Internal Combustion Engines Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 316.61 Billion |

| Market Size (2031) | USD 418.25 Billion |

| Growth Rate (2026 - 2031) | 5.73% CAGR |

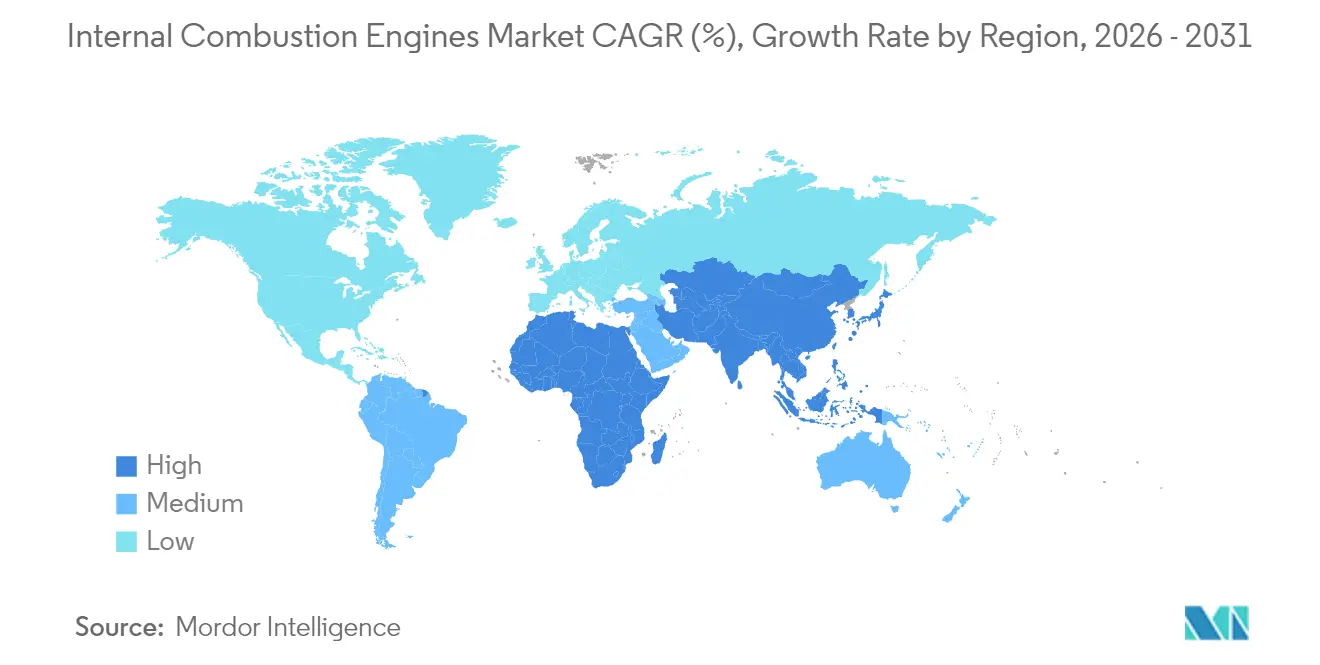

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

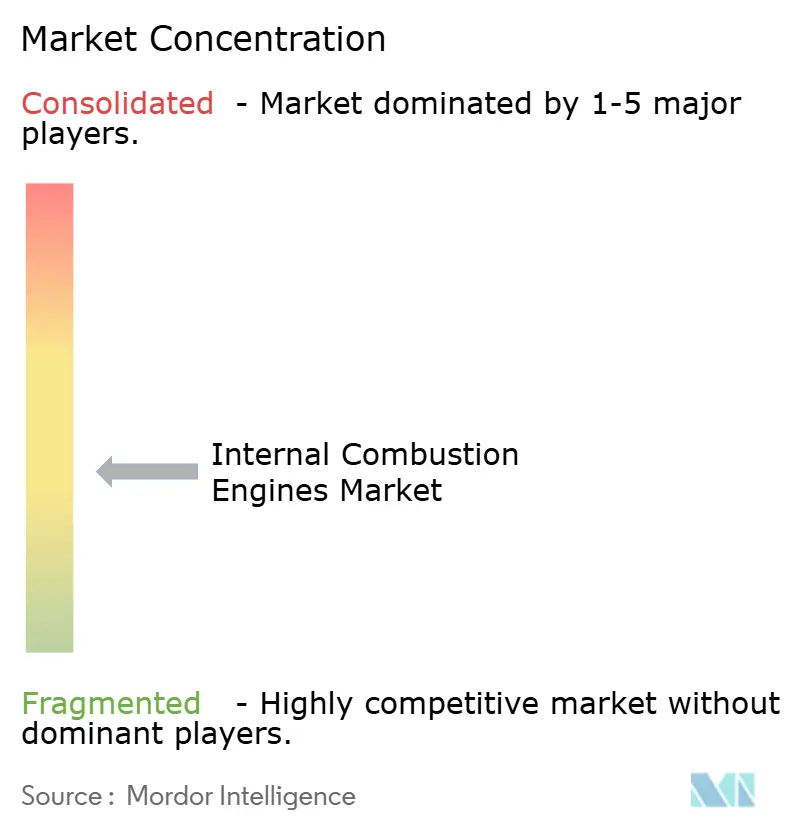

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Internal Combustion Engines Market Analysis by Mordor Intelligence

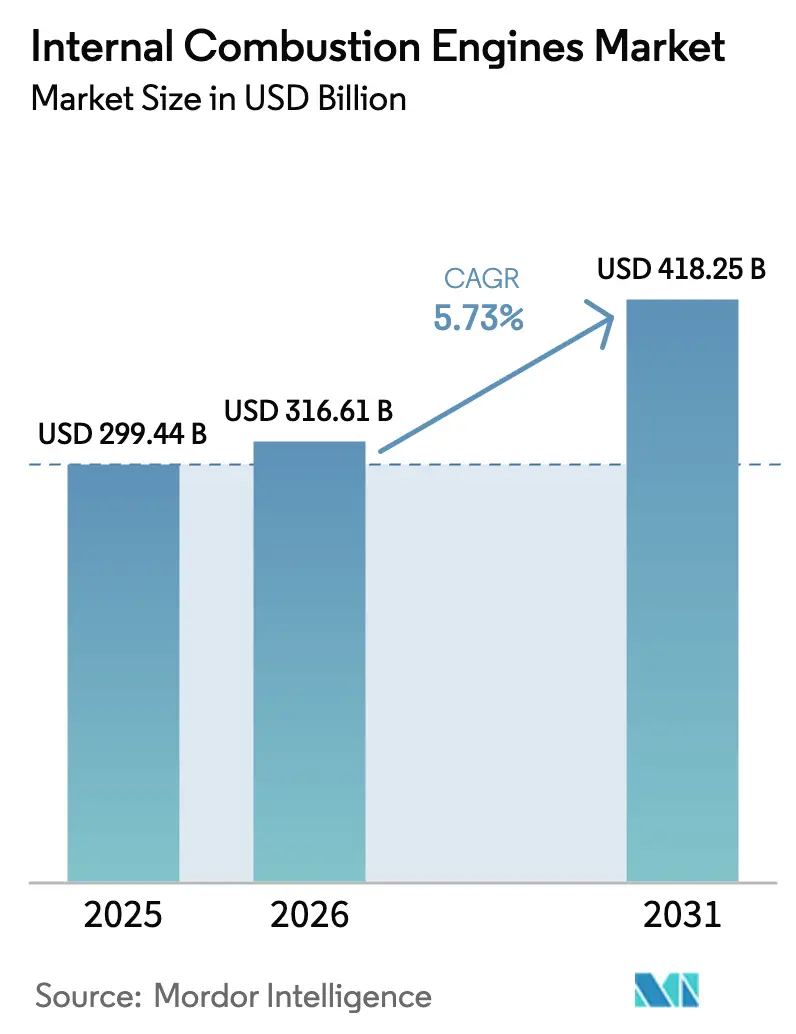

The Internal Combustion Engines Market size was valued at USD 299.44 billion in 2025 and estimated to grow from USD 316.61 billion in 2026 to reach USD 418.25 billion by 2031, at a CAGR of 5.73% during the forecast period (2026-2031).

Robust product redesign, a widening alternative-fuel portfolio, and region-specific regulatory strategies keep the internal combustion engines market relevant even as electrification accelerates. Heavy-duty and off-highway users continue to favor ICE platforms because batteries impose payload and range penalties, while advanced turbo-hybrid architectures blur the line between conventional and hybrid powertrains, delaying outright substitution. Investment commitments by global OEMs—often framed as “multi-pathway” programs—signal that traditional engine plants will coexist with EV lines through most of the decade. The parallel expansion of bio-, e-, and hydrogen-fuel infrastructure underpins new demand pockets, especially in regions where charging networks remain sparse.

Key Report Takeaways

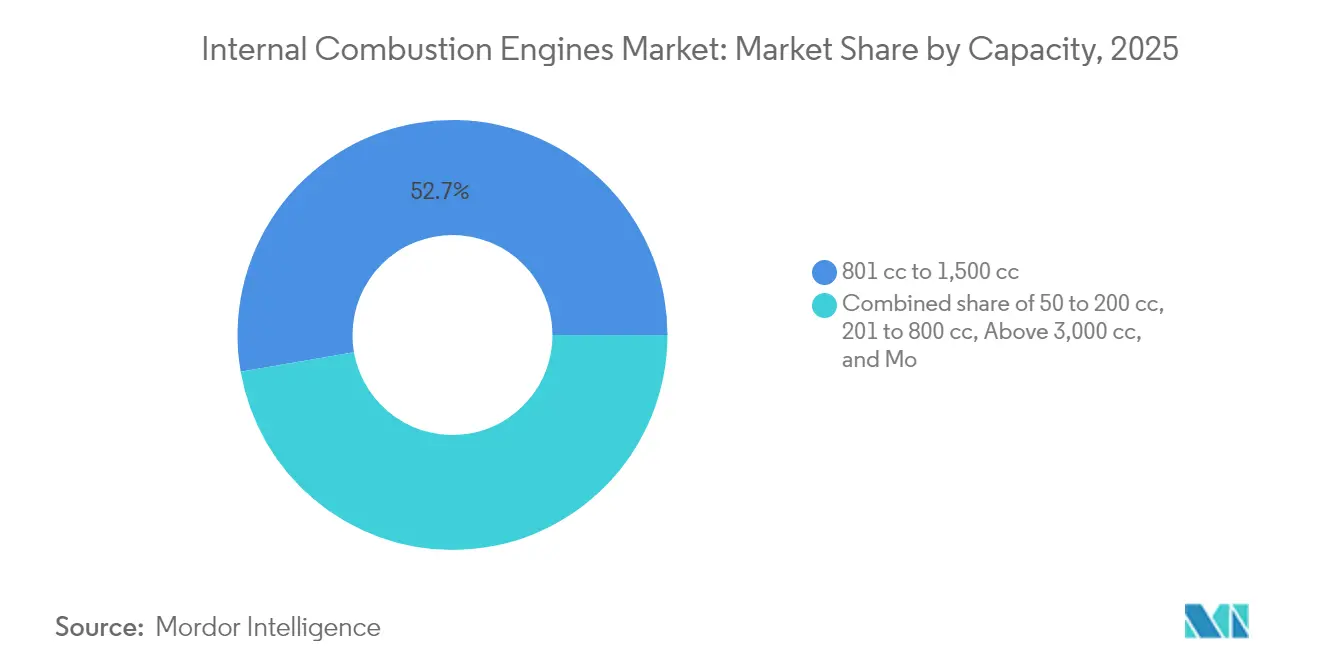

- By capacity, the 801 cc–1,500 cc band captured 52.74% of the internal combustion engines market share in 2025, whereas units above 3,000 cc are projected to compound at a 6.58% CAGR to 2031.

- By fuel type, gasoline led with a 60.12% share in 2025; hydrogen is forecast to grow at a 10.04% CAGR through 2031.

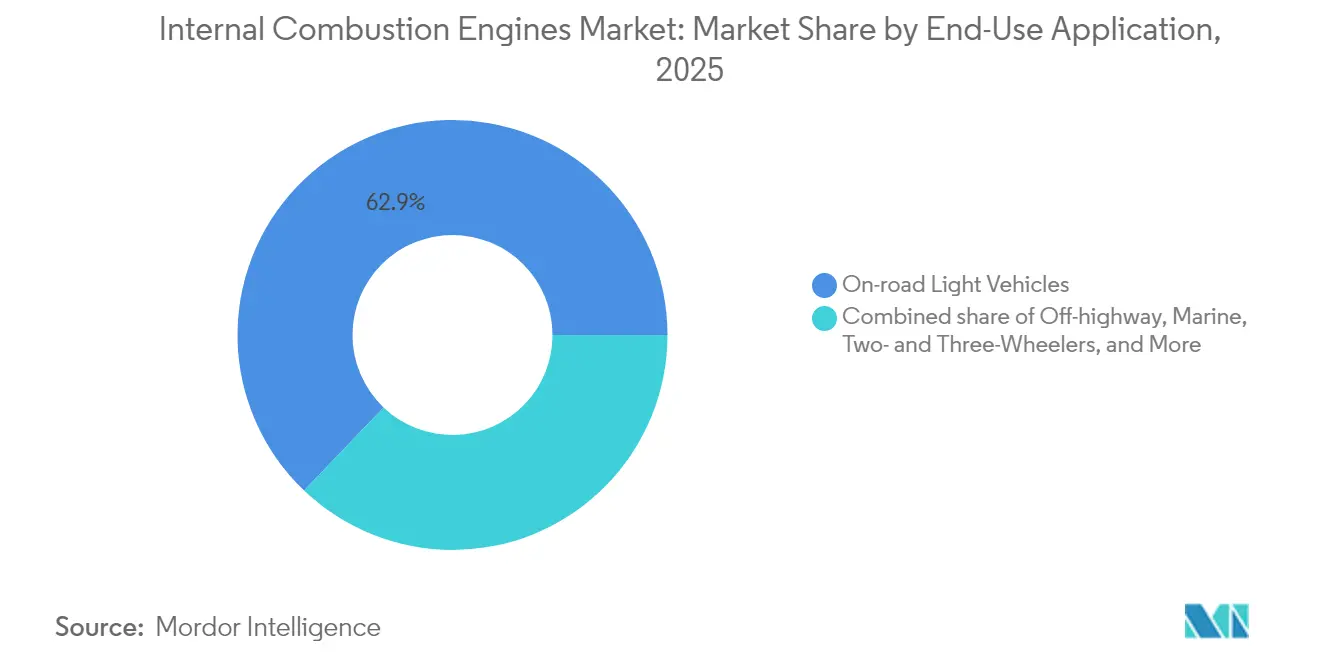

- By end-use, on-road light vehicles accounted for 62.88% of the internal combustion engines market size in 2025, while off-highway machinery is advancing at an 8.65% CAGR.

- By geography, the Asia-Pacific region commanded a 49.35% share in 2025 and is expected to expand at a 7.29% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Internal Combustion Engines Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening fuel-economy norms in emerging markets | +2.1% | Asia-Pacific, Latin America, MEA | Medium term (2-4 years) |

| Post-pandemic surge in two-wheeler demand across South & Southeast Asia | +1.8% | ASEAN Countries, India | Short term (≤ 2 years) |

| Infrastructure gaps slowing BEV roll-out in Africa & Latin America | +0.9% | Sub-Saharan Africa, Rural Latin America | Long term (≥ 4 years) |

| Turbo-hybrid ICE architectures lowering total cost of ownership | +1.2% | Global, with early adoption in Europe & Japan | Medium term (2-4 years) |

| Rapid growth of bio- & e-fuel supply chains | +0.8% | Europe, North America, Brazil | Long term (≥ 4 years) |

| Breakthroughs in hydrogen-ICE for heavy-duty mobility | +0.6% | Europe, North America, Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Tightening Fuel-Economy Norms in Emerging Markets

India’s BS-VI Phase 2 and China’s CN-VII standards compel OEMs to deliver high-efficiency engines, as broad charging networks remain incomplete.[1]Association of Equipment Manufacturers, “Fuel-Economy Regulations in Emerging Markets,” aem.org Instead of triggering rapid electrification, the rules stimulate localised redesign—variable compression, high-pressure direct injection, and mild-hybrid add-ons—so manufacturers stay compliant without shifting price-sensitive buyers to full EVs. Commercial fleets, conscious of payload limits, also prefer these lean-burn ICE solutions. Regional refineries accelerate the supply of ultra-low-sulfur fuel, which removes a bottleneck to the adoption of advanced after-treatment systems. Consequently, the internal combustion engines market benefits from regulatory pressure rather than suffering outright contraction.

Post-Pandemic Two-Wheeler Demand in South & Southeast Asia

Motorcycle registrations in India jumped 15% YoY in 2024 and similar momentum spread across Indonesia, Vietnam, and the Philippines. Suburban commuters see personal two-wheelers as safer than crowded buses, while rural households rely on them for first-mile logistics. Small 125 cc–150 cc engines dominate because they strike a balance between fuel economy and purchase affordability. Regional OEMs are ramping up localized casting and machining to keep pace, thereby lifting volumes in the internal combustion engines market. Parallel policy incentives—such as lower registration fees for Euro 5-compliant motorcycles—promote cleaner yet still ICE-based mobility.

Infrastructure Gaps Slowing BEV Roll-out in Africa & Latin America

Grid instability in South Africa and slow rural electrification in Brazil highlight why many fleets continue to opt for diesel or ethanol engines. Commercial haulers value refueling speed and route flexibility, conditions not yet matched by public chargers. Governments, unwilling to stall economic growth, embrace cleaner ICE variants and biofuel blends as stepping-stone technologies. The result is a prolonged addressable base for the internal combustion engines market, especially in agricultural and mining corridors that demand rugged high-torque powertrains.

Turbo-Hybrid ICE Architectures Lowering Total Cost of Ownership

Hyundai’s 1.6L turbo-hybrid system achieves 45% thermal efficiency, saving fleet operators substantial fuel without requiring alterations to depot infrastructure.[2]Hyundai Motor Group, “Next-Generation Hybrid Powertrain Technical Paper,” hyundai.com A smaller displacement, combined with electric boost, delivers city-grade torque while maintaining highway range. Component commonality with conventional engines keeps capital costs low, and the absence of plug-in requirements sidesteps grid constraints. This proposition appeals to municipalities seeking immediate CO₂ cuts, nudging the internal combustion engines market toward electrified yet fuel-dependent formats.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Zero-tailpipe-emission mandates | -1.4% | EU, California, select US states | Medium term (2-4 years) |

| Battery price parity by 2027 | -0.8% | Global developed markets | Short term (≤ 2 years) |

| Global re-allocation of R&D budgets toward solid-state EVs | -0.6% | Global, concentrated in automotive OEMs | Medium term (2-4 years) |

| Early-scrappage incentives reducing legacy ICE parc | -0.4% | Europe, North America, select developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerated Zero-Tailpipe-Emission Mandates in Europe & California

The Euro 7 regulations are set to begin in November 2026, while California aims to achieve 100% ZEV sales by 2035.[3]European Commission, “Euro 7 Regulation Text,” europa.eu Compliance costs for particulate filters and NOx control tilt the economic equation in favor of BEVs in light-duty segments. OEMs are forced to allocate R&D resources into parallel drivetrains, raising unit costs for ICE models sold in permissive regions. Nevertheless, loopholes permitting synthetic fuels and hydrogen keep specialty niches open, cushioning the internal combustion engines market from an abrupt collapse.

Battery-Price Parity in Light Vehicles Expected by 2027

Pack costs flirt with USD 100/kWh, narrowing the purchase-price differentials between compact EVs and ICE equivalents.[4]International Energy Agency, “Electric Vehicle Outlook 2024,” iea.org Urban customers who drive predictable daily distances perceive lifetime cost advantages shifting toward EVs, shrinking addressable urban passenger-car volumes. OEMs respond by doubling down on segments where battery mass or duty cycle still favors combustion, such as heavy trucks, marine propulsion, and portable power. This strategic realignment moderates, but does not eliminate, the forward momentum of the internal combustion engines market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Capacity: Balancing Mid-Range Scale with Heavy-Duty Upside

The 801 cc–1,500 cc band retained 52.74% of the internal combustion engines market share in 2025, anchoring supply for compact SUVs, light vans, and family hatchbacks. Urbanisation in emerging economies safeguards volume, while turbo-downsizing and start-stop technologies lift fuel economy enough to meet evolving norms. OEMs deploy modular block designs, allowing common machining lines to handle both gasoline and flex-fuel variants.

Meanwhile, engines above 3,000 cc are forecast to grow at a 6.58% CAGR through 2031, driven by demand in freight, construction, and power generation. Fleet operators prize high torque density and multi-fuel compatibility, particularly in markets where access to diesel, LNG, or biodiesel varies by province. Those attributes keep the internal combustion engines market relevant even in policy-progressive regions that exempt critical-use vehicles from ZEV quotas. Component suppliers invest in high-pressure common-rail systems and steel pistons, technologies that preserve durability while cutting specific emissions.

By Fuel Type: Gasoline Dominance Meets Hydrogen Momentum

Gasoline engines captured a 60.12% share in 2025, benefiting from ubiquitous retail distribution, established maintenance networks, and lower upfront costs compared to hybrids. Incremental efficiency gains—such as variable valve timing and lean stratified charge—sustain appeal in budget-conscious markets. The segment’s vast installed base also underwrites aftermarket parts volumes, reinforcing lock-in effects that buoy the internal combustion engines market.

Hydrogen, although starting from a small base, is expected to lead growth at a 10.04% CAGR as OEMs exploit its drop-in nature for heavy-duty fleets, where battery size penalties are untenable. Cummins and Toyota demonstrate spark-ignition and compression-ignition variants that meet Euro VII and EPA 2027 targets without carbon-intensive fuels. Regional hydrogen hubs in Europe, Japan, and California ensure early off-take, and subsidies help mitigate fuel-station build-out costs. Diesel retains freight loyalty, and natural-gas engines gain traction in India’s expanding CNG corridor. These overlapping pathways underscore how fuel agnosticism, rather than a single-fuel bet, will define the future of the internal combustion engine market.

By End-Use Application: Light Vehicle Volume versus Off-Highway Upsurge

On-road light vehicles accounted for 62.88% of the internal combustion engine market size in 2025, as passenger cars and light trucks continue to be the primary choice for personal mobility in developing cities. OEMs refresh model lines with mild hybrids, enabling CO₂ cuts without structural redesign. Dealership retention programs and an abundance of independent garages support lifecycle affordability, prolonging ICE dominance within this use case.

Off-highway machinery, including tractors, excavators, and mining haulers, is expected to advance at an 8.65% CAGR through 2031. Duty cycles require long idling, high load factors, and remote-site refueling—conditions that are poorly served by pure EVs. Manufacturers integrate Stage V after-treatment and flexible fuel maps, raising resale values and lowering the total cost of ownership. The internal combustion engines industry, therefore, sees parallel growth streams: volume-driven light vehicles and margin-rich heavy equipment.

Geography Analysis

Asia-Pacific controlled 49.35% of 2025 volume and is projected to expand at a 7.29% CAGR, anchored by China’s scale and India’s surging two-wheeler sales. Chinese plants produced more than 30 million engines in 2024, allowing tier-1 suppliers to amortise tooling over huge runs, which in turn keeps unit costs globally competitive. India’s rural electrification lag sustains demand for petrol and CNG scooters, while Indonesia and Vietnam deepen the localisation of component clusters. Japan pioneers hydrogen-ICE and hybrid exports, and South Korea perfects lean, high-volume casting for global OEMs.

Europe, under the Euro 7 and its Fit-for-55 roadmap, is experiencing a contraction in passenger-car output but sees pockets of investment in ICE engines for synthetic fuel readiness in the sports and luxury segments. Policy carve-outs for e-fuels postpone factory closures, and public funding for hydrogen corridors creates testbeds for long-haul trucks. North America leverages pickup demand and shale-gas abundance to sustain natural-gas and flex-fuel variants. US OEMs redirect some EV capex back to ICE plants to satisfy commercial-fleet backlogs, demonstrating the internal combustion engines market’s adaptive economics.

South America, the Middle East, and Africa represent expansion frontiers. Brazil’s ethanol economy underwrites flex-fuel portfolios; Argentina’s gas fields nurture LNG trucks; GCC nations capitalise on low diesel prices for construction booms. Persistent grid challenges encourage governments to classify advanced ICE as “transitional clean technology,” providing tax breaks for engines compatible with bio- or e-fuels. These regional stories collectively reinforce the premise that the internal combustion engine market will not fade uniformly but will fragment along economic and infrastructure fault lines.

Mordor Intelligence provides coverage of the internal combustion engines market across other key regional markets, including Europe, South America, and Middle East and Africa, each with their regulatory frameworks and demand patterns.

Competitive Landscape

The internal combustion engines market features moderate fragmentation, with global automakers such as Toyota, Volkswagen, and General Motors alongside dedicated engine makers—Cummins, Caterpillar, and Deutz—that specialise in high-horsepower niches. Differentiation hinges on fuel-agnostic platforms that can seamlessly convert among gasoline, diesel, natural gas, and hydrogen blends. Cummins’ HELM architecture, unveiled in 2025, standardizes bore spacing and accessory placement, allowing the same block to accommodate multiple fuel setups without requiring tooling changes.[5]Cummins Inc., “HELM Platform Launch Presentation,” cummins.com Toyota’s multi-pathway programme hedges bets across hybrid, hydrogen, and e-fuel engines, reallocating USD 4 billion in R&D to ensure compliance flexibility.

Joint ventures accelerate capability build-out. Volvo paired with Westport Fuel Systems to commercialise HPDI technology for LNG and hydrogen trucks, while Deutz acquired Blue Star Power Systems to capture off-grid genset demand. These moves correspond to rising white-space opportunities in marine propulsion and remote mining. Vendors that master emissions-after-treatment integration—selective catalytic reduction plus exhaust-gas recirculation—win orders from logistics firms juggling divergent regional regulations.

Price competition softens because many buyers now value regulatory compliance and multi-fuel adaptability over the lowest MSRP. Suppliers scale up high-pressure fuel-rail production and ceramic injector tips, lifting switching costs for customers. Consequently, the internal combustion engine market rewards players who blend scale with application-specific engineering rather than relying solely on volume.

Internal Combustion Engines Industry Leaders

Toyota Motor Corp.

Volkswagen AG

Stellantis N.V.

Hyundai Motor Co.

General Motors Co.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: General Motors confirmed a USD 1.4 billion upgrade for its Tonawanda plant to build sixth-generation small-block V8s from 2027, signalling long-term ICE commitment.

- April 2025: Cummins debuted the first hydrogen-ICE turbocharger series for Euro VII trucks in Europe. This turbocharger is intended to meet the Euro VII emission standards and is part of Cummins' broader strategy to support the transition to low-emission transportation.

- December 2024: Honda and Nissan signed an MoU to explore a merger valued near USD 79.9 billion, pooling ICE and EV assets.

- May 2024: Toyota, Mazda, and Subaru announced a joint next-generation ICE development centered on carbon-neutral fuels. This initiative aims to develop engines that seamlessly integrate with electric motors, batteries, and other drive units in hybrid and plug-in hybrid vehicles.

Global Internal Combustion Engines Market Report Scope

An internal combustion engine generates power by burning petrol, oil, or another fuel with air inside the engine. The hot gases produced are used to drive a piston or do other work as they expand.

The global internal combustion engine market is segmented by capacity, fuel type, and geography. By capacity, the market is segmented into 50 cm3 to 200 cm3, 201 cm3 to 800 cm3, 801 cm3 to 1500 cm3, and 1501 cm3 to 3000 cm3. By fuel type, the market is segmented into gasoline, diesel, and others. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The report also covers the market sizes and forecasts across major regions. For each segment, the market sizing and forecasts were made based on revenue (USD).

| 50 cc to 200 cc |

| 201 cc to 800 cc |

| 801 cc to 1,500 cc |

| 1,501 cc to 3,000 cc |

| Above 3,000 cc |

| Gasoline |

| Diesel |

| Natural Gas (CNG/LNG) |

| Bio and Synthetic Fuels |

| Hydrogen |

| On-road Light Vehicles |

| On-road Heavy-duty Trucks and Buses |

| Two- and Three-Wheelers |

| Off-highway (Agri, Construction, Mining) |

| Marine |

| Power Generation and Gensets |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Capacity | 50 cc to 200 cc | |

| 201 cc to 800 cc | ||

| 801 cc to 1,500 cc | ||

| 1,501 cc to 3,000 cc | ||

| Above 3,000 cc | ||

| By Fuel Type | Gasoline | |

| Diesel | ||

| Natural Gas (CNG/LNG) | ||

| Bio and Synthetic Fuels | ||

| Hydrogen | ||

| By End-use Application | On-road Light Vehicles | |

| On-road Heavy-duty Trucks and Buses | ||

| Two- and Three-Wheelers | ||

| Off-highway (Agri, Construction, Mining) | ||

| Marine | ||

| Power Generation and Gensets | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the internal combustion engines market in 2026?

The internal combustion engines market size is USD 316.61 billion in 2026 and is projected to reach USD 418.25 billion by 2031.

What CAGR is expected for internal combustion engines through 2031?

The market’s compound annual growth rate is forecast at 5.73% over 2026-2031.

Which region leads global demand?

Asia-Pacific holds 49.35% share and is growing at a 7.29% CAGR thanks to sustained ICE demand in China, India, and Southeast Asia.

Which fuel segment is growing fastest?

Hydrogen-ICE solutions register the highest growth at a 10.04% CAGR because they answer heavy-duty decarbonisation needs without large batteries.

What capacity range dominates shipments today?

Engines between 801 cc and 1,500 cc control 52.74% of global shipments, serving compact cars and light vans.

Are zero-emission mandates eliminating new ICE sales worldwide?

Strict rules in the EU and California are reducing light-vehicle volumes, but heavy-duty, off-highway, and multi-fuel niches keep ICE demand alive in many regions.

Page last updated on: