Inertial Measurement Unit Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

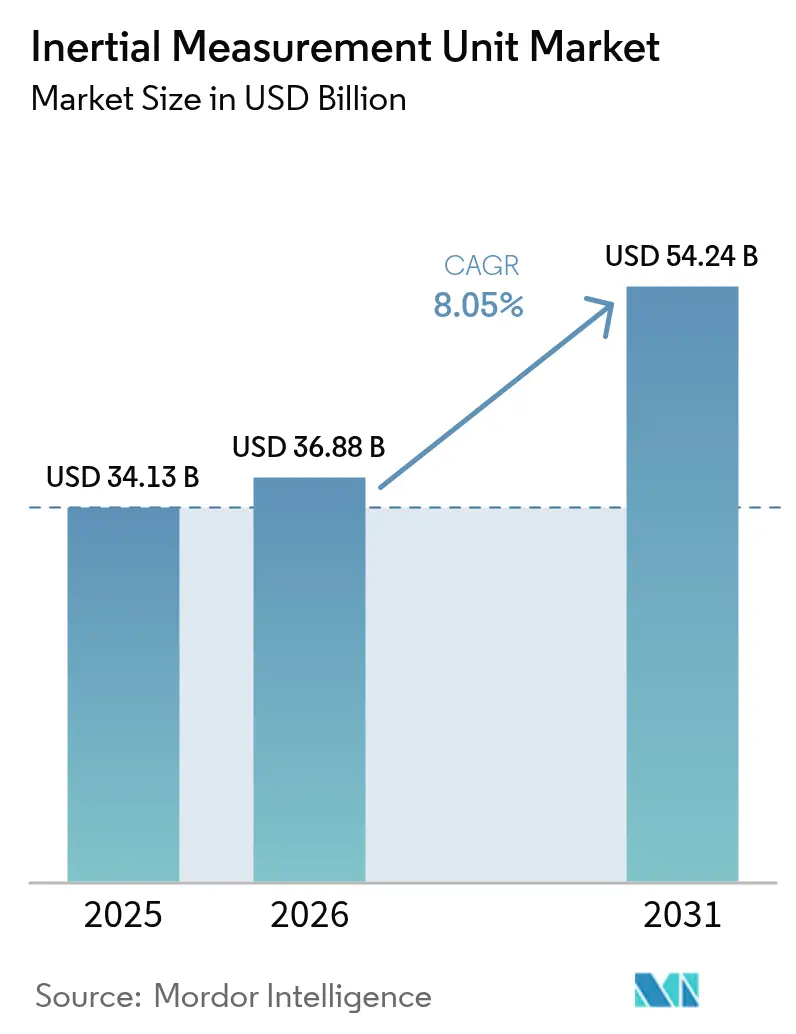

| Market Size (2026) | USD 36.88 Billion |

| Market Size (2031) | USD 54.24 Billion |

| Growth Rate (2026 - 2031) | 8.05% CAGR |

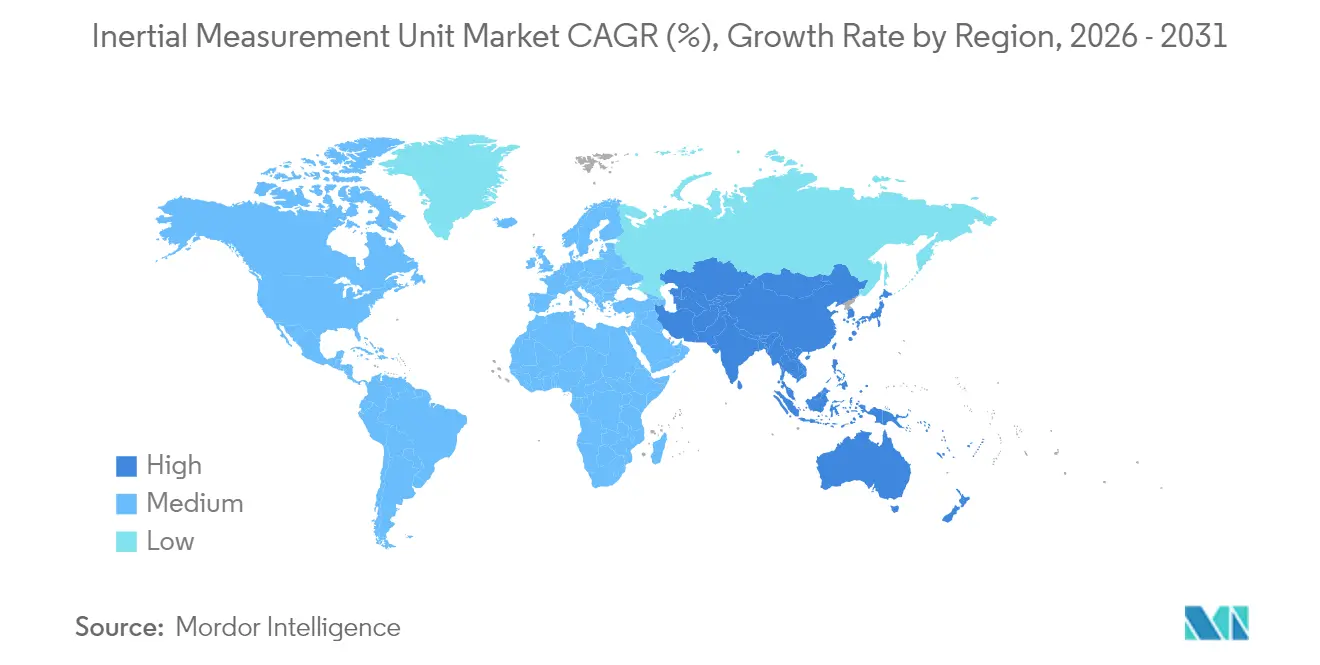

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Inertial Measurement Unit Market Analysis by Mordor Intelligence

The inertial measurement unit market size was valued at USD 34.13 billion in 2025 and estimated to grow from USD 36.88 billion in 2026 to reach USD 54.24 billion by 2031, at a CAGR of 8.05% during the forecast period (2026-2031). Demand gains stem from hybrid quantum-MEMS sensor fusion, which is reshaping precision navigation for defines, aerospace, and autonomous platforms. Boeing validated this shift when its 2024 flight test of a quantum IMU cut unaided-GPS navigation error from tens of kilometres to tens of meters. Escalating geopolitical risk, the spread of unmanned systems, and the maturity of quantum photonics all reinforce the near-term growth outlook for the inertial measurement unit market. Consumer pull is equally strong. China shipped 494,000 smart-glass units in Q1 2025, up 116.1% year over year, signalling record demand for low-cost six-axis sensors that balance accuracy and battery life. Maritime, mining, and LNG operators are adding tactical-grade MEMS IMUs to meet sub-degree dynamic-positioning tolerances, widening the addressable base for the inertial measurement unit market. [1]Boeing Tests Quantum Navigation System,” Boeing, boeing.com

Key Report Takeaways

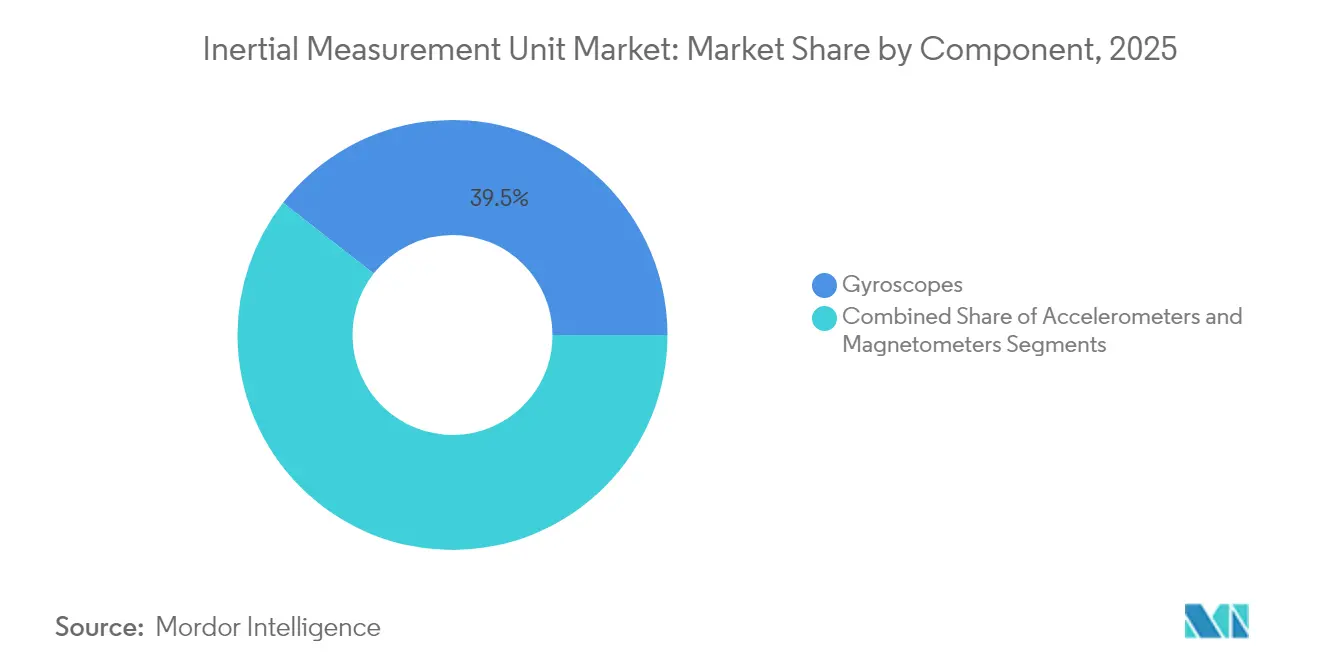

- By component, gyroscopes led with 39.45% of inertial measurement unit market share in 2025; magnetometers post the fastest 10.62% CAGR to 2031.

- By grade, commercial-grade units captured 34.55% share of the inertial measurement unit market size in 2025, while space-grade units expand at a 12.02% CAGR through 2031.

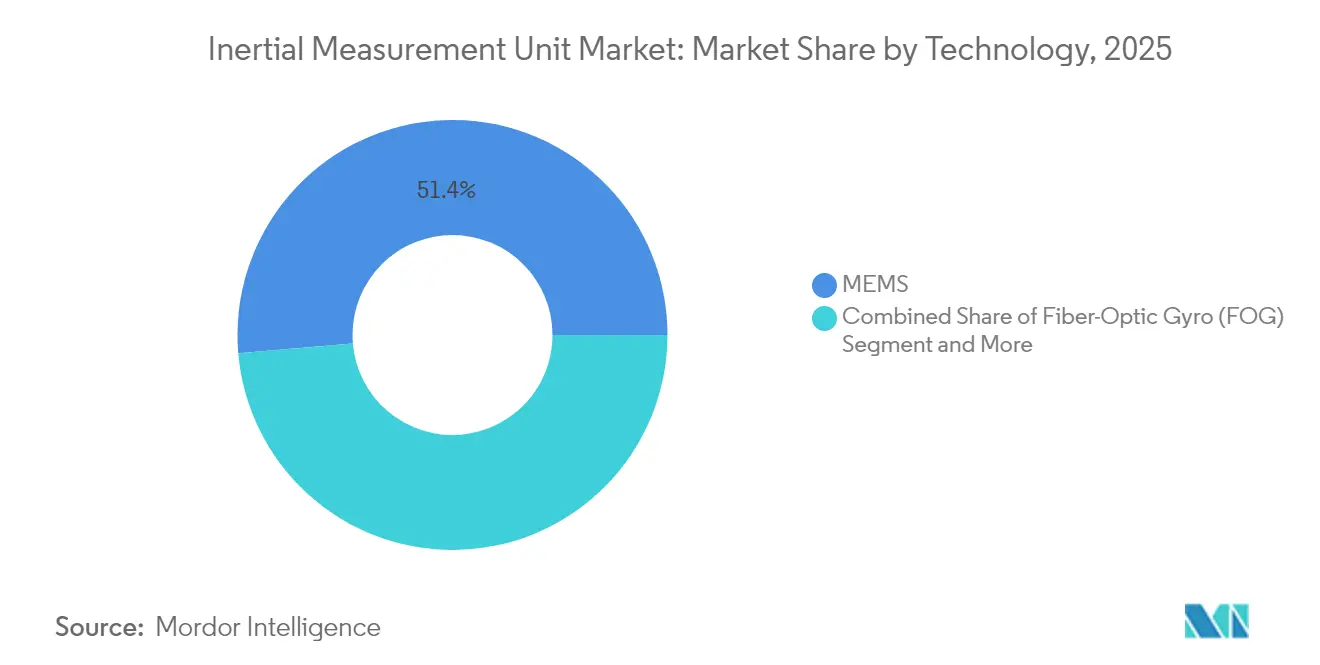

- By technology, MEMS dominated at 51.35% share in 2025; photonic devices record an 10.78% CAGR to 2031.

- By end user, aerospace and defense held 31.55% revenue share in 2025; automotive ADAS grows at 11.06% CAGR to 2031.

- By geography, North America accounted for 37.35% of the inertial measurement unit market size in 2025, whereas Asia-Pacific advances at an 11.42% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Inertial Measurement Unit Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated Deployment of Counter-UAS Platforms amid Middle-East Drone Incursions | 1.80% | Global, with concentration in Middle East & NATO countries | Short term (≤ 2 years) |

| Rising Adoption of MEMS-based Tactical-Grade IMUs in European LNG Tankers for Dynamic Positioning | 1.20% | Europe, with spillover to Asia-Pacific LNG routes | Medium term (2-4 years) |

| Integration of Cold-Atom IMUs in ESA Small-Satellite Constellations | 0.90% | Global space missions, led by Europe and North America | Long term (≥ 4 years) |

| Expansion of Photonic IMUs for Autonomous Mining Vehicles in Australia | 0.70% | Australia, with adoption in Canada and Chile mining sectors | Medium term (2-4 years) |

| Demand Spike for Retrofit Navigation Upgrades in U.S. Gen-II Fighter Fleet | 1.10% | North America, with export potential to allied nations | Short term (≤ 2 years) |

| High-volume Consumer-Electronics IMU Orders Driven by Asia's XR Headset Race | 2.10% | Asia-Pacific core, with global consumer electronics impact | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerated deployment of counter-UAS platforms amid Middle East drone incursions

Low-cost drones now outnumber legacy air defenses across several Middle East theatres. Nordic Air Defence’s Kreuger 100 interceptor relies on a simplified IMU-only flight computer, reaches 270 km/h, and cuts unit costs for swarm engagements. The U.S. Marine Corps selected Epirus microwave systems that couple agile IMUs with software-defined emitters to disable drone electronics. These moves signal a procurement pivot toward modular, software-centric weapons built around inertial cores rather than expensive radar or optical guidance. Suppliers that offer scalable IMU modules and open APIs stand to gain as militaries transition to volume-deployment counter-UAS doctrine. [2]Xavier Vavasseur, “Kreuger 100 Counter-UAV Interceptor,” Army Recognition, armyrecognition.com

Rising adoption of MEMS tactical-grade IMUs in European LNG tankers for dynamic positioning

European LNG shippers face tighter port queues and harsher Atlantic swells. Bourbon vessels now carry Exail Octans AHRS, based on fiber-optic gyros, to maintain roll, pitch, and heave integrity during crane operations. MEMS designs are also displacing ring-laser gyros on retrofit jobs because they slash purchase price by half while meeting sub-degree accuracy. Advanced Navigation’s Hydrus AUV lowered subsea survey costs 75% and removed the need for team-based diving missions. Such savings encourage fleet-wide sensor upgrades, expanding the inertial measurement unit market across commercial shipping.

Integration of cold-atom IMUs in ESA small-satellite constellations

The European Space Agency’s GENESIS project co-locates four geodetic payloads with a cold-atom interferometer that promises 1 mm terrestrial-reference accuracy. The Naval Research Laboratory achieved continuous 3-D atom-beam operation that prevents drift for months. Quantum stability resists GNSS jamming and spoofing, giving civil and military operators an independent navigation layer. As cold-atom packages shrink and ride-share launch costs fall, satellite builders will replace legacy ring-laser gyros, creating long-duration demand for quantum-enhanced IMUs.

Expansion of photonic IMUs for autonomous mining vehicles in Australia

Anello Photonics demonstrated chip-scale optical gyros that limit distance error to 0.1% over 100 km, unlocking unmanned road trains that haul ore between Pilbara pits and ports. Rio Tinto’s AutoHaul rail network already logs fuel and maintenance savings by using photonic IMUs for driverless routing. BHP reports a 20% jump in productivity and 90% accident reduction after introducing autonomous drills. Mining firms now view navigation sensors as strategic assets that guard output and worker safety, adding a new vertical growth track for the inertial measurement unit market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Design-in Cycles >7 Years Limiting Supplier Switch-Over in Commercial Aircraft | -1.40% | Global aerospace industry, concentrated in North America and Europe | Long term (≥ 4 years) |

| ITAR Restrictions Curtailing U.S. Space-grade IMU Exports to APAC New-Space Players | -0.80% | APAC new-space sector, with secondary effects in Europe | Medium term (2-4 years) |

| Cumulative Bias Drift in MEMS Arrays Exceeding ±0.3°/hr for Long-haul Maritime Routes | -0.60% | Global maritime industry, particularly affecting transoceanic shipping | Medium term (2-4 years) |

| Scarcity of Radiation-Hardened ASICs Raising BOM Costs in LEO Satellite IMUs | -0.90% | Global space industry, with acute impact on new-space ventures | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Design-in cycles less than 7 years limiting supplier switch-over in commercial aircraft

Certification risk makes air-framers conservative. Boeing flight-tested quantum IMUs for four hours but must still complete multi-year qualification before line-fit adoption. Honeywell’s miniature IMU that flew on Mars probes underscores how aerospace buyers favour proven designs that demonstrate multi-decade reliability. Lengthy validation locks in incumbent vendors and slows unit-price erosion, tempering the inertial measurement unit market growth rate in commercial aviation.

ITAR restrictions curtailing U.S. space-grade IMU exports to APAC new-space players

The U.S. Department of Commerce eased licensing for close allies in 2024 yet retained controls on radiation-hardened navigation parts to other regions. APAC launch startups therefore invest in domestic IMU design or pivot to European suppliers, leading to parallel supply chains that limit U.S. vendor reach. Scarce rad-hard ASICs also stretch lead times, delaying satellite schedules and muting near-term demand for U.S.-origin devices.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Sensor Fusion Drives Competitive Edge

Gyroscopes contributed 39.45% of inertial measurement unit market revenue in 2025 and remain foundational for dead-reckoning accuracy. Magnetometers, though smaller in absolute value, compound at 10.62% CAGR as augmented-reality developers embed digital compasses inside every headset. Accelerometers maintain consistent volume in vibration and ADAS roles. The inertial measurement unit market now leans toward single-package sensor fusion. STMicroelectronics’ LSM6DSV16X adds a machine-learning core that recognizes gestures while lowering standby power to extend battery life. Component vendors that offer on-chip analytics can charge premiums despite commoditization pressure.

Emerging packages combine gyro, accelerometer, and magnetometer data inside secure enclave micro-controllers. Integrated timing eliminates inter-sensor latency and hardens systems against spoof signals. As design teams adopt these modules, bill-of-materials simplicity overtakes raw component cost as the main selection factor. That transition supports steady pricing in the inertial measurement unit market despite rising shipment volumes.

By Grade: Commercial Dominance Meets Space-Grade Momentum

Commercial-grade devices captured 34.55% of inertial measurement unit market size in 2025 thanks to smartphone and auto-ADAS scale. Space-grade shipments, though smaller, are projected to climb 12.02% CAGR on the back of proliferated low-Earth-orbit (LEO) constellations. Northrop Grumman’s LR-450 uses milli-HRG gyros that log more than 70 million fault-free hours in orbit while halving size, weight, and power over ring-laser counterparts. That reliability attracts constellation operators who must launch hundreds of identical satellites.

Grade boundaries blur as commercial MEMS precision improves. Automotive suppliers now request tactical-grade bias stability, while drone makers procure space-qualified parts for radiation robustness. Vendors that master flexible production lines able to pivot from consumer to defense volumes gain resilience during sector downturns, reinforcing their share within the inertial measurement unit market.

By Technology: MEMS Hegemony Faces Photonic Upswing

MEMS accounted for 51.35% of revenue in 2025 due to wafer-level economies. Yet photonic IMUs register the highest 10.78% CAGR. Anello Photonics demonstrated a silicon optical gyro that shifts seamlessly to inertial guidance when GPS jamming occurs, making it attractive for commercial aircraft backup systems. Fiber-optic and ring-laser technologies keep niche dominance in long-range artillery and subsea survey roles, while hemispherical resonator gyros serve high-vibration space launchers.

Supply chains now invest in silicon photonics to shrink cost deltas versus MEMS. Sandia National Laboratories integrated quantum modulators onto 300 mm wafers, laying groundwork for mass-market quantum-enhanced IMUs. When yield stabilizes, optical devices could capture mid-tier price points, expanding their addressable slice of the inertial measurement unit market.

By End User: Aerospace Holds Lead as Automotive Surges

Aerospace and defense held 31.55% of inertial measurement unit market share in 2025 given mission-critical tolerance for premium pricing. Automotive ADAS applications, however, grow 11.06% CAGR, fuelled by mandatory lane-keeping and hands-off highway pilot programs. TDK’s ICM-456xy BalancedGyro delivers sub-0.3°/s bias instability for VR headsets and will migrate to high-volume driver-monitoring cameras. Industrial robotics and warehouse automation also pull volumes as e-commerce groups seek lights-out fulfilment.

Cross-sector innovation is now bidirectional. Consumer wearables push for lower-power AI on the edge, lessons that aerospace primes repurpose to cut cockpit workload. Conversely, quantum-grade stability perfected for missiles trickles down to luxury automotive lidar modules. This circulation enlarges total addressable demand and underpins long-run growth for the inertial measurement unit market.

Geography Analysis

North America commanded 37.35% of inertial measurement unit market revenue in 2025. U.S. defense budgets fund quantum interferometer research at the Naval Research Laboratory, extending navigation run-time without drift. Boeing’s quantum-IMU flight validated commercial-aviation use cases and keeps local OEMs ahead of European rivals. Export-control reforms in 2024 eased transfers to Australia, Canada, and the United Kingdom, giving North American vendors privileged access to allied aerospace programs.

Asia-Pacific posts the strongest 11.42% CAGR through 2031. Chinese smart-glass makers, buoyed by domestic subsidies, order tens of millions of six-axis MEMS sensors each quarter. Australia’s remote mines serve as live testbeds for photonic IMU trucks, encouraging regional universities to spin out navigation start-ups. New-space launch firms across India, Japan, and South Korea seek ITAR-free space-grade parts, fostering indigenous supply chains that challenge U.S. incumbents in cost-sensitive missions.

Europe retains strategic niches in marine, energy, and high-precision satellite payloads. The ESA GENESIS satellite will use cold-atom IMUs to underpin centimeter-level sea-level monitoring. Exail won Bourbon vessel contracts for fiber-optic gyro dynamic-positioning upgrades, reflecting regional expertise in harsh-sea sensor packaging. Honeywell’s EUR 200 million purchase of Civitanavi in 2024 gives the firm a deep European production base, ensuring continuity for aircraft programs even amid trans-Atlantic trade frictions.

Competitive Landscape

The inertial measurement unit market shows moderate fragmentation, yet M&A momentum is rising. VIAVI paid USD 150 million for Inertial Labs, coupling RF-test know-how with inertial sensors to address autonomous-system diagnostics. Honeywell acquired Civitanavi to secure fiber-optic gyro IP and comply with European sourcing rules. Start-ups leverage photonics and quantum physics to bypass MEMS incumbents, while big consumer brands file patents that fold IMUs into proprietary mixed-reality stacks; Apple’s 2024 headset sensor patent exemplifies this move.

Technology leadership now revolves around system-level intelligence. Bosch Sensortec ships BHI380 smart hubs that self-learn user motion and cut host-processor wakeups, a capability sought by drone makers for longer sorties. Suppliers that merge software, AI, and secure-element hardware achieve sticky design wins, cushioning margins even as unit prices for raw sensors fall. Consolidation continues as defense primes buy photonic or quantum specialists to protect sovereign navigation roadmaps.

Inertial Measurement Unit Industry Leaders

Honeywell International Inc.

Northrop Grumman Corp.

Bosch Sensortec GmbH

Analog Devices Inc.

Safran Sensing Technologies (Safran SA)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: VIAVI Solutions launched the ITAR-free IMU-H100 tactical-grade MEMS unit with 1 deg/hr gyro bias and 1 mg accelerometer bias for UAV and missile markets.

- March 2025: Boeing completed a four-hour flight test using a quantum IMU, reducing GPS-denied navigation error to tens of meters.

- January 2025: Honeywell and NXP extended cooperation on AI-enabled Anthem avionics built on i.MX 8 processors.

- December 2025: VIAVI closed its USD 150 million acquisition of Inertial Labs, adding around USD 50 million revenue in 2025

Global Inertial Measurement Unit Market Report Scope

Inertial measurement units (IMUs) is a self-contained system that measures linear and angular motion, usually with a triad of gyroscopes and triad of accelerometers. IMUs are basically used to maneuver aircraft and spacecraft. IMU is being segregated by gyroscopes, accelerometers, and magnetometers as components. In terms of grade, IMU is divided as marine grade, navigation grade, tactical grade, space grade, and commercial grade.

| Gyroscopes |

| Accelerometers |

| Magnetometers |

| Marine Grade |

| Navigation Grade |

| Tactical Grade |

| Space Grade |

| Commercial Grade |

| MEMS |

| Fiber-Optic Gyro (FOG) |

| Ring-Laser Gyro (RLG) |

| Hemispherical Resonator Gyro (HRG) |

| Mechanical Gyro |

| Aerospace and Defense |

| Automotive (ADAS and Autonomous) |

| Industrial Automation and Robotics |

| Consumer Electronics and XR |

| Marine and Offshore |

| Energy (Oil and Gas, Wind Turbines) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Israel |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Gyroscopes | |

| Accelerometers | ||

| Magnetometers | ||

| By Grade | Marine Grade | |

| Navigation Grade | ||

| Tactical Grade | ||

| Space Grade | ||

| Commercial Grade | ||

| By Technology | MEMS | |

| Fiber-Optic Gyro (FOG) | ||

| Ring-Laser Gyro (RLG) | ||

| Hemispherical Resonator Gyro (HRG) | ||

| Mechanical Gyro | ||

| By End User | Aerospace and Defense | |

| Automotive (ADAS and Autonomous) | ||

| Industrial Automation and Robotics | ||

| Consumer Electronics and XR | ||

| Marine and Offshore | ||

| Energy (Oil and Gas, Wind Turbines) | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Israel | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the inertial measurement unit market?

The inertial measurement unit market size reached USD 36.88 billion in 2026 and is projected to climb to USD 54.24 billion by 2031 at an 8.05% CAGR.

Which technology segment is growing fastest?

Photonic IMUs show the highest 10.78% CAGR as silicon photonics lowers cost and boosts accuracy for GPS-denied navigation.

Why is Asia-Pacific the fastest-growing region?

Explosive consumer-electronics demand, autonomous-vehicle pilots, and mining automation push Asia-Pacific toward an 11.42% regional CAGR through 2031.

How are quantum sensors affecting the inertial measurement unit market?

Quantum interferometry, such as cold-atom and hybrid quantum-MEMS designs, cuts long-term drift and resists GPS jamming, opening new aerospace and defense opportunities.

What restrains rapid IMU adoption in commercial aircraft?

Certification cycles exceeding seven years make air-framers reluctant to switch suppliers, limiting near-term penetration for new IMU entrants.

Which companies are driving consolidation?

VIAVI Solutions and Honeywell led 2024 deals by purchasing Inertial Labs and Civitanavi Systems, respectively, to gain fiber-optic and MEMS expertise.

Page last updated on: