Exocrine Pancreatic Insufficiency (EPI) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

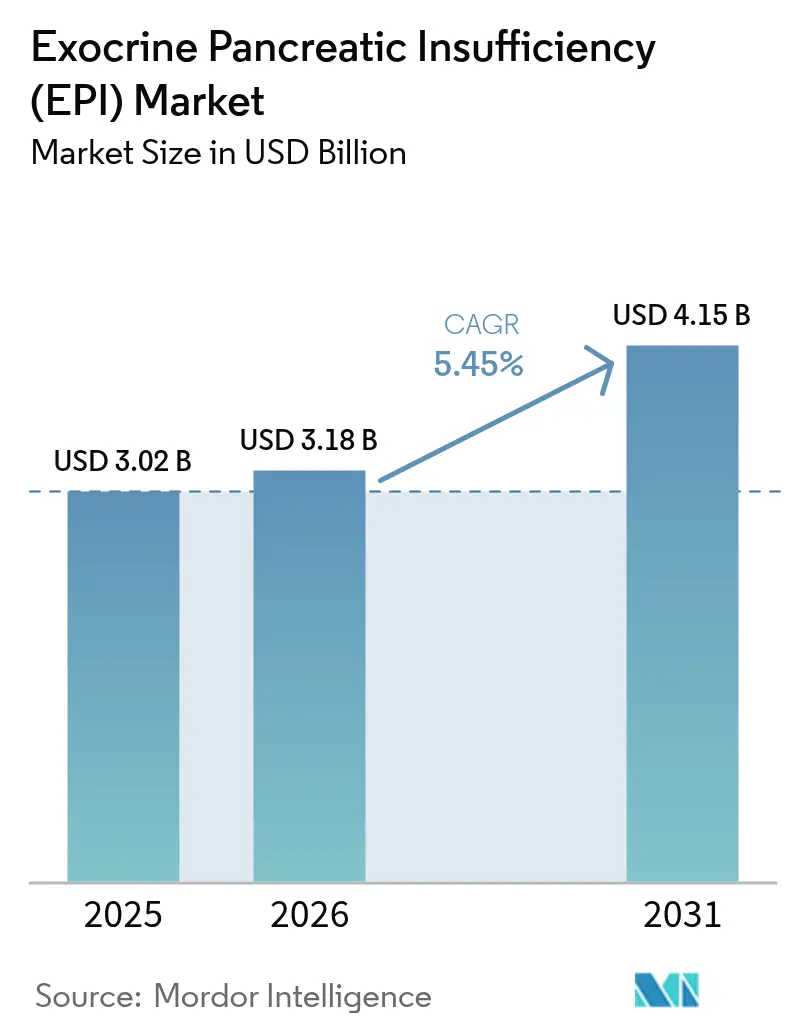

| Market Size (2026) | USD 3.18 Billion |

| Market Size (2031) | USD 4.15 Billion |

| Growth Rate (2026 - 2031) | 5.45% CAGR |

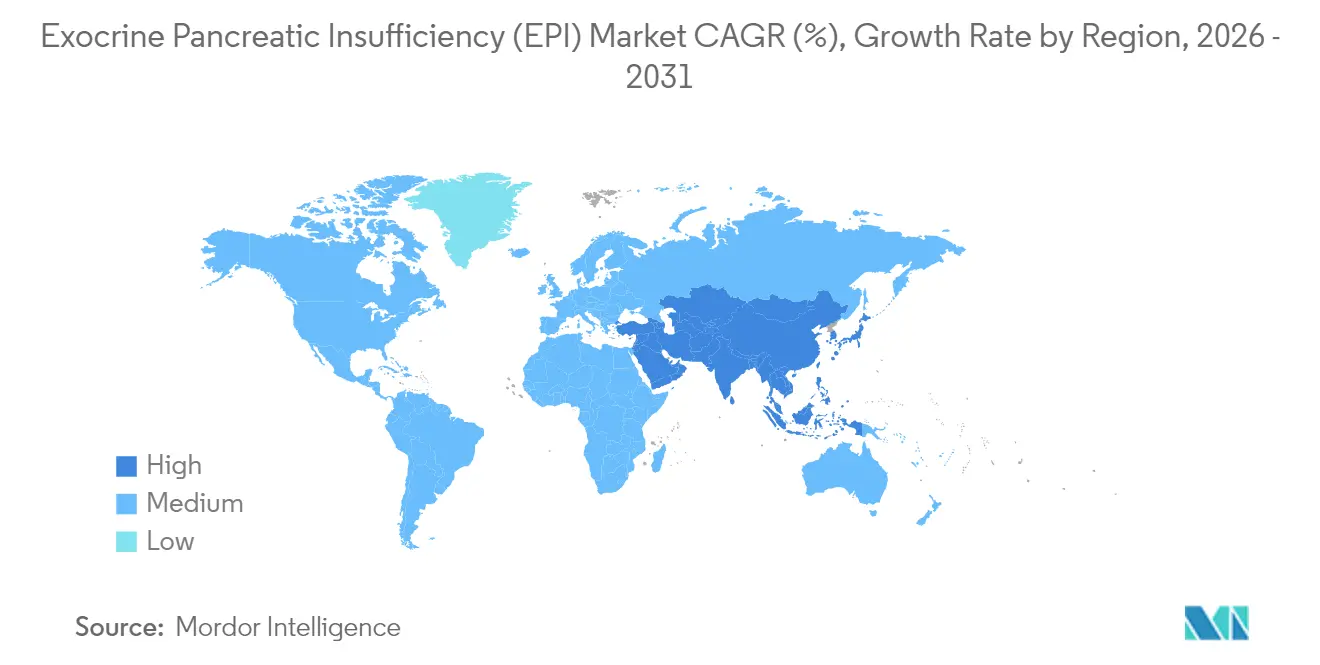

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Exocrine Pancreatic Insufficiency (EPI) Market Analysis by Mordor Intelligence

The Exocrine Pancreatic Insufficiency Market size was valued at USD 3.02 billion in 2025 and estimated to grow from USD 3.18 billion in 2026 to reach USD 4.15 billion by 2031, at a CAGR of 5.45% during the forecast period (2026-2031).

The expansion trajectory is underpinned by three macro forces: a persistent rise in pancreatic cancer prevalence, extended survival of cystic-fibrosis patients who now require lifelong therapy, and a looming patent cliff that opens the competitive landscape to cost-effective generics. Heightened diagnostic vigilance is exposing a sizable under-recognized patient pool, while porcine pancreatin supply constraints periodically tighten product availability. Market opportunities are intensifying around synthetic recombinant enzymes, digital adherence tools, and early-stage guideline interventions that mandate prompt initiation of pancreatic enzyme replacement therapy (PERT).

Key Report Takeaways

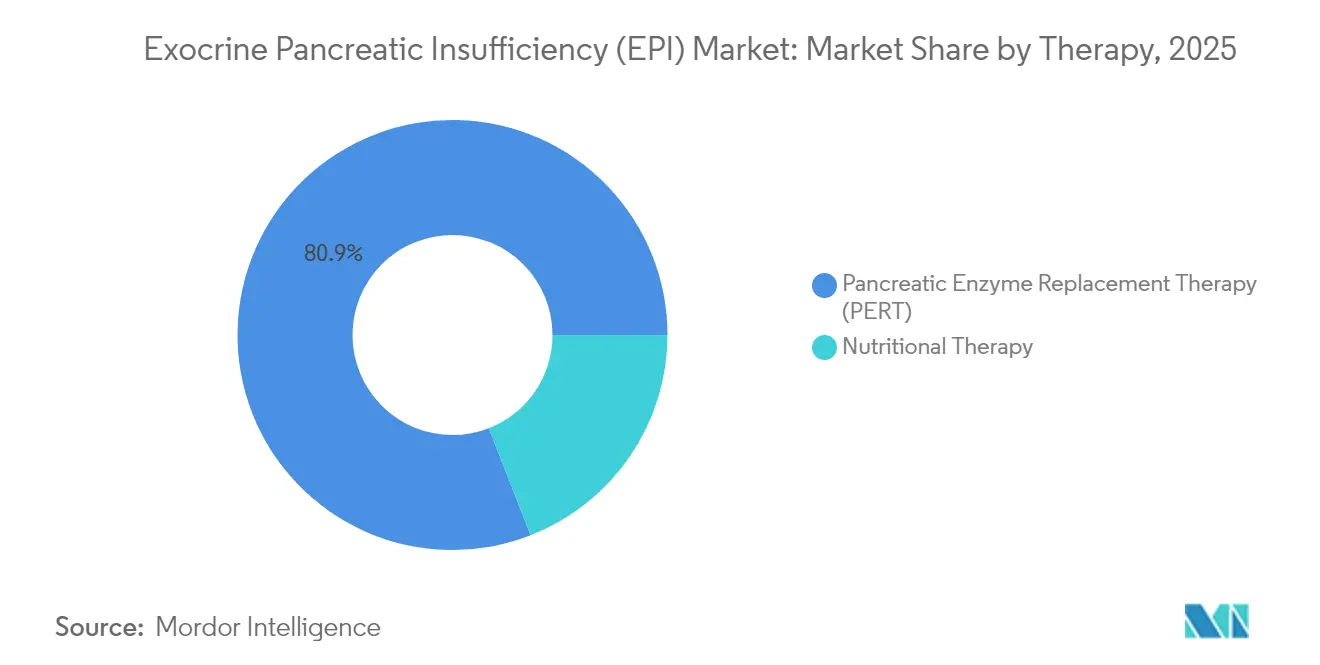

- - By therapy, pancreatic enzyme replacement commanded 80.92% revenue share in 2025; microbial and recombinant alternatives are advancing at an 8.55% CAGR through 2031.

- - By disease etiology, chronic pancreatitis accounted for 34.55% of the exocrine pancreatic insufficiency market size in 2025; pancreatic cancer applications are accelerating at an 7.79% CAGR through 2031.

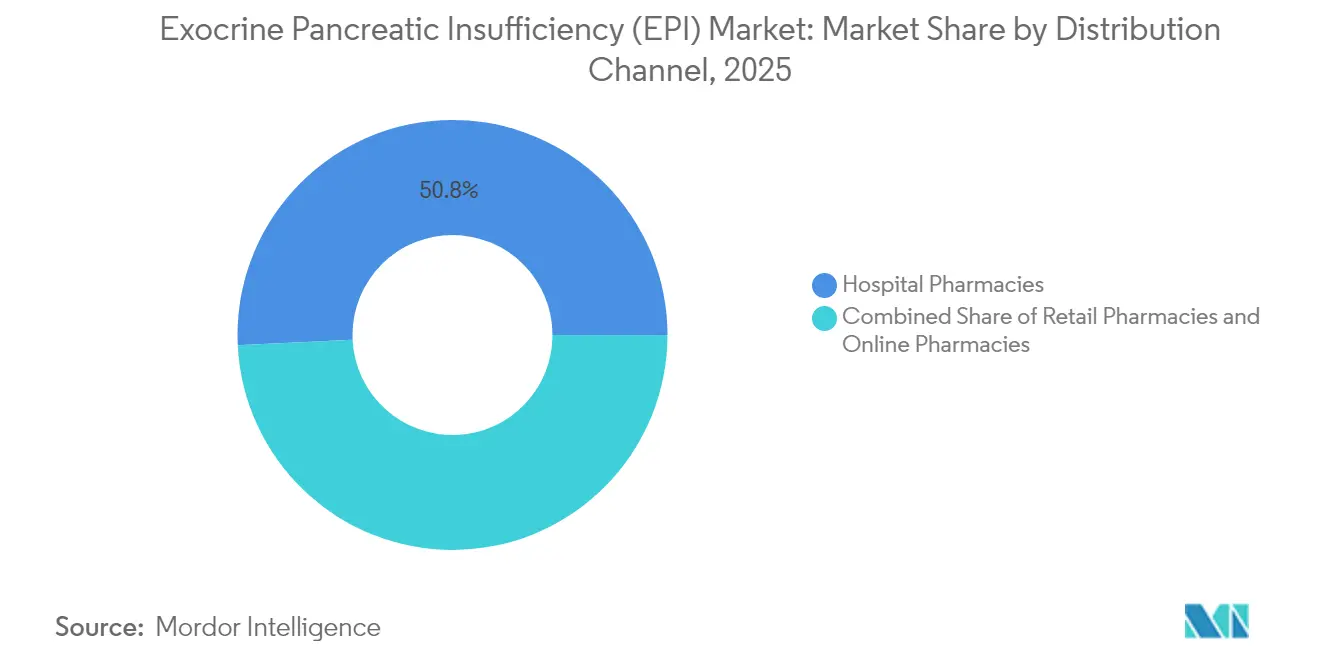

- - By distribution channel, hospital pharmacies held 50.76% of the exocrine pancreatic insufficiency market share in 2025, whereas online pharmacies are growing at a 10.41% CAGR through 2031.

- - By geography, North America captured 41.22% market share in 2025, while Asia-Pacific shows the fastest growth at a 6.29% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Exocrine Pancreatic Insufficiency (EPI) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence of EPI Linked to Chronic Pancreatitis & Pancreatic Cancer | +1.2% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Increasing Cystic-Fibrosis Survival Rates Expanding Lifetime Patient Pool | +0.8% | North America & EU, expanding to APAC | Long term (≥ 4 years) |

| Patent Expiries Spurring Affordable Generics | +0.9% | Global, with early impact in North America | Short term (≤ 2 years) |

| Supply-Chain Innovation in Microbial/Recombinant Enzymes | +0.7% | North America & EU core, spill-over to APAC | Medium term (2-4 years) |

| Digital Dosing Apps Improving Adherence & Outcomes | +0.4% | Global, with early adoption in developed markets | Medium term (2-4 years) |

| Strategic Guideline Updates Mandating Early PERT Initiation | +0.6% | Europe & North America, gradual APAC adoption | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of EPI Linked to Chronic Pancreatitis & Pancreatic Cancer

Chronic pancreatitis and pancreatic cancer together shape the largest at-risk cohort for enzyme replacement therapy. Longitudinal data show that 80-90% of chronic pancreatitis cases progress to exocrine pancreatic insufficiency, and up to 80% of pancreatic cancer patients ultimately manifest digestive insufficiency symptoms.[1]Luca Lambertini et al., “Pancreatic Cancer Epidemiology,” MDPI, mdpi.com Despite the high incidence, real-world studies indicate that only 21% of symptomatic cancer patients receive guideline-recommended PERT, highlighting a sizable treatment gap. The disconnect is gradually closing as oncology guidelines emphasize early enzyme therapy alongside chemotherapeutic regimens. Heightened public health campaigns and improved imaging modalities are unveiling latent cases, transforming what was once acute palliation into a chronic supportive-care model that extends throughout a patient’s survival journey. Consequently, demand patterns are shifting toward high-volume, long-duration prescriptions that favor sustained revenue visibility for manufacturers.

Increasing Cystic-Fibrosis Survival Rates Expanding Lifetime Patient Pool

Decades ago, cystic fibrosis was primarily a pediatric fatality; today, median survival in developed markets exceeds 45 years, courtesy of CFTR modulator therapies.[2]Hannah Shields et al., “Adult Cystic Fibrosis Health Outcomes,” BMJ Open, bmj.com Up to 85% of cystic-fibrosis patients exhibit pancreatic insufficiency at infancy and therefore initiate PERT soon after diagnosis. As these patients transition into adulthood and elderly age bands, lifetime prescription volumes multiply, embedding predictable, annuity-like demand for enzyme suppliers. Adult-centered care further magnifies product differentiation around pill burden, flavor masking, and digital dosing calculators that simplify adherence across diverse meal patterns. The sustained nature of therapy also strengthens the value proposition for long-acting recombinant options that reduce daily capsule counts, thereby improving quality of life and indirectly supporting nutritional status.

Patent Expiries Spurring Affordable Generics

Key intellectual-property protections surrounding leading porcine pancreatin brands begin to unwind in February 2028, notably for Zenpep. Once exclusivities lapse, abbreviated new-drug application pathways and the shift from NDA to BLA filing criteria unlock competitive entry, placing downward pressure on prices, especially in the United States where private insurers aggressively favor generics. Lower unit costs are expected to improve therapy accessibility in both mature and emerging regions, broadening the addressable patient pool. Brand incumbents are countering price erosion by investing in differentiated delivery formats, pediatric-friendly micro-granules, and value-added adherence apps, while simultaneously extending their geographic footprints into under-penetrated Asia-Pacific markets.

Supply-Chain Innovation in Microbial/Recombinant Enzymes

Recurring shortages of porcine pancreatin have elevated supply security from an operational consideration to a strategic imperative. Biotech innovators such as Entero Therapeutics are progressing adrulipase, a recombinant lipase produced in expression systems that bypass livestock sourcing constraints.[3]Entero Therapeutics, “Adrulipase Phase IIb Results,” enterotherapeutics.com Recombinant platforms promise tighter batch-to-batch consistency, improved viral-safety profiles, and scalability that can flex with demand surges a critical attribute given periodic livestock-related disruptions. Equally relevant are dietary or religious restrictions that limit porcine product acceptance in specific countries; recombinant enzymes nullify those barriers, expanding global addressable volumes. As validation data mature, payers may reward synthetic formats for their lower supply-risk premiums and potentially enhanced bioavailability.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intermittent Shortages of Porcine Pancreatin Supply | -1.1% | Global, acute impact in Europe & UK | Short term (≤ 2 years) |

| Low Clinician Confidence; Sub-Therapeutic PERT Dosing | -0.8% | Global, particularly in emerging markets | Medium term (2-4 years) |

| Regional Reimbursement Gaps for Long-Term PERT | -0.6% | Emerging markets, selective developed regions | Long term (≥ 4 years) |

| Stringent cGMP & Viral Safety Requirements Inflating COGS | -0.4% | Global manufacturing, regulatory compliance | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Intermittent Shortages of Porcine Pancreatin Supply

In 2024-2025, 96% of U.K. community pharmacies reported difficulty sourcing Creon, a shortage expected to linger through 2026. Root causes include a limited number of qualified slaughterhouses, batch-release testing delays, and pandemic-driven transportation bottlenecks. As inventory gaps widened, national regulators invoked Serious Shortage Protocols permitting pharmacists to make dose-for-dose substitutions, yet many patients rationed capsules or altered diets, risking malnutrition. The scarcity underscores the fragility of a supply chain reliant on a single animal source and catalyzes stakeholder interest in recombinant or microbial substitutes that circumvent porcine raw-material constraints.

Low Clinician Confidence; Sub-Therapeutic PERT Dosing

A cross-sectional survey showed that 40% of prescriptions contain enzyme units below guideline-recommended 40,000–50,000 lipase units per meal, while 72% of patients perceive their dosing as inadequate. Sub-optimal dosing often stems from limited gastroenterology access, variability in meal fat content, and physician concerns about pill burden. The under-dosing phenomenon exacerbates malabsorption-related complications, inflates healthcare costs through preventable hospitalizations, and suppresses potential market volume. Digital dose calculators integrated into mobile health applications are emerging as pragmatic countermeasures, yet broad implementation requires clinician buy-in and payer support.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Therapy: PERT Dominance Faces Synthetic Disruption

The exocrine pancreatic insufficiency market size for pancreatic enzyme replacement therapy held an 80.92% revenue share in 2025. Reliance on porcine-derived pancrelipase remains the norm because the formulation delivers the triad of lipase, amylase, and protease in ratios clinicians trust. Yet recombinant and microbial formulations, though representing under 5% of volume today, are clocking an 8.55% CAGR as they respond to supply insecurities and dietary constraints. The exocrine pancreatic insufficiency market share of synthetic enzymes is forecast to inch past 10.25% by 2031 as late-stage candidates like adrulipase accumulate phase III data.

Manufacturers of conventional PERT are deploying controlled-release micro-granules that withstand gastric acidity, while innovators explore immobilized enzyme cartridges compatible with enteral feeding pumps. Differentiation extends to ancillary services, mobile adherence platforms, tele-nutrition counseling, and patient-assistance programs—that lock in prescriber loyalty even as generic erosion looms. These converging developments suggest a future landscape where porcine and recombinant options coexist, each targeting specific patient segments based on allergy status, cultural preferences, and source-of-origin ethics.

By Disease Etiology: Chronic Pancreatitis Leadership Challenged by Cancer Growth

Chronic pancreatitis generated 34.55% of 2025 revenue thanks to high symptom prevalence and lifelong therapy duration. The segment benefits from well-established clinical referral pathways between gastroenterology and nutrition specialties, ensuring steady prescription renewals. Cystic-fibrosis patients, though numerically smaller, present a long-tail demand curve because enzyme dependency begins in early childhood and persists across decades. Post-surgical and idiopathic etiologies complete the residual market, often characterized by intermittent rather than perpetual dosing.

Pancreatic-cancer-related EPI, once a supportive adjunct to palliative care, now stands on the cusp of a volume inflection. An 7.79% CAGR to 2031 is anchored in double-digit survival gains linked to novel chemotherapy regimens such as Ipsen’s Onivyde approved in February 2024. The therapy extends life expectancy and thus enlarges the cumulative need for enzyme supplementation. Notably, oncology guidelines published in 2025 began advocating proactive enzyme replacement at the time of cancer diagnosis, a practice shift that could materially lift penetration rates in the next 5 years.

By Distribution Channel: Digital Transformation Accelerates Online Growth

Hospital pharmacies preserved a 50.76% sales share in 2025 due to their integral role at treatment initiation and their proximity to specialist consults. Institutional purchasing power grants these pharmacies favorable pricing tiers, which in turn influences formulary placement within integrated delivery networks. Retail chains continue to act as the bridge for chronic refills, especially in suburban geographies where hospital dispensaries are sparse.

However, online pharmacies are emerging as the system’s fastest-growing node, registering a 10.41% CAGR through 2031. The pandemic normalized doorstep delivery for chronic therapies, and regulatory allowances for e-prescriptions further removed friction. Digital platforms embed refill reminders, nutrition tracking, and clinician chat functions, minimizing missed doses. Yet product complexity remains a gating factor; portals must deploy pharmacists trained in titration nuances to uphold safety standards. The channel’s rise will likely spur collaborations between manufacturers and telehealth providers, integrating enzyme supply with remote dietitian consults.

Geography Analysis

North America retained a 41.22% revenue share in 2025, reflecting universal insurance coverage for approved PERT brands and a mature prescriber base familiar with high-dose regimens. Creon alone enjoys 93% preferred formulary placement across commercial and Medicare Part D plans. Nevertheless, episodic backorders linked to limited porcine gland supply have triggered payer scrutiny, nudging providers to consider future recombinant alternatives. Competitive dynamics may intensify as FDA guidances framed under the BLA pathway clarify requirements for biosimilar enzymes, accelerating generic filings post-2028.

Europe exhibits high clinical sophistication but is grappling with acutely constrained inventories. The European Medicines Agency expedited approval of Micrazym in June 2024 to diversify product availability. Despite this, 2025 surveys revealed U.K. patients resorting to dose rationing amid prolonged shortages. In response, national health systems are drafting contingency contracts that oblige suppliers to hold multi-month safety stocks, bolstering resilience until recombinant pipelines mature. Parallel developments in digital adherence tools exemplified by the MyCyFAPP app that customizes dosing based on meal photographs are quickly gaining traction among European cystic-fibrosis clinics.

Asia-Pacific is the fastest-growing region, charting a 6.29% CAGR through 2031 on the back of improved diagnostic reach, population aging, and rising chronic-disease burdens. Chinese epidemiological data reveal a disproportionate uptick in pancreatic cancer incidence among adults aged 35–49, a trend that directly feeds enzyme demand. Regulatory overhaul is equally salient: India’s 2024 revision of its National Essential Medicines List now explicitly names pancrelipase, streamlining public-hospital procurement. However, fragmented reimbursement and a reliance on imported brands keep treatment access uneven. Multinational firms are therefore partnering with regional contract manufacturers to establish local fill-and-finish capacity, simultaneously lowering tariffs and strengthening political goodwill.

Competitive Landscape

The exocrine pancreatic insufficiency market hosts a mix of long-established pharmaceutical majors and nimble biotech entrants. AbbVie, Viatris, and Nestlé Health Science collectively control more than half of worldwide revenue through brand equity, multiregional regulatory dossiers, and entrenched gastroenterology sales forces. To defend share ahead of the 2028 patent cliff, these incumbents are expanding manufacturing redundancy AbbVie commissioned an additional pancrelipase line in Puerto Rico in early 2025 and investing in micro-granule technologies that promise reduced capsule loads.

Biotech challengers, exemplified by Entero Therapeutics and Alcresta Therapeutics, pursue differentiation via recombinant enzymes and device-assisted delivery. Entero’s adrulipase completed phase IIb with statistically significant fat-absorption improvements over standard-of-care, setting the stage for a pivotal phase III readout in 2026. Alcresta, meanwhile, markets RELiZORB, an immobilized lipase cartridge cleared as a Class II medical device by the FDA, targeting tube-fed patients with severe malabsorption. Such device-drug hybrids blur traditional competitive lines and may capture niche yet high-value subsegments.

Supply resilience is now a competitive differentiator. Viatris signed a multi-year porcine-gland sourcing agreement with Smithfield Foods, while Nestlé Health Science diversified into microbial enzymes through its minority stake in a Danish synthetic-biology startup. Companies also race to integrate digital ecosystems; AbbVie partnered with MyHealthCoach in 2025 to embed Creon dosing reminders within a nutrition-logging app. Collectively, these moves illustrate a transition from product-centric to solution-centric competition, where clinical outcome optimization and supply assurance weigh as heavily as pill-count economics.

Exocrine Pancreatic Insufficiency (EPI) Industry Leaders

AbbVie Inc.

Nestlé Health Science

Digestive Care Inc.

Alcresta Therapeutics

First Wave BioPharma

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Alcresta Therapeutics Alcresta Therapeutics announced the enrollment of the first patient at Massachusetts General Hospital (MGH) in an investigator-initiated trial evaluating the efficacy of RELiZORB in managing exocrine pancreatic insufficiency (EPI) among tube-fed pancreatitis patients. This clinical milestone reinforces RELiZORB’s potential to address a critical need in nutritional support for patients facing severe pancreatic dysfunction.

- April 2025: Horizon Therapeutics (Uplizna) got FDA approval for Uplizna (inebilizumab-cdon) as the first and only treatment for Immunoglobulin G4-related disease (IgG4-RD) the underlying cause of Type 1 Autoimmune Pancreatitis (AIP). This landmark approval sets a new precedent for rare disease management in the pancreatitis community, paving the way for innovation in immune-targeted therapeutics for pancreatic disorders.

- March 2025: Adalvo is gearing up for a key European launch of Pancreatin Delayed-Release Capsules, expanding its peptide and biosimilar portfolio. As a blockbuster treatment for EPI, this development marks a strategic push to fill therapeutic gaps in enzyme replacement therapy across Europe and broaden access to affordable, high-impact care.

Global Exocrine Pancreatic Insufficiency (EPI) Market Report Scope

As per the scope of this report, exocrine pancreatic insufficiency is defined as an enzyme output less than 10.0% of the necessary level required to sustain normal digestion. Exocrine pancreatic insufficiency is mostly caused by diseases that destroy pancreatic parenchyma, such as chronic pancreatitis and cystic fibrosis, as well as pancreatic resection. The exocrine pancreatic insufficiency (EPI) Market is segmented by Therapies (Pancreatic exocrine replacement therapies (PERT), Nutritional Therapy (Dietary supplements)), By Distribution Channels (Hospital Pharmacies, Retail Pharmacies, and others), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the value (in USD million) for the above segments.

| Pancreatic Enzyme Replacement Therapy (PERT) | Porcine-derived formulations |

| Microbial/Recombinant formulations | |

| Nutritional Therapy | Macronutrient-specific supplements |

| Pro- & Synbiotics |

| Cystic Fibrosis |

| Chronic Pancreatitis |

| Pancreatic Cancer |

| Post-surgical & Other Causes |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Therapy | Pancreatic Enzyme Replacement Therapy (PERT) | Porcine-derived formulations |

| Microbial/Recombinant formulations | ||

| Nutritional Therapy | Macronutrient-specific supplements | |

| Pro- & Synbiotics | ||

| By Disease Etiology | Cystic Fibrosis | |

| Chronic Pancreatitis | ||

| Pancreatic Cancer | ||

| Post-surgical & Other Causes | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected exocrine pancreatic insufficiency market size by 2031?

The exocrine pancreatic insufficiency market size is forecast to reach USD 4.15 billion by 2031, reflecting a 5.45% CAGR over 2026-2031.

Which therapy type currently dominates sales?

Pancreatic enzyme replacement therapy held 80.92% of 2025 revenue due to strong clinical adoption and broad regulatory approvals.

Why are recombinant enzymes gaining attention?

Recombinant enzymes bypass porcine supply constraints, offer consistent purity, and align with dietary restrictions, leading to an 8.55% CAGR through 2031 for synthetic formulations.

Which region is expected to grow the fastest?

Asia-Pacific shows the strongest trajectory, expanding at a 6.29% CAGR to 2031 as diagnostics and healthcare access improve.

How will upcoming patent expiries affect the market?

The 2028 patent cliff will lower entry barriers for generics, expand patient access through reduced prices, and intensify competition, particularly in North America.

What factors contribute most to supply shortages?

Dependence on limited porcine-gland sourcing, quality-control bottlenecks, and transportation disruptions lead to intermittent product shortages, especially in Europe and the UK.

Page last updated on: