolate only the faulted phase, reducing customer interruptions by 30-40%.

What role do data centers play in future recloser installations?

Rapid data-center expansion in North America is driving medium-voltage feeder upgrades and micro-grid redundancy, lifting commercial demand for pad-mounted reclosers.

Page last updated on: