Profenofos Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Market Size (2025) | USD 600 Million |

| Market Size (2030) | USD 769 Million |

| Growth Rate (2025 - 2030) | 5.10% CAGR |

| Fastest Growing Market | Africa |

| Largest Market | Asia Pacific |

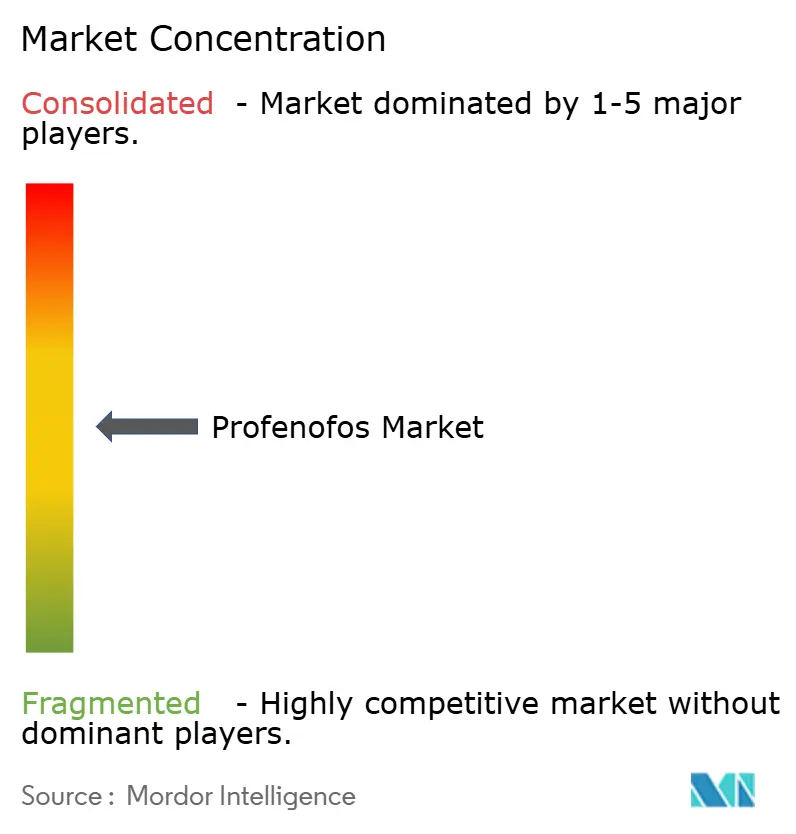

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Profenofos Market Analysis by Mordor Intelligence

The profenofos market reached USD 600 million by 2025 and is anticipated to grow to USD 769 million by 2030, registering a 5.1% CAGR over the forecast period. The profenofos market continues to expand because the active ingredient remains one of the most reliable tools against resistant cotton bollworm complexes, even as regulators tighten rules and biological alternatives mature. Rising adoption of resistance-rotation programs, investments in high-purity technical production, and steady deployment in integrated pest management (IPM) schemes underpin demand. Advances in drone-based ultra-low-volume (ULV) applications and the wider availability of cost-competitive Asian generic supplies are lowering total treatment costs for growers, thereby sustaining consumption across diverse farm sizes. Meanwhile, regulatory pressure in Europe and California is accelerating reformulation toward higher-purity grades, a shift that favors suppliers with sophisticated purification lines [1]Source: United States Environmental Protection Agency, “Pesticide Registration Review; Decisions for Several Pesticides,” federalregister.gov . Taken together, these forces signal stable volume growth and modest margin improvement for the profenofos market through 2030.

Key Report Takeaways

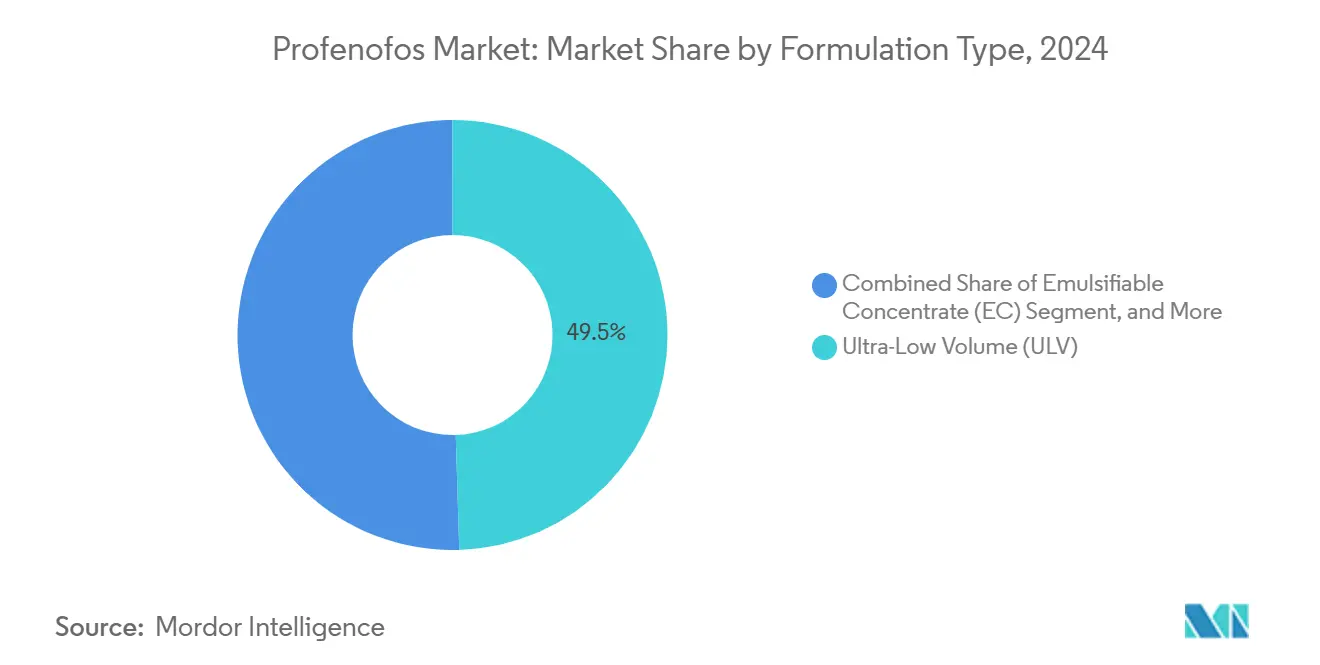

- By formulation type, emulsifiable concentrates held a 49.5% share of the profenofos market in 2024, whereas ultra-low volume (ULV) is advancing at an 8.1% CAGR through 2030.

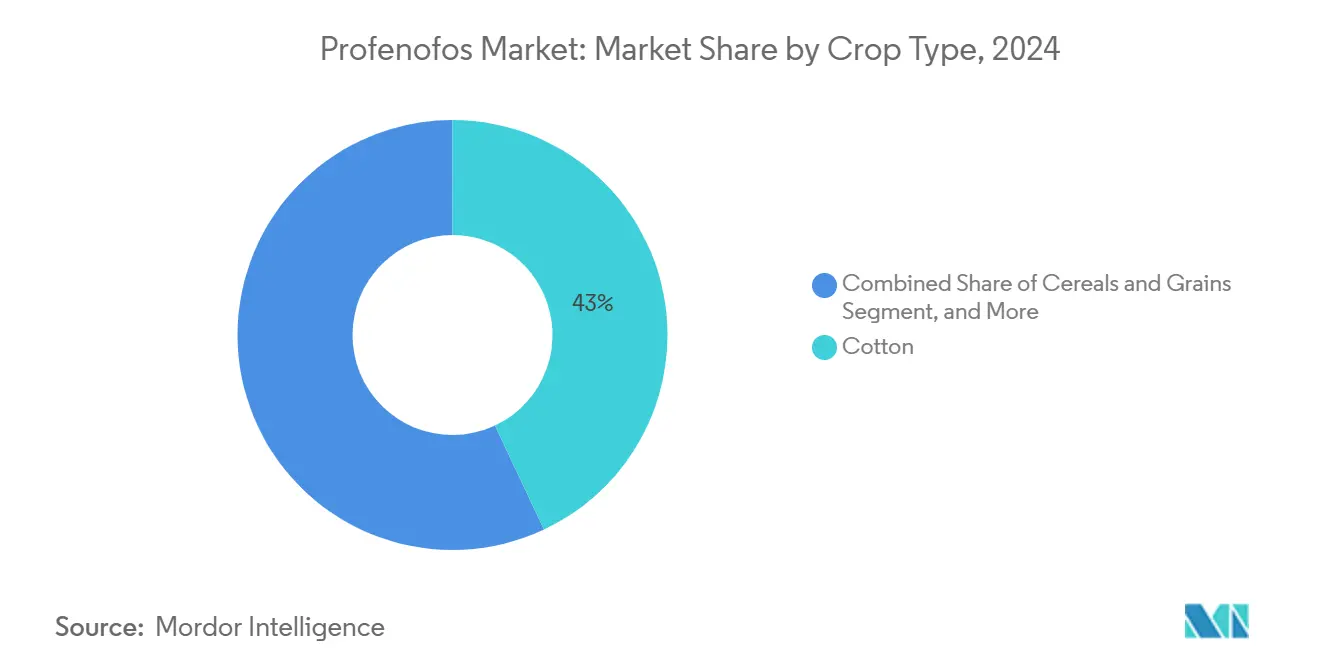

- By crop type, cotton commanded 43% of 2024 revenue, while fruits and vegetables are projected to expand at a 6.9% CAGR to 2030.

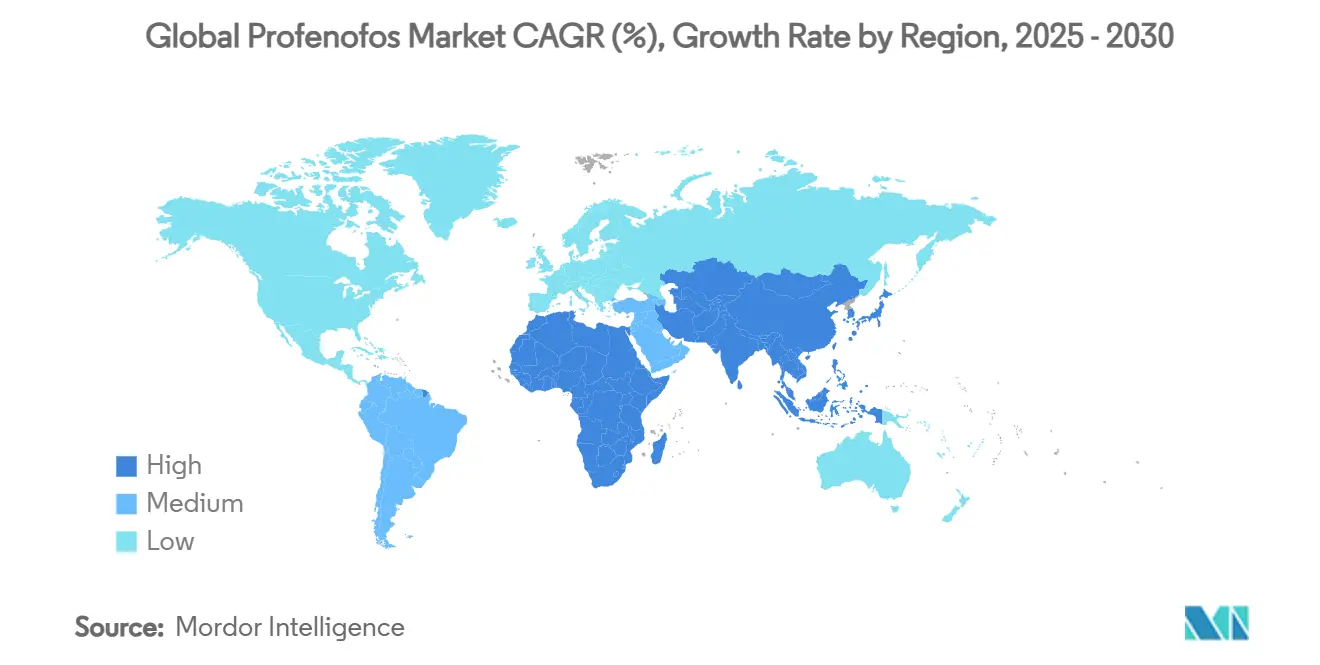

- By geography, Asia-Pacific led with a 52% of the profenofos market share in 2024, and Africa records the highest projected CAGR at 6.2% through 2030.

- By competitive landscape, Syngenta Group, UPL Ltd, Mitsui & Co., Ltd, Gharda Chemicals Ltd, and Coromandel International Ltd together accounted for around 54.3% of the profenofos market size in 2024.

Global Profenofos Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory push on cotton pest resistance management | +1.2% | Asia-Pacific, North America, and South America | Medium term (2-4 years) |

| Surge in demand for broad-spectrum insecticides in IPM programs | +0.9% | Global with strongest impact in Asia-Pacific and Africa | Short term (≤ 2 years) |

| Expansion of generic agrochemical manufacturing capacity in Asia-Pacific | +0.7% | Asia-Pacific core, spillover to Middle East and Africa | Long term (≥ 4 years) |

| Insect pressure escalation due to climate-induced pest migration | +0.6% | Global, especially subtropical regions | Long term (≥ 4 years) |

| Adoption of dual-mode organophosphate mixtures for resistance rotation | +0.4% | Asia-Pacific, South America, and Africa | Medium term (2-4 years) |

| Growth of low-cost drone spraying services in developing economies | +0.3% | Asia-Pacific, Africa, and parts of South America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory Push on Cotton Pest Resistance Management

Government mandates now require structured rotation of insecticide modes of action, positioning profenofos as a mandatory partner chemistry in numerous cotton belts [2]Source: Punjab Agricultural University, “Integrated Pest Management of Cotton in Punjab, India,” ipmworld.umn.edu. Indian guidelines introduced in 2024 oblige growers to rotate organophosphates with pyrethroids and diamides, and similar advisory frameworks are emerging in Brazil and the United States. Compliance is no longer optional as farmers who neglect rotation lose as much as 25% yield when resistance surges. These directives drive consistent baseline demand for profenofos, cushioning volumes against price swings. The certainty of repeat orders lets suppliers plan production runs more efficiently and negotiate favorable raw-material contracts. As adoption widens, regional extension agencies are distributing updated decision-support tools that embed profenofos in recommended spray schedules, further institutionalizing usage. Market players with well-documented resistance-management protocols gain a competitive advantage during registration renewals.

Surge in Demand for Broad-Spectrum Insecticides in IPM Programs

Contrary to early projections, IPM frameworks have strengthened rather than weakened the profenofos market. Field trials in New Mexico revealed that a single profenofos “knockdown” application can reduce total seasonal insecticide volume by 30% without compromising yield thresholds. Growers appreciate the insurance value of a proven broad-spectrum tool when selective biologicals falter under heavy pest pressure. Extension services now highlight profenofos as an emergency component within the IPM toolbox, which boosts its acceptance among sustainability-minded producers. Because IPM benchmarks emphasize outcome-based metrics, including economic injury levels, the dependable efficacy of profenofos often makes it the go-to rescue product. This driver has an immediate impact in Asia and Africa, where bollworm outbreaks routinely breach economic thresholds. Suppliers that bundle training on threshold-based applications report higher customer retention and cross-selling opportunities.

Expansion of Generic Agrochemical Manufacturing Capacity in Asia-Pacific

China and India are scaling technical profenofos output through backward integration into key intermediates, lowering export prices by up to 30% compared with traditional Gulf suppliers. Multiple Indian producers are investing in continuous-flow reactors and solvent-recovery systems, which shrink production cost and improve consistency. The result is a larger pool of high-purity active ingredient that meets tighter impurity rules in South America and Eastern Europe. Capacity additions align with national “Make in India” incentives and targeted export subsidies, ensuring that new plants run near nameplate volumes soon after commissioning. Asian suppliers leverage favorable exchange rates and proximity to raw materials to undercut competitors, prompting formulators worldwide to secure long-term technical supply contracts. Over the long run, this cost leadership cements Asia-Pacific’s role as the production hub for the profenofos market.

Insect Pressure Escalation Due to Climate-Induced Pest Migration

Warmer average temperatures are allowing cotton bollworm complexes to overwinter in once inhospitable locations, forcing growers in higher latitudes to add two or three insecticide sprays each season. Expanded pest ranges in northern India, southern China, and parts of Turkey have already raised demand for profenofos. Climate models predict an additional 0.5 °C rise in mean growing-season temperature by 2030 across these zones, intensifying pressure. Biological control agents often lag migrating pest fronts, creating a control gap that broad-spectrum organophosphates can immediately fill. Local cooperatives are stocking greater volumes of profenofos at planting time to ensure rapid response. This climatic driver operates over a multi-year horizon, providing a durable pull on market demand.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent EU and California residue regulations | -1.1% | Europe, North America, and export-oriented regions | Short term (≤ 2 years) |

| Rapid uptake of biopesticides in high-value crops | -0.8% | North America, Europe, and premium segments globally | Medium term (2-4 years) |

| Rising cases of counterfeit profenofos in South Asia supply chains | -0.5% | South Asia and parts of Africa | Short term (≤ 2 years) |

| Labor scarcity driving switch to systemic seed treatments | -0.4% | Global and especially developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent EU and California Residue Regulations

The European Food Safety Authority cut profenofos maximum residue limits (MRLs) in citrus fruit to 0.01 mg/kg in 2024, effectively barring usage for growers exporting to the European Union [3]Source: United States Environmental Protection Agency, “Cyclaniliprole; Pesticide Tolerance,” federalregister.gov. California’s Department of Pesticide Regulation is pursuing similar limits for leafy greens. Because many developing-nation farmers rely on export premiums to fund crop inputs, these tighter standards force a pivot away from profenofos or require expensive residue-degradation studies. Compliance costs for residue testing rose 35% in Morocco’s citrus sector in 2024, eroding price competitiveness. Distributors in Kenya have reported double-digit declines in orders for profenofos destined for export crops, with volumes shifting to shorter pre-harvest interval chemistries.

Rapid Uptake of Biopesticides in High-Value Crops

Premium fruit and vegetable producers gravitate to biopesticides to satisfy retailer sustainability audits. The economics are changing rapidly, wherein fermentation yields have improved, pushing unit costs down 20% since 2022. Multinationals such as Corteva Agriscience have publicly targeted USD 2 billion in biological revenue by 2035, giving them an incentive to redirect R&D budgets away from organophosphates. As shelf-stable microbial formulations hit the market, they displace profenofos in greenhouse and export niches where zero-residue labels command higher prices. While market displacement is still modest in broad-acre cotton, the effect on high-value crops is meaningful enough to trim the overall profenofos market CAGR by 0.8 percentage points.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Formulation Type: ULV Advances on Precision Agriculture Tailwinds

Emulsifiable concentrates still account for 49.5% of 2024 sales, owing to their easy tank-mix compatibility and straightforward manufacturing. Yet the profenofos market is witnessing the rapid rise of ultra-low volume (ULV) formulations, which are expanding at an 8.1% CAGR. ULV’s appeal stems from lower carrier volume, reduced operator exposure, and compatibility with drone delivery systems. Several Asia-Pacific region's contract formulators have licensed encapsulation know-how to extend field persistence in arid zones, where high evaporation rates previously limited ULV uptake.

Granular products remain relevant for soil-dwelling pests, although their share is stable rather than growing. The others segment, including microencapsulated suspension concentrates, is a hotbed of innovation, capturing interest from organic-transition farms that need drift-reduction profiles. Regulatory agencies now scrutinize co-solvent selection for volatile organic compound (VOC) compliance, nudging formulators toward renewable solvent systems. Consequently, R&D spending on formulation science has risen to 6% of sales among leading players, signaling that the next competitive frontier will hinge on delivery efficiency rather than solely active-ingredient cost.

By Crop Type: Cotton Core Meets Diversification Trend

Cotton absorbed 43% of the profenofos market size in 2024, cementing its status as the bedrock of the profenofos market. The profenofos market size for cotton is set to grow steadily, but the growth rate lags behind emerging horticulture demand. Fruits and vegetables represent the fastest-growing use case at a 6.9% CAGR through 2030, owing to expanding greenhouse acreage in China, Egypt, and Mexico. These crops require broad-spectrum rescue treatments when biologicals fall short, and profenofos fits the bill.

Cereals and grains, a historically minor outlet, are plateauing amid competition from systemics with longer residuals. Plantation crops such as cocoa and coffee form part of the other crops category, where integrated pest management guidelines increasingly include profenofos rotation to combat cross-resistant beetle populations. For suppliers, crop-specific formulation and tailored label expansions offer an avenue to diversify revenue and mitigate over-reliance on cotton cycles.

Geography Analysis

Asia-Pacific continues to command a 52% share of the profenofos market in 2024, with China and India functioning as both consumption and production anchors. Export-driven Indian formulators shipped USD 4.1 billion worth of insecticides in 2024, and profenofos ranked among their top three active ingredients. The region’s regulatory stance remains relatively supportive. For instance, Vietnam’s 2025 national crop-protection plan still endorses organophosphates within IPM frameworks. Domestic cotton acreage in India is projected to inch upward as hybrid seed adoption boosts yields, reinforcing baseline demand.

Africa is the quickest-growing region, growing at a 6.2% CAGR, propelled by West African cotton schemes supported by multilateral finance. Governments in Benin and Burkina Faso have earmarked subsidized input packages that include profenofos for bollworm management. Parallel capacity-building programs are improving safe-use training, which builds brand trust. Infrastructure gaps and counterfeit infiltration remain hurdles, yet donor-funded traceability pilots are showing early success in Kenya and Ghana.

North America and Europe represent mature yet innovative strongholds where regulatory stringency reshapes usage patterns rather than eliminating demand. California’s pending MRL revisions push growers toward higher-purity input, opening a niche for premium technical suppliers. Eastern Europe’s expanding cotton and sunflower cultivation still relies on organophosphates under carefully managed spray regimes, partially offsetting Western Europe’s decline. South America maintains steady uptake, aided by Brazil’s large-scale cotton estates that value profenofos for its fast knockdown during peak bollworm flights. Meanwhile, Middle Eastern countries are exploring localized formulation facilities to support food-security drives, presenting a moderate growth pocket.

Competitive Landscape

The profenofos market exhibits moderate concentration as the top five players command significant market share, while a long tail of regional formulators fills country-specific demand niches. Syngenta Group leads through its Curacron brand and an integrated distribution network that reaches 90 countries. UPL Ltd follows, leveraging strong footholds in India and sub-Saharan Africa with Tafaban. Gharda Chemicals Ltd and Coromandel International Ltd round out the top five, each focusing on differentiated formulations or strategic supply agreements with drone-service providers.

Competitive advantage is shifting from sheer capacity to regulatory agility and stewardship services. For instance, Mitsui’s creation of Certis Belchim in 2024 merges formulation expertise with biologicals, positioning the company to offer hybrid pest-control programs. Regional players in Bangladesh and Egypt compete on price and localized after-sales support, often bundling credit terms for smallholders. Mergers and acquisitions in 2024 centered on backward integration into key intermediaries, bolstering supply resilience. Strategic collaborations with drone analytics firms also emerged, giving early movers data-driven marketing insights.

R&D pipelines among leading firms prioritize drift-reduced emulsifiable concentrates (ECs) and encapsulated ULVs that pass forthcoming VOC rules in Europe. Investment focus is further tilting toward digital label-compliance tools that flag resistance management gaps for growers. The industry sees clear white-space in traceability technologies that authenticate genuine products, QR-based solutions anticipated to become standard on containers above 1 liter. As competitive edges hinge more on service overlays than on active-ingredient novelty, margin structure is likely to remain stable despite commoditization pressure.

Profenofos Industry Leaders

Mitsui & Co., Ltd.(Bharat Certis AgriScience Ltd.)

Gharda Chemicals Ltd.

Coromandel International Ltd.

Syngenta Group

UPL Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2024: Hailir Pesticides and Chemicals Group completed and commissioned its Phase II pilot plant facility at its Qingdao subsidiary, which started in 2022. The new phase increases the company's production and formulation capacity for multiple active ingredients, including organophosphate technicals such as profenofos, a key component of Hailir's insecticide portfolio. The facility supports large-scale manufacturing, quality control, and commercialization of combination products, including profenofos + pyrethroid blends used in cotton and vegetable protection.

- September 2023: Hailir Pesticides and Chemicals Group registered multiple profenofos-based combination formulations in China, including Profenofos 15% + Methomyl 10% EC and Cypermethrin 40% + Profenofos 400 g/L EC. The registrations expanded the company's insecticide portfolio for cotton, vegetables, and oilseed crops. These formulations enhanced Hailir's position in domestic and export markets, particularly in Asia and Africa, where the mixtures are in high demand for controlling resistant pests.

- February 2023: Heranba Industries Ltd. is expanding its technical and formulation manufacturing capacity at its Saykha and Sarigam facilities in Gujarat, India. The expansion includes additional production lines for organophosphate technicals and intermediates, including profenofos. This expansion strengthens the supply availability and competitiveness to meet the increasing demand in cotton, vegetables, and other crop segments.

Global Profenofos Market Report Scope

| Emulsifiable Concentrate (EC) |

| Granules (GR) |

| Ultra-Low Volume (ULV) |

| Others |

| Cotton |

| Cereals and Grains |

| Fruits and Vegetables |

| Other Crops |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Thailand | |

| Vietnam | |

| Philippines | |

| Indonesia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Formulation Type | Emulsifiable Concentrate (EC) | |

| Granules (GR) | ||

| Ultra-Low Volume (ULV) | ||

| Others | ||

| By Crop Type | Cotton | |

| Cereals and Grains | ||

| Fruits and Vegetables | ||

| Other Crops | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Thailand | ||

| Vietnam | ||

| Philippines | ||

| Indonesia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size of the profenofos market?

The profenofos market size is USD 600 million in 2025.

Which region is the largest consumer of profenofos?

Asia-Pacific accounts for 52% of global consumption, anchored by extensive cotton cultivation and robust manufacturing in China and India.

What is the fastest-growing formulation segment?

Ultra-low-volume formulations are expanding at an 8.1% CAGR due to compatibility with drone spraying and reduced water requirements.

How significant is cotton in profenofos usage?

Cotton represents 43% of total profenofos demand, making it the single largest crop segment for this insecticide.

Page last updated on: