Gas Compressors Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.98 Billion |

| Market Size (2031) | USD 2.29 Billion |

| Growth Rate (2026 - 2031) | 2.97% CAGR |

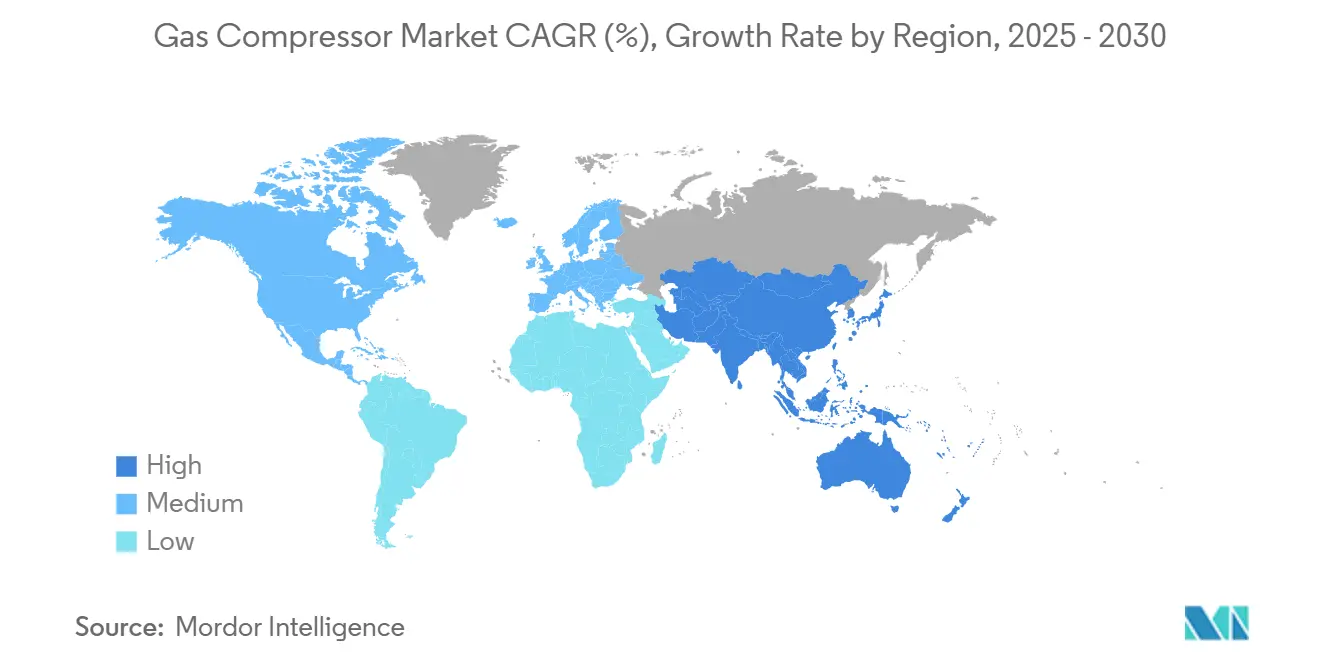

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

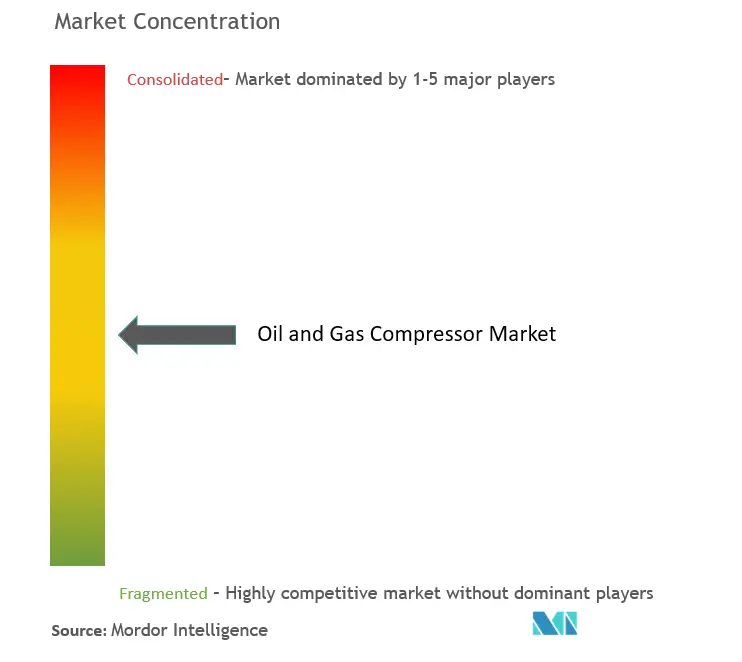

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Gas Compressors Market Analysis by Mordor Intelligence

The Gas Compressors Market size market is expected to grow from USD 1.92 billion in 2025 to USD 1.98 billion in 2026 and is forecast to reach USD 2.29 billion by 2031 at 2.97% CAGR over 2026-2031.

The Gas Compressors Market size is estimated at USD 1.92 billion in 2025, and is expected to reach USD 2.24 billion by 2030, at a CAGR of 3.13% during the forecast period (2025-2030).

- Over the long term, the market is largely driven by the growth in natural gas consumption for various applications, which has led to more gas production and transmission projects and reasonable natural gas prices in the current scenario, which has a positive impact on the upstream sector.

- On the other hand, the growing penetration of renewables in the energy sector offers stiff competition to natural gas consumption and thus impedes the growth of gas compressor deployment in numerous applications.

- Nevertheless, the increase in natural gas proved reserves, particularly offshore gas fields in the recent picture, places a tremendous opportunity for the gas compressor market. The very recent Russian group's Lukoil's oil and gas field discovery off the coast of Mexico is an example of the same. The new upcoming producing fields will lead to a greater deployment of gas compressors for gathering lines.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Gas Compressors Market Trends and Insights

Midstream Sector Expected to Dominate the Market

- The gas compressors used in the midstream oil and gas industry are deployed either within the gas transmission pipeline network or at the compressed gas storage units. Gas flowing in pipelines suffers from pressure losses that increase with flow velocity and the length of the pipe. Therefore, every 50 to 100 miles, a compressor station is necessary to recompress the gas and compensate for the pressure losses.

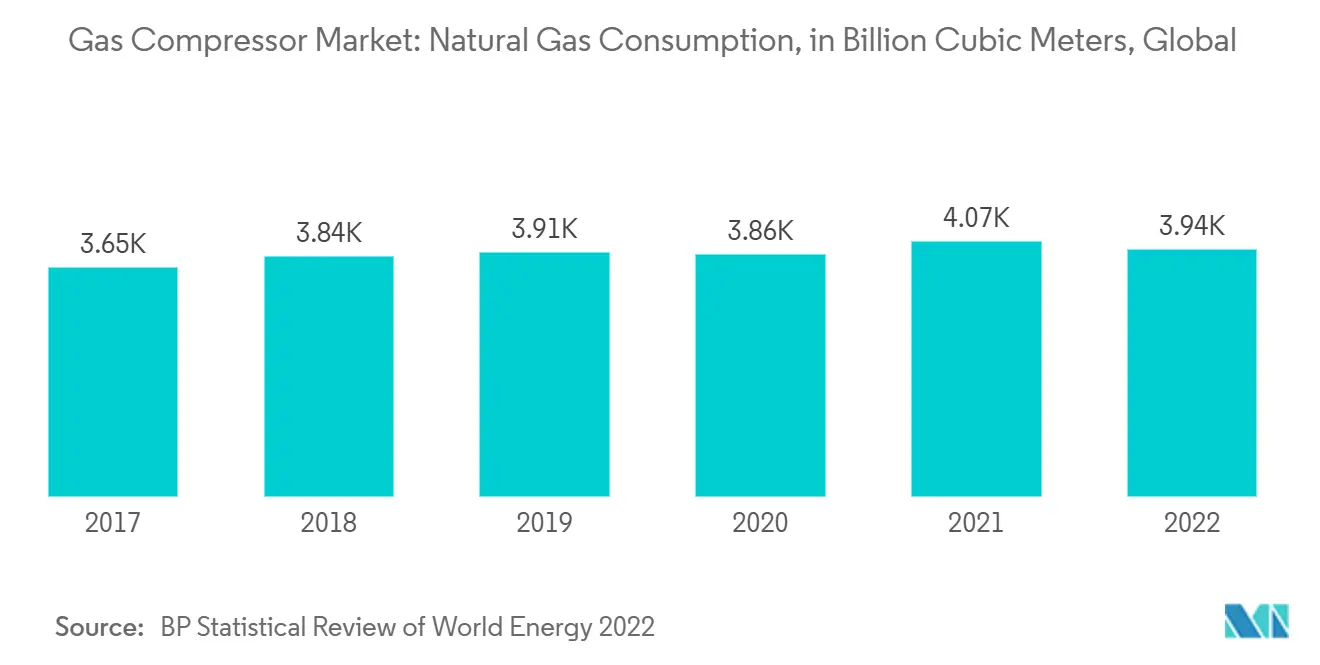

- Natural gas consumption continuously showed an advancing trend over the last 10 years, with around 3941.3 billion cubic meters of consumption in 2022. The demand is expected to grow in the coming years due to the government's push for cleaner methods of energy generation in many countries. A number of pipeline and LNG projects are about to be added to the list of accomplished projects of many midstream companies in the coming years.

- For instance, the Adelphia Gateway Project received approval for the construction of the second phase of the project from the Federal Energy Regulatory Commission (FERC), United States. The project includes the conversion of an existing 84-mile oil pipeline to a gas supply pipeline for distribution in the Philadelphia region. The developer, Adelphia Gateway LLC, is expected to be able to supply the first gas from the pipeline by the end of 2023.

- Furthermore, in February 2023, Oil and Natural Gas Corporation, India's state-owned hydrocarbon giant, initiated a big-buck pipeline replacement project, a crucial project for the company's production from key west coast fields. The USD 446 million project will ensure a stable supply of oil and gas from ONGC wells covering an area of 40,000 square kilometers along the western coast. Since compressors play a crucial role in the oil and gas industry in increasing the pressure of natural gas and allowing natural gas transportation from the production site, this kind of project will, in turn, promote the usage of compressors across the industry.

- Such developments will inevitably have a positive impact on the gas compressor market in the oil and gas industry during the forecast period.

Asia-Pacific Expected to Dominate Market Growth

- Asia-Pacific can account for half of the incremental gas demand in the near future due to increased consumption in the transport and industrial sectors. To serve the natural gas demand for the power generation industry and other applications, the region has witnessed an expansion in the pipeline network, mainly in countries like India and China.

- China's LNG and pipeline imports of natural gas reached record levels in 2022, with an increment of more than 16.6% in LNG imports during the last decade, whereas the gas pipeline monthly imports approached a peak level of 4 million metric tons. The surge in imports will lead to an expansion of the supporting pipeline infrastructure in the country. Moreover, India is expected to bring 34,384 km of new pipelines online by 2023.

- In March 2023, Aramco and joint venture partners Panjin Xincheng Industrial Group and NORINCO Group announced plans to start the construction of a significant integrated refinery and petrochemical complex in northeast China. The complex is going to have combination of a 300,000 barrels per day refinery and a petrochemical plant with an annual production capacity of 1.65 million tons of ethylene and 2 million metric tons of paraxylene. Construction is expected to start in the second quarter of 2023 after the project has secured administrative approvals. It is expected to be fully operational by 2026.

- Also, the rapidly growing network of CNG fueling stations has led to the development of the gas compressor market in the Asia-Pacific region. For example, in April 2023, the government of India announced the target has been fixed to establish around 17,700 CNG stations across the country by 2030.

- Owing to such developments, the gas compressor market is expected to flourish to the greatest extent in the Asia-Pacific region during the study period.

Competitive Landscape

The oil and gas industry's gas compressor market is semi-consolidated. Some of the major companies (in no particular order) include Atlas Copco AB, Ariel Corporation, Bauer Compressor Inc., Clean Energy Fuels Corp., and Ingersoll Rand PLC, among others.

Atlas Copco AB has adopted many strategies like focus on research and development, increase market coverage, increase operational efficiency, develop new sustainable products and solutions offering better value and improved energy efficiency. As an example, in February 2023, the company launched its next generation GA and GA+fixed speed smart industrial air compressors,. Such technological innovations would enable the company to better respond to the changing needs of the industrial customers with diversified product portfolio. These new type of compressors can also be used for clean energy applications like natural gas processing, and hydrogen production.

Gas Compressors Industry Leaders

Ariel Corporation

BAUER Compressors Inc.

Ingersoll Rand PLC

Clean Energy Fuels Corp.

Atlas Copco AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2023: Oilfield services specialist Baker Hughes has been awarded a contract to supply partner QatarEnergy with two main refrigerant compressors (MRCs) for Qatar's North Field South (NFS) project. Qatargas will execute the expansion project. Each MRC train will consist of three Frame 9E DLN Ultra Low NOx gas turbines and six centrifugal compressors across two LNG trains for a total scope of supply of six gas turbines to drive 12 compressors.

- January 2022: Industrial gas technology specialist Burckhardt Compression (Burckhardt) bagged a gas compressor supply contract from TECNIMONT SpA and Tecnimont Private Ltd. to provide compression solutions for the IOCL's upcoming polypropylene plant in Bihar, India. The company is expected to provide EPC and commissioning services for the compression systems.

Global Gas Compressors Market Report Scope

A substance (usually a gas) is compressed by reducing its volume and increasing its pressure in a compressor. It is possible to use compressors in various applications that involve increasing the pressure within the gas storage container, such as compressing gases in petroleum refineries and chemical plants.

The oil and gas industry gas compressor market report is segmented by type, application, and geography (North America, Europe, Asia-Pacific, South America, the Middle East, and Africa). By type, the market is segmented into reciprocating and screw. By application, the market is segmented into upstream, downstream, and midstream. The report also covers the market size and forecasts for the oil and gas industry gas compressor market across the major countries in the region. For each segment, the market size and forecasts have been done based on revenue (USD).

| Reciprocating |

| Screw |

| Upstream |

| Downstream |

| Midstream |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| Spain | |

| United Kingdom | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Malaysia | |

| Indonesia | |

| Rest of Asia-Pacifc | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East & Africa | Saudi Arabia |

| United Arab Emirated | |

| Nigeria | |

| South Africa | |

| Rest of Middle East & Africa |

| Type | Reciprocating | |

| Screw | ||

| Application | Upstream | |

| Downstream | ||

| Midstream | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| Spain | ||

| United Kingdom | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Malaysia | ||

| Indonesia | ||

| Rest of Asia-Pacifc | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East & Africa | Saudi Arabia | |

| United Arab Emirated | ||

| Nigeria | ||

| South Africa | ||

| Rest of Middle East & Africa | ||

Key Questions Answered in the Report

How big is the Oil And Gas Industry Gas Compressor Market?

The Oil And Gas Industry Gas Compressor Market size is expected to reach USD 1.98 billion in 2026 and grow at a CAGR of 2.97% to reach USD 2.29 billion by 2031.

What is the current Oil And Gas Industry Gas Compressor Market size?

In 2026, the Oil And Gas Industry Gas Compressor Market size is expected to reach USD 1.98 billion.

Who are the key players in Oil And Gas Industry Gas Compressor Market?

Ariel Corporation, BAUER Compressors Inc., Ingersoll Rand PLC, Clean Energy Fuels Corp. and Atlas Copco AB are the major companies operating in the Oil And Gas Industry Gas Compressor Market.

Which is the fastest growing region in Oil And Gas Industry Gas Compressor Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which region has the biggest share in Oil And Gas Industry Gas Compressor Market?

In 2025, the Asia Pacific accounts for the largest market share in Oil And Gas Industry Gas Compressor Market.

What years does this Oil And Gas Industry Gas Compressor Market cover, and what was the market size in 2025?

In 2025, the Oil And Gas Industry Gas Compressor Market size was estimated at USD 1.98 billion. The report covers the Oil And Gas Industry Gas Compressor Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Oil And Gas Industry Gas Compressor Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Page last updated on: