Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 23.21 Billion |

| Market Size (2031) | USD 29.79 Billion |

| Growth Rate (2026 - 2031) | 5.12% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cardiac Rhythm Management Devices Market Analysis by Mordor Intelligence

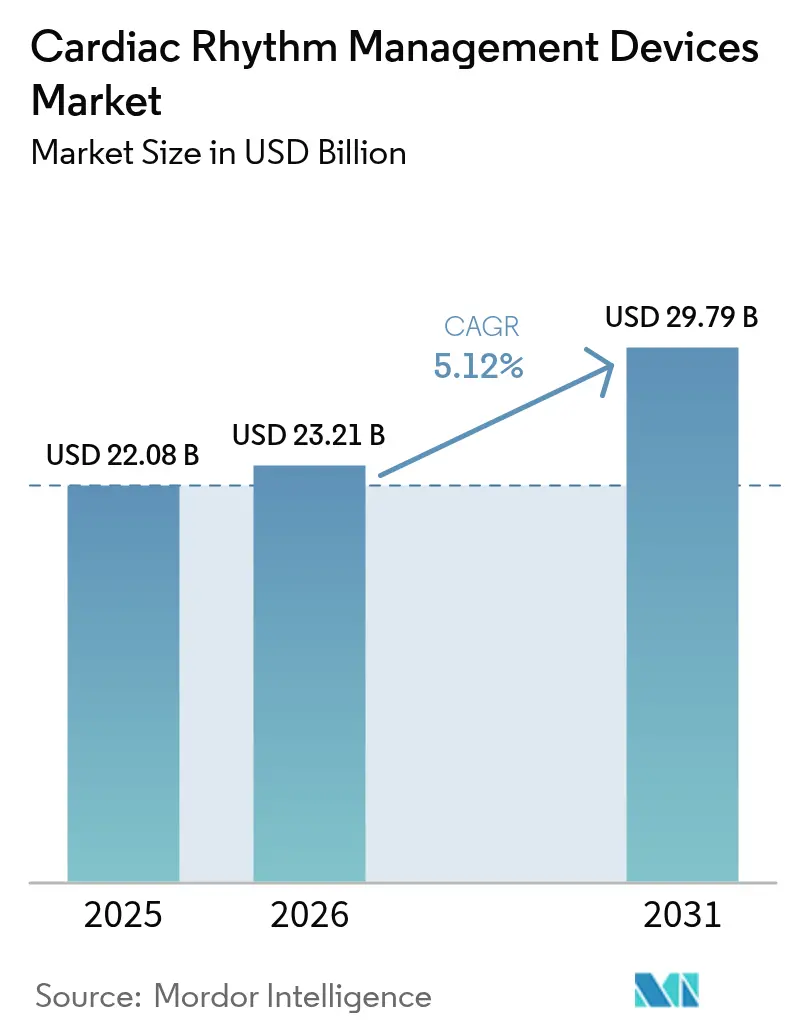

The cardiac rhythm management devices market size is expected to grow from USD 22.08 billion in 2025 to USD 23.21 billion in 2026 and is forecast to reach USD 29.79 billion by 2031 at 5.12% CAGR over 2026-2031. Growth is underpinned by an aging global population, rising arrhythmia incidence, and the expanding use of implantable devices that lower rehospitalization risks.[1]American Heart Association, “2025 Heart Disease and Stroke Statistics,” professional.heart.orgRapid advances in leadless pacemakers and artificial-intelligence (AI)–enabled monitoring platforms are improving clinical outcomes while reducing procedure times and follow-up visits. Reimbursement reforms that now cover next-generation devices in major markets are widening patient access, and remote patient-monitoring mandates are generating steady recurring revenue for device makers. Supply-chain pressures tied to semiconductor tariffs and specialty-metal price swings continue to tighten margins, but sustained R&D investment and targeted acquisitions keep competitive intensity high.

Key Report Takeaways

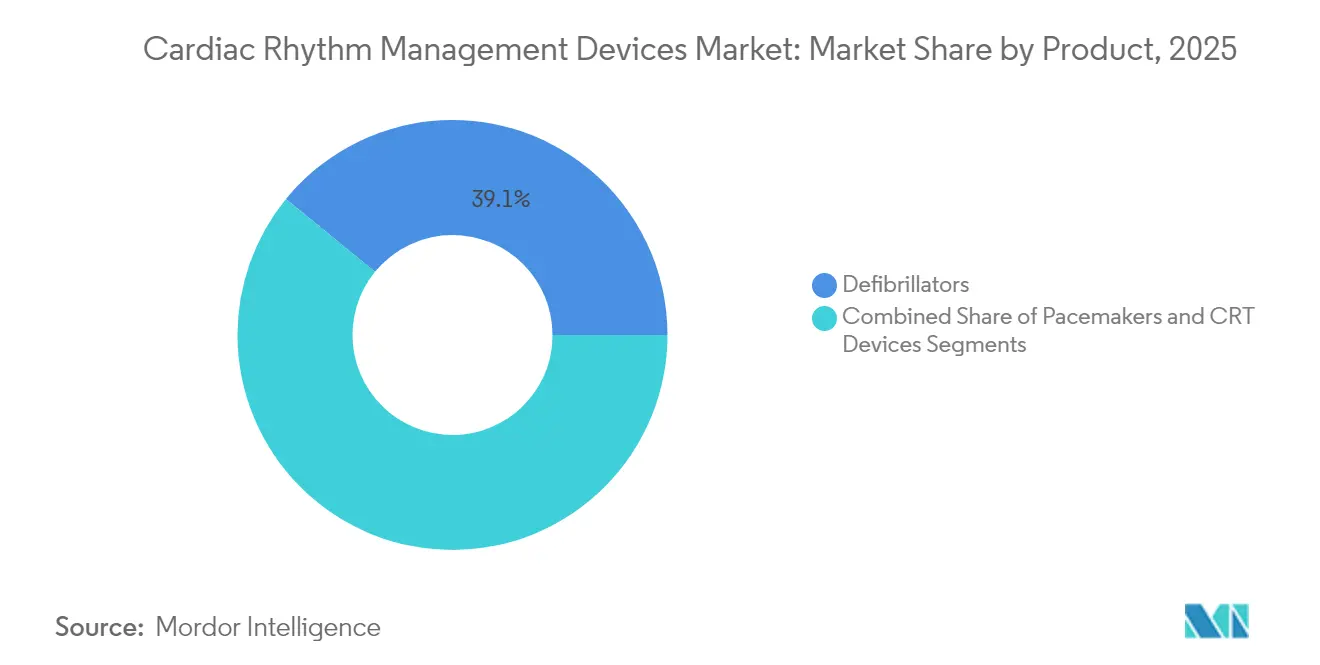

- By product category, defibrillators led with 39.10% revenue share of the cardiac rhythm management devices market in 2025, while pacemakers are projected to expand at a 7.25% CAGR through 2031.

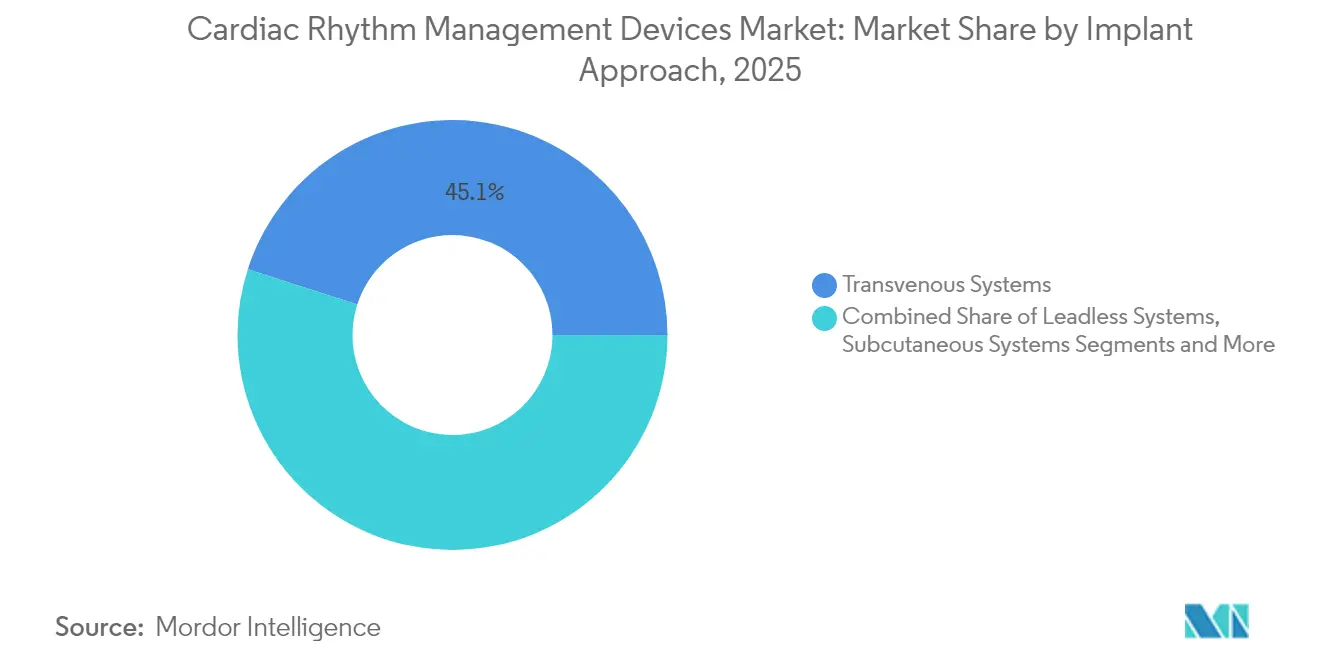

- By implant approach, transvenous systems held 45.05% of the cardiac rhythm management devices market share in 2025; leadless systems record the fastest growth at 7.78% CAGR to 2031.

- By end user, hospitals accounted for 60.70% share of the ardiac rhythm management devices market in 2025, whereas home and pre-hospital care settings are forecast to grow at an 8.10% CAGR.

- By geography, North America commanded 36.10% share of the ardiac rhythm management devices market in 2025; Asia-Pacific shows the strongest momentum with a 7.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cardiac Rhythm Management Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge In Cardiovascular Disease Prevalence Coupled with Increasing Aging Population | +1.8% | Global, with highest impact in North America and Europe | Long term (≥ 4 years) |

| Expanding Adoption and Reimbursement For Rhythm Management Systems | +1.2% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Large Public-Access AED Roll-Outs In Transport Hubs | +0.4% | Global, with early gains in developed urban centers | Short term (≤ 2 years) |

| Remote Patient Monitoring and Telehealth Integration | +0.9% | Global, accelerated adoption in APAC and rural areas | Medium term (2-4 years) |

| Technological Advancement and Device Miniaturization | +1.1% | Global, led by innovation centers in US and Europe | Long term (≥ 4 years) |

| Increasing Adoption of Implantable Devices Coupled with Launch of New Products | +0.8% | Global, with premium adoption in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Cardiovascular Disease and Population Aging

Cardiovascular disease will affect nearly 45 million U.S. adults by 2050, with hypertension prevalence expected to climb to 61% during the same period.[1]American Heart Association, “2025 Heart Disease and Stroke Statistics,” professional.heart.orgSimilar demographic shifts across Europe and parts of Asia increase demand for durable pacemakers, implantable cardioverter-defibrillators (ICDs), and cardiac resynchronization devices. Longer life expectancy extends device replacement cycles, raising the lifetime value of each implantation. Payers favor rhythm management over repeated hospitalizations, underpinning steady procedural volumes. The resulting uptick in elective implants cushions the cardiac rhythm management devices market against cyclical funding pressures.

Wider Adoption and Reimbursement of Next-Generation Systems

Medicare added specific billing codes for leadless pacemakers in mid-2024, removing a key barrier to adoption.[2]Noridian Medicare, “Billing and Coding: Leadless Pacemakers (A59819),” med.noridianmedicare.com European authorities continue moving toward value-based payment models, rewarding devices that demonstrate lower rehospitalization rates. Japan’s reference-pricing revisions pressure list prices yet still allow premium positioning when clinical evidence shows superior outcomes. Together these policies shorten the path from regulatory approval to widespread clinical use, lifting procedural volumes and driving incremental revenue for manufacturers.

Public-Access AED Roll-Outs in Transport Hubs

Major cities now mandate automated external defibrillators (AEDs) in airports, subways, and large-capacity venues, enlarging a high-volume replacement market. Studies show that strategic AED placement can cut response times by up to three minutes and lift survival from shockable rhythms by more than 30%. Programs often bundle maintenance contracts, giving OEMs annuity-like service income. Although bystander use remains below optimal levels, targeted training initiatives improve utilization and reinforce the value proposition of public-access defibrillators.

Remote Monitoring and Telehealth Integration

AI-enhanced algorithms in insertable cardiac monitors filter nuisance alerts by as much as 85%, saving clinical staff hundreds of hours each year. Hospital-at-home models show 30% cost savings and an 83% reduction in readmissions for eligible arrhythmia patients. These outcomes justify payer coverage for remote platforms, creating predictable recurring revenue streams. Continuous data capture also supports predictive analytics that may guide earlier interventions, further elevating the cardiac rhythm management devices market’s clinical relevance.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cyber-Vulnerability Of Connected CRM Devices | -0.7% | Global, with highest concern in developed markets | Medium term (2-4 years) |

| Lengthy Regulatory Approval Cycles | -0.5% | Global, with variations by regulatory jurisdiction | Long term (≥ 4 years) |

| Post-Radiation Malfunctions In Implantables | -0.3% | Global, affecting cancer treatment centers | Medium term (2-4 years) |

| Lithium & Tantalum Price Volatility Inflates BOM Costs | -0.6% | Global, with supply chain concentration in Asia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cyber-Vulnerability of Connected Devices

The FDA now requires cybersecurity plans as part of pre-market submissions, citing recent alerts that certain patient monitors could be remotely accessed.[3]FDA, “Aurora EV-ICD System – P220012,” fda.gov Older implants lacking modern encryption remain in service, exposing hospitals to network breaches and creating liability concerns. Manufacturers are investing in over-the-air patching and zero-trust architectures, but any data-breach headline can slow adoption of cloud-connected platforms, dampening cardiac rhythm management devices market growth.

Lengthy Regulatory Approval Cycles

Novel systems such as the AVEIR VR leadless pacemaker still face multiyear reviews that delay commercial rollout. Added evidence requirements for AI-enabled devices raise trial costs, discouraging smaller entrants. Regional divergence in data-submission formats further stretches timelines and heightens compliance overhead, limiting the number of new competitors able to scale globally.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Defibrillators Maintain Scale While Pacemakers Drive Innovation

Defibrillators represented 39.10% of the cardiac rhythm management devices market in 2025, anchored by widespread clinical guidelines that recommend ICD therapy for sudden-death prevention. New extravascular ICDs show 98.7% effective defibrillation rates, adding non-intravascular alternatives for infection-prone patients. External AED demand rises alongside mandated public installations, though real-world utilization remains below targets. Complementary service contracts add recurring revenue, supporting the cardiac rhythm management devices market size for defibrillator makers.

Pacemakers deliver the fastest expansion, advancing at a 7.25% CAGR as leadless designs eliminate pocket infections and venous complications. Dual-chamber leadless systems preserve physiologic pacing and achieve near-universal implant success, attracting electrophysiologists who previously hesitated to forgo transvenous leads. AI-driven alert filtering suppresses false positives by 85%, improving clinic efficiency and reinforcing the cardiac rhythm management devices market size advantage for connected pacemaker platforms.

By Implant Approach: Leadless Systems Disrupt Transvenous Dominance

Transvenous implants still account for 45.05% of the cardiac rhythm management devices market share due to entrenched surgical workflows and broad indication coverage. Multichamber configurations remain best suited for complex heart failure cases, and replacement familiarity sustains transplant volumes. Yet leadless solutions are advancing at an 7.78% CAGR, reflecting strong clinician acceptance of minimally invasive procedures with lower complication rates. Early studies report a 94% complication-free rate for single-chamber leadless implants, far surpassing historical benchmarks for wired systems. Retrievable modules now allow staged upgrades without leaving redundant hardware in place, enhancing long-term device management flexibility.

By End User: Hospitals Dominate; Home Care Gains Traction

Hospitals generated 60.70% of 2025 revenues as most device implantations still require catheter labs, anesthesia support, and acute-care monitoring. Same-day discharge pathways cut inpatient stay but keep procedure volumes high. Meanwhile, home and pre-hospital care segments grow at an 8.10% CAGR, propelled by payers that reimburse remote monitoring kits and telecardiology visits. Continuous patch-ECG services and cloud-connected pacemakers lower follow-up costs, positioning decentralized care as the next growth frontier.

Geography Analysis

North America led with 36.10% of 2025 sales thanks to favorable reimbursement and rapid uptake of AI-enabled monitoring. Updated CMS codes for leadless pacemakers widened access across U.S. electrophysiology centers. Canada’s national tender programs and Mexico’s private cardiology clinics add to regional demand, stabilizing the cardiac rhythm management devices market size in the short term.

Europe maintains steady growth on the back of value-based procurement that rewards outcome improvements. CE-marked dual-chamber leadless systems launched widely in 2024, accelerating replacements of legacy single-chamber devices. Country-level cost-containment pressures persist, yet proven reductions in rehospitalizations offset initial device premiums.

Asia-Pacific is the fastest-growing arena, expanding at a 7.55% CAGR. Japan’s device market encourages technology adoption despite price cuts, while China’s localization policies spur domestic production alongside foreign joint ventures. India scales public-health spending and private cardiac centers, and Australia subsidizes remote-monitoring platforms for rural populations, supporting sustained region-wide momentum within the cardiac rhythm management devices market.

Competitive Landscape

Moderate consolidation defines the field, with Medtronic, Abbott, and Boston Scientific holding leadership through full-line portfolios and deep clinical trial pipelines. Medtronic reported high-single-digit rhythm-management growth in fiscal Q1 2025, fueled by strong ICD sales and double-digit pacing-therapy expansion. Abbott’s AVEIR franchise sets benchmarks in leadless innovation, and Boston Scientific’s cardiovascular revenue surged 26.2% on FARAPULSE adoption.

Strategic acquisitions augment platform coverage. Johnson & Johnson’s USD 16.6 billion purchase of Abiomed adds heart-recovery devices, broadening its procedural stack. Teleflex agreed to acquire BIOTRONIK’s vascular intervention unit for USD 825 million, gaining access to a USD 10 billion coronary market that overlaps rhythm-management referrals. Niches such as pediatric leadless pacing and implant cybersecurity invite smaller specialists, but scale advantages in manufacturing and distribution give incumbents a persistently strong footing in the cardiac rhythm management devices market.

Cardiac Rhythm Management Devices Industry Leaders

Abbott

Boston Scientific Corporation

Medtronic PLC

MicroPort Scientific

Stryker

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Element Science received FDA PMA approval for its Jewel Patch wearable cardioverter-defibrillator, offering temporary protection for patients at elevated sudden-arrest risk.

- February 2025: Teleflex announced an agreement to acquire BIOTRONIK’s vascular intervention business for EUR 760 million (USD 825 million), with closing expected in Q3 2025.

- December 2024: Abbott completed the world’s first in-human leadless left-bundle-branch pacing procedures using its investigational AVEIR conduction system pacing technology, which holds FDA Breakthrough Device Designation.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the cardiac rhythm management (CRM) devices market as all implantable or external pacemakers, defibrillators, and cardiac resynchronization therapy systems that actively sense, pace, or deliver shocks to stabilize heart rhythm disorders.

Scope Exclusion: Purely diagnostic cardiac monitors and wearable ECG patches without therapeutic capability are left outside this estimate.

Segmentation Overview

- By Product

- Defibrillators

- Implantable Cardioverter Defibrillators (TV-ICD, S-ICD)

- External Defibrillators (Manual, AED, Wearable)

- Pacemakers

- Implantable (Single, Dual, Leadless, MRI-compatible)

- External Pacemakers

- Cardiac Resynchronization Therapy Devices

- CRT-Defibrillators (CRT-D)

- CRT-Pacemakers (CRT-P)

- Defibrillators

- By Implant Approach

- Transvenous Systems

- Leadless Systems

- Subcutaneous Systems

- Extravascular / Substernal Systems

- External / Non-invasive Systems

- By End User

- Hospitals

- Cardiac Specialty Centers

- Ambulatory Surgical Centers

- Home & Pre-Hospital Care Settings

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interview interventional cardiologists, electrophysiology nurses, and reimbursement managers across North America, Europe, and fast-growing Asia-Pacific hubs. Their inputs validate therapy mix shifts (for example, leadless pacing penetration) and refine price-band assumptions that secondary sources rarely capture.

Desk Research

We start by mapping published volumes from trusted public sources such as the World Health Organization, OECD health statistics, and national procedure registries; these reveal treated-patient pools and implant counts. Trade bodies like the Heart Rhythm Society, device adverse-event databases of the US FDA, and import-export shipment trackers (Volza) provide shipment, recall, and cross-border flow signals. Company 10-Ks, investor decks, and peer-reviewed journals then fill pricing, technology adoption, and replacement-cycle clues. Select paid repositories, including D&B Hoovers for financial splits and Questel for patent velocity, supply further context. This list illustrates but does not exhaust the documentary base we tap every cycle.

Market-Sizing & Forecasting

A top-down procedure build begins by aligning national implant counts and external shock deployments with weighted average selling prices, which are then corroborated through sampled supplier roll-ups and hospital channel checks to adjust anomalies. Key variables like arrhythmia prevalence trends, first-implant versus replacement ratios, reimbursement tariff revisions, ASP erosion curves, and device battery-life improvements drive the multivariate regression that underpins our 2025-2030 outlook. Gaps in bottom-up inputs (e.g., missing country price tiers) are bridged using regional analogs agreed upon during expert calls.

Data Validation & Update Cycle

Outputs pass two-step analyst review, variance checks against independent signals, and threshold alerts that trigger re-contact with experts. The model refreshes annually; material events such as major recalls prompt mid-year updates before final client delivery.

Why Mordor's Cardiac Rhythm Management Devices Baseline Commands Reliability

Published market values often diverge because firms differ in device scope, currency conversions, and refresh cadence.

Key gap drivers here include Mordor's exclusion of diagnostic monitors, our 2025 base year versus some 2024 anchors, and our implant-weighted ASP matrices, while others lift list prices or mix monitoring hardware with therapy devices.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 22.08 B (2025) | Mordor Intelligence | - |

| USD 21.30 B (2024) | Global Consultancy A | combines monitoring and therapy hardware, which inflates baseline |

| USD 17.17 B (2024) | Industry Association B | narrower country set and uses invoice net prices without replacement units |

| USD 21.10 B (2024) | Regional Consultancy C | omits external defibrillators and applies conservative ASP erosion from 2022 onward |

The comparison shows that, by anchoring on verified implant data, transparent price ladders, and annual refreshes, Mordor delivers a balanced, decision-ready baseline that clients can retrace and audit with minimal effort.

Key Questions Answered in the Report

What is the current valuation of the cardiac rhythm management devices market and how fast is it expanding?

The cardiac rhythm management devices market is valued at USD 23.21 billion in 2026 and is forecast to reach USD 29.79 billion by 2031, reflecting a 5.12% CAGR over 2026-2031.

Which product segment is growing the fastest?

Pacemakers lead growth with a 7.25% CAGR through 2031, fueled by leadless technology that simplifies implantation and reduces complications.

Why are leadless systems gaining momentum over traditional transvenous implants?

Leadless devices eliminate lead-related infections, offer simpler procedures, and now include dual-chamber options that preserve natural heart synchrony, pushing their CAGR to 7.78%.

How are reimbursement changes influencing market adoption?

Updated Medicare billing codes and value-based payment models in Europe have lowered financial barriers, accelerating uptake of next-generation pacemakers and ICDs.

Which region offers the strongest growth opportunity?

Asia-Pacific is the fastest-growing region, advancing at a 7.55% CAGR as healthcare access expands and aging populations drive demand for advanced cardiac therapies.

What major risk could slow market expansion?

Cyber-vulnerabilities in connected implants remain a key concern; tighter FDA rules now require robust security plans, and any breach could dampen clinician and patient confidence.

Page last updated on: