Chemotherapy-Induced Neutropenia Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

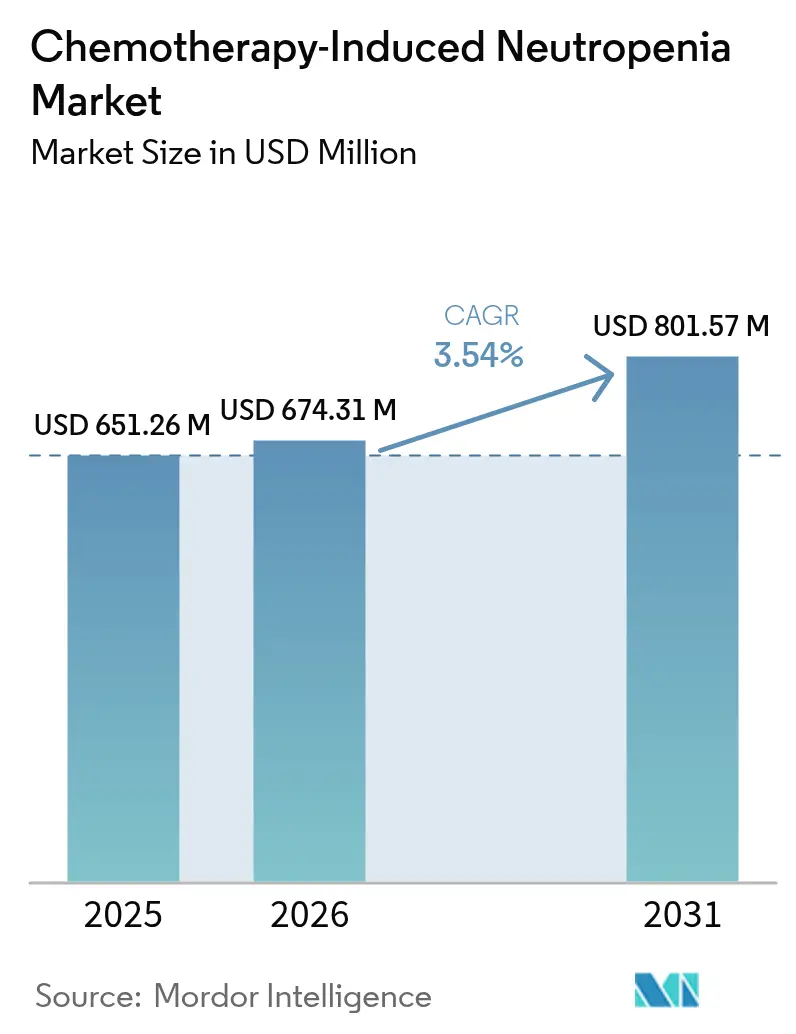

| Market Size (2026) | USD 674.31 Million |

| Market Size (2031) | USD 801.57 Million |

| Growth Rate (2026 - 2031) | 3.54% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Chemotherapy-Induced Neutropenia Market Analysis by Mordor Intelligence

The chemotherapy-induced neutropenia market size was valued at USD 651.26 million in 2025 and estimated to grow from USD 674.31 million in 2026 to reach USD 801.57 million by 2031, at a CAGR of 3.54% during the forecast period (2026-2031). Moderate expansion stems from the growing number of cancer patients who require myelosuppressive regimens, the steady roll-out of long-acting granulocyte colony-stimulating factors, and wider clinical uptake of predictive analytics that refine febrile neutropenia risk assessment. Although biosimilars continue to compress prices, regulatory approvals for differentiated products such as efbemalenograstim alfa offset margin pressure and maintain revenue growth drivers. The chemotherapy-induced neutropenia market now pivots on manufacturing reliability after multiple supply interruptions demonstrated the commercial importance of redundant facilities and robust quality controls. Parallel progress in outpatient oncology models and tele-pharmacy solutions supports geographic expansion as patients and payers increasingly prefer home-based prophylaxis options that reduce hospitalization costs.

Key Report Takeaways

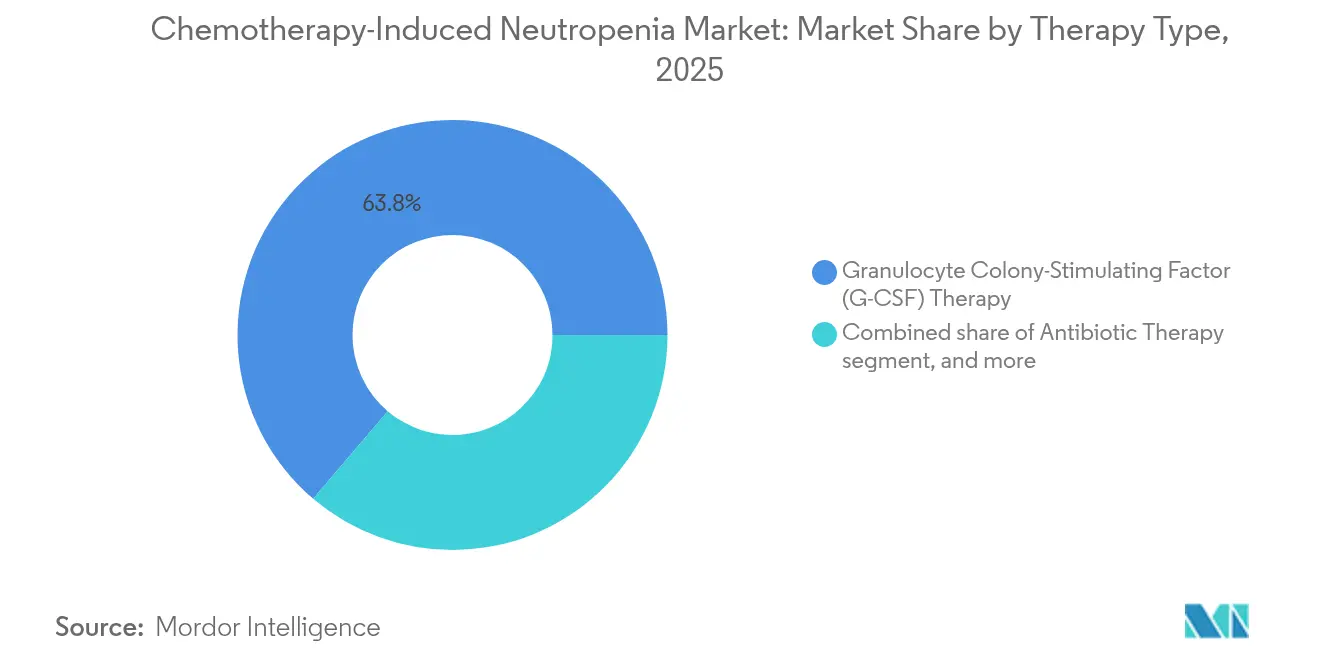

- By therapy type, granulocyte colony-stimulating factor commanded 63.78% of Chemotherapy-Induced Neutropenia market share in 2025, while granulocyte transfusion is advancing at a 5.21% CAGR through 2031.

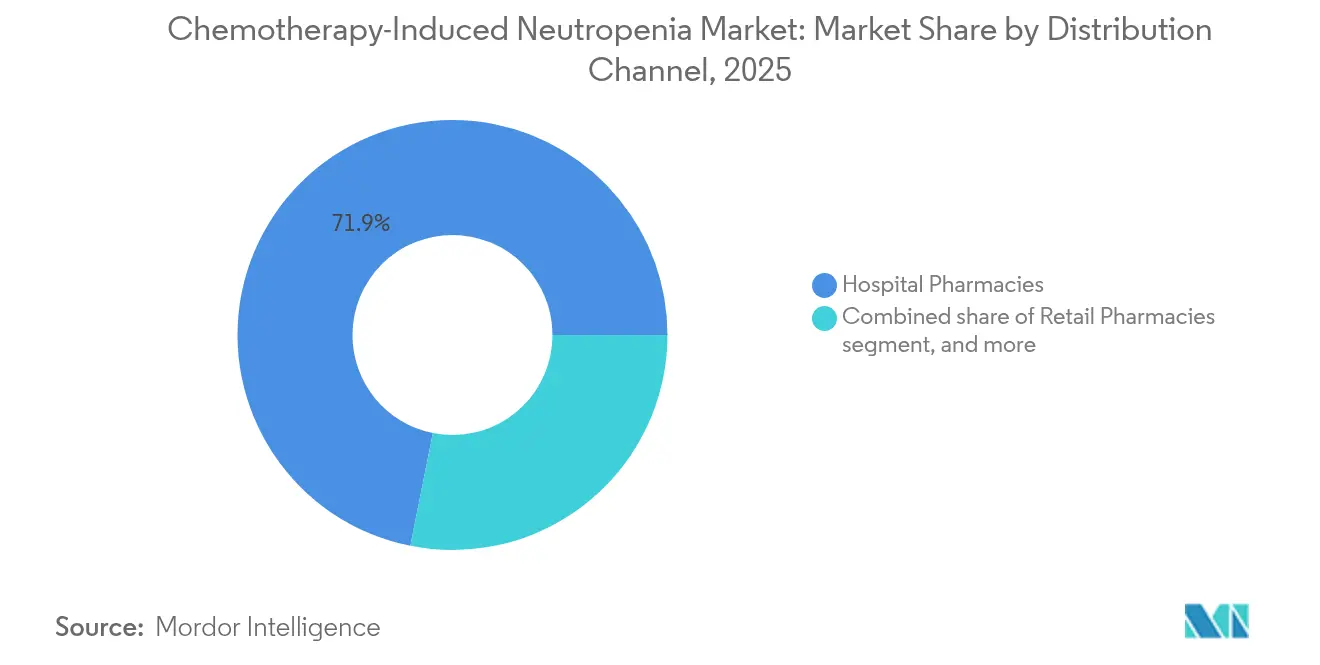

- By distribution channel, hospital pharmacies held 71.86% of the Chemotherapy-Induced Neutropenia market size in 2025, whereas online pharmacies record the fastest expansion at a 6.46% CAGR to 2031.

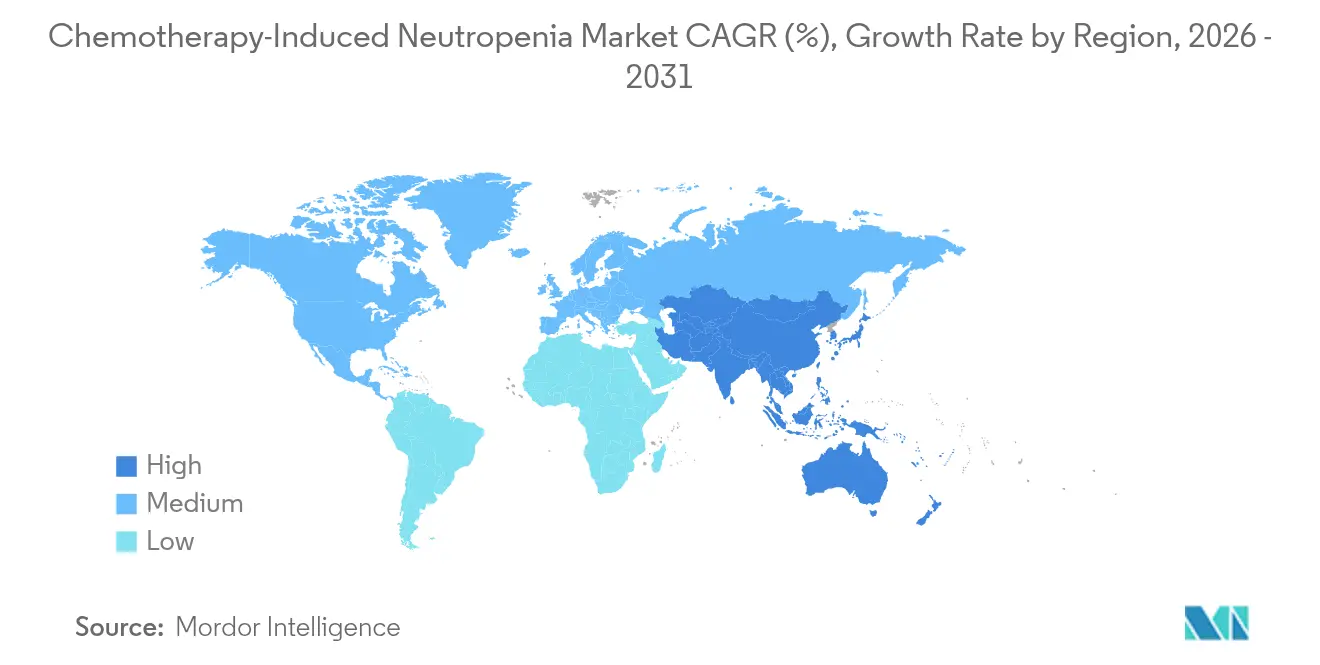

- By geography, North America led with 42.10% share in 2025 and Asia-Pacific is projected to increase at a 4.70% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Chemotherapy-Induced Neutropenia Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global cancer burden | +1.2% | Global with highest impact in Asia-Pacific | Long term (≥ 4 years) |

| Growing adoption of chemotherapy regimens | +0.8% | North America and Europe expanding to Asia-Pacific | Medium term (2-4 years) |

| Expanding access to biosimilar growth factors | +0.6% | Global, especially cost-sensitive markets | Short term (≤ 2 years) |

| Favorable clinical guidelines for prophylactic G-CSF | +0.4% | North America and Europe | Medium term (2-4 years) |

| Shift toward outpatient oncology care models | +0.3% | North America and Europe, early urban Asia-Pacific | Medium term (2-4 years) |

| Integration of predictive analytics for risk profiling | +0.2% | Technology-advanced markets in North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Global Cancer Burden

Higher incidence of solid tumors and hematologic malignancies raises demand for prophylactic supportive care. Acute myeloid leukemia treatment protocols that combine venetoclax with conventional 7+3 chemotherapy intensify myelosuppression, leading to more frequent G-CSF use. Aging populations in North America and Europe further enlarge the eligible patient base because elderly individuals carry increased risk for febrile neutropenia. In Asia-Pacific, adoption of Western-style dose-dense regimens expands addressable volumes as oncology capacity scales. Population-based screening programs also detect cancers earlier, allowing more patients to complete multi-cycle chemotherapy that necessitates prophylaxis. The Chemotherapy-Induced Neutropenia market therefore gains steady patient inflow even as overall chemotherapy utilization faces competitive pressure from immunotherapy.

Expanding Access to Biosimilar Growth Factors

Pegfilgrastim biosimilar average selling prices reached USD 2,050 compared with reference products above USD 3,600, reducing payer burden and unlocking treatment for under-insured patients. Streamlined FDA guidance that clarifies analytical similarity testing decreased review cycles by three months in 2024 and encouraged mid-size manufacturers to file abbreviated biologics license applications. Tanvex BioPharma’s filgrastim biosimilar won FDA approval and accessed a USD 403 million opportunity, illustrating the potential scale achievable through regulatory excellence. In Europe, interchangeability recommendations simplify substitution in hospital formularies and accelerate hospital tender volumes. Lower unit prices, paired with equivalent efficacy, strengthen the Chemotherapy-Induced Neutropenia market as payers authorize broader prophylaxis coverage.

Favorable Clinical Guidelines for Prophylactic G-CSF Use

The NCCN recommends primary prophylaxis when febrile neutropenia risk surpasses 20%, a threshold now reached by many modern regimens[1]NCCN, “Myeloid Growth Factors Guidelines,” nccn.org. European consensus statements similarly propose individualized risk models that integrate age, performance status, and comorbidities. The same-day administration paradigm gained validation through multi-center studies that documented no rise in infection events, thereby simplifying logistics. Japanese guidelines for acute myeloid leukemia formally incorporate long-acting G-CSF after consolidation cycles, raising standard-of-care expectations across Asia. Insurance reimbursement in the United States now mirrors guideline language, improving alignment between payers and prescribers and fortifying growth prospects for the Chemotherapy-Induced Neutropenia market.

Integration of Predictive Analytics for Neutropenia Risk Profiling

Machine-learning models using electronic health record data predicted febrile neutropenia with 97% accuracy and 93% sensitivity, allowing clinicians to target prophylaxis more precisely[2]Diego Garcia et al., “Machine-Learning Prediction of Febrile Neutropenia,” medrxiv.org. Adoption of these tools reduces overtreatment and optimizes scheduling of growth factors, especially in value-based care arrangements. Vendors now embed risk algorithms into oncology electronic prescribing modules, which simplifies clinician workflow and increases adherence to guideline-defined prophylaxis. Pharmaceutical companies partner with health-tech firms to offer integrated care pathways that pair biologics with analytics, reinforcing brand loyalty. As these models mature, they further stabilize volumes within the Chemotherapy-Induced Neutropenia market.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High treatment costs and reimbursement gaps | -0.8% | Global, strongly felt in emerging markets | Short term (≤ 2 years) |

| Stringent regulatory requirements for biologics | -0.4% | Global with variable local intensity | Medium term (2-4 years) |

| Declining chemotherapy utilization in IO era | -0.3% | Developed regions with rapid immunotherapy uptake | Long term (≥ 4 years) |

| Manufacturing capacity constraints for biologic APIs | -0.2% | Global with supply chain concentration risks | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Treatment Costs and Reimbursement Gaps

Average hospitalization cost for a febrile neutropenia episode reached USD 35,899 in 2024, placing a heavy burden on health systems. Patients in low-income countries confront out-of-pocket expenses exceeding annual household income. Although biosimilars reduce drug acquisition prices, ancillary costs such as infusion chair time and laboratory monitoring persist. Prior authorization processes delay therapy start by up to four days according to payer audits, potentially heightening infection risk. Charitable foundations fill financial gaps, yet lifetime maximums cap assistance at USD 2,200 per year, well below typical multi-cycle prophylaxis costs. These financial frictions temper the otherwise positive outlook for the Chemotherapy-Induced Neutropenia market.

Stringent Regulatory Requirements for Biologics and Biosimilars

An FDA biosimilar application requiring clinical data incurs USD 1.47 million in user fees, while post-approval pharmacovigilance adds further expense. Divergent dossier requirements among EMA, PMDA, and NMPA oblige manufacturers to run simultaneous regulatory tracks that elevate cost and stretch timelines. Maintaining cold-chain integrity and meeting global GMP audits tighten operational budgets, particularly for emerging market entrants. Although harmonization dialogues promise gradual alignment, near-term administrative complexity trims several basis points from the Chemotherapy-Induced Neutropenia market CAGR. Small developers sometimes license assets to regional partners instead of seeking global approvals, which fragments the competitive field.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Therapy Type: G-CSF Dominance Drives Innovation

G-CSF therapy generated the largest Chemotherapy-Induced Neutropenia market size contribution in 2025, accounting for 63.78% of revenues as hospitals adhere to evidence-based prophylaxis protocols. The product class includes filgrastim, pegfilgrastim, and efbemalenograstim alfa, each offering varying half-lives that align with different chemotherapy schedules. Competitive tendering in Europe fostered rapid biosimilar uptake, yet brand loyalty in on-body devices sustains premium segments. Long-acting agents reduce clinic visits and enhance adherence, which positions them favourably in value-based contracts. A pipeline of engineered variants aims to improve receptor affinity without raising bone pain incidence, indicating continued innovation within an already mature class.

Granulocyte transfusion, while niche, records the fastest CAGR at 5.21% through 2031 as gene-edited donor cells and ex-vivo expansion technologies overcome historical supply limitations. Pediatric oncology centres adopt high-dose transfusions for refractory infections that fail to respond to growth factors, thereby carving a unique clinical foothold. Academic collaborations investigate induced pluripotent stem cells to mass-produce functional neutrophils, an advance that could redefine supportive care. Antibiotic therapy remains an indispensable pillar, yet stewardship programs temper volume growth by encouraging de-escalation once cultures clear. Novel prophylactic agents such as trilaciclib aim to pre-empt neutropenia by transiently arresting bone-marrow cell cycling; positive phase III data sets the stage for commercial entry by 2027. Together, these sub-segments ensure a diversified and resilient Chemotherapy-Induced Neutropenia market.

By Distribution Channel: Digital Transformation Accelerates

Hospital pharmacies contributed 71.86% of Chemotherapy-Induced Neutropenia market size in 2025, anchored by integrated physician-pharmacy organisations that manage complex biologic logistics under one roof. Closed-door centralised locations streamline compounding, uphold cold-chain fidelity, and facilitate billing, which protects share despite the rise of external competitors. Oncology groups appreciate tighter control over formulary adherence and patient education that in-house settings provide.

Online pharmacies expand at a 6.46% CAGR on the strength of patient preference for doorstep delivery of specialty medicines and payer push for lower dispensing fees. Remote supervision protocols, including video-enabled injection training, assure safety and compliance. Legislative changes in several US states now permit biologic drop-shipping with temperature loggers, widening reach into rural markets. Retail pharmacies meet demand for oral supportive care, yet their share plateaus as biologics dominate revenue skew. Clinical home infusion companies partner with device makers to bundle on-body injectors with nursing services, an arrangement that reinforces direct-to-patient supply chains and reshapes competitive boundaries inside the Chemotherapy-Induced Neutropenia market.

Geography Analysis

North America delivered the largest regional revenue pool, holding 42.10% share of the chemotherapy-induced neutropenia market in 2025, propelled by broad insurance coverage and early adoption of long-acting biosimilars. Medicare reimbursement supports same-day G-CSF administration for qualifying regimens, which lowers infusion chair utilisation and supports outpatient growth. The region features advanced analytics that integrate electronic health records with risk algorithms, allowing oncologists to personalise prophylactic cycles and limit unnecessary spending. Amgen and Coherus maintain robust commercial infrastructure that secures high formulary presence across US hospital systems, while pharmaceutical benefit managers leverage biosimilar competition to negotiate lower price corridors.

Asia-Pacific represents the fastest expanding territory with a 4.70% CAGR to 2031. China approved Mabwell’s Mailisheng injection in 2025, adding a domestically produced long-acting G-CSF that reduces dependence on imports. Uptake of Western-style dose-dense chemotherapy grows across tier-2 cities, boosting prophylaxis volumes. Japan’s evidence-anchored guidelines encourage early G-CSF prophylaxis after intensive AML therapy, which solidifies class uptake. India and South-East Asia witness rising biosimilar penetration as government procurement favours cost-effective options for national cancer programmes. Tele-oncology services bridge geographic barriers, making remote G-CSF administration feasible in rural provinces.

Europe maintains a mature yet opportunity-laden environment where tender dynamics foster rapid micro-shifts in share between originators and biosimilars. The EMA approved Ryzneuta in 2024, adding a novel long-acting alternative that lengthens patient dosing intervals. National health services leverage central procurement to drive price deflation, benefiting budget sustainability but compressing margins. Eastern European countries with historically limited access to biologics adopt biosimilars at accelerated rates as reimbursement policies evolve. Latin America, the Middle East, and Africa still account for modest volumes, yet partnership models such as Teva’s Global HOPE programme improve paediatric oncology supportive care and lay groundwork for future chemotherapy-induced neutropenia market expansion.

Competitive Landscape

The chemotherapy-induced neutropenia market exhibits moderate consolidation with a top-five collective share hovering near 68%. Amgen leverages a diversified oncology portfolio and proprietary on-body injector technology to defend its leading position. Coherus BioSciences competes on value and recently won FDA approval for Udenyca Onpro, a five-minute injector that narrows the feature gap with Neulasta Onpro while undercutting on price. Sandoz continues to build a multi-region biosimilar footprint via aggressive tender strategies and broad product portfolios. Tanvex and Mabwell embody the rise of Asia-based challengers that rely on cost-efficient manufacturing, regulatory agility, and domestic procurement relationships.

Technology convergence sharpens competitive angles as players integrate remote monitoring devices, artificial intelligence risk tools, and digital companion apps. MIT’s Leuko device uses optical imaging to estimate white-blood-cell counts non-invasively and could pair with long-acting G-CSF to create a bundled adherence solution. Firms explore strategic partnerships, such as X4 Pharmaceuticals licensing Mavorixafor to Norgine for Europe and Oceania, broadening reach without diluting core focus. Horizontal mergers remain limited as regulators scrutinise biologic portfolio overlaps, yet supply chain collaborations flourish to ensure redundant drug substance capacity.

Manufacturing resilience emerges as a market differentiator after Covid-19 and isolated contamination events revealed vulnerabilities. Companies with dual sourcing and captive fill-finish lines gain purchasing preference from large group purchasing organisations. Innovative delivery devices further separate brands; retractable needle on-body systems and temperature-stable formulations promise lower nursing burden and higher patient satisfaction. Price competition intensifies, but differentiated service offerings and evidence-backed outcomes sustain profitability across the Chemotherapy-Induced Neutropenia market.

Chemotherapy-Induced Neutropenia Industry Leaders

Amgen, Inc.

Teva Pharmaceuticals Industries Ltd.

BeyondSpring Pharmaceuticals Inc

Aurobindo Pharma

Merck & Co.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Mabwell received Chinese NMPA approval for Mailisheng injection, a long-acting G-CSF for neutropenia prophylaxis.

- May 2025: Amgen reported USD 8.1 billion Q1 revenues, including USD 81 million from Japan launch of IMDELLTRA.

- March 2025: FDA cleared Coherus BioSciences’ Udenyca Onpro, the first Neulasta Onpro biosimilar.

- January 2025: Teva Pharmaceuticals Industries Ltd. and Alvotech announced FDA acceptance of AVT05 BLA, a proposed Simponi biosimilar.

- January 2025: X4 Pharmaceuticals licensed Mavorixafor to Norgine for Europe, Australia, and New Zealand commercialization.

Global Chemotherapy-Induced Neutropenia Market Report Scope

As per the report's scope, neutropenia is a condition in which the number of white blood cells (neutrophils) in the blood is reduced, lowering the body's ability to fight infections. Chemotherapy-induced neutropenia (CIN) is a common side effect of administering anticancer drugs. This adverse effect has been linked to life-threatening infections and can potentially change the chemotherapy regimen, affecting both short- and long-term outcomes. The Global Chemotherapy-Induced Neutropenia (CIN) Treatment Market is Segmented by Treatment (Antibiotic Therapy, Granulocyte Colony-Stimulating Factor Therapy, Granulocyte Transfusion, and Other Treatments), Distribution channel (Hospital Pharmacies, Retail Pharmacies, and Online Pharmacies), and Geography (North America, Europe, Asia-Pacific, and Rest of the World). The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD) for the above segments.

| Antibiotic Therapy |

| Granulocyte Colony-Stimulating Factor (G-CSF) Therapy |

| Granulocyte Transfusion |

| Other Therapy Types |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Therapy Type | Antibiotic Therapy | |

| Granulocyte Colony-Stimulating Factor (G-CSF) Therapy | ||

| Granulocyte Transfusion | ||

| Other Therapy Types | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the Chemotherapy-Induced Neutropenia market?

The market is valued at USD 674.31 million in 2026, with a projected CAGR of 3.54% to 2031.

Which therapy type holds the largest market share?

Granulocyte colony-stimulating factor therapy led with 63.78% share of 2025 revenues.

Why are biosimilars important in this market?

Pegfilgrastim biosimilars reduced average selling prices by over 40% and achieved 81% penetration five years after launch, making prophylaxis more accessible.

Which region is growing fastest?

Asia-Pacific is expanding at a 4.70% CAGR between 2026 and 2031, driven by regulatory approvals and greater chemotherapy adoption.

How are outpatient care models influencing demand?

A shift to ambulatory and home-based oncology services boosts use of long-acting injectors and online pharmacies, expanding patient reach.

What technological trends are emerging?

Predictive analytics with up to 97% accuracy and remote white-blood-cell monitoring devices are enhancing personalized prophylaxis and adherence.

Page last updated on: