Compact Dishwasher Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

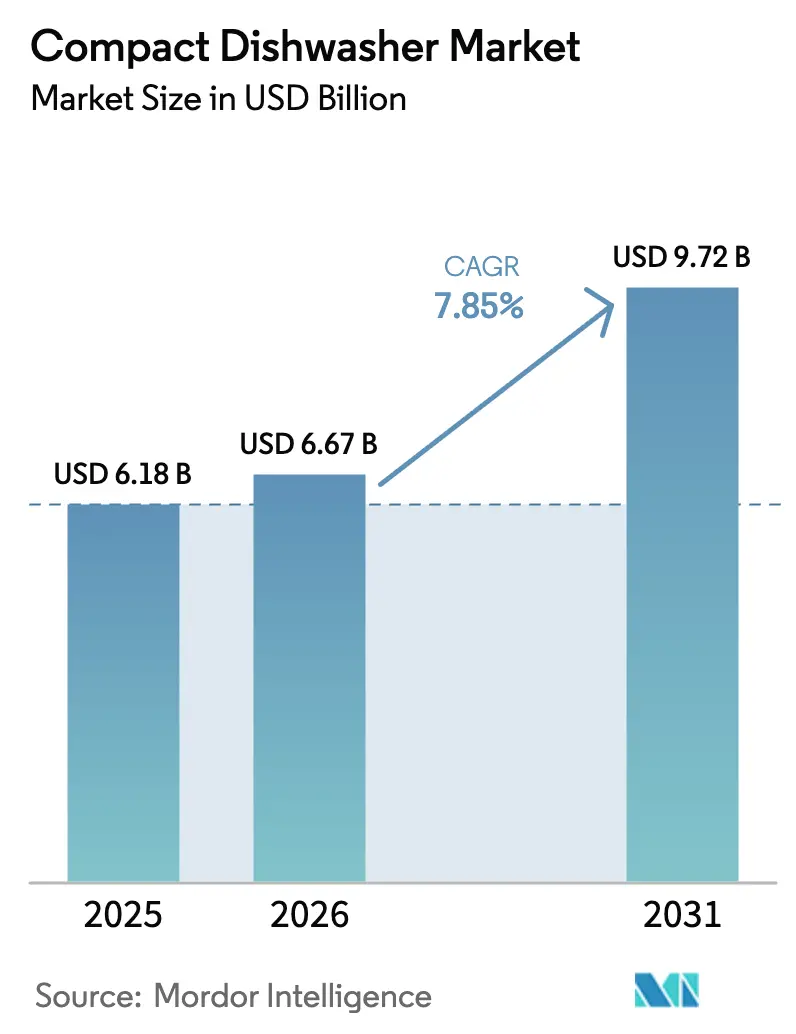

| Market Size (2026) | USD 6.67 Billion |

| Market Size (2031) | USD 9.72 Billion |

| Growth Rate (2026 - 2031) | 7.85% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Compact Dishwasher Market Analysis by Mordor Intelligence

Compact dishwasher market size in 2026 is estimated at USD 6.67 billion, growing from 2025 value of USD 6.18 billion with 2031 projections showing USD 9.72 billion, growing at 7.85% CAGR over 2026-2031. Urban infill projects, condominium construction, and micro-apartment conversions are compressing kitchen footprints in most major cities, pushing consumers toward appliances that reclaim countertop and cabinet real estate without sacrificing cleaning performance. Energy-efficiency regulations in the United States and the European Union reinforce this preference by rewarding smaller‐capacity machines with friendlier energy labels and lower utility bills, thereby accelerating replacement cycles in favor of compact formats[1]U.S. Department of Energy, “Energy Conservation Standards for Dishwashers,” energy.gov. Technology keeps pace; six-place-setting models now rely on brushless motors, precision soil sensors, and variable-pressure spray arms to deliver NSF-level sanitisation while consuming only 2 gallons of water per cycle, strengthening their value proposition in drought-prone regions[2]GE Appliances, “Smart Compact Dishwasher Product Sheet,” geappliances.com.

Key Report Takeaways

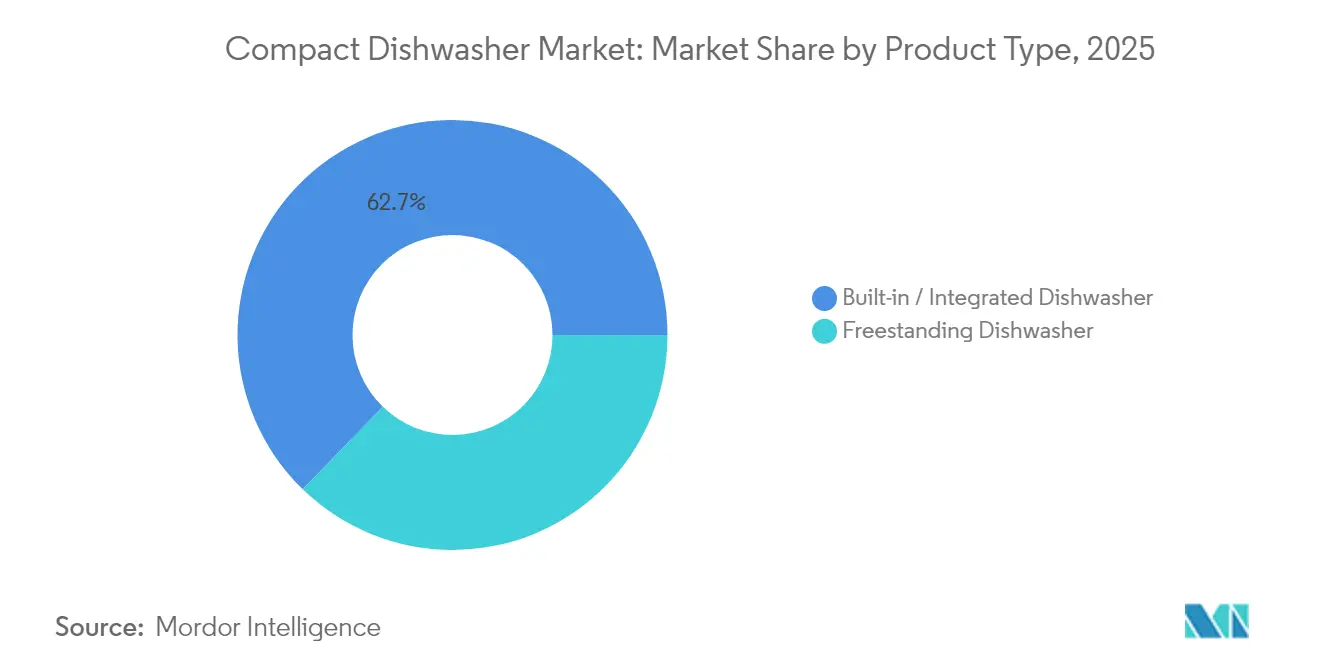

- By product type, built-in and integrated models led with 62.74% of the compact dishwasher market share in 2025, while freestanding formats are projected to expand at a 12.12% CAGR to 2031.

- By application, the residential segment held 51.76% of the compact dishwasher market share in 2025; commercial installations are forecast to grow at a 12.94% CAGR through 2031.

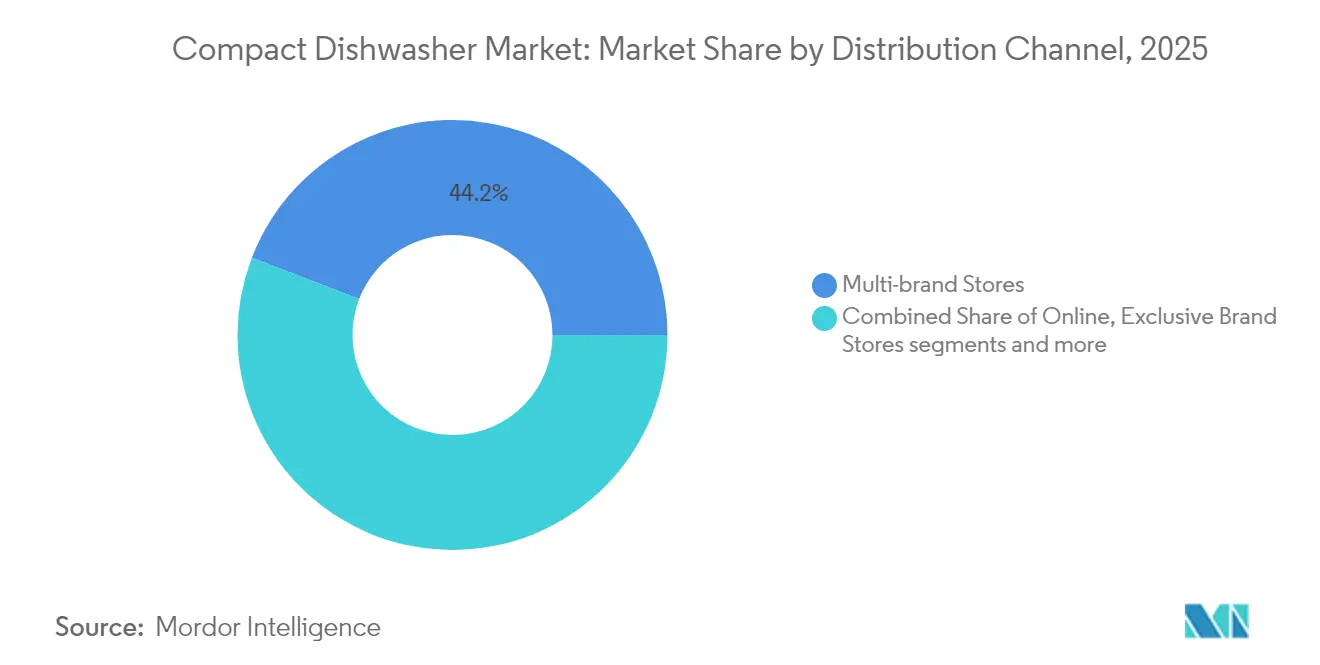

- By distribution channel, multi-brand stores captured 44.15% share in 2025; online platforms record the highest projected CAGR at 12.43% through 2031 of the compact dishwasher market.

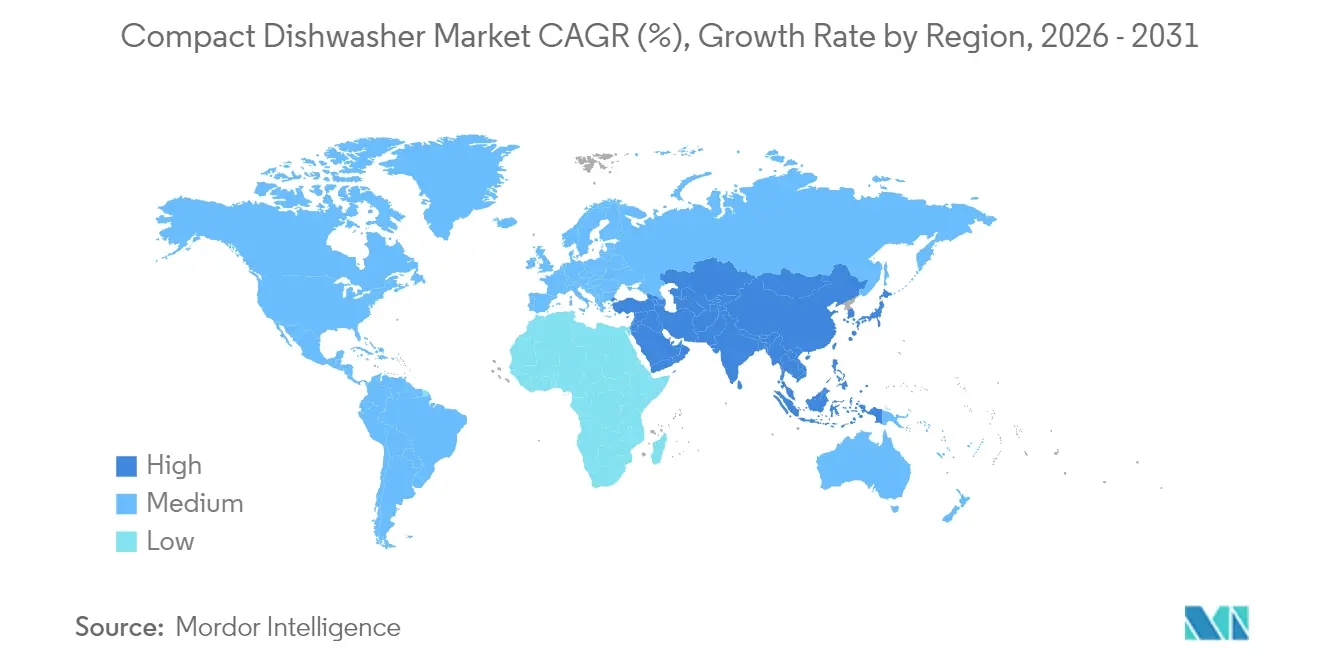

- Geographically, North America held 38.74% revenue share in 2025; Asia-Pacific is poised for the fastest CAGR at 12.68% to 2031 of the compact dishwasher market.

- Robert Bosch, Electrolux, Whirlpool, Haier, and LG collectively holds major market share in 2025, indicating a moderately concentrated seller landscape.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Compact Dishwasher Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Urbanisation & shrinking kitchens | 2.3% | Global, with concentration in APAC megacities and North American urban centers | Medium term (2-4 years) |

| Rising disposable income & dual-income households | 1.9% | North America & EU, expanding to APAC urban centers | Long term (≥ 4 years) |

| Energy- & water-efficiency regulations accelerate replacements | 1.6% | North America & EU regulatory zones | Short term (≤ 2 years) |

| Growth of short-term rental installations (Airbnb, co-living) | 1.1% | Urban centers globally, particularly North America & EU | Medium term (2-4 years) |

| E-commerce-only appliance brands disrupt pricing | 0.8% | Global, led by North America & EU | Short term (≤ 2 years) |

| Emergence of sink-dishwasher hybrids in Asia | 0.4% | APAC core, spill-over to MEA | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Urbanisation & Shrinking Kitchens

Rapid densification is pushing average new-build kitchen sizes below 100 ft² in Beijing, Los Angeles, and Paris, setting a clear design brief for six-place-setting or smaller machines that tuck under a 24-inch counter or sit atop a cart. GE Profile’s Smart Compact Dishwasher, launched in 2025, fits six place settings, uses 2 gallons per cycle, and connects via Wi-Fi to push filter-clean reminders, features aimed squarely at renters. Ultra-slim units like the LISSOME R1, only 11 inches wide, further illustrate the micro-living trajectory while introducing quick-wash cycles under 15 minutes to match fast-paced urban lifestyles.

Rising Disposable Income & Dual-Income Households

Nordic countries, long a bellwether for premium white goods, have 70–80% dishwasher penetration; their compact segment is outgrowing full-size replacements as downsizing retirees move to city apartments. Millennials and Gen Z buyers demonstrate an even steeper willingness-to-pay curve: the HAVA R09, a three-place-setting countertop unit priced at USD 329.99, sold out its first production run in under two months via direct-to-consumer preorders. Higher earnings in Tier-1 Chinese cities are unlocking purchases once considered discretionary, a pattern mirrored in Mumbai where dual-income households now top 45%. Premium connectivity features such as smartphone cycle selection add USD 40–60 to bill-of-materials yet deliver margin uplift of up to 7 percentage points, reinforcing innovation budgets across the compact dishwasher market.

Energy- & Water-Efficiency Regulations Accelerate Replacements

The U.S. Department of Energy capped compact dishwasher energy use at 174 kWh per year effective 2027, compared with 223 kWh for standard machines, tilting the playing field toward smaller cavities. The European Union’s simplified A-to-G energy label similarly favors compact designs because resource usage is tested on a per-cycle basis. California’s drought-driven plumbing codes now mandate maximum 3.1 gallons per dishwasher cycle in new multifamily construction, a benchmark easily met by leading six-place units such as Bob’s eco-compact dishwasher, which relies on a low-pressure recirculation pump to distribute 150 PSI spray within a 15-liter reservoir.

Growth of Short-Term Rental Installations (Airbnb, Co-living)

Hosts on Airbnb, Vrbo, and co-living platforms now list “dishwasher” among top five search filters, pushing property managers to retrofit kitchens quickly. Countertop machines that fill from a pitcher circumvent plumbing modifications, a critical factor in historic European buildings where drilling through tile backsplashes violates heritage codes. The LISSOME R1’s 15-minute express cycle enables same-day turnover for short-stay guests, allowing cleaners to start and unload during standard service windows.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront product & installation cost | -1.4% | Global, particularly emerging markets and price-sensitive segments | Medium term (2-4 years) |

| Legacy cabinetry / plumbing incompatibility | -0.9% | North America & EU retrofit markets, older housing stock | Long term (≥ 4 years) |

| Slow-down in new urban housing starts | -0.7% | North America & EU urban centers, with spillover to APAC | Short term (≤ 2 years) |

| Stricter regional water-use caps driving R&D cost | -0.5% | Water-stressed regions: California, Australia, parts of EU and MEA | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Product & Installation Cost

Professional installation can cost another USD 150–400 depending on cabinetry modification needs and local labor rates, extending payback periods beyond five years for water-and-energy savings alone. Manufacturers are responding through value-engineering, switching stainless interiors to hybrid ABS/stainless tubs and outsourcing control boards to contract electronics suppliers, trimming material costs by 8–12% without compromising warranty terms. Entry-level countertop SKUs such as the HAVA R01 at USD 279.99 demonstrate that sub-USD 300 price points stimulate incremental demand in India, Brazil, and Southeast Asia.

Legacy Cabinetry / Plumbing Incompatibility

European condominiums compound complexity with varying plumbing codes and centralized hot-water systems that fluctuate below the 120 °F minimum many dishwashers expect, triggering longer heat-up times and higher energy draw. Countertop designs address these hurdles but trade load capacity for portability, limiting appeal to families larger than three. Brands therefore introduce hybrid models equipped with both permanent-plumb and pitcher-fill options to widen the addressable base.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Flexibility Propels Freestanding Growth

Built-in variants generated USD 3.88 billion in 2025 and held 62.74% of compact dishwasher market share by excelling in seamless, high-end kitchen aesthetics. This dominance continues, yet freestanding and countertop designs are projected to record a 12.12% CAGR through 2031 as renters and urban nomads prize installation freedom. HAVA’s R01 plug-and-play countertop system has become emblematic of this surge, shipping with a collapsible 5-liter water tank and quick-connect drain hose that sidesteps permanent plumbing.

Manufacturers are blurring categories with convertible chassis that slot under the counter using an optional trim kit yet detach into countertop mode for relocations, tapping dual revenue streams. Premium built-ins continue to command price premiums of 18–25%, buoyed by demand for panel-ready fronts that disappear behind cabinetry. Nevertheless, shipment volume growth skews toward freestanding units because emerging-market consumers favor purchase immediacy over remodel complexity.

By Application: Commercial Uptake Accelerates

Residential buyers remained the spine of revenue, accounting for 51.76% of 2025 demand, yet commercial interest outpaced household orders with a 12.94% CAGR outlook. Owners of small cafés, shared office kitchens, and food trucks discover that a compact NSF-certified under-counter washer frees floor space while slashing labor devoted to manual cleaning. The Auto-Chlor AC TALL Space Maker, which carves out a mere 22 × 24-inch footprint, embodies this commercial shift by delivering 75% space savings relative to traditional rack machines.

Commercial adoption also pushes feature sets, high-temperature sanitization, 90-second express cycles, and digital usage logs that subsequently diffuse into premium household SKUs. Conversely, residential demand shapes noise-reduction and smart-home integration advances that benefit office break rooms aiming for open-plan serenity.

By Distribution Channel: Digital Commerce Scales

Multi-brand big-box and specialist stores commanded 44.15% share in 2025 because shoppers still value live-fire demonstrations and bundled installation services. Nevertheless, online revenue is slated for a 12.43% CAGR, reflecting shoppers' research on water consumption, dBA ratings, and interior rack photos among dozens of SKUs that a physical aisle cannot accommodate. The compact dishwasher market enjoys online advantages: lighter weight versus full-size washers reduces freight surcharges, and countertop units are classified as large parcels rather than freight, cutting delivery times by two days on average. E-tail algorithms also surface “apartment-sized dishwasher” searches, funneling high-intent buyers directly to SKU pages.

Brands such as LISSOME routinely launch first on their own sites, gather user feedback, then syndicate to marketplaces once firmware bugs are patched. Conversely, brick-and-mortar chains counter with same-day pick-up and white-glove install packages is a sticking point for built-in adapters. Going forward, omnichannel models will dominate: a customer might watch a YouTube review, size the cabinet via augmented-reality app, purchase online, and schedule installation through a local store’s service desk, fusing the best of both worlds.

Geography Analysis

North America led revenue with a 38.74% share in 2025 as urban dwellers in New York, Toronto, and Los Angeles embraced apartment-sized dishwashers to offset rising square-foot costs. The region’s average selling price topped USD 480 because buyers gravitate toward stainless tubs, Wi-Fi diagnostics, and voice-assistant commands. Domestic manufacturing capacity is strengthening: GE Appliances is investing USD 490 million in its Louisville plant to expand compact dishwasher lines, creating 800 jobs and shortening delivery lead times. Importers still play a role, yet reshoring initiatives reduce port congestion risks that bruised the supply chain in 2022.

Asia-Pacific delivers the highest growth slope at 12.68% CAGR, fueled by China’s 1.94 million compact units sold in 2023 and India’s apartment boom. Urban households in Shanghai and Shenzhen often allocate under 5 m² to combined kitchen–dining areas, leaving scant room for full-size appliances. Domestic Chinese manufacturers iterate quickly with software upgrades pushing over the air, while Japanese innovators like Panasonic refine sink-integrated dishwashers that double as drying racks, a format resonating with elderly homeowners seeking ergonomic accessibility. Penetration remains below 30% in Japan, signaling significant runway; government subsidies for water-saving devices could accelerate uptake. In India, players bundle EMI financing and installation kits compatible with low-pressure municipal water to overcome infrastructure gaps.

Europe shows mature unit volumes but a bifurcated profile. Nordic countries exceed 70% penetration thanks to decades of progressive gender-equity policies that normalized appliance adoption, yet Eastern European markets such as Poland (25%) and Romania (15–20%) trail, presenting white-space for compact entries that fit post-Soviet panel-block kitchens. EU eco-design legislation, tightened in 2024, obliges spare-parts availability for 10 years, lifting total cost-of-ownership appeal and nudging consumers to premium brands promising repairability.

Mordor Intelligence provides coverage of the compact dishwasher market across other key regional markets, including North America and Asia, each with their regulatory frameworks and demand patterns. Detailed country-level analysis extends to United Kingdom and Germany incorporating local coverage and market participation, as required.

Competitive Landscape

Incumbents Robert Bosch, Electrolux, Whirlpool, Haier, and LG collectively shipped 8.2 million compact units in 2024, representing just above 50-55% of global volume. Bosch leverages its CrystalDry zeolite system to achieve 89% moisture removal without a heating element, a differentiator in power-price-sensitive EU markets. Electrolux targets commercial niches through its Professional line, offering 70-second cycle times for bakeries craving rapid rack turnover. Whirlpool leans on its U.S. manufacturing base to deliver the Built-In Slim series with heated-dry options tailored to American preferences, while Haier and LG exploit Asian distribution muscle to push Wi-Fi-enabled models bundled with smart refrigerators for cross-selling gains.

BSH Home Appliances (Bosch, Siemens, Neff) reported 3.2% dish-care category growth in 2024, crediting its compact lineup for outpacing full-size sales in megacities such as São Paulo and Istanbul[3]BSH Home Appliances Group, “Annual Report 2024,” bsh-group.com. Miele’s decision to erect a 150-employee Alabama plant by late 2025 underscores the strategic importance of regional production to sidestep tariffs and cut logistics costs. Meanwhile, challengers HAVA and LISSOME apply direct-to-consumer playbooks: crowdfunding launches, influencer-led tutorials, and subscription-detergent bundles. Their countertop units now rank in Amazon’s top five dishwashers by monthly unit sales in the United States, validating niche segmentation via social channels.

Patent filings surged 18% year on year, focusing on fold-flat spray arms, AI-driven soil detection, and self-descaling rinse modules that extend pump life. Partnerships are forming between detergent makers and dishwasher OEMs to fine-tune low-suds formulations optimized for compact wash cavities. Competitive intensity remains moderate; barriers include stainless-steel tooling costs and regulatory compliance testing across 40+ markets. Still, margin pressure is rising as online players strip overhead and sell at 12–15% lower ASPs. Incumbents counter by bundling 10-year motor warranties and launching refurbishment programs that align with Europe’s Right-to-Repair ethos, aiming to lock customers into brand ecosystems for parts and service revenue.

Compact Dishwasher Industry Leaders

Electrolux AB

Haier Group Corporation

LG Electronics Inc.

Robert BOSCH

Whirlpool Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: GE Profile launched a Wi-Fi-enabled Smart Compact Dishwasher priced at USD 499, featuring six place settings and 2-gallon cycles.

- June 2025: GE Appliances announced USD 490 million investment to expand compact dishwasher production in Kentucky, creating 800 new jobs.

- February 2025: Auto-Chlor launched the AC TALL Space Maker, shrinking commercial footprints by 75%.

Global Compact Dishwasher Market Report Scope

Compact dishwashers are small-sized machines that are designed for limited spaces. It is used in residential and commercial places in particular industries, such as restaurants, hotels, and hospitals, where it has a huge demand. The compact dishwasher market is segmented by product type, application, distribution channel, and geography. By product type, the market is segmented into freestanding dishwashers and built-in dishwashers. By application, the market is segmented into commercial and residential. By distribution channel, the market is segmented into multi-branded stores, exclusive stores, online, and other distribution channels. And by geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and Middle East & Africa. The report offers market size and forecasts for the compact dishwasher market in Value (USD) for all the above segments.

| Freestanding Dishwasher |

| Built-in / Integrated Dishwasher |

| Residential |

| Commercial (HoReCa, offices, institutional) |

| Multi-brand Stores (Large & Specialty Retail) |

| Exclusive Brand Stores |

| Online (E-commerce & DTC) |

| Others (Builders, Catalog, etc.) |

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines) | |

| Rest of Asia Pacific | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | |

| Rest of Europe | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Product Type | Freestanding Dishwasher | |

| Built-in / Integrated Dishwasher | ||

| By Application | Residential | |

| Commercial (HoReCa, offices, institutional) | ||

| By Distribution Channel | Multi-brand Stores (Large & Specialty Retail) | |

| Exclusive Brand Stores | ||

| Online (E-commerce & DTC) | ||

| Others (Builders, Catalog, etc.) | ||

| Geography | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines) | ||

| Rest of Asia Pacific | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | ||

| Rest of Europe | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the compact dishwasher market?

The Compact Dishwasher Market is valued at USD 6.67 billion in 2026 and is projected to climb to USD 9.72 billion by 2031.

What is the current Compact Dishwasher Market size?

In 2026, the Compact Dishwasher Market size is expected to reach USD 6.67 billion.

Which region shows the fastest growth?

Asia-Pacific posts the steepest trajectory with a 12.68% CAGR through 2031, driven by rapid urbanization in China and India.

How are energy regulations shaping product design?

U.S. and EU standards cap annual energy consumption at 174 kWh for compact units, prompting brands to adopt brushless motors, soil sensors, and low-pressure recirculation pumps to exceed efficiency benchmarks.

Why are freestanding compact dishwashers gaining traction?

Installation flexibility appeals to renters and short-term rental hosts, helping freestanding formats log a 12.12% CAGR versus 7.85% overall.

Which companies lead the market?

Robert Bosch, Electrolux, Whirlpool, Haier, and LG together hold just over 55% of global shipments, supported by broad distribution and ongoing R&D in space-saving technologies.

Page last updated on: