Computer And Peripherals Special Purpose Logic IC Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

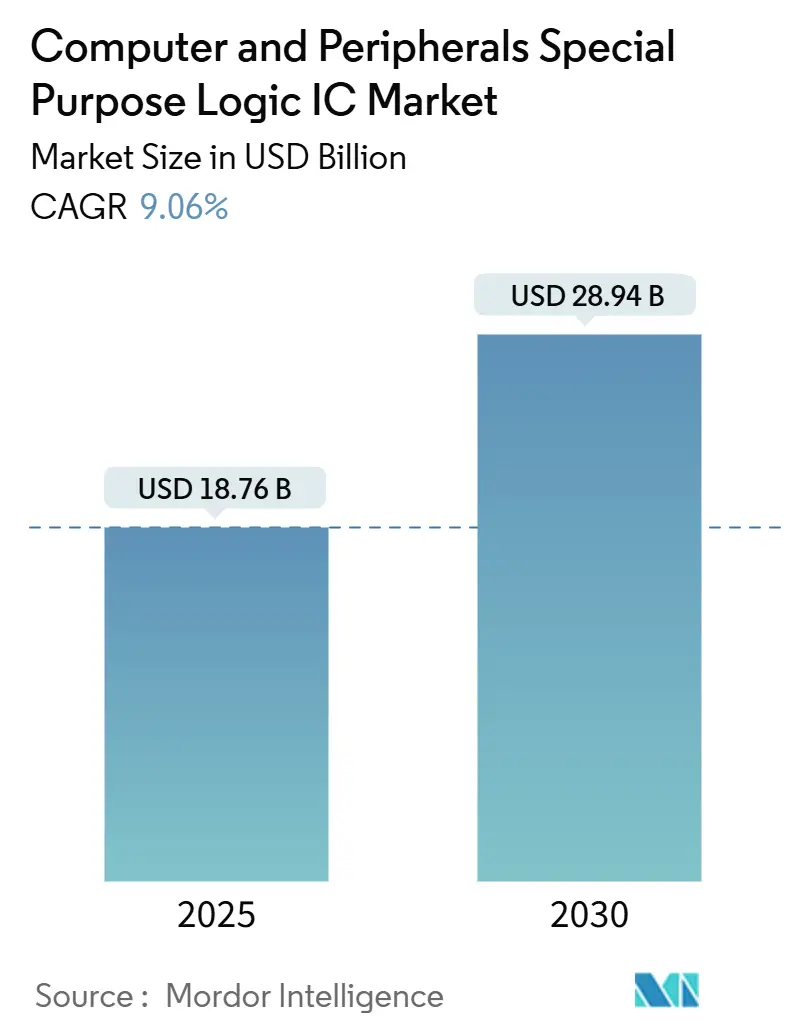

| Market Size (2025) | USD 18.76 Billion |

| Market Size (2030) | USD 28.94 Billion |

| Growth Rate (2025 - 2030) | 9.06% CAGR |

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

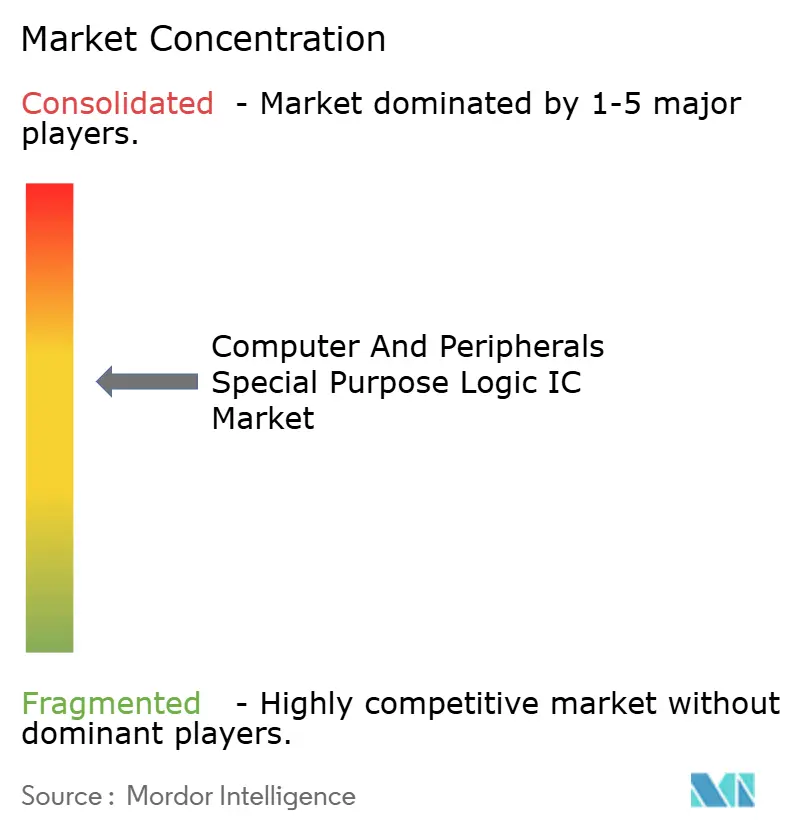

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Computer And Peripherals Special Purpose Logic IC Market Analysis by Mordor Intelligence

The computer and peripherals special purpose logic IC market size is valued at USD 18.76 billion in 2025 and is projected to reach USD 28.94 billion by 2030, advancing at a 9.06% CAGR. Mandatory USB-C adoption across the European Union, rapid adoption of AI-ready personal computers that embed neural processing unit (NPU) interfaces, and hyperscale data centers shifting to PCIe Gen5 storage are the three pivotal growth engines. Interface controllers dominate present revenue because every docking station, SSD enclosure, and hub relies on them to negotiate power, data, and video streams. Demand is now tilting toward custom ASICs, which enable gaming and industrial vendors to embed proprietary functions, thereby sustaining higher average selling prices despite a broader trend of 5%-7% annual price erosion on commodity parts. High-speed retimers, redrivers, and protocol bridges that enable USB4 Version 2.0 or Thunderbolt 5 carry a premium because only a handful of suppliers have passed compliance testing. On the demand side, consumer peripherals hold the largest share; however, industrial and embedded peripherals show the strongest unit growth as factories pursue smart manufacturing programs and retrofit IO-Link or Ethernet-based field devices.

Key Report Takeaways

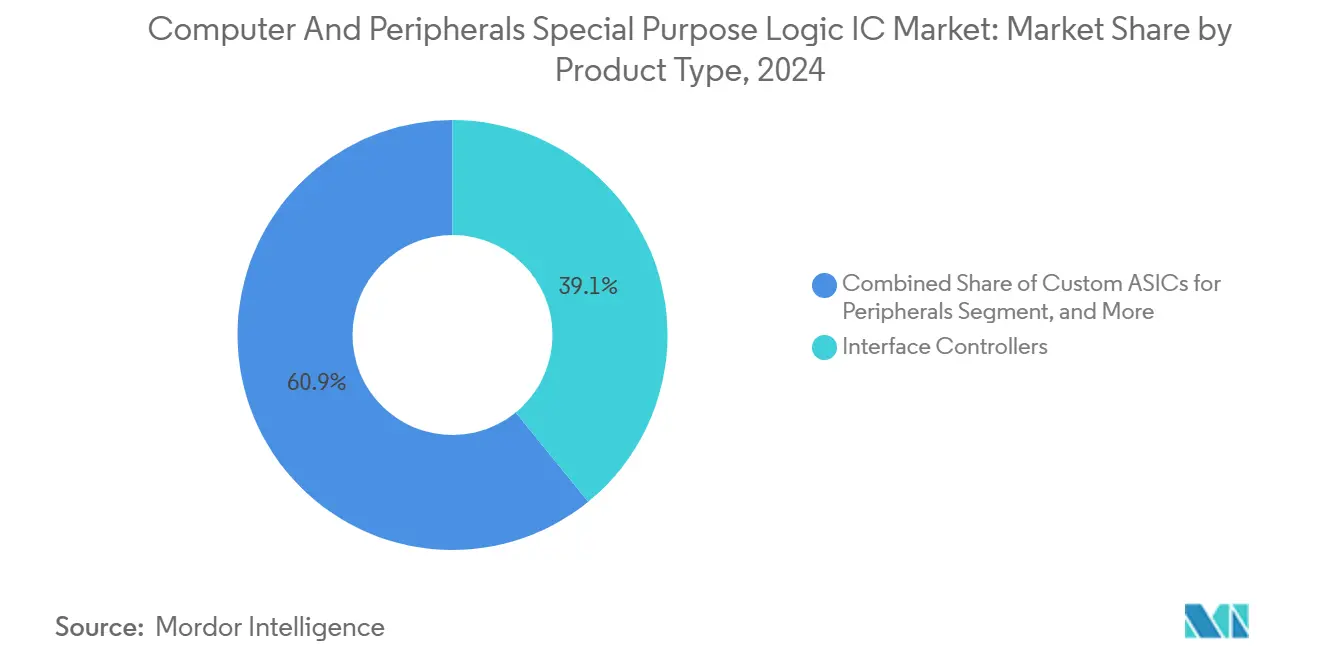

- By product type, interface controllers captured 39.12% of the computer and peripherals special purpose logic IC market size in 2024, while custom ASICs for peripherals are forecast to grow at a 9.87% CAGR through 2030.

- By application, storage peripherals commanded 35.78% of the computer and peripherals special purpose logic IC market size in 2024, and are forecast to expand at a 9.93% CAGR through 2030.

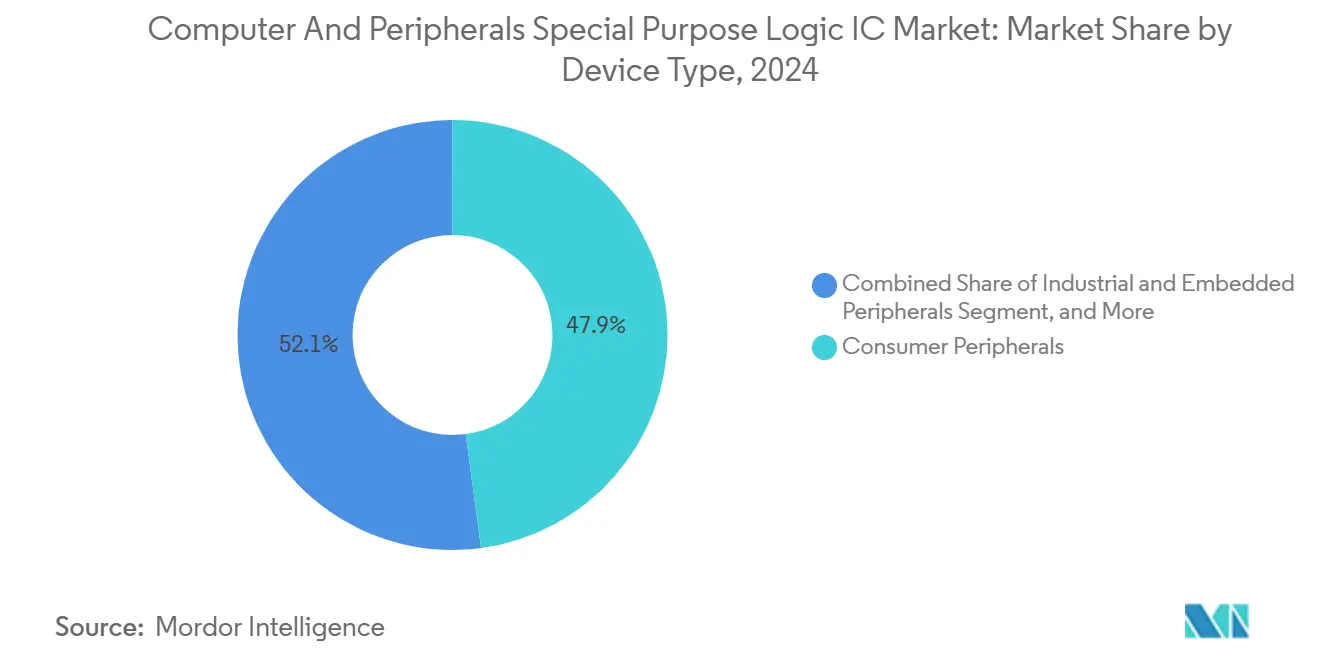

- By device type, consumer peripherals accounted for 47.89% of the computer and peripherals special purpose logic IC market size in 2024, whereas industrial and embedded peripherals are projected to advance at a 9.78% CAGR between 2025-2030.

- By end user, consumer electronics led with 42.37% of the computer and peripherals special purpose logic IC market size in 2024, while healthcare equipment is projected to post a 9.96% CAGR.

- By geography, the Asia Pacific region held 34.38% of the computer and peripherals special purpose logic IC market size in 2024, and the Middle East is predicted to record a 10.11% CAGR from 2024 to 2030.

Global Computer And Peripherals Special Purpose Logic IC Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Adoption of USB-C and Thunderbolt Interfaces | +1.8% | Global, with EU regulatory lead and North America enterprise uptake | Short term (≤ 2 years) |

| Rising Demand for High-Speed Peripheral ICs in Data Centers | +2.1% | North America and Asia Pacific core, expanding to Middle East | Medium term (2-4 years) |

| Proliferation of IoT Edge Devices Necessitating Interface Controllers | +1.5% | Asia Pacific manufacturing hubs, spillover to Europe industrial automation | Medium term (2-4 years) |

| Rapid Growth of Gaming Peripherals Requiring Custom Logic | +1.2% | North America and Europe consumer markets, Asia Pacific production | Short term (≤ 2 years) |

| Mainstream Integration of AI Acceleration in PC Accessories | +1.7% | Global, led by North America and China AI PC adoption | Medium term (2-4 years) |

| Regulatory Push Toward Universal Charging Standards | +1.3% | EU mandate driving global harmonization | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of USB-C and Thunderbolt Interfaces

The European Union’s Radio Equipment Directive, effective 28 December 2024, obliges every portable electronic device to integrate a USB-C receptacle, immediately retiring legacy micro-USB connectors.[1]European Commission, “Common Charger: EU Member States Adopt New Rules,” ec.europa.eu Peripheral makers therefore add USB Power Delivery 3.1 controllers that negotiate up to 240 watts, five times the power envelope of early USB-C versions, which raises semiconductor content per docking station by USD 4-USD 6. Intel’s Thunderbolt 5 specification, released in September 2023, doubles bidirectional bandwidth to 80 Gbps and supports asymmetric 120 Gbps uplinks for external GPUs. Taiwan-based ASMedia began sampling a USB4 Version 2.0 host controller during Q3 2024, allowing 80 Gbps over existing passive cables, an advantage that compresses the time incumbents have to refresh roadmaps. As enterprise IT departments refresh laptop fleets for hybrid work, demand for single-cable docks with dual 8K display support is spiking, pushing up aggregate demand for retimers and protocol converters.

Rising Demand for High-Speed Peripheral ICs in Data Centers

Hyperscale operators now replace PCIe Gen4 SSDs with Gen5 models to sustain inference workloads, a migration that doubles sequential read throughput to more than 14 GBps per drive.[2]Phison Electronics, “PS5026-E26 PCIe Gen5 NVMe SSD Controller,” phison.com Marvell’s Bravera SC5 controller integrates hardware encryption and inline compression, letting cloud providers reduce rack count 25% while maintaining security. Upgrades ripple into network-attached storage, which must shift to 100 GbE links, increasing demand for packet-processing PHYs that offload CPU resources. Enterprises face latency penalties if they postpone SSD refresh cycles, so purchasing intent has accelerated into the 2025 budget window. The cumulative effect is a robust, medium-term uplift in the computer and peripherals special purpose logic IC market because every Gen5 drive uses multiple low-power PCIe redrivers and power-management companions.

Proliferation of IoT Edge Devices Necessitating Interface Controllers

Factories in Japan and Germany retrofit IO-Link hubs into legacy programmable controllers, extending installed machinery life yet adding interface controller sockets that never existed before. Renesas introduced an RE-series transceiver in June 2024 with galvanic isolation plus diagnostics that meet IEC 61131-2, a specification increasingly demanded by industrial automation auditors. Edge gateways aggregate Modbus, CANopen, and EtherCAT, elevating semiconductor spend because single-protocol hubs no longer suffice. Time-sensitive networking chips synchronize sensors with sub-microsecond precision, enabling predictive maintenance that can slash unscheduled downtime by 15-20% according to 2024 field trials by PROFIBUS and PROFINET International.[3]PROFIBUS and PROFINET International, “Time-Sensitive Networking Field Trials,” profibus.com As smart-factory rollouts expand, demand for multi-protocol interface logic rises faster than factory output of mechanical parts, underpinning steady controller unit growth through 2030.

Rapid Growth of Gaming Peripherals Requiring Custom Logic

Esports players insist on sub-millisecond input latency and per-key RGB effects that cannot be achieved with off-the-shelf silicon. Razer introduced an 8,000 Hz polling USB dongle ASIC in 2024, shrinking latency eightfold compared with commodity mouse controllers. Logitech updated its Lightspeed protocol the same year with adaptive frequency hopping to avoid congested 2.4 GHz channels, an innovation made viable by embedding a custom radio core. Order volumes of only 50,000-100,000 units once made ASIC economics prohibitive; multi-project wafer services at 28 nm have cut non-recurring engineering costs to under USD 500,000, inviting mid-tier brands to fund bespoke chips. Consequently, the computer and peripherals special purpose logic IC market gains a new revenue stream from specialized dies that remain price-resilient even where commodity USB controllers experience deflation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cyclical Volatility in PC Shipments | -1.4% | Global, with pronounced swings in North America and Europe enterprise segments | Short term (≤ 2 years) |

| Supply Chain Disruptions in Advanced Node Foundries | -1.1% | Asia Pacific foundry concentration, ripple effects to North America and Europe OEMs | Medium term (2-4 years) |

| Escalating Design Costs for Sub-10 nm Nodes | -0.9% | Global, affecting fabless vendors and custom ASIC developers | Long term (≥ 4 years) |

| Increasing IP Litigation in Interface Controller Space | -0.7% | North America and Europe legal jurisdictions, licensing friction in Asia Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cyclical Volatility in PC Shipments

Global PC unit volumes grew just 2.7% in 2024 after two successive contraction years, highlighting how sensitive peripheral attachment rates are to refresh cycles. Enterprises extended laptop lifetimes from a typical four to six years during budget freezes, slowing purchases of docks, hubs, and external monitors that embed interface logic. Consumer demand also remained erratic; European spending on gaming peripherals fell 8% during H1 2024 amid inflation pressures. Such swings produce lumpy order books for IC vendors, forcing cautious wafer starts that may miss surges if the market rebounds faster than forecast. Although AI-PC refresh programs could smooth demand in 2026-2027, the near-term drag trims market CAGR by an estimated 1.4 percentage points.

Supply Chain Disruptions in Advanced Node Foundries

TSMC’s Arizona fab entered 4 nm pilot output in Q2 2024, yet yields lag mature Taiwan lines by 15-20%, extending lead times on complex USB4 retimers to 18-22 weeks. Samsung’s 3 nm gate-all-around process similarly battled yield noise that pushed customer tape-outs back as much as nine months. Concentration of advanced nodes in seismic-prone Taiwan heightens risk; a magnitude 6.4 quake shuttered multiple fabs for inspection in April 2024. These bottlenecks compel fabless vendors to dual-source on older nodes, raising die size and cost while delaying new-generation controller launches, cutting projected CAGR by roughly 1.1 percentage points.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Custom ASIC Momentum Offsets Commoditization Pressure

Interface controllers remained the largest revenue contributor in 2024, holding 39.12% share, yet their average selling price keeps slipping because USB hub and card-reader designs rely on standardized PHY blocks. Custom ASICs stand out, expanding at a 9.87% CAGR, because gaming and industrial customers crave proprietary latency, security, or ruggedization features that generic chips lack. ODMs leverage multi-project wafers at 28 nm to prototype in under 16 weeks, shrinking time-to-market. Power-management ICs integrate USB-C negotiation, buck-boost regulation, and battery charging in single packages, enabling ultrathin docks that still deliver 100 W to laptops. Connectivity silicon comprising Ethernet PHYs and Wi-Fi controllers serves niche gateways where extended temperature ranges allow premium pricing. Razer’s dedicated wireless-dongle SOC bundles encryption keys with frequency-hopping logic and remains incompatible with rival accessories, protecting aftermarket revenue. Parade Technologies’ DisplayPort 2.1 retimer ASIC introduced adaptive equalization for three-meter cables, expanding conference-room addressable markets. The computer and peripherals special purpose logic IC market size for custom ASICs is therefore projected to grow faster than the sector average as vendors seek stickier differentiation.

Semiconductor houses now offer firmware-upgradable packet parsers, so OEMs can toggle between USB4 and Thunderbolt modes without hardware spins. Interface controllers anchored to tightly managed reference designs enable cheap, rapid certification but limit unique value, encouraging migration to semi-custom variants. Power IC suppliers add gallium-nitride gate drivers that lift efficiency to 96% at 240 W, making single-cable workstations possible. Connectivity suppliers embed hardware root-of-trust blocks that satisfy USB-C authentication requirements, unlocking medical and payment-terminal sockets that carry higher gross margins. Collectively, these trends sustain a price mix that stabilizes the computer and peripherals special purpose logic IC market even as unit growth plateaus in mature consumer categories.

By Application: Storage Leads on PCIe Gen5 but Docking Solutions Gain Hybrid-Work Tailwinds

Storage peripherals accounted for 35.78% revenue in 2024 and will grow at a 9.93% CAGR as enterprises roll out Gen5 NVMe arrays. Phison’s PS5026-E26 achieves 14.5 GBps reads double Gen4, demanding low-jitter clock generators and multi-lane redrivers per drive. External SSD enclosures with USB4 bridges now match Thunderbolt 3 performance at lower bill-of-materials cost, expanding consumer uptake. Printing devices lose share because digitized workflows reduce office printer fleets by high single-digits annually. Input devices such as high-end mechanical keyboards and esports mice integrate RGB lighting and polling ASICs that cost several dollars per unit, cushioning revenue despite volume stagnation. Display and docking solutions ride hybrid-work demand; companies outfit employees with two-monitor hot-desking setups that need multi-protocol hub controllers combining USB, DisplayPort, and Ethernet on one die. Consequently, the computer and peripherals special purpose logic IC market share for storage stays foremost yet the incremental dollar opportunity migrates to docks where controller content rises 20% per unit.

Thunderbolt 5 docks that support 80 Gbps require dual retimers plus lane-multiplexing FPGAs, doubling controller dollar content over USB-C Gen2 designs. DisplayPort 2.1 alternate-mode integration heightens complexity, adding equalizers to combat cable losses. On the storage side, enterprise IT budgets favor compression-enabled controllers because they defer costly rack expansions. Consumer creators adopt bus-powered enclosures that draw 15 W via USB Power Delivery, eliminating bulky adapters and stimulating adoption of integrated power-negotiation ASICs. As both corporate and consumer spending patterns converge on high-throughput, single-cable solutions, controller attach rates gain resiliency, ensuring the computer and peripherals special purpose logic IC market continues to register healthy top-line growth.

By Device Type: Industrial Logic Sustains Double-Digit Momentum

Consumer peripherals retained 47.89% revenue in 2024, but saturation in developed economies and lengthening PC lifecycles temper volume growth. In contrast, industrial and embedded peripherals post a 9.78% CAGR because factories retrofit IO-Link sensors and time-sensitive networking gateways. Commercial peripherals, which span conference-room equipment and network-attached storage deliver steady mid-single-digit growth as hybrid-work policies settle into steady-state refresh intervals. The computer and peripherals special purpose logic IC market size tied to industrial peripherals benefits from longer product lifetimes and high ASPs due to wide temperature and longevity requirements.

Edge AI gateways bundle multi-protocol bridges so factories can add Ethernet-based sensors without ripping legacy CANopen or Modbus wiring, boosting semiconductor value per gateway by 35-45%. Automotive plants piloting time-sensitive networking lowered cycle-time variance 18%, validating the business case for deterministic Ethernet interfaces. Such proof points accelerate adoption, keeping industrial revenue streams less cyclical than consumer accessory sales. The upshot is that industrial units, though smaller in volume, generate a rising share of the computer and peripherals special purpose logic IC market’s gross profit.

By End User Industry: Healthcare Connectivity Mandates Drive Fastest Uptake

Consumer electronics still produce 42.37% of 2024 demand because every smartphone, tablet, and laptop now integrates USB-C ports and Qi chargers needing power-management controllers. Healthcare equipment, however, grows fastest at 9.96% because regulators demand encrypted, interoperable USB-C ports on imaging systems and patient monitors. The U.S. FDA’s March 2024 cybersecurity guidance obliges medical-device OEMs to authenticate chargers and cables, forcing adoption of controllers with hardware root-of-trust blocks.

GE HealthCare integrated Thunderbolt 4 into ultrasound carts, cutting radiologist file-transfer wait times by 50%. Industrial automation users upgrade RS-485 networks to Ethernet, increasing controller spending, while IT and telecom customers buy PCIe Gen5 bridge chips for new servers. All together, healthcare’s compliance-driven purchases plus industrial modernization fuel the highest incremental growth pockets inside the computer and peripherals special purpose logic IC market.

Geography Analysis

Asia Pacific captured 34.38% revenue in 2024, anchored by Taiwan-based controller specialists that collectively shipped 28% of global USB hub silicon. China’s state-backed National Integrated Circuit Industry Fund underwrites domestic retimer projects, narrowing reliance on imports. Japan’s Rapidus began constructing a 2 nm fab slated for 2027, a strategic move to cut dependence on Taiwanese supply. South Korea focuses more on HBM and advanced packaging than interface logic, yet Samsung Foundry’s progress on 3 nm gate-all-around transistors provides an alternate node for high-speed PHYs. India’s chip incentives draw assembly proposals but wafer-fab projects remain nascent.

The Middle East is the fastest-growing sub-region at a 10.11% CAGR, propelled by Saudi Arabia’s USD 6.4 billion semiconductor design center and the UAE’s Tier IV data centers that specify PCIe Gen5 SSDs and 400 GbE switches. High-speed interconnect requirements lift controller content per rack by as much as 50%.

North America and Europe exhibit mature but stable demand. U.S. enterprises refreshing laptops for Windows 11 and AI workflows sustain sizable orders for USB-C docks. Germany’s automotive OEMs specify USB4 infotainment links, opening sockets for European vendors such as Infineon and STMicroelectronics. South America remains limited in scale, though Brazil earmarked USD 250 million for fabless startups. Africa sees groundwork for future design talent through Intel’s Cairo center. Together, these regional nuances shape allocation of the computer and peripherals special purpose logic IC market investment through 2030.

Competitive Landscape

The market remains moderately concentrated, with the top five suppliers—Broadcom, Texas Instruments, Analog Devices, Infineon Technologies, and NXP Semiconductors—collectively holding roughly 45% revenue in 2024. Their scale lets them integrate interface logic with power-management ICs, offering turnkey reference designs. Taiwanese specialists, however, erode share by pricing USB4 and Thunderbolt 5 controllers 25-30% lower. White-space opportunities exist in industrial Ethernet bridges where legacy RS-485 equipment transitions toward deterministic networking.

ASMedia’s USB4 Version 2.0 controller samples at 80 Gbps and operates over passive 0.8 m cables, eliminating retimers in many laptop docks and trimming bill-of-materials cost. Parade Technologies filed 14 DisplayPort 2.1 patents in 2024, providing potential royalty leverage. Realtek’s recall of USB-C hub silicon after data-corruption incidents underlines how compliance failures can damage reputation and open doors for challengers.

Broadcom expanded its European footprint by acquiring a Munich-based IP portfolio in January 2025, reinforcing automotive infotainment ambitions. Texas Instruments began volume production of the first domestically fabricated USB4 redriver at its Texas wafer plant in December 2024. Analog Devices paired with TSMC on a 5 nm gallium-nitride PMIC, merging analog precision with digital integration. These moves collectively sustain robust R&D pipelines, ensuring continual innovation and shaping competitive dynamics inside the computer and peripherals special purpose logic IC market.

Computer And Peripherals Special Purpose Logic IC Industry Leaders

Broadcom Inc.

Texas Instruments Incorporated

Analog Devices, Inc.

Infineon Technologies AG

NXP Semiconductors N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Genesys Logic enlarged its Hsinchu design center by 15,000 square feet, adding capacity for 120 engineers focused on USB4 Version 2.0 hub controllers and card-reader ICs targeting gaming peripheral and content-creation markets.

- March 2025: Parade Technologies received the Taiwan Excellence Award for its PS8830 USB4 retimer IC, which extends cable reach to 3 meters through adaptive equalization and supports full 80 Gbps bandwidth without signal degradation.

- February 2025: ASMedia Technology entered a strategic partnership with a Japanese electronics conglomerate to co-develop USB4 Version 2.0 controllers optimized for industrial cameras and machine-vision systems requiring deterministic latency below 10 microseconds.

- January 2025: Broadcom announced the acquisition of a portfolio of interface controller IP assets from a European fabless vendor, expanding its DisplayPort and HDMI lines for USB-C docking stations and reinforcing its automotive infotainment presence.

Global Computer And Peripherals Special Purpose Logic IC Market Report Scope

The Computer and Peripherals Special Purpose Logic IC Market Report is Segmented by Product Type (Interface Controllers, Power Management ICs, Connectivity and Networking ICs, Custom ASICs for Peripherals), Application (Printing Devices, Storage Peripherals, Input Devices, Display and Docking Solutions), Device Type (Consumer Peripherals, Commercial and Enterprise Peripherals, Industrial and Embedded Peripherals), End User Industry (Consumer Electronics, Information Technology and Telecom, Industrial Automation, Healthcare Equipment), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

| Interface Controllers |

| Power Management ICs |

| Connectivity and Networking ICs |

| Custom ASICs for Peripherals |

| Printing Devices |

| Storage Peripherals |

| Input Devices |

| Display and Docking Solutions |

| Consumer Peripherals |

| Commercial and Enterprise Peripherals |

| Industrial and Embedded Peripherals |

| Consumer Electronics |

| Information Technology and Telecom |

| Industrial Automation |

| Healthcare Equipment |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Product Type | Interface Controllers | ||

| Power Management ICs | |||

| Connectivity and Networking ICs | |||

| Custom ASICs for Peripherals | |||

| By Application | Printing Devices | ||

| Storage Peripherals | |||

| Input Devices | |||

| Display and Docking Solutions | |||

| By Device Type | Consumer Peripherals | ||

| Commercial and Enterprise Peripherals | |||

| Industrial and Embedded Peripherals | |||

| By End User Industry | Consumer Electronics | ||

| Information Technology and Telecom | |||

| Industrial Automation | |||

| Healthcare Equipment | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

How large is the computer and peripherals special purpose logic IC market in 2025?

The computer and peripherals special purpose logic IC market size stands at USD 18.76 billion in 2025.

What is the expected CAGR through 2030?

The market is projected to expand at a 9.06% CAGR from 2025 to 2030.

Which product category grows fastest?

Custom ASICs for peripherals lead with a 9.87% CAGR because gaming and industrial vendors seek proprietary features.

Which geographic region shows the highest growth?

The Middle East achieves the fastest regional growth with a 10.11% CAGR as Saudi Arabia and the UAE invest in data centers.

Why are data centers important to controller demand?

Hyperscale operators moving to PCIe Gen5 SSDs require high-speed NVMe controllers and redrivers, boosting unit demand and average selling prices.

How does the EU charger mandate influence IC sales?

The 2024 USB-C directive forces vendors to adopt USB Power Delivery 3.1 controllers, lifting semiconductor content per peripheral device.

Page last updated on: