Interventional Neurology Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

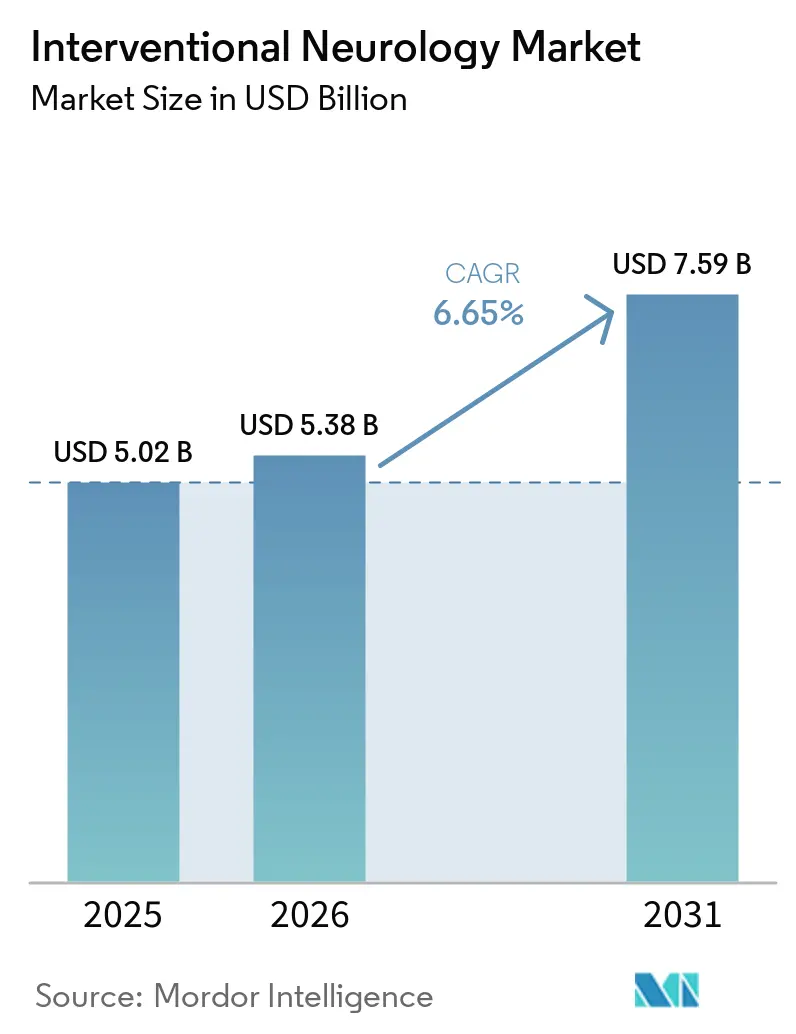

| Market Size (2026) | USD 5.38 Billion |

| Market Size (2031) | USD 7.59 Billion |

| Growth Rate (2026 - 2031) | 6.65% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Interventional Neurology Market Analysis by Mordor Intelligence

The Interventional Neurology Market size is expected to increase from USD 5.02 billion in 2025 to USD 5.38 billion in 2026 and reach USD 7.59 billion by 2031, growing at a CAGR of 6.65% over 2026-2031.

Aging populations in every major region, rapid mechanical thrombectomy uptake, and hospital network consolidation are combining to lift device utilization rates, especially at certified comprehensive stroke centers. AI-guided triage software is shortening door-to-puncture times, which raises procedure volumes and underpins the strong outlook for imaging platforms. Meanwhile, health-system mergers in North America and Western Europe are clustering capital budgets, pushing sophisticated biplane angiography and robotic navigation systems to the top of replacement cycles. Suppliers that pair treatment devices with cloud-based decision-support modules are best positioned to capture enterprise-level contracts and lock in recurring software revenue.

Key Report Takeaways

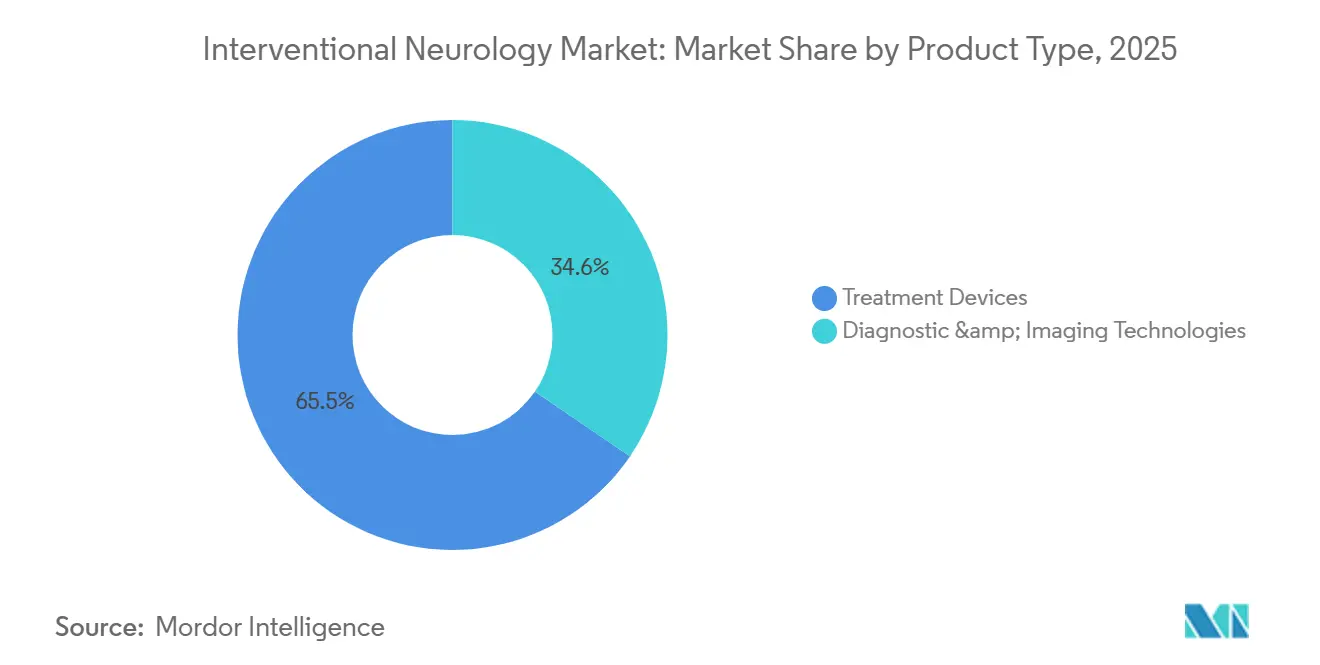

- By product type, treatment devices led with 65.45% of the interventional neurology diagnosis and treatment market share in 2025, while imaging platforms will advance at a 7.56% CAGR through 2031.

- By therapeutic application, ischemic stroke dominated at 42.12% of the interventional neurology diagnosis and treatment market size in 2025, whereas hemorrhagic stroke interventions are poised to expand at 7.60% annually to 2031.

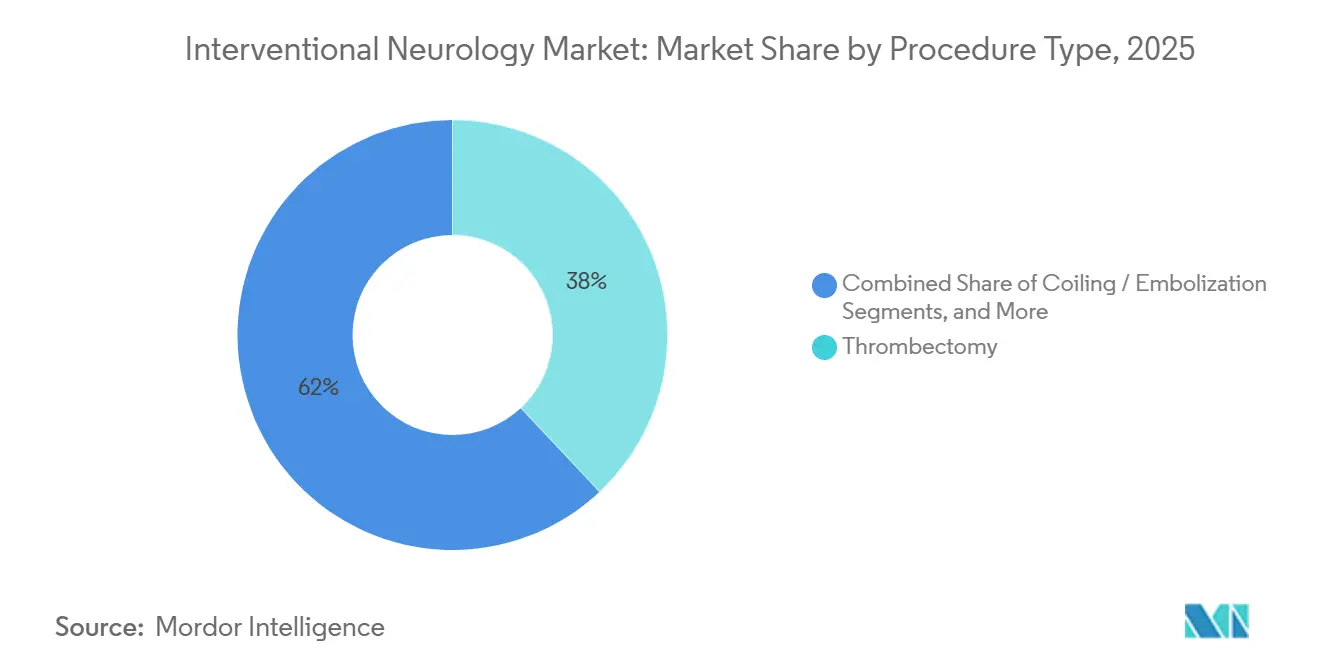

- By procedure type, thrombectomy accounted for 38.00% of 2025 revenue and is projected to register a 7.90% CAGR to 2031.

- By end-user, hospitals and academic medical centers held 65.45% of 2025 sales, yet specialty stroke centers represented the fastest trajectory at 8.20% to 2031.

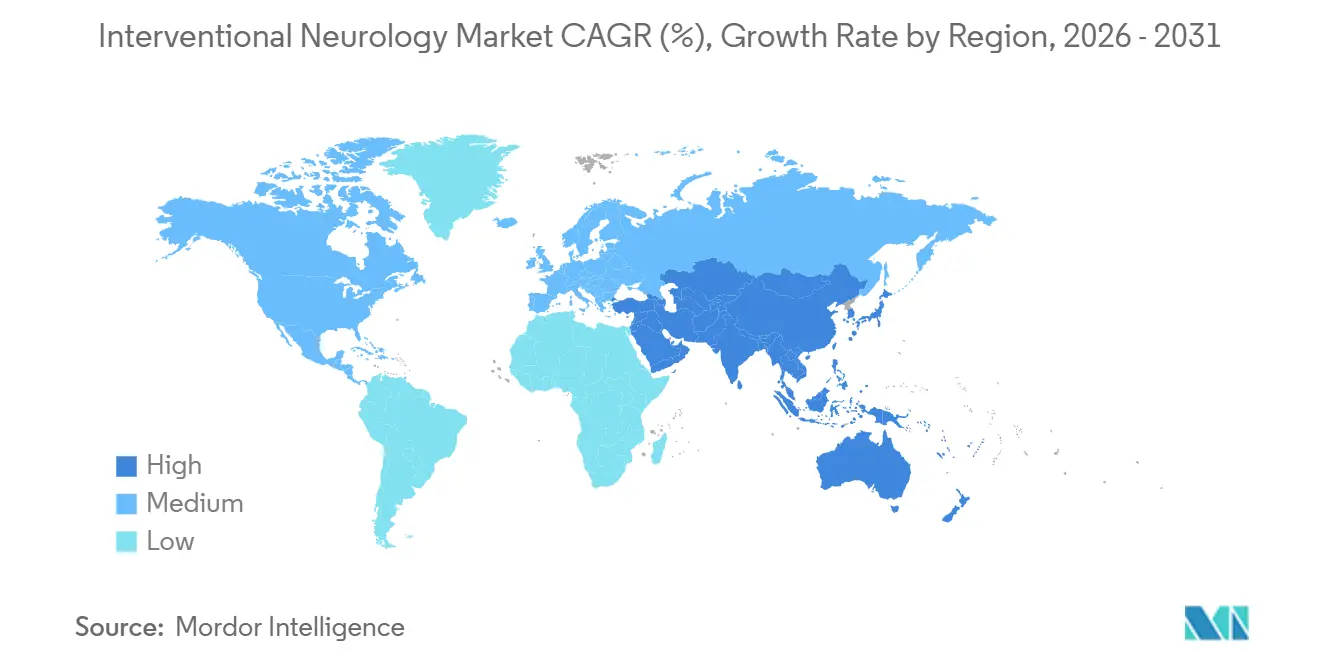

- By geography, North America retained 41.25% of 2025 demand, but Asia-Pacific is expected to grow at a CAGR 8.50%, powered by China’s 5,000-center stroke program and India’s private-hospital suite build-outs.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Interventional Neurology Market Trends and Insights

Driver Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Ageing population & stroke incidence surge | +1.8% | Global, pressure highest in APAC and Europe | Long term (≥ 4 years) |

| Rapid adoption of mechanical thrombectomy | +1.5% | North America and EU core, expanding to urban APAC | Medium term (2-4 years) |

| Hospital consolidation elevating capex | +1.2% | North America, Western Europe | Medium term (2-4 years) |

| Ai-guided imaging for faster triage | +1.0% | North America, EU, large APAC metros | Short term (≤ 2 years) |

| Technological advancements in device design | +0.9% | Global, led by United States and Germany | Medium term (2-4 years) |

| Neuro-icu tele-intervention programs | +0.7% | United States, Australia, select EU networks | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stroke Incidence Outpaces Interventional Capacity

As stroke incidence rises, the gap between this surge and the capacity for intervention widens, driving a consistent demand for both diagnostic software and thrombectomy kits. In 2021, global data reported 7.63 million new ischemic strokes and projected a potential 50% increase by 2050 if current risk trends persist. Projections indicate that by 2030, China will have over 300 million citizens aged 65 and older, and India's stroke mortality has more than doubled from 1990 to 2019.[1]Xiaochuan Huo et al., “Trial of Endovascular Therapy for Acute Ischemic Stroke with Large Infarct,” New England Journal of Medicine, nejm.org In response, governments are certifying stroke centers and subsidizing endovascular training. Notably, Japan expanded its thrombectomy-capable facilities from 800 in 2020 to a projected 1,100 by 2024. With the demand for specialists lagging behind the growing caseload, hospitals are increasingly turning to AI-triage modules.

Mechanical Thrombectomy Gains Traction

Once 24-hour outcome data validated its efficacy, mechanical thrombectomy transitioned from a niche procedure to a standard care practice. A 2024 trial highlighted a significant difference: 49.2% of patients achieved functional independence at 90 days when thrombectomy was performed within a full-day window, compared to just 33.3% with optimal medical care. Reflecting this trend, Germany's data indicated a jump in thrombectomy usage from 8.2% of ischemic stroke admissions in 2015 to 22.7% by 2021, with analysts projecting penetration to exceed 30% by 2026. However, access remains inconsistent; many small U.S. community hospitals and facilities in emerging markets lack essential resources like biplane angiography and 24/7 specialists, leading to a two-tiered system.[2]European Medicines Agency, “Recall of Hydrophilic-Coated Guidewires,” EMA, ema.europa.eu In response, manufacturers introduced compact aspiration catheters and single-plane C-arm suites, reducing upfront costs by 25%.

Hospital Mergers Drive Up Capital Expenditure

In the U.S. and Europe, hospital mergers are consolidating neurovascular case volumes into larger systems, enabling them to negotiate bulk discounts on devices. Data indicates a 12% decline in independent stroke units from 2020 to 2024, juxtaposed with an 18% rise in certified comprehensive centers. In 2024, major players like Kaiser Permanente, Geisinger, and RWJBarnabas each poured over USD 50 million into constructing hybrid operating theaters, equipped with advanced technologies like cone-beam CT and 3D rotational angiography.[3]Washington State Department of Health, “Telestroke Annual Report 2024,” doh.wa.gov These larger systems can amortize the USD 2 million investment for biplane systems over 200-plus annual thrombectomies, enhancing their competitive edge.

AI Imaging Enhances Triage Efficiency

Between 2024 and 2025, several AI algorithms, including RapidAI’s Rapid LVO and Methinks’ Stroke Suite, received clearance for their ability to detect large-vessel occlusions within minutes of CT scans. A 2024 multicenter study revealed that AI integration reduced the median door-to-groin puncture time by 23 minutes and improved 90-day functional independence rates by 15%. In a notable achievement, Washington State's telestroke network, after integrating AI, managed to cut down non-essential helicopter transfers by 18%, resulting in a USD 7 million annual saving. Looking ahead, China has mandated the use of AI-triage software in all tier-2 hospitals by 2025, setting the stage for a lucrative USD 200 million domestic software market. Given the influx of algorithm approvals, imaging vendors are now prioritizing seamless cloud connectivity and robust cybersecurity measures as essential components for future system tenders.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High device cost & reimbursement hurdles | -1.3% | Global, acute in emerging markets and U.S. community hospitals | Medium term (2-4 years) |

| Shortage of trained neuro-interventionalists | -1.1% | Global, severe in APAC, MENA, rural North America | Long term (≥ 4 years) |

| Saturation of primary stroke centers tier 1 | -0.6% | North America, Western Europe | Short term (≤ 2 years) |

| Supply-chain exposure to rare-earth volatility | -0.4% | Global, highest risk in APAC manufacturing hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Device Costs & Reimbursement Challenges

Hospitals face significant financial barriers due to the high costs of biplane angiography suites, which range between USD 2-3 million. Additionally, disposables for a single thrombectomy procedure can exceed USD 12,000. Revisions to Medicare’s fee structures have further strained hospital margins in the United States. In India, the National Health Mission reimburses only USD 1,200 per procedure, prompting many public hospitals to discontinue the service. In Latin America, thrombectomy is generally excluded from standard benefit packages, with coverage largely restricted to private insurers in countries like Brazil and Argentina. While manufacturers have introduced catheter lines priced 30% lower than flagship systems, the cost disparity remains a significant challenge for low-income regions. Without the development of sustainable payment models, penetration into secondary cities will remain limited, constraining overall procedural growth.

Shortage of Qualified Neuro-Interventionalists

The global supply of board-certified neuro-interventionalists is unable to keep pace with demand, with an annual shortfall projected at 8%. In the MENA region, current capacity meets only 19.1% of the required demand, with some countries having fewer than five accredited specialists. In the United States, only 52 fellows were matched to interventional programs in 2024, highlighting the workforce gap. China is piloting live-streamed mentorship programs, allowing experts in major cities to supervise procedures in tier-2 hospitals, but scalability is hindered by infrastructure and credentialing challenges. In India, Apollo Hospitals is offering competitive salaries of USD 300,000 to attract foreign specialists, but visa-related issues are limiting the inflow of talent. Until autonomous robotics receive full regulatory approval, workforce shortages will continue to impact night-shift coverage outside of major centers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Imaging Platforms Surge Ahead of Treatment Devices

In 2025, treatment devices led in revenue generation, but diagnostic technologies are rapidly gaining ground as hospitals adopt comprehensive stroke pathways. Mechanical thrombectomy kits, anchored by Penumbra’s Lightning Flash and Vesalio’s NeVa systems, promise higher first-pass rates, solidifying their position in the interventional neurology market. Flow diverters, like Stryker’s Surpass Evolve, expedite aneurysm healing, and liquid embolics, such as Onyx, achieve a notable 78% complete obliteration in arteriovenous malformation cases. Hospitals are increasingly allocating budgets for AI-integrated technologies, including CT and biplane labs. Diagnostic vendors are enhancing their value through bundled software licenses, leading to a projected 7.56% CAGR growth for imaging systems by 2031, while maintaining gross margins around 45%.

By Therapeutic Application: Hemorrhagic Stroke on the Rise

In 2025, ischemic stroke accounted for 42.12% of spending, underscoring its dominance in clot retrieval. While ischemic care remains a significant share of the interventional neurology market, hemorrhagic indications are gaining traction. Advancements like improved coil technology and low-profile microcatheters are enhancing success rates and reducing retreatments. The 2024 CURES trial highlighted minimally invasive repairs' benefits, leading payers to endorse them. New evidence linking early intervention to reduced cognitive decline is prompting guideline updates, potentially increasing case captures.

With hemorrhagic procedures projected to grow at 7.60% through 2031, their contribution to the interventional neurology market is set to rise, especially in Japan and South Korea, where over 70% of adults over 50 are screened for aneurysms. Vendors focusing on detachable coils and flow disruptors stand to benefit from this trend, providing a cushion against potential price erosions in thrombectomy.

By Procedure Type: Thrombectomy Leads the Charge

Thrombectomy accounted for 38.00% of turnover in 2025 and is poised for the swiftest growth from 2026 to 2031. The interventional neurology market recognizes thrombectomy as its cornerstone procedure, bolstered by data supporting treatment windows extending up to 24 hours. Device manufacturers are prioritizing aspiration power and reliability, with Lightning Flash setting new benchmarks. Projections from Germany’s registry indicate thrombectomy's presence in over 30% of ischemic admissions by 2026. While coiling and flow diversion will see steady growth, they won't match thrombectomy's trajectory, positioning them as complementary.

By End-User: Specialty Stroke Centers on the Fast Track

In 2025, hospitals and academic medical centers accounted for 65.45% of revenue, leveraging their biplane labs and dedicated staff for urgent neurovascular care. Consolidation efforts have boosted comprehensive stroke center certifications by 18% from 2020 to 2024. These centers utilize their case volume to negotiate lucrative 5-year deals encompassing devices, software, and services. They're also pioneers in robotics, with Siemens’ Corindus platform currently in neurovascular adaptation trials.

Specialty stroke centers, often located next to cardiac labs, are the fastest-growing segment, with an anticipated 8.20% CAGR. In India and Southeast Asia, private equity-backed operators are integrating stroke, cardiac, and critical-care services to optimize shared imaging resources.

Geography Analysis

In 2025, North America accounted for 41.25% of the revenue, driven by significant thrombectomy adoption and a well-established network of comprehensive stroke centers. Between 2016 and 2021, U.S. case volumes grew by 60%. However, Medicare payment reductions created margin pressures, leading multistate systems to consolidate purchasing power and prioritize vendors offering lifecycle services and AI-driven solutions. In 2024, Canada launched 12 new stroke centers in Ontario and British Columbia. Meanwhile, Mexico introduced pilot thrombectomy programs, although reimbursement remains limited.

Asia-Pacific is expected to be the fastest-growing region, with a projected growth rate of 8.50% through 2031. China plans to establish 5,000 certified stroke centers by 2030 and has mandated AI triage implementation in tier-2 hospitals by 2025. In India, private healthcare providers are investing in endovascular suites in metropolitan areas. Japan, despite challenges related to a shortage of skilled operators, has increased the number of thrombectomy-ready hospitals to 1,100 as of 2024.

Europe continues to benefit from coordinated national strategies. Germany, with its 340 stroke units and rapidly increasing thrombectomy rate, highlights the success of structured rollouts. By 2024, France is expected to expand population access to 75%, while the United Kingdom operates 24 thrombectomy hubs. However, rural areas in Scotland and Wales still lack 24/7 coverage.

Latin America and the Middle East show uneven progress. In Brazil, the national healthcare system covers thrombolysis but not thrombectomy, limiting the number of procedures performed. Argentina's private insurers are piloting coverage, signaling potential future growth. In the Gulf states, expertise is being imported through tele-intervention to address workforce shortages. Africa remains in the early stages of development, constrained by limited reimbursement frameworks and a shortage of specialists.

Competitive Landscape

The interventional neurology market remains moderately concentrated; Medtronic, Stryker, and Penumbra together captured the majority of 2025 revenue. Medtronic leverages its Pipeline diverter brand equity and global service force, while Stryker exploits an installed biplane imaging base and bundled consumables that extend customer lock-in. Penumbra differentiates with aspiration catheters that undercut peers on price and offer flexible-shaft profiles favored in tortuous anatomy. Siemens Healthineers, though not a catheter supplier, influences buying decisions through its CorPath GX robotics that integrates with multiple device brands, expanding ecosystem power beyond hardware margin.

Venture-backed challengers add complexity. Vesalio, financed with USD 40 million Series B in 2025, promotes a self-expanding mesh thrombectomy system that captures floating clot without aspiration, appealing to operators seeking simplicity. Rapid Medical’s Comaneci earned momentum as a temporary bridging mesh for coil procedures before being absorbed by Medtronic, showing incumbents’ appetite for bolt-on buys that pre-empt disintermediation. Nanocoated guidewire innovations, such as Stryker’s Synchro-2 and Johnson & Johnson’s Cereglide, deepen portfolios with safety narratives that resonate post-EMA recall, supplying an incremental but sticky edge as ISO adhesion tests harden.

Interventional Neurology Industry Leaders

Boston Scientific Corporation

Medtronic PLC

Stryker Corporation

Johnson & Johnson (Cerenovus)

Terumo Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Sonorous Neurovascular secured FDA 510(k) clearance for the BosCath next-generation cerebral catheter, enabling U.S. commercialization.

- April 2026: AIIMS New Delhi initiated clinical deployment of Hyperfine’s portable MRI, the first bedside MRI in India, signaling a shift toward point-of-care neuro-imaging.

- February 2025: Johnson & Johnson MedTech introduced the CEREGLIDE 92 Catheter System, a next-generation 0.092-inch platform paired with the INNERGLIDE 9 delivery aid to simplify the placement and guidance of devices inside delicate neurovascular pathways

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the interventional neurology market as all minimally invasive, image-guided devices, coils, stents, aspiration systems, flow diverters, catheters, guidewires, and support accessories used to diagnose or treat intracranial aneurysm, arteriovenous malformation, and acute ischemic or hemorrhagic stroke. Procedures performed in hybrid operating rooms, neuroangiography suites, and ambulatory cath labs across 17 major countries are counted at manufacturer selling price; capital imaging systems are not.

Scope exclusion: neurostimulation implants, open surgical clips, and diagnostic only consumables sit outside our frame.

Segmentation Overview

- By Product Type

- Treatment Devices

- Mechanical Thrombectomy Devices

- Neurovascular Stent Systems

- Embolic Coils & Intrasaccular Implants

- Flow-Diverter Devices

- Liquid Embolic Agents

- Balloon Guide & Aspiration Catheters

- Neurovascular Micro-catheters & Guidewires

- Diagnostic & Imaging Technologies

- Biplane Cerebral Angiography Systems

- 3-D Rotational Angiography

- Intra-operative CT / Cone-Beam CT

- MRI / fMRI for Neuro-intervention Planning

- Trans-cranial & Carotid Doppler Ultrasound

- Neuro-navigation & Robotics Platforms

- AI-based Stroke Imaging & Triage Software

- Treatment Devices

- By Therapeutic Application

- Ischemic Stroke

- Hemorrhagic Stroke

- Sub-arachnoid Hemorrhage

- Cerebral Aneurysm

- Arteriovenous Malformation

- By Procedure Type

- Thrombectomy

- Coiling / Embolization

- Stenting & Flow Diversion

- Clipping

- Angioplasty

- By End-User

- Hospitals

- Ambulatory Surgical Centers

- Specialty Stroke Centers

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Interviews with neurosurgeons, interventional radiologists, and supply chain managers across North America, Europe, China, and India walked our analysts through case mix evolution, average selling prices, and device replacement cycles, allowing us to close gaps spotted in desk work and pressure test every key assumption.

Desk Research

We began by mining publicly available tier 1 datasets such as WHO Global Health Observatory stroke incidence files, CDC FAST-Stats, OECD hospital discharge records, and Eurostat procedure volumes, which offered hard epidemiology and utilization baselines. Trade association notes from the European Stroke Organization, FDA 510(k) summaries, and peer-reviewed journals in JNIS clarified technology adoption curves and failure rates.

Commercial fundamentals were further refined with D&B Hoovers company filings, Volza shipment bills for micro catheters, patent trends via Questel, and targeted news pulls from Dow Jones Factiva. These sources, while illustrative, are not exhaustive, and many other documents supported data checks and context building.

Market-Sizing & Forecasting

A top down prevalence to treated patient build paired with sampled ASP × volume roll ups provides the core model; the two views are reconciled once through a single top down and bottom up checkpoint to remove double counts. Input fingerprints include annual mechanical thrombectomy counts, intracranial aneurysm screening rates, elective vs emergency mix, replacement interval of detachable coils, health insurer reimbursement shifts, and precious metal cost swings. Multivariate regression fed with these variables, and validated by expert consensus, projects demand through 2030 while scenario analysis cushions regulatory or pricing shocks.

Data Validation & Update Cycle

Mordor analysts benchmark model outputs against independent metrics each quarter, flagging ≥5% variances for senior review, after which revised numbers flow into the live dashboard. Reports refresh yearly, and material recalls or guideline changes trigger ad hoc updates before final delivery.

Why Mordor's Interventional Neurology Devices Baseline Commands Reliability

Published estimates vary because firms choose different device baskets, patient pools, and refresh cadences.

Our disciplined scope alignment and annual expert rechecks keep the Mordor baseline tightly tethered to observable procedure volumes.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.44 B | Mordor Intelligence | - |

| USD 2.87 B | Regional Consultancy A | excludes flow diverters and emergency thrombectomy kits |

| USD 3.12 B | Global Consultancy B | uses 2023 ASPs without metal price inflation adjustment |

| USD 2.45 B | Trade Journal C | models only hospital purchases, omits ambulatory cath labs |

The comparison shows that scope omissions, dated pricing, or narrow channel coverage can swing totals by almost a billion dollars. Mordor's carefully delineated device list, live ASP tracking, and multi setting demand capture therefore provide decision makers the most balanced and transparent starting point.

Key Questions Answered in the Report

What is the interventional neurology diagnosis and treatment market size in 2026?

The market is valued at USD 5.38 billion in 2026 and is projected to reach USD 7.59 billion by 2031.

How fast is thrombectomy growing within the field?

Thrombectomy revenue is forecast to expand at 7.90% CAGR between 2026-2031, the fastest among all procedure types.

Which region is the quickest to adopt advanced neurovascular procedures?

Asia-Pacific leads with an 8.50% forecast CAGR, propelled by China's stroke-center build-out and India's private-hospital investments.

Why are AI-ready imaging platforms gaining traction?

AI triage shortens door-to-puncture by roughly 23 minutes, improving 90-day outcomes and boosting imaging platform return on investment.

What are the principal barriers to wider adoption in emerging markets?

High capital costs and limited reimbursement remain the key hurdles, trimming forecast CAGR by 1.3% despite underlying demand.

How concentrated is supplier power in this space?

The top five companies hold about 60% of global revenue, giving the market a concentration score of 6 yet still leaving room for niche innovators.

Page last updated on: