Market Overview

| Study Period | 2020 - 2031 |

|---|---|

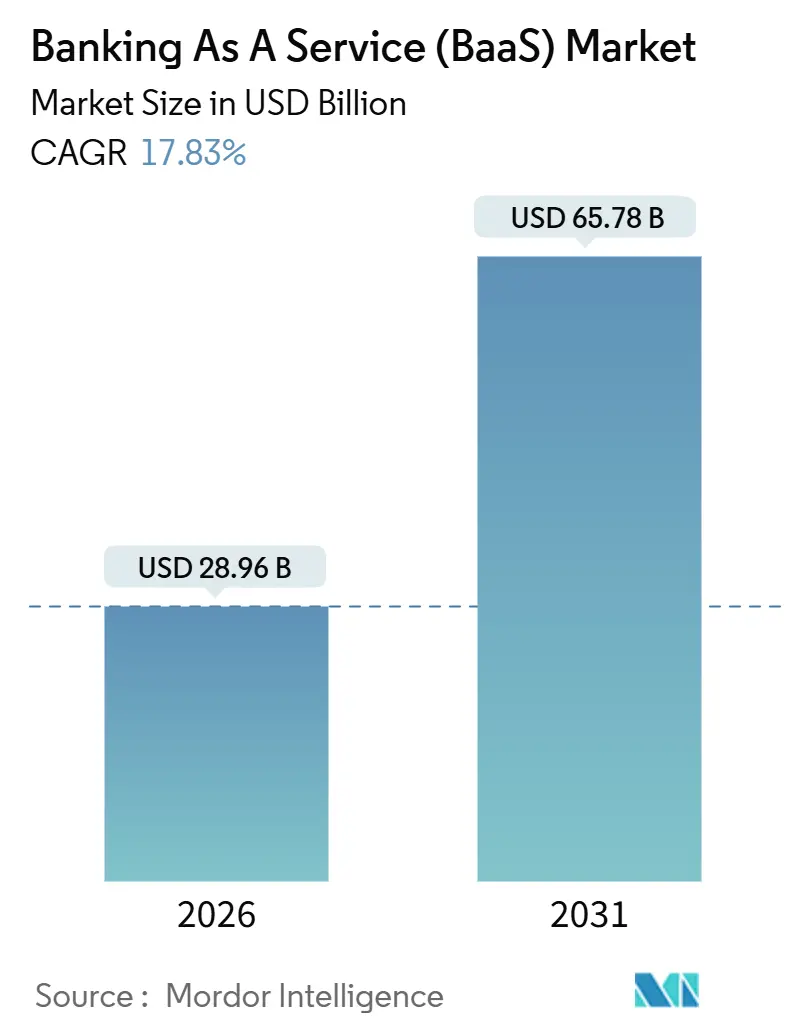

| Market Size (2026) | USD 28.96 Billion |

| Market Size (2031) | USD 65.78 Billion |

| Growth Rate (2026 - 2031) | 17.83% CAGR |

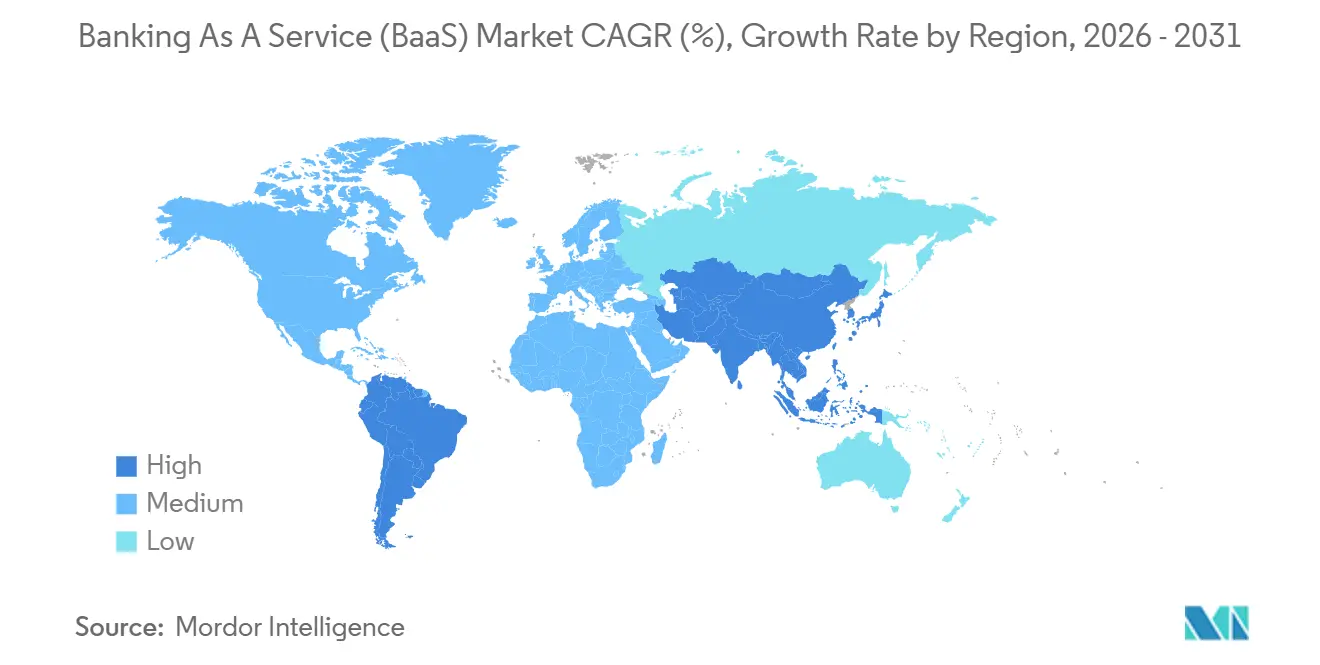

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

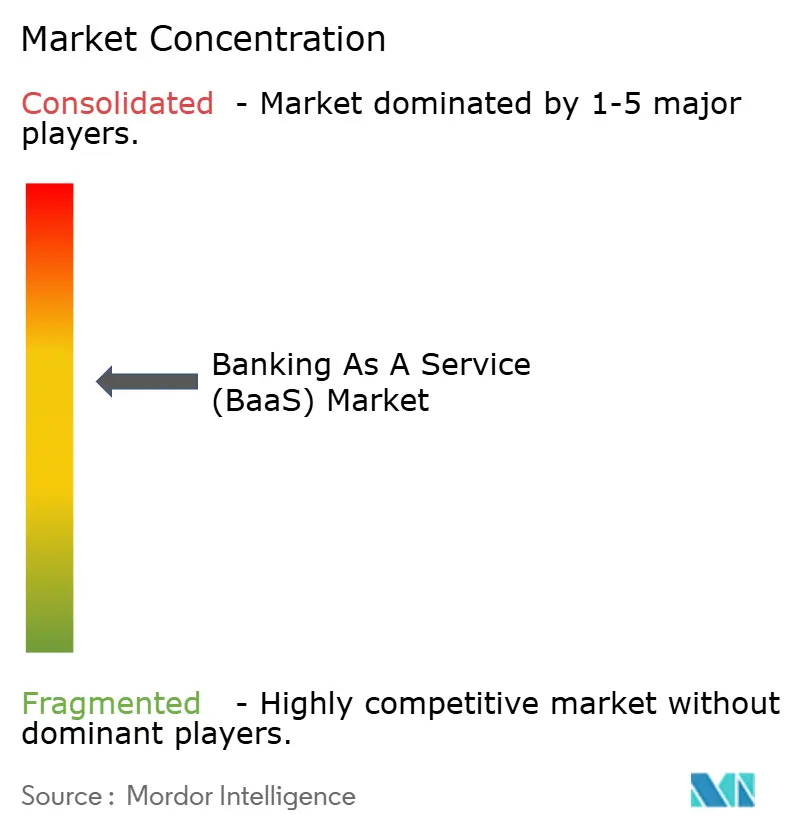

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Banking As A Service (BaaS) Market Analysis by Mordor Intelligence

The banking as a service market size is USD 28.96 billion in 2026 and is projected to reach USD 65.78 billion by 2031 at a 17.83% CAGR. This trajectory reflects a structural shift as ISO 20022 adoption standardizes payment messaging and compresses integration timelines for bank connectivity via APIs. Growth also aligns with open banking mandates that normalize permissioned data sharing and expand developer access to account and payment functionality across regions. Embedded finance models are scaling within vertical software and marketplace platforms, which monetize financial workflows such as acceptance, payouts, and working capital without carrying licenses. Instant payment infrastructure and data portability rules are reinforcing this platform-led distribution of financial services across the banking-as-a-service market.

Key Report Takeaways

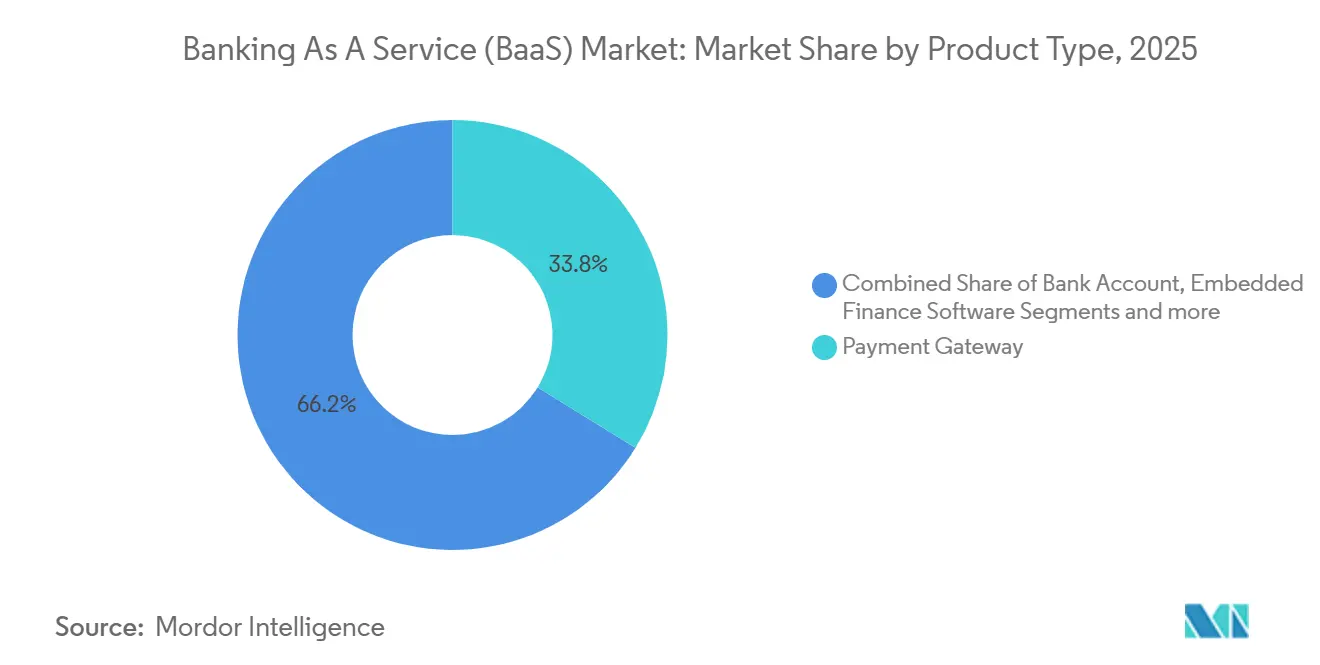

- By product type, Payment Gateway led with 33.79% of the banking as a service market share in 2025, while Embedded Finance Software is forecasted to expand at a 22.12% CAGR to 2031.

- By enterprise size, Large Enterprises held 62.18% of the banking as a service market share in 2025, while Small and Medium Enterprises recorded the highest projected CAGR at 20.42% through 2031.

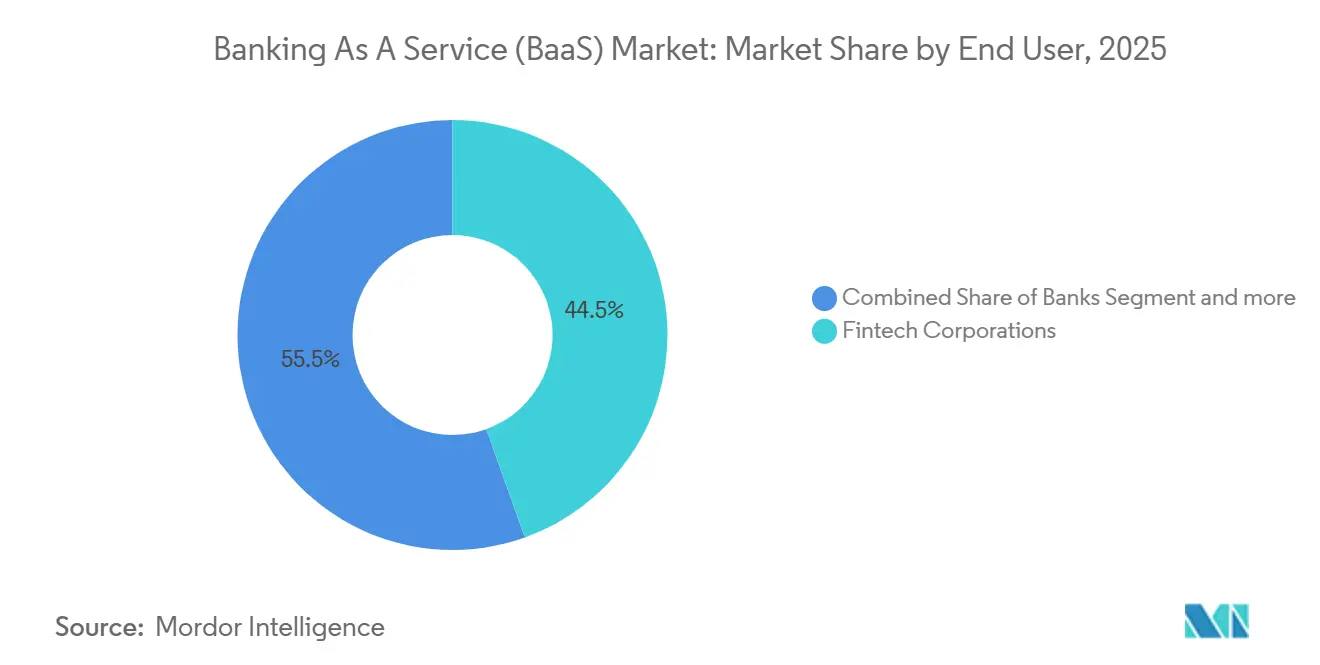

- By end user, Fintech Corporations accounted for 44.52% of the banking as a service market share in 2025 and are advancing at a 21.56% CAGR through 2031.

- By component, Platform and Infrastructure commanded 55.09% of the banking as a service market share in 2025, while the Services segment is projected to grow at a 19.68% CAGR through 2031.

- By geography, North America held 35.33% of the banking as a service market share in 2025, while Asia-Pacific is forecast to grow at 21.05% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Banking As A Service (BaaS) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising adoption of open-banking regulations | +3.2% | Global, with early concentration in the United Kingdom, the EU, India, and emerging in Canada, Australia | Medium term (2-4 years) |

| Digital transformation initiatives among incumbent banks | +2.8% | Global, particularly North America, Europe, and Japan | Medium term (2-4 years) |

| Shift toward embedded-finance revenue models | +4.1% | North America and Europe lead, spilling over to Latin America and the Asia-Pacific core | Long term (≥ 4 years) |

| API standardization lowers integration costs | +2.5% | Global, with ISO 20022 adoption in 70+ countries | Short term (≤ 2 years) |

| Surging VC funding for BaaS infrastructure start-ups | +2.3% | Concentrated in the United States, the United Kingdom, the United Arab Emirates, Singapore, and emerging in Mexico and Brazil | Medium term (2-4 years) |

| Generative-AI-driven hyper-personalization of financial products | +2.9% | North America, Europe, select Asia-Pacific markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Open-Banking Regulations

Mandatory account data-sharing frameworks are enabling providers in the banking-as-a-service market to deliver payment initiation and account aggregation on top of incumbent systems through standardized APIs. The United Kingdom reported 13.3 million active open banking users in 2025, alongside 31 million open banking payments made, underscoring scalable demand for API-based connectivity in consumer and merchant journeys. [1]Open Banking Limited, “UK Open Banking Statistics 2025,” Open Banking Limited, openbanking.org.uk Canada’s Consumer-Driven Banking framework under Bill C-69 targets a phased launch in early 2026 and aligns with ISO 20022-based real-time rails, which support interoperable data payloads for more reliable clearing and settlement. India’s UPI processed 131.1 billion transactions in fiscal 2024 and runs in multiple countries, which demonstrates how open-loop API rails can serve as cross-border infrastructure for the banking-as-a-service market. Across major markets, rulemaking and implementation timetables continue to normalize consumer-permissioned data access, which strengthens the foundations for embedded experiences and partnerships.

Digital Transformation Initiatives Among Incumbent Banks

Banks are shifting from monolithic cores to API-first architectures to accelerate product launches and integrate real-time payment, onboarding, and fraud capabilities within weeks rather than quarters across the banking-as-a-service market. SWIFT’s final migration deadline in November 2025 for ISO 20022 has driven structured, machine-readable data fields that improve reconciliation and screening use cases across payment flows. [2]SWIFT, “ISO 20022 Migration and November 2025 Milestones,” SWIFT, swift.com The Federal Reserve completed the Fedwire Funds Service migration to ISO 20022 on July 14, 2025, enabling enriched remittance data that can reduce manual intervention and exception handling. [3]Federal Reserve, “Fedwire Funds Service ISO 20022 Migration Completed July 14, 2025,” Federal Reserve, federalreserve.gov A Bank for International Settlements survey indicates that many real-time gross settlement operators plan to expose APIs within the medium term, signalling a steady expansion of direct interconnectivity pathways. These investments channel demand to orchestration platforms that bundle compliance workflows, ledgering, and network connectivity in the banking-as-a-service market.

Shift Toward Embedded-Finance Revenue Models

Vertical software and marketplace platforms continue to integrate payment acceptance, payouts, and working-capital tools into daily workflows, capturing interchange and financing economics that once sat with banks in the banking-as-a-service market. This motion reduces user friction since financial features are triggered within the system of record for scheduling, invoicing, or checkout flows. Evidence of mainstream traction includes point-of-sale lending and installment products in e-commerce and in-store settings, with platforms reporting rising adoption across consumer and small-business segments. Affirm reported 23 million active consumers as of June 2025, which illustrates how embedded credit at the point of transaction has scaled across retail and services. [4]Affirm, “Q2 2025 Shareholder Letter and KPI Update,” Affirm Holdings, affirm.com Banks and sponsors supply licenses and regulatory oversight while platforms handle product experiences, a division of labour that plays to the strengths of each participant.

API Standardization Lowering Integration Costs

ISO 20022 adoption across high-value payment systems in 70 or more countries is creating a common semantic layer that simplifies onboarding for fintechs and software platforms in the banking-as-a-service market. The Financial Data Exchange standard covered 114 million customer accounts in the United States by April 2025, which gives a royalty-free alternative to proprietary methods and supports predictable performance for aggregation and payment initiation. Japan’s Zengin API Gateway launched in November 2025, standardizing connectivity for more than 1,000 institutions to initiate domestic transfers without one-off bilateral arrangements. The European Banking Authority’s rules under revised payment directives require dedicated interfaces with uptime and fallback, which elevates reliability from a competitive feature to a regulatory obligation. These changes reduce fragmentation, lower engineering costs, and improve service consistency for embedded finance providers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heightened regulatory scrutiny on sponsor banks | -2.1% | The United States is primary, with spillover to the EU under outsourcing rules | Short term (≤ 2 years) |

| Complex cross-border compliance requirements | -1.8% | Global, acute in the EU and Asia-Pacific, with fragmented regimes | Medium term (2-4 years) |

| Rising fintech failures are increasing counterparty risk | -1.4% | North America and Europe, and emerging in Latin America | Short term (≤ 2 years) |

| Cloud-concentration risk with a handful of hyperscalers | -1.2% | Global, heightened focus in the EU and the United Kingdom | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Heightened Regulatory Scrutiny on Sponsor Banks

United States agencies clarified in July 2024 that banks remain fully accountable for compliance and safety obligations when partnering with fintechs, which has increased due diligence requirements and tightened oversight across the banking-as-a-service market. The FDIC proposed enhanced recordkeeping in September 2024 for deposit accounts held on behalf of multiple consumers, a response aimed at improving reconciliation and customer protections when third parties are involved. Recent supervisory actions have prompted several banks to reassess onboarding standards and reserve practices for partner programs as examiners evaluate third-party arrangements. European guidance on outsourcing imposes requirements for exit plans, data portability, and audit rights, which increase contractual complexity and ongoing monitoring costs for bank-fintech partnerships. These steps raise the bar for documentation, controls, and operational resilience across the sponsor ecosystem that underpins the banking-as-a-service market.

Complex Cross-Border Compliance Requirements

Fragmented regulatory expectations across jurisdictions create friction for multi-currency accounts, cross-border payments, and pan-regional card programs in the banking-as-a-service market. The Financial Stability Board’s October 2024 report showed that many jurisdictions lack comprehensive expectations for payment service providers, risk assessments of cross-border systems, and legal frameworks for cross-border data transfer, which introduces operational uncertainty. Average costs in retail cross-border payments remain elevated in several corridors due to network fees, FX margins, and compliance screening that providers must absorb or pass through. The European Union is consolidating anti-money-laundering supervision under a new authority, an effort that aims to harmonize customer due diligence while firms await final technical standards. Until there is more uniformity in legal and supervisory requirements, providers will continue to face integration complexity and scale limits across regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Modular Stacks Replace Monoliths

Payment Gateway captured 33.79% of the banking as a service market share in 2025, reflecting broad adoption of virtual cards to streamline corporate spend and procurement. The segment’s role in the banking as a service market is reinforced by merchant and enterprise demand for instant payouts, tokenized credentials, and richer ISO 20022 data for reconciliation. Embedded Finance Software is forecasted to grow at 22.12% through 2031 as vertical SaaS platforms integrate lending and acceptance, which expands addressable revenue beyond subscription fees. Bank Account and Core Banking modules enable deposit accounts with associated KYC and ledger capabilities that can be surfaced through APIs to non-bank brands. Lending and Credit Services leverage cash flow data and platform histories to underwrite segments that traditional models underserved, a pattern visible in point-of-sale installment adoption.

Mastercard expanded an embedded virtual-card program with SAP Concur and SAP Taulia in 2025, inserting one-time-use credentials into booking and invoice workflows to limit fraud exposure and support straight-through processing. As enterprise workflows standardize around API-based payouts and acceptance, providers in the banking as a service market are packaging fraud controls, sanctions screening, and onboarding checks as managed services. Affirm reported 23 million active consumers by June 2025, which signals momentum for embedded credit models that are integrated at checkout or invoice submission. TransUnion reported that fintechs originated a significant portion of new personal loan balances in 2025, which shows rising trust in digital origination and alternative data models where permitted. These shifts pull more transaction volume, and lending flows toward modular stacks across the banking-as-a-service market.

By Enterprise Size: SMEs Gain Velocity

Large Enterprises held 62.18% of deployments in 2025 due to complex treasury, multi-entity operations, and audit needs that benefit from industrial-grade API orchestration and evidence-grade logging. These buyers also require resilience, scalability, and integration to existing ERP systems, which sustains demand for bank-grade controls in the banking as a service market. Small and Medium Enterprises are projected to grow at a 20.42% CAGR as independent software vendors bundle acceptance, issuing, payouts, and reconciliation into single dashboards. This approach simplifies back-office tasks and reduces manual reconciliation as financial operations become embedded in the software SMEs already use. The banking-as-a-service market continues to add features that reduce setup effort and time to value for smaller firms, which accelerates adoption when paired with vertical workflow integrations.

Banks and platforms are expanding co-branded offerings that let software vendors integrate business banking and payment features while the bank maintains regulatory relationships. U.S. Bank expanded its embedded payments suite in 2025 with new API endpoints for issuing, acquiring, and real-time payouts, a model that aligns with SME needs for fast onboarding and unified reporting. Green Dot announced a strategic split in November 2025 that created separate bank and non-bank entities, a move intended to align balance-sheet capacity and risk oversight with large-scale sponsor programs. These steps illustrate how the banking-as-a-service industry aligns infrastructure with distinct buyer needs across enterprise tiers while safeguarding compliance and operational continuity. Adoption patterns in this segment are likely to remain stable as large customers prioritize reach and resilience, and SMEs emphasize speed and simplicity.

By End User: Fintechs Outpace Banks

Fintech Corporations accounted for 44.52% of end-user share in 2025 and are projected to grow at 21.56% through 2031 as neobanks, payment apps, and lending platforms launch new products rapidly on modular rails. These organizations rely on the banking as a service market to issue cards, open accounts, and implement real-time transfers through pre-integrated sponsor relationships. Banks also participate as both partners and distributors, often white-labelling capabilities to retain deposit relationships and support commercial clients with co-branded offerings. The end-user mix shows that product velocity and flexibility are central to capturing new use cases and segments across consumer and small businesses. This dynamic supports continuous iteration in onboarding, fraud, and credit decisioning, which sustains platform demand.

Adoption also reflects changing credit access channels for small businesses and consumers, with a visible role for online lenders and embedded products in the borrowing mix. The Federal Reserve’s 2024 small business survey observed continued use of online lenders by small firms, an indicator that digital channels are a durable part of the financing stack. U.S. Bank’s expanded embedded suite adds co-branded paths that bring issuing and payouts to software environments where small businesses already operate. Affirm’s 23 million active consumers illustrate how installment credit has become a mainstream option for retail purchases through integrations at checkout. These signals confirm that the banking-as-a-service market remains a preferred foundation for rapid product deployment in financial services.

By Component: Infrastructure Anchors, Services Accelerate

Platform and Infrastructure commanded 55.09% of revenue in 2025 as sponsors, processors, and gateways licensed API connectivity to support issuing, accounts, and payments. This layer anchors the banking as a service market by providing the connectivity, ledgering, and network access required for regulated transactions. Services are projected to grow at 19.68% through 2031 as compliance orchestration, identity verification, sanctions screening, and fraud monitoring become continuous and regulator-reviewed components of third-party arrangements. Growth reflects tighter supervisory expectations and the operational need for elastic capacity during onboarding spikes or high-volume events. Providers that deliver integrated services alongside platform access reduce complexity and improve time to value for both fintechs and banks.

Ecosystem examples show scale and product velocity indicators. Galileo reported managing multi-million account relationships and significant annual transaction volume and deposits by late 2025, signalling sustained demand for card issuing and account wallet orchestration. FIS signed 40 new clients to its Money Movement Hub in 2025, and Starling Bank’s Engine platform powered rapid customer acquisition for bank partners, demonstrating the benefits of modern cores and orchestration. Anti-money-laundering enforcement actions totalled substantial penalties in 2025, an outcome that reinforces the importance of embedded compliance and real-time monitoring features. DORA, effective January 2025, mandates incident reporting and grants direct oversight of critical ICT providers, which raises infrastructure reliability and testing expectations across the banking-as-a-service market.

Geography Analysis

North America held 35.33% of the banking as a service market share in 2025. The FedNow Service expanded from launch to more than 1,500 participating institutions by late 2025, which strengthened the case for API-exposed instant payouts and bill pay in retail and commercial contexts. Consumer research also reflects strong preferences for faster payments that support everyday transactions, which encourages banks and platforms to integrate request for pay and instant disbursements. Request for pay is expected to gain commercial adoption as treasury and billing platforms automate collection flows within embedded finance journeys. Interoperability between Canada’s Real-Time Rail and the country’s Consumer-Driven Banking framework is set to reinforce API connectivity with real-time, ISO 20022-rich clearing.

Asia-Pacific is projected to grow at 21.05% through 2031 on the strength of real-time infrastructure and API-based innovations. India’s UPI processed 20.47 billion transactions in November 2025 and continues to extend into additional markets, which expands cross-border use cases for API-initiated payments. The program’s share of retail digital payments underscores the scale of API-first rails supporting embedded experiences. Japan’s policy and industry steps to increase cashless adoption, together with bank investments in digital transformation, sustain the case for modern payment and onboarding stacks. Regional hubs such as Singapore are providing grants and sandboxes that encourage adoption of advanced financial technology and data sharing.

Europe, the Middle East, and Africa display varied adoption patterns shaped by payment regulation and supervisory frameworks. The European Payments Council’s SEPA Instant requirements effectively mainstreamed euro instant payments, and DORA elevated resilience obligations for ICT providers that serve financial institutions. The United Kingdom counted 13.3 million open banking users in 2025 with growing monthly payment volumes, reinforcing the role of standardized APIs in retail and small-business flows. Central banks in the Gulf have advanced multi-jurisdiction projects that pilot cross-border settlements and have introduced guidance for digital assets that interact with traditional banking. Regulatory modernization across these regions reinforces the case for unified compliance and technical orchestration within the banking-as-a-service market.

Competitive Landscape

Competitive intensity in the banking as a service market is moderate, with scale incumbents anchoring sponsor relationships and specialist platforms differentiating on composability and time to value. Incumbents leverage card-network certifications, core processing breadth, and proven compliance operations to serve banks and larger fintechs. Specialist banks and platforms offer configurable modules for issuing, account management, onboarding, compliance, and fraud that help clients assemble only the services they need. The result is a market where breadth of capability coexists with specialization, supporting a wide range of use cases across consumer, SME, and enterprise flows. As sponsors and regulators demand stronger controls and auditability, providers that combine infrastructure with compliance services are positioned to win.

Strategic moves in 2025 reinforced consolidation and platform expansion themes that shape the banking-as-a-service market. Fiserv completed its acquisition of StoneCastle Cash Management, adding deposit-network capabilities that support commercial treasury needs. FIS and Episode Six launched an international issuing hub that enables multi-currency, multi-market card programs from a single integration. ClearBank partnered with Circle to enable stablecoin acceptance and disbursements for European clients, an offering that expands options for near-instant settlement. U.S. Bank expanded embedded payments APIs for issuing, acquiring, and real-time payouts that target independent software vendors in priority verticals. Starling Bank’s Engine supported rapid launches and customer growth at partner institutions, demonstrating how modern cores compress time to market across regions.

Regulatory and operational resilience requirements are shaping investment and vendor selection criteria across the banking as a service market. DORA’s implementation tightened expectations for incident reporting, testing, and oversight of critical ICT providers. U.S. supervisory guidance clarified accountability for outsourced activities and increased the rigor of third-party risk management for sponsor banks and fintech partners. AML enforcement activity in 2025 highlighted the need for continuous monitoring, sanctions screening, and auditable workflows that scale during onboarding and peak demand. Announced restructurings, such as Green Dot’s separation of bank and non-bank operations, show how firms are aligning legal entities to better serve regulated client needs at scale. Partnerships and product launches that improve speed, coverage, and compliance will continue to define competitive differentiation through the forecast period.

Banking As A Service (BaaS) Industry Leaders

Solaris SE

ClearBank

Green Dot Corp.

Intergiro

Weavr

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Green Dot Corporation announced a strategic split, with Smith Ventures acquiring its non-bank operating businesses for approximately USD 690 million and CommerceOne Holdings acquiring Green Dot Bank for an aggregate value that, combined with the Smith Ventures transaction, underscores the market's recognition of separate valuations for regulated banking entities versus fintech platforms; the split enables each business to pursue focused growth strategies, with the bank entity serving large-scale BaaS clients requiring substantial deposit capacity.

- October 2025: ClearBank, a United Kingdom clearing and embedded-banking provider, partnered with Circle to enable businesses across Europe and the United Kingdom to accept and disburse USDC and EURC stablecoins through the Circle Payments Network, expanding digital-asset settlement options for fintech clients and reflecting growing institutional demand for blockchain-based payment rails that offer near-instant settlement at lower cost than traditional correspondent banking.

- September 2025: FIS acquired Amount, a digital account origination and loan management platform, to enhance its banking modernization framework, adding cloud-native decisioning engines that compress consumer and commercial loan underwriting from days to minutes.

- September 2025: Fiserv acquired Smith Consulting Group, a provider of audit and regulatory compliance advisory services for financial institutions, to strengthen governance and risk-management capabilities that sponsor banks require when evaluating BaaS partnerships.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global banking-as-a-service market as the total revenue earned when licensed financial institutions expose deposit, payment, card, lending, or compliance functions through API or cloud platforms that third-party brands embed inside their own products.

Excluded: stand-alone data aggregators that never touch regulated balance-sheet activities.

Segmentation Overview

- By Product Type

- Payment Gateway

- Bank Account/Core Banking

- Lending and Credit Services

- Embedded Finance Software

- Other Product Types

- By Enterprise Size

- Large Enterprises

- Small & Medium Enterprises (SMEs)

- By End User

- Banks

- Fintech Corporations

- Other End Users

- By Component

- Platform / Infrastructure

- Services (Compliance, KYC, Fraud, etc.)

- By Region

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Colombia

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- Benelux (Belgium, Netherlands, and Luxembourg)

- Nordics (Sweden, Norway, Denmark, Finland, and Iceland)

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- South-East Asia (Singapore, Indonesia, Malaysia, Thailand, Vietnam, and Philippines)

- Rest of Asia-Pacific

- Middle East and Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Nigeria

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

We interview bank platform heads, fintech product leads, and regulators across North America, Europe, and Asia-Pacific to validate pricing bands, onboarding timelines, and likely API-call growth.

Short online surveys with mid-tier retailers and SaaS firms confirm adoption intent and close data gaps we spotted in secondary material.

Desk Research

Mordor analysts begin with tier-one public sources such as the IMF Financial Access Survey, BIS Red Book digital-payment tables, FDIC and ECB open-banking adoption studies, and white papers from bodies such as the European Payments Council and the FinTech Association of Japan. These datasets frame reachable deposit, card, and loan pools.

Company filings, 10-Ks, investor presentations, and press releases then reveal partner counts and fee splits, which are cross-checked against Volza shipment records for prepaid cards and news flow monitored on Dow Jones Factiva for fresh BaaS launches.

The sources named are illustrative only; many additional references underpin our desk work.

Market-Sizing & Forecasting

A top-down construct converts global digital-transaction value into a BaaS revenue pool via penetration rates gathered from interviews. Results are further filtered through sampled service fees to anchor the 2025 baseline. Supplier roll-ups of disclosed revenues provide a bottom-up check.

Five fingerprints live BaaS partnerships, average API calls per partner, cloud cost per call, share of consumer payments routed through embedded rails, and regulatory approvals issued feed a multivariate regression that projects growth to 2030.

Where disclosures lapse, regional precedent ratios bridge gaps.

Data Validation & Update Cycle

Outputs pass two-level peer review, variance checks against quarterly filings, and anomaly scans; if deviations top five percent, we rerun the model.

The dataset refreshes yearly, with interim updates triggered by major regulations or mega funding rounds so clients receive the latest view.

Why Our Banking as a Service Baseline Commands Reliability

Published estimates often diverge because each publisher selects different service lists, price capture points, and refresh timings.

Some studies omit compliance add-ons or keep 2021 exchange rates, while others backcast from an early 2022 snapshot that ignores the 2024 embedded-finance surge. Mordor Intelligence includes every monetized module, uses live currency averages, and revisits assumptions annually, making our 2025 figure the most current and complete.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 24.58 B (2025) | Mordor Intelligence | |

| USD 18.60 B (2024) | Global Consultancy A | Platform fees only; excludes compliance and card issuance revenue |

| USD 22.49 B (2022) | Industry Databook B | Older base year and fixed 2021 FX; pre-surge adoption snapshot |

The comparison shows that scope, timing, and currency choices explain most gaps; by harmonizing all three, our baseline offers decision makers a transparent, balanced starting point.

Key Questions Answered in the Report

What is the size and growth outlook for the banking as a service market through 2031?

The banking as a service market size is USD 28.96 billion in 2026 and is projected to reach USD 65.78 billion by 2031 at a 17.83% CAGR.

Which product types lead adoption in banking as a service?

Payment Gateway led with 33.79% share in 2025, while Embedded Finance Software is the fastest growing with a 22.12% CAGR to 2031.

Who are the primary end users driving demand for banking as a service?

Fintech Corporations accounted for a 44.52% share in 2025 and are forecast to grow at a 21.56% CAGR through 2031, supported by rapid launches of issuing, accounts, and instant transfers.

Which regions are most important for near-term banking as a service expansion?

North America held a 35.33% share in 2025, and Asia-Pacific is forecast to grow at a 21.05% CAGR through 2031, driven by instant payments and open banking.

What regulatory themes shape banking as a service programs?

ISO 20022 migrations, open-banking frameworks, and operational resilience mandates like DORA drive API reliability, data portability, and incident management requirements.

Which recent moves signal competitive shifts in banking as a service?

Fiserv’s StoneCastle deal, FIS’s international issuing hub launch, and ClearBank’s Circle partnership reflect consolidation and product expansion focused on scale and speed.

Page last updated on: