MEMS For Mobile Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

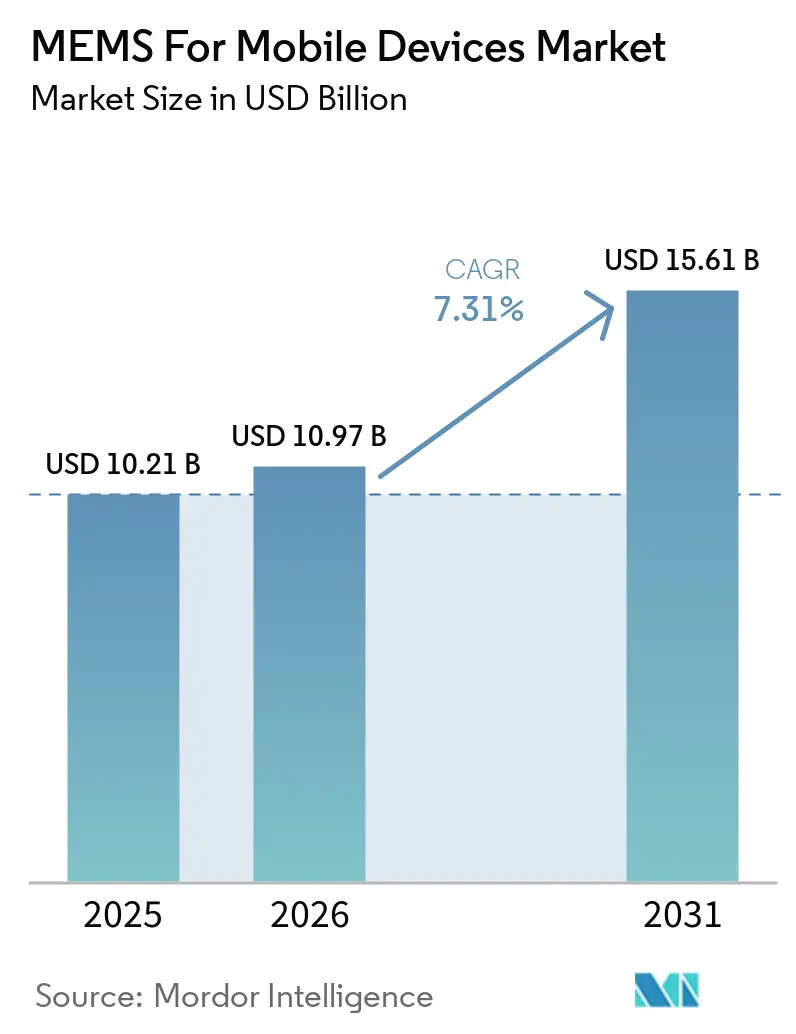

| Market Size (2026) | USD 10.97 Billion |

| Market Size (2031) | USD 15.61 Billion |

| Growth Rate (2026 - 2031) | 7.31% CAGR |

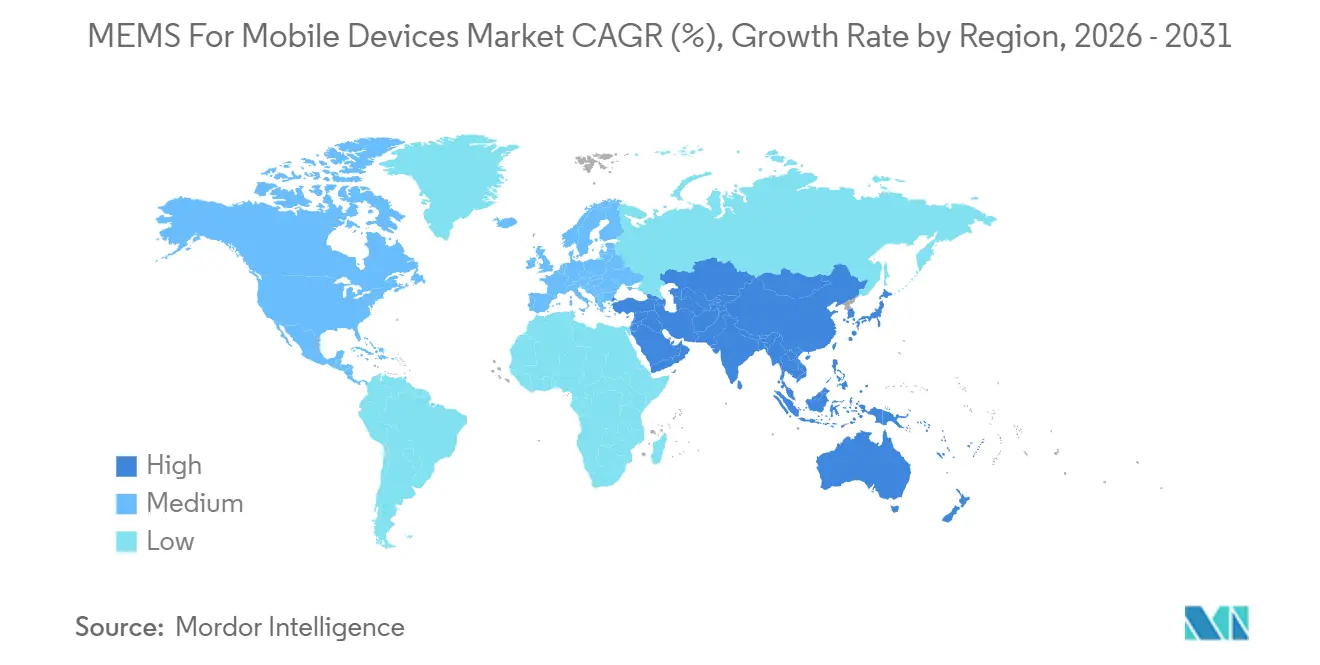

| Fastest Growing Market | Middle East |

| Largest Market | Asia-Pacific |

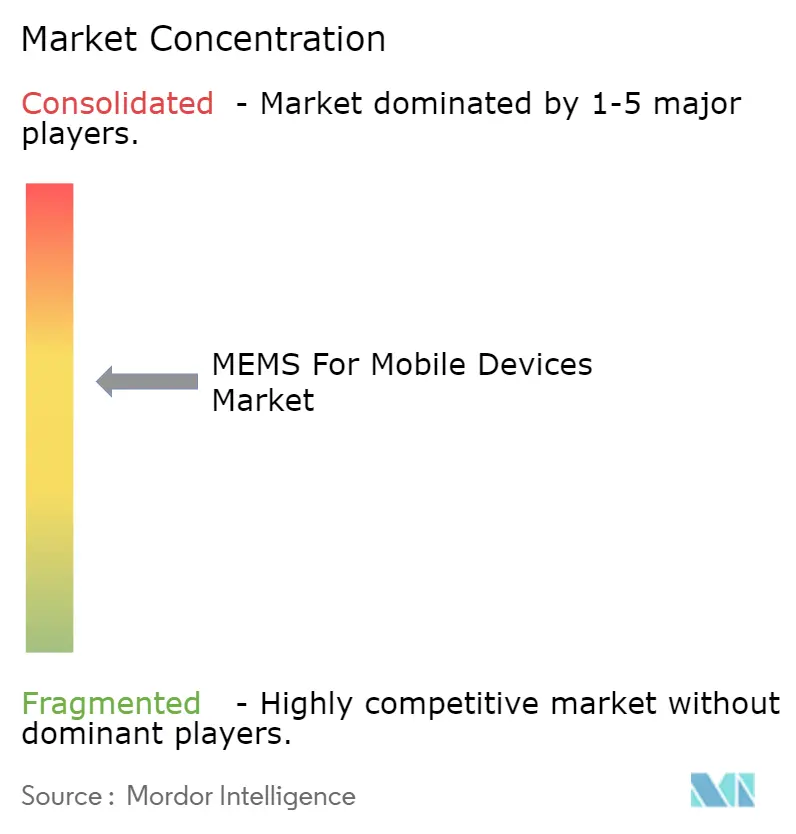

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

MEMS For Mobile Devices Market Analysis by Mordor Intelligence

The MEMS for mobile devices market size is projected to expand from USD 10.21 billion in 2025 and USD 10.97 billion in 2026 to USD 15.61 billion by 2031, registering a CAGR of 7.31% between 2026 to 2031. Device makers are embedding intelligence at the sensor level to meet privacy rules in the European Union and to deliver battery life that now exceeds 48 hours under mixed-use conditions.[1]IEEE Xplore Editors, “Energy-Efficient Sensor Architectures,” ieee.org The shift is accelerating demand for edge-AI sensor hubs that cut continuous power draw by 30%, while the migration to 5G and ultra-wideband is boosting unit volumes of bulk acoustic wave (BAW) filters with quality factors above 3,000. Fingerprint sensors remain the revenue anchor, but hybrid and 3D-stacked packages are gaining ground as hinge modules in foldable phones require 6 × 6-millimeter footprints. Competitive intensity stays high: the five largest vendors shipped more than 60% of 2025 units, yet fabless specialists that master sub-50-femtosecond-jitter timing references continue to win sockets in Wi-Fi 7 and 5G radios.

Key Report Takeaways

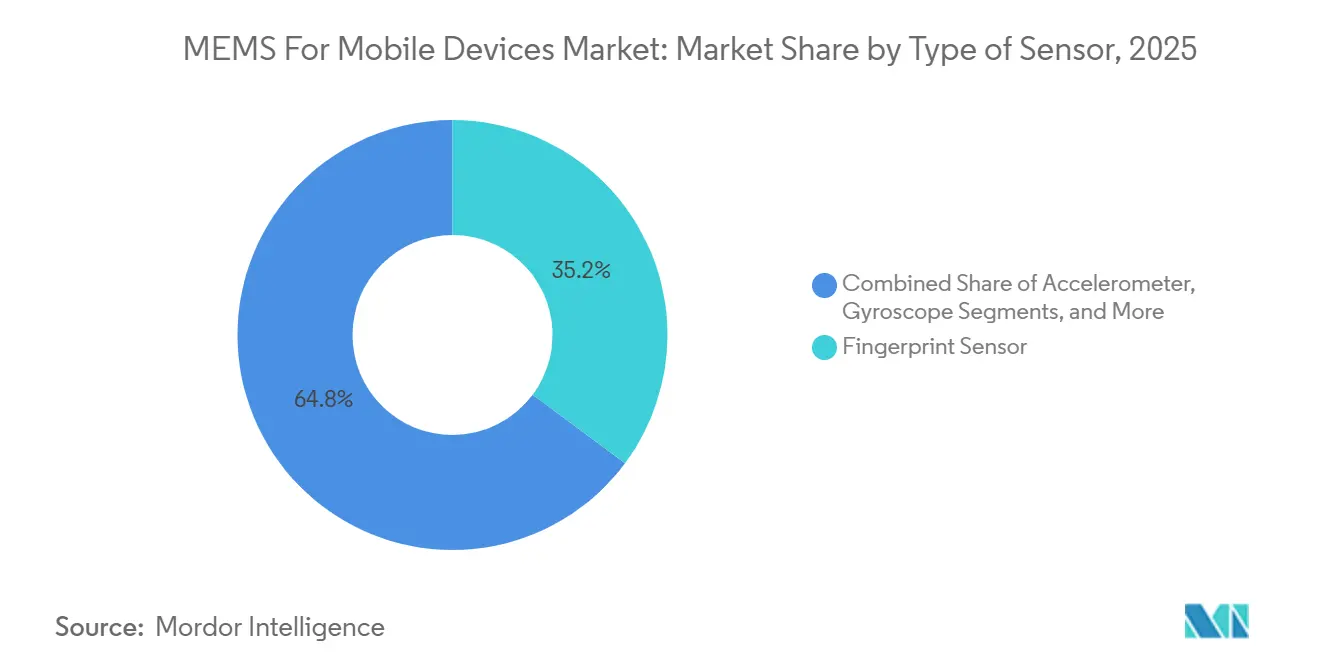

- By type of sensor, fingerprint devices led with 35.21% revenue share in 2025, whereas BAW components are forecast to grow at a 9.32% CAGR through 2031.

- By application, smartphones accounted for 66.41% of shipments in 2025, while wearables are projected to advance at a 7.52% CAGR to 2031.

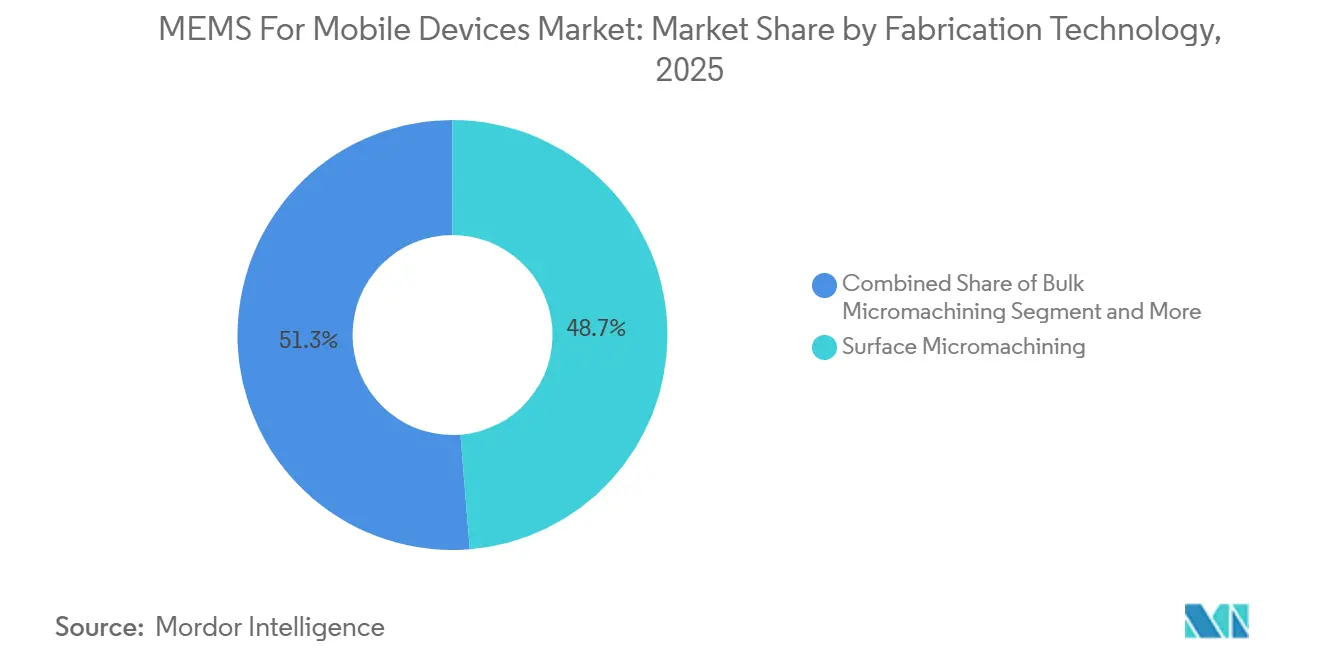

- By fabrication technology, surface micromachining held 48.73% of 2025 revenue, but CMOS-MEMS integration is expected to record a 9.88% CAGR during 2026-2031.

- By integration method, system-in-package captured 41.30% of 2025 deployments, yet hybrids and 3D-stacked configurations are poised to expand at an 8.98% CAGR over the same horizon.

- By geography, Asia-Pacific commanded 46.82% of 2025 value, whereas the Middle East is projected to grow at an 8.36% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global MEMS For Mobile Devices Market Trends and Insights

Drivers Impact Analysis*

| Growing Adoption of 5G and Ultra-Wideband Connectivity | +1.4% | Global, early concentration in North America, China, South Korea | Medium term (2-4 years) |

|---|---|---|---|

| Rising Integration of MEMS in Foldable and Rollable Displays | +0.9% | Asia-Pacific core, spill-over to Europe | Short term (≤ 2 years) |

| Demand for Low-Power Always-On Sensors in AI Edge Processing | +1.6% | Global, led by North America and China AI ecosystems | Medium term (2-4 years) |

| Standardization of Acoustic Zoom and Spatial Audio in Smartphones | +0.8% | Global, premium-tier adoption in North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Surge in Mobile Health and Environmental Sensing Applications | +1.1% | North America and Europe (regulatory approval), Asia-Pacific (volume adoption) | Long term (≥ 4 years) |

| Expansion of CMOS-Compatible MEMS Foundry Ecosystem | +1.2% | Asia-Pacific (Taiwan, China), North America (advanced nodes) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of 5G and Ultra-Wideband Connectivity

Millimeter-wave radios need BAW filters with insertion loss below 1.5 dB and temperature coefficients under 25 ppm/°C, thresholds that piezoelectric thin-film resonators meet at high volume.[2]David Aichele, “5G BAW Filters for Handsets,” Qorvo Technical White Paper, qorvo.com Qualcomm’s Snapdragon 8 Elite integrates ultra-wideband co-processors that trim power by 40%, enabling centimeter-level indoor positioning for augmented-reality services. These architectures depend on MEMS timing references providing phase-noise floors below -160 dBc/Hz at a 1 MHz offset, a metric unattainable by similarly sized quartz parts. Europe’s recent spectrum auctions in the 3.4-3.8 GHz range triggered handset replacement cycles because legacy 4G filters cannot contain adjacent-channel interference in dense cells. The convergence of 5G and ultra-wideband is also enabling cross-platform applications, such as smartphone-driven keyless entry systems for vehicles. The MEMS for mobile devices market, therefore, benefits directly from every new mid-band or millimeter-wave launch worldwide.

Rising Integration of MEMS in Foldable and Rollable Displays

Flexible form factors endure more than 100,000 bends at radii below 5 mm, forcing sensor placement inside the display stack instead of on rigid boards.[3]Samsung Display R&D Team, “Sensor OLED White Paper,” samsungdisplay.com Samsung’s Sensor OLED embeds organic photodiodes beneath each pixel to collect fingerprint and heart-rate data, pushing screen-to-body ratios beyond 95%. BOE shipped its first rollable OLED panels with integrated pressure sensors in Q3 2024, allowing interfaces that differentiate taps from palm contact. Such designs demand polyimide-compatible MEMS processes operating below 250 °C and favor thin-film piezoelectric materials over silicon-on-insulator, widening the material toolkit used in the MEMS for mobile devices market. Panel makers are capturing value that once flowed to discrete sensor vendors, compelling traditional suppliers to specialize in ultrathin die bonding and laser lift-off services.

Demand for Low-Power Always-On Sensors in AI Edge Processing

Routing raw accelerometer streams to a CPU consumes 10-15 mW continuously, while embedded finite-state machines draw under 1 mW and wake the host only on anomalies. STMicroelectronics’ LSM6DSV32X, unveiled at CES 2026, classifies 16 gestures locally and extends smartwatch standby life by 30%. Bosch Sensortec’s BHI360 hub ships with TensorFlow Lite Micro support and can identify audio events, such as glass breaking, in <5 ms. The European Union’s AI Act, effective August 2024, compels biometric identifiers to stay on-device unless users consent, cementing local processing as a default design rule. As a result, demand for intelligent sensor hubs is a structural tailwind lifting the MEMS for mobile devices market through 2031.

Standardization of Acoustic Zoom and Spatial Audio in Smartphones

Premium handsets now ship with four to six matched MEMS microphones to support beamforming that isolates a speaker’s voice amid crowd noise. Apple’s iPhone 15 Pro records spatial audio by pairing cardioid and omnidirectional elements with head-tracking inertial data. The Audio Engineering Society’s March 2025 standard sets a floor of 64 dB SNR and <1% THD, benchmarks met only by backside-ported MEMS microphones. Goertek’s IP68-rated unit retains a 68 dB SNR after 30 minutes under 1.5 m of water, addressing durability gaps for outdoor content creators. As handset brands converge on spatial-audio features, microphone suppliers that can bin arrays with <1 dB sensitivity variance are positioned to gain share within the MEMS for mobile devices market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Yield Losses from Wafer-Level Packaging Defects | -0.7% | Global, acute in high-aspect-ratio MEMS (Asia-Pacific, North America) | Short term (≤ 2 years) |

| Limited Availability of Qualified MEMS Design Engineers | -0.5% | Global, most severe in North America and Europe | Medium term (2-4 years) |

| IP Fragmentation Across Motion, Pressure and Acoustic MEMS | -0.3% | Global, litigation concentrated in North America, Europe, China | Long term (≥ 4 years) |

| Supply-Chain Concentration in Specialty Piezoelectric Materials | -0.4% | Global, dependencies on Japan (sputtering targets), China (rare earths) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Yield Losses from Wafer-Level Packaging Defects

Wafer-level encapsulation lowers unit cost but introduces cavity leaks, particle contamination, and stress-induced cracks that are hard to screen prior to test; field returns can exceed 500 ppm in high-volume mobile programs. ECTC 2024 papers attribute 60% of failures to microcracks created during through-silicon-via reveal steps. Bosch reported scrapping 8% of gyroscope wafers for hermeticity issues, cutting 2025 gross margin by 300 bps. New metrology tools detect subsurface voids but add USD 2-5 million per line and slow inspection by 30%. Although fan-out packages reduce stress, adoption still covers <10% of MEMS volume, prolonging the drag on the MEMS for mobile devices market.

Limited Availability of Qualified MEMS Design Engineers

MEMS design demands fluency in mechanics, electronics, and materials science, a blend taught by fewer than 50 universities worldwide. The U.S. National Science Foundation noted in 2024 that 20% of relevant job postings sat open >90 days, versus 12% for broader semiconductor roles. SEMI forecasts a 1 million-engineer global gap by 2030 with MEMS specialists over-represented. Firms now pay signing bonuses above USD 50,000 to experienced designers, inflating costs as they race to staff projects. Corporate training and university partnerships may ease strain after 2028, yet near-term talent scarcity limits the pace at which the MEMS for mobile devices market can absorb new opportunities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type of Sensor: Biometric Modules Dominate Revenue

Fingerprint units accounted for 35.21% of 2025 income, securing the largest MEMS for mobile devices market share thanks to second-generation ultrasonic solutions that authenticate through wet fingers in 0.3 seconds. The bulk acoustic wave category, although smaller, is advancing at 9.32% annually because each 5G flagship now embeds up to 60 filters spanning 600 MHz to 41 GHz. Accelerometers and gyroscopes together supplied roughly one-quarter of shipments, underpinned by gaming, optical-image stabilization, and indoor navigation. Pressure sensors contributed close to 8%, while MEMS microphones captured 18% as spatial-audio and noise-cancellation became standard in premium devices. Environmental sensing, magnetometers, humidity, gas detectors. made up the remainder and is climbing in pollution-sensitive regions.

Bulk acoustic wave resonators are crossing into precision timing, where their high Q supports oscillators with phase noise below -160 dBc/Hz, displacing quartz in Wi-Fi 7 routers. Fingerprint vendors are experimenting with blood-flow detection that may add continuous heart-rate tracking without extra optics, signaling further overlap among sensing modalities. Such cross-pollination amplifies shipment growth prospects and sustains pricing discipline inside the MEMS for mobile devices market.

By Application: Wearables Set the Growth Pace

Smartphones absorbed 66.41% of 2025 unit demand, reflecting their unrivaled scale. Wearables, however, are forecast to post a 7.52% CAGR, buoyed by FDA-cleared health functions and by smartwatches that now sample motion at 256 Hz for atrial-fibrillation screening. Tablets represented 12% of volume as stylus-pressure sensing broadened creative use cases. Mobile gaming devices comprised roughly 5%, and other gadgets, e-readers, AR glasses filled the balance.

Goertek’s sub-200 µA always-on voice pickup straddles smart-glasses and earbud categories, illustrating how miniaturization unlocks design freedom across applications. Tablets continue to adopt force sensors offering 4,096 pressure levels, while gaming handhelds specify gyroscopes rated to 4,000 °/s. As smartphones import wearable-grade health metrics and wearables inherit cellular connectivity, platform boundaries blur, amplifying cross-category leverage within the MEMS for mobile devices market.

By Fabrication Technology: CMOS Integration Accelerates

Surface micromachining retained 48.73% of 2025 output because it yields sub-1 µm air gaps essential for high-gain capacitive accelerometers, driving a notable portion of the MEMS for mobile devices market size. CMOS-MEMS integration, though smaller today, is rising 9.88% per year as TSMC’s 28 nm flow co-locates sensor structures with ADCs, shrinking 3 × 3 mm packages. Bulk micromachining owns roughly 20% for pressure and microphone diaphragms, high-aspect-ratio SOI about 15% for low-drift gyros, while piezoelectric thin films and polymer MEMS occupy the rest.

GlobalFoundries and Bosch now offer 130 nm process design kits featuring pre-characterized inertial libraries, trimming tape-out times by 6-9 months. X-FAB’s XMB10 platform enables gyroscope noise densities under 0.004 °/s/√Hz, underscoring how process innovation upgrades performance ceilings. Material diversification, scandium-doped AlN resonators, polyimide substrates, signals that competitive differentiation is tilting from geometry scaling toward material science mastery.

By Integration Method: 3D-Stacked Architectures Gain Traction

System-in-package led with 41.30% of 2025 assemblies, combining dies from multiple nodes to shave 30-40% off NRE relative to monolithic solutions. Hybrids and 3D-stacked modules are advancing at 8.98% because through-silicon vias allow vertical bonding of MEMS, analog, and digital blocks within a 6 × 6 mm envelope suited to foldable-phone hinges. System-on-chip alternatives own 22% of volume and excel in power but require CMOS-MEMS foundries, limiting node flexibility. Discrete MEMS parts persist in cost-sensitive or high-reliability niches.

TDK’s SmartSonic time-of-flight sensor stacks a piezoelectric transducer on a 28 nm ADC using 40 µm copper pillars to achieve 1 mm range resolution. Bosch’s BMI323 fuses inertial, magnetic, and quaternion-output algorithms inside one mini-module, indicating where integration is headed. As TSV costs fall, heterogeneous 3D stacking may eclipse SiP over the forecast, infusing further momentum into the MEMS for mobile devices market.

Geography Analysis

Asia-Pacific captured 46.82% of 2025 revenue, driven by China’s thin-film deposition scale, South Korea’s CMOS-MEMS co-integration, and Taiwan’s foundries that anchor global fabless supply. Beijing’s USD 3 billion subsidy aims to lift domestic MEMS wafer capacity 40% by 2027, and Japan’s Murata plus TDK delivered over 30% of global MEMS microphone volume by exploiting ceramic-packaging prowess. Samsung Electro-Mechanics is piloting fan-out wafer-level packaging at thicknesses below 0.6 mm, while India’s Tata Electronics is building a 300 mm fab that will allocate one-fifth of capacity to MEMS from Q4 2026, reinforcing regional self-sufficiency.

North America produced roughly 24% of 2025 revenue. The United States leads fabless design, and the FDA’s string of wearable clearances validates medical MEMS use cases. Canada earmarked CAD 50 million to train 500 MEMS engineers, and Mexico’s emerging packaging nodes serve automotive and industrial customers. Europe held 18%; Infineon and Bosch dominate local production, and the AI Act cements on-device processing as a continental norm. The MEMS for mobile devices market therefore sees regulatory pull in the West and volume pull in Asia.

The Middle East, while only mid-single digit today, is growing 8.36% annually as Gulf sovereign funds finance assembly lines that localize supply. Turkey courts test and packaging investment to act as a Europe-Asia bridge. Africa and South America collectively remain below 10% but score double-digit growth tied to rising smartphone penetration: Brazilian and Nigerian assemblers integrate multi-sensor arrays to differentiate camera stabilization and biometric security. Regional diversification thus tempers geopolitical supply-chain risks and enlarges the aggregate MEMS for mobile devices market size.

Competitive Landscape

The five largest vendors shipped more than 60% of 2025 units, placing the sector in moderately consolidated territory. STMicroelectronics’ intelligent sensor processing unit in the LSM6DSV32X pushes classification to the edge, trimming system power by 30%. Bosch Sensortec targets 90% portfolio coverage with on-sensor inference by 2027, while TDK exploits copper-pillar stacking to pair transducers and ADCs in sub-4 mm² footprints. Knowles acquired Syntiant for USD 150 million to bring neural accelerators into its SiSonic microphones, enabling keyword spotting without sending audio off-device.

Specialists such as SiTime unsettle incumbents by delivering sub-50-fs-jitter MEMS oscillators vital for Wi-Fi 7 and 5G synchronization. Foundry access compresses tape-out cycles to nine months, allowing startups to chase niche algorithms rapidly. Patent filings in acoustic beamforming and piezoelectric energy harvesting rose 18% year-over-year, indicating IP will remain a moat even as CMOS-compatible capacity democratizes fabrication.

Vertical integration is also re-shaping roles: sensor houses buy thin-film tool makers, and handset brands invest in captive fabs, blurring customer-supplier lines. Collectively, these forces reinforce dynamic competition yet maintain sufficient margin opportunities, sustaining healthy expansion of the MEMS for mobile devices market.

MEMS For Mobile Devices Industry Leaders

Analog Devices Inc.

Bosch Sensortec GmbH

STMicroelectronics N.V.

InvenSense Inc. (TDK)

Goertek Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: STMicroelectronics unveiled the LSM6DSV32X inertial unit with a finite-state machine that recognizes 16 gestures locally, extending smartwatch standby by 30%.

- September 2025: Apple released iPhone 15 Pro featuring spatial-audio recording achieved with matched MEMS microphone arrays and head-tracking data.

- June 2025: GlobalFoundries partnered with Bosch to launch 130 nm CMOS-MEMS design kits, cutting NRE by 40% for fabless startups.

- March 2025: Goodix introduced a second-generation ultrasonic fingerprint reader that authenticates two fingers over a 64 mm² zone in 0.3 seconds.

Global MEMS For Mobile Devices Market Report Scope

The MEMS For Mobile Devices Market Report is Segmented by Type of Sensor (Fingerprint, Accelerometer, Gyroscope, Pressure, BAW, Microphones, and More), Application (Smartphones, Tablets, Wearables, Gaming, and More), Fabrication Technology (Surface, Bulk, SOI, CMOS-MEMS, and More), Integration Method (SiP, SoC, 3D-Stacked, Discrete, and More), and Geography. Market Forecasts are in Value (USD).

| Fingerprint Sensor |

| Accelerometer |

| Gyroscope |

| Pressure Sensor |

| Bulk Acoustic Wave (BAW) Sensor |

| Microphones |

| Other Types of Sensors |

| Smartphones |

| Tablets |

| Wearable Devices |

| Mobile Gaming Devices |

| Other Mobile Device Types |

| Surface Micromachining |

| Bulk Micromachining |

| High Aspect Ratio SOI |

| CMOS-MEMS Integration |

| Other Fabrication Technologies |

| System-in-Package (SiP) |

| System-on-Chip (SoC) |

| Hybrids and 3D-Stacked |

| Discrete MEMS |

| Other Integration Methods |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

| By Type of Sensor | Fingerprint Sensor | ||

| Accelerometer | |||

| Gyroscope | |||

| Pressure Sensor | |||

| Bulk Acoustic Wave (BAW) Sensor | |||

| Microphones | |||

| Other Types of Sensors | |||

| By Mobile Device Type | Smartphones | ||

| Tablets | |||

| Wearable Devices | |||

| Mobile Gaming Devices | |||

| Other Mobile Device Types | |||

| By Fabrication Technology | Surface Micromachining | ||

| Bulk Micromachining | |||

| High Aspect Ratio SOI | |||

| CMOS-MEMS Integration | |||

| Other Fabrication Technologies | |||

| By Integration Method | System-in-Package (SiP) | ||

| System-on-Chip (SoC) | |||

| Hybrids and 3D-Stacked | |||

| Discrete MEMS | |||

| Other Integration Methods | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Australia | |||

| New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Kenya | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large will the MEMS for mobile devices market be by 2031?

The MEMS for mobile devices market size is forecast to reach USD 15.61 billion by 2031, expanding at a 7.31% CAGR from 2026.

Which sensor type holds the biggest revenue share today?

Fingerprint modules led with 35.21% of 2025 revenue, reflecting broad deployment across mid-range and flagship smartphones.

What is driving the fastest growth segment?

Bulk acoustic wave components are growing at 9.32% a year because 5G and ultra-wideband radios need high-Q filters across dozens of frequency bands.

Why are wearables important for sensor suppliers?

Wearables are projected to post a 7.52% CAGR through 2031, underpinned by FDA-cleared health functions that demand low-power, always-on MEMS hubs.

Page last updated on: