Nuclear Medicine Radioisotopes Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 8.09 Billion |

| Market Size (2031) | USD 13.12 Billion |

| Growth Rate (2026 - 2031) | 10.17% CAGR |

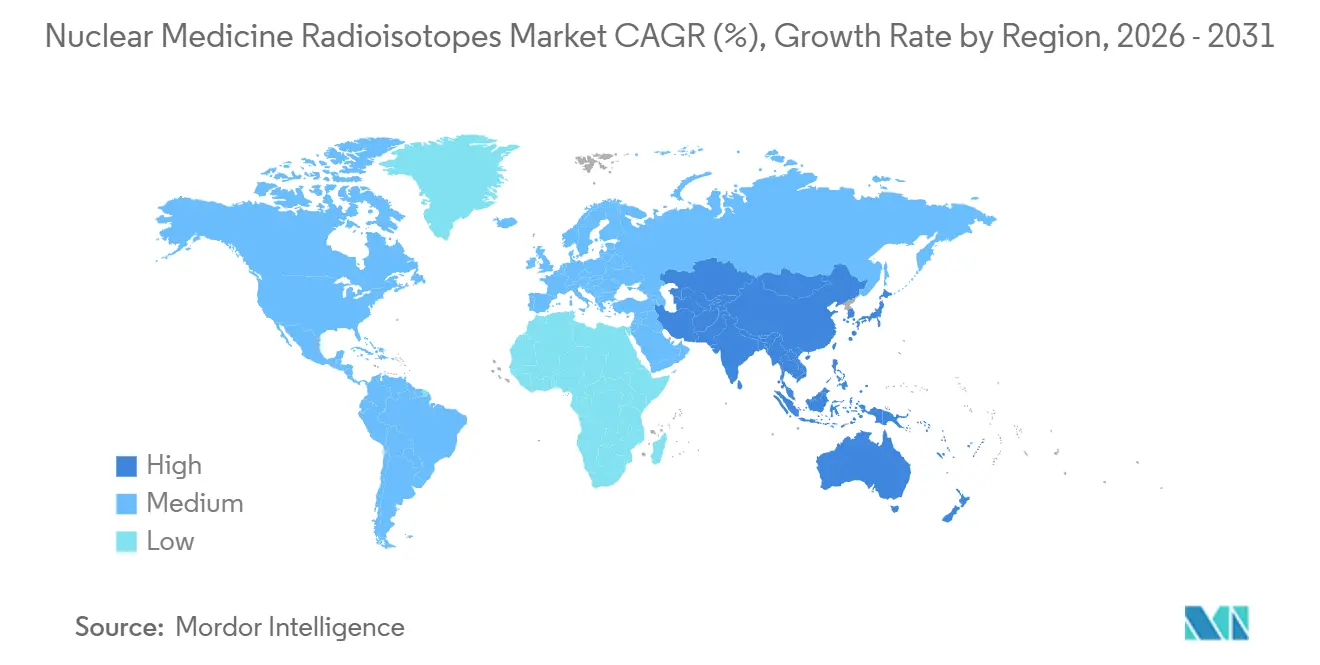

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

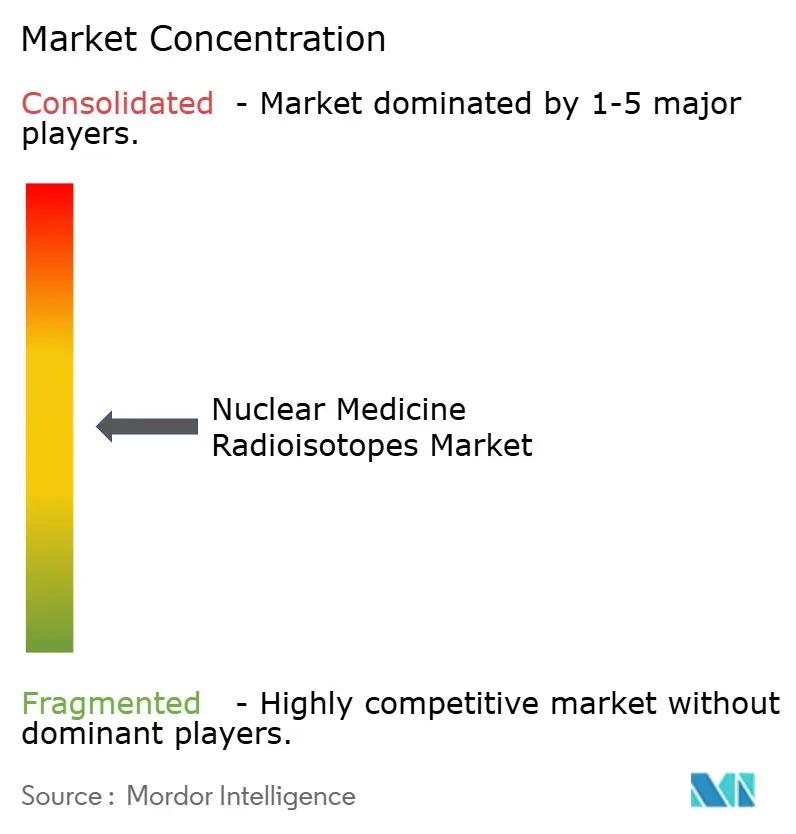

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Nuclear Medicine Radioisotopes Market Analysis by Mordor Intelligence

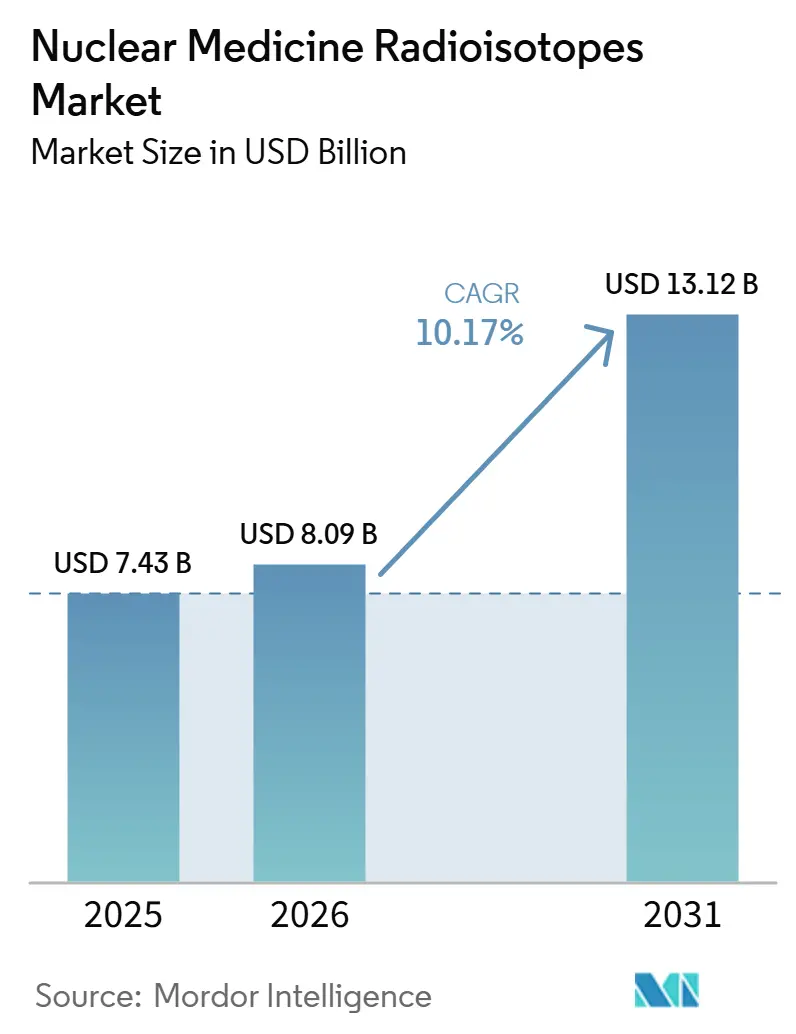

The Nuclear Medicine Radioisotopes Market size is projected to be USD 7.43 billion in 2025, USD 8.09 billion in 2026, and reach USD 13.12 billion by 2031, growing at a CAGR of 10.17% from 2026 to 2031.

The nuclear medicine radioisotopes market is growing on the back of persistent demand from cancer care and cardiovascular care, where imaging and targeted therapy are becoming more integrated into treatment pathways. The nuclear medicine radioisotopes market is also benefiting from the shift toward radioligand therapy, where commercial production, dose logistics, and hospital readiness are improving together rather than in isolation. Supply strategy is becoming a more important competitive factor because producers that can secure isotope feedstock, processing capacity, and distribution channels are in a stronger position to support both diagnostic and therapeutic demand. Commercial power reactor co-production and the diversification of precursor supply are reducing some of the bottlenecks that had kept therapeutic expansion exposed to concentration risk. At the same time, the nuclear medicine radioisotopes market still faces pressure from short isotope half-lives, aging research reactors, and policy uncertainty around cross-border supply, which means market opportunity increasingly favors operators that can combine production resilience with compliant delivery networks.

Key Report Takeaways

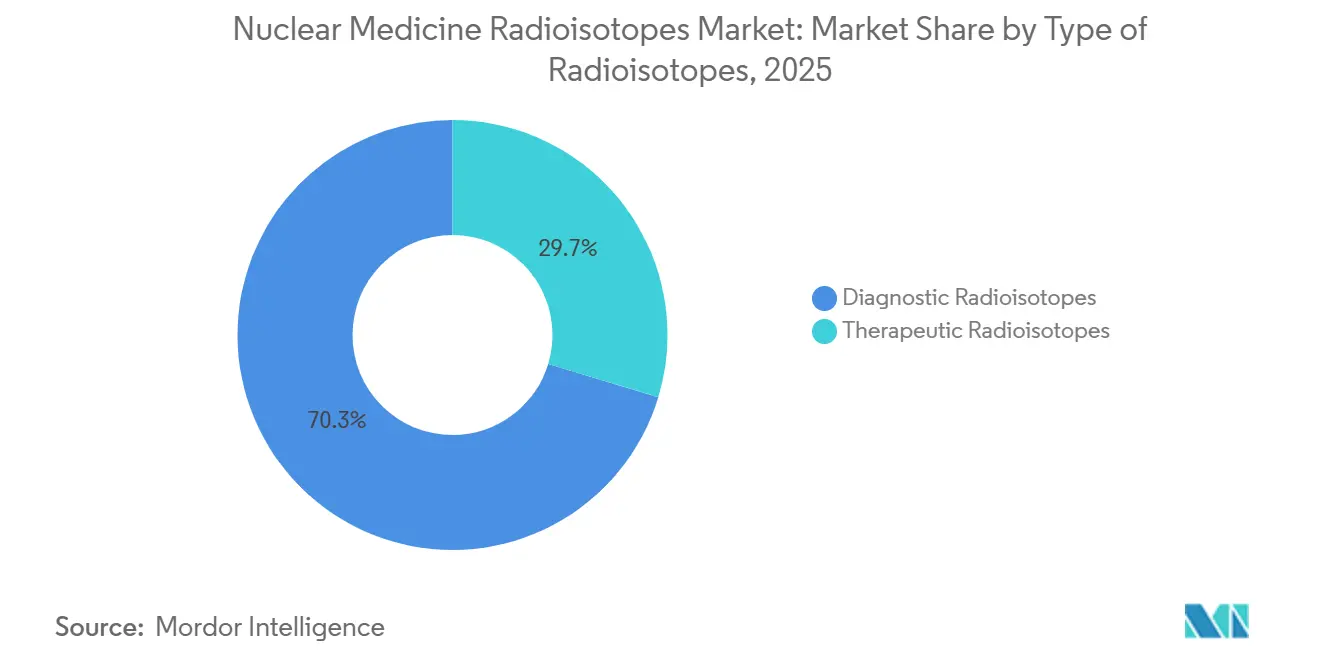

- By type of radioisotopes, diagnostic radioisotopes led with 70.33% of the nuclear medicine radioisotopes market share in 2025, while therapeutic isotopes are expected to advance at an 12.99% CAGR through 2031.

- By application, oncology captured 45.75% revenue in 2025, and is projected to expand at a 10.82% CAGR to 2031.

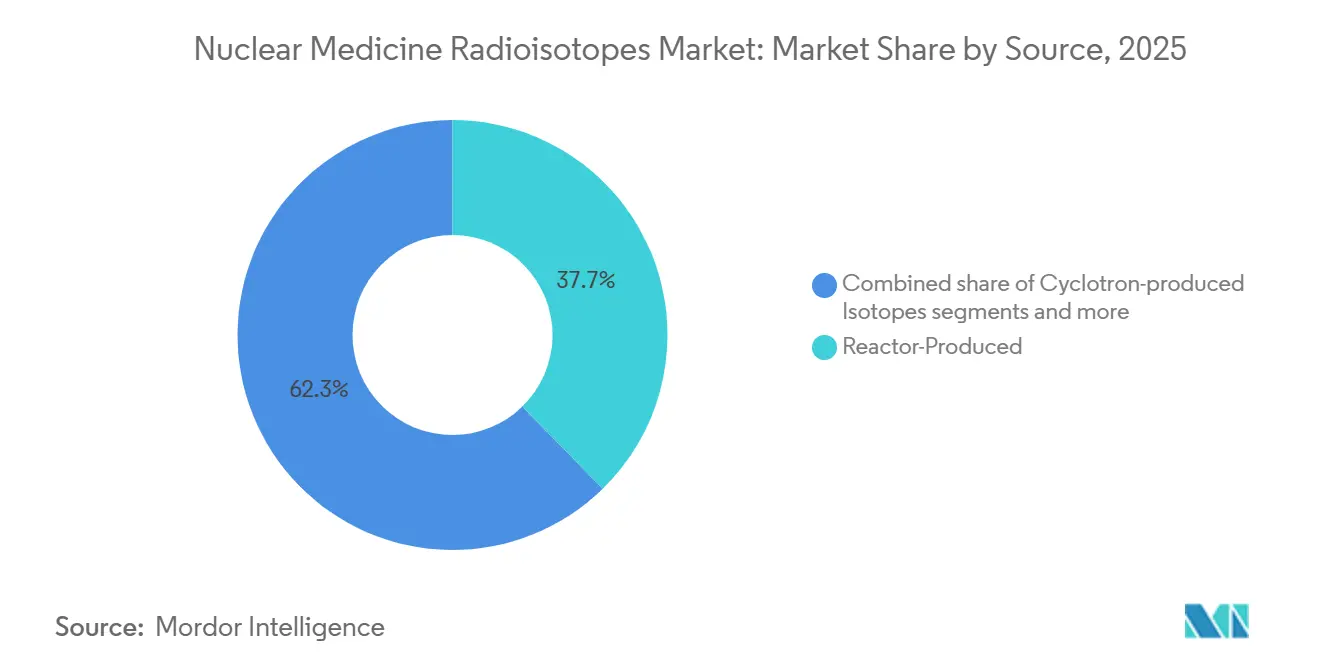

- By source, reactor-produced isotopes dominated with 37.69% share in 2025, but power-reactor co-production isotopes are forecast to grow at an 13.29% CAGR through 2031.

- By end user, the private sector held 54.67% revenue share in 2025, and is poised for a 11.26% CAGR through 2031.

- By geography, North America retained 37.33% share in 2025, but Asia-Pacific is projected to deliver a 10.87% CAGR through 2031 as local distribution networks scale.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Nuclear Medicine Radioisotopes Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Burden of Cancer and Cardiac Disorders | +3.2% | Global, highest concentration in Asia-Pacific and North America | Long term (≥ 4 years) |

| Widening Applications of Nuclear Medicine | +2.0% | Global, early gains in APAC and MEA | Medium term (2-4 years) |

| Increasing SPECT and PET Applications | +1.6% | North America, Europe, Japan, South Korea | Medium term (2-4 years) |

| Increasing Patient Awareness of Radiation and Radiation Therapy | +0.7% | North America, Europe, urban APAC | Long term (≥ 4 years) |

| Co-Production of Isotopes in Power Reactors Cutting Marginal Costs | +1.1% | North America (CANDU), APAC, spill-over to Europe | Short term (≤ 2 years) |

| AI-Driven Radiopharmacy Automation Lifting Dose Yields | +0.6% | North America, Europe, early gains in Japan and South Korea | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Burden of Cancer and Cardiac Disorders

The nuclear medicine radioisotopes market has a durable demand base because cancer and cardiovascular disease continue to generate large and recurring diagnostic and treatment needs across health systems. The global burden of cardiovascular disease now accounts for more than 437 million disability-adjusted life years each year, while cancer incidence is nearing 20 million new cases annually, which keeps molecular imaging and targeted isotope therapy clinically relevant at scale. This matters for the nuclear medicine radioisotopes market because both disease groups often require repeated scans, staging work, treatment monitoring, and follow-up procedures rather than a single encounter. Older patients are also more likely to present with both cardiac disease and cancer, which raises repeat utilization per patient and supports steady procedure demand in hospitals and specialty centers. The World Heart Federation reported in 2025 that the cardiovascular burden will continue to rise through 2050, which supports a long planning horizon for isotope procurement and cardiac imaging capacity. As a result, the nuclear medicine radioisotopes market is supported not only by headline incidence growth, but also by a patient mix that requires more intensive imaging and therapy pathways over time.

Widening Applications of Nuclear Medicine

The nuclear medicine radioisotopes market is widening its clinical reach as theranostics links imaging and therapy around the same molecular targets, which expands use beyond conventional diagnostic workflows. This change is no longer limited to oncology because cardiology and neurology are drawing greater attention as hospitals build familiarity with targeted imaging pathways and dose handling requirements. The World Health Assembly adopted Resolution WHA78.13 in May 2025, which placed medical imaging capacity, including nuclear medicine, into national planning priorities and established progress reporting milestones for 2027, 2029, and 2031. That policy shift matters for the nuclear medicine radioisotopes market because access remains very uneven, with 1 SPECT scanner serving nearly 33 million people in low-income countries compared with 57,000 people in high-income countries. A formal push to close that access gap creates room for procedure growth using existing isotope classes rather than depending entirely on new isotope discovery. It also improves the long-run outlook for the nuclear medicine radioisotopes market in countries where reimbursement and equipment coverage had previously delayed adoption.

Increasing SPECT and PET Applications

The nuclear medicine radioisotopes market remains closely tied to the installed base and clinical use of SPECT and PET systems because those modalities account for most isotope procedure volume. More than 27,000 SPECT/CT systems and nearly 5,200 PET/CT systems are installed globally, which shows that nuclear medicine already operates on a meaningful infrastructure base rather than on isolated pilot programs. SPECT continues to support high-volume workflows in cardiology, oncology, and neurology, while PET keeps expanding its role in more targeted and high-value diagnostic use cases. The nuclear medicine radioisotopes market is also being helped by software improvements because deep-learning image reconstruction, partial-volume correction, and dosimetry tools are improving the usable output from each scan. Better image quality and dose interpretation strengthen the case for equipment refresh cycles and sustained isotope purchasing even when hospitals remain careful on capital spending. This means the nuclear medicine radioisotopes market is advancing through both higher procedural relevance and stronger productivity from existing imaging platforms.

Co-Production of Isotopes in Power Reactors Cutting Marginal Costs

The nuclear medicine radioisotopes market is starting to benefit from a supply model that uses commercial power reactors to produce isotopes without interrupting electricity generation. Ontario Power Generation received approval in May 2025 for Darlington to produce Y-90 and Lu-177 commercially, with Y-90 production beginning in 2026 and Lu-177 expected from 2027. The project is expected to support annual output of 3 million Y-90 doses and enough Lu-177 for 500,000 patient treatments, which is a meaningful increase in scale for therapeutic supply. In the nuclear medicine radioisotopes market, this model matters because it can reduce the cost burden that dedicated research reactors carry when production depends on outage windows and less flexible operating schedules. Darlington-linked doses are also planned for distribution to more than 30 countries through BWXT Medical, which shows that co-production is being built around export-ready networks rather than local use alone. Over time, that creates a stronger cost and reliability benchmark that other suppliers in the nuclear medicine radioisotopes market will need to match.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Short Half-Life, Just-In-Time Logistics & Waste Challenges | -1.9% | Global, most acute in APAC and South America | Long term (≥ 4 years) |

| Aging Research-Reactor Fleet Limiting Isotope Output | -1.5% | Global, acute in Europe and North America | Short term (≤ 2 years) |

| Export Controls on Enriched Yb-176 Constraining NCA Lu-177 Supply | -1.0% | APAC core, North America, Europe | Medium term (2-4 years) |

| Evolving Trade Policies and Import Duties on Radiopharmaceuticals | -0.7% | North America, EU, spill-over to global supply chains | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Short Half-Life, Just-In-Time Logistics & Waste Challenges

The nuclear medicine radioisotopes market remains constrained by the fact that many isotopes decay too quickly to support conventional pharmaceutical inventory practices. Mo-99 has a 66-hour half-life, which makes the supply chain highly sensitive to timing between irradiation, processing, shipment, and patient administration[1]OECD Nuclear Energy Agency, “Current Trends in the Supply and Utilisation of Medical Radioisotopes,” OECD NEA, oecd-nea.org. Shorter-lived isotopes such as Ga-68 and F-18 create an even tighter logistics window, so regional production access becomes a structural requirement rather than a commercial preference. Waste handling adds another layer because licensed transport, controlled storage, and documentation obligations increase cost and reduce operational flexibility across borders. In the nuclear medicine radioisotopes market, these limits are especially relevant for emerging supply chains that are still building cyclotron coverage, radiopharmacy networks, and trained handling capacity. The same issue becomes more demanding as alpha-emitting therapies scale because contamination control and dose management requirements are stricter than what many beta-emitter workflows were designed to handle.

Aging Research-Reactor Fleet Limiting Isotope Output

The nuclear medicine radioisotopes market still depends heavily on an older research-reactor base for key isotopes, especially in the Mo-99 and Tc-99m chain. That dependence keeps the market exposed to outages, maintenance delays, and operating limits that were not originally designed around modern commercial isotope demand. The vulnerability is visible in Europe, where strong output has still been paired with concern over long-term resilience and replacement timing for major reactor infrastructure[2]European Nuclear Society, “BR2 Research Reactor Sets a New Production Record Helping 13 Million Patients in 2025,” EuroNuclear, euronuclear.org. Curium and NRG PALLAS extended their collaboration in May 2025 to support continuity of medical isotope supply, which shows that supply assurance remains a strategic priority rather than a settled issue. In the nuclear medicine radioisotopes market, this creates a planning challenge because downstream radiopharmacies and hospitals need dependable weekly availability even when upstream production is concentrated. Until newer capacity enters service at scale, the nuclear medicine radioisotopes market will continue to carry a reliability discount tied to the age profile of core reactor assets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type of Radioisotopes: Therapeutic Growth Is Rising Against Diagnostic Scale

Diagnostic radioisotopes retained a 70.33% share of the nuclear medicine radioisotopes market in 2025, which reflected the large and established procedure base for routine nuclear imaging. This lead rested on the daily role of Tc-99m in hospital and imaging center workflows, where access, familiarity, and reimbursement are more mature than in newer therapeutic pathways. Japan's Atomic Energy Commission noted in December 2024 that Tc-99m supports nearly 60% of SPECT procedures, which shows how deeply diagnostic use remains embedded in clinical practice[3]Japan Atomic Energy Commission, “Medical RI Situation and Challenges,” AEC Proceedings, aec.go.jp. The diagnostic side of the nuclear medicine radioisotopes industry also benefits from broad application diversity because the same supply base serves cardiology, oncology, neurology, and thyroid imaging. That breadth keeps diagnostic demand more stable across health systems than treatment categories that are still building center-level expertise and treatment slots.

Therapeutic radioisotopes are forecast to grow at a 12.99% CAGR through 2031 in the nuclear medicine radioisotopes market, which makes them the faster-moving side of the product mix. Lu-177 remains the commercial anchor because it has already moved from pipeline promise into scaled revenue generation and wider treatment use. Novartis reported that Pluvicto generated USD 642 million in Q1 2026 revenue, up 70% year on year at constant currency, and combined 2025 revenue from Pluvicto and Lutathera reached USD 2.8 billion. That revenue profile matters because it supports further investment in isotope production, treatment center readiness, and radiolabeling capacity across the nuclear medicine radioisotopes market. Research published in Annals of Nuclear Medicine also pointed to Terbium-161 as a promising future option, which suggests that therapeutic breadth may expand beyond the current commercial leaders during the forecast period.

By Application: Oncology Leads While Other Clinical Uses Continue to Build

Oncology accounted for 45.75% of the nuclear medicine radioisotopes market size in 2025, which made it the largest application area by a clear margin. That position came from the combined use of diagnostic agents such as PSMA-PET and FDG-PET and therapeutic options such as radioligand therapy and somatostatin receptor-targeted treatment. The oncology profile of the nuclear medicine radioisotopes market is reinforced by strong clinical validation in prostate cancer and neuroendocrine tumors, where molecular targeting has already shaped care pathways. It also benefits from the fact that cancer treatment pathways often include serial imaging and response monitoring, which supports recurring isotope demand rather than one-time use. This kept oncology at the center of the nuclear medicine radioisotopes market in 2025 and will likely preserve its leadership through the forecast period.

Cardiology remained a major volume contributor in the nuclear medicine radioisotopes market because myocardial perfusion SPECT and Rb-82 PET continue to serve routine clinical decision-making in large patient populations. Neurology is gaining more strategic importance because amyloid and tau imaging are moving deeper into memory disorder assessment pathways and are becoming more aligned with clinical practice guidance. That broadening use case matters because it allows the nuclear medicine radioisotopes market to grow from new clinical pathways without relying only on further oncology penetration. Thyroid disorders remain a stable and mature use area, with demand shaped by established referral patterns and long-standing treatment protocols. Other applications, including infection imaging and pulmonology, remain smaller but give the nuclear medicine radioisotopes market room to diversify its future demand base. The practical result is that oncology remains dominant today, while adjacent applications are gradually widening the procedural and commercial base of the market.

By Source: Co-Production Is Changing the Supply Mix

Reactor-produced isotopes held 37.69% share in 2025, which kept them as the largest source category in the nuclear medicine radioisotopes market. This position reflected the long-standing role of reactors in Mo-99, Tc-99m, and several therapeutic isotope routes that already serve commercial volume. Reactor infrastructure still anchors the supply base for the nuclear medicine radioisotopes market because many hospitals and radiopharmacies were built around those established flows. At the same time, the category now faces more pressure to prove resilience and cost efficiency as newer production models move beyond pilot scale. That shift is making source diversification a more visible factor in purchasing and partnership decisions across the nuclear medicine radioisotopes market.

Power-reactor co-production is projected to expand at a 13.29% CAGR through 2031, which makes it the fastest-growing source in the nuclear medicine radioisotopes market. Darlington's entry into commercial isotope output is central here, with Y-90 production beginning in 2026 and distribution planned across more than 30 countries through BWXT Medical. Cyclotron production remains essential for PET imaging and is also becoming more efficient, with an automated in-house F-18-NaF method reporting radiochemical yield of at least 97% through a disposable-kit workflow. LINAC-based production continues to develop for selected isotopes, while generator systems remain important for Ga-68 access and future multi-isotope planning. Eckert and Ziegler's June 2026 opening of its Jintan site for Ge-68, with Ac-225 planned in a later phase, showed that suppliers are building source platforms that can serve several isotopes instead of relying on a single product line.

By End-User: Private Providers Lead Adoption While Public Systems Shape Scale

The private sector held 54.67% of the nuclear medicine radioisotopes market share in 2025, which gave it the lead among end users. That lead reflected earlier investment by private hospitals, oncology clinics, and imaging centers in PET/CT systems, radiopharmacy workflows, and theranostic service lines. The private side of the nuclear medicine radioisotopes market often moves faster because procurement cycles are shorter and pricing flexibility is greater when a center is adding a high-value treatment pathway. Telix reported in Q1 2026 that Illuccix was commercially available in 21 countries, with 16 European launches, which shows how quickly private-capable networks can extend imaging access once regulatory approvals are in place. This operating model helped private providers establish an early lead in the nuclear medicine radioisotopes market before many public systems completed reimbursement and capacity adjustments.

The private sector is also projected to grow at an 11.26% CAGR through 2031, which keeps it as both the largest and fastest-moving end-user category in the nuclear medicine radioisotopes market. Public institutions still matter deeply because they shape coverage decisions, referral norms, and national treatment adoption pathways that can later drive higher volume for the whole market. France Biotech stated in June 2025 that public hospital networks are central to national radioligand therapy adoption and that isotope production is being treated more like a strategic capability. Japan's Atomic Energy Commission also highlighted stronger Lu-177 demand after health insurance coverage began, which shows how public reimbursement can build durable treatment pipelines. In practice, the nuclear medicine radioisotopes market grows faster when private centers introduce new services early and public systems later normalize reimbursement and patient access at scale.

Geography Analysis

North America held 37.33% of the nuclear medicine radioisotopes market share in 2025, which kept it as the leading regional market. The region benefits from dense PET and SPECT infrastructure, broad reimbursement support, and stronger clinical readiness for both imaging and radioligand therapy. Canada adds an important supply layer because Darlington begins commercial Y-90 production in 2026 and is expected to add Lu-177 from 2027, with planned distribution to more than 30 countries. The North American position in the nuclear medicine radioisotopes market is also shaped by ongoing domestic manufacturing investment and by efforts to reduce reliance on imported inputs. At the same time, medical societies have urged the U.S. administration to delay radiopharmaceutical tariffs until domestic supply is better established, which shows that trade policy still poses a near-term planning risk for the region.

Europe remained the second-largest regional market in the nuclear medicine radioisotopes market, supported by mature imaging infrastructure and several established isotope suppliers. The region combines strong clinical usage with an industrial base that still plays a major role in global supply continuity. Belgium's BR2 reactor reached a record level in 2025 by helping 13 million patients worldwide, which showed the scale that individual European facilities can deliver. Curium and NRG PALLAS extended their collaboration in May 2025 to maintain essential isotope supply, which reflected the continued need for planned continuity during the infrastructure transition period. France is also treating nuclear medicine as a strategic area, with France Biotech calling for stronger domestic isotope capabilities and coordinated support for radioligand therapy expansion.

Asia-Pacific is forecast to grow at a 10.87% CAGR through 2031, making it the fastest-growing region in the nuclear medicine radioisotopes market. The region is advancing through infrastructure buildout, a rising disease burden, and gradually improving reimbursement support across major healthcare systems. Japan has already moved Lu-177-PSMA therapy into national coverage and is also pushing for domestic Ac-225 capability under its economic security framework, which supports both treatment demand and supply planning. In China, SHINE and C-Ray Therapeutics formed an exclusive mainland distribution partnership for no-carrier-added Lu-177 in March 2026, which highlighted the importance of supply access in regional growth. Eckert and Ziegler also opened its Jintan production site in June 2026, reinforcing the view that Asia-Pacific is becoming a priority location for new isotope capacity before demand peaks. Middle East and Africa, along with South America, remain earlier-stage areas where access is still limited by equipment gaps and funding limits, but the WHA78.13 reporting framework creates a formal path for gradual capacity development through 2031.

Competitive Landscape

The nuclear medicine radioisotopes market shows moderate concentration, with Curium, Eckert & Ziegler Radiopharma, Cardinal Health, Telix Pharmaceuticals, and others forming a leading supplier group across several isotope classes. Competitive strength in the nuclear medicine radioisotopes market is increasingly tied to vertical integration rather than to reactor access alone. Producers that can combine isotope sourcing, radiolabeling, dose processing, and distribution are in a better position to serve both routine imaging demand and higher-value therapeutic programs. This is why supply security, manufacturing depth, and partnership reach are becoming the main differentiators across the nuclear medicine radioisotopes market.

Cardinal Health expanded Ac-225 production at its Indianapolis Center for Theranostics Advancement in April 2026 and reported that weekly output had quadrupled since routine production began at the end of 2024. The company also filed new Drug Master Files for cGMP-compliant Ac-225 in multiple countries, which gives it a stronger regulatory position as targeted alpha therapy programs advance. NorthStar confirmed routine commercial-scale Ac-225 production in January 2026 and followed with a May 2026 partnership with QSA Global to secure Ra-226 target supply, addressing one of the most upstream bottlenecks in the chain. Those moves show that competition in the nuclear medicine radioisotopes market is now extending further upstream into precursor control and compliance readiness. They also show that the market is being shaped by companies that are willing to lock in feedstock before demand fully matures.

Telix acquired RLS Radiopharmacies for USD 230 million in January 2025 and then selected 4 IBA Cyclone KIUBE cyclotrons in March 2026 to support U.S. manufacturing expansion, which strengthened its in-house delivery model. Telix also entered a strategic radiopharma collaboration with Regeneron in April 2026, including USD 40 million upfront for platform access across therapeutic programs. SHINE completed the acquisition of the Lantheus SPECT business in January 2026 and later received a conditional USD 263 million U.S. Department of Energy loan commitment for domestic isotope manufacturing using fusion technology. These moves indicate that the nuclear medicine radioisotopes market is rewarding companies that can secure long-horizon supply while also building direct market access through integrated operating platforms.

Nuclear Medicine Radioisotopes Industry Leaders

Cardinal Health

Curium

Eckert & Ziegler Radiopharma

GE HealthCare

Telix Pharmaceuticals

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Eckert & Ziegler SE and DC Pharma officially opened the Qi Kang Medical Technology isotope production site in Jintan, Changzhou, China, focused initially on Ge-68 (parent isotope for Ga-68 PET diagnostics), with a second phase planned for China's first commercial Ac-225 production facility; commercial Ge-68 production is scheduled to begin in early 2027.

- May 2026: NorthStar Medical Radioisotopes and QSA Global announced a multi-year strategic services agreement securing Ra-226 target supply for NorthStar's commercial-scale Ac-225 production, addressing the most upstream raw-material bottleneck in the targeted alpha therapy supply chain.

- April 2026: Cardinal Health announced a significant expansion of Ac-225 production at its Indianapolis Center for Theranostics Advancement, reporting that weekly output had quadrupled since establishing routine production at end-2024; new Drug Master Files for cGMP-compliant Ac-225 have been filed in multiple countries.

Global Nuclear Medicine Radioisotopes Market Report Scope

As per the scope of the report, nuclear medical radioisotopes are defined as safe radioactive substances that are primarily used in the diagnosis of medical conditions. These radioisotopes, used in a diagnosis, emit gamma rays of energy that are sufficient to escape from the body. The rays also have a short half-life, which is appropriate since the rays can decay as soon as the imaging is completed.

The nuclear medicine radioisotopes market is segmented by type, application, source, end users, and geography. By type of radioisotopes, the market is segmented into diagnostic radioisotopes (Technetium-99m, Fluorine-18, Gallium-68, Iodine-123, Others) and therapeutic radioisotopes (Lutetium-177, Yttrium-90, Iodine-131, Actinium-225, Radium-223, and Others). By application, the market is segmented into oncology, cardiology, neurology, thyroid disorders, and others. By source, the market is segmented into reactor-produced isotopes, cyclotron-produced isotopes, linear accelerator, power-reactor co-production, and generator-produced isotopes. By end users, the market is segmented into hospitals and diagnostic imaging centers. academic & research institutes, and pharmaceutical & biotechnology companies. Geographically, the market is segmented across North America, Europe, the Asia-Pacific region, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Diagnostic Radioisotopes | Technetium-99m (Tc-99m) |

| Fluorine-18 (F-18) | |

| Gallium-68 (Ga-68) | |

| Iodine-123 (I-123) | |

| Copper-64 (Cu-64) | |

| Other Diagnostic Radioisotopes (Carbon-11 and Zirconium-89, among others) | |

| Therapeutic Radioisotopes | Lutetium-177 (Lu-177) |

| Yttrium-90 (Y-90) | |

| Iodine-131 (I-131) | |

| Actinium-225 (Ac-225) | |

| Radium-223 (Ra-223) | |

| Copper-67 (Cu-67) | |

| Other Therapeutic Radioisotopes (Samarium-153 and Holmium-166, among others) |

| Oncology |

| Cardiology |

| Neurology |

| Thyroid Disorders |

| Other Applications (Infection Imaging and Pulmonology, among others) |

| Reactor-produced Isotopes |

| Cyclotron-produced Isotopes |

| Linear Accelerator / LINAC Isotopes |

| Power-reactor Co-production |

| Generator-produced Isotopes |

| Public Sector | Government Hospitals |

| Public Cancer Institutes | |

| Government-funded Diagnostic Centers | |

| Private Sector | Private Hospitals |

| Private Diagnostic Imaging Centers | |

| Specialty Oncology Clinics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Type of Radioisotopes | Diagnostic Radioisotopes | Technetium-99m (Tc-99m) |

| Fluorine-18 (F-18) | ||

| Gallium-68 (Ga-68) | ||

| Iodine-123 (I-123) | ||

| Copper-64 (Cu-64) | ||

| Other Diagnostic Radioisotopes (Carbon-11 and Zirconium-89, among others) | ||

| Therapeutic Radioisotopes | Lutetium-177 (Lu-177) | |

| Yttrium-90 (Y-90) | ||

| Iodine-131 (I-131) | ||

| Actinium-225 (Ac-225) | ||

| Radium-223 (Ra-223) | ||

| Copper-67 (Cu-67) | ||

| Other Therapeutic Radioisotopes (Samarium-153 and Holmium-166, among others) | ||

| By Application | Oncology | |

| Cardiology | ||

| Neurology | ||

| Thyroid Disorders | ||

| Other Applications (Infection Imaging and Pulmonology, among others) | ||

| By Source | Reactor-produced Isotopes | |

| Cyclotron-produced Isotopes | ||

| Linear Accelerator / LINAC Isotopes | ||

| Power-reactor Co-production | ||

| Generator-produced Isotopes | ||

| By End-user | Public Sector | Government Hospitals |

| Public Cancer Institutes | ||

| Government-funded Diagnostic Centers | ||

| Private Sector | Private Hospitals | |

| Private Diagnostic Imaging Centers | ||

| Specialty Oncology Clinics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the 2026 value and 2031 outlook for nuclear medicine radioisotopes?

The nuclear medicine radioisotopes market stands at USD 8.09 billion in 2026 and is forecast to reach USD 13.12 billion by 2031 at a 10.17% CAGR.

Which product category is growing fastest in this space?

Therapeutic radioisotopes are growing fastest, with a forecast CAGR of 12.99% through 2031, even though diagnostic radioisotopes still held the larger 70.33% share in 2025.

Why does oncology account for the largest use of these isotopes?

Oncology held 45.75% in 2025 because the same care pathway often uses both molecular imaging and targeted radionuclide treatment, especially in prostate and neuroendocrine cancer settings.

Which region currently leads and which one is expanding fastest?

North America led with 37.33% share in 2025, while Asia-Pacific is projected to expand fastest at a 10.87% CAGR through 2031.

What is changing on the supply side for Lu-177, Y-90, and Ac-225?

Supply is shifting toward vertically integrated models, power-reactor co-production, and tighter control of precursor materials, with new moves from OPG, Cardinal Health, NorthStar, SHINE, Telix, and Eckert and Ziegler.

What are the main risks holding back wider adoption?

The main constraints are short half-lives, complex just-in-time logistics, waste handling demands, and continued reliance on aging reactor infrastructure for parts of the supply chain.

Page last updated on: