E-prescribing Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 4.21 Billion |

| Market Size (2030) | USD 12.44 Billion |

| Growth Rate (2025 - 2030) | 24.19% CAGR |

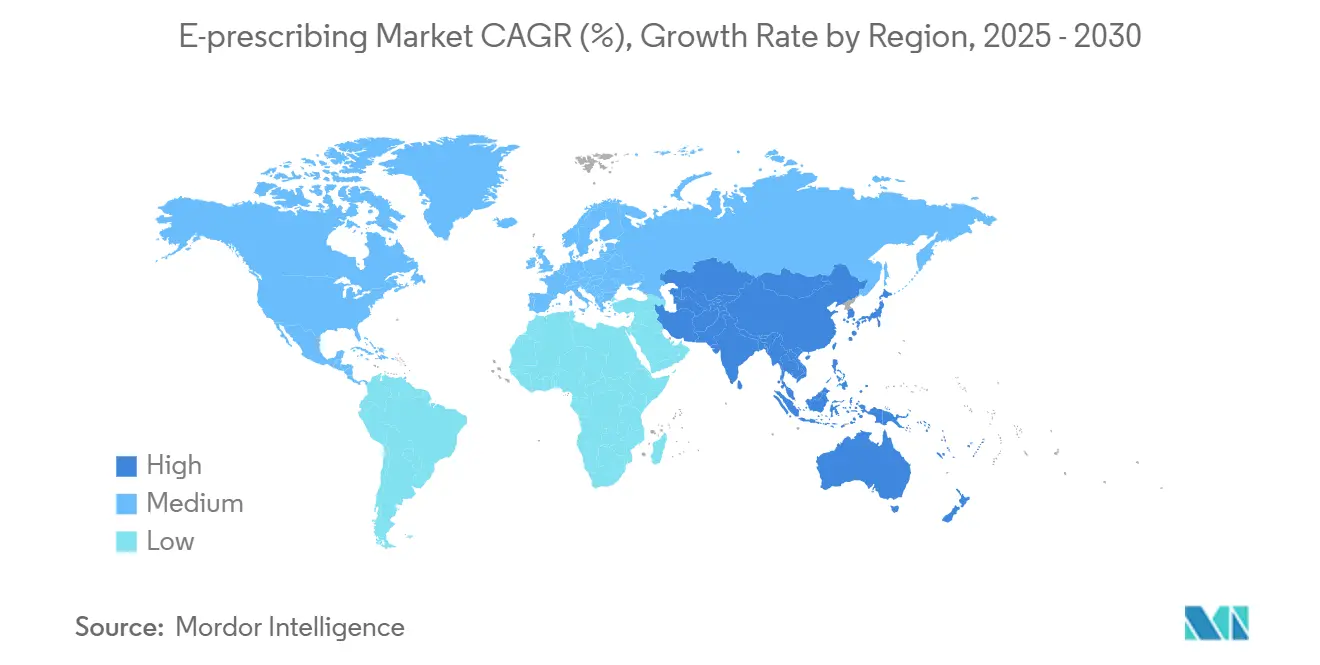

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

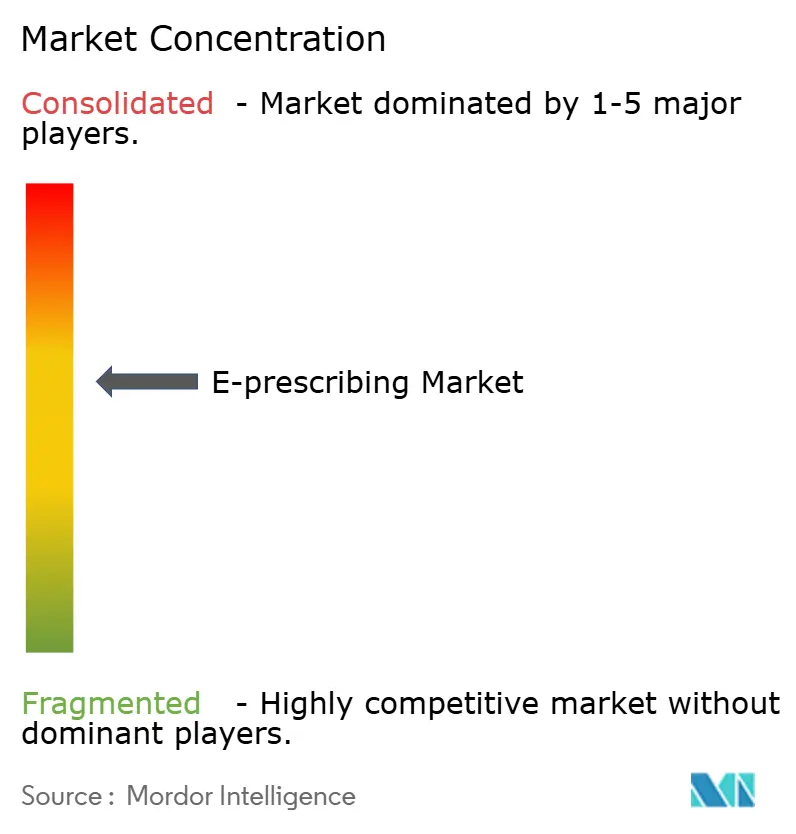

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

E-prescribing Market Analysis by Mordor Intelligence

The electronic prescribing market reached USD 4.21 billion in 2025 and is forecast to climb to USD 12.44 billion by 2030, advancing at a 24.19% CAGR. Regulatory mandates, healthcare digitization, and the need to curb prescription fraud that costs the United States about USD 250 billion every year continue to accelerate demand. Momentum is further supported by the Drug Enforcement Administration’s decision to extend telemedicine prescribing flexibilities for Schedule II-V medications through December 2025[1]U.S. Drug Enforcement Administration, “Telemedicine Flexibilities for Prescription of Controlled Substances,” dea.gov. Rapid adoption across hospitals, clinics, pharmacies, and growing telehealth networks keeps the electronic prescribing market on a robust growth path.

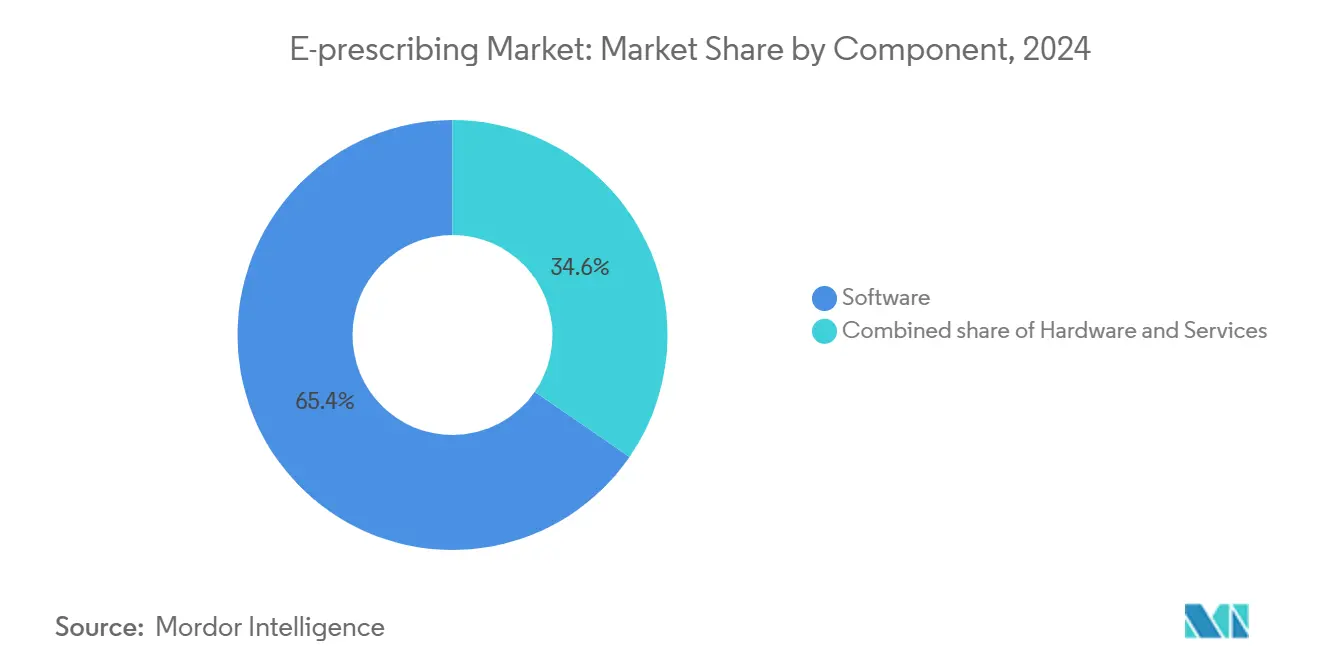

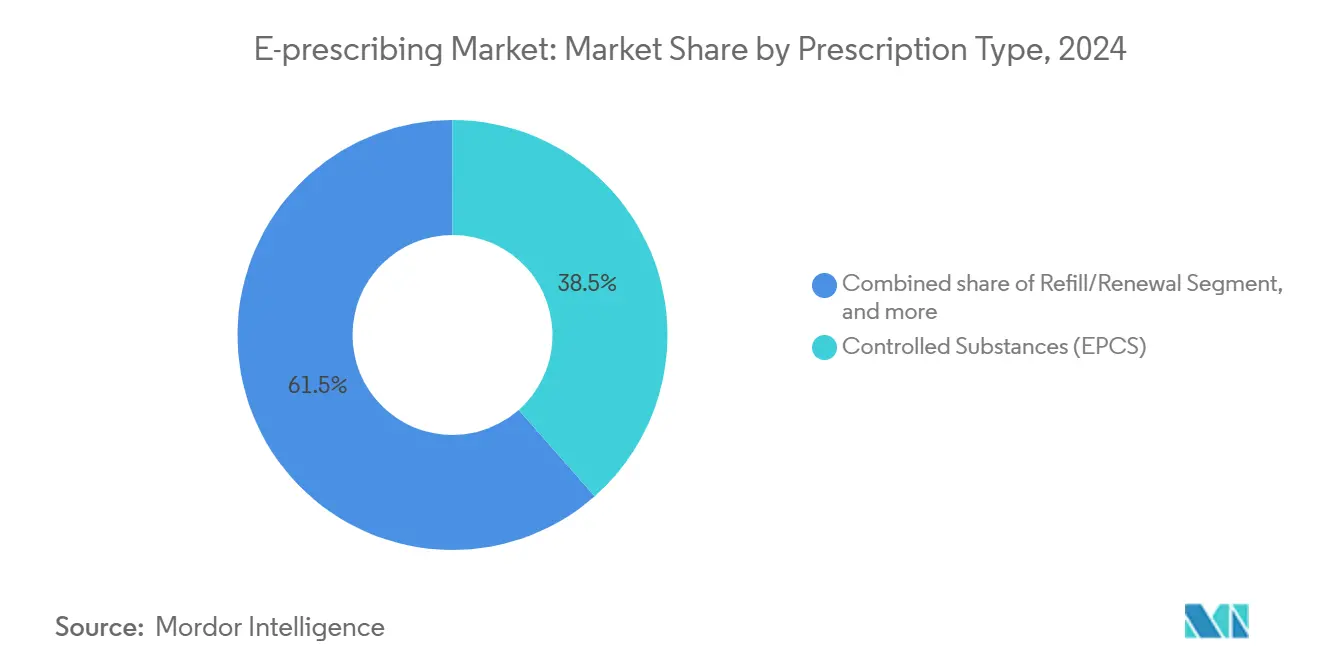

North America held 38.54% of the electronic prescribing market in 2024, lifted by the Centers for Medicare & Medicaid Services (CMS) rule obligating providers to write at least 70% of controlled substance prescriptions electronically, with enforcement that began in 2023[2]Centers for Medicare & Medicaid Services, “Electronic Prescribing of Controlled Substances Requirements,” cms.gov. Asia-Pacific is expanding at a 25.45% CAGR through 2030 due to Japan’s medical DX program that links My Number cards to electronic prescriptions and China’s three-medical linkage reforms that connect care, insurance, and pharmaceutical supply chains. Software remained dominant with 65.45% share in 2024, yet services are the fastest-growing component at 26.45% CAGR. Integrated EHR or hospital information systems account for 72.34% of usage, but mobile-first apps are rising at 26.56% CAGR. Cloud delivery leads with 54.34%, and controlled substances (EPCS) form the largest prescription class at 38.54%, while specialty drugs grow fastest at 25.67% CAGR.

Key Report Takeaways

- By component, the software segment led with 65.45% of 2024 revenue; services are forecast to grow at 26.45% CAGR to 2030.

- By type of system, integrated EHR/HIS platforms commanded 72.34% electronic prescribing market share in 2024, while mobile-first applications are tracking a 26.56% CAGR.

- By delivery mode, cloud-based solutions captured 54.34% of the electronic prescribing market size in 2024; web-based platforms are advancing at 26.98% CAGR through 2030.

- By prescription type, controlled substances held 38.54% electronic prescribing market share in 2024; specialty drugs are projected to expand at 25.67% CAGR to 2030.

- By end user, hospitals accounted for 46.79% of the electronic prescribing market size in 2024; telehealth providers exhibit the quickest growth at 27.86% CAGR.

- By geography, North America led with 38.54% revenue share in 2024, whereas Asia-Pacific is set to rise at a 25.45% CAGR.

Global E-prescribing Market Trends and Insights

Driver Impact Analysis

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government mandates for electronic prescription adoption | +6.2% | Global, strongest in North America & EU | Medium term (2-4 years) |

| Rising focus on medication safety and quality of care | +4.8% | Global, especially North America | Long term (≥ 4 years) |

| Need for healthcare cost reduction and operational efficiency | +3.9% | Global, emphasis on APAC & emerging markets | Long term (≥ 4 years) |

| Growing penetration of cloud-based healthcare IT infrastructure | +3.2% | Global, accelerated in APAC & Latin America | Medium term (2-4 years) |

| Expansion of telehealth and digital pharmacy ecosystems | +2.8% | Global, highest uptake in rural and underserved areas | Short term (≤ 2 years) |

| Emerging value-based care and medication price transparency | +2.1% | North America & EU, pilots in APAC | Long term (≥ 4 years) |

Source: Mordor Intelligence

Government Mandates for Electronic Prescription Adoption

Mandatory e-prescribing laws are realigning prescription workflows worldwide. The DEA’s forthcoming special registration framework introduces three tiers of telemedicine authorization, obliging clinicians to hold state-specific telemedicine credentials and use electronic prescriptions for Schedule II-V drugs. California’s rule that all prescriptions—controlled or not—be electronic since January 2022 shows how quickly mandates expand, with 35 states now enforcing EPCS legislation. CMS has already confirmed the transition to NCPDP SCRIPT Standard version 2023011 in January 2028, compelling systems to support real-time benefit tools and enhanced formulary data. A federal requirement to check state Prescription Drug Monitoring Programs is set for implementation within three years, further cementing e-prescribing as the only secure route for controlled substances. These cascading rules create a replacement cycle that drives the electronic prescribing market far beyond organic growth.

Rising Focus On Medication Safety And Quality Of Care

Patient-safety imperatives push healthcare systems to adopt advanced prescribing tools that reduce errors linked to 125,000 deaths a year in the United States. Surescripts’ Sig IQ translated 4.1 billion patient directions in 2024, converting free text to structured instructions that cut emergency department visits for adverse events. Epic Systems embedded more than 100 AI-based prescription management features that screen interactions and suggest optimal dosing. The DEA also requires biometric authentication with a false match rate below 0.001 for EPCS, escalating security needs that favor premium platforms. Medication therapy management systems now combine prescription histories with real-time adherence monitoring, addressing USD 250 billion in annual non-adherence costs. Real-time benefit tools further enhance safety by saving patients USD 37 per prescription through on-screen cost and formulary feedback.

Need For Healthcare Cost Reduction And Operational Efficiency

Provider groups look to e-prescribing to relieve budget pressure and streamline operations. Medicare Shared Savings Program ACOs reported USD 1.8 billion in 2022 savings, with optimized medication management a core driver. Electronic prescriptions paired with benefit verification now allow prescribers to choose cost-effective substitutes, cutting prior-authorization-related overhead estimated at USD 31 billion each year. E-prescribing also lowers pharmacy callback rates by 40%, improving staff productivity. Cloud-native deployments reduce on-premise hardware spending, and AI transcription tools such as eClinicalWorks’ Sunoh.ai save clinicians around two hours daily while improving billing precision. Centralized medication management platforms like Omnicell OmniSphere add enterprise level control across multi-site networks.

Growing Penetration Of Cloud-Based Healthcare IT Infrastructure

Widespread cloud adoption cuts implementation time and scales access to e-prescribing. Automatic software updates, continuous security patches, and subscription pricing remove capital barriers for smaller practices. HITRUST r2 certifications awarded to leading networks underscore the maturity of cloud security controls. Multi-tenant designs give clinics enterprise-grade functions without dedicated IT teams and enable seamless integration with telehealth platforms that became mission-critical during the pandemic. Combining cloud e-prescribing with AI analytics and natural language processing is creating extended digital health ecosystems that go beyond simple prescription routing.

Restraints Impact Analysis

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data privacy and cybersecurity concerns | -3.4% | Global, heightened in EU under GDPR | Short term (≤ 2 years) |

| Lack of interoperability and data standardization | -2.8% | Global, more acute in fragmented systems | Medium term (2-4 years) |

| Provider workflow disruption and usability barriers | -2.3% | Global, impacts high-volume clinical settings | Short term (≤ 2 years) |

| Limited technical expertise in small and rural practices | -1.9% | Rural areas in North America, APAC & Africa | Medium term (2-4 years) |

Source: Mordor Intelligence

Data Privacy And Cybersecurity Concerns

Healthcare remains a prime ransomware target. The Change Healthcare attack interrupted prescription workflows for more than one-third of U.S. patients, forcing emergency paper-based processes. The DEA has also warned about EHR credential theft that allows criminals to generate massive volumes of fraudulent scripts. Legislative proposals like the Health Care Cybersecurity Improvement Act would tie Medicare payments to security readiness, adding cost burdens for small practices. Mandatory two-factor authentication, digital signatures, and detailed audit trails further raise operating complexity. Rural or small providers often lack funds and expertise to meet stringent requirements, slowing adoption and narrowing the electronic prescribing market in underserved regions.

Lack Of Interoperability And Data Standardization

Inconsistent data models hamper seamless exchange even where electronic prescribing is widespread. Only 23% of U.S. physicians say external health information is very easy to use, pointing to gaps that complicate medication reconciliation. Fragmented systems leave patients vulnerable when moving between providers that operate incompatible platforms. Upgrading to NCPDP SCRIPT 2023011 demands extensive testing between every network participant and can disrupt workflows. Semantic interoperability issues remain because different EHRs label medication fields in unique ways, requiring manual mapping that risks errors[3]JMIR, “Semantic Interoperability Challenges in e-Prescribing,” jmir.org. Absent uniform APIs, health systems must maintain bespoke interfaces for each vendor, inflating maintenance costs and discouraging platform switching.

Segment Analysis

By Component: Services Drive Integration Complexity

In 2024 software accounted for 65.45% of revenue, reflecting core licensing demand across hospitals and clinics. Services, however, projected at a 26.45% CAGR, underline how organizations now value onboarding support, regulatory guidance, and continuous optimization. Surescripts’ 4.1 billion Sig IQ instructions in 2024 illustrate a shift from basic data transport to value-added medication management.

The services boom reinforces that technology alone does not solve prescribing challenges. Implementation now routinely covers classroom training, change-management workshops, and help-desk outsourcing. This service overlay creates sticky, subscription-like income for vendors and sustains the electronic prescribing market even in mature geographies. Recurrent upgrades to meet DEA biometrics or upcoming SCRIPT standards secure the segment’s long-term growth trajectory.

Note: Segment shares of all individual segments available upon report purchase

By Type of System: Mobile Innovation Challenges EHR Dominance

Integrated EHR or HIS solutions held 72.34% of the electronic prescribing market in 2024, capitalizing on their embedded role in point-of-care workflow. Mobile-first apps are catching up with a 26.56% CAGR thanks to secure tablets and smartphones that enable immediate order entry during rounds or home visits. Stand-alone systems stay relevant in niche environments where full EHR rollouts remain impractical.

Epic’s wave of AI-enabled prescribing tools demonstrates how EHR giants defend share, while smaller mobile entrants compete on usability and low upfront cost. Mobile solutions also serve outreach programs, pop-up clinics, and disaster zones. Yet integrated suites still provide deeper access to lab values, problem lists, and decision support—capabilities crucial for complex polypharmacy management.

By Delivery Mode: Web-Based Solutions Gain Momentum

Cloud platforms already represent 54.34% revenue in 2024, but browser-based deployments are growing fastest at 26.98% CAGR as providers prefer log-in-and-go convenience. On-premise installations linger where policy or security demands local control, while API Platform-as-a-Service models appeal to health tech firms that embed prescribing into broader applications.

Cloud migration simplifies version control and accelerates security patching, benefits recognized by systems that process millions of scripts each day. Web access also eases multi-site expansion for retail pharmacy chains and telehealth networks. Browser-based tools keep pace with stringent authentication rules and eliminate local software conflicts, ensuring the electronic prescribing market remains accessible for organizations large and small.

By Prescription Type: Specialty Drugs Drive Premium Growth

Controlled substances represented 38.54% electronic prescribing market share in 2024, reflecting the regulatory push to digitize opioids and stimulants. Specialty medications, though smaller in volume, generate the quickest value growth at 25.67% CAGR because biologics and gene therapies demand rigorous tracking. NewRx scripts remain foundation volume, while automated refill modules trim staff workload.

Surescripts recorded 310.5 million electronic controlled-substance scripts in 2024, with 83.9% of active prescribers EPCS-enabled and 96.3% of pharmacies ready to dispense digitally. Specialty therapy often triggers prior authorizations and financial-assistance requests, so advanced platforms that integrate payer workflows command premium fees, further enlarging the electronic prescribing market size for high-complexity drugs.

By End User: Telehealth Providers Accelerate Adoption

Hospitals contributed 46.79% of 2024 revenue, reflecting enterprise EHR penetration and high script volumes. Telehealth providers, however, record a 27.86% CAGR as remote visits become a standard care pathway. Clinics and pharmacy or mail-order channels adopt e-prescribing steadily, driven by compliance and efficiency targets.

The DEA’s extended flexibilities let virtual clinicians continue to e-prescribe Schedule II-V medications, removing geographic barriers that once limited remote addiction and mental-health therapy. Hospital groups benefit from economies of scale, yet telehealth networks gain ground by offering convenient home delivery and medication coaching. The resulting multichannel landscape broadens reach and diversifies the electronic prescribing industry revenue base.

Geography Analysis

North America dominated the electronic prescribing market with 38.54% share in 2024, sustained by mature network infrastructure and strong federal mandates. Surescripts routed 2.5 billion prescriptions on its U.S. platform that year, highlighting entrenched adoption. Persistent cybersecurity events such as the Change Healthcare breach and ongoing data-sharing challenges underscore the region’s future investment needs, yet incentives embedded in Medicare and commercial insurance maintain growth momentum.

Asia-Pacific posted the fastest trajectory at 25.45% CAGR through 2030. Japan is rolling out a nationwide database that links every citizen’s My Number ID to prescription histories, while China builds integrated treatment-insurance-pharmacy networks under its three-medical linkage policy. Governments in India, South Korea, and Australia are equally prioritizing national drug monitoring systems, creating leapfrog opportunities that let providers deploy cloud and mobile solutions without legacy constraints. A projected USD 138 billion healthcare outlay in China by 2027 offers substantial room for electronic prescribing market expansion.

Europe exhibits steady progress driven by Germany’s e-Rezept program and the NHS mobile-app prescription service that now handles 3.1 million repeat requests monthly. Diverse regulatory environments across 27 EU states slow harmonization, but strict data-protection frameworks bolster consumer trust. South America along with the Middle East & Africa remain nascent but attractive; public-sector digitization drives early projects in Brazil, Saudi Arabia, and the United Arab Emirates. The global outlook therefore pairs mature usage in North America and Europe with rapid scale-up in Asia-Pacific and selective pilot adoption across emerging regions, sustaining long-term growth for the electronic prescribing market.

Competitive Landscape

The electronic prescribing market is moderately concentrated. Surescripts anchors the ecosystem, connecting over 2.14 million providers and enabling 24 billion health-information exchanges in 2023. Epic Systems expanded its acute-care EHR footprint to 42.3% of U.S. hospitals after onboarding 176 multispecialty facilities in 2024, deepening its integrated prescribing base. Oracle Health’s share dropped to 22.9% after it lost 74 hospital clients post-acquisition, illustrating competitive pressure.

Technology differentiation centers on AI decision support, seamless network interoperability, and compliance tooling. Epic introduced over 100 AI features that flag interactions and suggest personalized dosing. Oracle Health is rolling out voice commands and facial ID to streamline clinician logins. New entrants target specialized niches: Surescripts extended its network to veterinary prescriptions via DAW Systems and digital pharmacies pursue direct-to-consumer refills. Platforms with advanced biometrics and full DEA compliance attract hospitals managing high-risk controlled substances, while lightweight mobile apps appeal to telehealth startups. Vendor roadmaps increasingly integrate value-based analytics and outcome tracking to align with payer incentives, pushing the electronic prescribing industry toward data-rich, AI-assisted ecosystems.

Strategic partnerships and acquisitions illustrate market dynamics. Omnicell launched its cloud-native OmniSphere to link robotics and smart cabinets, securing HITRUST certification. McKesson’s USD 850 million move for PRISM Vision Holdings added ophthalmology reach and augmented data-analytics capacity. Francisco Partners bought AdvancedMD for USD 1.125 billion, betting on integrated ambulatory software that embeds prescribing tools. These deals underscore how scale, data depth, and workflow breadth define competitiveness in the electronic prescribing market.

E-prescribing Industry Leaders

-

Allscripts Healthcare Solutions (Veradigm)

-

Surescripts

-

Epic Systems Corporation

-

Oracle (Cerner)

-

DrFirst

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: McKesson Corporation agreed to buy an 80% stake in PRISM Vision Holdings for USD 850 million, strengthening its specialty-care and analytics portfolio.

- January 2025: The DEA published three final rules that create special telemedicine registrations, permitting Schedule II-V prescribing without prior in-person visits under defined conditions.

- January 2025: Surescripts formed a national growth partnership with TPG to scale intelligent prescribing, benefits, and interoperability services.

- January 2025: Avel eCare acquired Amwell Psychiatric Care, expanding virtual behavioral health services across 46 states.

- December 2024: HEALWELL AI purchased Orion Health Holdings for CAD 165 million, uniting AI-driven interoperability with a client base covering 150 million lives.

Global E-prescribing Market Report Scope

As per the scope of the report, e-prescribing, or electronic prescribing is a technology framework that allows physicians and other medical practitioners to write and send prescriptions to a participating pharmacy in an electronic format instead of using written prescriptions. The e-prescribing Market is segmented by component (Hardware, Software, and Services), Type of System (Stand-alone E-prescribing System and Integrated E-prescribing System), By Delivery Mode (Cloud Based, Web Based, and On-Premise), End User (Hospitals and Clinics), and Geography (North America, Europe, Asia-Pacific, Middle East, and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the value (in USD million) for the above segments.

| By Component | Hardware | ||

| Software | |||

| Services | |||

| By Type of System | Stand-alone Systems | ||

| Integrated EHR/HIS Systems | |||

| Mobile-first Apps | |||

| By Delivery Mode | Cloud-based | ||

| Web-based | |||

| On-premise | |||

| API Platform-as-a-Service | |||

| By Prescription Type | NewRx | ||

| Refill / Renewal | |||

| Controlled Substances (EPCS) | |||

| Specialty Drugs | |||

| By End User | Hospitals | ||

| Clinics | |||

| Pharmacies & Mail-order | |||

| Telehealth Providers | |||

| Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| Australia | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East & Africa | GCC | ||

| South Africa | |||

| Rest of Middle East & Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Hardware |

| Software |

| Services |

| Stand-alone Systems |

| Integrated EHR/HIS Systems |

| Mobile-first Apps |

| Cloud-based |

| Web-based |

| On-premise |

| API Platform-as-a-Service |

| NewRx |

| Refill / Renewal |

| Controlled Substances (EPCS) |

| Specialty Drugs |

| Hospitals |

| Clinics |

| Pharmacies & Mail-order |

| Telehealth Providers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

Key Questions Answered in the Report

What is the size of the electronic prescribing market and how fast is it growing?

The market reached USD 4.21 billion in 2025 and is forecast to climb to USD 12.44 billion by 2030, reflecting a 24.19% CAGR

Which regions are leading and which are expanding fastest?

North America held 38.54% of 2024 revenue, while Asia-Pacific is projected to advance at a 25.45% CAGR through 2030, driven by national digital-health initiatives

What regulatory changes are driving wider adoption?

Federal and state mandates such as the U.S. DEA’s extended telemedicine flexibilities and CMS rules requiring electronic transmission of most controlled-substance scripts are accelerating deployment

Why is electronic prescribing important for controlled substances?

Controlled substances accounted for 38.54% of 2024 revenue, and electronic workflows support biometric authentication, audit trails, and Prescription Drug Monitoring Program checks that curb diversion and fraud

What cybersecurity risks affect electronic prescribing systems?

Ransomware incidents such as the Change Healthcare attack, along with credential-theft schemes targeting DEA numbers, highlight the need for two-factor authentication, encryption, and continuous threat monitoring

Who are the main vendors and how consolidated is the market?

Surescripts, Epic Systems, Oracle Health, Omnicell, and McKesson lead the space; the top five players collectively control just over 60% of transactions, indicating moderate concentration.

Page last updated on: June 23, 2025