Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.34 Trillion |

| Market Size (2031) | USD 2.44 Trillion |

| Growth Rate (2026 - 2031) | 12.72% CAGR |

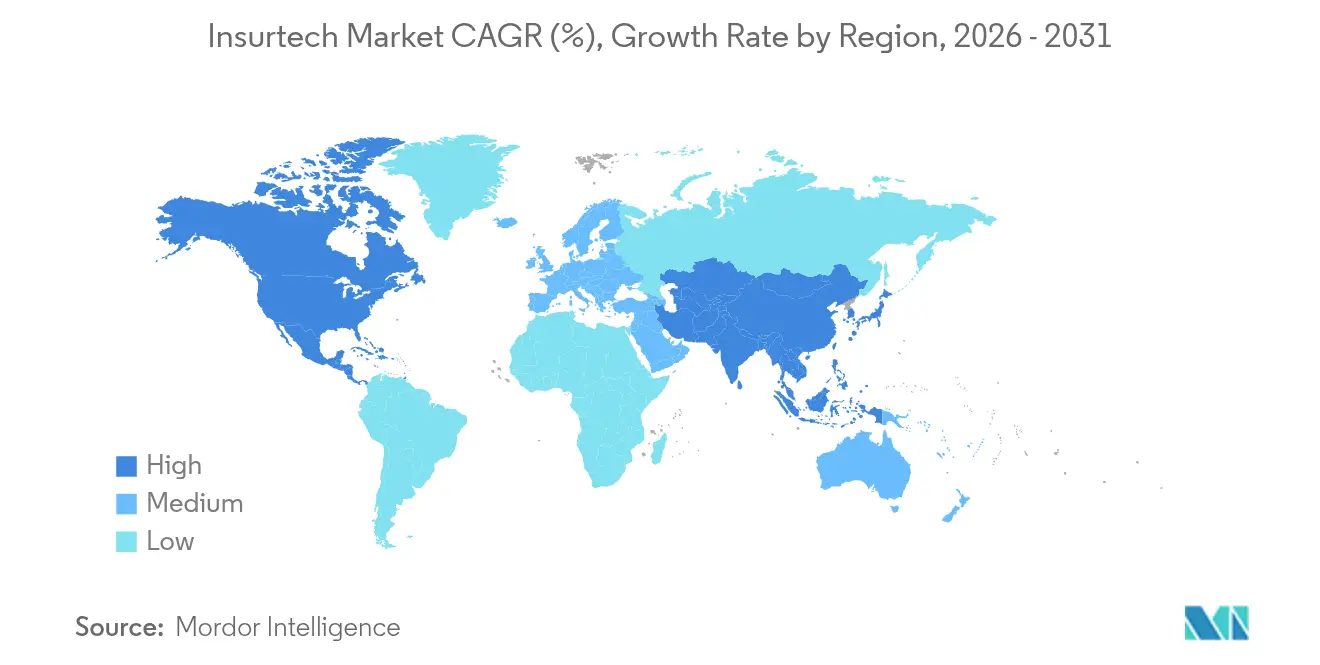

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

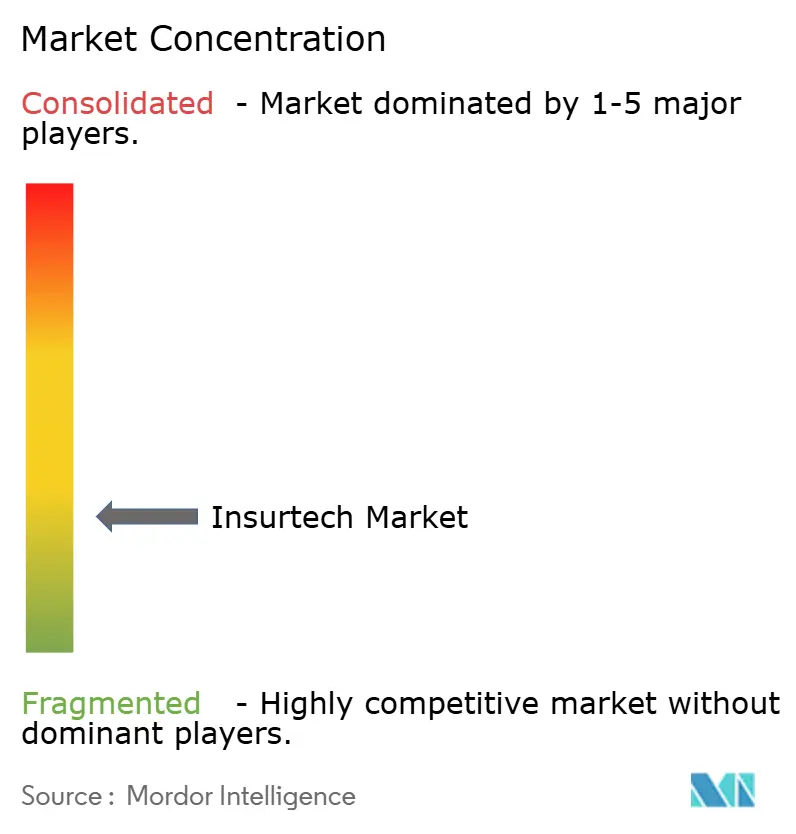

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Insurtech Market Analysis by Mordor Intelligence

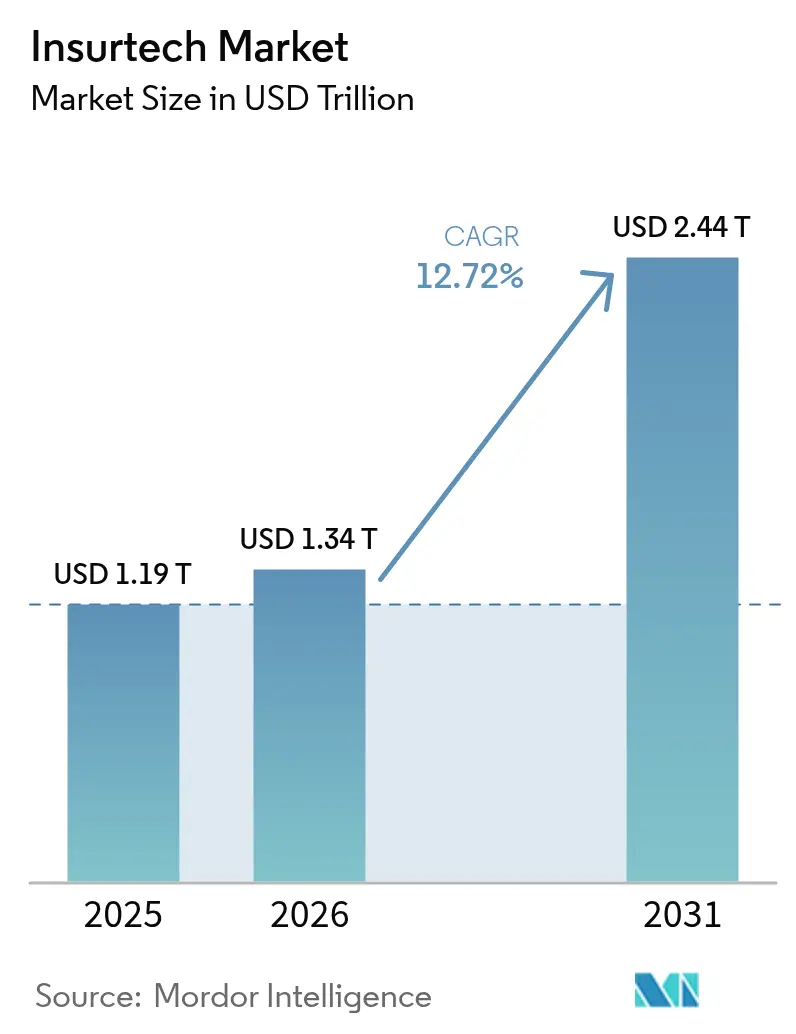

The Insurtech Market size is expected to increase from USD 1.19 trillion in 2025 to USD 1.34 trillion in 2026 and reach USD 2.44 trillion by 2031, growing at a CAGR of 12.72% over 2026-2031.

The sharp growth reflects a structural change in how insurers design, distribute, and service policies as digital-first experiences become table stakes. Cloud-native migrations, AI-enabled underwriting, and embedded insurance have shifted from pilot initiatives to enterprise standards, allowing carriers to cut operating costs, improve speed-to-market, and reach new customer segments. Government sandboxes in more than a dozen jurisdictions have accelerated solution rollouts, while strategic partnerships with mobility and IoT platforms are redefining risk assessment in auto and property lines. Competitive differentiation now rests on data access, platform agility, and the ability to embed coverage seamlessly into non-insurance purchase journeys, rather than on balance-sheet scale alone.

Key Report Takeaways

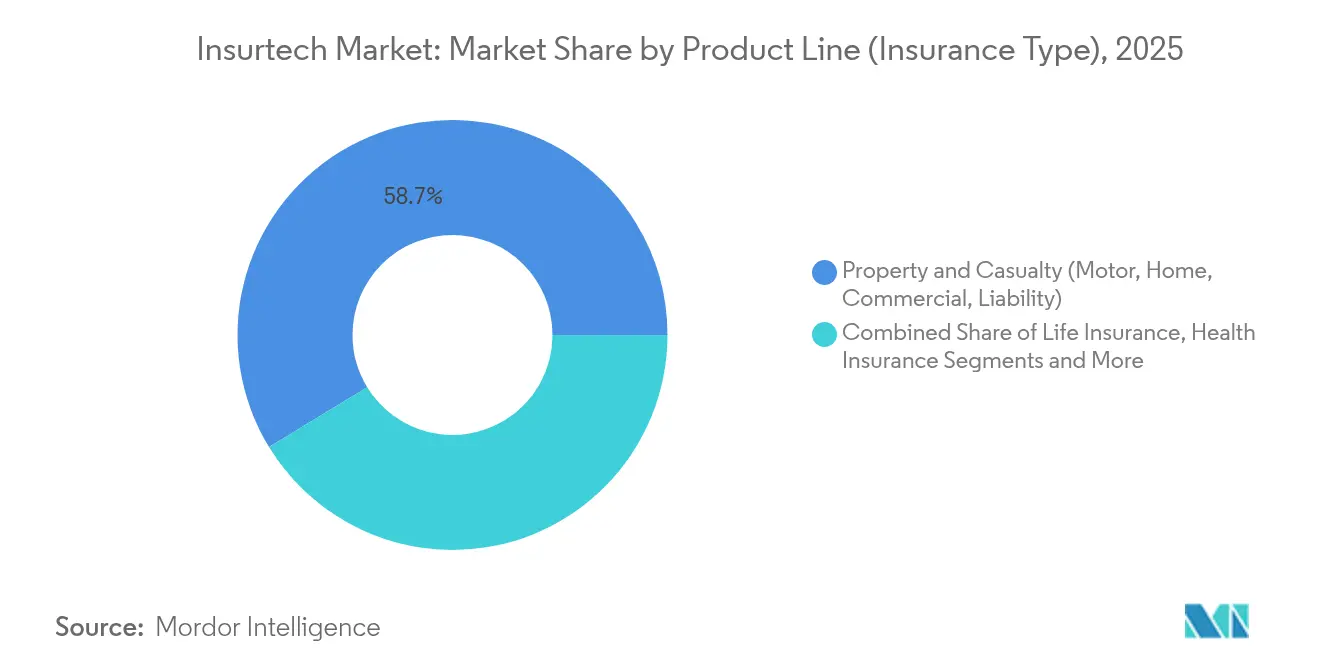

- By product line, Property & Casualty led with 58.73% of the insurtech market share in 2025, while Specialty Lines are projected to post the fastest 18.63% CAGR through 2031.

- By distribution channel, Traditional Agents/Brokers held 40.62% revenue share of the insurtech market in 2025, whereas Embedded Insurance Platforms are advancing at a 16.78% CAGR to 2031.

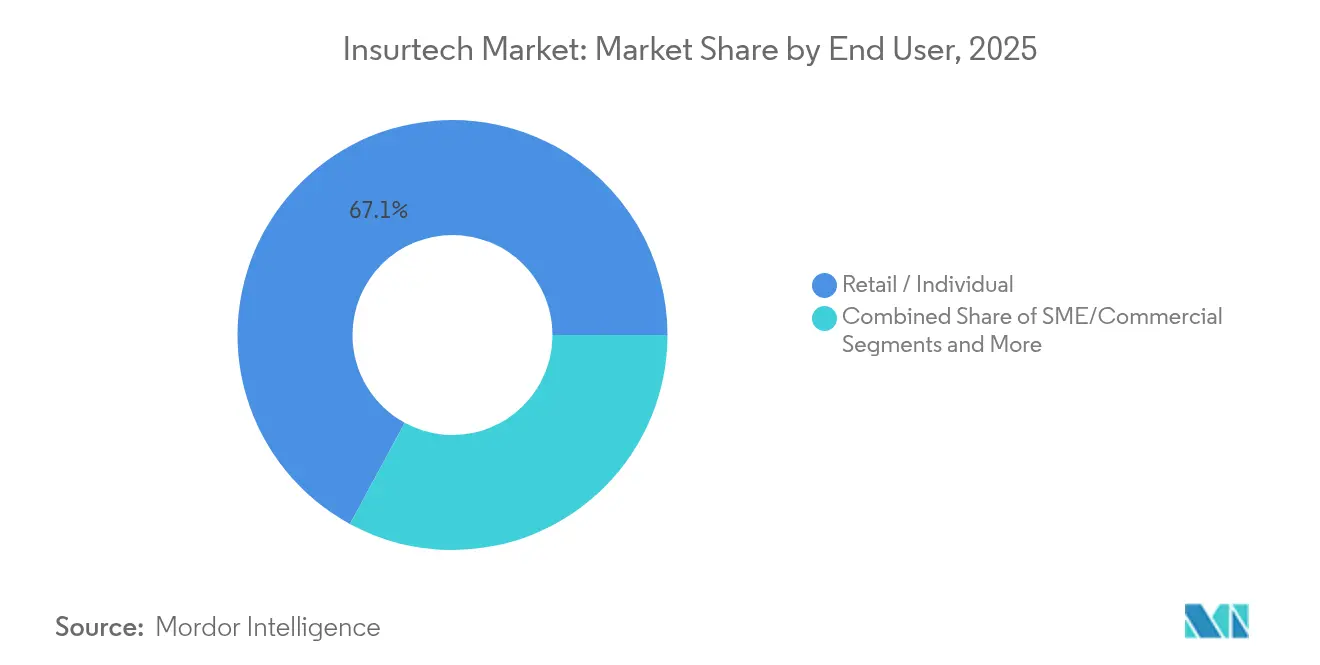

- By end user, Retail/Individual policies accounted for 67.08% of the demand of the insurtech market in 2025; the SME/Commercial segment is forecast to grow at 15.18% CAGR to 2031.

- By geography, North America commanded 37.25% of the insurtech market in 2025, yet Asia-Pacific is poised for the highest 16.25% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Insurtech Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising adoption of AI & ML for underwriting & claims | 3.2% | Global, with North America and Europe leading | Medium term (2-4 years) |

| Growing demand for personalized, on-demand insurance products | 2.8% | Global, particularly strong in APAC and North America | Short term (≤ 2 years) |

| Increasing migration to cloud-native core systems | 2.1% | Global, with Europe and North America at the forefront | Medium term (2-4 years) |

| Regulatory sandboxes accelerating product launches | 1.5% | Europe, Asia-Pacific, selective North American states | Short term (≤ 2 years) |

| Data partnerships with mobility & IoT platforms | 1.8% | Global, with Europe leading due to the regulatory framework | Long term (≥ 4 years) |

| Rapid growth of embedded distribution models | 2.4% | Global, with Asia-Pacific showing the highest adoption | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising adoption of AI & ML for underwriting and claims

AI-driven decision engines now automate large portions of policy issuance and claims triage, shrinking average handling times and improving predictive accuracy. Swiss Re reported that shifting its claims analytics to Microsoft Azure enabled the majority of infrastructure automation, cutting assessment time in half. Insurers that master supervised learning on proprietary datasets gain defensible underwriting moats, pushing competitors to accelerate data-engineering roadmaps. The technology also unlocks new micro-duration products, such as usage-based mobility cover, because risk can be priced in real time. As regulators grow comfortable with explainable models, AI penetration is expected to rise fastest in personal auto, small commercial, and cyber lines. Vendor ecosystems offering pre-trained models on cloud marketplaces further lower adoption barriers.

Growing demand for personalized, on-demand insurance products

Consumers increasingly expect insurance to mimic e-commerce checkout flows, selecting coverage amounts and durations as easily as adding items to a cart. Allianz’s partnership with Cosmo Connected embeds accident coverage in connected helmets for a fixed monthly fee, illustrating how IoT data can trigger automatic policy activation without paperwork [1]Allianz SE, “Connected Vehicle Data and the Future of Auto Products,” allianz.com. Parametric products are likewise filling gaps in travel, agriculture, and climate risk because they pay when predefined triggers hit, sidestepping lengthy claims adjustment. Marketplaces that bundle ancillary value-added services, such as health coaching or cyber monitoring, see higher renewal rates because propositions resonate with everyday needs. This shift forces carriers to re-platform legacy policy administration so riders and limits can adjust dynamically, moving away from static annual contracts.

Increasing migration to cloud-native core systems

Core-system modernisation has become an operational imperative as CFOs target double-digit cost savings and CIOs pursue elastic compute to scale AI. Lincoln Financial Group completed a phased move of 120 on-premise systems to a multi-cloud architecture in under two years. Europe’s AXA Germany achieved 25% faster batch processing after finalising its cloud transition, proving that regulated entities can meet stringent data-residency rules while leveraging modern DevSecOps pipelines [2]AXA Deutschland, “Cloud-Native Conversion Milestones,” axa.de . Faster environment spin-up accelerates product launches, allowing teams to iterate coverage and pricing weekly instead of quarterly. Cloud adoption also facilitates cross-border rollouts because microservices can be reused in multiple jurisdictions without duplicating infrastructure. Over the forecast horizon, insurers without cloud-native cores risk uncompetitive expense ratios.

Regulatory sandboxes accelerating product launches

Insurance regulators are increasingly adopting sandbox regimes to spur innovation without compromising consumer protection. The UK Financial Conduct Authority’s sandbox admitted three new insurtechs in 2025, enabling limited-scope pilots under supervisory oversight. In the United States, Kentucky’s Insurance Innovation Sandbox provides time-boxed regulatory relief, attracting start-ups seeking nationwide expansion paths[3]Commonwealth of Kentucky, “House Bill 386 Insurance Innovation Sandbox,” kentucky.gov. Sandbox cohorts typically graduate to full licences faster because regulators familiarise themselves with product designs during trial phases. Successful frameworks encourage reciprocal agreements, allowing firms to transplant approved models across borders, thereby shortening market-entry timelines. As more jurisdictions formalise innovation pathways, regulatory risk becomes less of a bottleneck in scaling digitally native propositions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy core-system integration complexity | -2.1% | Global, particularly acute in North America and Europe | Medium term (2-4 years) |

| Regulatory & compliance fragmentation | -1.8% | Global, with cross-border operations most affected | Long term (≥ 4 years) |

| Re-insurance capacity constraints for MGAs | -1.4% | North America and Europe, spreading to other regions | Short term (≤ 2 years) |

| Investor pivot from "growth at all costs" to profitability | -2.3% | Global, with venture capital markets most impacted | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Legacy core-system integration complexity

Decades-old mainframes often lack modern APIs, making real-time data exchange expensive and risky. Carriers, therefore, face a trade-off between wholesale replacement and piecemeal wrap-and-renew approaches. Failed conversions can stall policy issuance or claims payouts, eroding customer trust and drawing regulator scrutiny. Integration projects also carry hidden costs when data lineage and audit trails need preservation for compliance. As a result, some incumbents partner with greenfield entities instead of renovating core estates, slowing digital change within the mothership.

Regulatory and compliance fragmentation

Unlike banking, insurance lacks a global Basel-style accord, so capital, solvency, and distribution rules diverge widely. Companies expanding into multiple jurisdictions must customise policy wordings, disclosure formats, and complaint processes country-by-country, raising cost-to-serve. Data-localisation statutes further complicate multi-cloud deployments because customer records must reside within national borders. Small insurtechs often redirect resources from product development to regulatory counsel, diluting innovation velocity. Harmonisation progress remains slow, suggesting compliance drag will persist over the long term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Line: Specialty Lines outpace mature P&C growth

Property & Casualty dominated revenue with a 58.73% insurtech market share in 2025, reflecting entrenched auto and homeowner demand foundations. Nonetheless, Specialty Lines, encompassing cyber, pet, marine, and travel, are forecast to expand at a 18.63% CAGR through 2031, delivering the fastest incremental premium. Embedded IoT sensors and parametric triggers allow Specialty products to circumvent traditional loss-adjustment delays, creating superior customer experiences that command higher margins. Carriers such as AXA XL have already debuted generative-AI cyber covers to address data-poisoning exposures arising from enterprise AI rollouts. As niche risks proliferate, Specialty innovators can capture outsized wallet-share increases, suggesting the insurtech market size for these lines will compound materially over the forecast window.

Property & Casualty incumbents, meanwhile, leverage telematics to reclaim pricing precision, yet their extensive legacy books create change-management headwinds. Life and Health insurers pilot accelerated underwriting on cloud platforms, but stricter mortality and morbidity regulations temper speed relative to non-regulated specialty covers. Reinsurers increasingly partner with cyber MGAs to collect proprietary claims datasets, improving portfolio modelling accuracy. Given the divergent growth curves, investors may shift capital allocations toward Specialty underwriters that demonstrate robust risk controls and scalable distribution frameworks.

By Distribution Channel: Embedded models challenge agent dominance

Traditional Agents/Brokers still commanded 40.62% of the 2025 premium, proving that relationship-based advice remains valued. However, embedded channels are set to post a 16.78% CAGR, positioning them as the structural growth engine of the insurtech market. E-commerce, airline ticketing, and ride-sharing apps now integrate one-click coverage, shrinking quote-to-bind times significantly as compared with manual processes. Digital brokers complement the movement by providing API bridges that surface multiple carrier quotes inside partner platforms, improving attachment rates without adding checkout friction. While direct-to-consumer portals gain traction in commoditised lines, they struggle in complex commercial risks where advisory depth matters, keeping agents relevant.

Aggregators and marketplaces exploit transparency regulation to encourage price competition, yet their commission-based economics invite disintermediation by carriers building native digital storefronts. Banks are reviving bancassurance via in-app offers tied to account-transaction triggers, broadening distribution without branch networks. For carriers, channel diversification mitigates concentration risk and captures incremental data at each customer touchpoint. The insurtech market size attributed to embedded sales is therefore projected to rise materially, even if absolute agent revenue continues to grow in lockstep with overall premium expansion.

By End User: SMEs emerge as digital adoption catalysts

Retail/Individual policyholders generated 67.08% of the 2025 premium, underscoring the outsized contribution of personal lines. Nonetheless, the SME/Commercial cohort is on course for a 15.18% CAGR because vertical SaaS integrations dramatically reduce acquisition costs for policies under USD 5,000 annual premium. Cloud accounting platforms and e-commerce suites embed general liability or shipping cover at invoice creation, moving insurance purchase from afterthought to workflow staple. For large enterprises, captive programmes and risk analytics platforms deliver self-insurance efficiencies but limit third-party premium growth, aligning carrier strategies toward mid-market niches.

SMEs historically lacked tailored products due to sparse loss data, yet IoT devices and open banking feeds now furnish underwriting signals that enable parametric and pay-as-you-use constructs. Embedded insurers partnering with point-of-sale vendors can secure daily micro-premiums, smoothing cash flow relative to lump-sum annual invoices. Government entities are also experimenting with digital procurement of infrastructure and crop-risk covers, creating public-sector proof points for insurtech market adoption. Over the forecast period, platforms able to aggregate fragmented SME demand are projected to capture an increasing insurtech market share by leveraging data-driven pricing.

Geography Analysis

North America retained 37.25% insurtech market share in 2025, benefiting from deep venture capital pools and established innovation hubs. State-level regulatory competition, exemplified by the Kentucky Insurance Innovation Sandbox, accelerates pilots that often expand nationwide after proof-of-concept results meet solvency criteria. US auto insurers remain early adopters of telematics, while Canadian carriers deploy cloud-native policy administration to overcome geographic service dispersion. M&A activity intensifies as incumbents buy capabilities; Munich Re’s USD 2.6 billion purchase of Next Insurance marked a notable 2025 expansion into US primary lines. Although market maturity constrains headline growth, North American carriers drive profit through operating expense reductions and cross-selling of ancillary cyber and identity-protection bundles.

Asia-Pacific, forecast to grow 16.25% annually to 2031, benefits from high smartphone penetration, government-backed fintech policies, and limited legacy system drag. China and India liberalised foreign ownership caps, encouraging global insurers to localise AI underwriting engines on hyperscale clouds with regional data centres. Singapore’s Monetary Authority operates a well-defined sandbox and grants digital composite licences that cover life, general, and health, accelerating regional scaling. Japanese carriers tackle longevity risk with AI-enabled annuity pricing, and South Korean platforms integrate usage-based mobility cover into ride-hailing super-apps. Lower insurance penetration leaves ample headroom for first-time buyers, so embedded micro-policies sold alongside e-commerce purchases drive volume even at modest ticket sizes.

Europe sustains steady single-digit growth anchored by GDPR-aligned data-governance frameworks, which give local insurtechs credibility on privacy. The forthcoming EU Data Act will mandate standardised vehicle data access, further catalysing telematics product innovation. The UK pursues post-Brexit regulatory agility, enabling faster product approvals while remaining Solvency II-equivalent for cross-border capital relief. Germany’s industrial base spurs demand for advanced commercial and cyber risk solutions, whereas France’s sizeable personal-lines market supports scale economics for behavioural-based pricing. As ESG disclosure rules tighten, European carriers innovate parametric climate-risk covers for agriculture and renewable-energy projects, creating exportable frameworks for other regions.

South America along with the Middle East & Africa remain nascent but promising. Mobile-money ecosystems in Brazil, Kenya, and Nigeria increasingly bundle micro-accident and hospital-cash products, leapfrogging traditional agency networks. Government-to-person payment platforms provide instant premium-collection rails, de-risking small-ticket offerings. Sovereign risk pools in the Caribbean and East Africa adopt parametric hurricane and drought solutions that trigger emergency funds within 24 hours, validating proof of concept for broader disaster markets. International development agencies often co-underwrite early portfolios, encouraging private carriers to enter once loss-frequency models mature.

Regulatory Landscape

The regulatory environment for insurtech is tightening around AI governance, operational resilience, and prudential oversight, while continuing to preserve innovation pathways such as sandboxes. In the European Union, the AI Act (Regulation (EU) 2024/1689) classifies certain AI uses in insurance, including risk assessment and pricing in life and health insurance, as high-risk. This classification is pushing carriers and insurtech vendors toward stronger model governance, human oversight, and bias controls.

EIOPA reinforced this direction in February 2026 with its Generative AI Market Survey, based on responses from 347 undertakings across 25 countries, and in March 2026 its Board of Supervisors agreed targeted suggestions to clarify how the AI Act applies within insurance to support coherent supervision. Globally, the International Association of Insurance Supervisors (IAIS) adopted the Insurance Capital Standard (ICS) in December 2024 as a globally comparable, risk-based capital measure for internationally active insurance groups, and its January 2026 Roadmap for 2026-2027 emphasizes finalizing ICS-related standards for supervisory reporting and public disclosure. In parallel, jurisdiction-specific frameworks continue to shape market entry and scaling, from EU recovery and resolution rules (Directive (EU) 2025/1) to country-level insurance rulemaking such as the UAE’s federal insurance regulations, contributing to compliance fragmentation that insurtechs must manage when expanding cross-border.

Value Chain Analysis

The insurtech value chain begins with data and distribution signal capture (telematics, IoT, mobility platforms, e-commerce, and vertical SaaS), then moves through digital front ends such as embedded insurance platforms, aggregators, and digitally enabled agents and brokers. It ultimately feeds into the core insurance functions delivered by carriers and MGAs, including pricing, underwriting, policy administration, and claims. Technology suppliers provide the operating fabric, including cloud infrastructure, core-system modernization platforms, AI/ML underwriting and claims engines, identity and fraud tools, and integration layers (APIs and middleware). Upstream, reinsurers and capital providers shape product economics through quota share and excess-of-loss structures, while third-party administrators and other service partners (repair networks, healthcare providers, and cyber incident response) handle fulfillment and loss mitigation.

Bottlenecks increasingly show up at governance and integration points rather than in software availability alone. Regulatory and supervisory attention to AI controls and cyber risk is filtering through the chain, including the NAIC pilot of an AI Systems Evaluation Tool across 12 states beginning in January 2026 to assess AI governance during market conduct exams. In 2026, NYDFS advisories also urged stronger cyber risk assessments as frontier models broaden threat surfaces. In emerging markets, operational requirements can be equally binding: Nigeria’s NAICOM issued insurtech operational guidelines effective August 1, 2025, with a 30-day compliance window, affecting licensing readiness, local partnerships, and onboarding timelines for platforms. Across geographies, legacy core integration, audit trails, and model risk management remain persistent friction points that influence how quickly insurtech capabilities move from pilots into scaled production.

Competitive Landscape

The current competitive landscape exhibits moderate fragmentation, with the top five players collectively accounting for a limited market share. This scenario presents substantial opportunities for differentiation and strategic positioning. Players cluster into three archetypes: incumbent carriers digitizing cores, born-digital full-stack insurers, and technology vendors selling SaaS modules. Incumbents leverage brand trust and balance-sheet heft but must modernize legacy estates to match the insurtech market’s agility. Born-digital firms prize rapid iteration and often specialize in a single line before broadening through multi-risk platforms. Technology vendors, including DXC Technology and Microsoft Azure partners, monetize migration toolkits and AI accelerators that enable carriers to leapfrog multi-year waterfall projects.

Strategic activity intensified in 2025 as reinsurers moved downstream to secure data access and underwriting talent; Munich Re’s integration of Next Insurance into ERGO illustrates the trend. Meanwhile, Zurich’s minority stake in European auto-insurance Ominimo demonstrates how incumbents hedge innovation risk through option-like investments that maintain future acquisition rights. Embedded-platform specialist Bolttech attained a USD 2.1 billion valuation after its Series C, signalling investor belief in orchestration layers that connect insurers and non-insurance brands. Despite funding pullbacks for early-stage ventures, scale-ups with positive loss ratios continue to attract capital, particularly when they expand into under-penetrated APAC or LATAM markets. Over time, competitive advantage will likely accrue to firms that combine proprietary data, modular tech stacks, and prudent re-insurance partnerships, positioning them to expand insurtech market share as consolidation gathers pace.

Insurtech Industry Leaders

Lemonade

Hippo Insurance

Root Insurance

Oscar Health

Bright Health

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Near-term whitespace clusters around three build areas: (1) production-grade AI governance and controls for underwriting and claims, (2) embedded distribution infrastructure capable of supporting new verticals and geographies, and (3) core modernization and integration services that reduce time-to-launch for modular products. Regulatory change is also creating demand for controllable AI. In the EU, the AI Act’s high-risk classification for certain insurance AI systems and EIOPA’s 2026 focus on GenAI risk management are increasing needs for explainability, bias testing, monitoring, and human-in-the-loop workflows that can be audited across the policy lifecycle.

Market evidence indicates buyers and vendors are funding these build areas. In April 2026, ACORD’s Insurance Digital Maturity Study found that only 7% of the largest insurers qualify as top digital competitors based on end-to-end digital capabilities, leaving room for platforms and integrators that can operationalize digital at scale from underwriting through claims. On the implementation side, Duck Creek Technologies acquired Send Technology Solutions in July 2026 to connect agentic underwriting orchestration into a core platform, and Infosys signed a definitive agreement in March 2026 to acquire Stratus, a P&C insurance technology consulting firm, highlighting ongoing demand for delivery capacity alongside software. Embedded protection is also attracting financing for scale and partnerships, with Cover Genius securing USD 100 million in financing in July 2026 to expand embedded protection and AI infrastructure, consistent with a shift toward one-click coverage inside non-insurance purchase journeys.

Recent Industry Developments

- July 2026: Duck Creek Technologies acquired Send Technology Solutions Ltd to integrate AI-native underwriting orchestration with its core platform. The deal strengthens Duck Creek’s ability to operationalize agentic underwriting workflows closer to policy administration, tightening the link between quote, bind, and servicing for carriers and MGAs adopting modular stacks.

- June 2026: Root, Inc. partnered with Hugo to integrate Root insurance into Hugo’s digital platform, expanding access to coverage options for drivers across 16 states. The partnership advances API-led distribution and illustrates how insurtech carriers are using platform integrations to reach underserved segments through digital-first purchasing journeys.

- July 2025: Munich Re acquired Next Insurance for USD 2.6 billion, moving a major reinsurer deeper into US primary small-business insurance through ERGO. The transaction broadened Munich Re’s access to SME underwriting and distribution data, reinforcing the downstream push by capacity providers to secure technology-enabled origination and risk insights.

Research Methodology Framework and Report Scope

Market Definition and Coverage

The insurtech market, as defined for this study, covers technology-led products and services that are used by insurers, intermediaries, and related partners to improve how insurance is sold, underwritten, and serviced, including claims and policy administration, across all major regions.

Scope exclusions: This sizing excludes the full value of insurance premiums and only counts insurtech-related technology value when it is directly tied to insurance workflows.

Segmentation Overview

- By Product Line (Insurance Type)

- Life Insurance

- Health Insurance

- Property & Casualty (P&C): Motor, Home, Commercial, Liability, etc.

- Specialty Lines (e.g., cyber, pet, marine, travel)

- By Distribution Channel

- Direct-to-Consumer (D2C) Digital

- Aggregators/Marketplaces

- Digital Brokers/MGAs

- Embedded Insurance Platforms

- Traditional Agents/Brokers (digitally enabled)

- Bancassurance (digitally enabled)

- Other Channels

- By End User

- Retail/Individual

- SME/Commercial

- Large Enterprise/Corporate

- Government/Public Sector

- By Geography (Value, USD Bn)

- North America

- Canada

- United States

- Mexico

- South America

- Brazil

- Peru

- Chile

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- BENELUX (Belgium, Netherlands, Luxembourg)

- NORDICS (Denmark, Finland, Iceland, Norway, Sweden)

- Rest of Europe

- Asia-Pacific

- India

- China

- Japan

- Australia

- South Korea

- South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- Rest of Asia-Pacific

- Middle East & Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Nigeria

- Rest of Middle East & Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with public signals that describe the insurance and digital adoption backdrop, and then we narrow it down to what can realistically be attributed to insurtech spending. For this, we use sources such as insurance supervisors and central banks for financial-system indicators, the OECD for insurance statistics, the World Bank for macro and digital access markers, the ITU for connectivity metrics, and the World Intellectual Property Organization for patent activity that helps validate technology focus areas.

We also review annual reports, investor presentations, and earnings transcripts of listed insurers and distribution firms to understand how digital budgets are being allocated and how fast operational modernization is moving. A paid subscription for company financials and intelligence is used to standardize revenue and ownership mapping, and a patent database is used to cross-check whether the technology themes being discussed are actually being filed and built. The above list is illustrative, and many other public sources were used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work is used to confirm which parts of technology spend are incremental to insurance processes, and which areas are general IT that should not be counted. We cover insurers, brokers and agencies, digital distributors, and enabling technology providers. For a global view, we also include viewpoints from APAC, EMEA, and the Americas so regional adoption differences are reflected in the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 12% | APAC: 51% |

| Mid tier: 47% | Functional/Unit leaders: 43% | EMEA: 29% |

| Smaller Players: 19% | Managers: 45% | Americas: 20% |

Market-Sizing & Forecasting

Our sizing logic uses top-down first, where insurance activity and digitization indicators are used to reconstruct the addressable technology value tied to insurance workflows, and then these totals are tested using selective bottom-up checks. The checks typically include sampled vendor revenue ranges, channel and partner splits, and simple ASP times volume approximations for common software and service bundles, which helps adjust for over-counting and missing categories.

Inputs used in the model include insurance penetration and premium pools by region, the share of policies originated or serviced through digital channels, claims frequency and automation intensity (especially in property and casualty), technology spending patterns disclosed by insurers, and observed pricing progression for software and managed-service bundles. Because adoption does not move in a straight line, we use scenario analysis for forecasting, and assumptions are aligned to what experts see for regulation-driven digitization, AI-enabled claims and fraud workflows, and the pace of cloud modernization. Where bottom-up visibility is weak in smaller markets, we fill gaps using peer-market proxies based on similar insurance density and digital adoption, and then we re-check with regional interview feedback.

Data Validation & Update Cycle

Outputs are validated through multiple passes, so large variances are not accepted unless they can be explained with a real market signal. We compare modeled values against independent indicators such as reported insurance IT spend direction, digital policy and claims volumes, and regional investment momentum, and then unusual jumps are reviewed again before sign-off.

The model is also re-tested when new regulation, a major funding cycle change, or a visible shift in insurer digital priorities occurs, since these events can move adoption assumptions quickly. Reports are refreshed annually, and before delivery an analyst runs a final check so the latest updates are reflected in the numbers clients receive.

Mordor Intelligence's Global Insurtech Market Size Compared With Other Published Estimates

Different published market values for insurtech can look far apart, even when they describe similar themes like digital distribution and automated claims. In most cases, the gap comes from what is counted as insurtech value, the year used as the reference point, and whether the figures are anchored to insurance premium scale or to technology supplier revenue.

Some external estimates stay narrow and mostly total the revenues of insurtech solution providers and platforms, which keeps the value in the tens of billions. For Mordor Intelligence, the number is built to reflect insurtech as technology applied across insurance lines and workflows, so it is sized at the activity-linked value layer rather than only vendor-side sales.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.34 T (2026) | |

| Global Consultancy A | USD 19.06 B (2025) | Uses a vendor-revenue lens focused on insurtech solutions and platforms, and the base year differs, which reduces scale versus workflow-linked value sizing. |

| Industry Publisher B | USD 17.83 B (2024) | Reported as sales revenue in US$ millions and anchored to a different year, and it appears to emphasize product revenue capture rather than insurance-activity based reconstruction. |

The spread in the table is mainly explained by scope and measurement unit choices, not by a disagreement that adoption is growing. When scope is clearly stated and cross-checked with insurance activity, digital process penetration, and pricing logic, the output becomes easier to replicate and easier to compare across regions and time.

Key Questions Answered in the Report

What is the current size of the insurtech market?

The Insurtech market stands at USD 1.34 trillion in 2026 and is forecast to reach USD 2.44 trillion by 2031 at a 12.72% CAGR.

Which product line is growing fastest within the Insurtech space?

Specialty Lines—including cyber, pet, marine, and travel—are projected to grow at a 18.63% CAGR, outpacing mature Property & Casualty offerings.

How significant is embedded insurance in upcoming distribution models?

Embedded platforms are expected to log a 16.78% CAGR through 2031, integrating coverage directly into e-commerce, travel, and SaaS workflows.

Why is Asia-Pacific viewed as the high-growth region for Insurtech?

APAC benefits from smartphone-first consumers, supportive fintech policies, and low existing insurance penetration, driving a 16.25% forecast CAGR.

What challenges do Insurtech's face when scaling internationally?

Fragmented regulatory regimes, legacy system integration, and fluctuating re-insurance capacity remain the main barriers to rapid cross-border expansion.

How fragmented is the competitive landscape?

Moderate fragmentation defines the current competitive scene; the largest five participants hold only a combined share, leaving ample whitespace for differentiation.

Page last updated on: