Defibrillator Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 15.65 Billion |

| Market Size (2031) | USD 22.05 Billion |

| Growth Rate (2026 - 2031) | 7.10% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Defibrillator Market Analysis by Mordor Intelligence

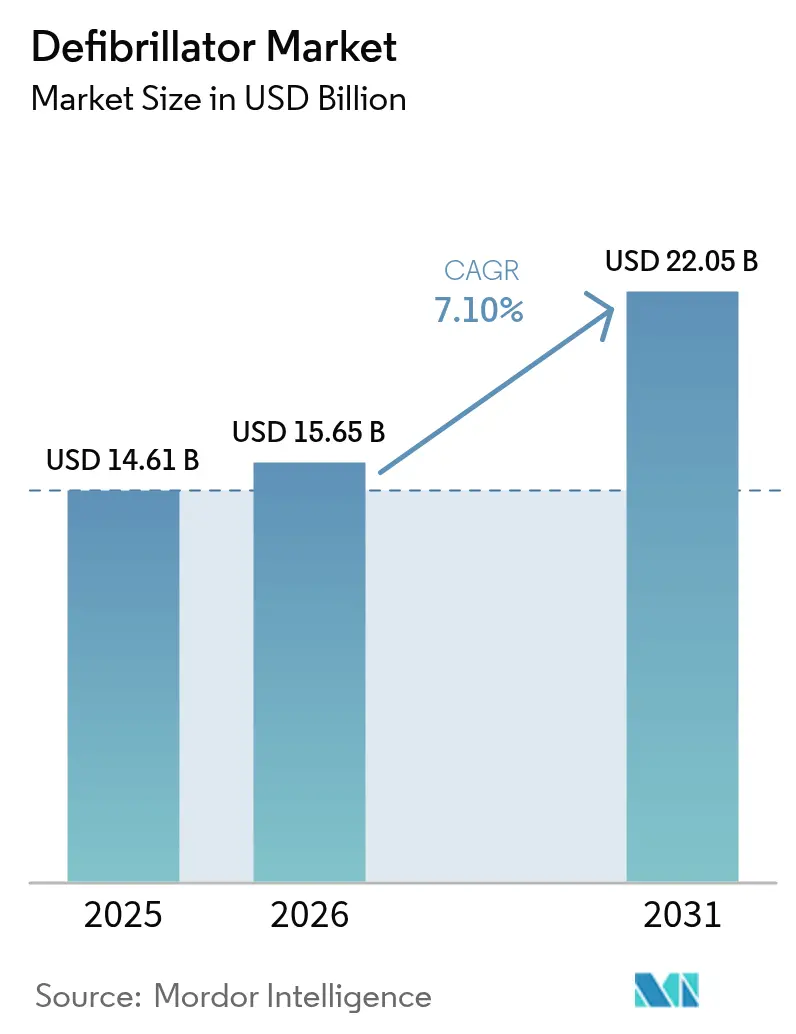

The Defibrillator Market size was valued at USD 14.61 billion in 2025 and is estimated to grow from USD 15.65 billion in 2026 to reach USD 22.05 billion by 2031, at a CAGR of 7.10% during the forecast period (2026-2031).

Sustained incidence of sudden cardiac arrest, rapid adoption of AI-enabled devices, and wider public-access programs keep demand resilient despite supply-chain headwinds. Device makers are lengthening battery life, embedding cloud connectivity, and leaning on predictive analytics to differentiate. Payers and regulators in high-income countries increasingly reimburse cloud monitoring, while emerging markets boost baseline healthcare outlays to narrow treatment gaps. Competitive intensity rises as innovators secure FDA clearances for extravascular implantation and patch-based wearables, signaling a new product cycle poised to accelerate the defibrillator market over the next five years.

Key Report Takeaways

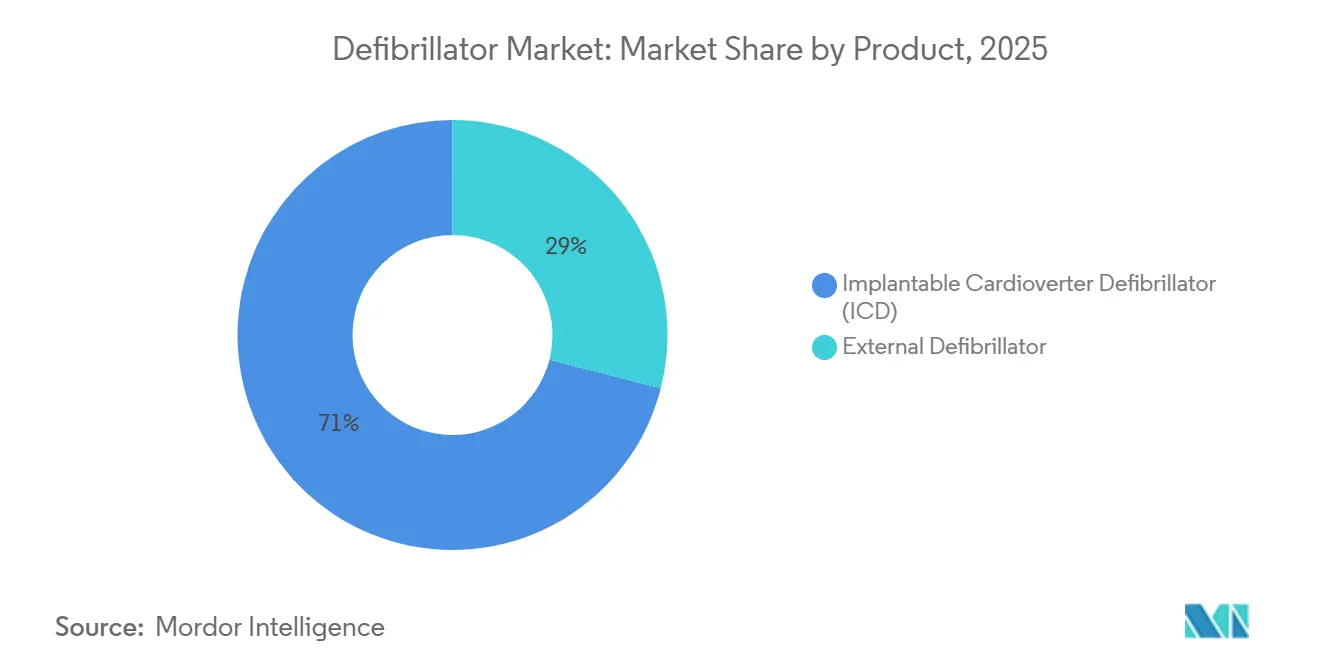

- By product category, implantable cardioverter defibrillators held 71.02% of defibrillator market share in 2025, while external defibrillators are projected to expand at a 7.64% CAGR to 2031.

- By end user, hospitals and cardiac centers accounted for 77.60% of the defibrillator market in 2025; home-care settings are projected to record the highest CAGR at 7.98% through 2031.

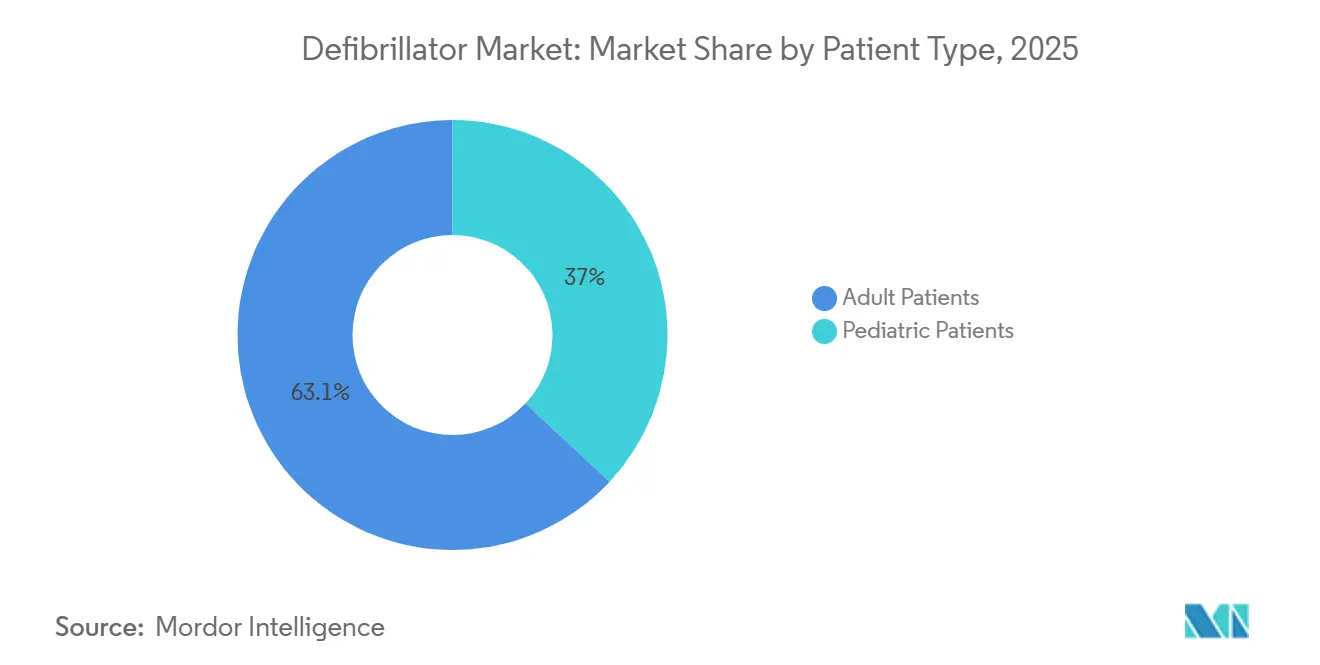

- By patient type, adult patients captured 63.05% share of the defibrillator market size in 2025, whereas pediatric applications are advancing at a 7.78% CAGR over the same horizon.

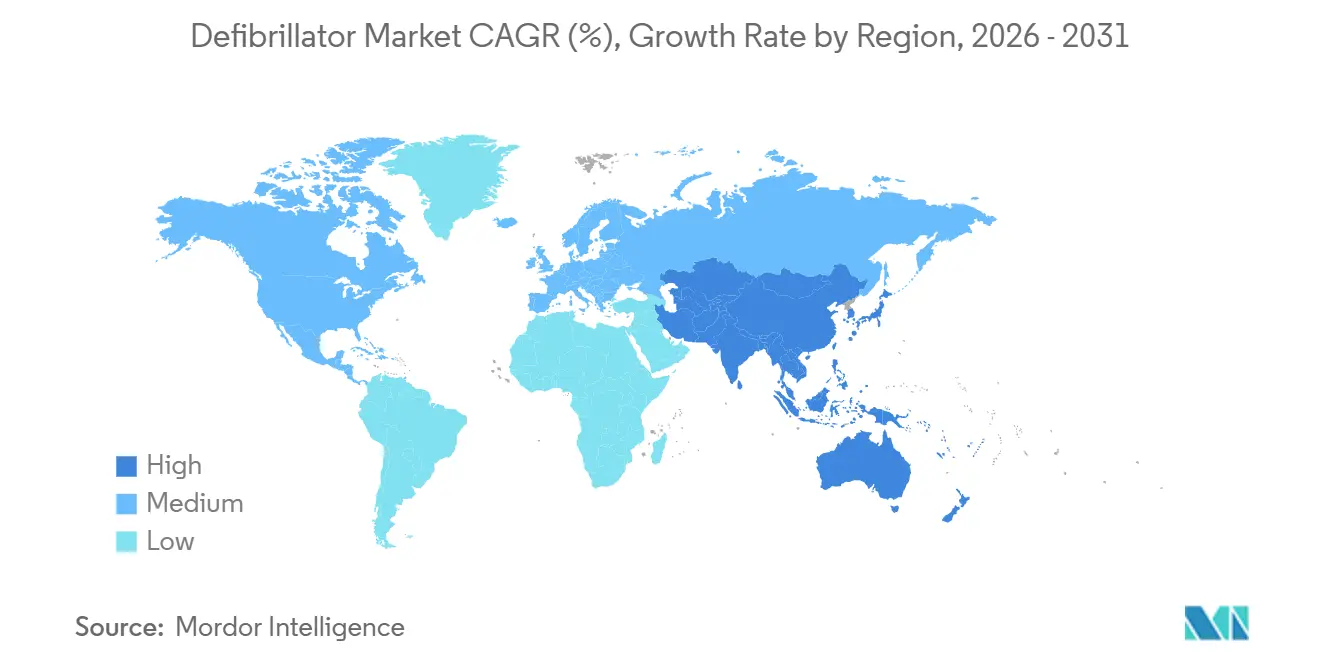

- By geography, North America commanded 43.85% of the defibrillator market share in 2025; Asia-Pacific is forecast to grow fastest at an 8.21% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Defibrillator Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising prevalence of cardiovascular diseases | +1.8% | Global, highest absolute growth in APAC & MEA | Long term (≥ 4 years) |

| Technological advancements in ICDs and AEDs | +1.5% | North America & EU lead, APAC lags 18-24 months | Medium term (2-4 years) |

| Expansion of public-access defibrillation programs | +1.2% | Strongest in EU, variable in North America | Medium term (2-4 years) |

| Aging workforce training & simulation demand | +0.6% | North America & EU | Short term (≤ 2 years) |

| Subscription-based cloud-connected models | +0.7% | North America early, EU pilots, limited APAC | Medium term (2-4 years) |

| Drone-delivered AED networks | +0.4% | Nordics operational, U.S. pilots, APAC exploratory | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Cardiovascular Diseases

Cardiovascular disease (CVD) continues to be the top cause of mortality in the U.S., leading to over 940,000 deaths annually. By 2050, projections suggest that more than 60% of American adults may grapple with some form of CVD, a rise from the current 50%.[1]American Heart Association, “2026 Heart and Stroke Statistics,” heart.org In 2025, updated appropriate-use criteria expanded the candidacy for ICDs to include patients with non-ischemic cardiomyopathy and left-ventricular ejection fractions ranging from 35% to 40%. In alignment with these guidelines, Medicare introduced new reimbursement codes in 2025, potentially benefiting an additional 180,000 eligible beneficiaries. These combined clinical and reimbursement shifts are broadening the market for both implantable and external devices, bolstering the Defibrillator market. Meanwhile, India and China, grappling with rapid urbanization and dietary changes, are witnessing a swift rise in CVD prevalence, with hypertension rates surpassing 30% in major urban centers.

Technological Advancements in ICDs and AEDs

FDA approval of Medtronic’s Aurora EV-ICD in 2023 shifted the defibrillator market toward extravascular implantation, which avoids venous complications while delivering antitachycardia pacing, achieving 98.7% effectiveness.[2]Medtronic plc, “Medtronic Receives FDA Approval for Extravascular Defibrillator,” medtronic.com Battery longevity extends about 60%, improving lifetime economics for providers and patients. AI algorithms now curtail false alarms; Element Science’s Jewel Patch wearable won clearance in 2025 after demonstrating high compliance and low inappropriate-shock rates. Modular architectures are gaining traction, with Boston Scientific reporting 97.5% complication-free performance for its leadless pacemaker/defibrillator combination. Collectively, these innovations reinforce premium pricing and stimulate replacement demand, supporting mid-single-digit unit growth across the defibrillator market.

Expansion of Public-Access Defibrillation Programs

Jurisdictions mandate broader automated external defibrillator (AED) deployment, propelling the defibrillator market into non-clinical venues. All 50 U.S. states had supporting statutes by 2017, and new rules continue: Washington now obliges fitness centers to host on-site AEDs, while South Australia enforces similar requirements for public buildings by 2026. King County registers more than 5,000 devices linked to 911, bolstering survival odds when placement and dispatcher guidance converge. Yet bystander AED use appears in only 4% of out-of-hospital arrests, leaving a sizable adoption runway. Evidence from San Diego’s Project Heart Beat shows that municipal programs can raise access to levels mirroring the ubiquity of fire extinguishers, corroborating policy momentum.

Aging Workforce Training & Simulation Demand

As of 2024, the median age of American workers has risen to 44, a five-year increase since 2015.[3]U.S. FAA, “Draft Airworthiness Standards for Medical Payload Drones,” faa.gov In response, OSHA has begun recommending annual CPR refreshers. Moving away from traditional classroom drills, digital simulations are taking the lead. For instance, Laerdal’s QCPR Instructor app transmits compression metrics to cloud dashboards. This innovation has led to a 35% reduction in training costs per learner and an 18% increase in skill retention over six months, as highlighted in a 2025 peer-reviewed study. Furthermore, corporate buyers are increasingly opting for subscription-based e-learning packages. These packages not only align with workforce safety audits but also enhance institutional readiness and boost sales of external units.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Stringent multi-region regulatory frameworks | −1.1% | Global, longest delays in EU & U.S. | Medium term (2-4 years) |

| High total cost of ICD implantation & follow-ups | −0.9% | APAC, MEA, Latin America | Long term (≥ 4 years) |

| Cyber-security risks for connected devices | −0.5% | North America & EU | Short term (≤ 2 years) |

| Lithium-supply pressure on batteries | −0.6% | Global, Asia-Pacific hubs most exposed | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Multi-Region Regulatory Frameworks

The EU Medical Device Regulation (MDR 2017/745) obliges recertification of legacy products, with half of manufacturers planning portfolio cuts and roughly one-third of devices slated for exit owing to cost and timeline burdens. ZOLL’s sequential MDR approvals for its AED line illustrate the added year or more now needed for market entry. Across the Atlantic the U.S. Food and Drug Administration requires software bills of materials and vulnerability reporting for “cyber devices,” adding documentation layers that elongate clearance cycles. Divergent rule sets compel dual certification efforts, straining budgets and slowing innovation throughput in the defibrillator market.

High Total Cost of ICD Implantation & Follow-Ups

Economic burden remains pronounced, especially in health systems lacking broad reimbursement. Italian registry data record mean EUR 5,662 hospitalization costs after generator replacement, with 9.6% of patients rehospitalized within a year. The EuroEco study found remote monitoring profitable for German and UK providers but loss-making in Belgium, Spain, and the Netherlands where payment codes lag. In Asia-Pacific, lower per-capita spend and insurance coverage suppress implant volumes despite rising clinical need, muting potential of the defibrillator market until affordability improves.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Implantables Dominate, External Units Accelerate

In 2025, implantable systems dominated the defibrillator market, securing a commanding 71.02% share, particularly for patients with ejection fractions below 35%. While implantable defibrillators are set to grow at a steady 6.8% CAGR, the external segment is on a faster track, projected to expand at 7.64% through 2031. This surge is buoyed by regulatory support, notably the push for placing AEDs in every European workplace within three years. Transvenous ICDs are still divided between single- and dual-chamber models, but subcutaneous and extravascular designs are gaining traction by mitigating lead-related complications.

External defibrillators, while contributing a smaller base, are projected to compound at 7.64% through 2031, reflecting public-access expansion and AI-driven form factors. Wearable cardioverter units such as the FDA-cleared Jewel Patch enhance compliance by suppressing nuisance alarms and enabling barefoot therapy, factors that deepen user adoption. Drone-delivered automated external devices could raise survival by 34% in four-minute response scenarios, underscoring logistical innovation now shaping the defibrillator market. The segment also gains from subscription models that bundle connectivity, maintenance, and analytics, making budgeting predictable for municipalities and enterprises.

By End User: Home Care Gains as Remote Monitoring Matures

Hospitals and cardiac centers accounted for 77.60% of the defibrillator market in 2025, driven by procedural complexity and the concentration of electrophysiology expertise. In-facility use involves manual defibrillators and advanced resynchronization implants, which support intensive replacement cycles and capital budget allocation. Cloud platforms extend monitoring beyond discharge, enabling providers to bill for remote interrogation and trigger a services annuity that lifts spend per patient.

Home-care settings, though smaller, are scaling at a 7.98% CAGR as insurers back telemonitoring and patients seek autonomy. Studies show patients connected to St. Jude Medical’s Merlin network experienced 2.4 times higher survival, validating the value proposition for payers. South Korea’s first remote program reduced clinic visits by nearly 1 per patient annually while maintaining satisfaction above 90%, demonstrating operational feasibility. As AI-enabled wearables proliferate, daily monitoring becomes frictionless, expanding the defibrillator market in domiciliary environments.

By Patient Type: Pediatric Applications Expand with Miniaturized Leads

Adult patients accounted for 63.05% of the defibrillator market in 2025, reflecting the epidemiology of coronary artery disease and heart failure. Adoption patterns remain stable, but upgrades to newer extravascular systems should prompt a replacement wave over the forecast period. Leadless options also mitigate infection risks, adding incremental adult demand.

Pediatric deployments, though modest in number, are projected to grow 7.78% annually as miniaturization and battery advances align with unique anatomical needs. Successful extravascular ICD placement in patients as young as two years eliminates transvenous-lead challenges and positions the defibrillator market for durable pediatric growth. Research into left-bundle pacing and adaptive algorithms promises long-term cardiac support compatible with maturing physiology.

Geography Analysis

North America led the defibrillator market with 43.85% market share in 2025, supported by integrated emergency systems and reimbursement clarity. King County’s 5,000-plus registered AEDs linked to dispatch exemplify best-practice public-access integration. The FDA’s prompt clearance of innovations such as the Aurora EV-ICD and Jewel Patch cultivates early adoption and reinforces regional leadership. Drone pilots in North Carolina cut response times to 4 minutes, hinting at further survival gains once scaled.

Europe sustains moderate growth as MDR compliance stabilizes. Although roughly one-third of devices risk discontinuation, successful certifications, such as ZOLL’s AED line, demonstrate that committed manufacturers can navigate the process. Remote monitoring uptake remains uneven: Germany and the UK reimburse connectivity, whereas Belgium and Spain lag, tempering defibrillator market penetration. Netherlands-based drone-AED projects highlight technological enthusiasm, and mandated installations in South Australia mirror the regulatory push for accessibility.

Asia-Pacific exhibits the highest CAGR of 8.21%, driven by healthcare expenditure growth above OECD averages despite lower baseline spending. Training deficits are sizable only 17.5% of Chinese nurses feel AED-ready but national curricula and corporate upskilling initiatives aim to bridge gaps. ICD adoption still trails Western benchmarks due to cost constraints, yet expanding insurance coverage and local manufacturing e.g., MicroPort’s European catheter rollout should ease affordability and bolster the defibrillator market. Venture funding volatility poses a short-term challenge, but demographic shifts and policy support suggest durable demand through 2031.

Regulatory Landscape

Defibrillators operate under stringent, multi-region medical-device rules that shape time-to-market and lifecycle compliance. In the United States, automated external defibrillators (AEDs) are regulated by the FDA as Class III devices under 21 CFR 870.5310, requiring Premarket Approval (PMA) and robust post-market controls, while FDA expectations for connected and software-driven features also increase documentation and vulnerability-management obligations. A notable systems-level change is the FDA Quality Management System Regulation (QMSR), which became effective on February 2, 2026, updating device CGMP requirements and pushing manufacturers to align quality systems more tightly with modern design controls for hardware-software products. In Europe, defibrillators fall under the Medical Devices Regulation (MDR) (EU) 2017/745, where recertification and Notified Body capacity continue to influence portfolio decisions for legacy devices and new launches. Policy activity has accelerated around MDR implementation, including the European Parliament and Commission proposal COM(2025) 1023 (December 16, 2025) aimed at reducing administrative burden, and Commission-adopted delegated regulations in March 2026 that amend certain MDR obligations for specific implantable and Class III devices. On the trade side in the United States, defibrillators and certain related assemblies are classified under HTS codes such as 9018.90.64 and 9018.90.68 with a general duty rate of Free, keeping tariff exposure limited compared with other medtech categories.

Competitive Landscape

The defibrillator market is moderately consolidated, with incumbents leveraging R&D heft to maintain share. Medtronic commands leadership in extravascular systems; its Aurora EV-ICD hit 98.7% effectiveness, underscoring clinical edge.

Abbott capitalizes on dual-chamber leadless pacing, having secured the the CE mark for the AVEIR DR system, which achieves 97% AV synchrony, positioning the firm firmly in combined therapy domains. Boston Scientific’s modular mCRM platform validates wireless cardiac ecosystem strategy and opens cross-sell avenues between pacemakers and defibrillators.

Strategic transactions reshape portfolios: Johnson & Johnson integrated heart-pump maker Abiomed for USD 16.6 billion to broaden cardiovascular offerings, while Teleflex bought BIOTRONIK’s vascular intervention unit for USD 825 million, adding cath-lab synergies. New entrants exploit connectivity niches; ZOLL’s cloud analytics and Medtronic’s subscription services signal migration toward recurring revenue. Cybersecurity compliance now differentiates suppliers as FDA regulations require software bills of materials, pushing smaller players to partner or exit, and potentially raising barriers to entry.

Defibrillator Industry Leaders

Boston Scientific Corporation

Abbott Laboratories

Medtronic PLC

Koninklijke Philips NV

Nihon Kohden Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Product-cycle opportunity is expanding in extravascular and physiologic-pacing compatible architectures, where suppliers are attempting to reduce transvenous lead complications while maintaining therapy performance. Medtronic advanced this direction with U.S. FDA approval (March 2026) for an expanded indication for its OmniaSecure defibrillation lead for left bundle branch area placement, reinforcing a pathway that ties high-voltage defibrillation to conduction system pacing workflows.

Early-stage pipeline activity is also visible in parasternal extravascular ICD approaches, with AtaCor Medical treating the first patient in its ALARION-EV pivotal trial in July 2026 using an investigational Abbott pulse generator, highlighting whitespace for less invasive implant strategies that may compete with or complement subcutaneous and transvenous systems. In external and professional-use segments, opportunities concentrate around platform refreshes, MDR-compliant launches, and service-led models for hospitals, EMS, and public-access programs. ZOLL obtained EU MDR approval for its Zenix professional monitor/defibrillator in February 2026, supporting replacement and standardization cycles in Europe where MDR compliance has become a differentiator. Industry structure is also shifting through portfolio consolidation and specialization, demonstrated by Emergency Care Holdings completing the acquisition of Philips Emergency Care in January 2026 and operating it under the Heartstream brand, which creates room for integrated emergency-care platforms that bundle devices, consumables, software connectivity, and training. Meanwhile, public-access deployment remains underpenetrated in real-world use in many markets, and evidence from integrated systems such as King County having 5,000-plus AEDs registered with 911 underscores the operational model that vendors can target with connectivity, maintenance subscriptions, and dispatcher integration.

Recent Industry Developments

- July 2026: AtaCor Medical treated the first patient globally in the ALARION-EV pivotal trial evaluating a parasternal extravascular ICD system used with an investigational Abbott pulse generator. The milestone validates clinical momentum behind extravascular defibrillation architectures aimed at avoiding transvenous lead pathways. It also signals a competitive R&D lane that could diversify future implantable system options beyond traditional T-ICD and S-ICD approaches.

- February 2026: ZOLL obtained EU MDR approval for its Zenix professional monitor/defibrillator, enabling replacement cycles in Europe where MDR compliance differentiates vendors and drives standardization.

- May 2024: Boston Scientific reported that its MODULAR ATP Study for the mCRM system met primary safety and efficacy endpoints. Clinical validation for modular cardiac rhythm management supports the strategy of combining subcutaneous defibrillation with pacing capabilities to broaden addressable patient cohorts. The readout strengthens evidence generation needed for adoption discussions with clinicians and regulators as companies pursue more integrated device ecosystems.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the defibrillator market covers revenue generated from devices that deliver an electric shock (or therapy) to restore a normal heart rhythm, used in clinical, emergency, public access, and home settings, and counted at the manufacturer level.

Scope exclusions: We exclude CPR-only products, basic monitoring equipment without defibrillation capability, and service-only revenues where no device sale is involved.

Segmentation Overview

- By Product

- Implantable Cardioverter Defibrillator (ICD)

- Transvenous ICDs (T-ICDs)

- Single-Chamber

- Dual Chamber

- Subcutaneous ICDs (S-ICDs)

- Cardiac Resynchronization Therapy-D (CRT-D)

- Transvenous ICDs (T-ICDs)

- External Defibrillator

- Automated External Defibrillators (AEDs)

- Semi Automated

- Fully Automated

- Manual External Defibrillators

- Wearable Cardioverter Defibrillators (WCDs)

- Automated External Defibrillators (AEDs)

- Implantable Cardioverter Defibrillator (ICD)

- By End User

- Hospitals & Cardiac Centers

- Home Care Settings

- Other End Users

- By Patient Type

- Adult Patients

- Pediatric Patients

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the base demand picture and to keep assumptions realistic before we spoke with the market. We relied on public and official sources such as CDC cardiac arrest and cardiovascular statistics, FDA device databases and safety communications, WHO health system indicators, OECD health statistics, and peer-reviewed cardiology and emergency medicine journals that track survival and response patterns.

To translate demand signals into a value model, we also reviewed company annual reports, investor presentations, earnings transcripts, and reputable press coverage on tenders, product launches, and recalls. Where available, we referenced paid subscriptions for company financials and news context, along with patent databases to understand refresh cycles and technology shifts. These examples are not exhaustive, and we checked additional public sources for data collection, validation, and clarification during the work.

Primary Interviews and Surveys

Primary work focused on interviews and structured surveys with manufacturers, distributors, clinical users, and procurement stakeholders, so pricing, replacement timing, and adoption barriers could be confirmed. Because this is a global market, we validated inputs across APAC, EMEA, and the Americas to reduce single-region bias, and then we rechecked the final assumptions when desk and field signals did not align.

Respondent mix was used to stress-test pricing and replacement assumptions at both institutional and distributor levels, including how often hospitals and public access programs rotate AED devices and how that timing varies by country-level procurement cadence.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 39% | CXOs: 19% | APAC: 43% |

| Mid tier: 42% | Functional/Unit leaders: 28% | EMEA: 30% |

| Smaller Players: 19% | Managers: 53% | Americas: 27% |

Market-Sizing & Forecasting

Sizing starts with a top-down build that reconstructs device demand from procedure and care setting activity, then converts it into value using typical price bands and replacement cycles. In practice, the model is anchored on a few measurable signals such as ICD implantation volumes, AED placement density in public access programs, EMS deployment levels, hospital procurement cadence, and the installed base replacement rate for aging units.

After that, selective bottom-up checks are used to keep totals realistic, such as sampled ASP times shipment ranges by product type and channel checks on tender volumes in priority countries. When some country-level inputs are not available, we handle gaps using proxy indicators (healthcare spend, cardiovascular disease burden, and emergency response infrastructure) and then normalize them using interview feedback.

For forecasting, we used scenario analysis supported by trend curves on key drivers, since demand can shift with guideline changes, reimbursement updates, and public access mandates. Growth rates were adjusted using expert consensus on pricing pressure, mix shifts between implantable and external devices, and expected refresh cycles for connected and wearable formats.

Data Validation & Update Cycle

Validation is done through triangulation across the model outputs, external reference indicators, and what interviewees confirm as reasonable ranges. We run variance checks by region and product type, and we review outliers for explainable causes such as one-time tenders, regulatory actions, or temporary supply constraints.

Before sign-off, assumptions and calculations go through multiple analyst reviews, and re-contact is triggered when a major mismatch shows up between desk signals and primary inputs. Reports are refreshed annually, with interim updates when material events occur, and a final pre-delivery review is completed so clients receive the most current view available at that time.

Mordor Intelligence's Defibrillator Market Estimate Compared With Other Published Estimates

Published market values for defibrillators can look far apart, even when they describe similar devices and regions, because the scope and timing choices are not always the same. Differences usually come from what is counted as a defibrillator sale, which year is treated as the base, and how pricing and replacement are projected forward.

Some published totals appear to be built from a narrower demand pool that leans on a limited set of end uses or shorter product lists, and others include broader lines such as services and accessories that inflate reported revenue. In Mordor Intelligence, we count ICDs and external defibrillators (including AEDs, manual external defibrillators, and wearable cardioverter defibrillators) and keep the value tied to device revenues, with annual checks on procedure volumes, placements, and replacement timing so the pricing and unit assumptions stay consistent.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 15.65 B (2026) | |

| Trade Journal A | USD 7.99 B (2024) | Uses an earlier base year and may concentrate on a smaller addressable pool that tracks selected product categories and settings, which can reduce the counted installed base and replacement contribution in the modeled year. |

| Regional Consultancy B | USD 13.43 B (2023) | Anchors on a different base year and can apply a different mix and pricing progression across implantable and external devices, which shifts totals when inflation, currency timing, and replacement cycles are not aligned to the same forecast start year. |

The spread in the table is mainly explained by year selection and what revenue lines are included in the total, followed by how replacement demand is treated versus only new placements. By keeping the inputs traceable to measurable usage signals and then rechecking them through interviews, the estimate stays balanced and can be repeated with the same steps as new data comes in.

Key Questions Answered in the Report

How big is the Defibrillator Market?

The Defibrillator Market size is expected to reach USD 15.65 billion in 2026 and grow at a CAGR of 7.10% to reach USD 22.05 billion by 2031.

How fast will demand for external defibrillators grow?

External defibrillators are forecast to register a 7.64% CAGR between 2026 and 2031.

Who are the key players in Defibrillator Market?

Boston Scientific Corporation, Abbott Laboratories, Medtronic PLC, Koninklijke Philips NV and Nihon Kohden Corporation are the major companies operating in the Defibrillator Market.

Which is the fastest growing region in Defibrillator Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which region has the biggest share in Defibrillator Market?

North America commanded 43.85% of global sales in 2025.

Page last updated on: