Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 73.21 Billion |

| Market Size (2031) | USD 117.35 Billion |

| Growth Rate (2026 - 2031) | 9.92% CAGR |

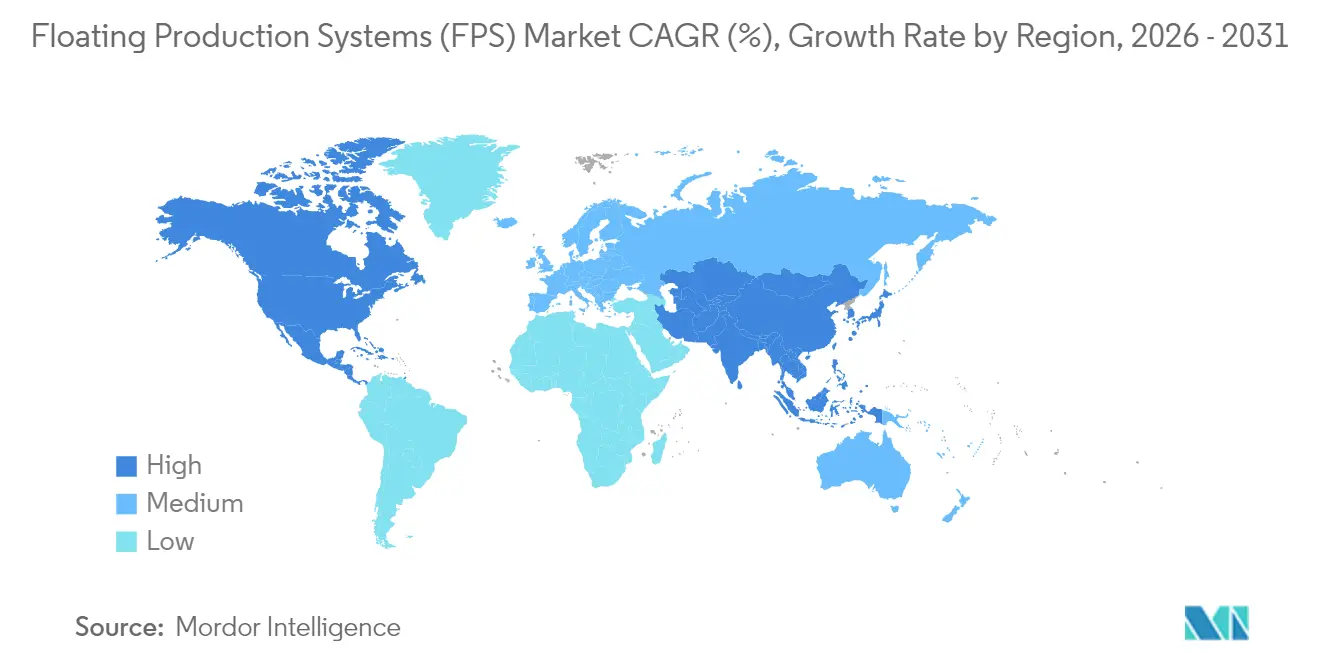

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

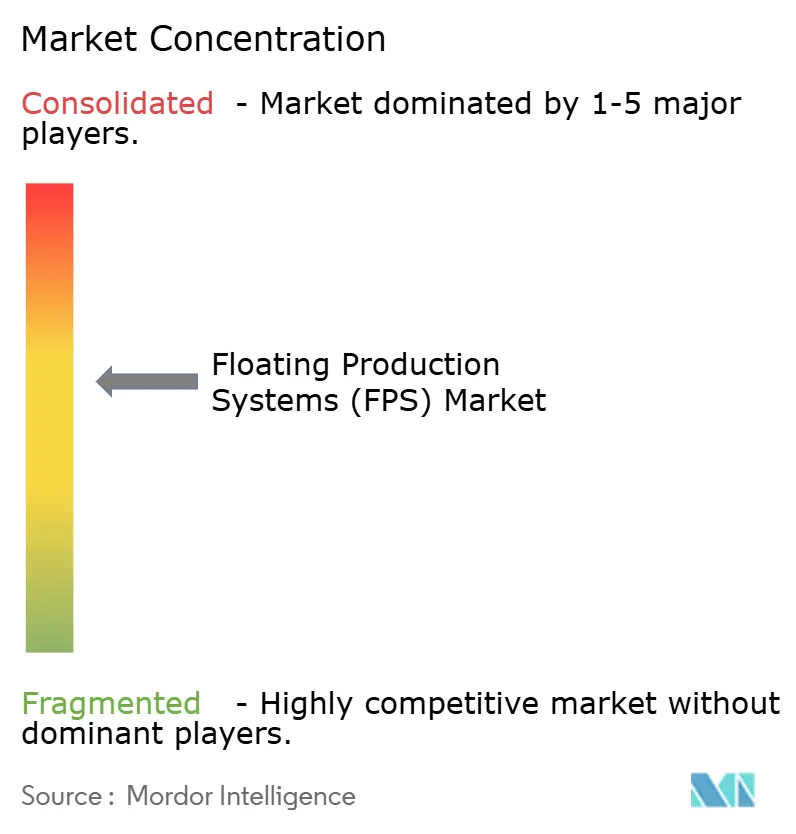

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Floating Production Systems (FPS) Market Analysis by Mordor Intelligence

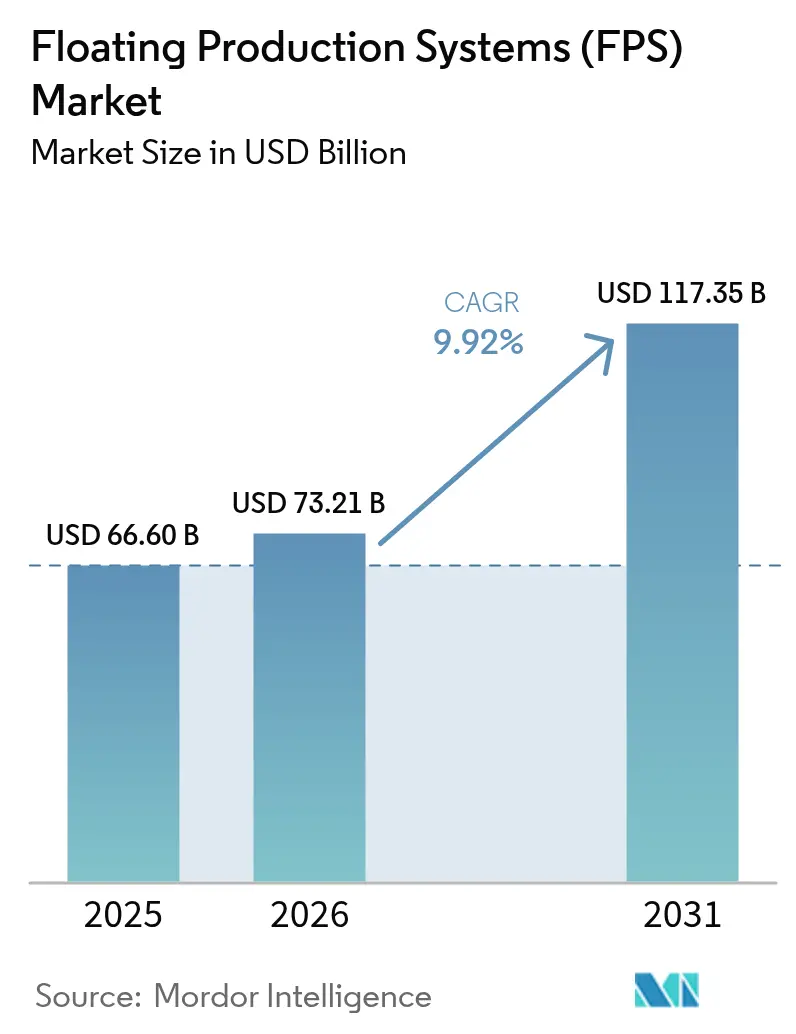

The Floating Production Systems Market size was valued at USD 66.60 billion in 2025 and estimated to grow from USD 73.21 billion in 2026 to reach USD 117.35 billion by 2031, at a CAGR of 9.92% during the forecast period (2026-2031).

Operators are steering capital toward deeper waters as legacy shallow-water basins mature, and this pivot aligns with rising adoption of standardized hulls, electrified topsides, and carbon-capture-ready designs. North America remains the revenue anchor, owing to the prolific Gulf of Mexico projects, while the Asia-Pacific is expanding the fastest, as governments treat domestic offshore output as a strategic priority. Technology breakthroughs in 20 kpsi equipment, modular CO₂-capture packages, and digital well surveillance are compressing project cycles, lowering breakeven thresholds, and broadening the addressable reservoir base. Mergers between yard majors and EPC players are tightening supply chains yet raising execution certainty for multi-billion-dollar orders placed by national oil companies pursuing energy security.

Key Report Takeaways

- By type, FPSO units led with 54.10% revenue share in 2025, and the segment is projected to grow at a 10.12% CAGR through 2031.

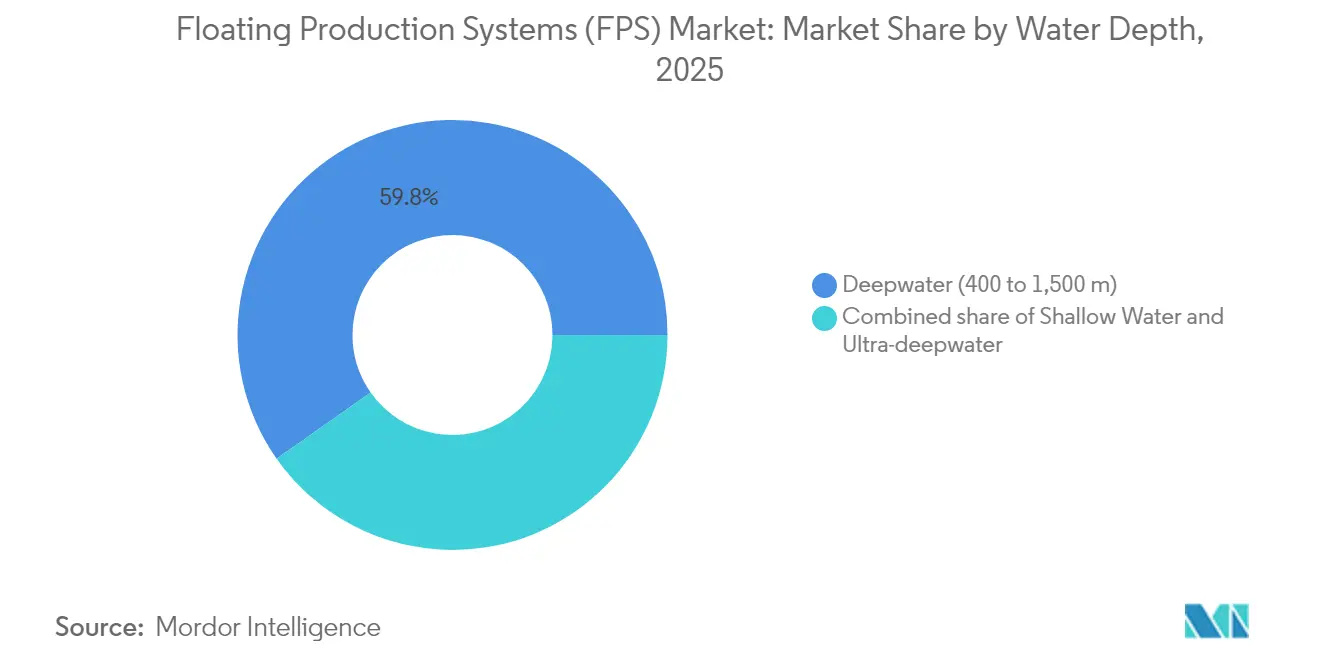

- By water depth, deepwater installations captured 59.75% of the floating production systems (FPS) market share in 2025, while ultra-deepwater projects are expected to compound at an annual rate of 10.62% to 2031.

- By build method, conversions accounted for 62.15% of the floating production systems (FPS) market size in 2025; however, newbuilds are forecasted to accelerate at a 10.95% CAGR during 2026-2031.

- By geography, North America accounted for 38.30% of the floating production systems (FPS) market size in 2025, whereas Asia-Pacific is expanding at a 11.18% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Floating Production Systems (FPS) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising deep-water exploration investments | +2.8% | Gulf of Mexico, Brazil, West Africa, Guyana | Medium term (2-4 years) |

| Declining shallow-water reserves | +2.1% | North Sea, Gulf of Mexico mature basins | Long term (≥ 4 years) |

| Advances in FPSO conversion technologies | +1.7% | Asia-Pacific, Europe, West Africa | Short term (≤ 2 years) |

| Energy-security push by emerging economies | +1.4% | Asia-Pacific, Latin America, Middle East & Africa | Medium term (2-4 years) |

| Surge in marginal-field leasing models | +0.9% | North America, European Union, selective Asia-Pacific markets | Short term (≤ 2 years) |

| Electrification of topsides | +0.6% | Norway, United Kingdom, selected global pilot projects | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Deep-water Exploration Investments

Capital is moving rapidly into deep and ultra-deepwater acreage as operators chase high-impact discoveries outside legacy provinces. ExxonMobil’s fourth FPSO in Guyana lifts the country’s installed capacity toward 900,000 b/d and underscores investor confidence in ultra-deep finds that remain profitable at mid-cycle oil prices. Chevron’s Anchor and BP’s Kaskida developments utilize a 20 kpsi subsea architecture to deliver Paleogene barrels that conventional equipment could not unlock(1)Chevron Corporation, “Chevron bolsters U.S. Gulf of Mexico production with Whale facility startup,” chevron.com . TotalEnergies’ Kaminho project in Angola demonstrates that African frontiers can now absorb multi-billion-dollar floating investments without relying on fixed platforms. Collectively, these programs illustrate how technology maturity, robust reservoir productivity, and fiscal incentives are sustaining a pipeline of new build contracts for the floating production systems market.

Declining Shallow-water Reserves Shifting Production Offshore

Reservoir depletion across the North Sea and other shelf provinces is pushing operators to re-platform toward deeper turbidite plays where only floating concepts are technically feasible. Equinor’s NOK 10 billion life extension of Oseberg leverages electrification to extend plateau production beyond 2040, while freeing fixed-platform budgets for deeper targets nearby. Gulf of Mexico incumbents mirror this strategy: the Whale semi-submersible began pumping in January 2025 with a 100,000 b/d capacity, replacing output from legacy topsides that were approaching decommissioning. The consequence is a structural rise in demand for hulls, mooring lines, and subsea systems that can be redirected to new reservoirs once primary leases decline, thereby reinforcing the attractiveness of redeployable FPSOs.

Advances in FPSO Conversion Technologies

Standardized tanker-to-FPSO programs are reducing project cycles by 18-24 months and reducing capital budgets by as much as 30% compared to bespoke newbuilds. SBM Offshore’s Fast4Ward® inventory of generic hulls underpins a USD 33.7 billion contracted backlog, validating the scale economies of repetition engineering(2)SBM Offshore, “2024 Half-Year Earnings,” sbmoffshore.com . Carbon-capture modules sized for 100,000 barrels per day (b/d) topsides are now offered as plug-ins, enabling converted units to meet tightening financial covenants without extensive redesign. Shell’s Whale project demonstrates how modular electrification reduces greenhouse-gas intensity to below 10 kg CO₂e/boe, while allowing brownfield tie-backs that extend reservoir life(3)Shell plc, “Whale: Setting new standards for deep water,” shell.com . These technology pathways expand the floating production systems market by unlocking marginal discoveries that would otherwise fail screening tests.

Energy-security Push by Emerging Economies

National oil companies in Brazil, China, and Indonesia are accelerating offshore developments to curb import dependence. Petrobras has earmarked USD 111 billion through 2029, of which 70% is dedicated to pre-salt FPSOs that collectively add 3.2 million barrels per day (b/d) of capacity. China’s first FPSO fitted with CO₂ capture entered service in February 2025, aligning with the government’s target to lift the domestic energy self-sufficiency ratio to 95% by 2060. Indonesia’s production-sharing reforms now prioritize domestic gas offtake, encouraging independent operators to employ lease-and-operate FPSOs that can switch fields once plateau rates taper. These policies channel sovereign capital and export-credit guarantees toward the floating production systems market, compressing financing timelines and spurring regional shipyard activity.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Crude-oil price volatility | -1.8% | Global, especially high-cost frontier areas | Short term (≤ 2 years) |

| High CAPEX & OPEX requirements | -1.2% | Global, acute for independents and marginal fields | Medium term (2-4 years) |

| Limited mega-hull shipyard capacity | -0.7% | Asia-Pacific yards handling most FPSO construction | Medium term (2-4 years) |

| ESG-linked financing constraints | -0.5% | Europe and North America first, spreading worldwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Crude-oil Price Volatility

Floating developments are capital-intensive and rely on multi-year payback horizons so that rapid oil-price swings can freeze final investment decisions. Operators paused several Gulf of Mexico tie-backs in late 2024 when benchmark prices dipped below USD 70/bbl, and rig utilization slid five percentage points in tandem. While integrated majors can hedge, independents often defer sanctioning until strip prices stabilize, creating a lumpy ordering pattern for hull fabricators. The counterweight is that the floating production systems market now benefits from lower structural breakevens—many deepwater projects operate profitably at USD 45–50/bbl after standardization and digital optimization—softening the impact of short-term price shocks.

High CAPEX & OPEX Requirements

Fully integrated FPSO projects frequently exceed USD 1 billion, and for complex pre-salt units, can reach USD 3 billion or more. Petrobras’ twin P-84 and P-85 contracts reached USD 8.15 billion, underscoring the financial burden even on large NOCs. Operating expenditure is also elevated: specialist shuttle tankers, dynamic-positioning support vessels, and subsea inspection programs face inflationary pressure amid global yard congestion. Standardized designs and supply-chain partnerships are reducing these costs, yet budget overruns still force smaller licensees to surrender acreage or seek farm-ins, thereby limiting market breadth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: FPSO Dominance Meets Expanding Niche Platforms

The floating production systems market size for FPSO units stood at USD 36.03 billion in 2025 and, supported by a 10.12% CAGR, is set to nearly double by 2031. FPSOs perform well in cyclonic basins, can be relocated as field economics evolve, and integrate topside processing for 225,000 b/d or more, as evidenced by SBM’s Almirante Tamandaré unit off Brazil. Tension-leg platforms continue to serve slender ultra-deep targets where heave suppression is vital, while SPARs and semi-subs retain roles in harsh-environment drilling and early production testing. The market’s environmental pivot is most visible in FPSOs that bundle CO₂-stripping columns and shore-power readiness, technologies that are harder to retrofit on legacy semi-subs or barges.

Second-generation FPSOs are utilizing digital twins to predict equipment fatigue, optimize gas-lift allocation, and schedule maintenance, resulting in uptime exceeding 96%. These improvements underpin the segment’s leading growth within the floating production systems market and encourage financiers to treat FPSO revenue streams as quasi-infrastructure. Niche hull classes, such as barges, retain strategic importance for shallow Asian deltas, but their growth potential is capped by water-depth limits. Overall, FPSOs will continue ruling both absolute revenue and incremental demand as operators seek flexible, low-staffed solutions that align with emerging decarbonization mandates.

By Water Depth: Ultra-deepwater Momentum Builds on Technology Maturity

Deepwater deployments (400–1,500 m) contributed the bulk of 2025 revenue; however, ultra-deepwater fields (>1,500 m) are the growth pacesetters and will steadily increase their share of the floating production systems market size through 2031. BP’s 20 kpsi Kaskida scheme at 1,800 m and Chevron’s Anchor at comparable depths illustrate how next-wave metallurgy, high-pressure risers, and subsea multiphase pumps unlock reservoirs once deemed stranded. Deepwater acreage benefits from mature logistics, lower uncertainty, and, in regions such as Brazil’s Campos Basin, robust subsea infrastructure that mitigates unit costs.

Ultra-deepwater schemes increasingly incorporate high-density power distribution from shore, enabling operators to run electric compressors and seawater injection pumps at depths of 3,000 m without relying on local gas turbines. The shift narrows OPEX differentials versus shallower projects and positions ultra-deepwater capacity as an efficient back-fill for cash-generating brownfields. Simultaneously, reservoir engineers utilize longer horizontal laterals and high-strength flowlines to mitigate hydrate risk, resulting in quicker ramp-ups and flatter decline curves. Consequently, the floating production systems market continues to rotate toward ultra-deep licenses whenever fiscal terms and political risk are manageable.

By Build Method: Conversions Hold Volume, Newbuilds Capture Premium Growth

Conversions dominated 2025 activity, thanks to an inventory of aging VLCCs available at a discount, enabling operators to place units in service within 30-36 months and at a capital intensity of below USD 15,000 per daily barrel processed. This cost edge secures a 62.15% slice of the floating production systems market share, yet purpose-built hulls are attracting record interest as owners pursue Net-Zero readiness. Seatrium’s P-84 and P-85 FPSOs integrate zero routine flaring, dedicated CO₂ reinjection, and closed-bus electric distribution, features that raise upfront costs but can prolong hull life beyond 30 years and avoid stranded-asset risk.

Newbuilds also support heavier topsides demanded by 20 kpsi reservoirs and high-GOR fluids, capacities rarely achievable within VLCC hull envelopes. Digital native designs incorporate fiber-optic backbone cabling, condition-based monitoring, and remote operations centers, resulting in a 40% reduction in offshore headcount and a 15% decrease in OPEX over the first decade of service. Conversely, conversions are refining work scopes with prefabricated modules that shorten quayside integration, preserving their role as the quickest route to first oil for marginal fields. Over the forecast horizon, the floating production systems market will exhibit a balanced profile, with conversions supplying volume and cash flow, and newbuilds delivering higher growth and showcasing technology opportunities.

Geography Analysis

North America retained a 38.30% revenue share in 2025, anchored by the Gulf of Mexico, where the U.S. Energy Information Administration projects stable offshore oil output of 1.80 million barrels per day (b/d) for 2025. Discoveries, such as Ballymore and Swordfish, leverage existing pipeline hubs, and regulatory certainty fosters a steady backlog of tie-backs that favor mid-sized FPSOs. Mexico’s deepwater Salina Basin, although still at the appraisal stage, promises upside once fiscal incentives mature. Canada’s Bay du Nord is the country’s first floater-ready prospect and, should it proceed, will extend regional fabrication capacity beyond Newfoundland yard upgrades.

Asia-Pacific is the fastest-growing territory, recording an 11.18% CAGR to 2031 as China, Indonesia, and Australia prioritize domestic hydrocarbons. CNOOC’s record discovery success keeps shipyards busy, and Chinese contractors have launched the world’s first carbon-capture-equipped FPSO to underpin national climate goals while boosting liquids output. Indonesia’s reformed production-sharing contracts are designed for the rapid monetization of frontier blocks off East Kalimantan, where lease-and-operate FPSOs offer the most feasible evacuation route. Meanwhile, Korea and Japan strengthen regional competitiveness by supplying high-end topside modules, dynamic positioning thrusters, and cryogenic equipment to neighboring markets.

Europe’s share is stable but relatively low-growth, limited by the maturity of the North Sea. Nevertheless, the United Kingdom’s electrified West of Shetland tie-backs and Norway’s power-from-shore initiatives sustain a niche cluster of high-specification floaters equipped for low-carbon operations. Further south, Mediterranean deepwater acreage off Cyprus and Israel is at pre-FID stage and could lift orders later in the decade. Russia’s Arctic FPSO ambitions pause under geopolitical constraints, redirecting European engineering capacity toward African mega-projects and Brazilian pre-salt campaigns. Overall, geographic diversification cushions the floating production systems market from cyclical swings in any single basin.

Regulatory Landscape

Floating production systems operate under overlapping offshore safety and marine regimes, and recent guidance is tightening how regulators handle long-life floaters and novel deepwater designs. In the United States, the Bureau of Safety and Environmental Enforcement (BSEE) issued NTL No. 2024-G03 (August 2024) detailing how operators should submit and justify life extension (LEx) requests for floating platforms under 30 CFR 250.900, creating a clearer compliance pathway for aging floaters that need renewed integrity assurance. BSEE also finalized updates in August 2024 to deepwater and new or unusual technology submission requirements, reinforcing expectations for pre-installation review as projects incorporate higher pressure systems and complex subsea architectures connected to floaters.

Across other key basins, project-specific environmental and safety approvals remain key gating items. In the United Kingdom, the Petrojarl Rosebank FPSO entered the public notice process in April 2026 and received a Secretary of State decision notice in May 2026, underscoring the continued role of formal environmental assessment steps in schedule certainty for large FPSO redevelopments. In Australia, the Offshore Petroleum and Greenhouse Gas Storage (Safety) Regulations 2024 (active version referenced in March 2026) sit alongside NOPSEMA guidance and maritime administration requirements, which together require operators to manage facility safety cases and environmental plans while also meeting vessel-side obligations under frameworks such as MARPOL for pollution prevention when units are operating as production facilities and when they are in transit or under flag-state control.

Competitive Landscape

Industry concentration is moderate and edging higher as shipyard and EPC consolidations proceed. The merger of Keppel Offshore & Marine with Sembcorp Marine folds complementary yard facilities and could realize procurement synergies on an SGD 18 billion order book. SBM Offshore tops the contractor leaderboard with USD 33.7 billion backlog anchored by charter contracts that span more than two decades, demonstrating the appeal of annuity-like cash flows. MODEC, BW Offshore, and Bumi Armada round out the established leasing tier, each emphasizing hull standardization and digital twins to differentiate on uptime.

Technology is the new competitive frontier. Equinor’s Step-Change digital platform integrates data lakes from Johan Sverdrup, enabling AI-driven flow assurance and achieving 75% recovery factors, which raise the bar for future awards. TechnipFMC’s iEPCI™ model, recently selected for Johan Sverdrup Phase 3, bundles subsea kit with life-of-field services, allowing clients to compress interface risk and schedule. OEMs like SLB and Baker Hughes vie to supply electrified wellheads and carbon-capture skids, forming alliances with hull contractors to embed their equipment in design templates that can be built multiple times.

Supply-chain tightness, especially in key forgings, mooring chains, and high-pressure risers, increases the value of early-stage framing agreements. Operators with multi-asset portfolios, notably Petrobras and Shell, secure yard slots years in advance, relegating late entrants to second-wave hulls or pushing them toward marginal-field charters. As a result, the floating production systems market favors integrated players who can combine fabrication, leasing, operations, and decarbonization credentials in a single proposal.

Floating Production Systems (FPS) Industry Leaders

TechnipFMC PLC

Keppel Offshore & Marine Ltd

MODEC Inc.

BW Offshore Ltd

SBM Offshore N.V.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

The most visible whitespace in the floating production systems market is concentrated around standardized, repeatable FPSO delivery models and high-spec deepwater systems that shorten cycle time while still meeting tighter emissions and operability requirements. In Brazil, Petrobras continues to anchor multi-unit demand and template-based execution, with SBM Offshore signing contracts in May 2026 for two Sergipe-Alagoas basin FPSOs (SEAP-I and SEAP-II) using Fast4Ward hull concepts, each designed for 120,000 bpd. This supports a lane for contractors to lock in hull standardization, serial engineering, and long-lead procurement for mooring, topsides modules, and risers, especially as shipyard slots face competition from LNG and large commercial shipbuilding programs.

Opportunity is also widening in frontier and re-emerging provinces where deepwater developments lean on integrated EPCI and subsea-to-floater packages to manage interfaces and accelerate readiness. Saipem’s July 2026 award for FPSO EPCI for Eni’s Kutei North Hub development in Indonesia indicates renewed contracting momentum in Asia-Pacific beyond the traditional Brazil and Guyana-Suriname axis, while TechnipFMC’s Baleine Phase 3 scope offshore Cote d’Ivoire (July 2026) reinforces West Africa as an active demand center for new floating production units and associated flexible flowlines and risers. Delivery lead-time pressure, with newbuild FPSOs commonly cited at 5 to 6 years and major conversions at 3 to 4 years, increases the value of early FEED placement and pre-FID capability decisions, favoring suppliers that can offer remote-operations-ready designs, modularized topsides, and repeatable commissioning approaches that reduce offshore personnel exposure and shorten quayside integration windows.

Recent Industry Developments

- July 2026: TechnipFMC won a contract from Eni for Baleine Phase 3 offshore Cote d’Ivoire, covering the design and manufacture of flexible flowlines and risers associated with a new floating production unit. The award reinforces West Africa as an active theater for floating production reinvestment and strengthens TechnipFMC’s subsea-to-floater execution footprint where schedule and interface management are central.

- May 2026: SBM Offshore signed contracts with Petrobras for two FPSOs (SEAP-I and SEAP-II) for Brazil’s Sergipe-Alagoas basin, with each unit designed for 120,000 barrels of oil per day production capacity. The deal expands Fast4Ward-based standardization in Brazil and improves demand visibility for hulls, topsides modules, and mooring and riser supply chains tied to multi-unit campaigns.

- July 2024: TechnipFMC secured a large iEPCI award for Equinor’s Johan Sverdrup Phase 3 offshore Norway. The contract highlighted the shift toward integrated engineering, procurement, construction, and installation models that bundle subsea hardware with life-of-field services to reduce interface risk on complex offshore developments.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the floating production systems market is defined as revenue generated from offshore floating units that process hydrocarbons at sea and support production in shallow, deepwater, and ultra-deepwater fields.

Scope exclusions: We do not count fixed platforms, subsea-only production systems, or onshore processing infrastructure under this market.

Segmentation Overview

- By Type

- FPSO

- Tension Leg Platform

- SPAR

- Semi-submersible

- Barge

- By Water Depth

- Shallow Water (Below 400 m)

- Deepwater (400 to 1,500 m)

- Ultra-deepwater (Above 1,500 m)

- By Build Method

- Newbuild

- Conversion

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- Norway

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Thailand

- Vietnam

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Trinidad and Tobago

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- Qatar

- Egypt

- Nigeria

- Angola

- Namibia

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research began by mapping the offshore development environment to the types of floating production systems being deployed, and then tying that activity to revenue that can be supported with public evidence. We relied on non-paywalled sources such as the US Energy Information Administration (EIA), the International Energy Agency (IEA), the US Bureau of Ocean Energy Management (BOEM), OPEC publications, and official offshore regulator releases that cover licensing, development plans, and safety or operational reporting.

To translate those signals into a workable model, we also reviewed company annual reports and filings, investor presentations, tender notices, and reputable industry press to understand award timing, conversion versus newbuild patterns, and where execution risk is rising. Select paid database access was used only for company financials and intelligence, and for patent databases when checking technology direction around hull concepts and topside integration. These examples are not exhaustive, and other public references were also used to collect, validate, and clarify the final assumptions.

Primary Interviews and Surveys

Primary work focused on validating what is actually being ordered, converted, installed, and operated, since project pipelines can look different from what ends up executed. We spoke with a mix of offshore project stakeholders, including developers, engineering and commissioning teams, and commercial roles, across APAC, EMEA, and the Americas. The respondent input was used to confirm timing slippage, typical contracting structures, and how spend shifts between newbuild and conversion cycles.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 21% | APAC: 48% |

| Mid tier: 46% | Functional/Unit leaders: 23% | EMEA: 29% |

| Smaller Players: 21% | Managers: 56% | Americas: 23% |

Market-Sizing & Forecasting

The core model is built using a top-down approach where offshore project activity and expected deployment by water depth are reconstructed by region and then translated into revenue pools for floating production systems. To keep the totals realistic, we corroborate them with selective bottom-up approximations, such as sampled project value ranges, yard and integration capacity checks, and simple ASP x volume sanity checks by unit type.

Inputs used in the sizing include the offshore field development pipeline, the split between newbuild and conversion activity, expected delivery timelines from award to commissioning, and the mix shift between shallow water and deepwater projects. We also track oil price expectations and offshore capex guidance as supporting indicators, because they influence sanctioning and re-timing decisions, and those changes show up quickly in FPS demand. For forecasting, scenario analysis is applied so the base case reflects what experts expect for award pace and execution, while alternate cases capture schedule risk and faster redevelopment cycles. Where activity data is incomplete for a country or basin, gaps are handled through ratio-based allocation using verified project counts, and then rechecked through follow-up calls.

Data Validation & Update Cycle

Validation is done by comparing model outputs against independent market signals, including offshore capex trends, observed project awards, and regional deployment momentum by water depth. When a region shows an unusual jump, variance checks are run and the drivers are reviewed again, followed by a second analyst review before sign-off.

Reports are refreshed annually, and interim updates are triggered when material events occur, such as large award announcements, major project delays, or policy changes impacting offshore development. Before delivery, a fresh pass is completed on key assumptions like conversion intensity and delivery timing so clients receive the most current view.

Mordor Intelligence's Global Floating Production Systems Market Market Sizing Compared With Other Published Estimates

Published market sizes for floating production systems often differ because the scope boundaries are not the same, and because the timing assumptions for offshore projects can swing the reported value from one year to the next. Differences also come from whether the numbers represent platform and integration revenue only, or if longer operating periods and adjacent service revenue are blended into the same total.

Key gap drivers in this market usually come down to which unit types are counted, how conversions are treated versus newbuild programs, and whether values are attributed to award year, delivery year, or multi-year revenue recognition. Currency conversion timing and refresh cadence can widen the gap further, since repricing and re-phasing is common for large offshore developments.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 73.21 B (2026) | |

| Industry Publisher A | USD 33.70 B (2024) | Uses a different base year and a broader floating production framing that can combine development, deployment, and operating revenue, which makes its total less comparable to a platform and system revenue view. |

| Industry Publisher B | USD 7.12 B (2024) | The published number appears to reflect a narrower counted revenue pool or a partial system definition, and limited scope notes can lead to undercounting when conversions and multiple floating system types are not fully captured. |

The table points to a spread that is largely explained by base-year selection and what revenue streams are included, and under Mordor Intelligence's scope the market value is tied to defined floating production system types across water depths, with conversion and newbuild activity treated separately so totals stay aligned with executed project cycles. With those scope rules made explicit, the final number is easier to trace back to clear drivers and to repeat when assumptions are updated.

Key Questions Answered in the Report

What is the current value of the floating production systems market?

The floating production systems market size was USD 73.21 billion in 2026 and is projected to reach USD 117.35 billion by 2031.

Which segment holds the largest floating production systems market share?

FPSO units held the leading 54.10% floating production systems market share in 2025.

What CAGR is expected for ultra-deepwater floating production systems between 2026-2031?

Ultra-deepwater deployments are projected to expand at a 10.62% CAGR through 2031.

Which region is growing fastest in the floating production systems market?

Asia-Pacific is forecast to grow at an 11.18% CAGR through 2031 due to energy-security policies and sizable offshore discoveries.

Why are conversions still popular in the floating production systems industry?

Conversions offer shorter lead times and lower capital intensity, ensuring a 62.15% share of 2025 deployments despite the rise of technology-rich newbuilds.

Page last updated on: