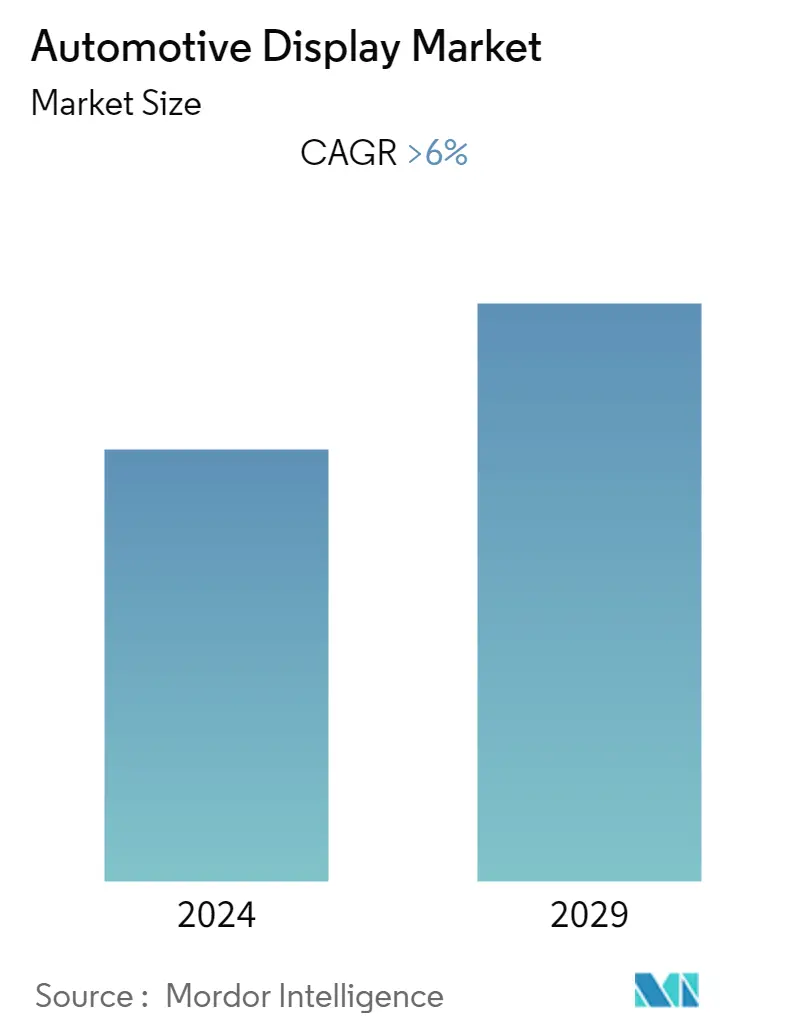

Automotive Display Market Size

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

| CAGR | > 6.00 % |

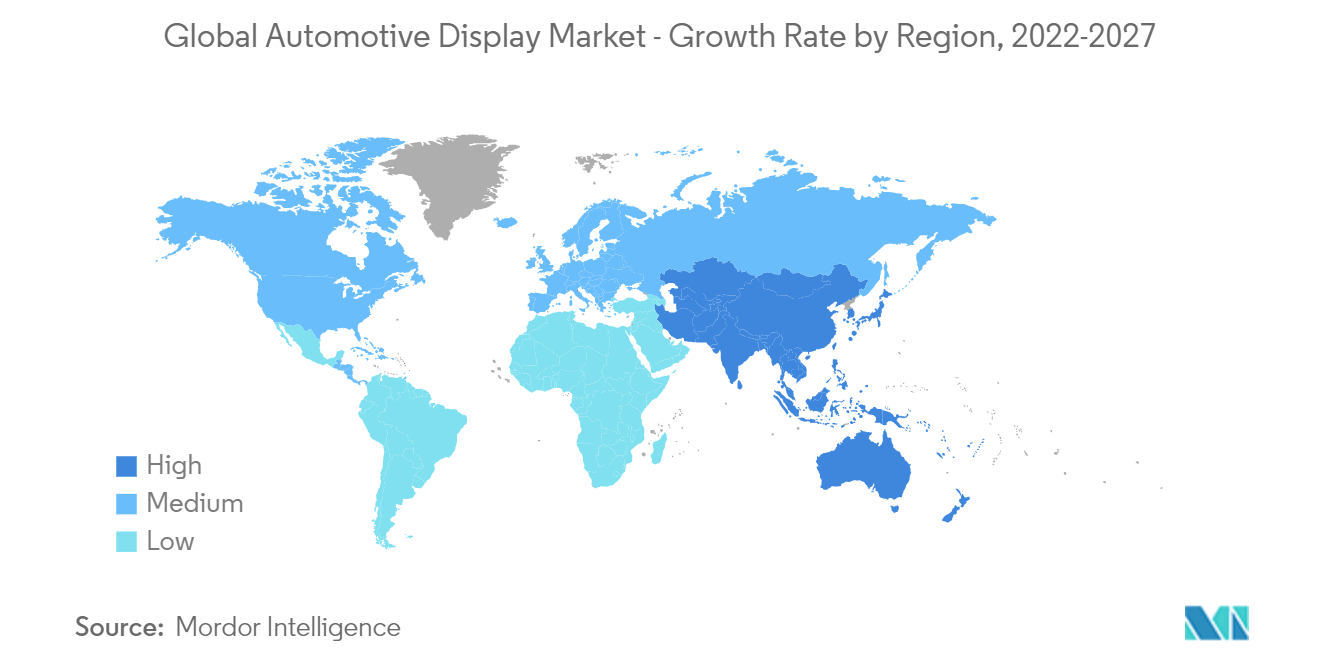

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

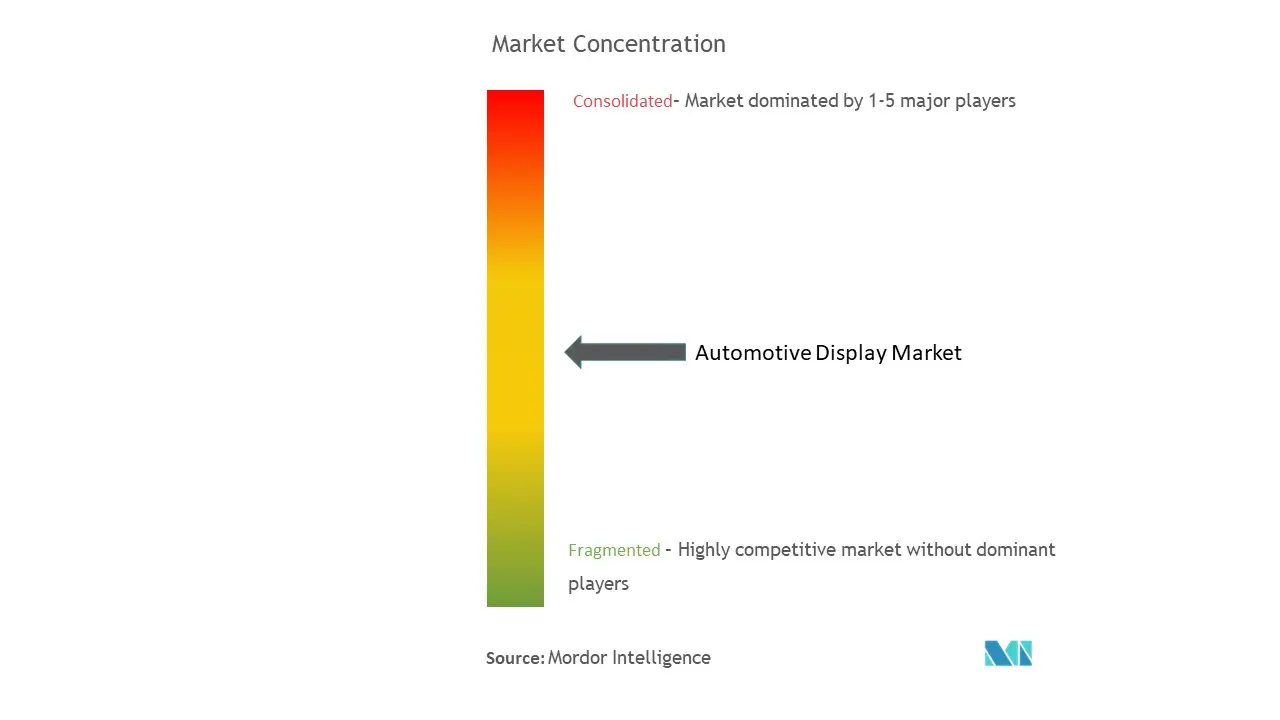

| Market Concentration | Medium |

Major Players.webp)

*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

Automotive Display Market Analysis

The automotive display market was valued at USD 11.9 billion and is expected to reach USD 17.3 billion, registering a CAGR above 6.41% during the forecast period.

- The recent COVID-19 has disrupted market growth. With lockdowns and travel restrictions, the demand for vehicles declined. As a result, the growth of automotive parts of the automotive industry also declined in the past two years. This trend is seen in all segments related to the automotive industry. However, post-pandemic,, as the situation is improving, the companies are focusing on developing new products that suit the customers' demands.

- For instance, in November 2022, Marelli Corporation updated its featured technology portfolio. "Digital Design Studio" by Marelli will be on display. In addition to the Smart Surface solution, the company will launch the Horizon Head-Up Display, which projects navigation, indicator, and warning information close to the bottom edge of the windshield, allowing objects in the driver's blind spot to be easily recognized.

- Over the long term, the market is primarily driven by technological advancements and innovations in various vehicle display systems such as infotainment, telematics, instrument cluster, etc. In developed nations, rising consumer preference toward driving convenience and safety is driving the market's growth. Further, with an increased need for vehicle safety features, technologies such as augmented reality have turned from a mere concept into reality. Many luxury car brands, such as BMW, Jaguar, and Mercedes-Benz, have already implemented AR head-up displays and brought real-time gaming experiences.

- For instance, in October 2022, AirConsole and the BMW Group announced a collaboration to integrate casual gaming into new BMW vehicles. AirConsole is a gaming platform that works perfectly with the BMW Curved Display and has a large and diverse game catalog.

- With the growing sales of passenger cars, the rising demand for connected vehicles, and a high disposable income, the automotive display market has been witnessing rapid growth, particularly in Asia-Pacific. Moreover, the region is expected to dominate the market due to the increasing sales of luxury cars such as Mercedes-Benz, Audi, Porsche, BMW, and Jaguar Land Rover. Therefore, the automotive display players focus on developing displays for automakers' needs.

- For instance, in December 2022, Faurecia Clarion Electronics, a subsidiary of the Forvia Group, stated that the company would focus on developing large, irregular displays. The company will create high-value-added products to meet automakers' needs.

Automotive Display Market Trends

This section covers the major market trends shaping the Automotive Display Market according to our research experts:

Increasing Demand of OLED Displays in the Luxury Vehicle is Expected to Witness Faster Growth Rate

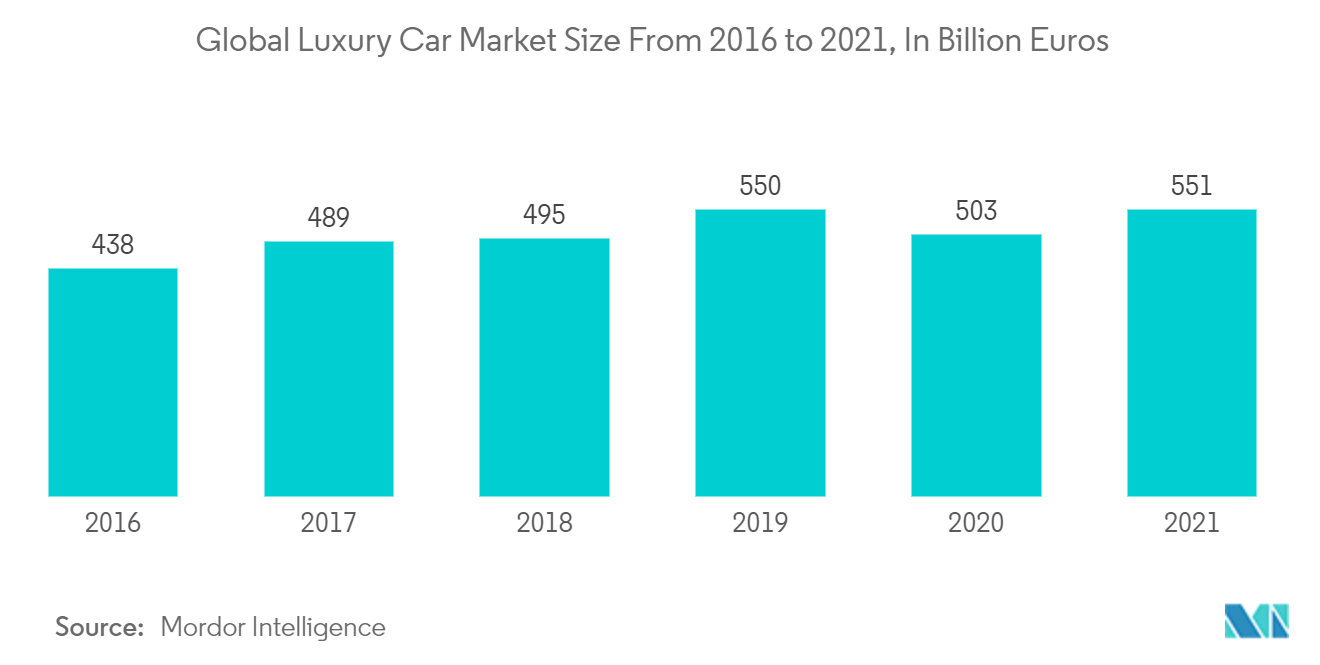

- The rising demand for luxury vehicles in developing countries is expected to fuel the automotive display system market. The luxury car market segment is expected to grow at a rate ranging from 8 to 14 per cent per year during the forecast period. In India, Mercedes-Benz, BMW, and Audi are the top luxury car manufacturers. These car manufacturers collectively reported sales of around 22,500 units in 2021.

- Luxury car manufacturers such as Lexus, Audi, and others have integrated technologically advanced display systems into their vehicles. For instance, in October 2022, Cadillac unveiled the Celestiq, its handcrafted, all-electric flagship. The vehicle's large, 55-inch-diagonal advanced HD screen is one of five high-definition displays, with rear passengers having their 12.6-inch-diagonal advanced displays.

- Technology has advanced to the point where it is cost-effective, such as thin-film-transistor liquid-crystal display (TFT-LCD) and organic light-emitting diode (OLED), which aids in the enhancement of display resolution and features. Furthermore, it is useful in map navigation and multimedia options, which will likely drive demand for automotive display systems. OLED panels are gaining popularity in the luxury car market owing to their high flexibility in design and growing demand from original equipment manufacturers (OEMs) in their new model launches. For instance, Currently, Active Matrix OLED (AMOLED ) screens are being used mostly for rear seat entertainment in luxury cars.

- However, to reach automotive-grade specifications, AMOLED material and display costs are expected to be high. This is expected to slightly hinder the market's growth. With the evolvement of intelligent connectivity technology, cars will be mobile smart terminals. In addition to cluster & center console dual displays, HUD, electronic rearview mirror displays, copilot recreation displays, rear seat entertainment displays, and transparent A-pillars have emerged.

- Moreover, according to the concept models released by Oz EMs, curved displays will shine in the automotive display field in the future. Luxury brand cars and new energy vehicles are now making use of OLED displays. Previously, they only used small displays such as transparent A-pillars, and Audi virtual rearview mirror displays. Such developments are likely to enhance the demand for displays in the market during the forecast period.

Asia-Pacific Expected to Capture Significant Market Share During the Forecast Period

- Asia-Pacific is expected to see faster growth in the market studied, owing to the increasing adoption of rear seat entertainment displays in taxis as well as display manufacturers have been focusing on the production of OLED technology.

- In India, automobile production has increased; Passenger car production has increased from 3,062,280 units in 2020-21 to 3,650,698 units in 2021-22. On the other hand, Commercial Vehicles production has increased from 624,939 units in 2020-21 to 805,527 units in 2021-22. Major taxi aggregators like Uber and Ola have been significantly installing rear seat entertainment display panels in their premium and luxury taxi cabs over the past two years to attract customers' attention and booking preferences.

- Automotive display manufacturers like Visionox in China will be providing Zhejiang Hozon New Energy Automobile Co., Ltd. (Hozon) with intelligent cabin display products featuring centre information display (CID) systems, dashboards, head-up display instruments, and rear seat entertainment display instruments for autonomous New Energy Vehicles (NEVs). These displays are manufactured based on advanced organic light-emitting diode (OLED) technology. Moreover, key players in the other Asia-Pacific countries are also installing the advanced display system in their vehicles which is also expected to play a dominant role in the market growth.

- In October 2022, Mazda Sale Thailand introduced four special models under the brand name Carbon Edition, each with its personality. The Mazda3 Carbon Edition 4-door sedan features black alloy wheels and a 360-degree image display system.

- Therefore, all the above-mentioned developments and advancements in the market will likely contribute to the holistic development of the Asia-pacific region over the forecast period.

Automotive Display Industry Overview

The automotive display market is moderately consolidated as the presence of some of the key major players, like Continental AG, Visteon Corporation, Panasonic Corporation, Denso Corporation, Robert Bosc GmbH, etc., have captured significant shares in the market. With companies focusing on product innovation and technology advancement, the automotive display business is experiencing high competition in the global market.

In January 2022, Visteon announced the launch of a fourth-generation smart core cockpit domain controller for enhanced safety and connected mobility. The smart display offers seamless support of multiple displays along with integrated infotainment, safety, and security features. The smart display comes with artificial intelligence-based speech recognition and camera-domain integration.

In November 2021, Continental AG technology company earned its first major order for OLED displays in a production vehicle from a global vehicle manufacturer. The multi-display stretches from the driver's area to the center console and integrates two screens, which are optically bonded behind a curved glass surface. Production of the display solution is scheduled to start in 2023.

Automotive Display Market Leaders

Denso Corporation

Robert Bosch GmbH

Visteon Corporation

Continental AG

Harman International Industries, Inc

*Disclaimer: Major Players sorted in no particular order

Automotive Display Market News

- April 2022: TouchNetix announced fully integrated aXiom touchscreen chips that offer new 3D sensing capabilities by detecting air gestures allowing touchless functions in automotive, industrial, and consumer environments, among others. aXiom provides more than 100 times higher Signal-to-Noise Ratio (SNR) than the traditional touchscreen controllers on the market.

- May 2022: Nippon Seiki Co., Ltd. announced on May 9 that it had started production of head-up displays (HUDs) at its new plant in Poland. The plant will first manufacture HUDs for the BMW Group. Vehicles are increasingly equipped with HUDs in Europe, the United States, and China, and the HUD market is rapidly expanding. Nippon Seiki established the new plant to deal with the increasing demand for HUDs from European automakers.

- May 2022: Faurecia announced introducing its newest perceptual image processing and immersive user experience solutions to the market during SID Display Week in California. Faurecia will also present MyDisplay, a platform solution that creates a personalized, enhanced visual experience. MyDisplay incorporates physiological algorithms that mimic how our eyes work to enhance the screen's 3D, color, and brightness in one seamless process.

- June 2021: Visteon Company announced a new business win with a North American OEM for its microZone™ display technology. The award is for a multi-display system that will be featured in multiple premium and performance vehicles expected to launch in 2024.

Automotive Display Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

4.1 Market Drivers

4.2 Market Restraints

4.3 Industry Attractiveness - Porter's Five Forces Analysis

4.3.1 Threat of New Entrants

4.3.2 Bargaining Power of Buyers/Consumers

4.3.3 Bargaining Power of Suppliers

4.3.4 Threat of Substitute Products

4.3.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION (Market Size by Value - in USD billion)

5.1 Product Type

5.1.1 Center Stack Display

5.1.2 Instrument Cluster Display

5.1.3 Head-Up Display

5.1.4 Rear Seat Entertainment Display

5.2 Display Technology

5.2.1 LCD

5.2.2 OLED

5.3 Geography

5.3.1 North America

5.3.1.1 United States

5.3.1.2 Canada

5.3.1.3 Rest of North America

5.3.2 Europe

5.3.2.1 Germany

5.3.2.2 United Kingdom

5.3.2.3 France

5.3.2.4 Rest of Europe

5.3.3 Asia Pacific

5.3.3.1 China

5.3.3.2 Japan

5.3.3.3 India

5.3.3.4 South Korea

5.3.3.5 Rest of Asia-Pacific

5.3.4 Rest of the World

5.3.4.1 South America

5.3.4.2 Middle-East and Africa

6. COMPETITIVE LANDSCAPE

6.1 Vendor Market Share

6.2 Company Profiles*

6.2.1 Denso Corporation

6.2.2 Robert Bosch GmbH

6.2.3 Visteon Corporation

6.2.4 Continental AG

6.2.5 Harman International Industries, Inc.

6.2.6 Magneti Marelli SpA

6.2.7 Panasonic Corporation

6.2.8 Yazaki Corporation

6.2.9 LG Display Co.

6.2.10 Nippon Seiki Co. Ltd

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

Automotive Display Industry Segmentation

Various applications of car electronic systems, namely infotainment, back seat entertainment, instrument cluster, etc., include display units constructed of LCD and OLED panels. There are various categories of the display, which are segmented based on various formats.

The automotive display market has been segmented by product type (center stack display, instrument cluster display, head-up display, and rear seat entertainment display), by display technology (LCD and OLED), and by geography (North America, Europe, Asia-Pacific, and Rest of the world).

The report offers market size and forecast for the automotive display market in value (USD billion) for all the above-mentioned segments.

| Product Type | |

| Center Stack Display | |

| Instrument Cluster Display | |

| Head-Up Display | |

| Rear Seat Entertainment Display |

| Display Technology | |

| LCD | |

| OLED |

| Geography | |||||||

| |||||||

| |||||||

| |||||||

|

Automotive Display Market Research FAQs

What is the current Automotive Display Market size?

The Automotive Display Market is projected to register a CAGR of greater than 6% during the forecast period (2024-2029)

Who are the key players in Automotive Display Market?

Denso Corporation, Robert Bosch GmbH, Visteon Corporation, Continental AG and Harman International Industries, Inc are the major companies operating in the Automotive Display Market.

Which is the fastest growing region in Automotive Display Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2024-2029).

Which region has the biggest share in Automotive Display Market?

In 2024, the Asia-Pacific accounts for the largest market share in Automotive Display Market.

What years does this Automotive Display Market cover?

The report covers the Automotive Display Market historical market size for years: 2019, 2020, 2021, 2022 and 2023. The report also forecasts the Automotive Display Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

Automotive Display Industry Report

Statistics for the 2024 Automotive Display market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. Automotive Display analysis includes a market forecast outlook to 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.