Hand Blender Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

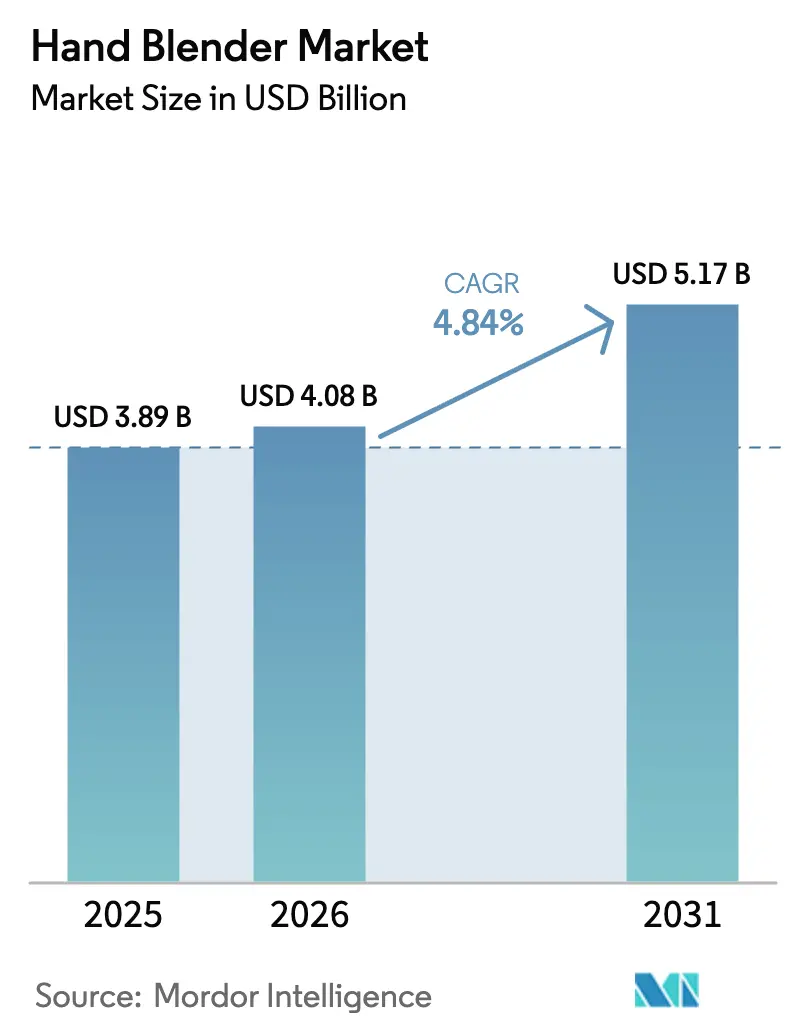

| Market Size (2026) | USD 4.08 Billion |

| Market Size (2031) | USD 5.17 Billion |

| Growth Rate (2026 - 2031) | 4.84% CAGR |

| Largest Market | Asia |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hand Blender Market Analysis by Mordor Intelligence

The global hand blender market size is expected to grow from USD 3.89 billion in 2025 to USD 4.08 billion in 2026 and is forecast to reach USD 5.17 billion by 2031 at 4.84% CAGR over 2026-2031. Steady gains come from urban living trends, lithium-ion cordless innovations, and greater preference for compact, multifunctional tools that suit smaller kitchens. The modest growth rate also signals resilience, given recent component shortages and tougher safety regulations that have affected many small appliance categories. Manufacturers continue to prioritize battery management systems, attachment versatility, and premium build quality to protect margins while broadening geographic reach. Strategic opportunities exist in Asia-Pacific’s fast-expanding urban centers, premium price tiers in mature markets, and commercial settings such as ghost kitchens that need portable blending equipment.

Key Report Takeaways

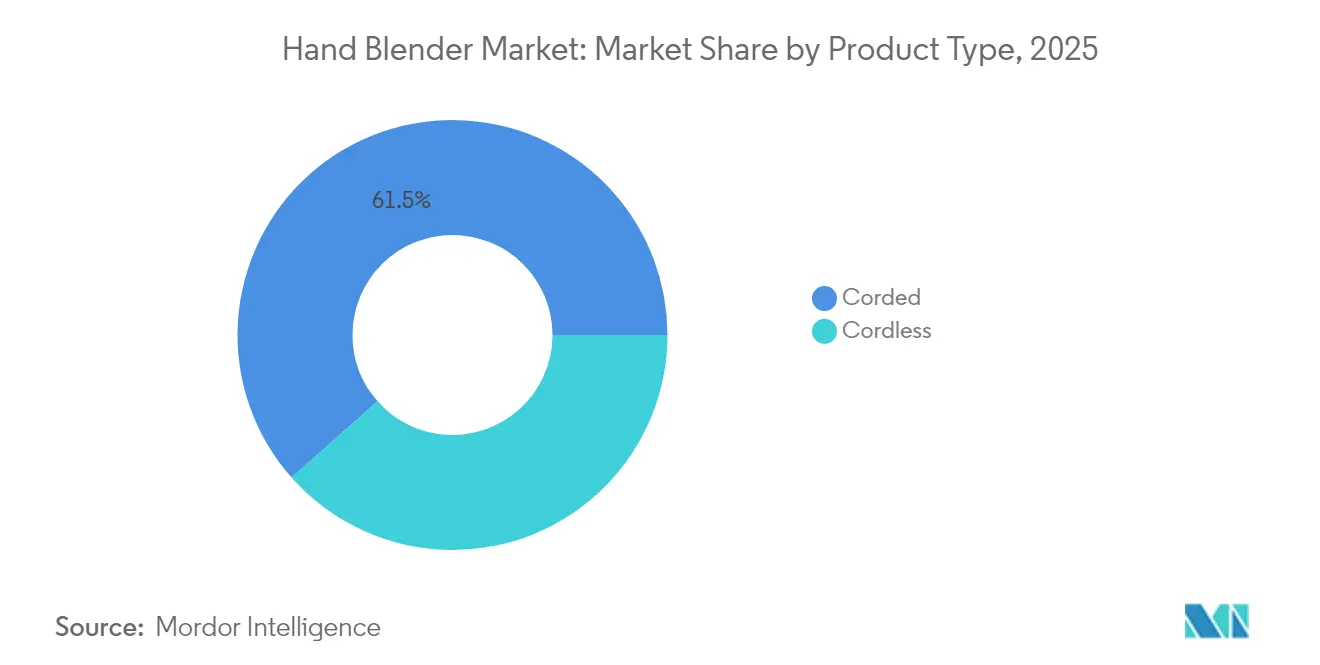

- By product type, corded models led with 61.54% of hand blender market share in 2025, whereas cordless units are projected to post the highest 7.55% CAGR to 2031.

- By end user, the residential segment accounted for 78.54% of the hand blender market size in 2025, while the commercial segment is set to expand at 7.31% CAGR through 2031.

- By distribution channel, offline retail held 55.98% of revenue in 2025; online retail shows the quickest 7.84% CAGR for 2026-2031.

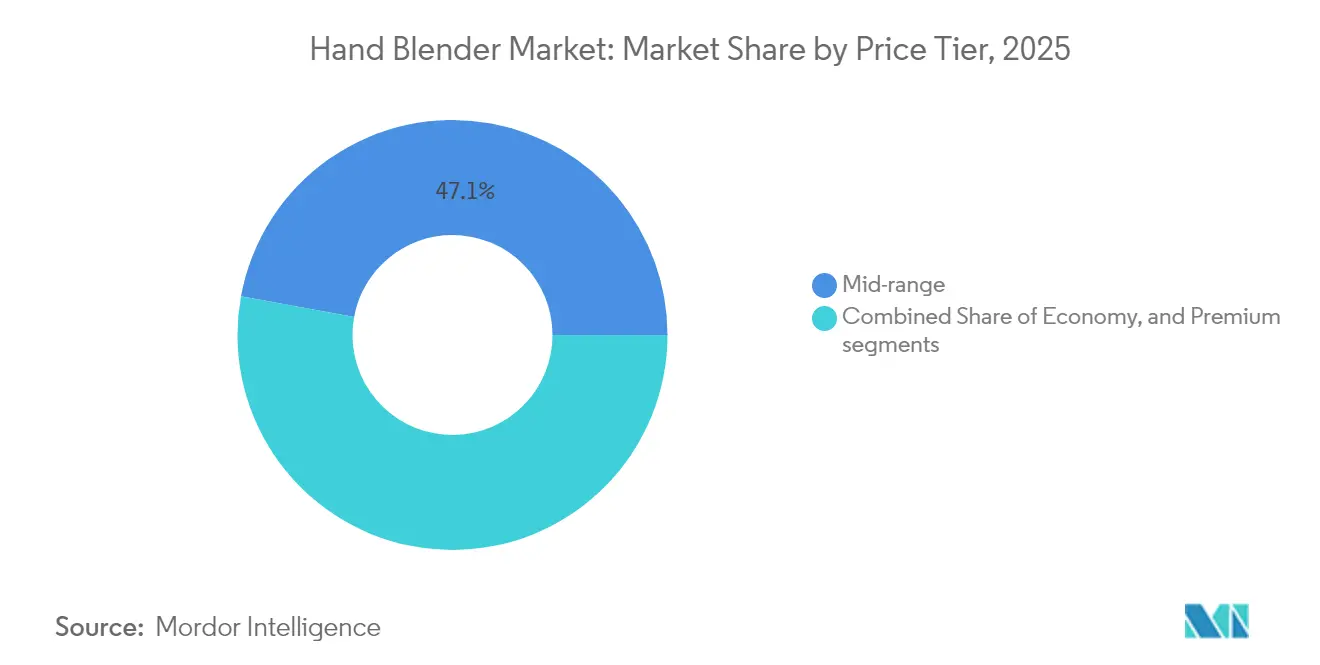

- By price tier, mid-range products (USD 40-100) commanded 47.12% of the hand blender market size in 2025; premium units (>USD 100) lead growth with a 8.95% CAGR.

- By application, soups and sauces retained 33.98% share of the hand blender market size in 2025, while smoothies and beverages advance at a 7.18% CAGR.

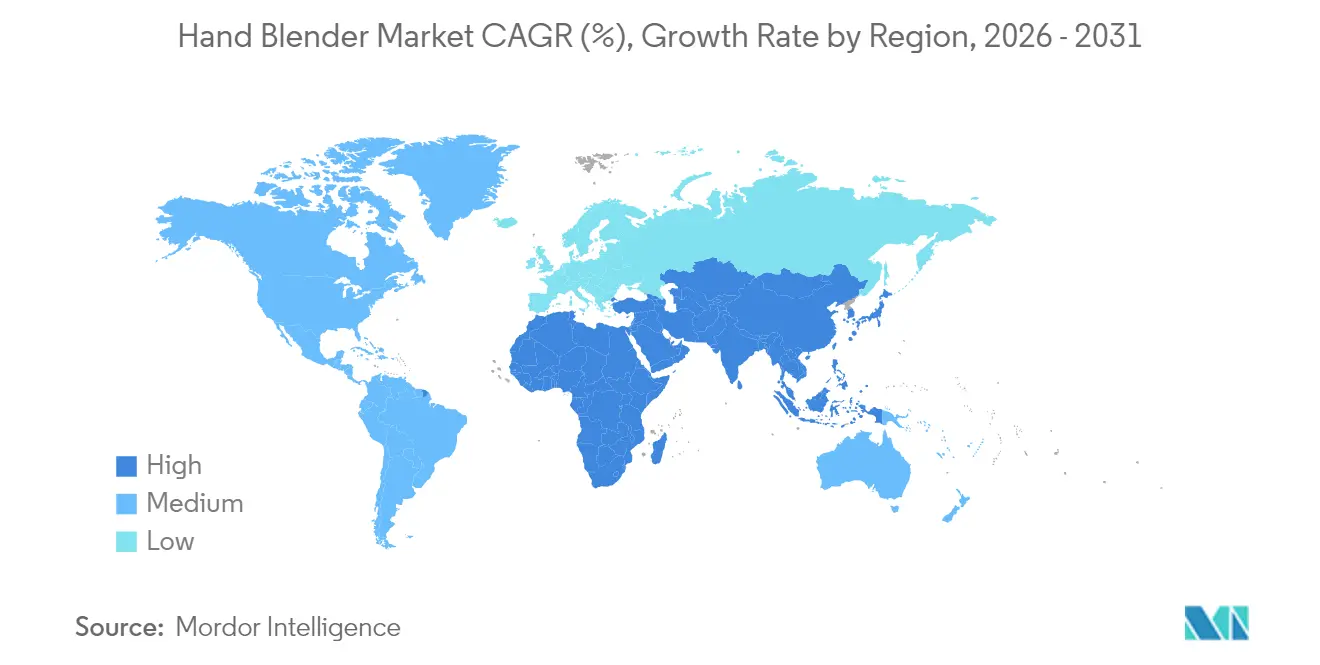

- By geography, Europe led at 36.02% revenue share in 2025; Asia-Pacific is the fastest regional climber at 7.60% CAGR to 2031.

- The hand blender market exhibits moderate concentration with the top 5 players—KitchenAid (Whirlpool Corp.), Braun Household (De'Longhi Group), Philips Domestic Appliances (Versuni), Breville Group, and Cuisinart (Conair Corp.)—commanding significant market share in 2024.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Hand Blender Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for compact appliances in urban kitchens | +1.2% | Global, concentrated in Asia-Pacific urban centers | Medium term (2-4 years) |

| Accelerating online retail penetration for small appliances | +1.0% | Global, led by North America and Europe | Short term (≤ 2 years) |

| Rapid innovation in cordless Li-ion hand blenders | +0.9% | Global, with early adoption in developed markets | Medium term (2-4 years) |

| Special-diet use cases (infant and elderly nutrition) | +0.7% | Developed markets, expanding to emerging economies | Long term (≥ 4 years) |

| Growth of ghost kitchens and small food-service formats | +0.6% | Urban centers globally, concentrated in Asia-Pacific | Short term (≤ 2 years) |

| Modular attachment ecosystems boosting upgrade sales | +0.5% | Premium segments in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Compact Appliances in Urban Kitchens

Dense housing and kitchen footprints of 50-70 sq ft in megacities are elevating the need for small, versatile tools, positioning hand blenders as space-efficient essentials. Developers of micro-kitchens in Tokyo, Mumbai, and London focus on modular layouts where every device must serve multiple uses. Consumers choose units with interchangeable accessories that swap whisking, chopping, and blending tasks while fitting into limited storage. The hand blender market therefore benefits from faster replacement cycles, as residents value devices that can adapt to restricted counter space. Retailers in Asia-Pacific urban clusters showcase compact appliance bundles, amplifying brand exposure and driving premium up-sell within the category. A mid-term sales tailwind emerges as urbanization spreads into Tier 2 cities that replicate the micro-home trend.

Accelerating Online Retail Penetration for Small Appliances

Digital storefronts enhance product storytelling through 360-degree views, live-stream demonstrations, and AI-driven comparison tools that clarify torque, noise, and runtime specifications. The online channel shortens decision cycles by aggregating verified user feedback and ease-of-return policies, nudging consumers toward affluent cordless SKUs. Subscription models for blades and seals add predictable income streams for brands while guaranteeing peak performance for users. North American and European buyers, already comfortable ordering high-ticket electronics online, are migrating small appliance purchases for the same convenience. The shift enables direct-to-consumer strategies that cut distribution layers and protect margins, a crucial gain amid rising production costs.

Rapid Innovation in Cordless Li-ion Hand Blenders

New cell chemistries now match corded peak wattage yet deliver 20-minute duty cycles, removing mobility constraints in kitchens without dedicated outlets. Brands are pairing optimized battery packs with high-efficiency brushless motors to sustain torque during viscous tasks such as nut butter or dough preparation. Supply chain volatility for lithium-ion cells, however, increases lead times and cost pressure, raising retail prices for premium cordless lines. Firms mitigate risk by dual-sourcing battery modules and developing proprietary management firmware that prevents over-discharge, extending product lifespan. The technology unlocks slimmer, more ergonomic handles that appeal to aging households seeking lightweight tools with reduced vibration.

Special-diet Use Cases (Infant and Elderly Nutrition)

Demographic shifts amplify demand for appliances able to produce fine, homogeneous textures suited to swallowing disorders and infant weaning. Hospitals and elder-care facilities integrate hand blenders into nutritional programs that require batch consistency and strict hygiene standards. Safety-certified plastics free of bisphenol A and intuitive one-hand controls cater to caregivers who need reliability under time constraints. Manufacturers are launching color-coded blades and jars to separate allergen-free and regular food preparation, reducing cross-contamination risk. Over the long term, the hand blender market sees new revenue from care-oriented SKUs with extended warranties and third-party validation from medical associations, lifting brand credibility.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Substitution threat from countertop blenders | -1.4% | Global, particularly in markets with larger kitchen spaces | Medium term (2-4 years) |

| Product-safety and durability recalls eroding trust | -1.1% | Global, with higher impact in regulated markets | Short term (≤ 2 years) |

| Li-ion battery supply constraints for cordless models | -0.8% | Global, affecting premium cordless segments | Short term (≤ 2 years) |

| Stricter energy-efficiency mandates raising costs | -0.6% | Europe and North America primarily | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Substitution Threat from Countertop Blenders

In regions where kitchens exceed 150 sq ft, owners gravitate toward high-horsepower countertop models that manage larger volumes and harder ingredients. Marketing for countertop blenders highlights full-jar stability and automated programs, diminishing the perceived value of handheld units. Retail promotions in North America often bundle countertop models with smoothie cups, reinforcing the one-appliance solution narrative. To counter the threat, hand-held brands spotlight precision control for small batches and direct-pot blending that avoids messy transfers. Designers also accentuate collapsible shafts that store in drawers, a feature that countertop machines cannot replicate.

Stricter Energy-Efficiency Mandates Raising Costs

Proposed Tier II eco-design rules in the European Union set maximum standby draw and minimum conversion efficiency benchmarks for all plug-in appliances [1]European Commission, “Ecodesign and Energy Labelling Working Plan 2022-2024,” ec.europa.eu. . Achieving compliance forces redesign around higher-grade magnetic materials, advanced power electronics, and low-resistance wiring. North American utilities encourage voluntary adoption of similar specifications through rebate schemes for energy-rated models. The hand blender market must manage a delicate price-feature balance, as cost increases may outweigh energy bill savings in buyers’ eyes. Manufacturers invest in lifecycle assessments to document emissions-reduction benefits, providing marketing support for higher prices.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Cordless Innovation Drives Future Growth

Corded units held 61.54% of the hand blender market share in 2025 with uninterrupted runtime, rugged motors, and familiar price points. Their leadership anchors the overall hand blender market with dependable revenue streams, especially from commercial and heavy home users. Cordless lines, while smaller in absolute value, post a strong 7.55% CAGR, signaling that lithium-ion maturity and ergonomic gains are resonating with consumers seeking cable-free cooking. The segment’s expansion will elevate the hand blender market size for cordless variants over the next five years, provided battery supply stabilizes.

Rapid growth also reshapes brand portfolios. Vendors now launch cordless flagships first, then cascade technology to lower tiers, re-energizing mid-cycle refreshes. Corded models counterbalance by featuring high-torque settings ideal for dense dough and prolonged kitchen tasks. Manufacturers pair them with specialty beaters and extended shafts targeted at professional kitchens. The coexistence of both formats keeps overall replacement rates healthy, supporting a robust hand blender market through diversified positioning.

By End User: Commercial Segment Accelerates Despite Residential Dominance

Residential buyers accounted for 78.54% of the hand blender market size in 2025 as small-batch cooking and post-pandemic culinary habits spurred purchases. Home chefs favor lightweight designs, dishwasher-safe parts, and multi-speed triggers. Advertising often pairs the blender with smoothie bowls and infant purees, reinforcing household versatility. Commercial kitchens, though starting from a lower base, advance at a 7.31% CAGR owing to ghost kitchen adoption and specialist cafés requiring compact yet rugged gear. This upswing steadily lifts the hand blender industry’s professional revenue slice, prompting suppliers to certify products for continuous duty cycles and NSF-compliant hygiene.

Restaurant operators seek models capable of four-hour daily usage, detachable stainless steel shafts, and sealed buttons to resist cleaning fluids. Manufacturers price such units above residential SKUs, buffering margins against broader cost inflation. As delivery-only venues spread across dense urban corridors, commercial penetration adds stability to overall sales, diversifying demand beyond household replacement cycles and bolstering the hand blender market.

By Distribution Channel: Online Retail Transforms Purchase Patterns

Offline outlets still held 55.98% of revenue in 2025, reflecting shoppers’ desire to physically test weight and grip. Big-box retailers promote bundle discounts with pots or slicing sets, encouraging impulse purchases. Yet online retail’s 7.84% CAGR underlines shifting discovery habits; buyers increasingly research torque ratings and noise-level data via mobile apps before deciding. Optimization of last-mile logistics reduces breakage rates for fragile shafts, alleviating a historical barrier. The hand blender market size derived from pure-play e-commerce will therefore climb incrementally, especially in post-purchase ecosystems where automatic accessory replenishment boosts lifetime value.

Web-based platforms run algorithmic promotions synchronized with health-trend spikes, for example post-holiday detox periods, spurring seasonal peaks. Offline chains counter with experiential setups featuring chef-led demos that showcase texture control for popular dishes. A blended omnichannel strategy emerges: shoppers watch livestream tutorials, inspect units in store, then finalize transactions online for home delivery. The dynamic keeps both routes relevant and supports balanced growth across the hand blender market.

By Price Tier: Premium Segment Leads Growth Despite Mid-range Dominance

Mid-range products captured 47.12% of the hand blender market size in 2025, serving pragmatic households that expect solid performance without luxury finishes. This tier benefits from scale manufacturing and feature trickle-down, extending sophisticated motors to accessible price points. Premium units priced above USD 100 grow at 8.95% CAGR, showing that affluent consumers value quieter operation, brushless motors, and full metal construction that remains cool during long blending sessions. Premium success pushes brands to invest in artisan-grade colorways and smart-connectivity chips, adding further differentiation.

Economy SKUs under USD 40 cater to first-time buyers and emerging markets but face tightening safety regulations and higher commodity costs, eroding already thin margins. Brands focusing on this tier pursue efficiency in assembly lines or partner with regional distributors to lower logistics expenditures. Over time, gradual consumer trading-up from economy to mid-range or premium benefits overall profitability in the hand blender market.

By Application: Health-conscious Trends Drive Smoothie Segment Growth

Soups and sauces retained 33.98% of the hand blender market size in 2025, anchored by long-established cooking habits that value in-pot blending for hot preparations. The category relies on consistent temperature-resistant shafts and splash-reduction bell shapes. Smoothies and beverages post a 7.18% CAGR; this trend aligns with social media-led wellness challenges and the rise of plant-based diets. Influencers demonstrate fast breakfast smoothies assembled directly in portable beakers, reinforcing blender mobility.

Baby food and bakery applications see stable demand linked to population dynamics and at-home baking booms. Each additional attachment—whisks, frothers, and slicers—broadens utility and encourages accessory upgrades, reinforcing ecosystem stickiness in the hand blender market.

Geography Analysis

Europe remained the largest contributor with 36.02% revenue share in 2025. Mature households replace older units frequently and gravitate toward premium models featuring energy-efficient motors to meet EU eco-design norms. Brands leverage European engineering credentials to justify pricing, and rigorous certification frameworks push continuous safety enhancements. Distribution remains evenly split between specialist kitchen stores and online outlets, sustaining balanced growth within the regional hand blender market.

Asia-Pacific, on a 7.60% CAGR trajectory, benefits from rising disposable income and dense urban expansion in China and India. Smaller kitchen footprints favor handheld multifunction tools over countertop equipment. Local manufacturing clusters offer cost advantages, supporting competitive pricing that accelerates category penetration. Cross-border e-commerce further widens access to global brands, though trade policy fluctuations and component sourcing challenges represent ongoing hurdles for the hand blender market in the region.

North America shows replacement-driven demand buoyed by premiumization and kitchen remodel trends that incorporate color-coordinated appliances. Competition from countertop models remains high, so manufacturers highlight precision control and easy storage to maintain relevance. South America and Middle East & Africa emerge more slowly due to macroeconomic volatility and limited retail infrastructure, yet urbanization unlocks pockets of future growth especially in middle-income segments. Suppliers adopting flexible voltage designs and region-specific plug types enhance accessibility, incrementally expanding the global hand blender market.

Competitive Landscape

Five leading companies—KitchenAid (Whirlpool Corp.), Braun Household (De'Longhi Group), Philips Domestic Appliances (Versuni), Breville Group, and Cuisinart (Conair Corp.)—hold a significant portion of 2024 sales, indicating moderate market concentration. Technology leadership is the principal battleground: brands race to optimize battery longevity, blade aerodynamics, and intuitive speed modulation. Intellectual-property acquisitions, such as De'Longhi’s cordless patents, safeguard differentiation and support premium pricing.

Sustainability ranks high on the innovation agenda. Electrolux partners with recycled-plastic suppliers to cut virgin-material content, aligning with EU circular-economy targets. Bosch’s 25% energy-use reduction underscores compliance readiness ahead of 2026 EcoDesign mandates [2]BSH Hausgeräte, “New Energy-Efficient Motor Technology,” bosch-home.com. . Meanwhile, Whirlpool’s USD 50 million connectivity fund accelerates IoT features that link KitchenAid with voice assistants, nurturing a services ecosystem around firmware updates and recipe libraries [3]Whirlpool Corporation, “Smart-Connectivity Investment Announcement,” whirlpoolcorp.com. . Moderate consolidation leaves niches for region-specific challengers that adapt shaft length and input voltage to local culinary practices, though the scale of global leaders poses formidable entry barriers.

A moderate level of consolidation leaves room for regional challengers that tailor designs to local culinary practices, for instance longer shafts for traditional South American stews. Partnerships with local influencers further localize marketing messages. However, the scale advantages of global leaders in supply chain and R&D funding continue to shape the competitive baseline in the hand blender industry.

Hand Blender Industry Leaders

KitchenAid (Whirlpool Corp.)

Braun Household (De’Longhi Group)

Philips Domestic Appliances (Versuni

Breville Group

Cuisinart (Conair Corp.)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Midea Group announced expanded global manufacturing with 17 R&D centers and 22 production sites to buffer supply-chain risks.

- December 2024: De'Longhi Group acquired additional cordless-appliance patents focused on battery management and motor efficiency.

- November 2024: Whirlpool Corporation invested USD 50 million in smart-appliance connectivity research for KitchenAid products.

- October 2024: Versuni introduced a modular attachment ecosystem for premium hand blenders, enabling user customization.

Global Hand Blender Market Report Scope

A hand blender, also called an immersion blender, is an electrically powered handheld kitchen tool. They have a reasonably large and usually thicker handle with buttons to operate the blender, a long, skinnier tube in the middle, and a wider dome-shaped opening with the blades at the bottom. They're long in design, which means they can get to the bottom of a tall container without much trouble.

The hand blender market is segmented by product type, distribution channel, application, and geography. By product type, the market is sub-segmented into corded and cordless. Distribution channel The market is sub-segmented into multi-brand stores, exclusive stores, online, and other distribution channels. By application, the market is sub-segmented into residential and commercial. By geography, the market is sub-segmented into North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. The report offers market sizes and forecasts in value (USD) for all the above segments.

| Corded |

| Cordless |

| Residential |

| Commercial |

| Offline Retail |

| Online Retail |

| Economy (Greater than USD 40) |

| Mid-range (USD 40 - 100) |

| Premium (Less than USD 100) |

| Soups and Sauces |

| Smoothies and Beverages |

| Baby Food and Purees |

| Bakery and Dessert Prep |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab of Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East And Africa |

| By Product Type | Corded | |

| Cordless | ||

| By End User | Residential | |

| Commercial | ||

| By Distribution Channel | Offline Retail | |

| Online Retail | ||

| By Price Tier | Economy (Greater than USD 40) | |

| Mid-range (USD 40 - 100) | ||

| Premium (Less than USD 100) | ||

| By Application | Soups and Sauces | |

| Smoothies and Beverages | ||

| Baby Food and Purees | ||

| Bakery and Dessert Prep | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab of Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East And Africa | ||

Key Questions Answered in the Report

What is the expected value of the hand blender market by 2031?

The market is projected to reach USD 5.17 billion by 2031 at a 4.84% CAGR.

Which region is growing fastest for hand blenders?

Asia-Pacific leads with a forecast 7.60% CAGR thanks to urbanization and income growth.

Are cordless hand blenders gaining traction?

Yes, cordless models show the highest 7.55% CAGR due to lithium-ion improvements and greater kitchen mobility.

What price tier is expanding most quickly?

Premium units priced above USD 100 grow at a 8.95% CAGR as consumers invest in advanced features.

How concentrated is competition in the sector?

The top five brands command roughly three-quarters of global revenue, reflecting moderate concentration.

Which application category drives the greatest growth?

Smoothies and beverages segment expands at 7.18% CAGR, propelled by health-focused consumer habits.

Page last updated on: