Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

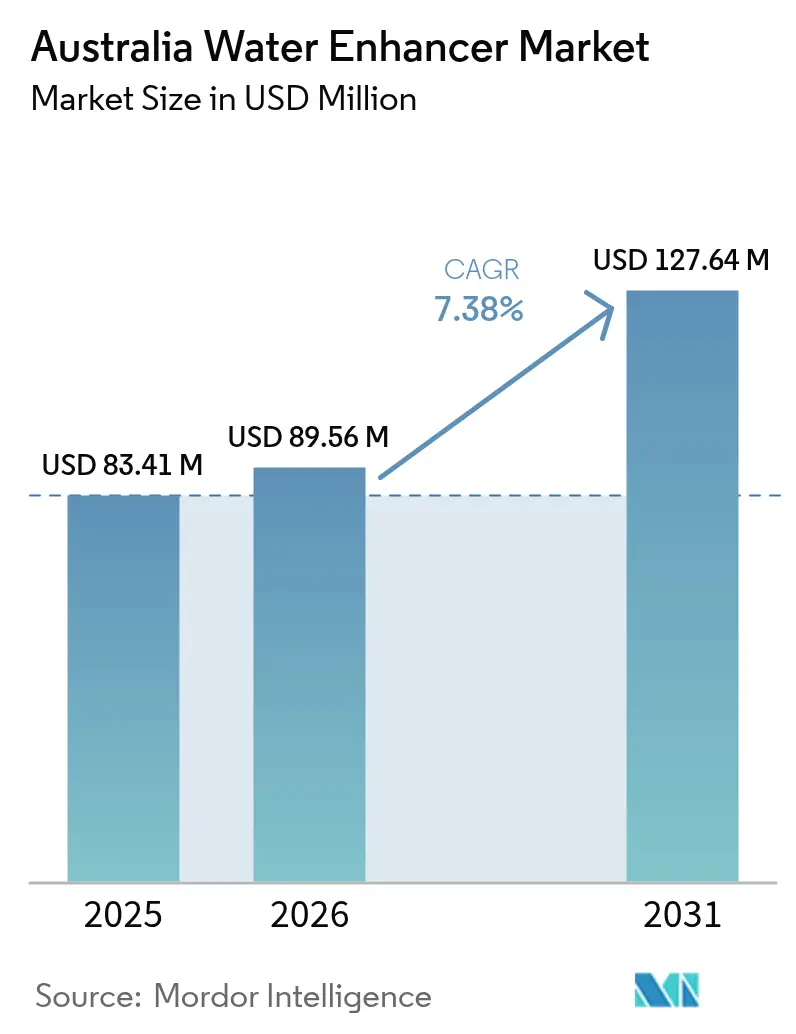

| Base Year Market Size (2025) | USD 83.41 Million |

| Market Size (2026) | USD 89.56 Million |

| Market Size (2031) | USD 127.64 Million |

| Growth Rate (2026 - 2031) | 7.38% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Australia Water Enhancer Market Analysis by Mordor Intelligence

Australia water enhancers market size in 2026 is estimated at USD 89.56 million, growing from 2025 value of USD 83.41 million with 2031 projections showing USD 127.64 million, growing at 7.38% CAGR over 2026-2031. Health-conscious consumers, coupled with favorable regulations on sweeteners, are driving revenue growth. This surge occurs amidst competition for shelf space between flavored bottled water and other ready-to-drink (RTD) options. Producers are leveraging zero-calorie claims and natural flavor systems, often bundling promotions with reusable bottles, aligning closely with consumer priorities centered on wellness and sustainability. There's a noticeable shift in focus: moving from mere taste customization to performance hydration, highlighted by the rising popularity of functional extensions like electrolyte and branched-chain amino acid (BCAA) blends. Additionally, climate-driven events, such as outdoor work and sports, have intensified demand in states with higher temperatures. Meanwhile, online subscription models are challenging the traditional dominance of supermarkets, streamlining replenishment and extending their reach into regional communities.

Key Report Takeaways

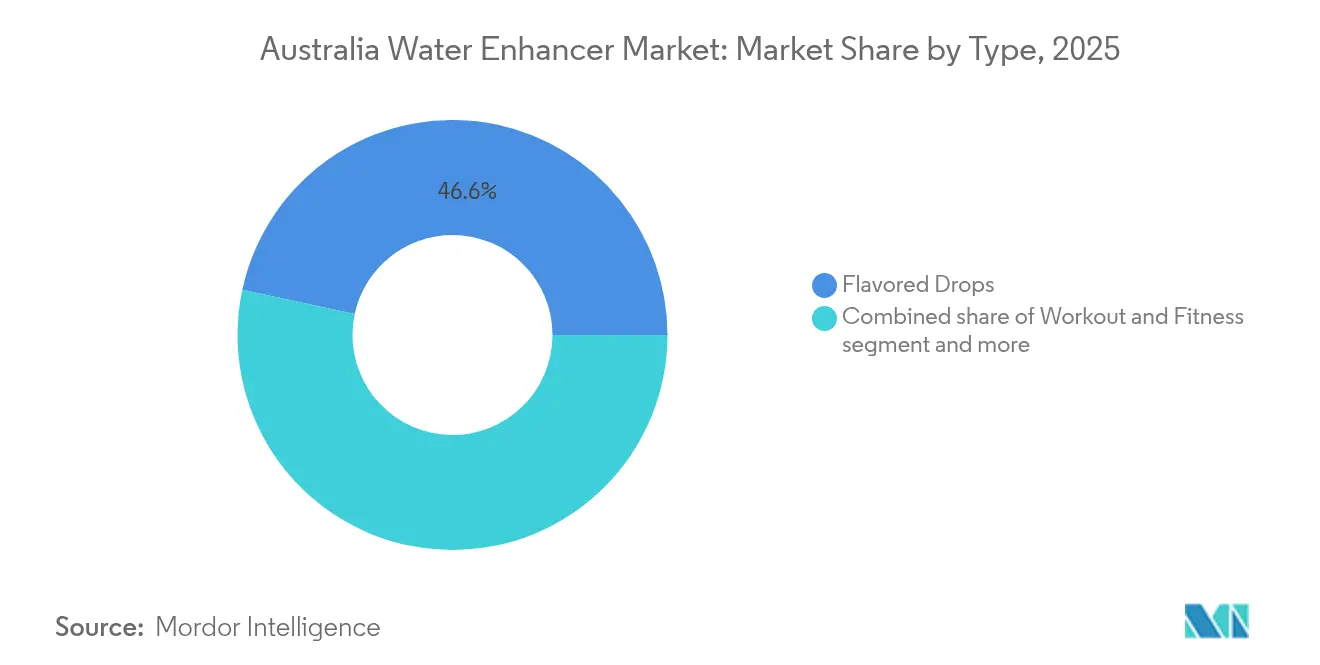

- By product type, flavored drops led with a 46.62% Australia water enhancers market share in 2025 and are on course for a 6.74% CAGR between 2026–2031, while workout and fitness enhancers are forecast to grow at the fastest 8.01% CAGR over the same horizon.

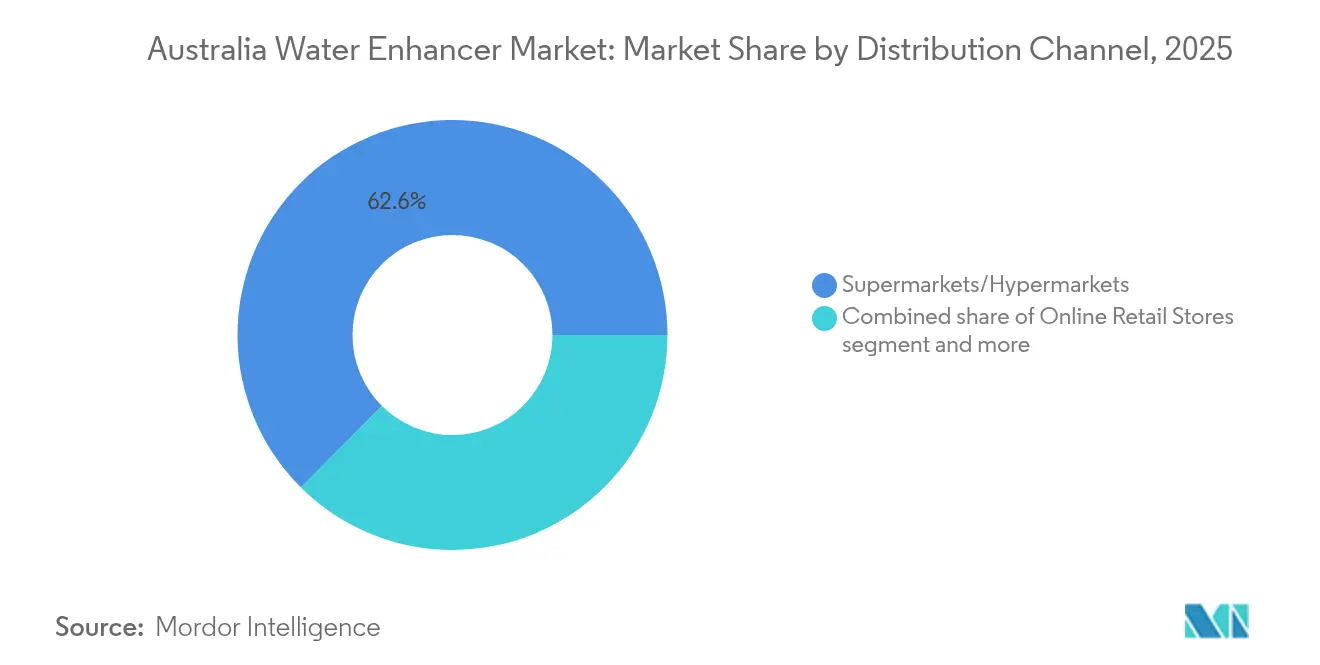

- By distribution channel, supermarkets and hypermarkets controlled 62.55% of the Australia water enhancers market size in 2025; online retail is set to expand at a 7.63% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Australia Water Enhancer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health-conscious consumers replacing sugary beverages | +1.8% | National, stronger in Sydney, Melbourne, Brisbane | Medium term (2-4 years) |

| Portability and convenience of drops/cubes | +1.2% | Regional areas with limited retail density | Short term (≤ 2 years) |

| New product launches emphasizing natural, zero-sugar claims | +1.5% | Premium SKUs in metropolitan markets | Medium term (2-4 years) |

| Heat-resistant formulations for out-of-home occasions | +0.9% | Northern Territory, Queensland, Western Australia | Long term (≥ 4 years) |

| Retailers in CDS-driven states bundling enhancers with reusable bottles | +0.6% | Container Deposit Scheme (CDS)-active jurisdictions | Short term (≤ 2 years) |

| Wide availability and merchandising in retail stores | +1.0% | National, with supermarket chains driving volume | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Health-conscious consumers replacing sugary beverages

Australian adults are cutting back on added sugars, shifting their spending from carbonated soft drinks to low-calorie flavor solutions. This trend reflects growing health consciousness and a desire to reduce sugar-related health risks. Medical advocates push for a sugar levy, highlighting the metabolic risks of sweetened drinks and intensifying scrutiny on labels. Enhancers based on stevia and sucralose cater to sweet cravings while adhering to Food Standards Australia New Zealand (FSANZ) intake limits. These enhancers not only provide a healthier alternative but also align with regulatory standards, ensuring consumer safety. The economics are compelling: a 45 ml bottle, offering 90 servings, is significantly cheaper per liter than bottled flavored water. As grocery budgets tighten, households are increasingly viewing enhancers as a budget-friendly means to achieve healthier hydration, making them an attractive option for cost-conscious consumers.

Portability and convenience of drops/cubes format

Liquid concentrates and micro-cubes, designed to fit easily into pockets and handbags, effectively address the bulkiness issue of RTD bottles. This innovation is particularly beneficial for commuters, students, and office workers who prioritize convenience and portability in their daily routines. A mere 45 ml pack can produce approximately 18 liters of flavored water, all while weighing in at under 50 grams. This lightweight design not only promotes ease of use but also aligns with the Container Deposit Scheme (CDS) incentives, which encourage the use of reusable bottles to reduce waste. Furthermore, retailers are leveraging cross-merchandising opportunities by pairing these enhancers with stainless-steel drinkware, leading to increased basket sizes at checkouts and driving additional sales.[1]Source: New South Whales Environment Protection Authority, "Return and Earn", epa.nsw.gov.au Online specialty stores are also tapping into this growing demand by offering subscription bundles that automate the restocking process, ensuring consumers never run out of their preferred products. These combined strategies create a seamless portability and convenience proposition that competitors in the RTD market find difficult to replicate, giving liquid concentrates and micro-cubes a distinct edge.

New product launches emphasizing natural, zero-sugar claims

Brand owners are racing to outdo one another with clean labels, increasingly turning to fruit concentrates, botanical extracts, and plant-based sweeteners to meet growing consumer demand for healthier and more transparent ingredient lists. Waterdrop’s microdrink cubes, which combine fruit and vitamin powders, have made their way to Woolworths nationwide and are gaining visibility as the hydration partner for the Australian Open 2025, a move that aligns with its strategy to target health-conscious and active consumers. PepsiCo’s Gatorade Hydration Booster, which made its debut overseas with a zero-sugar formulation, is now poised for an Australian launch through Asahi’s bottling network, leveraging its established distribution channels to capture market share. Vital Zing has ventured into soda flavors, aiming to attract those switching from soft drinks, all while maintaining its natural brand image to appeal to a broader audience seeking healthier alternatives. This steady stream of product launches not only keeps consumers engaged but also revitalizes shelf space in both supermarkets and e-commerce platforms, ensuring brands remain competitive in an evolving market landscape.

Heat-resistant formulations for out-of-home occasions

In Queensland, Northern Territory, and Western Australia, summer heatwaves frequently exceed 35 °C, jeopardizing the flavor stability of standard liquids[2]Source: Australia Bureau of Meteorology, "Annual climate statement 2024", bom.gov.au. This creates a significant challenge for beverage brands aiming to maintain product quality in extreme conditions. To address this, brands gain a competitive edge for outdoor activities, road trips, and sports with powder cubes and advanced liquid bases that resist separation, ensuring consistent performance even in high temperatures. Mining firms, recognizing the value of hydration solutions, incorporate electrolyte drops into worker hydration kits, ensuring trial usage among their workforce and promoting adoption in demanding environments. Powerade Drops capitalizes on its sports equity to appeal to active consumers, whereas Waterdrop’s cube sidesteps spill risks in sweltering vehicles, offering a practical solution for on-the-go hydration. With a durable taste even in high temperatures, these innovative products find consumption occasions extending well beyond the traditional household kitchen, catering to diverse consumer needs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from flavored bottled water, RTD teas, functional beverages | -1.1% | National, strongest among urban millennials | Medium term (2-4 years) |

| FSANZ reviews of high-intensity sweetener acceptable daily intakes | -0.5% | National, tied to federal regulation | Medium term (2-4 years) |

| Competition from flavored bottled water, RTD teas, functional beverages | -1.1% | National, with premium RTD brands capturing urban millennials | Medium term (2-4 years) |

| Consumer skepticism about product classification and efficacy | -0.4% | National, particularly among older demographics unfamiliar with category | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Competition from flavored bottled water, rtd teas, and functional beverages

RTD brands, strategically positioned in prime cooler facings, are successfully tapping into impulse buys at petrol stations and convenience outlets[3]Source: Australian Competition and Consumer Commission, "Supermarket Inquiry 2024", accc.gov.au. These placements ensure high visibility and capitalize on consumer behavior driven by convenience and immediacy. Premium sparkling waters, priced between AUD 3–6 per bottle, are drawing in shoppers seeking immediate refreshment, with offerings from industry giants like Coca-Cola and Asahi. These products cater to a growing demand for premium, on-the-go beverages. Meanwhile, RTD tea lines are emphasizing antioxidant and probiotic benefits, aligning with the functional promises of enhancers and appealing to health-conscious consumers. Start-ups such as Nexba and Remedy are harnessing the power of social influencers to boost brand visibility on digital platforms, effectively reaching younger, tech-savvy audiences. However, the prominent display of chilled RTDs is overshadowing enhancers, limiting their visibility and potentially diverting converts from the category. This visual dominance in retail spaces poses a challenge for enhancers to capture consumer attention and expand their market share.

FSANZ reviews of high-intensity sweetener acceptable daily intakes

FSANZ keeps a close watch on global toxicology updates, periodically reassessing the safety of stevia, sucralose, and acesulfame-K. If intake thresholds tighten, brands might have to cut back on sweetener dosages per serving. This not only complicates formulations but also drives up costs, as manufacturers may need to invest in alternative ingredients or technologies to maintain product quality. Such reformulations could change the taste, potentially pushing consumers towards other hydration options, thereby impacting market share. Additionally, labels might need more prominent warnings, which could tarnish the perception of the category as a healthy choice and deter health-conscious consumers. Thus, the looming regulatory scrutiny adds a layer of strategic uncertainty to R&D plans, forcing companies to reassess their innovation strategies and timelines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Electrolyte Blends Outpace Flavor-Only Offerings

In 2025, flavored drops captured 46.62% of the Australia water enhancers market, thanks to their widespread appeal for daily hydration across various age groups. Priced lower per serving than their functional counterparts, these drops encourage repeat purchases and dominate shelf space in supermarkets and convenience stores. With a diverse flavor range, they attract casual consumers who prioritize taste over nutritional claims, solidifying their brand presence amidst evolving preferences. The segment thrives on its easy accessibility and habit-forming allure, maintaining its volume lead even as performance-driven options rise in popularity. Additionally, their versatility allows consumers to customize water to their taste preferences, making them a convenient and appealing choice for on-the-go hydration. This adaptability ensures their continued relevance in a market where consumer preferences are constantly evolving.

Electrolyte-rich variants tailored for workouts and fitness are set to lead the market with an 8.01% CAGR from 2026 to 2031, riding the wave of increasing gym memberships and a surge in endurance sports. Positioned alongside BCAAs and vitamins in sports-nutrition aisles, these premium-priced enhancers resonate with athletes and fitness enthusiasts. To combat competition from soft drinks, manufacturers have introduced caffeine-infused variants targeting students and shift workers. Innovations like heat-stable carriers and microencapsulation techniques ensure flavor stability, even in extreme climates. Furthermore, these products cater to the growing demand for functional beverages that support hydration and recovery, making them an essential part of active lifestyles. Additionally, strategies like cross-promotions with reusable bottles, loyalty apps, and influencer-driven recipes amplify engagement, attracting both casual drinkers and dedicated enthusiasts. These marketing efforts not only boost brand visibility but also foster a sense of community among users, further driving category growth.

By Distribution Channel: Online Subscriptions Cut Replenishment Friction

In 2025, supermarkets and hypermarkets led Australia's water enhancers market, capturing 62.55% of national sales. Their success stemmed from savvy end-cap displays, enticing multi-buy promotions, and shoppers' familiarity with nearby beverage categories. By strategically placing products near water, sports drinks, and health snacks, these retailers encouraged trial purchases from health-conscious grocery shoppers. The channel's high foot traffic and impulse buying tendencies solidified its status as the go-to venue for everyday hydration enhancers.

On the other hand, pure-play e-commerce and direct-to-consumer platforms emerged as the fastest-growing channel, boasting a 7.63% CAGR. Their growth was fueled by subscription discounts and enticing free-shipping offers, which in turn boosted the average order value. These online platforms granted regional households and convenience-store shoppers access to a wider assortment than what local physical shelves could provide. Furthermore, influencer campaigns on social media, featuring unboxings and flavor-mix challenges, funneled traffic directly to brand websites, enhancing consumer engagement and retention. While niche channels like pharmacies, gyms, and specialty health stores remained vital for premium electrolyte formulations, petrol stations ventured into single-serve sachets for spontaneous road-trip purchases, despite facing limited shelf space. This varied channel landscape shields the market from becoming overly dependent on any single retailer's bargaining power.

Geography Analysis

New South Wales and Victoria, home to the largest metropolitan clusters, dominate in premium SKU turnover and swiftly embrace novel formats. Urban consumers in these states boast higher discretionary incomes and show a pronounced willingness to invest in natural claims, recyclability, and vitamin fortification. These preferences align with the growing trend of health-conscious and environmentally aware purchasing behaviors, making these regions key markets for premium and innovative products. Meanwhile, Queensland's tropical climate and outdoor lifestyle drive a heightened demand for electrolyte drops, especially those resilient to vehicle and backpack heat. This demand is further fueled by the state's active participation in outdoor activities and sports, where hydration solutions are essential. In Western Australia, the mining sector's prominence lends credibility to performance hydration, with electrolyte powders becoming staples in workplace health protocols. The physically demanding nature of mining work and the harsh environmental conditions make hydration products a necessity, embedding them into daily routines.

Across all states and territories, active Container Deposit Schemes bolster the habit of using reusable bottles. Retailers capitalize on this trend, often bundling stainless-steel drinkware with starter packs of enhancers. These initiatives not only promote sustainability but also encourage consumers to adopt refillable solutions, creating a shift in consumption patterns. South Australia, a trailblazer in CDS initiatives, boasts the highest rates of container returns, solidifying a foundation for refill-friendly solutions. The state's long-standing commitment to recycling has fostered a culture of environmental responsibility, making it a leader in sustainable practices.

Victoria's CDS rollout in late 2023 spurred a surge in reusable bottle sales, with early redemption statistics hinting at lasting habit formation. This development reflects a growing consumer inclination toward sustainable and cost-effective hydration options. However, remote areas in Northern Territory and Far North Queensland grapple with e-commerce freight surcharges, hindering adoption among budget-conscious households. These logistical challenges limit access to innovative products, creating a disparity in market penetration. Despite this, state health agencies persist in funding campaigns to prevent dehydration, subtly enlightening these communities about the advantages of portable flavor solutions. These campaigns play a crucial role in raising awareness and educating consumers on the benefits of hydration enhancers, gradually driving adoption even in underserved regions.

Competitive Landscape

In Australia water enhancer market characterized by moderate concentration, beverage giants like Coca-Cola, PepsiCo, and Nestlé dominate shelf negotiations. However, these multinationals are honing in on ready-to-drink (RTD) lines, inadvertently carving out opportunities for niche brands. Waterdrop, a rising player, made waves with its 2025 roll-out at Woolworths, leveraging an innovative cube format. This design not only enhances portability but also champions sustainability, filling gaps left by traditional liquid competitors. Meanwhile, Coca-Cola Europacific Partners is bolstering its Moorabbin plant, signaling robust confidence in the enduring demand for concentrates and powders. In tandem, Powerade Drops is broadening the company's foothold in the sports domain.

Vital Zing is making strides with its stevia-infused formulations, leveraging competitive pricing through niche online outlets. This strategy has garnered a loyal following, especially among keto enthusiasts and diabetics who prioritize health-conscious and low-sugar options. On another front, Hydralyte is adeptly navigating both OTC pharmacies and the broader wellness arena, highlighting the functional appeal of its offerings. Its dual positioning allows it to cater to consumers seeking hydration solutions for both medical and lifestyle purposes.

Today's marketing strategies have shifted gears. Instead of traditional TV spots, there's a pronounced emphasis on athlete endorsements, collaborations with esports, and engaging TikTok challenges. This evolution underscores a strategic pivot towards a digitally-savvy consumer base. As the Australia water enhancers market charts its growth, key players are doubling down on investments in heat-stable chemistries, clean labels, and a robust omnichannel distribution strategy, carving out a distinct competitive edge.

Australia Water Enhancer Industry Leaders

-

The Coca-Cola Company

-

Kraft Heinz Company

-

Keurig Dr Pepper, Inc.

-

Wisdom Natural Brands

-

Bolero Drink Australia

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Waterdrop forged a nationwide alliance with Woolworths, introducing five of its microdrink cube variants in about 900 stores. This rollout covers nearly 90% of Woolworths' footprint in Australia. Strategically, the products are shelved in the health-food aisle, targeting shoppers in search of convenient, eco-friendly alternatives to pre-mixed drinks.

- September 2025: Waterdrop, in a strategic move, secured its position as the official hydration partner for the Australian Open 2025. In tandem, the brand unveiled a co-branded product line, SILA x waterdrop, in collaboration with tennis legend Novak Djokovic. This partnership underscores Waterdrop's strategy of harnessing elite athlete endorsements to bolster its functional hydration claims, particularly targeting fitness-conscious consumers.

Australia Water Enhancer Market Report Scope

The Australia water enhancer market offers the product through Pharmacies & Health Stores, Convenience Stores, Hypermarkets/Supermarkets, Online Channels, and Other Distribution Channels.

By Product Type

| Energy Drops |

| Workout and Fitness (Electrolyte / BCAA) |

| Flavoured Drops |

By Distribution Channel

| Supermarket/Hypermarket |

| Convenience Stores |

| Online Retail Stores |

| Other Distribution Channels |

| By Product Type | Energy Drops |

| Workout and Fitness (Electrolyte / BCAA) | |

| Flavoured Drops | |

| By Distribution Channel | Supermarket/Hypermarket |

| Convenience Stores | |

| Online Retail Stores | |

| Other Distribution Channels |

Key Questions Answered in the Report

How large will Australia’s water-flavor segment be by 2031?

Forecasts indicate the Australia water enhancers market will reach USD 127.64 million by 2031, expanding at a 7.38% CAGR.

Which product type is growing the fastest?

Workout and fitness enhancers, rich in electrolytes and BCAAs, are projected to log the highest 8.01% CAGR between 2026–2031.

Where do most shoppers buy enhancers today?

Supermarkets and hypermarkets contribute 62.55% of 2025 sales, benefiting from high foot traffic and promotional displays.

Are online subscriptions significant for repeat purchase?

Yes, direct-to-consumer websites and pure-play e-commerce are the fastest-growing channels, advancing at a 7.63% CAGR through 2031.

Page last updated on: