Market Overview

| Study Period | 2021 - 2031 |

|---|---|

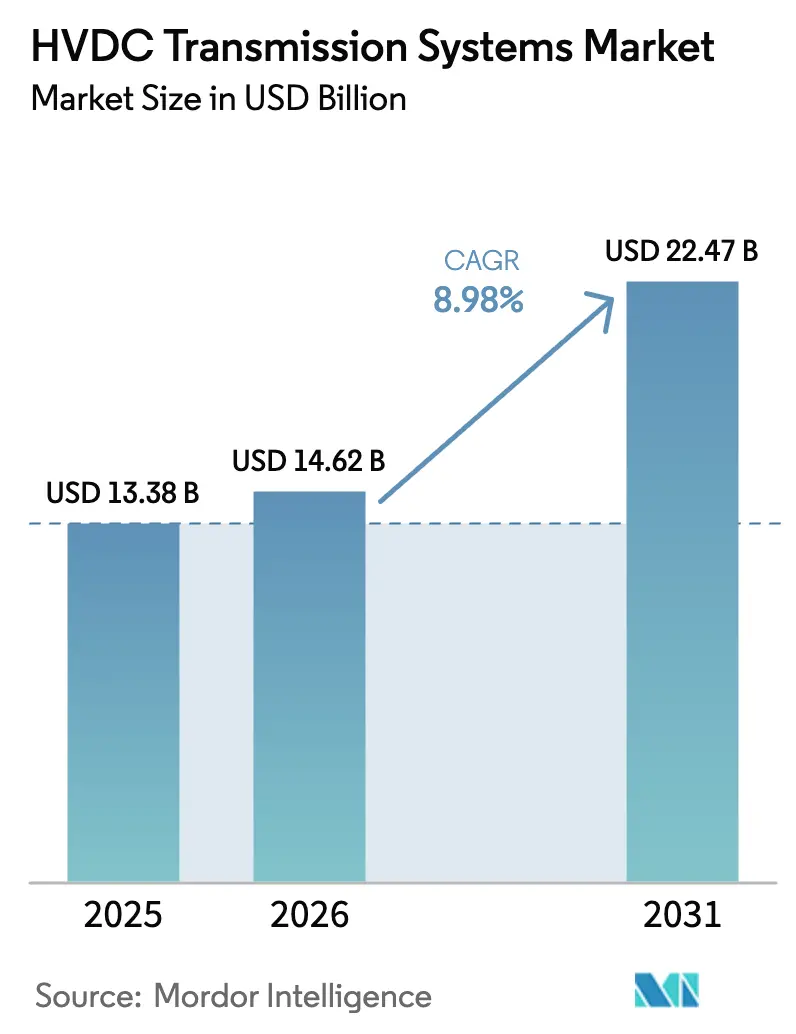

| Market Size (2026) | USD 14.62 Billion |

| Market Size (2031) | USD 22.47 Billion |

| Growth Rate (2026 - 2031) | 8.98% CAGR |

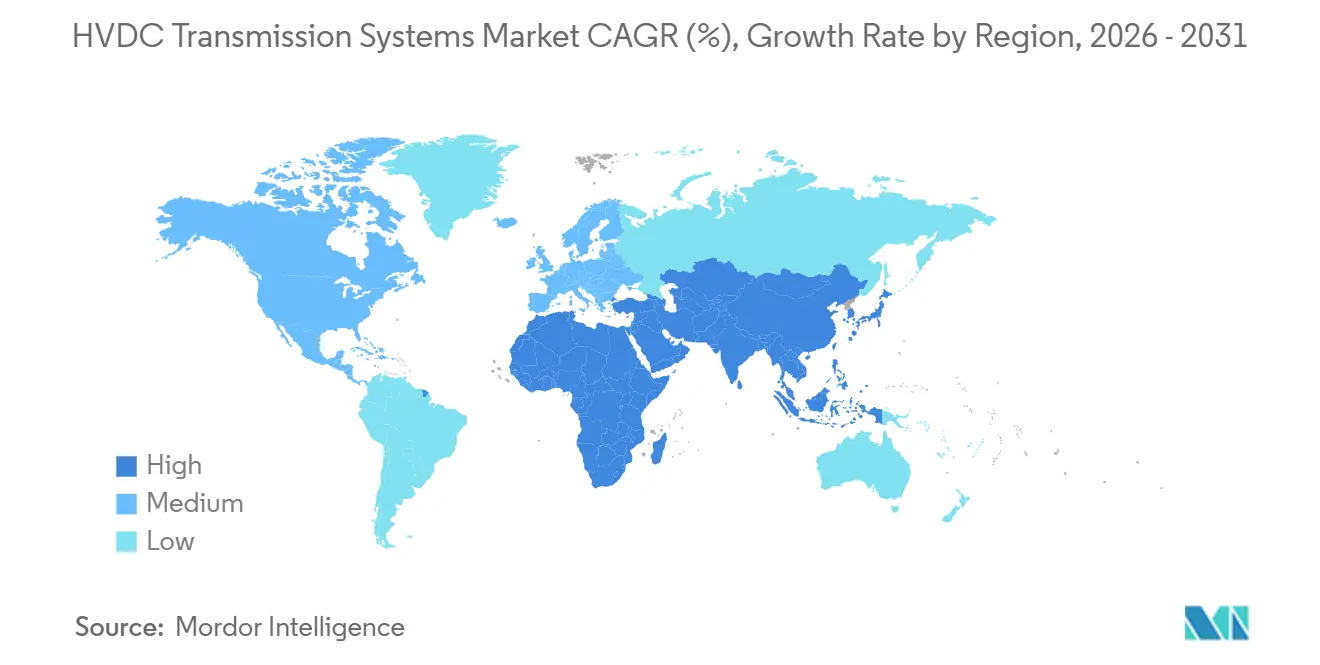

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

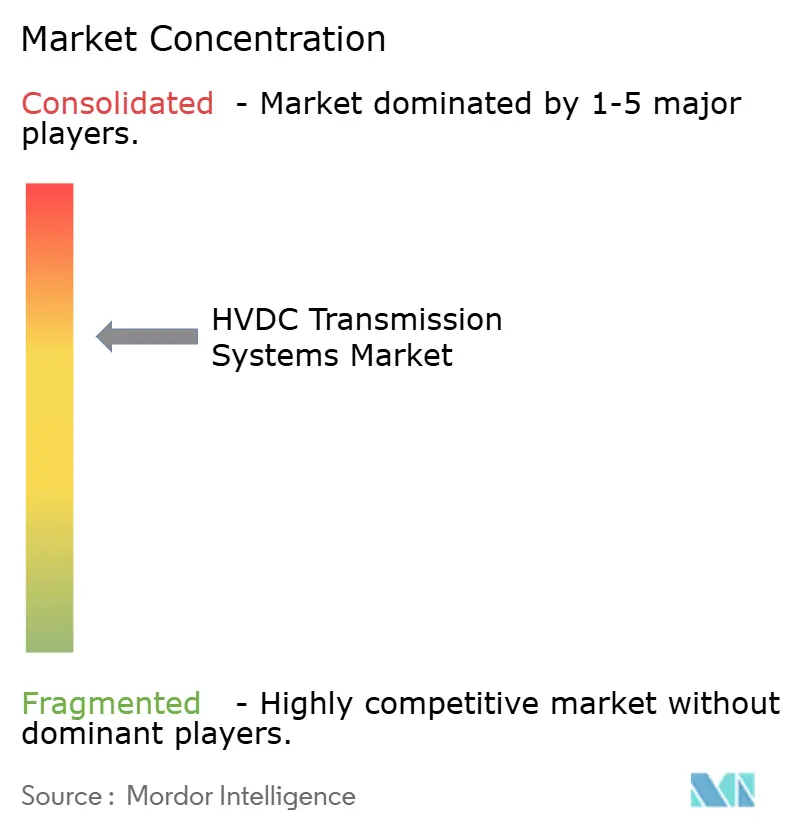

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

HVDC Transmission Systems Market Analysis by Mordor Intelligence

The HVDC Transmission Systems Market size is expected to grow from USD 13.38 billion in 2025 to USD 14.62 billion in 2026 and is forecast to reach USD 22.47 billion by 2031 at 8.98% CAGR over 2026-2031.

Strong capital spending on offshore wind export cables, ultra-high-voltage corridors in Asia, and grid-hardening programs in North America and Europe are steering this advance. Developers increasingly favor voltage-source converter (VSC) schemes because they inject or absorb reactive power without synchronous condensers, cutting both footprint and lifetime operating cost. Converter manufacturers are also capitalizing on an electronics refresh cycle: modular multilevel converter (MMC) stations using 6.5 kV IGBTs, reducing harmonic distortion to below 1% and enabling compliance with stricter grid codes. Meanwhile, cable suppliers are booking record orders as seabed routes outpace overhead corridors; each new gigawatt of offshore wind typically consumes up to 120 km of ±525 kV XLPE cable. A parallel driver is the replacement of aging 1960s-era alternating-current lines whose capacity no longer meets modern renewable build-out targets.

Key Report Takeaways

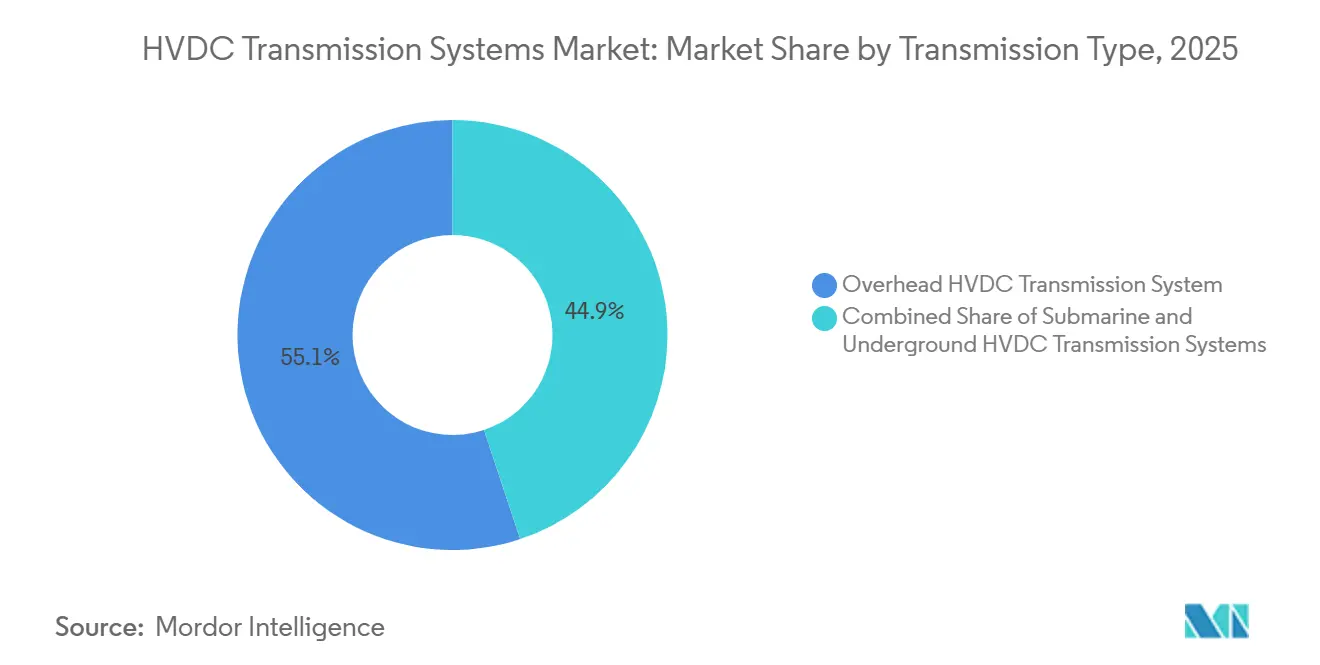

- By transmission type, overhead systems held 55.1% of the HVDC transmission systems market share in 2025, whereas submarine schemes are forecast to expand at an 11.3% CAGR to 2031.

- By component, converter stations captured 53.5% revenue in 2025; the accessories category is advancing at a 10.1% CAGR through 2031.

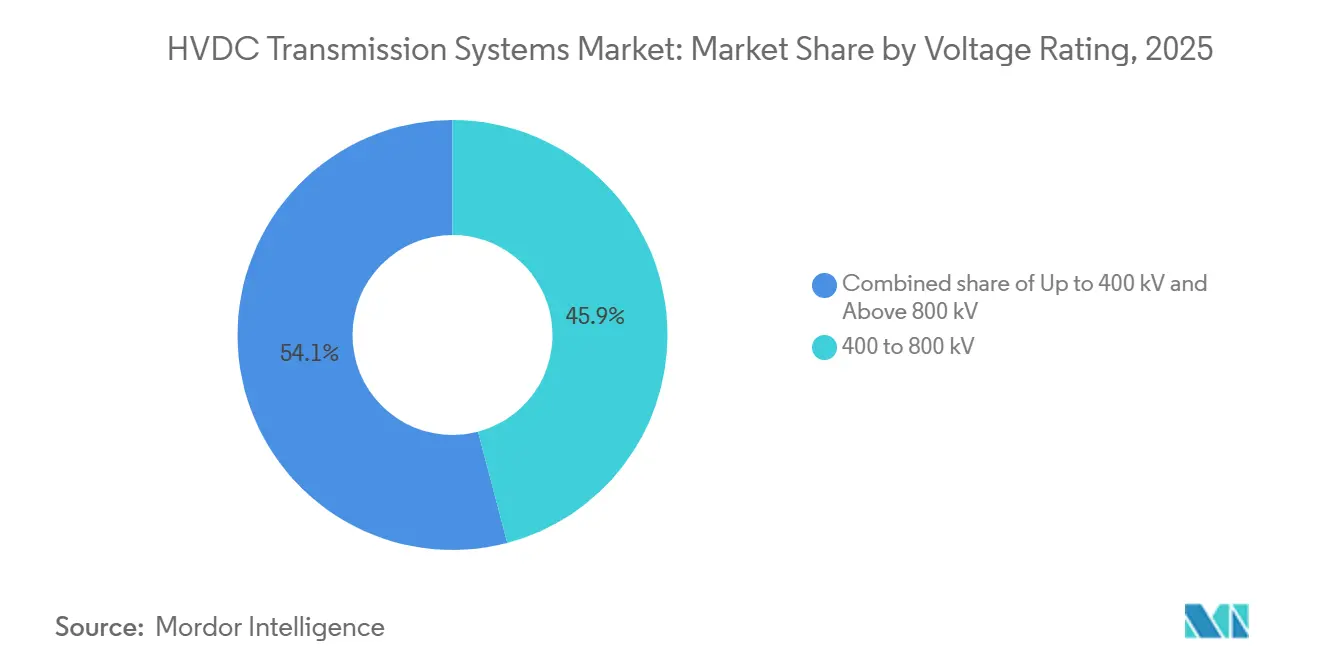

- By voltage rating, the 400 to 800 kV class accounted for 45.9% of installations in 2025, while the above-800 kV tier is expected to post an 11.6% CAGR by 2031.

- By geography, Asia-Pacific commanded 41.6% of 2025 revenue and is set to grow at a 9.9% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global HVDC Transmission Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing integration of renewable energy generation | +2.1% | Global, with concentration in APAC (China, India), Europe (North Sea offshore wind), North America (Atlantic coast offshore wind) | Medium term (2-4 years) |

| Aging grids & T&D reinvestment cycles | +1.8% | North America & Europe, with spillover to Australia and select Latin American markets (Brazil, Argentina) | Long term (≥ 4 years) |

| Need for long-distance, high-capacity interconnections | +1.6% | APAC core (China west-to-east corridors, India renewable zones), ASEAN cross-border, Middle East GCC grid | Medium term (2-4 years) |

| Electrification of offshore oil & gas assets | +0.9% | North Sea (Norway, UK), Middle East (Saudi Arabia, UAE), Southeast Asia (Malaysia, Indonesia) | Medium term (2-4 years) |

| Multi-vendor offshore wind HVDC hubs | +1.2% | Europe (North Sea Wind Power Hub, TenneT DC overlay), APAC (Taiwan, Japan floating wind), North America (Atlantic Shores) | Long term (≥ 4 years) |

| Defense-critical islanded power corridors | +0.5% | National, with early adoption in strategic island territories (Taiwan, Japan, Australia) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Integration of Renewable Energy Generation

Utilities are deploying HVDC corridors to relieve curtailment as variable renewables outpace local load absorption. China’s desert bases host 120 GW of wind and solar, yet local demand absorbs less than 30% of output; the ±800 kV Gansu–Zhejiang link now moves 8 GW across 2,383 km with only 3.2% losses, roughly half those on a 750 kV AC route. In offshore wind, VSC platforms export power beyond 40 km from shore, where AC export becomes uneconomic; the 3,600 MW Dogger Bank project validated this model in 2024. The United Kingdom, India, and Germany now mandate HVDC for renewable zones over 5 GW, accelerating new project sanctions. National regulators increasingly stipulate synthetic inertia delivery, favoring MMC converters that can modulate power within 50 milliseconds. These factors make renewable integration the single largest driver of the HVDC transmission systems market through 2031.[1]Central Electricity Authority of India, “Renewable Evacuation Guidelines,” ceaindia.gov.in

Aging Grids & T&D Reinvestment Cycles

North American and European utilities are replacing 1960s-era AC lines with HVDC to double capacity on existing rights-of-way. The U.S. Department of Energy reserved USD 2.5 billion in 2025 for HVDC corridors that bypass congested 345 kV interties.[2]U.S. Department of Energy, “Transmission Facilitation Program Funding,” energy.gov Germany’s SuedLink, re-scoped from overhead AC to underground ±525 kV HVDC, cut 15 years of local opposition and secured a 2028 go-live date. Brazil’s Furnas added modular multilevel converters to its Rio Madeira bipole, boosting transfer capacity by 1 GW without new conductors. Although converter stations cost USD 150 million to USD 300 million per GW, they defer even costlier parallel AC builds that face lengthy environmental reviews. Consequently, reinvestment cycles will prop up the HVDC transmission systems market for at least the next decade.

Need for Long-Distance, High-Capacity Interconnections

Economic dispatch favors HVDC once overhead lines exceed 600 km or submarine routes surpass 50 km. China’s Baihetan–Jiangsu ±800 kV link spans 2,087 km and moves 8 GW of hydropower, displacing coal generation that would emit 28 million tCO₂ annually. ASEAN’s 1,400 km Lao-Thailand-Malaysia-Singapore corridor plans to carry 3 GW by 2030. Australia’s 1,500 MW Marinus Link chose HVDC after AC studies showed the need for three parallel cables and reactive compensation platforms costing AUD 1.2 billion more. Bidirectional flow capability also underpins the 3 GW Saudi-Egypt link, which balances seasonal peaks across the Red Sea. These examples illustrate how long-haul corridors continue to expand the HVDC transmission systems market.

Electrification of Offshore Oil & Gas Assets

Regulators are placing carbon-pricing pressure on offshore installations powered by gas turbines that emit up to 20 million tCO₂ yearly in the North Sea alone. Norway now requires shore-power evaluations for all new fields, prompting 450 MW of HVDC orders covering Johan Sverdrup, Johan Castberg, and Snorre. Saudi Aramco followed in 2025 with two 300 MW VSC links to the Marjan and Berri complexes, freeing associated gas for petrochemical feedstock. Economics hinge on carbon prices above EUR 90 per tonne, where avoided emissions offset converter capital cost over a 15-year field life. Even in lower-priced carbon regimes such as Malaysia, operators have begun feasibility studies to hedge against future regulation. Such projects add a specialized but expanding niche to the HVDC transmission systems market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront capital & permitting hurdles | -1.4% | Global, with acute impact in North America (NEPA reviews), Europe (cross-border approvals), Latin America (financing constraints) | Short term (≤ 2 years) |

| Distributed & behind-the-meter generation growth | -0.7% | North America, Europe, Australia (rooftop solar penetration), with emerging impact in India and Southeast Asia | Medium term (2-4 years) |

| Global shortage of XLPE / MI HVDC cable core | -1.1% | Global, with supply bottlenecks concentrated in Europe (Prysmian, Nexans, NKT production lines) | Short term (≤ 2 years) |

| Lack of interoperability standards for multi-vendor MT-HVDC | -0.6% | Europe (North Sea hubs), APAC (China-ASEAN interconnections), North America (offshore wind meshed grids) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Capital & Permitting Hurdles

Converter stations cost 50%–70% more per MW than comparable AC substations, and permitting often exceeds four years. The 1,250 MW Champlain Hudson Power Express required 14 years of approvals, pushing costs from USD 2.2 billion to USD 3.9 billion. Germany’s SuedLink saw its budget triple to EUR 10 billion after 27 route changes mandated by regulators. Emerging-market developers face higher financing costs: Brazil’s Belo Monte line needed 70% debt underwriting from BNDES because commercial banks balked at currency risk.[3]BNDES, “Belo Monte Transmission Financing,” bndes.gov.br

Distributed & Behind-the-Meter Generation Growth

Rooftop solar and residential batteries reduce peak-hour demand, weakening the utilization case for bulk transmission in mature economies. Behind-the-meter solar in California reached 18 GW in 2025, forcing curtailment of 2.4 TWh of utility-scale renewables and deferring planned HVDC links with Arizona.[4]California ISO, “2025 Annual Curtailment Report,” caiso.com Australia’s residential battery installations grew 40% in 2025, prompting a 1 GW downgrade of proposed interconnectors. Similar trends in Germany caused regulators to question the Ultranet HVDC corridor.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Transmission Type: Subsea Cables Outpace Overhead Growth

Overhead corridors held 55.1% of the HVDC transmission systems market share in 2025. They remain the least-cost option for long-haul terrestrial transfers; China’s ±800 kV lines deliver power at USD 0.012 per kWh per 1,000 km, roughly 40% below comparable AC rates. Yet environmental opposition and urban density are slowing new overhead builds. Germany buried SuedLink underground at a 35% cost premium to avoid a decade of litigation.

Submarine links are forecast to grow at an 11.3% CAGR between 2026 and 2031, the fastest among transmission types. Offshore wind pipelines in the North Sea alone require 60 km–120 km of export cable per gigawatt, keeping factories at Prysmian and Nexans booked well into 2029. Underground HVDC sits between the two, typically chosen where overhead rights-of-way face insurmountable opposition; Italy’s 1,000 MW Tyrrhenian Link accepted a 35% premium to preserve UNESCO sites.

By Component: Converter Stations Dominate, Accessories Accelerate

Converter stations garnered 53.5% of 2025 revenue because each GW of VSC capacity demands 400–600 IGBT submodules that can total USD 150 million–USD 300 million per GW. Although cable revenue ranks second, XLPE extrusion bottlenecks now cap cable growth at an 8.5% CAGR through 2031.

Accessories, control systems, DC breakers, and cybersecurity modules will rise at a 10.1% CAGR thanks to emerging meshed grids. Hitachi Energy’s hybrid breaker interrupts 16 kA in 2 milliseconds and has already logged 60 unit orders for North Sea projects.

By Voltage Rating: Ultra-High Voltage Gains Traction

Installations in the 400 to 800 kV band captured 45.9% of 2025 deployments. ±525 kV VSC links balance semiconductor losses with manageable converter costs, making them the default choice for offshore wind exports. Ultra-high-voltage systems above 800 kV will grow at an 11.6% CAGR during 2026-2031, driven by China’s ±1,100 kV corridors carrying 12 GW over 3,000 km with sub-7% losses.

Sub-400 kV links hold niche roles such as electrifying offshore platforms; Norway approved six ±320 kV projects totaling 1.8 GW since 2024. Each voltage class thus aligns to distinct application needs, collectively expanding the HVDC transmission systems market.

Geography Analysis

Asia-Pacific generated 41.6% of global revenue in 2025 and is expected to post a 9.9% CAGR to 2031. State Grid commissioned the 16 GW Baihetan–Jiangsu and Baihetan–Zhejiang lines in 2025, shrinking east-coast coal burn by 35 million t annually. India’s Phase-II Green Energy Corridors add 6 GW via the 1,830 km Raigarh–Pugalur link and three intra-state projects, cutting renewable curtailment from 12% in 2024 to below 3% by 2028. ASEAN’s 3 GW power-integration corridor and Australia’s 1.5 GW Marinus Link underscore regional momentum.

Europe follows with aggressive offshore mandates. The TEN-E regulation requires HVDC for any wind farm beyond 12 nautical miles, triggering EUR 8 billion of cable and converter orders since 2024. Germany’s SuedLink and A-Nord underground projects will send 8 GW southward by 2028, enabling lignite retirements. The UK’s Dogger Bank export cables and Eastern Link subsea route add another 7.6 GW of transfer capacity. Nordic hydropower balancing via NordLink and North Sea Link earned Norway EUR 500 million in arbitrage revenue during 2025.

North America remains bifurcated. Atlantic offshore wind requires radial HVDC exports, yet onshore converter permitting stretches three years, delaying Empire Wind to 2028. Cross-border schemes such as the 1.25 GW Champlain Hudson Power Express reached service in 2025, delivering Canadian hydropower into New York. Mexico’s Baja-Sonora study and Brazil’s long-distance corridors round out the hemisphere’s activity.

Competitive Landscape

The five largest converter suppliers, Hitachi Energy, Siemens Energy, GE Vernova, Mitsubishi Electric, and TBEA, collectively hold about 60% of global revenue, leaving room for regional challengers. Hitachi Energy leads VSC deliveries with 40% of the installed base and 60 hybrid DC breakers on order. Siemens Energy is vertically integrating IGBT fabrication, shaving converter costs by 12% and capturing recent Saudi contracts. Chinese firms dominate ultra-high-voltage LCC projects and leverage concessional financing from China Development Bank to win Southeast Asian bids.

Hybrid AC-DC software coordination has emerged as a white-space opportunity. GE Vernova’s Grid Software unit aims to supply the algorithms that balance power flows across dual networks. Medium-sized players such as Hyosung Heavy Industries and LS Cable target 200–400 MW shore-power packages, undercutting Tier-1 bespoke solutions by 20%. Product roadmaps reveal diverging bets: Siemens files patents on low-cost submodule designs, while Chinese suppliers focus on insulation breakthroughs for ±1,500 kV corridors.

HVDC Transmission Systems Industry Leaders

Siemens Energy AG

Nexans S.A.

Prysmian Group

ABB Ltd (Hitachi Energy)

GE Vernova, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Hitachi Energy India secured INR 11,594.3 crore Khavda–Nagpur HVDC award, its largest domestic order.

- January 2025: Saudi Arabia issued bids for 500 kV projects under the Vision 2030 infrastructure drive.

- June 2024: LS Cable & System began the mass production of 525 kV High Voltage Direct Current (HVDC) cables, which are to be used for TenneT’s 2 GW grid connection systems, BalWin4 & LanWin1.

- May 2024: LS Eco Advanced Cables has secured a long-term lease for a cable factory at the Port of Tyne in the United Kingdom. The company plans to invest USD 1,190 million in a high-voltage direct current (HVDC) factory at the Tyne Renewables Quay site in northeast England.

Global HVDC Transmission Systems Market Report Scope

High-voltage direct current (HVDC) power systems use direct current (DC) to transmit bulk power across large distances. HVDC lines are less expensive and have lower losses than AC lines for long-distance power transmission. It joins networks with varying frequencies and characteristics.

The HVDC transmission systems market is segmented by transmission type, component, voltage rating, and geography. By transmission type, the market is segmented into submarine, overhead, and underground HVDC transmission systems. By component, the market is segmented into converter stations, transmission medium, and others (including control systems, transformers, and ancillary equipment). By voltage rating, the market is segmented into up to 400 kV, 400 to 800 kV, and above 800 kV. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The report covers the market sizes and forecasts for the global HVDC transmission systems market across major countries within each region. For each segment, the market sizing and forecasts have been conducted on the basis of value (USD).

By Transmission Type

| Submarine HVDC Transmission System |

| Overhead HVDC Transmission System |

| Underground HVDC Transmission System |

By Component

| Converter Stations |

| Transmission Medium (Cables) |

| Others (Control & Protection Systems, Reactive Power Equipment, Accessories) |

By Voltage Rating

| Up to 400 kV |

| 400 to 800 kV |

| Above 800 kV |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Transmission Type | Submarine HVDC Transmission System | |

| Overhead HVDC Transmission System | ||

| Underground HVDC Transmission System | ||

| By Component | Converter Stations | |

| Transmission Medium (Cables) | ||

| Others (Control & Protection Systems, Reactive Power Equipment, Accessories) | ||

| By Voltage Rating | Up to 400 kV | |

| 400 to 800 kV | ||

| Above 800 kV | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the HVDC transmission systems market today?

It stood at USD 14.62 billion in 2026 and is forecast to reach USD 22.47 billion by 2031, reflecting an 8.98% CAGR.

Which segment holds the highest HVDC transmission systems market share?

Overhead corridors led with 55.1% share in 2025, mainly due to lower per-kilometer costs over long terrestrial routes.

What is the fastest-growing transmission type?

Submarine schemes tied to offshore wind are projected to grow at 11.3% CAGR between 2026 and 2031.

Why are converter stations the largest revenue contributor?

Each gigawatt of VSC capacity requires hundreds of power-electronic modules, pushing converter costs to USD 150 million–USD 300 million per GW.

Which region offers the strongest growth outlook?

Asia-Pacific is expected to expand at a 9.9% CAGR through 2031, driven by ultra-high-voltage corridors in China and India’s Green Energy Corridors.

Page last updated on: