Emotion Analytics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

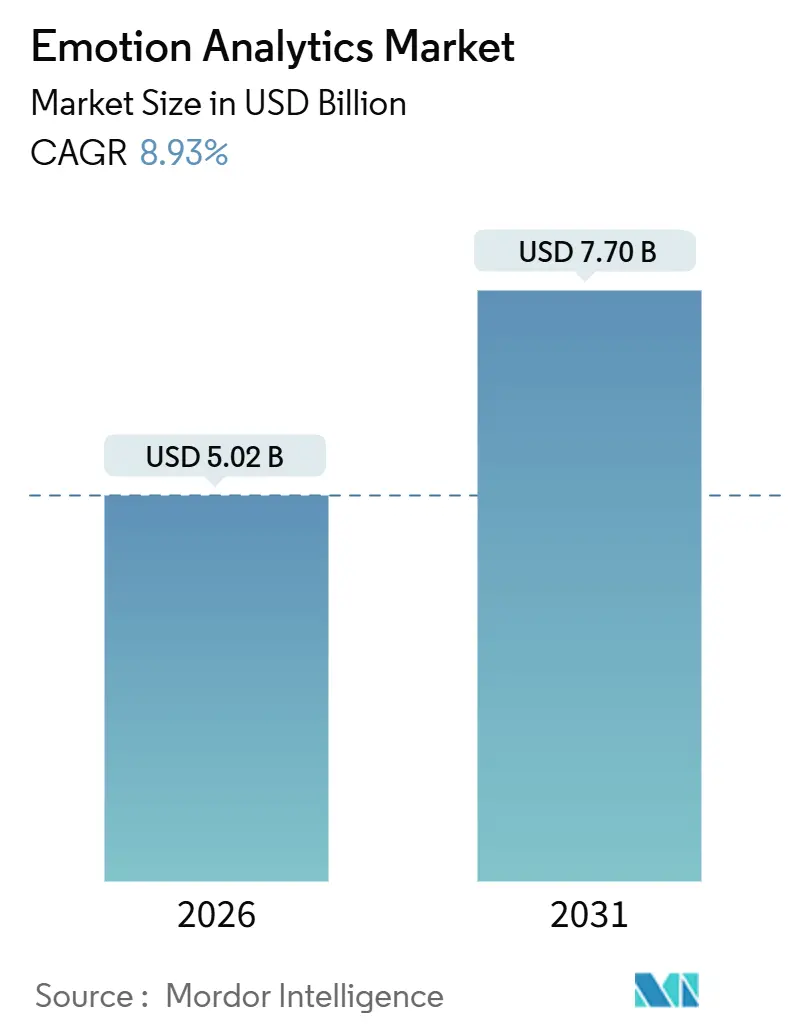

| Market Size (2026) | USD 5.02 Billion |

| Market Size (2031) | USD 7.70 Billion |

| Growth Rate (2026 - 2031) | 8.93% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

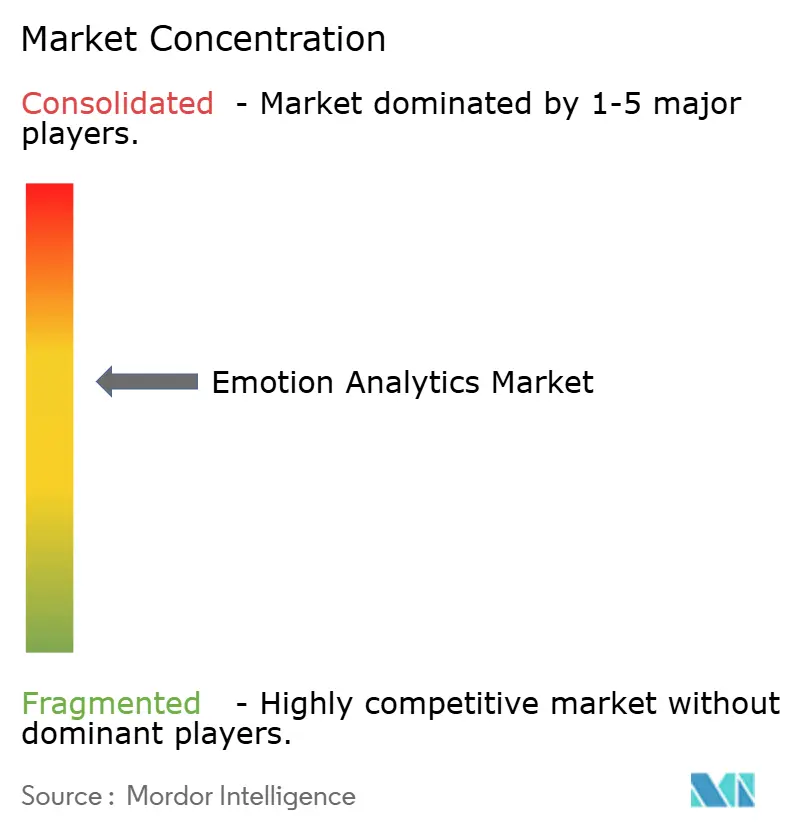

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Emotion Analytics Market Analysis by Mordor Intelligence

The Emotion Analytics Market size is estimated at USD 5.02 billion in 2026, and is expected to reach USD 7.70 billion by 2031, at a CAGR of 8.93% during the forecast period (2026-2031).

Momentum reflects enterprises moving from one-dimensional sentiment tagging toward real-time, multimodal inference that fuses facial micro-expressions, voice prosody, bio-signals, and text sentiment. Mandatory driver-monitoring regulations in automotive cabins, coupled with measurable gains in contact-center time-to-resolution, have accelerated purchase decisions. Cloud deployment still dominates but sovereignty, latency, and bandwidth economics are steering the shift toward edge and on-device processing, especially where millisecond safety alerts are critical. Vendors able to embed privacy-preserving learning or homomorphic encryption are positioned to capture European demand amid stringent biometric rules.

Key Report Takeaways

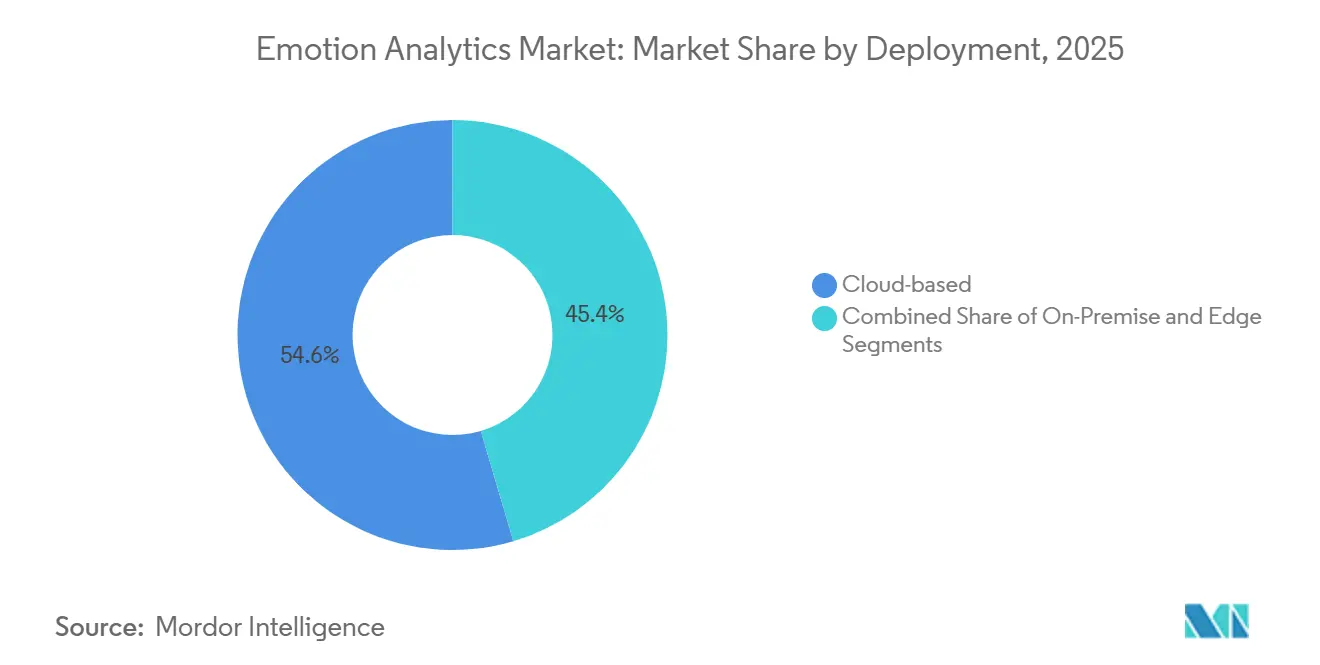

- By deployment, cloud-based solutions accounted for 54.57% of the emotion analytics market share in 2025, while edge and on-device inference is projected to advance at a 10.11% CAGR to 2031.

- By component, software platforms held 45.72% of the emotion analytics market size in 2025, whereas hardware modules will post the fastest 9.43% CAGR through 2031.

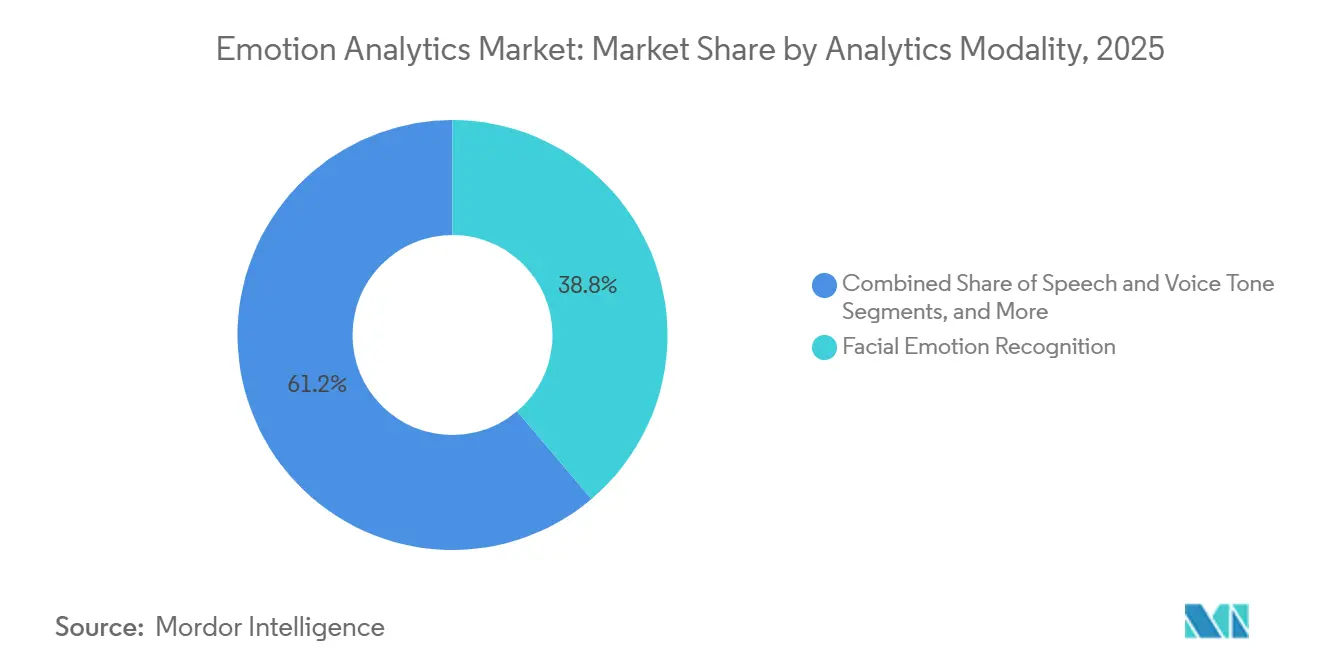

- By modality, facial emotion recognition commanded 38.82% of revenue in 2025; biosignal-driven multimodal systems will expand at a 10.96% CAGR.

- By application, customer service and contact centers captured 55.47% share in 2025, yet healthcare and well-being use cases are forecast to grow at 9.08% CAGR to 2031.

- By geography, North America led with 36.64% share in 2025, while Asia-Pacific is expected to log an 11.61% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Emotion Analytics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of IoT wearables and smart devices | +2.8% | Global | Medium term (2-4 years) |

| Advances in deep-learning-based computer vision and natural language processing | +3.2% | Global | Medium term (2-4 years) |

| Demand for hyper-personalised customer engagement tools | +2.5% | North America and Europe | Short term (≤ 2 years) |

| Regulatory mandate for driver-monitoring systems (EU GSR 2024) | +1.8% | Europe | Short term (≤ 2 years) |

| Emergence of empathetic AI in tele-mental-health platforms | +1.5% | Global | Medium term (2-4 years) |

| Edge-compute frameworks for privacy-preserving analytics | +2.0% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Proliferation of IoT Wearables and Smart Devices

Wearable emotion-sensing hardware has scaled from laboratory prototypes to enterprise rollouts, exemplified by the Emotiv EPOC X, a 14-channel electroencephalography headset priced at USD 999 that now ships for workplace stress audits and user experience trials.[1]Emotiv Inc., “Emotiv Epoc X,” emotiv.com The BIOPAC Research Ring combines galvanic skin response, photoplethysmography, electrocardiogram, temperature, and accelerometer streams into a single form factor, delivering continuous affect tracking without chest straps or facial cameras. A December 2025 Nature Scientific Data paper introduced the LLaMAC dataset that fuses Epoc-X and Empatica E4 signals with synchronized video and audio to train multimodal emotion models. Physiological signals, such as heart rate variability and skin conductance, exhibit greater cross-population consistency than facial cues, thereby reducing demographic bias. On-device inference further limits latency and data-leak risk by removing the need to stream raw biosignals to cloud servers.

Advances in Deep-Learning-Based Computer Vision and Natural Language Processing

Transformer architectures and self-supervised pre-training have reduced the need for labeled data, allowing vendors to fine-tune foundation models on call-center audio, clinical interviews, or in-cabin driver videos with far fewer annotations than their convolutional predecessors.[2]Google LLC, “Contact Center AI Insights,” cloud.google.com Google Cloud’s Conversational Insights surfaces sentiment, intent, and escalation cues from live audio, while Microsoft Azure AI offers pre-built sentiment APIs that parse text, speech, and video, reducing barriers for firms lacking machine-learning staff. Real-time emotion routing lowers handle time and boosts throughput in contact centers, turning potential churn into loyalty gains. Text analysis also tracks brand perception across social media, product reviews, and surveys within minutes. Together, these advances extend affective computing from isolated pilots to routine business workflows.

Demand for Hyper-Personalized Customer Engagement Tools

Companies recognize that generic journeys miss revenue, so emotion signals now trigger dynamic content, offers, and service escalation inside customer-relationship-management and marketing-automation suites. Retail banks use sentiment-aware chatbots that transfer distressed users to human agents before abandonment, while e-commerce sites adjust recommendations as engagement fluctuates during browsing. By layering affect data on click streams and purchase history, marketers gain causal insight into cart abandonment and feature-trial outcomes. User-experience teams pair eye-tracking, facial coding, and galvanic skin response to locate friction points, shortening iteration cycles. These practices lift conversion, retention, and lifetime value across digital channels.

Regulatory Mandate for Driver-Monitoring Systems (EU GSR 2024)

European Union Regulation 2019/2144 requires driver drowsiness and distraction warnings for all new vehicle types from July 2024 and for every newly registered vehicle from July 2026. United Nations Regulations 158 and 159 set performance criteria and are transposed into Commission Delegated Regulations 2023/1231 and 2023/1230. These rules require automakers to embed in-cabin cameras and infrared sensors that monitor gaze, blink rate, head pose, and facial microexpressions, issuing alerts when thresholds are breached. The mandate creates a captive installed base of tens of millions of sensor units each year, spurring tier-one suppliers to rapidly certify compliant systems. Similar harmonization discussions in Asia-Pacific and North America signal the formation of a global driver-monitoring ecosystem around hardware and inference software.

Restraint Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent data-privacy regulations (GDPR, CPRA, etc.) | -1.5% | Global, with acute impact in Europe and North America | Short term (≤ 2 years) |

| Bias and accuracy issues in facial-emotion data sets | -1.2% | Global | Medium term (2-4 years) |

| High latency and bandwidth cost in real-time video analytics | -0.8% | Emerging markets in Asia-Pacific, Middle East, and Africa | Short term (≤ 2 years) |

| Ethical backlash against emotion surveillance in schools and workplaces | -0.6% | North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent Data-Privacy Regulations (GDPR, CPRA, etc.)

General Data Protection Regulation Article 9 treats biometric inference as sensitive data, demanding explicit consent, purpose limitation, and strict retention windows. The California Privacy Rights Act imposes similar rules on biometric identifiers, adding deletion rights and algorithmic-decision explanations. The forthcoming European Union Artificial Intelligence Act will categorize school and workplace emotion analytics as high risk, requiring conformity assessments and post-market monitoring.[3]European Commission, “Regulation (EU) 2019/2144,” europa.eu Compliance overhead raises deployment costs and delays procurement for small firms. Privacy-preserving tools such as federated learning and homomorphic encryption mitigate exposure but add latency and compute expense, slowing global rollouts.

Bias and Accuracy Issues in Facial-Emotion Data Sets

Audits show higher error rates for darker-skinned individuals and women, exposing demographic bias in commercial classifiers. A 2024 study found misclassifications in non-Western cultural contexts where emotional norms differ from Western-centric training data. Researchers also report low agreement on subtle states, such as polite versus genuine smiles, questioning the benchmark reliability. Such gaps pose legal and reputational risks in hiring, education, and mental-health use cases. Demand is rising for independent fairness tests and explainable artificial-intelligence dashboards that reveal confidence intervals and demographic performance splits.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment: Edge Inference Gains Momentum

Edge and on-device deployment is projected to advance at a 10.11% CAGR between 2026 and 2031 as enterprises push inference closer to sensors to satisfy data-sovereignty mandates and millisecond-level latency targets. Cloud architectures still held 54.57% of the emotion analytics market share in 2025 thanks to elastic compute and centralized model updates. However, round-trip delays make cloud impractical for safety-critical driver monitoring or tele-mental-health sessions that require sub-second feedback. On-premise stacks appeal to banks and hospitals that ban biometric data egress, yet they demand capital outlays for local accelerators and skilled machine-learning staff.

Technical progress is lowering the hurdles to run models at the edge. The open-source BioGAP-Ultra platform, published in 2025, processes electroencephalography, electromyography, electrocardiogram, and photoplethysmography streams on low-power microcontrollers, proving that accurate emotion inference can run without cloud connectivity. Federated-learning toolkits let thousands of devices co-train a shared model while keeping raw data local, cutting bandwidth cost and helping firms comply with General Data Protection Regulation Article 9. As chip makers add neural-processing units to standard system-on-chip designs and model-compression methods shrink footprints, the economic gap between edge and cloud continues to close.

By Component: Hardware Sensors Accelerate

Hardware sensors, including cameras, electroencephalography headsets, galvanic skin response rings, and electrocardiogram modules, are forecast to grow at a 9.43% CAGR through 2031, the fastest rate among all component groups. Software layers (software development kits, application programming interfaces, and managed dashboards) captured 45.72% of the emotion analytics market size in 2025, reflecting the early ease of spinning up cloud APIs. Service offerings that bundle integration and custom model training expand in parallel as buyers seek turnkey rollouts.

Regulation and wearable adoption explain hardware momentum. EU driver-monitoring rules push automakers to install infrared cameras in every new cabin. In healthcare and corporate wellness, the Emotiv Epoc X 14-channel electroencephalography headset ships with pre-trained stress and engagement metrics, lowering the entry bar for non-specialist teams.[4]Emotiv Inc., “Epoc X 14-Channel EEG Headset,” emotiv.com The BIOPAC Research Ring fuses galvanic skin response, photoplethysmography, electrocardiogram, temperature, and accelerometer streams in a finger-worn form factor, giving researchers a multimodal option when privacy policies restrict video capture. Ongoing sensor miniaturization and rising production volume are set to bring hardware from labs to consumer wearables and ambient-intelligence ceilings.

By Analytics Modality: Bio-Signal Multimodal Systems Surge

Facial emotion recognition accounted for 38.82% of revenue in 2025, driven by mature computer vision pipelines and widespread camera infrastructure. Bio-signal multimodal systems that blend electroencephalography, electrocardiography, and galvanic skin response are projected to grow at a 10.96% CAGR, the fastest among modalities. Video-based multimodal engines add body language and scene context, while speech analysis captures pitch contour and energy patterns linked to arousal. Text sentiment models mine polarity and intent from written feedback across social channels and support tickets.

The outperformance of physiological fusion stems from bias mitigation and continuous coverage. Signals from the autonomic nervous system vary less across demographic groups than facial landmarks, trimming fairness gaps documented in many vision-only classifiers. Wearable biosensors also work in low-light or occluded settings such as vehicle cabins at night. The December 2025 LLaMAC corpus pairs Epoc X electroencephalography and Empatica E4 wrist data with synchronized video and audio, giving developers a large open dataset to train and benchmark multimodal fusion architectures. Because physiological data do not identify a person in the same way a face does, European privacy law treats them with fewer restrictions, easing consent workflows for longitudinal studies.

By Application: Healthcare Leads Growth

Customer service and contact centers accounted for 55.47% of revenue in 2025, after firms reported faster call resolution and higher customer satisfaction scores. Healthcare and well-being use cases are expected to rise at a 9.08% CAGR through 2031, making them the fastest-growing segment. Insurers, hospitals, and digital therapeutics providers deploy empathetic chatbots and remote-patient-monitoring dashboards that flag distress or therapy non-adherence in real time. Automotive and transportation applications benefit from mandated driver-state monitoring, while education pilots continue at a measured pace due to surveillance concerns.

Clinical validation is paving the way for reimbursement. A 2025 meta-analysis in JMIR Mental Health found conversational agents produced effect sizes of 0.62 for anxiety and 0.74 for depression, numbers that payers and regulators now cite when reviewing coverage requests. Platforms such as Woebot and Replika fine-tune large language models on psychotherapy transcripts to deliver round-the-clock coaching. The United States Food and Drug Administration convened expert panels in 2025 to draft guidance on software-as-a-medical-device for generative artificial intelligence, signaling that clear approval pathways are imminent. As reimbursement codes emerge, healthcare buyers gain the budget certainty needed to scale deployments.

Geography Analysis

North America accounted for 36.64% of revenue in 2025, driven by early pilots, venture funding, and cloud credits from hyperscale providers. Asia-Pacific is projected to log an 11.61% CAGR through 2031, the steepest regional trajectory. China promotes emotion analytics within intelligent-vehicle programs and smart-city cameras, while Japan invests in eldercare robots that track affect to improve engagement. India’s business-process-outsourcing hubs embed sentiment dashboards into quality-assurance workflows, and South Korean electronics firms integrate mood-sensing capabilities into smartphones and televisions.

Europe is growing more slowly because vendors must demonstrate compliance with both the General Data Protection Regulation (Article 9) and the forthcoming Artificial Intelligence Act. Suppliers that package federated-learning pipelines and homomorphic encryption gain procurement preference.

South America, the Middle East, and Africa report early pilots in retail, hospitality, and public safety, yet bandwidth and infrastructure gaps temper near-term contributions. Overall, the regional revenue mix is poised to diversify as the Asia-Pacific narrows the gap with North America over the forecast window.

Competitive Landscape

Fragmentation defines the 2025 baseline, with no vendor holding double-digit global share as hyperscale cloud providers (Microsoft Azure AI, Google Cloud, Amazon Web Services, and IBM Watson) jostle with specialist pure plays such as Smart Eye Affectiva, Realeyes, Entropik Technologies, iMotions, and Cogito. Incumbents monetize distribution reach by bundling sentiment-analysis application programming interfaces into broader cloud suites, whereas pure plays lean on vertical datasets, proprietary biosensors, and domain expertise to win automotive, healthcare, or market-research contracts. Procurement teams increasingly weigh privacy engineering credentials and third-party bias audits alongside raw accuracy scores, a shift that favors suppliers willing to open model cards and demographic test results.

Platform expansion and partnership deals accelerated through 2025-2026. In January 2025, Affectiva and iMotions linked their facial-coding and physiological-signal toolkits, enabling user-experience researchers to use a synchronized multimodal workflow. Realeyes followed in October 2025 by optimizing its lightweight transformer library for Intel Movidius vision processors, cutting laptop power draw by 37% and opening a new consumer electronics channel. These moves illustrate three broader strategies: adding new modalities to create full-stack inference suites, vertical integration that marries hardware with algorithms, and silicon-level co-design to meet latency and thermal budgets in cars and wearables.

Open-source disruptors also exert competitive pressure. The BioGAP-Ultra modular edge artificial-intelligence platform, released as a 2025 preprint, lets startups spin up multimodal biosignal inference on low-power microcontrollers at negligible licensing cost. Buyers facing General Data Protection Regulation and California Privacy Rights Act obligations reward vendors that ship models capable of federated learning and homomorphic encryption, tilting demand toward privacy-preserving architectures. Because the five largest providers together controlled roughly 32% of 2025 revenue, analysts expect selective mergers and data-sharing alliances rather than winner-take-all dynamics, especially as regional regulations continue to fragment deployment requirements.

Emotion Analytics Industry Leaders

IBM Corporation

Affectiva Inc.

Clarifai Inc.

Sensum Co.

Realeyes OÜ

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Nature Scientific Data released the open-access LLaMAC corpus, pairing Emotiv Epoc X 14-channel electroencephalography and Empatica E4 wrist-worn physiological signals with synchronized video and audio across multiple affective tasks, giving researchers a large multimodal training and benchmarking set.

- April 2025: Emotiv updated its Epoc X product page, highlighting workplace-stress audits and user-experience testing at enterprise clients; the 14-channel headset, priced at USD 999, ships with pre-trained engagement, relaxation, and stress metrics.

- January 2025: Affectiva and iMotions launched an integration that synchronizes facial-expression coding with galvanic-skin-response, electrocardiogram, and heart-rate streams, enabling neuromarketing and user-experience teams to build multimodal ground truth without relying on self-reports.

- January 2025: BIOPAC Systems expanded the Research Ring line, adding photoplethysmography, electrocardiogram, temperature, accelerometer, and galvanic-skin-response channels to a finger-worn device for unobtrusive continuous monitoring in laboratory and field studies.

Global Emotion Analytics Market Report Scope

The Emotion Analytics Market Report is Segmented by Deployment (On-Premise, Cloud, and Edge), Component (Software, Hardware, and Services), Analytics Modality (Facial, Video, Speech, Text, Bio-signal), Application (Customer Service, Market Research, Healthcare, Automotive, Education, Gaming, and Security), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa). The Market Forecasts are in Value (USD)

| On-Premise |

| Cloud-based |

| Edge/On-Device |

| Software (SDK/API) |

| Hardware (Sensors/Camera) |

| Services (Integration and Managed) |

| Facial Emotion Recognition |

| Video-based Multimodal |

| Speech and Voice Tone |

| Text and Sentiment |

| Bio-signal (EEG/ECG/GSR) Multimodal |

| Customer Service and Contact Centers |

| Product and Market Research |

| Healthcare and Well-being |

| Automotive and Transportation |

| Education and E-Learning |

| Gaming and Entertainment |

| Security and Public Safety |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Deployment | On-Premise | |

| Cloud-based | ||

| Edge/On-Device | ||

| By Component | Software (SDK/API) | |

| Hardware (Sensors/Camera) | ||

| Services (Integration and Managed) | ||

| By Analytics Modality | Facial Emotion Recognition | |

| Video-based Multimodal | ||

| Speech and Voice Tone | ||

| Text and Sentiment | ||

| Bio-signal (EEG/ECG/GSR) Multimodal | ||

| By Application | Customer Service and Contact Centers | |

| Product and Market Research | ||

| Healthcare and Well-being | ||

| Automotive and Transportation | ||

| Education and E-Learning | ||

| Gaming and Entertainment | ||

| Security and Public Safety | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the forecast value for the emotion analytics market in 2031?

The emotion analytics market is projected to reach USD 7.70 billion by 2031, expanding at a 8.93% CAGR.

Which deployment model is growing fastest within emotion analytics?

Edge and on-device inference is forecast to grow at 10.11% CAGR through 2031 due to latency and data-sovereignty advantages.

Which component category is expected to outpace overall market growth?

Hardware modules such as specialized cameras and biosignal sensors will expand at a 9.43% CAGR through 2031.

Which region shows the highest future growth rate?

Asia-Pacific is anticipated to register an 11.61% CAGR from 2026 to 2031, propelled by automotive and manufacturing deployments.

What is the main regulatory hurdle for emotion analytics in Europe?

General Data Protection Regulation Article 9 treats biometric inference as special-category data, necessitating explicit consent and privacy-preserving architectures.

Why are biosignal multimodal systems gaining traction?

Integrating electroencephalography, electrocardiogram, and galvanic skin response data provides physiological ground truth that mitigates demographic bias inherent in vision-only models.

Page last updated on: