Chipless RFID Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

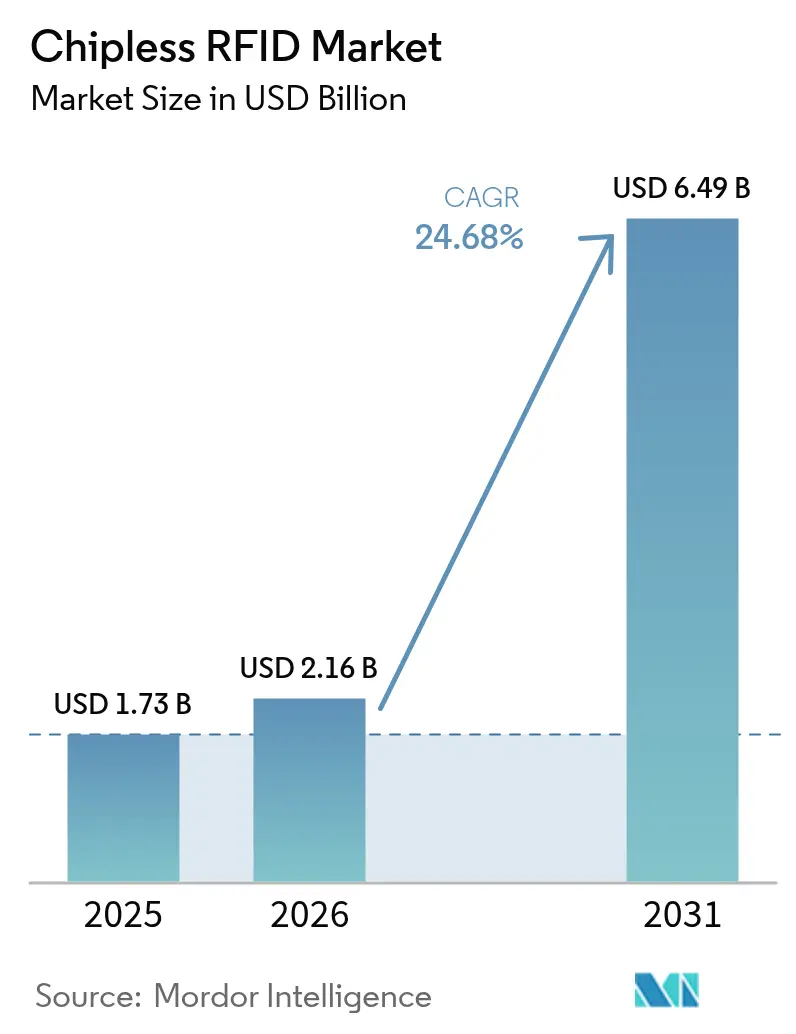

| Market Size (2026) | USD 2.16 Billion |

| Market Size (2031) | USD 6.49 Billion |

| Growth Rate (2026 - 2031) | 24.68% CAGR |

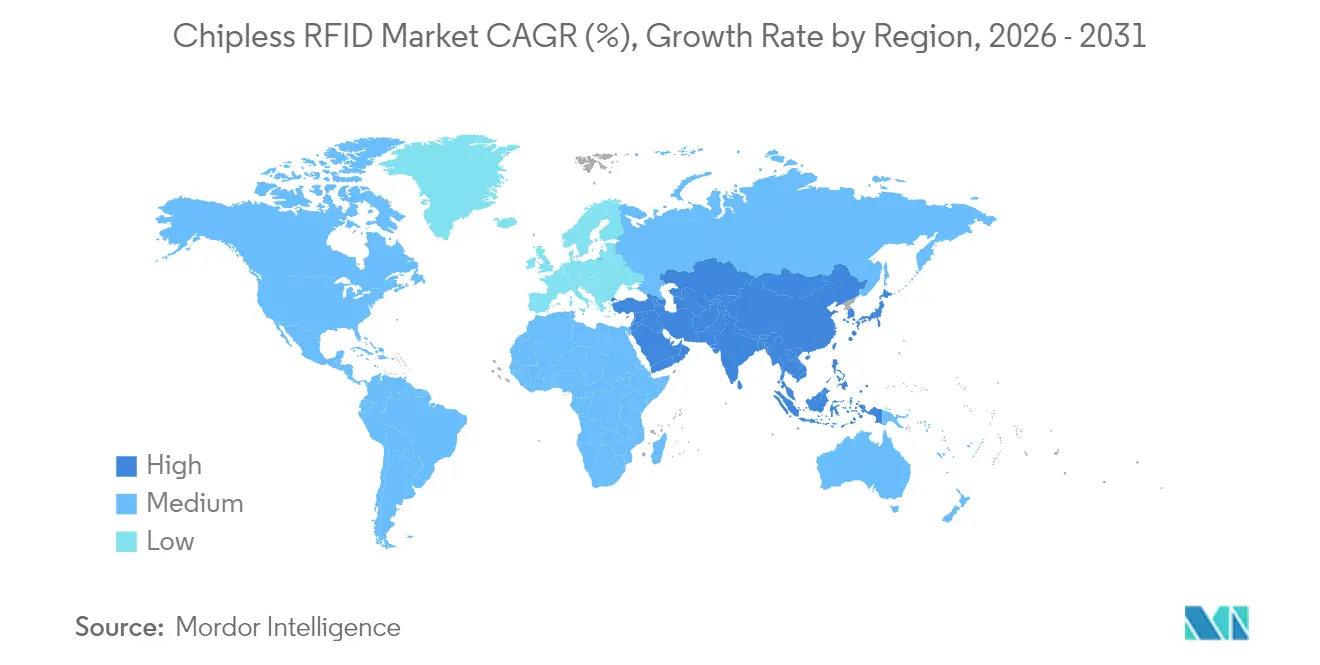

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Chipless RFID Market Analysis by Mordor Intelligence

The chipless RFID market size was valued at USD 1.73 billion in 2025 and estimated to grow from USD 2.16 billion in 2026 to reach USD 6.49 billion by 2031, at a CAGR of 24.68% during the forecast period (2026-2031). Demand acceleration stems from fast-moving consumer-goods packaging in Asia, stricter authentication regulations in Europe and the Middle East, and advances in printable conductive inks that have cut per-tag manufacturing costs below USD 0.05. Leadership in low-cost authentication solutions, longer read-range antenna designs, and passive temperature-sensing features is reshaping competitive priorities. Suppliers are expanding vertically into inks, substrates, and middleware in order to safeguard margins and offer one-stop solutions. Convergence with blockchain and cold-chain monitoring platforms is opening additional revenue streams in regulated industries.

Key Report Takeaways

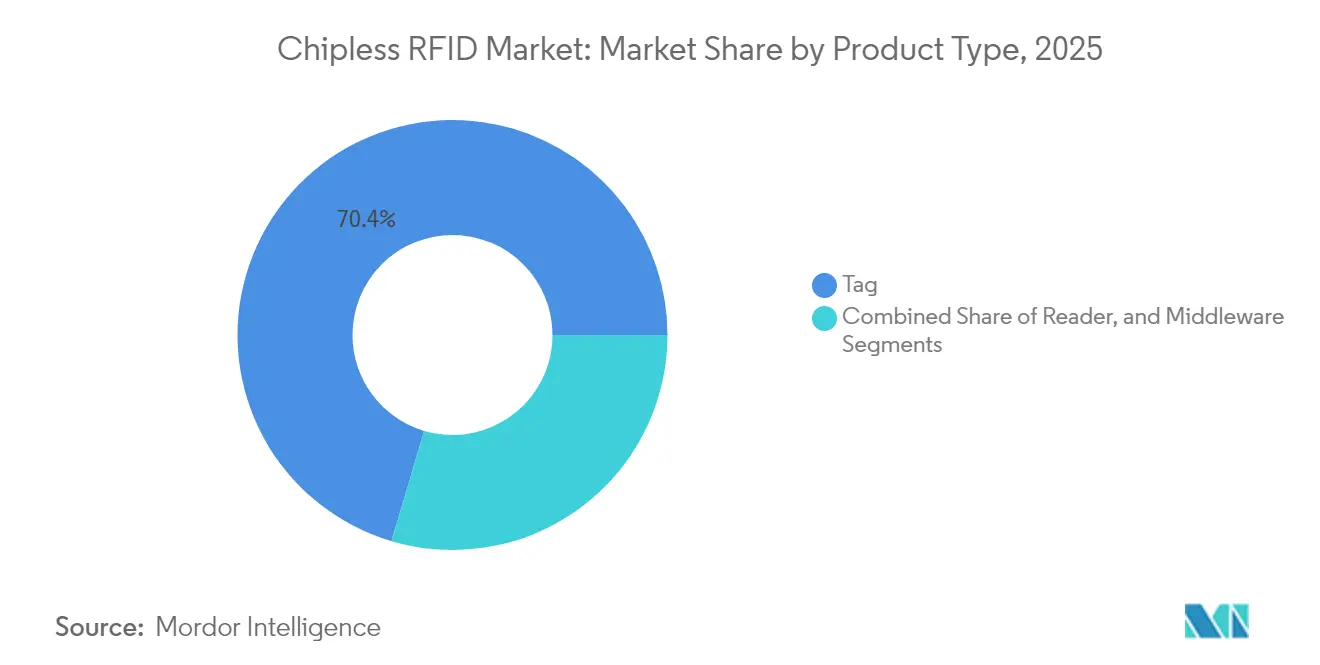

- By product type, tags held 70.42% of the chipless RFID market share in 2025, while middleware is projected to expand at a 26.05% CAGR to 2031.

- By printing technology, screen printing led with 37.35% revenue share in 2025; ink-jet printing is forecast to advance at a 27.15% CAGR through 2031.

- By operating frequency, HF commanded 51.25% share of the chipless RFID market size in 2025, whereas UHF is expected to grow at 26.6% CAGR during 2026-2031.

- By material, silver-nano inks accounted for 61.10% of the chipless RFID market size in 2025; graphene-based inks record the highest projected CAGR at 27.4% to 2031.

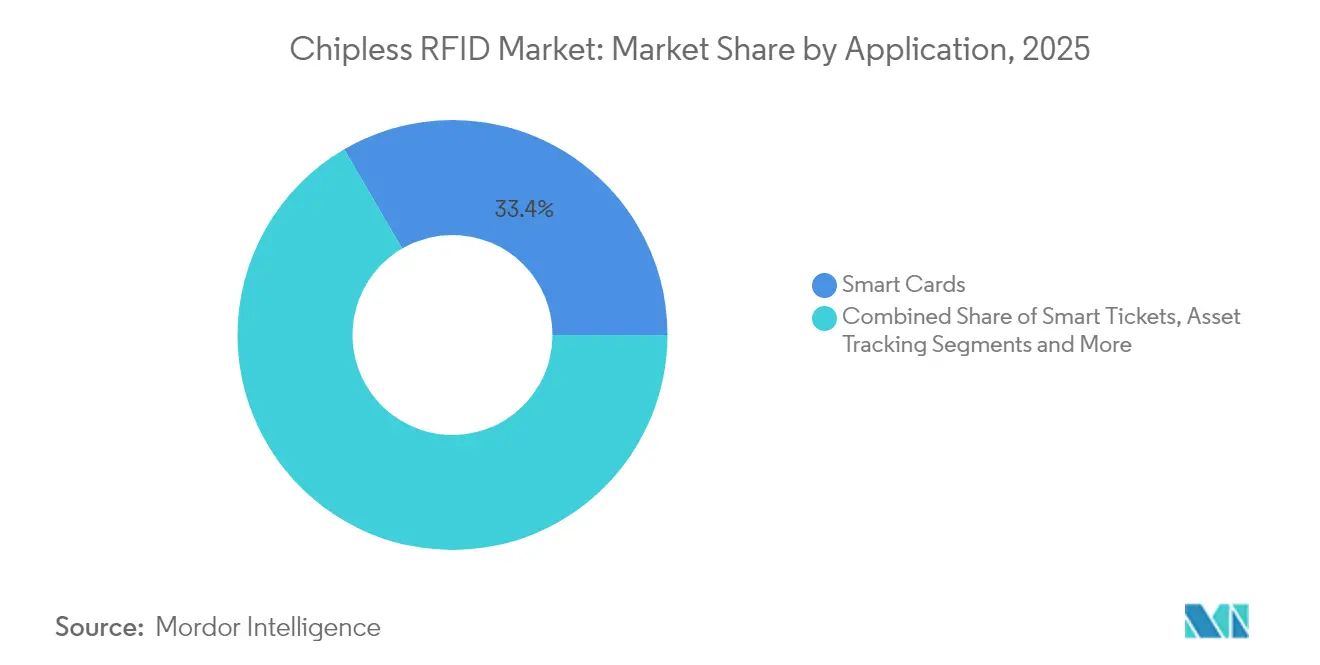

- By application, smart cards captured 33.40% of the chipless RFID market size in 2025, and brand & document authentication is accelerating at a 27.55% CAGR to 2031.

- By end-user industry, retail held 28.55% revenue share in 2025; healthcare & pharmaceuticals is forecast to expand at a 29.0% CAGR through 2031.

- By geography, Asia Pacific owned 39.30% of the chipless RFID market size in 2025, while the Middle East & Africa is poised for the highest regional CAGR at 26.9% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Chipless RFID Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lower-cost Mass-production of IC-less Tags in Asian FMCG Packaging | +6.2% | Asia Pacific core, spill-over to global FMCG | Medium term (2-4 years) |

| Government Excise/Tax-stamp Mandates (EU Counter-feiting) | +4.8% | Europe & Middle East, expanding to emerging markets | Long term (≥ 4 years) |

| Printable Conductive-Ink Advances in North American Label Converting | +5.1% | North America & EU, technology transfer to APAC | Short term (≤ 2 years) |

| Passive Sensor Adoption for Cold-chain Healthcare Logistics | +3.9% | Global, with concentration in developed markets | Medium term (2-4 years) |

| Banknote & Secure-Document Authentication Demand (Middle East) | +2.7% | Middle East & Africa, selective adoption globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Lower-cost Mass Production of IC-less Tags in Asian FMCG Packaging

Manufacturers in China and Southeast Asia have combined flexible substrates with silver-nano paste to reach sub-5-cent tags, positioning the chipless RFID market for high-volume adoption in consumer-goods multipacks. Contract printers are running multi-lane flexographic lines at speeds above 120 m/min, allowing over 2 billion units per plant annually. Fast payback on retrofits and geographic proximity to packaging converters accelerate uptake. Suppliers are piloting recyclable cellulose substrates to align with brand sustainability targets. As costs fall, single-use tags are extending into disposable electronics and unit-dose pharmaceutical packs.

Government Excise / Tax-stamp Mandates

EU loss estimates of EUR 16 billion (USD 17.3 billion) in counterfeited goods prompted Directive 2024/1640, which endorses tamper-evident identifiers with unique RF signatures.[1]European Union Intellectual Property Office, “Economic Impact of Counterfeiting in the Clothing, Cosmetics, and Toy Sectors in the EU,” euipo.europa.eu Ministries of finance in Italy, Spain, and Saudi Arabia now specify chipless formats for alcohol and tobacco stamps so printers can embed security in a single press pass. Long-run contracts incentivise end-to-end traceability platforms and open replacement cycles for high-resolution readers. Similar legislation is under review in ASEAN, suggesting a second wave of demand by 2028.

Printable Conductive-Ink Advances in North American Label Converting

Silver nanoparticle and graphene hybrid inks have reached sheet resistances below 10 mΩ/□ at 80 °C sintering, enabling narrow-line antennas printed on standard BOPP labels without separate ovens. [2]Tamara Tomašegović et al., “Fine-Tuning Flexographic Ink’s Surface Properties,” doi.orgUS converters integrate digital front ends that switch from CMYK to conductive layers within the same job queue, lowering downtime. Partnerships with ink makers secure exclusive formulations, creating entry barriers. The approach reduces capex for new players yet raises intellectual property complexity that favours incumbents with patent portfolios.

Passive Sensor Adoption for Cold-chain Healthcare Logistics

Copper-doped ionic-liquid sensors link temperature excursions directly to a tag’s phase response, producing an immutable history for biologics during transit. Global distributors integrate GS1 EPCIS event structures, allowing regulators to audit chain-of-custody in near real time. [3]GS1 US, "Standards & Sensors for Visibility in the Pharmaceutical Cold Chain," documents.gs1us.org Hospitals receive automated alerts through existing RFID gateways, avoiding active data loggers and batteries. The cost profile fits vaccine campaigns and cell-therapy shipments, while blockchain pilots aim to secure data integrity.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Read Range vs. Chipped UHF Systems | -3.4% | Global, particularly in logistics applications | Short term (≤ 2 years) |

| Absence of Harmonised ISO/IEC Encoding Standards | -2.1% | Global, with regional variation in adoption | Long term (≥ 4 years) |

| Retrofit Cost of Reader Infrastructure | -1.8% | Developed markets with existing RFID infrastructure | Medium term (2-4 years) |

| Moisture & Abrasion Vulnerability of Printed Antennas | -1.2% | Global, with higher impact in harsh environments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Limited Read Range versus Chipped UHF Systems

Chipless tags typically peak at 3 m in free air, compared with over 10 m for chipped UHF tags, forcing warehouses to increase reader density, which can double infrastructure budgets. Multi-layer metamaterial antennas now in prototype add 40% range, yet metallic racks and liquid contents still attenuate signals. Integrators respond with zone-based portals and hybrid deployments, reserving chipless tags for package-level items while pallets continue to carry chipped inlays.

Absence of Harmonised ISO / IEC Encoding Standards

Proprietary encoding schemes fragment middleware development and complicate cross-border shipments. Retailers running multi-supplier imports must map five or more tag signatures into a single ERP instance. Industry groups work on a unifying data model, but spectrum coordination challenges in the 860-960 MHz range delay ratification. Until a standard is formalised, large buyers hedge by dual-sourcing or favour vendors with open-source firmware.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Tags Remain Core While Middleware Gains Ground

Tag sales generated 70.42% of 2025 revenue, underscoring their indispensability across every deployment scenario in the chipless RFID market. Asian contract printers leverage scale to drive unit costs down, while European security printers focus on high-value authenticators. Middleware revenues, although smaller today, are set to climb faster at a 26.05% CAGR because enterprises require cloud connectors, data cleansing, and analytics to turn raw RF echoes into actionable dashboards.

Accelerated middleware growth alters bargaining power; software vendors now influence hardware design road maps and push for open APIs. As a result, tag manufacturers invest in data-services teams to defend share. The trend positions middleware as a gatekeeper for future functionality such as predictive maintenance and AI-based signature matching.

By Printing Technology: Ink-jet Precision Challenges Screen Dominance

Screen printing held a 37.35% share in 2025 thanks to long-run productivity and mature supply chains, especially within food and beverage packaging. The chipless RFID market now sees ink-jet processes expanding at 27.15% CAGR because droplet-on-demand heads create fine-line antennas suitable for high-density signature encoding.

Ink-jet adoption also supports on-site customisation. Brand owners can print limited-edition authenticity marks days before product launch, cutting obsolescence risk. Screen lines keep their advantage in very high-volume SKUs where tooling amortisation offsets changeover costs. Hybrid lines that start with screen for ground planes and finish with ink-jet for micro-antennas are gaining traction, reflecting a transition phase rather than outright displacement.

By Operating Frequency: UHF Momentum Builds Behind HF Install Base

HF frequencies dominated with 51.25% of 2025 revenue because payment, ticketing, and secure access ecosystems already employ 13.56 MHz readers. UHF, however, is forecast to rise at 26.6% CAGR as antenna breakthroughs mitigate near-metal detuning and extend read windows beyond 5 m, crucial for warehouse portals.

Dual-frequency tags are emerging; they carry HF for consumer NFC interactions and UHF for logistics checkpoints, helping brand owners justify a single label across the product life cycle. LF maintains niche roles in livestock tracking and liquid-filled container identification where penetration depth outweighs data-rate needs.

By Material: Silver-Nano Leads Yet Graphene Advances

Silver-nano inks supplied 61.10% of antenna coatings in 2025 owing to unmatched conductivity and compatible curing profiles. The chipless RFID market is witnessing rapid progress in graphene and carbon nanotube alternatives that target cost and sustainability concerns. Graphene prints drop silver loading by up to 80%, lowering exposure to price volatility while reducing environmental impact.

Copper formulations cater to disposable tags in ultra-high-volume retail units where brief shelf life overshadows oxidation risks. Material selection is now part of corporate ESG scorecards, compelling suppliers to document lifecycle carbon footprints and recycling pathways.

By Application: Smart Cards Hold Lead While Authentication Surges

Smart cards contributed 33.40% of 2025 revenue, benefiting from ongoing EMV migration and mass transit upgrades. Authentication applications, however, will outpace all others at a 27.55% CAGR as governments and brands confront counterfeiting losses. MIT-developed terahertz-encoded tags promise forensic-grade security levels suitable for luxury goods and pharmaceuticals.

Diversification into asset tracking and smart tickets widens the total addressable demand. Bundled offerings that include cloud dashboards and mobile readers lower entry barriers for small and mid-sized enterprises that lack internal RFID expertise.

By End-user Industry: Retail Leads, Healthcare Accelerates

Retail and e-commerce retained a 28.55% share in 2025. Grocery chains in North America demonstrated inventory-shrink reduction after deploying paper-based chipless labels at the item level. Healthcare & pharmaceuticals, poised for a 29.0% CAGR, benefit from mandatory cold-chain tracking rules and rising biologic therapy volumes.

Logistics operators integrate disposable chipless tags for last-mile parcels, complementing reusable chipped tags on pallets. Government agencies test chipless identifiers for national ID programs, while BFSI firms evaluate document security use cases.

Geography Analysis

Asia Pacific led the chipless RFID market with 39.30% revenue in 2025. China’s converters run integrated screen and flexographic lines, serving domestic and export FMCG brands, while Japanese rail operators extend RFID-enabled fare systems to rural routes. Australia’s postal service is trialling chipless tags on cross-border parcels to cut declaration fraud. Regional governments co-fund research into biodegradable substrates, aligning with zero-plastic directives.

North America follows with strong intellectual-property portfolios and an early-adopter customer base in healthcare and aerospace. Universities collaborate with start-ups to commercialise graphene inks, and federal grants support secure supply chains for biologics and critical spare parts. Supermarket chains deploy chipless tags to reduce perishables wastage and tie item-level data into ESG reporting.

Europe ranks third yet posts steady gains driven by anti-counterfeiting mandates. Tax-stamp programs in Italy and Poland stipulate chipless RF security layers. Nordic packaging firms integrate paper inlays to meet circular-economy targets, and German machine builders ship modular ink-jet heads to Asian OEMs. The Middle East & Africa region, while smaller today, is the fastest growing; GCC central banks standardise banknote RF authentication and South African customs rolls out chipless seals on high-value exports.

Competitive Landscape

The chipless RFID market shows moderate fragmentation. The top five players control about 45% of global revenue through integrated portfolios that span inks, substrates, antenna IP, and middleware. Avery Dennison leverages materials expertise to secure multi-year agreements with grocery and apparel leaders, while Impinj invests in reader chipsets that interpret both chipped and chipless signatures, anchoring an ecosystem lock-in effect.

Emerging entrants concentrate on graphene and metal-compatible antenna architectures, often licensing patents from university labs. These challengers form joint ventures with regional converters to gain scale without heavy capex. M&A activity targets software and analytics specialists, evident in the Seagull-Mojix merger that created an end-to-end visibility stack.

Strategic road maps emphasise sustainability credentials, with players marketing plastic-free inlays and low-energy curing processes. Intellectual-property assertions rise, especially around ink chemistries and dual-frequency structures. Large buyers mitigate vendor risk by insisting on escrowed manufacturing files and performance warranties.

Chipless RFID Industry Leaders

-

Alien Technology Corporation

-

Zebra Technologies Corporation

-

Avery Dennison Corporation

-

SATO Holdings

-

Smartrac Technology

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Impinj reported USD 366.1 million revenue for 2024, up 18%, and highlighted deployment synergies between RAIN and chipless platforms.

- January 2025: Avery Dennison partnered with Kroger to extend item-level RFID in grocery aisles, targeting waste cuts and inventory accuracy gains.

- October 2024: Trimco Group launched PaperMark, a plastic-free RAIN inlay made from FSC-certified paper, spotlighting market pivot toward sustainable substrates

- October 2024: Seagull merged with Mojix to deliver end-to-end traceability software that complements low-cost chipless identifiers

Global Chipless RFID Market Report Scope

Chipless RFID (Radio Frequency Identification) is an emerging disruptive wireless technology for identification, tracking, and sensing. A chipless RFID tag does not contain an application specific integrated circuit (ASIC), hence the reader does all signal processing to read the tag. Chipless RFID tags are low-cost passive microwave/millimeter wave circuits where the information is stored in printable resonators and delay lines and typically implemented in flexible substrates such as polymers and papers, like optical barcodes.

| Tag |

| Reader |

| Middleware |

| LF (125-134 kHz) |

| HF (13.56 MHz) |

| UHF (860-960 MHz) |

| Silver-nano Ink |

| Copper-based Ink |

| Graphene/Carbon Ink |

| Smart Cards |

| Smart Tickets |

| Brand and Document Authentication |

| Asset Tracking |

| Retail and E-commerce |

| Healthcare and Pharmaceuticals |

| Logistics and Transportation |

| Banking, Financial Services and Insurance (BFSI) |

| Government and Public Sector |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Tag | |

| Reader | ||

| Middleware | ||

| By Operating Frequency | LF (125-134 kHz) | |

| HF (13.56 MHz) | ||

| UHF (860-960 MHz) | ||

| By Material | Silver-nano Ink | |

| Copper-based Ink | ||

| Graphene/Carbon Ink | ||

| By Application | Smart Cards | |

| Smart Tickets | ||

| Brand and Document Authentication | ||

| Asset Tracking | ||

| By End-user Industry | Retail and E-commerce | |

| Healthcare and Pharmaceuticals | ||

| Logistics and Transportation | ||

| Banking, Financial Services and Insurance (BFSI) | ||

| Government and Public Sector | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How fast is the chipless RFID market growing?

The chipless RFID market is projected to grow from USD 2.16 billion in 2026 to USD 6.49 billion by 2031 at a 24.68% CAGR.

Which region currently leads the chipless RFID market?

Asia Pacific leads with 39.30% revenue share in 2025 due to manufacturing scale and packaging demand.

What segment shows the quickest growth?

Brand & document authentication applications are expanding at 27.55% CAGR, driven by anti-counterfeiting regulations.

Why is middleware important in chipless RFID deployments?

Middleware translates raw RF signatures into actionable data, enabling analytics and system interoperability, and is forecast to grow at a 26.05% CAGR.

What is the primary technological restraint today?

Limited read range compared with chipped UHF systems reduces effectiveness in large warehouses, though antenna innovations are improving performance.

How are sustainability goals influencing material choices?

Brand owners increasingly favor graphene or paper-based inlays to cut precious metal usage and align with ESG commitments.

Page last updated on: