Glufosinate Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 2.30 Billion |

| Market Size (2031) | USD 3.40 Billion |

| Growth Rate (2026 - 2031) | 7.20% CAGR |

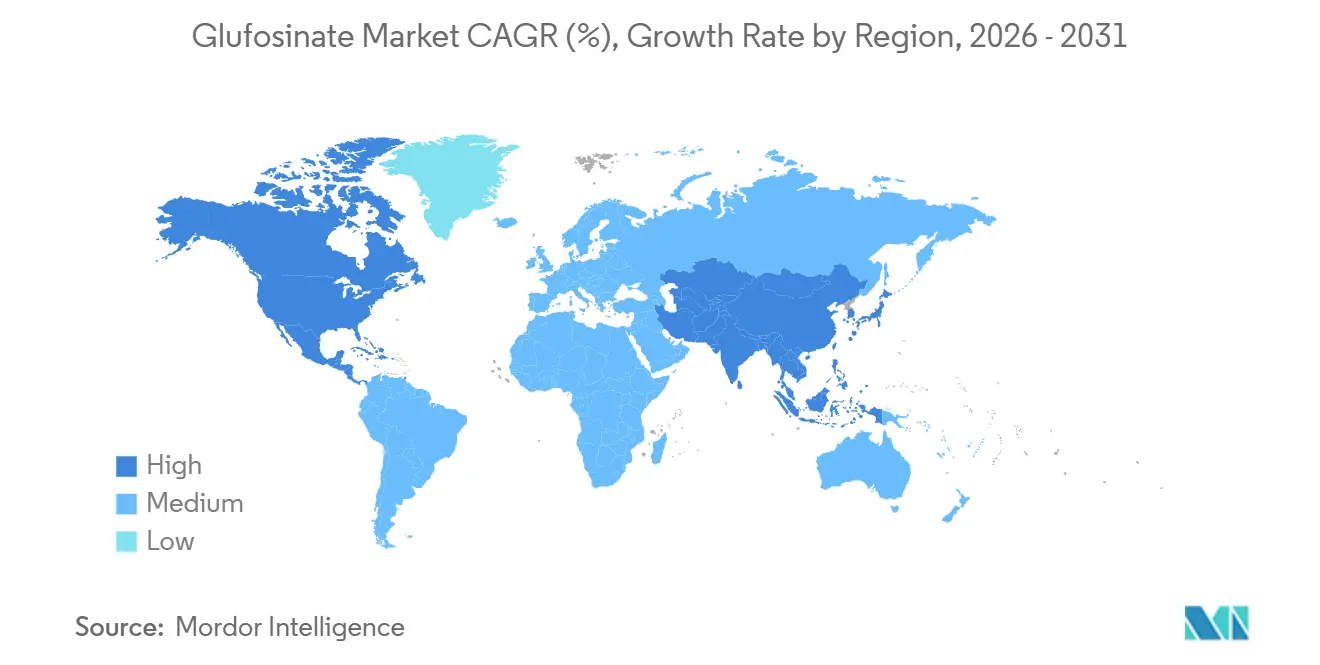

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Glufosinate Market Analysis by Mordor Intelligence

The glufosinate market size is projected to increase from USD 2.1 billion in 2025 to USD 2.3 billion in 2026 and reach USD 3.4 billion by 2031, growing at a CAGR of 7.2% over 2026-2031. Glyphosate-resistant weeds now infest more than 35 million hectares worldwide, forcing growers to pivot toward contact herbicides with alternative modes of action such as glufosinate. Trait-stack adoption under Bayer’s LibertyLink and XtendFlex platforms embeds glufosinate into seed decisions and locks in multi-year herbicide programs. Chinese capacity expansions add price volatility but also open access for cost-sensitive growers, reshaping regional dynamics and intensifying competition. Increased regulatory scrutiny on glyphosate usage in major agricultural markets, particularly in Europe, is driving a shift toward alternative herbicides, thereby boosting glufosinate demand. Advancements in formulation technologies, such as improved surfactant systems and tank-mix compatibility, are enhancing glufosinate's field performance and expanding its application across crops like soybean, corn, and cotton. The growing adoption of herbicide-tolerant genetically modified seeds and the expansion of crop acreage are further supporting steady demand.

Key Report Takeaways

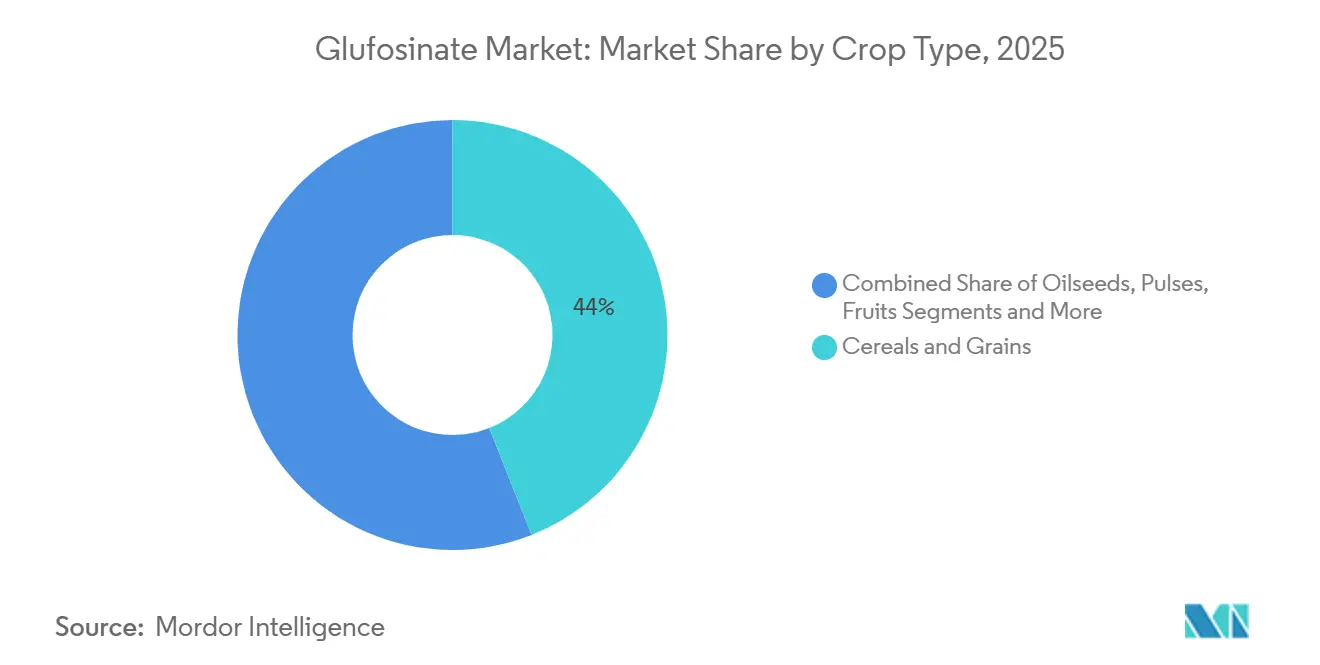

- By crop type, cereals and grains accounted for the largest segment, with 44% of the glufosinate market share in 2025, while oilseeds and pulses are the fastest-growing, advancing at a 9.8% CAGR through 2026-2031.

- By formulation, aqueous suspension concentrate led the largest segment, with 52% of glufosinate market share in 2025, while dry formulation (water-dispersible granules) is the fastest-growing, projected to grow at an 11.2% CAGR to 2026-2031.

- By treatment stage, post-emergence applications accounted for the largest segment, 62% of the glufosinate market share in 2025. In contrast, pre-emergence is the fastest-growing, forecast to rise at an 8.6% CAGR over 2026-2031.

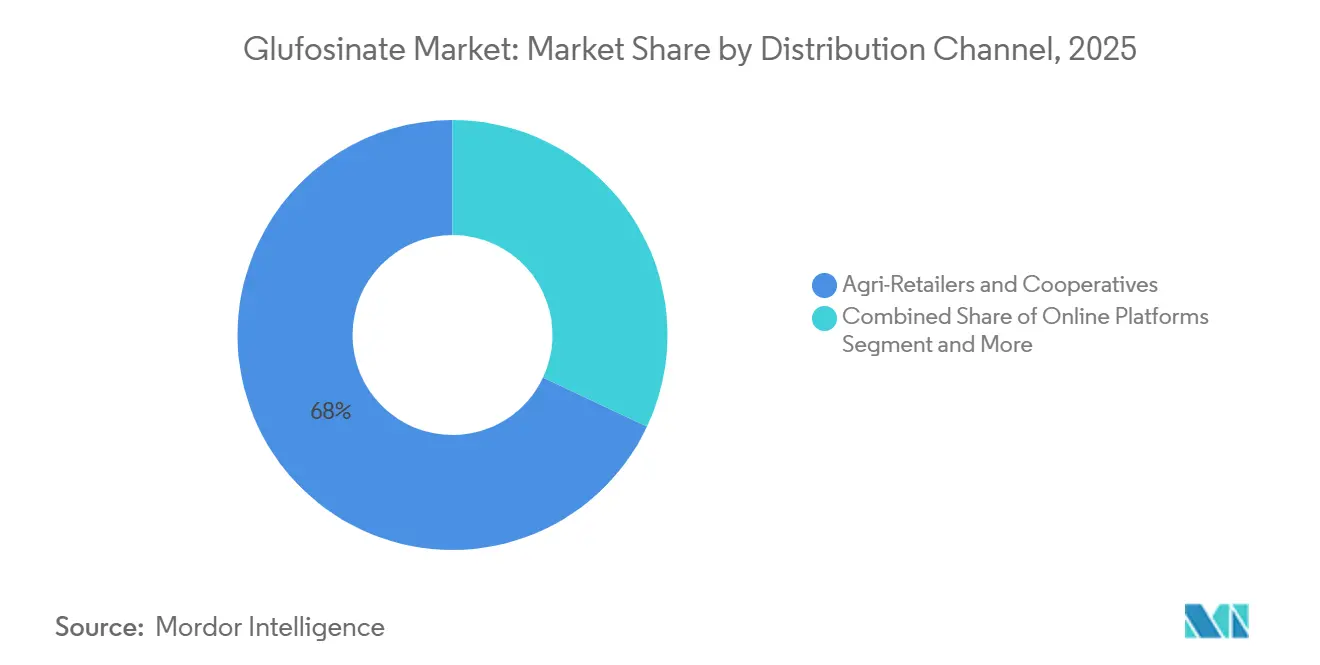

- By distribution channel, agri-retailers and cooperatives hold the largest position, accounting for 68% of the glufosinate market size in 2025, yet online platforms exhibit the fastest-growing trajectory at 14.5% CAGR through 2026-2031.

- By geography, North America remains the largest regional contributor in 2025 with a market share of 32.5% in the global glufosinate market, and Asia-Pacific is the fastest growing with a CAGR of 11.2% through 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Glufosinate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Impact of glyphosate-resistant weed proliferation on the market | +1.8% | North America, South America, and Asia-Pacific | Medium term (2-4 years) |

| Expansion of glufosinate-tolerant biotech crops | +2.1% | Global, peaks in Americas and Asia-Pacific | Long term (≥4 years) |

| Impact of paraquat and dicamba regulatory exit on the market | +1.3% | Global, strongest in Europe and South America | Short term (≤2 years) |

| Precision-spraying adoption boosting post-emergence demand | +0.9% | North America, Europe, China, and Australia | Medium term (2-4 years) |

| Rapid uptake of nano-microencapsulated glufosinate formulations | +0.6% | Asia-Pacific, Europe, and North America | Long term (≥4 years) |

| Stacked-trait seed mixes enabling dual-mode herbicide programs | +1.1% | Americas and Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Impact of Glyphosate-Resistant Weed Proliferation on the Market

Palmer amaranth nowadays infests 31 United States states and waterhemp 25 states, both showing confirmed glyphosate resistance that slashes soybean yields by up to 90% when unmanaged[1]Source: Weed Science Society of America, “Herbicide Resistance Database,” weedscience.org. The increasing prevalence of glyphosate-resistant weeds is a significant driver for the glufosinate market. Farmers dealing with resistant weed populations are turning to glufosinate as an effective alternative herbicide. It offers control over a broad spectrum of weeds that no longer respond to glyphosate. This trend is particularly prominent in regions with high glyphosate usage, where resistance management strategies are essential to maintaining crop yield and quality.

Expansion of Glufosinate-Tolerant Biotech Crops

The growth of glufosinate-tolerant genetically modified crops is driving market demand. These biotech crops, such as soybeans, maize, and cotton, enable farmers to apply glufosinate without harming the crop. The adoption of these tolerant varieties is expanding globally, particularly in North and South America, as they facilitate effective weed control while supporting higher productivity and flexibility in crop management practices. Furthermore, the increasing investments in biotechnology research and development are leading to the introduction of new glufosinate-tolerant crop varieties, which is projected to further boost market growth. The compatibility of glufosinate with sustainable farming practices also makes it a preferred choice for farmers aiming to balance productivity with environmental stewardship.

Impact of Paraquat and Dicamba Regulatory Exit on the Market

The regulatory phase-out of older herbicides like paraquat and dicamba has created a significant opportunity for glufosinate. Stricter regulations and bans on these chemicals, driven by environmental and health concerns, are prompting farmers to adopt glufosinate as a safer and compliant alternative. This shift is especially evident in Europe, North America, and parts of Asia, where regulatory compliance heavily influences herbicide selection. The growing emphasis on sustainable agriculture and the need to reduce the environmental impact of farming practices are further contributing to the increased adoption of glufosinate. As governments and regulatory bodies continue to tighten restrictions on harmful chemicals, the demand for safer alternatives like glufosinate is projected to rise steadily.

Precision-Spraying Adoption Boosting Post-Emergence Demand

The adoption of precision-spraying technologies is bolstering glufosinate usage by enabling more accurate and efficient herbicide application. Precision spraying minimizes chemical waste, reduces crop exposure to non-target areas, and enhances overall weed control efficacy. As farmers increasingly invest in smart spraying equipment and digital agriculture tools, glufosinate benefits from higher adoption in both conventional and biotech crop systems, making it a preferred choice in modern, technology-driven farming operations. Moreover, the integration of artificial intelligence and machine learning in precision agriculture is further enhancing the effectiveness of glufosinate application. These advancements are helping farmers optimize resource utilization, reduce costs, and achieve better crop protection outcomes, thereby driving the market growth for glufosinate.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price volatility driven by Chinese oversupply affects the market | -1.2% | Global, severe in Asia-Pacific and South America | Short term (≤2 years) |

| Stringent toxicology reviews in the European Union | -0.8% | Europe, spillover to Middle East and Africa | Medium term (2-4 years) |

| Emergence of next-gen Hydroxyphenylpyruvate Dioxygenase (HPPD) and bio-herbicides | -0.7% | North America, Europe, and Asia-Pacific | Long term (≥4 years) |

| Rainfastness concerns under increasingly erratic rainfall patterns | -0.5% | Monsoon regions of Asia and South America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Emergence of Next-gen Hydroxyphenylpyruvate Dioxygenase (HPPD) and Bio-Herbicides

The introduction of next-generation Hydroxyphenylpyruvate Dioxygenase (HPPD) inhibitors and bio-herbicides is intensifying competition in the glufosinate market. Hydroxyphenylpyruvate Dioxygenase (HPPD) inhibitors are effective at controlling broadleaf weeds, while bioherbicides derived from natural sources, such as microbes or plant extracts, appeal to farmers prioritizing environmentally sustainable weed control methods. As these advanced alternatives gain popularity, particularly in organic, precision, or sustainable agricultural practices, they may partially replace glufosinate in certain crop applications. In response, manufacturers are focusing on improving formulations, enhancing tank-mix compatibility, and implementing targeted marketing strategies to retain market share.

Rainfastness Concerns Under Increasingly Erratic Rainfall Patterns

Climate variability increases the probability of rainfall within the critical 30-minute window after application. The University of Delaware's analysis shows that control effectiveness drops significantly during rainfall events[2]Source: European Food Safety Authority, “Glufosinate Re-approval Assessment,” efsa.europa.eu. Growers in monsoon-prone markets are wary, dampening adoption unless adjuvants or encapsulated formulations guarantee performance. Heavy or unpredictable rain may wash away the herbicide before it is adequately absorbed by weeds, reducing its effectiveness. This issue, known as rainfastness, presents challenges for achieving consistent weed control, especially in regions with unpredictable weather patterns or high rainfall variability. Consequently, farmers may need to adjust application timing or incorporate additional herbicides, which can influence adoption rates and affect glufosinate demand in areas prone to erratic rainfall.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Crop Type: Oilseeds Gain Momentum Against Cereal Dominance

Cereals and grains led the largest segment, with 44% of the glufosinate market share in 2025, this leadership is attributed to the extensive cultivation of staple crops such as wheat, rice, and maize, which require effective herbicidal solutions to manage weeds and enhance yield. Glufosinate’s broad-spectrum weed control and low residual activity make it particularly suitable for cereal and grain farming. Furthermore, the segment benefits from established application practices and widespread adoption among large-scale cereal producers, solidifying its position as the largest crop-type segment.

Oilseeds and pulses are the fastest growing, advancing at a 9.8% CAGR through 2026-2031. This growth is driven by increasing global demand for plant-based oils and protein-rich pulses, coupled with expanded cultivation in regions such as Asia-Pacific and South America. Farmers are increasingly adopting glufosinate to enhance weed management efficiency and minimize crop losses, particularly in rotation systems involving oilseeds and legumes. Additionally, the transition toward sustainable and no-till farming practices is boosting glufosinate usage in these crops, as it supports soil conservation while ensuring effective weed control.

By Formulation: Granules Disrupt Liquid Supremacy

Aqueous suspension concentrate led largest segment, with 52% of glufosinate market share in 2025, because they integrate smoothly into existing tank mixes and distribution infrastructure. This dominance is attributed to their ease of handling, uniform dispersion in water, and reliable weed control performance. Suspension concentrates are widely utilized by farmers for cereal, grain, and oilseed crops due to their consistent efficacy and compatibility with standard spraying equipment.

Dry formulation (water-dispersible granules) is fastest growing, projected to grow at an 11.2% CAGR to 2026-2031, aligning with e-commerce shipping models favored by large farms. This growth is driven by their extended shelf life, ease of transport, and compatibility with precision and mechanized spraying systems. WDGs are increasingly adopted in regions with high rainfall or irrigation variability, as they minimize runoff and enhance rainfastness compared to liquid formulations. Additionally, advancements in dry formulation technology are improving solubility and efficacy, making them a preferred choice for large-scale and resource-efficient farming practices.

By Treatment Stage: Pre-Emergence Slots into Layered Programs

Post-emergence applications led the largest segment, 62% of the glufosinate market size in 2025. Post-emergence use is preferred because it targets weeds after crop emergence, offering flexible, effective control of a wide range of grass and broadleaf weeds. This stage enables farmers to address actual weed pressure, making glufosinate particularly valuable for cereals, grains, and oilseed crops, where early-season weed control is essential for optimizing yield.

Pre-emergence is fastest growing, forecast to rise at an 8.6% CAGR over 2026-2031. This growth is driven by the increasing need for proactive weed management, where glufosinate suppresses weeds before they emerge, reducing competition and enhancing crop establishment. The adoption of pre-emergence applications is rising in high-value and precision farming systems, as it aligns with sustainable farming practices and minimizes reliance on multiple post-emergence treatments.

By Distribution Channel: Digital Commerce Reshapes Access

Agri-retailers and cooperatives holds largest position, 68% glufosinate market size in 2025 in 2025, due to embedded credit lines, localized advice, and in-season logistics support. These channels dominate due to their direct access to farmers, provision of technical guidance, and efficient supply of large volumes, particularly in both traditional and emerging agricultural regions. Their strong presence ensures the widespread availability of glufosinate formulations, including liquid and dry products, across various crop segments.

Online platforms exhibit the fastest-growing trajectory at a 14.5% CAGR through 2026-2031, as growers compare transparent prices and bulk-order bundled seed traits and herbicides.This growth is driven by the expansion of e-commerce, digital marketplaces, and precision agriculture platforms, which enhance the accessibility of glufosinate products for smallholders and tech-savvy farmers. Online channels also facilitate efficient delivery, provide detailed product information, and offer access to new formulation types, supporting increased adoption in regions with limited traditional retail penetration.

Geography Analysis

North America remains the largest regional contributor in 2025, with a 32.5% share of the glufosinate market. This dominance is attributed to the widespread adoption of herbicide-tolerant crops, advanced agricultural infrastructure, and a well-established agrochemical supply chain. Farmers in the United States and Canada utilize glufosinate for its broad-spectrum weed control, effectiveness against glyphosate-resistant weeds, and compatibility with biotech crop systems. Additionally, robust distribution networks and strong regulatory frameworks ensure the availability and consistent use of glufosinate products across the region.

Asia-Pacific is the fastest-growing region, with a 11.2% CAGR through 2026-2031. This growth is driven by the increasing cultivation of cereals, grains, oilseeds, and pulses, alongside the adoption of glufosinate-tolerant crop varieties and the rapid implementation of modern farming techniques in countries such as China, India, and Southeast Asia. The expansion of agri-retail infrastructure, adoption of digital farming solutions, and advancements in precision spraying technologies further support the uptake of glufosinate.

South America glufosinate market growing propelled by Brazilian sugarcane, coffee and soybean segments that filled the paraquat void and by Argentine double-hit programs for multi-resistant weeds[3]Source: Ministry of Agriculture, Brazil, “Glufosinate Registrations,” gov.br/agricultura. Currency swings and Chinese oversupply create input-cost rollercoasters, but trait adoption and stacked programs counterbalance price-induced hesitancy. Europe countries like Germany and France remain core users in corn and cereals, yet high-value fruit growers may pivot if endocrine-disruptor rules tighten.

Competitive Landscape

The glufosinate market is moderately concentrated, with BASF SE, Bayer AG, Syngenta AG, UPL Limited, and Corteva, Inc. collectively holding a significant share in 2025. BASF SE leads the market with products such as Liberty and Liberty ULTRA, supported by in-house manufacturing to reduce fixed costs. Bayer AG maintains a substantial market presence through products like Finale and Basta, leveraging its seed franchise to offer bundled herbicide and trait solutions. Syngenta AG utilizes branded formulations to replace paraquat in burndown programs, contributing to its notable market share. UPL and Nufarm focus on strong distribution networks, particularly in emerging markets.

Competition in the market is further fragmented by factors such as patent expirations, data-protection expiry, and varying global regulatory standards. In Europe, re-approval risks have driven the adoption of multi-active premixes, which reduce reliance on single-ingredient sales while maintaining market presence. Additionally, niche players like Indorama are targeting specialty crops with nano-microencapsulated formulations, where attributes such as residue control and rainfastness are key value drivers.

Seed companies, including Corteva Agriscience, are co-developing traits that ensure in-crop use rights for glufosinate, stabilizing demand despite fluctuations in raw-active pricing. These developments indicate a shift in competition, moving from a focus on product tonnage to system integration and service packages within the glufosinate market.

Glufosinate Industry Leaders

BASF SE

Bayer AG

Syngenta AG

UPL Limited

Corteva, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Shandong Lubachem launched Jinxunchu (glufosinate‑P K⁺ 194 g/L SL), its second-generation herbicide. The product demonstrates higher absorption rates than conventional glufosinate-P salts, resulting in faster and more effective weed control. Field trials confirm its efficacy across wastelands, crop rotations, vegetable rows, and orchards, successfully controlling resistant weeds including green foxtail, crab grass, goose grass, beggarticks, and sedge.

- October 2024: BASF's Liberty ULTRA herbicide received EPA registration and is now approved for use, pending state approvals. The herbicide, which uses patented Glu-L Technology and refined L-glufosinate ammonium, provides up to 20% improved control of broadleaf and grass weeds compared to generic alternatives.

- May 2024: UPL Limited obtained United States regulatory approval for a supplemental label amendment for its glufosinate-based herbicide Interline. The amendment allows over-the-top application on glufosinate-tolerant camelina varieties developed by Yield10 Bioscience, providing broadleaf weed control in camelina oilseed crops. The approval expands UPL's herbicide portfolio in the United States market for traited crops.

Global Glufosinate Market Report Scope

Glufosinate is a broad-spectrum, non-selective herbicide commonly used in agriculture to manage weeds and unwanted vegetation across various crops. The glufosinate market report is segmented by crop type (cereals and grains, oilseeds and pulses, fruits and vegetables, and other crop types), by formulation (aqueous suspension concentrate, liquid (soluble) concentrate, dry formulation (water-dispersible granules)), by treatment stage (pre-emergence, and post-emergence), by distribution channel (online platforms, agri-retailers and cooperatives, and other distribution channels), and by geography (North America, Europe, Asia-Pacific, South America, Africa, and the Middle East). The market forecasts are provided in terms of value (USD).

| Cereals and Grains |

| Oilseeds and Pulses |

| Fruits and Vegetables |

| Other Crop Types |

| Aqueous Suspension Concentrate |

| Liquid (Soluble) Concentrate |

| Dry Formulation (Water-Dispersible Granules) |

| Pre-Emergence |

| Post-Emergence |

| Agri-Retailers and Cooperatives |

| Online Platforms |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Russia | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Australia | |

| Japan | |

| Thailand | |

| Vietnam | |

| Philippines | |

| Rest of Asia-Pacific | |

| Middle East | Turkey |

| Saudi Arabia | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Crop Type | Cereals and Grains | |

| Oilseeds and Pulses | ||

| Fruits and Vegetables | ||

| Other Crop Types | ||

| By Formulation | Aqueous Suspension Concentrate | |

| Liquid (Soluble) Concentrate | ||

| Dry Formulation (Water-Dispersible Granules) | ||

| By Treatment Stage | Pre-Emergence | |

| Post-Emergence | ||

| By Distribution Channel | Agri-Retailers and Cooperatives | |

| Online Platforms | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Russia | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Australia | ||

| Japan | ||

| Thailand | ||

| Vietnam | ||

| Philippines | ||

| Rest of Asia-Pacific | ||

| Middle East | Turkey | |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How fast is the glufosinate market growing?

The market is forecast to reach USD 3.4 billion by 2031 expanding at a 7.2% CAGR over 2026-2031.

Which is the largest segment by formualtion?

Aqueous suspension concentrate led the largest segment, with 52% of glufosinate market share in 2025.

Which crop segment will grow the quickest?

Oilseeds and pulses are projected to rise at a 9.8% CAGR from 2026-2031.

Why are dry formulation granules gaining share?

They offer up to 80% active loading, cutting freight costs by 40% and improving handling safety.

Page last updated on: