Military Aircraft Collision Avoidance Systems Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

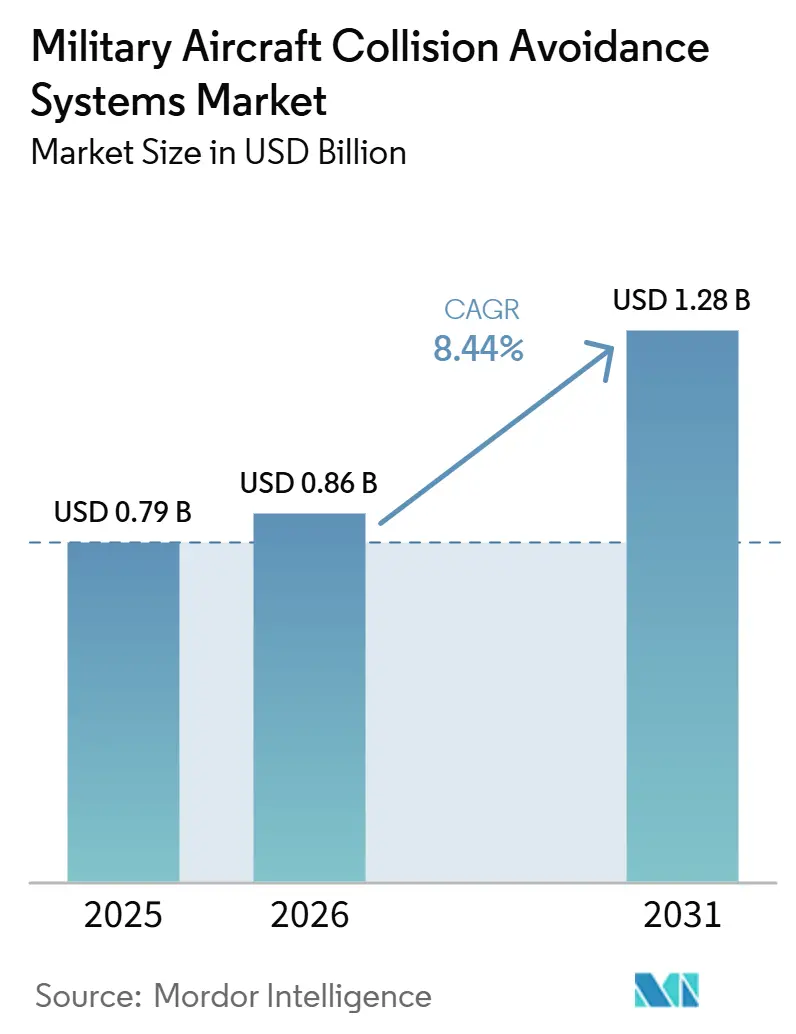

| Market Size (2026) | USD 0.86 Billion |

| Market Size (2031) | USD 1.28 Billion |

| Growth Rate (2026 - 2031) | 8.28% CAGR |

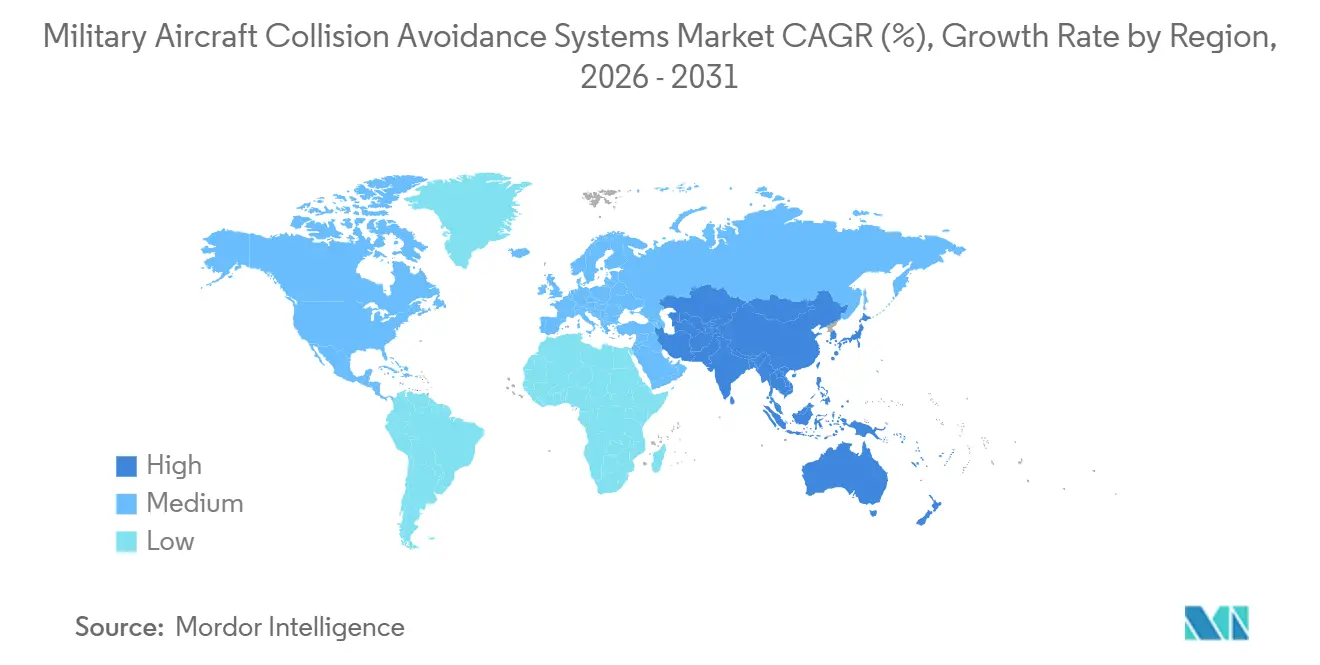

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

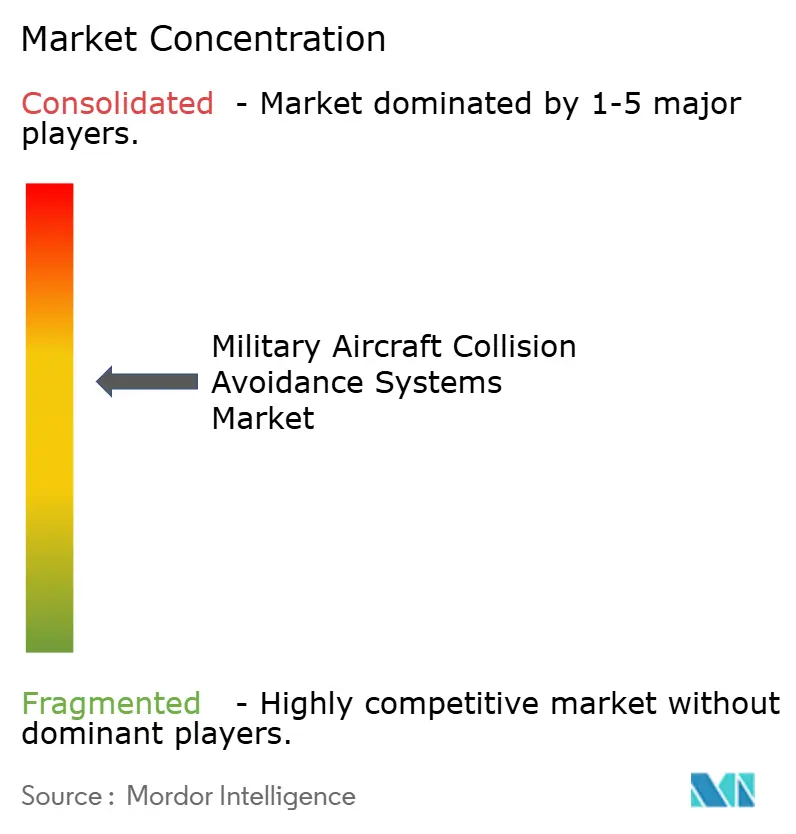

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Military Aircraft Collision Avoidance Systems Market Analysis by Mordor Intelligence

The military aircraft collision avoidance systems market size in 2026 is estimated at USD 856.68 million, up from the 2025 value of USD 790 million, with projections to USD 1.28 billion in 2031, growing at an 8.28% CAGR over 2026-2031. This expansion is propelled by mandatory upgrades to TCAS II v7.1, rapid integration of unmanned aerial vehicles (UAVs), and growing demand for predictive threat management in contested airspace. Increasing defense allocations in North America, large fighter acquisition programs in the Asia-Pacific, and rising multi-domain operations worldwide sustain spending momentum. Hardware miniaturization that enables 4D AESA radar array and AI-driven sensor fusion reshapes product design by shifting systems from reactive alerting to anticipatory avoidance. The aftermarket’s faster growth underscores the urgency of modernizing legacy fleets ahead of compliance deadlines. At the same time, supply constraints on gallium nitride (GaN) radio-frequency devices and spectrum congestion create both risks and opportunities for suppliers innovating in passive and non-cooperative detection methods.

Key Report Takeaways

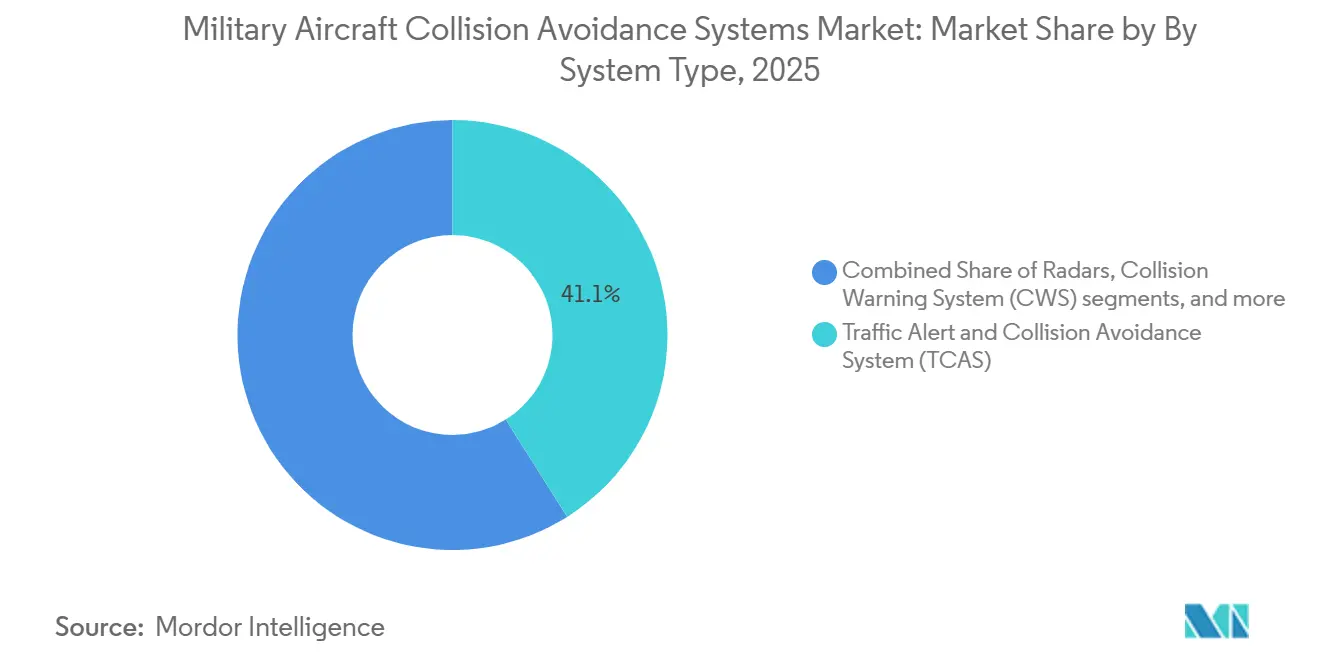

- By system type, TCAS held 41.05% of the military aircraft collision avoidance systems market share in 2025; the segment is forecast to grow at a 9.03% CAGR through 2031.

- By platform, manned aircraft accounted for 78.92% share of the military aircraft collision avoidance systems market size in 2025, whereas UAVs are projected to grow at a 9.31% CAGR over the forecast period.

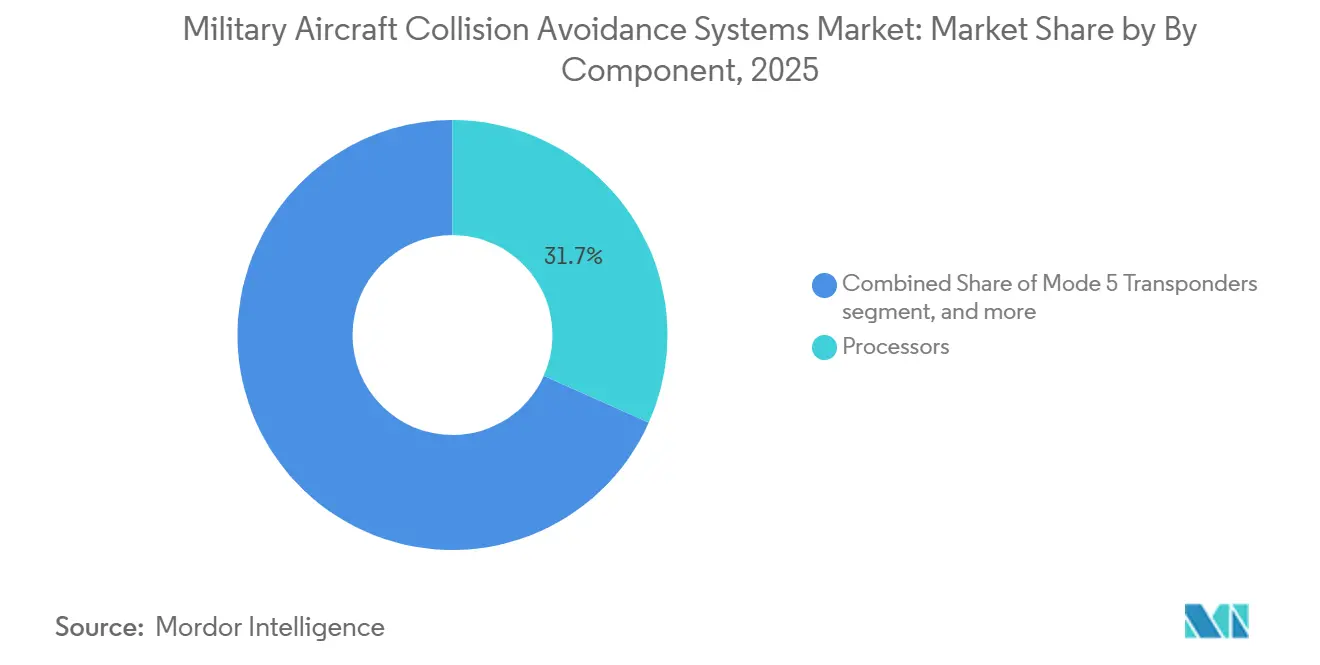

- By component, processors captured 31.68% of revenue in 2025, while antennas and sensors are set to grow at a 9.41% CAGR through 2031.

- By end user, OEM installations commanded a 53.64% share in 2025, while the aftermarket segment is expected to grow at a 9.60% CAGR through 2031.

- By geography, North America led with a 40.78% share in 2025; Asia-Pacific is anticipated to be the fastest-growing region at a 9.76% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Military Aircraft Collision Avoidance Systems Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising defense spending and new aircraft procurement | +1.50% | Global, concentrated in North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Mandatory compliance with TCAS II v7.1 and ACAS-X standards | +1.20% | NATO members and allied nations | Short term (≤ 2 years) |

| Advancements in miniaturized 4D AESA radar and AI-based sensor fusion | +1.10% | North America, Europe, advanced Asia-Pacific markets | Long term (≥ 4 years) |

| Deployment of ground-based BVLOS sense-and-avoid (SAA) networks | +1.00% | North America, Europe, and select Asia-Pacific countries | Medium term (2-4 years) |

| Surge in UAV acquisitions requiring detect-and-avoid capabilities | +0.80% | Asia-Pacific and North America | Medium term (2-4 years) |

| Increasing need for manned-unmanned teaming (MUM-T) interoperability | +0.90% | North America, Europe, with spillover to allied nations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Defense Spending and New Aircraft Procurement

Escalating global defense outlays shape the primary demand curve for the military aircraft collision avoidance systems market. The US Indo-Pacific Command allocates substantial funding to new tactical air platforms that integrate avoidance capability at the design stage, reducing retrofit complexity later. India’s 114-fighter tender embeds collision avoidance as a baseline avionics requirement, cementing supplier pipelines for processors, sensors, and secure transponders. High-value procurement contracts bundle collision-avoidance upgrades with open-systems architectures, enabling continued capability insertion throughout the fleet life cycle. The spending uptrend, spanning fighters, transports, and special-mission aircraft, tilts revenue growth toward suppliers capable of quickly certifying modular, multi-function packages. Procurement agencies also emphasize commonality to reduce training and sustainment costs, thereby creating follow-on opportunities for software-defined upgrades after initial delivery.

Mandatory Compliance with TCAS II v7.1 and ACAS-X Standards

Regulatory obligations convert avoidance upgrades from discretionary to non-negotiable investments. TCAS II v7.1 requires new threat-resolution logic and Mode S surveillance performance, often forcing complete line-replaceable unit swaps rather than firmware patches. Rotary-wing fleets need altitude-inhibition waivers or specialized low-altitude variants, adding complexity and certification fees. NATO STANAG 4193 interoperability mandates encrypted Mode 5 identification that tightly couples IFF transponders with collision-avoidance computations.[1]Company Release, “Identification Friend or Foe (IFF),” HENSOLDT, hensoldt.net Certification bottlenecks concentrate demand among a handful of approved suppliers, heightening price pressure yet reinforcing long-term aftermarket revenue as fleets queue for installation slots. Operators unable to meet 2027 compliance cut-offs risk grounding, underscoring the short-term acceleration in contract awards.

Surge in UAV Acquisitions Requiring Detect-and-Avoid Capabilities

The accelerating UAV portfolio, from Group 1 quad-rotors to HALE reconnaissance systems, is driving new technical requirements across the industry. Autonomous UAVs lack onboard pilots, so detect-and-avoid algorithms must classify threats and command evasive maneuvers without latency. US Marine Corps evaluations of Collaborative Combat Aircraft highlight the need for shared threat pictures between manned and unmanned wingmen. Cooperative surveillance remains unreliable in GNSS-denied zones, pushing industry toward multi-sensor fusion that blends radar, electro-optics, and passive RF mapping. Suppliers focusing on lightweight AESA arrays and edge-computing processors tap into the swiftly expanding UAV retro- and forward-fit market, raising the proportion of software revenue as fleets adopt periodic AI model refresh cycles.

Advancements in Miniaturized 4D AESA Radar and AI-Based Sensor Fusion

Rapid strides in G device manufacturing allow centimeter-class T/R modules that pack 4D imaging functionality into small form factors suitable for fighters and tactical UAVs. India’s Virupaksha radar exemplifies dual-use sensor architectures that merge air-to-air targeting with collision-avoidance mapping in a single LRU. On the processing side, Honeywell’s integration of NXP S32N processors enables real-time neural-network inference at lower thermal loads. AI-enabled sensor fusion shifts avoidance from reactive audio alerts to predictive trajectory management, offering value-added upgrades even to TCAS-compliant aircraft. Higher processing demand calls for enhanced power-thermal management, driving secondary opportunities in environmental control systems and aircraft electrical subsystems.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Radio frequency spectrum congestion affecting cooperative systems | -1.10% | Europe, North America, and dense military operation zones | Medium term (2-4 years) |

| High retrofit and certification costs for legacy military fleets | -0.70% | Global, particularly affecting budget-constrained militaries | Short term (≤ 2 years) |

| Risk of GNSS jamming disrupting collision avoidance algorithms | -0.60% | Global, with heightened risk in contested regions | Short term (≤ 2 years) |

| Supply chain limitations for GaN-based RF devices | -0.40% | Global, with particular impact on advanced radar systems | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Retrofit and Certification Costs for Legacy Military Fleets

Aging aircraft often lack spare weight, power, and space margins, so installing next-generation processors or antenna suites demands structural rewiring, rack redesign, and extensive ground-test cycles. Certification authorities require flight-safety evidence for each airframe-unique installation, prolonging test campaigns and inflating the cost per tail. Budget-constrained operators delay upgrades, stretching compliance grace periods and dampening near-term demand curves. Suppliers respond with plug-and-play kits that fit existing avionics bays, but unit pricing remains high due to one-off engineering and limited production volumes. The retrofit burden tempers overall market velocity even as it guarantees a longer revenue tail in technical services and spares.

Radio Frequency Spectrum Congestion Affecting Cooperative Systems

Crowded 1030/1090 MHz channels degrade the integrity of TCAS interrogation-reply, especially near major exercise corridors and joint-civil air routes. European EMIT data records increasing numbers of synchronous garbage events that delay threat-resolution computations.[2]Company Release, “HENSOLDT Passive Radar to Be Used in Civil Aviation,” HENSOLDT, hensoldt.net 5G telecommunications rollouts encroach on neighboring frequency bands, creating additional interference. Military planners explore passive radar that piggybacks on satellite broadcast illuminators, lowering spectrum emissions while maintaining situational awareness. Adoption remains limited because passive sensors trade responsiveness for stealth, raising doctrinal debates on acceptable risk thresholds. Suppliers must juggle investment between cooperative and non-cooperative technologies, heightening R&D spending and compressing margins.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By System Type: TCAS Leads Modernization Wave

The TCAS segment accounted for 41.05% of the military aircraft collision avoidance systems market in 2025 and is projected to grow at a 9.03% CAGR through 2031. Mandatory v7.1 upgrades drive complete hardware refreshes, lifting demand for processors with larger computational margins. TAWS remains relevant for low-altitude helicopter operations, while synthetic vision systems blend multiple sensor feeds into 3D cockpit displays that enhance pilots' situational awareness beyond simple alerting.

Replacement cycles gain momentum because operators find that installing advanced processors and Mode 5-capable transponders deliver cost synergies when bundled with broader avionics modernization. Cooperative logic within TCAS now integrates with onboard electronic warfare self-protection suites, enabling real-time deconfliction between mission maneuvers and collision avoidance. Manufacturers that certify such integrated packages capture higher-margin streams as customers prioritize holistic upgrades that ensure compliance without compromising combat capability.

By Platform: UAVs Challenge Manned Dominance

Manned aircraft platforms accounted for 78.92% of the military aircraft collision avoidance systems market share in 2025, but UAVs are expected to deliver the fastest 9.31% CAGR to 2031. Fighter programs embed collision-avoidance logic within mission computers to minimize cockpit workload during high-G maneuvers, whereas large transports emphasize system reliability and integration with flight-management computers.

Unmanned platforms force suppliers to adopt edge AI processors that run avoidance logic locally, eliminating latency in datalink-dependent decision loops. MUM-T concepts require standardized threat-data schemas so that piloted aircraft and UAVs share situational awareness without saturating communications bandwidth. The focus on the MUM-T concept drives the development of compressed data formats and standard application programming interfaces, creating a niche for software vendors specializing in middleware bridging legacy avionics and next-generation autonomous cores.

By Component: Sensors Drive Innovation

Processors accounted for 31.68% of revenue in 2025, yet antennas and sensors are poised to post the highest CAGR, at 9.41%, through 2031 as miniaturized AESA arrays become the linchpin of non-cooperative detection. The military aircraft collision avoidance systems market size for the antenna-sensor cluster is forecast to expand as suppliers leverage advanced GaN fabrication to enhance range and field of view without increasing the aperture footprint.

Component makers invest significantly in cryptographically secure Mode 5 transponders to satisfy NATO mandates, while display vendors transition from textual advisories to augmented-reality overlays projected onto helmet-mounted sights. This evolution of human-machine interfaces shortens reaction times and harmonizes collision-avoidance alerts with other tactical cues. Suppliers offering integrated sensor-processor packages gain a competitive edge because bundled certification accelerates aircraft-level qualification.

By End User: Aftermarket Accelerates

OEM installations captured a 53.64% share in 2025, but the aftermarket is set to grow faster at a 9.60% CAGR. Legacy fleets parked decades of service life ahead, particularly transport and special-mission aircraft, present sizable revenue pools for retrofit kits that bring systems up to TCAS II v7.1 and Mode 5 standards. The military aircraft collision avoidance systems market benefits from maintenance depots scheduling fleet-wide modification blocks aligned with heavy checks, ensuring high installation density per maintenance slot.

Aftermarket providers differentiate through turnkey packages that include engineering drawings, parts provisioning, and on-site technical support. Modular open-systems architectures are gaining traction because they future-proof fleets against rapidly evolving sensor technology, lowering the total cost of ownership. Contracts often incorporate software sustainment clauses that guarantee periodic updates, adding annuity streams for suppliers with strong field-support networks.

Geography Analysis

North America dominated the military aircraft collision avoidance systems market in 2025 with 40.78% revenue share. The US Department of Defense (DoD) modernization budgets fund large-scale upgrades to fighters, rotorcraft, and tankers, each of which requires compliant avoidance subsystems. Canada's Future Fighter Capability Project similarly stipulates Mode 5 identification and collision-avoidance alignment at initial delivery, reinforcing demand for integrated solutions.

Europe maintains balanced growth as NATO standardization initiatives push members toward identical avoidance logic and encrypted transponders. Collaborative programs such as the Eurodrone and the Future Combat Air System (FCAS) embed collision-avoidance requirements, sustaining a steady backlog for prime contractors. Spectrum congestion concerns drive regional interest in passive radar technology, and suppliers partnering with air navigation service providers accelerate certification for dual-civil-military use cases.

Asia-Pacific is the fastest-growing region, with a 9.76% CAGR, driven by substantial aircraft procurement in India, South Korea, Japan, and Australia. Due to export-control barriers, China's domestic demand remains significant but inward-focused, prompting indigenous sensor development. ASEAN nations invest in ground-based beyond-visual-line-of-sight (BVLOS) networks that complement airborne systems, extending collision-avoidance coverage over dispersed archipelagic territories. These factors collectively expand the region's military aircraft collision-avoidance systems market footprint, attracting Western and local suppliers to enter joint ventures to navigate offset requirements and technology-transfer rules.

Competitive Landscape

The military aircraft collision avoidance systems market exhibits moderate concentration. Honeywell Aerospace Inc., Collins Aerospace (RTX Corporation), Thales Group, Lockheed Martin Corporation, and Leonardo S.p.A. leverage large installed bases, proprietary sensor fusion algorithms, and certification track records to defend their share. Honeywell’s USD 1.9 billion acquisition of CAES expanded its RF and processing portfolio, enabling end-to-end packages that unite collision-avoidance, electronic warfare, and communications modules in common form factors.[3]Company Release, “Honeywell Completes Acquisition of CAES,” Honeywell Aerospace, honeywell.com Collins Aerospace’s multi-year contract for UH-60M modular open-systems architecture illustrates competition centered on scalability and lower life-cycle cost.

Emerging firms focus on radar miniaturization and AI-based non-cooperative detection, particularly for UAV traffic. Partnerships between start-ups and primes proliferate because niche innovators need access to certified production lines, while incumbents seek fresh IP to accelerate product cycles. Competitive intensity rises in the sensor domain, where GaN shortages pressure margins; suppliers with vertically integrated semiconductor lines mitigate risk and secure schedule certainty, winning preference in fixed-price tenders.

Supplier strategies increasingly revolve around software update ecosystems that treat avoidance algorithms like subscription content. This pivot aligns revenue with fleet digital modernization trends and protects incumbents against hardware commoditization. Market entrants that provide open-source libraries risk intellectual property leakage but gain adoption speed, underscoring the divergent business models in the military aircraft collision-avoidance systems industry.

Military Aircraft Collision Avoidance Systems Industry Leaders

Honeywell Aerospace Inc.

Lockheed Martin Corporation

Thales Group

Leonardo S.p.A.

Collins Aerospace (RTX Corporation)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Taiwan announced that it will begin upgrading its F-16V fleet with an Automatic Ground Collision Avoidance System (Auto-GCAS) in July 2026, followed by hardware upgrades in September 2026. The system uses flight data to help prevent crashes and is scheduled for full installation across all jets by the end of 2028.

- July 2025: The US and the UK announced plans to develop a safety system for the F-35 Lightning II to prevent midair collisions between military and civilian aircraft.

- November 2022: Honeywell International Inc. signed a memorandum of understanding (MoU) with PT Dirgantara Indonesia (PTDI), Indonesia's state-owned aircraft manufacturer, to supply the Indonesian Air Force with its military airborne collision avoidance system (MILACAS). MILACAS has a 100 nm surveillance range in all azimuths and uses improved interrogation methods and hybrid surveillance (ADS-B).

Global Military Aircraft Collision Avoidance Systems Market Report Scope

Military aircraft collision avoidance systems help defense operators mitigate the risk of mid-air collisions and prevent collisions with terrain. These systems integrate automated transponders, advanced radar sensors, and computerized processing to identify conflicting flight paths. They deliver preventive alerts and real-time resolution advisories, enabling flight crews to maintain safe airspace separation and support mission continuity.

The military aircraft collision avoidance systems market is segmented by system type, platform, component, end user, and geography. By system type, the market is segmented into radars, traffic alert and collision avoidance system (TCAS), terrain awareness and warning system (TAWS), collision warning system (CWS), obstacle collision avoidance system (OCAS), and synthetic vision systems. By platform, the market is segmented into manned aircraft and unmanned aerial vehicles (UAVs). By component, the market is segmented into processors, mode 5 transponders, antennas and sensors, and display/warning units. By end-user, the market is segmented into original equipment manufacturer (OEM) and aftermarket. The report also covers the market sizes and forecasts for the military aircraft collision avoidance systems market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| Radars |

| Traffic Alert and Collision Avoidance System (TCAS) |

| Terrain Awareness and Warning System (TAWS) |

| Collision Warning System (CWS) |

| Obstacle Collision Avoidance System (OCAS) |

| Synthetic Vision Systems |

| Manned Aircraft | Combat Aircraft |

| Transport Aircraft | |

| Special Mission Aircraft | |

| Helicopters | |

| Unmanned Aerial Vehicles (UAVs) |

| Processors |

| Mode 5 Transponders |

| Antennas and Sensors |

| Display/Warning Units |

| Original Equipment Manufacturer (OEM) |

| Aftermarket |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By System Type | Radars | ||

| Traffic Alert and Collision Avoidance System (TCAS) | |||

| Terrain Awareness and Warning System (TAWS) | |||

| Collision Warning System (CWS) | |||

| Obstacle Collision Avoidance System (OCAS) | |||

| Synthetic Vision Systems | |||

| By Platform | Manned Aircraft | Combat Aircraft | |

| Transport Aircraft | |||

| Special Mission Aircraft | |||

| Helicopters | |||

| Unmanned Aerial Vehicles (UAVs) | |||

| By Component | Processors | ||

| Mode 5 Transponders | |||

| Antennas and Sensors | |||

| Display/Warning Units | |||

| By End-User | Original Equipment Manufacturer (OEM) | ||

| Aftermarket | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the 2026 value of the military aircraft collision avoidance systems market and how fast is the market expected to grow through 2031?

The military aircraft collision avoidance systems market is valued at USD 856.68 million in 2026 and is projected to reach USD 1.28 billion, growing at an 8.28% CAGR through 2031.

Which system type leads revenue and growth?

TCAS leads with 41.05% share in 2025 and is also the fastest growing at 9.03% CAGR.

Why is the aftermarket segment expanding faster than OEM sales?

Fleet-wide retrofit programs to meet TCAS II v7.1 deadlines push aftermarket growth to a 9.60% CAGR.

Which region will grow the quickest?

Asia-Pacific is forecasted to advance at a 9.76% CAGR because of extensive aircraft procurement and modernization plans.

What is a key technological trend reshaping product design?

Miniaturized 4D AESA radar combined with AI-driven sensor fusion shifts systems from reactive alerts to predictive avoidance.

Page last updated on: