Brazil Biostimulants Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

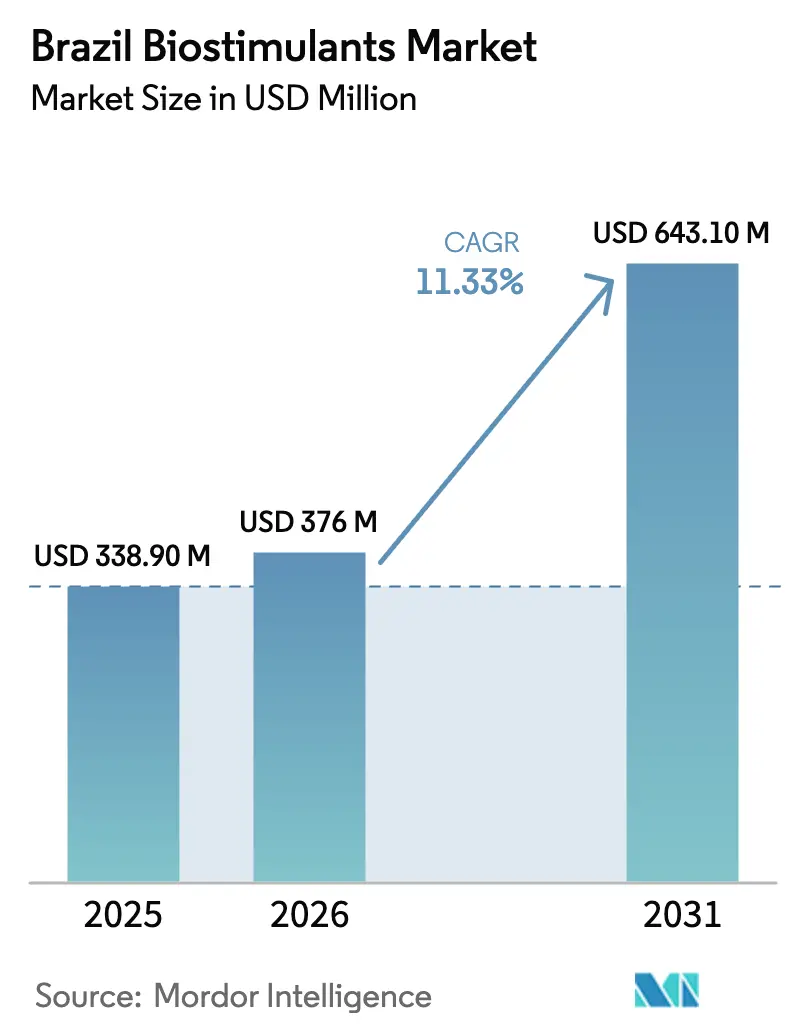

| Base Year Market Size (2025) | USD 338.90 Million |

| Market Size (2026) | USD 376 Million |

| Market Size (2031) | USD 643.10 Million |

| Growth Rate (2026 - 2031) | 11.33% CAGR |

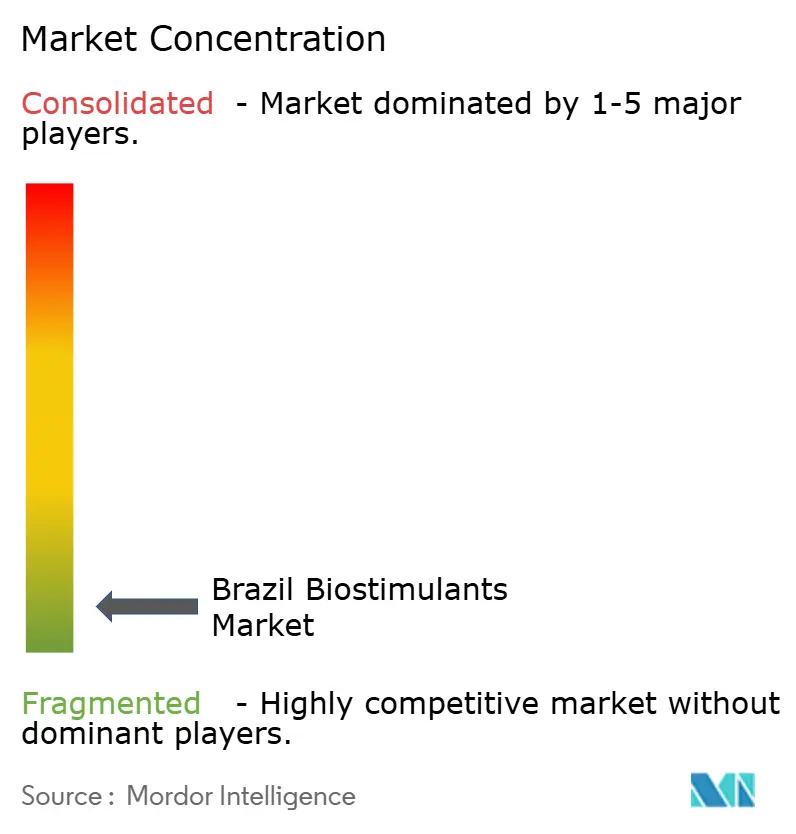

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Biostimulants Market Analysis by Mordor Intelligence

The Brazil biostimulants market size is projected to grow from USD 338.9 million in 2025 to USD 376.0 million in 2026, reaching USD 643.1 million by 2031, with a CAGR of 11.33% during 2026-2031. Robust credit incentives, streamlined bio-input regulation, and carbon-credit pilots are moving biological inputs from niche status to core nutrient-management tools, which is lifting demand across soybeans, sugarcane, coffee, and citrus. The federal Reference Specification pathway now cuts product registration to roughly one year and has increased new-product launches, while RenovAgro’s discounted rural credit is reducing the cost premium that historically slowed adoption. Growers are also integrating biostimulants into variable-rate maps generated by Climate FieldView and similar platforms, linking biological prescriptions to real-time soil variability. Seaweed extracts continue to dominate because of proven drought-stress relief in sugarcane and micronutrient mobilization in acidic Cerrado soils. At the same time, amino acids are gaining speed as export-oriented coffee and citrus growers seek input portfolios that align with Ecocert and Organic Products Development Institute certification rules.

Key Report Takeaways

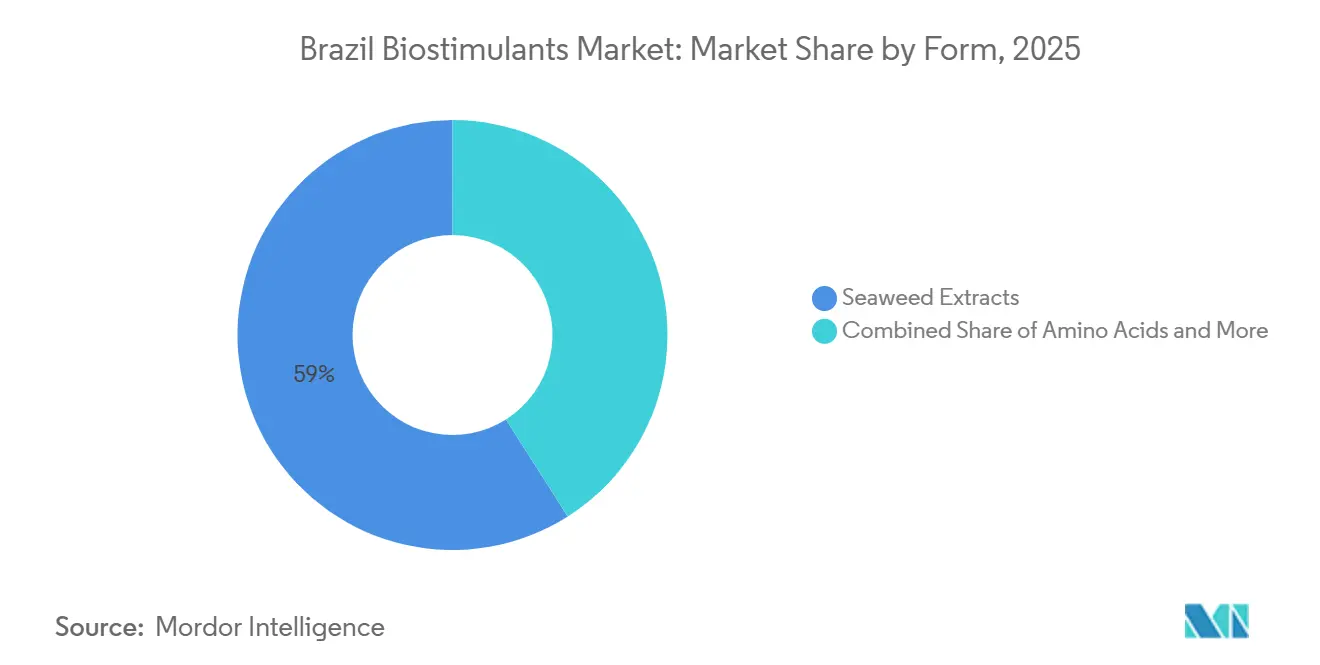

- By form, seaweed extracts are projected to account for 59.0% of the Brazil biostimulants market share in 2025, while amino acids are anticipated to grow at a CAGR of 14.0% from 2026-2031.

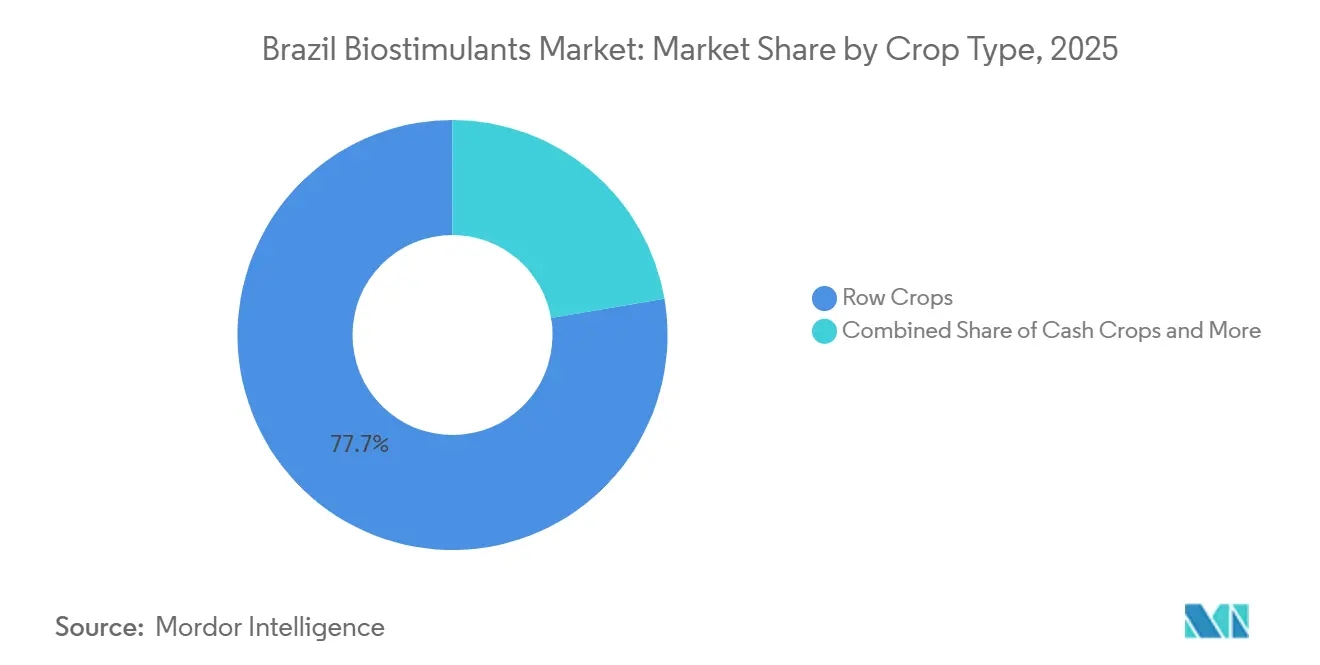

- By crop type, row crops are anticipated to represent 77.7% of the Brazil biostimulants market size in 2025, with a projected CAGR of 11.4% from 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Brazil Biostimulants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government subsidies for sustainable farming | +2.1% | Nationwide, strongest in Mato Grosso, Paraná, and Rio Grande do Sul | Medium term (2-4 years) |

| Rising demand for certified export horticulture | +2.4% | São Paulo citrus belt, Minas Gerais coffee zone, and southern berry areas | Short term (≤ 2 years) |

| Soil degradation driving biological inputs | +1.9% | Mato Grosso, Goiás, Bahia, Tocantins | Long term (≥ 4 years) |

| Carbon-credit pilots rewarding biostimulants | +1.2% | Paraná and Rio Grande do Sul, São Paulo and Mato Grosso | Long term (≥ 4 years) |

| Integration with agronomy platforms offering tailored biostimulant recommendations | +1.3% | Row-crop heartland where precision adoption tops 30% | Medium term (2-4 years) |

| ABC+ transition incentives linking low-carbon financing | +1.5% | States meeting Rural Environmental Registry enrollment targets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government Subsidies for Sustainable Farming

RenovAgro, which succeeded the Low Carbon Agriculture plan, allocated BRL 364 billion (USD 73 billion) in subsidized credit for the 2023-2024 crop year[1]Source: BNDES, “Renovagro – Programa de Financiamento a Sistemas de Produção Agropecuária Sustentável,” BNDES.gov.br. Government initiatives are enhancing access to affordable credit for biological inputs by offering subsidized interest rates, thereby shortening farmers' repayment periods and promoting the adoption of biostimulants. The Agro Brasil + Sustentável platform, introduced in December 2024, seeks to modernize agriculture by streamlining credit analysis for sustainable producers and providing interest rate reductions of up to 0.5%. Additionally, state-level incentives linked to soil health verification help lower initial investment barriers. Sustainability programs further link financing to improvements in nutrient management, encouraging the use of efficient biological and amino-acid-based alternatives rather than conventional nitrogen sources. These efforts are contributing to sustained growth in Brazil's biostimulants market throughout the decade.

Rising Demand for Certified Export Horticulture

European Union Farm-to-Fork targets aim for a 50% cut in chemical pesticide use by 2030, pushing Brazilian citrus and coffee exporters toward Organic Products Development Institute and Ecocert approval lists[2]Source: Ecocert Brasil, “Organic Agriculture Brazil (Lei 10.831/2003) Certification,” Ecocert.com. Biostimulants help lower residue readings while also boosting cup scores and Brix values that influence premium brackets. São Paulo orange-juice processors have begun requiring supplier declarations that at least one certified biostimulant is used per orchard cycle. Organic coffee estates are paying substantial premiums for protein hydrolysate inputs that comply with international organic standards, thereby supporting high-value market segments. As certification compliance increases overall landed costs, growers are increasingly preferring inputs that streamline audit and documentation processes. Consequently, export-oriented horticulture has become one of the most active sectors in Brazil's agricultural market, adopting biostimulants early.

Soil Degradation Driving Biological Inputs

Cerrado soils exhibit low pH levels and high aluminum saturation, which restricts the availability of phosphorus and trace metals. Continuous soybean-corn double cropping has reduced soil organic matter, decreased cation exchange capacity, and increased nutrient leaching. The application of humic and fulvic acids helps chelate micronutrients and release phosphorus that would otherwise become unavailable in these acidic soils. This enables growers to reduce synthetic fertilizer usage without compromising yields. Experiments have demonstrated soybean yield improvements when biostimulants are incorporated, enhancing long-term grower confidence. This focus on soil health strengthens the resilience of the Brazil biostimulants market against fluctuations in commodity prices.

Carbon-Credit Pilots Rewarding Biostimulants

In Paraná and Rio Grande do Sul, growers are compensated for verified CO₂-equivalent sequestered through practices such as biostimulant application. Early participants reported revenue generation that offsets the cost of premium products. Federal lawmakers are preparing a national carbon-market framework, anticipated to launch in the coming years, with the potential to scale across millions of hectares. However, verification fees and soil-testing requirements pose challenges for smallholders, while larger enterprises are already securing credits through offtake agreements with multinational food companies. As a result, monetized soil carbon introduces a new profit incentive within the Brazil biostimulants market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost competitiveness challenges limit mass-market penetration | −1.8% | Smallholder regions nationwide | Short term (≤ 2 years) |

| Regulatory approval delays for novel ingredients | −1.3% | National | Medium term (2-4 years) |

| Scarcity of local seaweed feedstock inflates raw-material costs | −0.9% | National | Medium term (2-4 years) |

| Smallholder fragmentation hampers robust efficacy data | −1.1% | South and Northeast | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cost Competitiveness Challenges Limit Mass-Market Penetration

Seaweed and amino acid concentrates are regularly price 15-25% above equivalent units of N-P-K, and most financing programs require Rural Environmental Registry enrollment. Biostimulant products are significantly more expensive than conventional foliar fertilizers, prompting growers to assess them against strict return-on-investment criteria. Average subsistence plots of 20 hectares or less often lack collateral for bank loans, so input decisions revolve around immediate liquidity. In the semiarid Northeast, adoption below 5% underscores price sensitivity, even when field trials show yield gains. The availability of low-cost generic humic-acid products, often sold at substantial discounts, fragments demand and exerts pressure on the margins of multinational suppliers. These economic factors collectively limit biostimulant adoption among cost-conscious growers.

Regulatory Approval Delays for Novel Ingredients

Federal Law 15,070 introduced a fast-track process. However, the Ministry of Agriculture, Livestock, and Food Supply still processes over 100 filings annually with limited laboratory capacity. Multicomponent blends require multi-site residue testing, often spanning more than two seasons, tying up working capital for domestic start-ups. The regulatory approval process for new biostimulant active substances has become increasingly time-consuming, with review periods now surpassing standard product development timelines. A growing backlog of applications further impedes progress, while high registration fees disproportionately affect smaller companies, shifting much of the innovation pipeline toward larger multinational firms. These extended timelines continue to limit the introduction of new technologies in the Brazilian biostimulants market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Seaweed Extracts Lead, Amino Acids Accelerate

The seaweed extracts segment accounted for 59.0% of the Brazil biostimulants market share in 2025, while the fastest-growing segment is amino acids, with a 14.0% CAGR from 2026-2031. Seaweed extracts are growing largely because they mitigate drought stress in sugarcane and mobilize nutrients bound in acidic Cerrado soils[3]Source: Brazilian Agricultural Research Corporation, “Soil Health BR Platform: Resilient Soils for Sustainable Agricultural Systems,” Embrapa.br. Brazil's extensive 8,000-kilometer coastline, characterized by coral reefs and highly diversified ecosystems, provides significant potential for seaweed cultivation and extraction, ensuring a steady supply of raw materials for this segment. Humic and fulvic acids support a phosphorus-unlocking mechanism that reduces the cost of mineral fertilizers in degraded soils.

Investors are funding local fermentation capacity, which should narrow landed-cost gaps versus Asian imports and widen gross margins. Seaweed’s leadership, therefore, faces impending pressure from locally produced amino acids and humic alternatives that bypass marine-biomass logistics risks. Meanwhile, protein hydrolysates and other smaller categories are gaining traction as domestic manufacturers convert fish and soybean byproducts into liquid formulations, thereby reducing reliance on foreign exchange. Continuous formulation innovation, supported by the streamlined Reference Specification pathway, is likely to redistribute Brazil biostimulants market share toward multifaceted products that blend more than one bio-active class.

By Crop Type: Row Crops Dominate, Horticulture Gains Pace

Row crops accounted for 77.7% of the Brazil biostimulants market in 2025 and were also the fastest-growing segment, with a CAGR of 11.4% from 2026-2031. With millions of hectares dedicated to soybeans, corn, and cotton, even a modest yield increase translates to a significant boost in absolute tonnage. The dominance of this segment is primarily due to the growing adoption of biostimulants as part of integrated crop management practices, serving as an alternative to traditional chemical fertilizers. Seaweed extracts are the most commonly used biostimulants in row crops, with studies indicating significant improvements in nutrient absorption and yield increases of up to 50% in soybean cultivation. Additionally, the segment's growth is bolstered by the Brazilian government's efforts to promote sustainable farming practices and organic agriculture.

Horticulture is experiencing growth as exporters adopt residue-compliant inputs to secure 20-40% premiums in European and North American markets. Producers of mango, melon, and grapes in Rio Grande do Norte and Bahia incorporate seaweed and amino-acid formulations to improve fruit color and shelf life, thereby expanding their premium market acceptance. Cash crops such as coffee and sugarcane utilize humic-acid products to enhance root vigor during off-season frosts and droughts. These diversified demand sources collectively strengthen the medium-term growth prospects for the biostimulants market in Brazil.

Geography Analysis

The Center-West region, led by Mato Grosso, Goiás, and Mato Grosso do Sul, held a significant share of Brazil's biostimulants market in 2025. Large, mechanized farms and precision tools on soybean plantations drive efficient application of biological inputs. Climate variability and thin topsoil in Cerrado fields boost demand for drought-mitigating seaweed extracts. Agricultural credit uptake further supports growth.

The Southeast region, anchored by São Paulo and Minas Gerais, contributed significantly to sales. Sugar, citrus, and coffee producers use certified inputs to comply with export residue regulations. Regional universities provide agronomy consultants for integrated input regimens. Proximity to ports reduces logistics costs for imported seaweed, while awareness of carbon credits supports growth.

The Southern states of Paraná, Rio Grande do Sul, and Santa Catarina saw strong demand, driven by second-crop corn and wheat rotations benefiting from humic acids and microbial blends. Carbon-credit initiatives shorten payback periods, and cooperative networks lower costs for small and mid-scale farms. The Northeast and North regions contribute minimally due to small plots, limited services, and low credit penetration. However, they offer long-term growth potential as policies and market conditions improve.

Competitive Landscape

The top five suppliers captured a minimal share of market revenue in 2025, with the market being fragmented. The key players are Vittia S.A., Trade Corporation International S.A.U., Atlántica Agrícola S.A., Humic Growth Solutions, Inc., Valagro S.p.A., and Vittia S.A. is utilizing its manufacturing facilities in Brazil to shorten lead times and establish itself as a formulation partner for distributors of sugarcane and coffee inputs. Trade Corporation International S.A.U. and Atlántica Agrícola S.A. are also prominent players, supported by product portfolios approved for export-focused horticulture. Humic Growth Solutions, Inc. and Valagro S.p.A. round out the top five, offering fulvic and humic acids aimed at addressing phosphorus-fixation issues in Cerrado clays.

BASF SE, Bayer AG, Corteva Agriscience, and UPL Ltd are expanding their biological product divisions through capital investments and collaborative trials with the Brazilian Agricultural Research Corporation. These initiatives focus on developing single-tank solutions that integrate biostimulants with crop-protection actives. Additionally, digital agronomy partnerships are gaining traction. Climate FieldView incorporates dose calculators from various suppliers, while Aegro integrates product-advice tools that provide in-season recommendations for farms.

Growth opportunities in the market include smallholder-friendly packaging sizes, carbon-credit-verified formulations, and multi-action products that combine plant-growth stimulation with pest-resistance mechanisms. However, proving product efficacy across Brazil's diverse micro-climates remains a significant challenge. To address this, leading companies are investing in shared trial networks to accelerate data collection. Additionally, as regulatory bodies expand laboratory capacity, approval backlogs are anticipated to decrease, enabling faster portfolio turnover and intensifying competition. With the top players holding minimal share, the Brazil biostimulants market remains fragmented, where differentiated agronomic support is as critical as logistical scale.

Brazil Biostimulants Industry Leaders

Trade Corporation International S.A.U.

Humic Growth Solutions Inc.

Valagro S.p.A.

Vittia S.A.

Atlántica Agrícola S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Spanish agribusiness Sustainable Agro Solutions (SAS), supported by Stirling Square Capital Partners, has acquired a majority stake in Aqua do Brasil. This acquisition enhances SAS's presence in South America, with a focus on botanical-based fertilizers, biostimulants, and soil conditioners, reinforcing its role in sustainable plant nutrition.

- March 2025: Koppert B.V. has transferred the management of its biostimulant and fertilizer portfolio, including Veni, Vidi, Vici, and Panoramix, to REKA Group B.V. This move allows Koppert B.V. to concentrate on biological crop protection. REKA Group B.V. will now handle the production, logistics, research and development, regulatory affairs, sales, and marketing of these products.

- October 2024: FMC Corporation partnered with Ballagro to co-develop fungi-based biosolutions for glyphosate-resistant weed complexes prevalent across Brazil’s soy belt. The partnership combines FMC's expertise in microbial solutions with Ballagro's specialization in fungi-based solutions to enhance the biosolutions market in Brazil.

Brazil Biostimulants Market Report Scope

Biostimulants are substances or microorganisms applied to plants, seeds, or soil to enhance natural processes, improving nutrient uptake, stress tolerance, and crop quality. Unlike fertilizers, they influence the plant's physiological processes rather than supplying direct nutrients. These products are commonly derived from natural sources such as seaweed extracts, humic acids, or beneficial microbes. The Brazil Biostimulants Market Report is Segmented by Form (Amino Acids, Fulvic Acid, Humic Acid, Protein Hydrolysates, Seaweed Extracts, and Other Biostimulants), and by Crop Type (Cash Crops, Horticultural Crops, and Row Crops). The Market Forecasts are Provided in Terms of Value (USD) and Volume (metric Tons).

| Amino Acids |

| Fulvic Acid |

| Humic Acid |

| Protein Hydrolysates |

| Seaweed Extracts |

| Other Biostimulants |

| Cash Crops |

| Horticultural Crops |

| Row Crops |

| By Form | Amino Acids |

| Fulvic Acid | |

| Humic Acid | |

| Protein Hydrolysates | |

| Seaweed Extracts | |

| Other Biostimulants | |

| By Crop Type | Cash Crops |

| Horticultural Crops | |

| Row Crops |

Market Definition

- AVERAGE DOSAGE RATE - The average application rate is the average volume of biostimulants applied per hectare of farmland in the respective region/country.

- CROP TYPE - Crop type includes Row crops (Cereals, Pulses, Oilseeds), Horticultural Crops (Fruits and vegetables) and Cash Crops (Plantation Crops, Fibre Crops and Other Industrial Crops)

- FUNCTION - The Crop Protection function of agirucultural biological include products that prevent or control various biotic and abiotic stress.

- TYPE - Biostimulants boost crop growth and yield by preventing or controlling various abiotic stresses.

| Keyword | Definition |

|---|---|

| Cash Crops | Cash crops are non-consumable crops sold as a whole or part of the crop to manufacture end-products to make a profit. |

| Integrated Pest Management (IPM) | IPM is an environment-friendly and sustainable approach to control pests in various crops. It involves a combination of methods, including biological controls, cultural practices, and selective use of pesticides. |

| Bacterial biocontrol agents | Bacteria used to control pests and diseases in crops. They work by producing toxins harmful to the target pests or competing with them for nutrients and space in the growing environment. Some examples of commonly used bacterial biocontrol agents include Bacillus thuringiensis (Bt), Pseudomonas fluorescens, and Streptomyces spp. |

| Plant Protection Product (PPP) | A plant protection product is a formulation applied to crops to protect from pests, such as weeds, diseases, or insects. They contain one or more active substances with other co-formulants such as solvents, carriers, inert material, wetting agents or adjuvants formulated to give optimum product efficacy. |

| Pathogen | A pathogen is an organism causing disease to its host, with the severity of the disease symptoms. |

| Parasitoids | Parasitoids are insects that lay their eggs on or within the host insect, with their larvae feeding on the host insect. In agriculture, parasitoids can be used as a form of biological pest control, as they help to control pest damage to crops and decrease the need for chemical pesticides. |

| Entomopathogenic Nematodes (EPN) | Entomopathogenic nematodes are parasitic roundworms that infect and kill pests by releasing bacteria from their gut. Entomopathogenic nematodes are a form of biocontrol agents used in agriculture. |

| Vesicular-arbuscular mycorrhiza (VAM) | VAM fungi are mycorrhizal species of fungus. They live in the roots of different higher-order plants. They develop a symbiotic relationship with the plants in the roots of these plants. |

| Fungal biocontrol agents | Fungal biocontrol agents are the beneficial fungi that control plant pests and diseases. They are an alternative to chemical pesticides. They infect and kill the pests or compete with pathogenic fungi for nutrients and space. |

| Biofertilizers | Biofertilizers contain beneficial microorganisms that enhance soil fertility and promote plant growth. |

| Biopesticides | Biopesticides are natural/bio-based compounds used to manage agricultural pests using specific biological effects. |

| Predators | Predators in agriculture are the organisms that feed on pests and help control pest damage to the crops. Some common predator species used in agriculture include ladybugs, lacewings, and predatory mites. |

| Biocontrol agents | Biocontrol agents are living organisms used to control pests and diseases in agriculture. They are alternatives to chemical pesticides and are known for their lesser impact on the environment and human health. |

| Organic Fertilizers | Organic fertilizer is composed of animal or vegetable matter used alone or in combination with one or more non-synthetically derived elements or compounds used for soil fertility and plant growth. |

| Protein hydrolysates (PHs) | Protein hydrolysate-based biostimulants contain free amino acids, oligopeptides, and polypeptides produced by enzymatic or chemical hydrolysis of proteins, primarily from vegetal or animal sources. |

| Biostimulants/Plant Growth Regulators (PGR) | Biostimulants/Plant Growth Regulators (PGR) are substances derived from natural resources to enhance plant growth and health by stimulating plant processes (metabolism). |

| Soil Amendments | Soil Amendments are substances applied to soil that improve soil health, such as soil fertility and soil structure. |

| Seaweed Extract | Seaweed extracts are rich in micro and macronutrients, proteins, polysaccharides, polyphenols, phytohormones, and osmolytes. These substances boost seed germination and crop establishment, total plant growth and productivity. |

| Compounds related to biocontrol and/or promoting growth (CRBPG) | Compounds related to biocontrol or promoting growth (CRBPG) are the ability of a bacteria to produce compounds for phytopathogen biocontrol and plant growth promotion. |

| Symbiotic Nitrogen-Fixing Bacteria | Symbiotic nitrogen-fixing bacteria such as Rhizobium obtain food and shelter from the host, and in return, they help by providing fixed nitrogen to the plants. |

| Nitrogen Fixation | Nitrogen fixation is a chemical process in soil which converts molecular nitrogen into ammonia or related nitrogenous compounds. |

| ARS (Agricultural Research Service) | ARS is the U.S. Department of Agriculture's chief scientific in-house research agency. It aims to find solutions to agricultural problems faced by the farmers in the country. |

| Phytosanitary Regulations | Phytosanitary regulations imposed by the respective government bodies check or prohibit the importation and marketing of certain insects, plant species, or products of these plants to prevent the introduction or spread of new plant pests or pathogens. |

| Ectomycorrhizae (ECM) | Ectomycorrhiza (ECM) is a symbiotic interaction of fungi with the feeder roots of higher plants in which both the plant and the fungi benefit through the association for survival. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms.