Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

The Big Data in Banking Market Report is Segmented by Solution Type (Data Discovery and Visualization, Advanced Analytics, and More), Deployment Mode (On-Premise, Cloud, and Hybrid), Application (Risk Management, and More), Organization Size (Large Banks, Mid-Sized Banks, and Community/Small Banks), Analytics Technique (Descriptive, Diagnostic, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

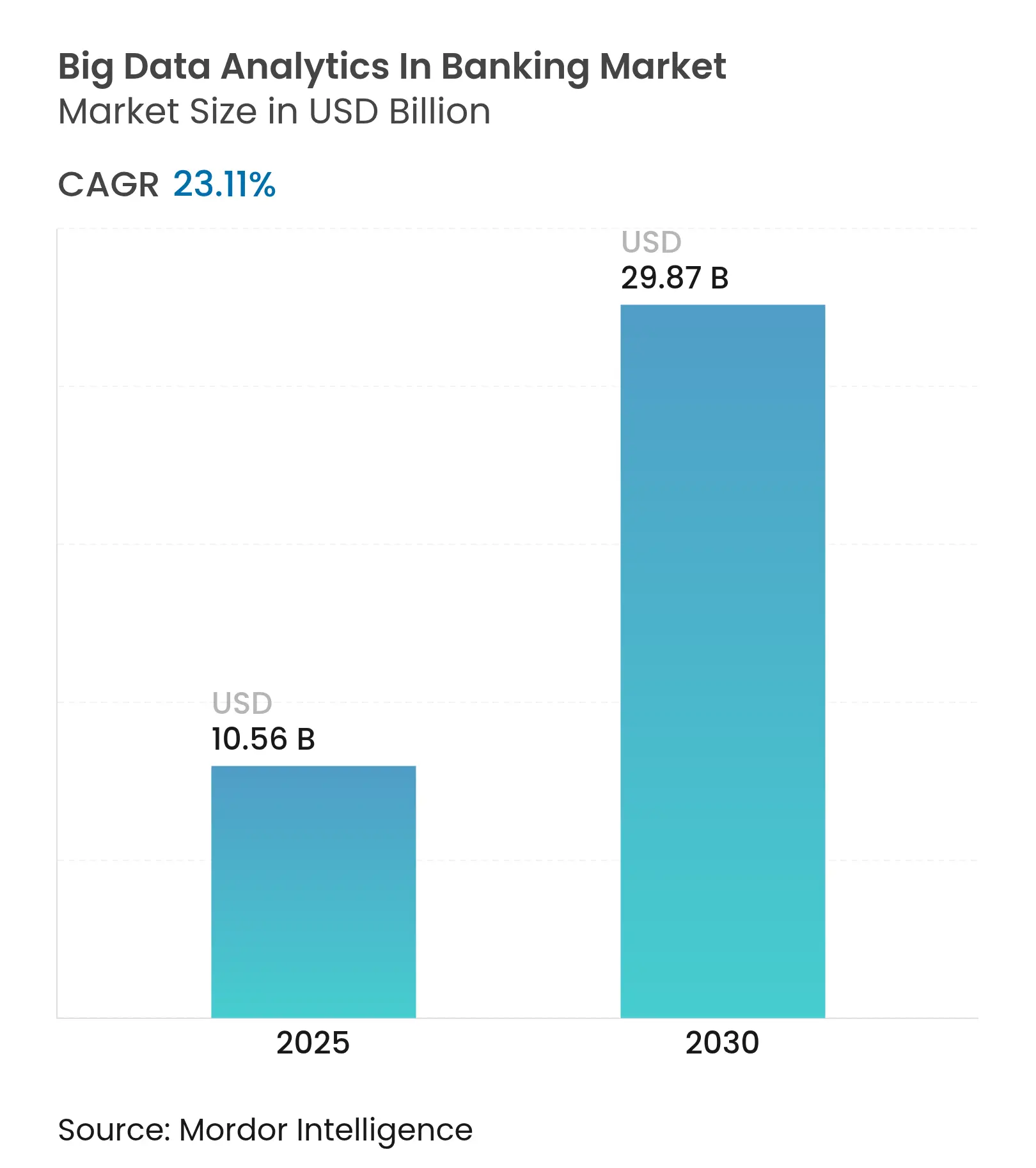

| Market Size (2025) | USD 10.56 Billion |

| Market Size (2030) | USD 29.87 Billion |

| Growth Rate (2025 - 2030) | 23.11 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The big data in the banking market size is valued at USD 10.56 billion in 2025 and is forecast to reach USD 29.87 billion by 2030, expanding at a robust 23.11% CAGR over the period. Rising transaction volumes on instant-payment rails, enforcement of data-heavy regulatory mandates, and the monetization of open-banking APIs are converging to accelerate investment in streaming analytics and cloud-native data platforms. Financial institutions are reallocating budgets from legacy batch warehouses toward real-time decision engines that support millisecond‐level fraud scoring, intraday liquidity optimization, and automated compliance reporting. Hyperscale cloud providers are winning a growing share of infrastructure spending as banks embrace multi-cloud architectures to satisfy operational-resilience tests under the European Union’s Digital Operational Resilience Act. At the same time, specialist fintechs are commercializing niche use cases such as synthetic-fraud detection and ESG risk scoring, creating a fragmented but opportunity-rich landscape.

Key Report Takeaways

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Increasing Volume of Data Generated by Banking Transactions Increasing Volume of Data Generated by Banking Transactions | +5.2% | Global, with peak intensity in Asia-Pacific (India UPI, China digital yuan) and Latin America (Brazil PIX) | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+5.2% | Geographic Relevance:Global, with peak intensity in Asia-Pacific (India UPI, China digital yuan) and Latin America (Brazil PIX) | Impact Timeline:Medium term (2-4 years) |

Rising Regulatory Compliance Requirements for Data Reporting Rising Regulatory Compliance Requirements for Data Reporting | +4.8% | Europe (DORA, FIDA), North America (Basel III finalization, SR 11-7), Asia-Pacific (MAS, RBI) | Short term (≤ 2 years) | |||

Growing Adoption of Cloud-Based Analytics Platforms Growing Adoption of Cloud-Based Analytics Platforms | +4.3% | Global, led by North America and Europe; accelerating in Middle East (SAMA Cloud First) | Medium term (2-4 years) | |||

Integration of Real-Time Payments Infrastructure Requiring Instant Analytics Integration of Real-Time Payments Infrastructure Requiring Instant Analytics | +3.9% | Asia-Pacific (UPI, PromptPay), Latin America (PIX), North America (FedNow, RTP) | Short term (≤ 2 years) | |||

Monetization of Open Banking APIs Creating New Analytics Revenue Streams Monetization of Open Banking APIs Creating New Analytics Revenue Streams | +2.7% | Europe (PSD2/PSD3, FIDA), United Kingdom, Australia (CDR), emerging in Middle East | Medium term (2-4 years) | |||

ESG Risk Scoring Demands Advanced Data Analytics in Lending Portfolios ESG Risk Scoring Demands Advanced Data Analytics in Lending Portfolios | +2.2% | Europe (CSRD, Taxonomy Regulation), North America (SEC climate disclosure), Asia-Pacific (ISSB standards) | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Increasing Volume of Data Generated by Banking Transactions

Instant-payment systems now clear billions of transfers each month, shifting the analytics bottleneck from storage to sub-second processing. India’s Unified Payments Interface processed 13.4 billion transactions in April 2024, creating 2.1 petabytes of metadata that must be scored for fraud, merchant risk, and customer behavior in under 100 milliseconds. [1]National Payments Corporation of India, “UPI Product Statistics,” NPCI.ORG.IN Brazil’s PIX system settled 42 billion payments in 2024, with a Banco Central rule that requires suspicious transfers to be flagged before completion, forcing banks to utilize streaming analytics engines capable of evaluating more than 200 behavioral variables per event.[2]Banco Central do Brasil, “PIX – Instant Payments,” BCB.GOV.BR Revised European open-banking rules have increased API call volumes by 340% year-over-year, generating vast consent logs and audit trails that feed directly into data lake pipelines. [3]European Banking Authority, “EBA Report on Big Data and Advanced Analytics,” EBA.EUROPA.EU

Rising Regulatory Compliance Requirements for Data Reporting

The Digital Operational Resilience Act, effective January 2025, requires EU banks to maintain continuous ICT monitoring, conduct threat-led penetration tests, and report major incidents within four hours, all of which necessitate centralized log ingestion and automated root-cause analytics. In the United States, OCC SR 11-7 mandates independent validation of every machine-learning model used for credit, fraud, or capital allocation, accelerating demand for automated model-risk-management platforms that document lineage, backtests, and sensitivity metrics. Basel’s revised operational-risk framework, effective from January 2025, requires banks to demonstrate lineage on granular loss-event data, underscoring the need for immutable data catalogs and metadata tracking.

Growing Adoption of Cloud-Based Analytics Platforms

Cloud deployments accounted for 48.53% of total spend in 2024 and are on course to rise at 25.31% CAGR as regulators explicitly endorse multi-cloud resilience testing. Saudi Arabia’s Cloud First directive obliges banks to justify any new on-premise investment, catalyzing deals between GCC institutions and hyperscalers. IBM’s Watsonx.data, launched in 2024, enables banks to query distributed storage layers with a single SQL statement, reducing replication overhead by 40%.

Integration of Real-Time Payments Infrastructure Requiring Instant Analytics

FedNow processed 75 million transactions in its inaugural year, with participants required to run real-time fraud detection and liquidity monitoring. India’s Account Aggregator scheme enables consent-based data sharing across 1.4 billion accounts, obliging lenders to underwrite within seconds of receiving transaction feeds. Europe’s TIPS platform demands intra-day collateral pledging, pushing banks toward prescriptive analytics that optimize funding across multiple currencies.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High Implementation Costs of Legacy Core System Integration High Implementation Costs of Legacy Core System Integration | -3.4% | Global, most acute in North America and Europe where banks operate mainframe cores; moderate in Asia-Pacific | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:-3.4% | Geographic Relevance:Global, most acute in North America and Europe where banks operate mainframe cores; moderate in Asia-Pacific | Impact Timeline:Medium term (2-4 years) |

Data Privacy and Security Concerns Amid Strict Banking Regulations Data Privacy and Security Concerns Amid Strict Banking Regulations | -2.8% | Europe (GDPR, NIS2), North America (CCPA, state laws), Asia-Pacific (PDPA, PIPL) | Short term (≤ 2 years) | |||

Shortage of Domain-Specific Data Scientists in Smaller Banks Shortage of Domain-Specific Data Scientists in Smaller Banks | -1.9% | North America (community banks), Europe (regional savings banks), emerging markets | Long term (≥ 4 years) | |||

Model Risk Management Scrutiny Limiting Rapid Deployment of AI Models Model Risk Management Scrutiny Limiting Rapid Deployment of AI Models | -1.7% | North America (OCC SR 11-7), Europe (EBA AI guidelines), Asia-Pacific (MAS FEAT principles) | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

High Implementation Costs of Legacy Core System Integration

Regional banks in North America operate core systems that are on average 27 years old, with 43% still running on mainframes that lack real-time APIs, resulting in additional costs of USD 2 million to USD 5 million per analytics integration. European savings banks face similar COBOL-based barriers, forcing nightly batch exports that preclude sub-second fraud scoring. Vendor lock-in exacerbates costs as core providers charge per-transaction fees for data extraction, making high-volume analytics economically challenging.

Data Privacy and Security Concerns Amid Strict Banking Regulations

GDPR’s purpose-limitation clause obliges banks to justify every data field used in a model, narrowing feature sets and reducing predictive lift. NIS2 expands mandatory breach reporting to 24 hours, prompting institutions to extend security audits to every third-party cloud vendor and lengthening implementation timelines. State-level rules, such as California’s CCPA, fragment compliance, forcing multi-jurisdictional frameworks that complicate model training.

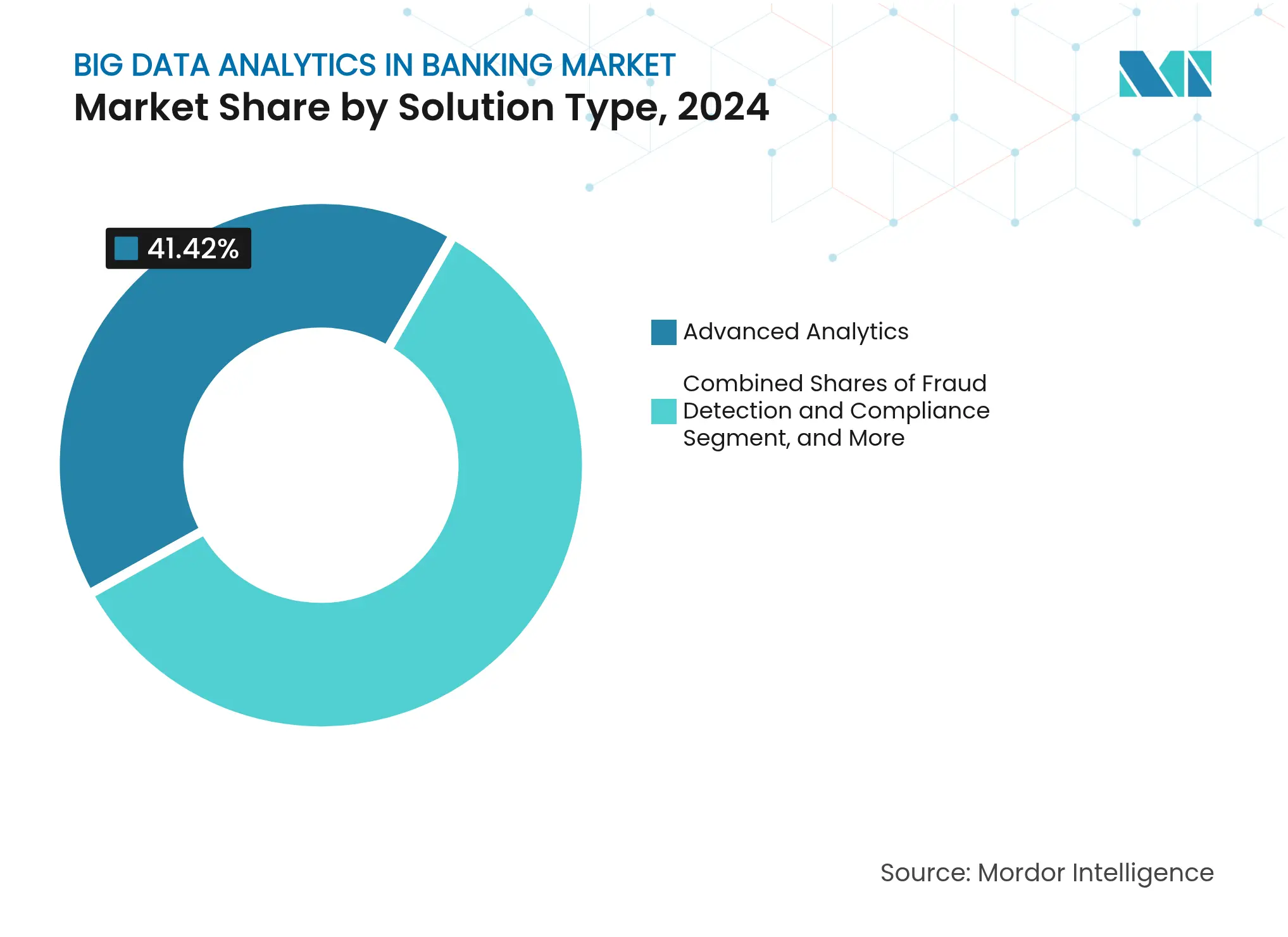

By Solution Type: Advanced Analytics Anchors Spend, Fraud Detection Surges

Advanced analytics generated 41.42% of 2024 revenue, reflecting widespread use of machine-learning models for credit underwriting, liquidity forecasting, and collateral optimization across the big data in banking market. Institutions continue upgrading feature-engineering pipelines and monitoring dashboards to manage drift in production models. Fraud detection and compliance solutions are expanding at a 24.52% CAGR, fueled by synthetic-identity attacks on instant-payment networks. Streaming analytics engines now score transactions against 200 behavioral vectors in under 100 milliseconds to satisfy mandatory pre-settlement checks in Brazil and India. Data-management suites, including catalogs and lineage trackers, underpin these capabilities by ensuring quality, traceability, and audit readiness required under DORA. Visualization tools round out the stack, providing business users with low-code access to dashboards that surface trends without requiring SQL knowledge.

Prescriptive analytics is gaining attention as banks automate loan pricing and intraday liquidity moves, shifting focus from prediction to recommended action. Vendors are embedding optimization solvers that factor in regulatory liquidity-coverage ratios and funding-cost curves. Explainability has become critical since 2024, when the European Banking Authority required transparent AI for customer-facing models. Platforms now bundle SHAP plots and counterfactual analysis to accelerate model-risk approvals. The result is a broader ecosystem where descriptive, predictive, and prescriptive modules coexist, enabling financial institutions to transition seamlessly across analytics maturity stages within the big data in banking market.

Note: Segment shares of all individual segments available upon report purchase

By Deployment Mode: Cloud Dominance Driven by Resilience Mandates

Cloud captured 48.53% of 2024 spending as banks sought to scale and achieve redundancy to meet operational resilience tests. Under DORA, EU institutions must show automated failover across two or more cloud regions, a stipulation that heavily favors hyperscalers. Adoption is reinforced by consumption-based pricing that aligns cost with usage, appealing to community banks. On-premise deployments persist in jurisdictions with stringent data-sovereignty rules or among banks burdened by monolithic cores that cannot stream data. Hybrid architectures are emerging as a transition strategy, with raw transaction data stored on-site while model training and scenario simulations run in the cloud.

The migration is reshaping vendor relationships. Hyperscalers bundle compliance tooling, key-management services, and AI accelerators, eroding the historical advantage of on-premise incumbents. Legacy providers now package containerized versions of their platforms to run on Kubernetes clusters, allowing banks to port workloads between private clouds and public regions. In the big data in banking market, cloud’s 25.31% forecast CAGR reflects not only technology economics but also the regulatory imperative to demonstrate resilience, traceability, and rapid recovery.

By Application: Risk Management Leads, Fraud Detection Accelerates

Risk management applications accounted for 29.66% of revenue in 2024 as Basel III’s capital formulas require daily exposure aggregation, stress testing, and scenario analysis. Banks ingest tick-level pricing feeds, collate collateral positions, and compute value-at-risk metrics in near real time. Fraud detection and compliance solutions, the fastest-growing slice at 24.64% CAGR, address rising synthetic-identity fraud on instant-payment rails. Ensemble models blend rule-based filters, anomaly detection, and neural networks to keep false positives below 2% while meeting sub-second latency targets. Customer analytics engines personalize product recommendations and boost cross-sell rates; wealth-management tools automate tax-loss harvesting and portfolio rebalancing for mass-affluent segments.

Generative AI is reshaping customer interaction workflows. Large language models fine-tuned on proprietary transaction data compose personalized financial summaries and answer natural-language queries. Relationship managers gain conversational interfaces that fetch credit exposure, product holdings, and upcoming maturities instantly. Within the big data in banking market, banks are reallocating budgets toward these AI-enabled front-office applications even as they maintain core investment in risk and compliance engines.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

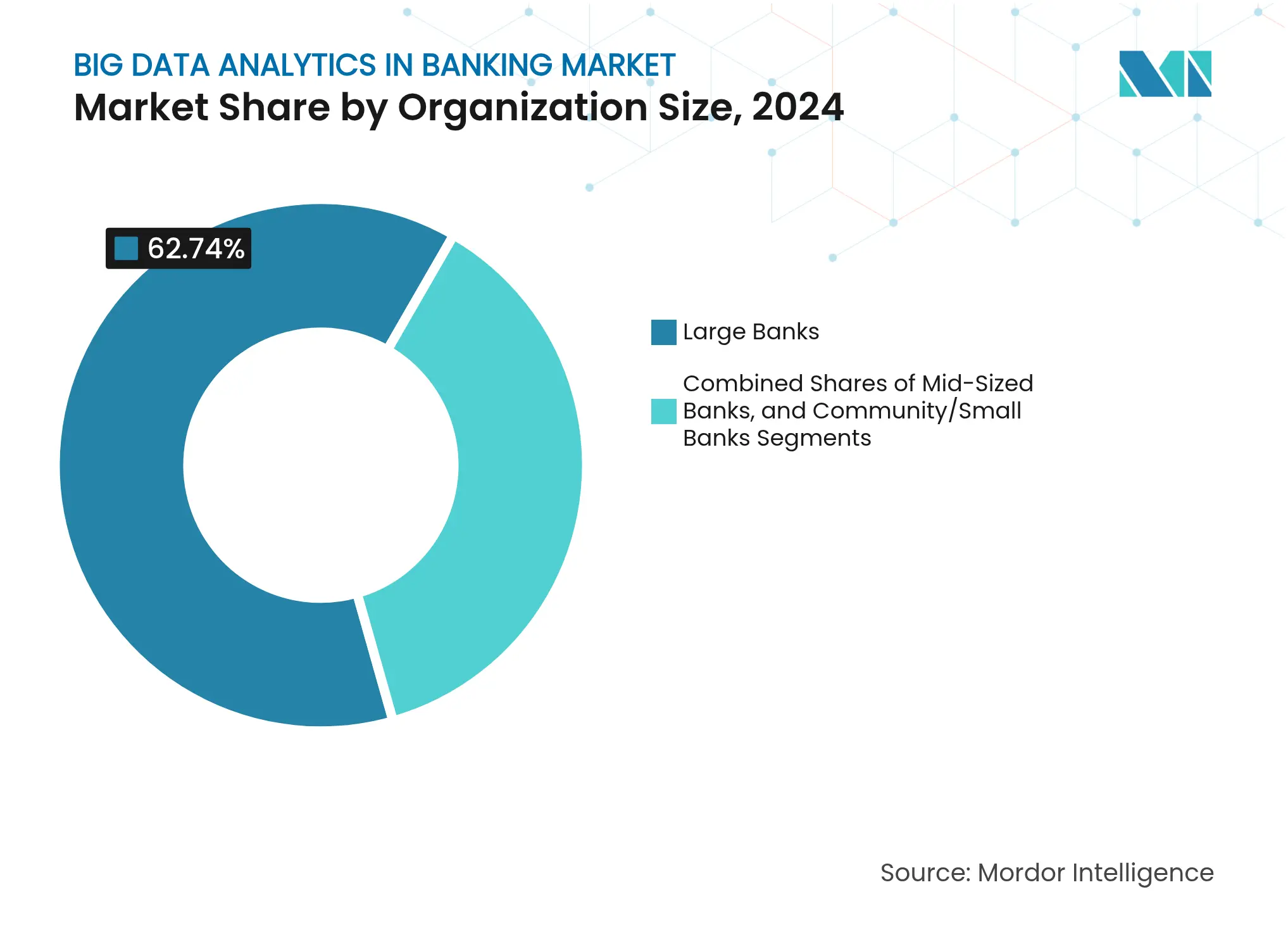

By Organization Size: Large Banks Dominate, Community Banks Catch Up

Large banks captured 62.74% of 2024 outlays, leveraging scale to maintain 200-plus data-science teams and annual analytics budgets that can exceed USD 200 million. Community institutions, however, are closing the capability gap thanks to cloud-based, consumption-priced platforms that eliminate capital expenditure. Their 25.23% CAGR reflects aggressive vendor outreach and shared-services initiatives that pool data-science talent. Mid-sized players straddle both worlds, benefiting from volume discounts yet struggling to match salary offers from money-center institutions.

The talent shortage remains acute. Median compensation for senior data scientists at regional banks trails large-bank peers by up to 40%, prompting reliance on automated machine-learning platforms that empower business analysts. Consortium models, such as the Independent Community Bankers of America shared-services network, are emerging to democratize expertise. As hyperscalers embed no-code model-building features, smaller institutions can deploy predictive engines without writing Python, further leveling the playing field across the big data in banking market.

Note: Segment shares of all individual segments available upon report purchase

By Analytics Technique: Predictive Models Prevail, Prescriptive Gains

Predictive analytics accounted for 46.76% of 2024 revenue, underscoring the maturity of credit-scoring, churn-prediction, and fraud-detection use cases across the big data in banking market. Models are refreshed weekly to combat drift driven by faster transaction cycles. Prescriptive analytics, advancing at 24.85% CAGR, is applied to intraday liquidity allocation, collateral optimization, and dynamic loan pricing. Optimization solvers integrate regulatory constraints and funding curve inputs to recommend low-cost funding sources in real-time. Descriptive and diagnostic modules remain essential for regulatory reporting and root-cause analysis, particularly under DORA’s automated incident-analysis requirement.

The shift toward prescriptive tooling is amplified by generative-AI interfaces that translate optimization outputs into plain-language recommendations for traders and treasury staff. Explainability remains front and center as OCC SR 11-7 demands transparency in model logic. Vendors bundle global-sensitivity graphs and counterfactual scenarios to satisfy auditors. Consequently, the big data in the banking market is moving from hindsight to foresight, and finally to real-time action.

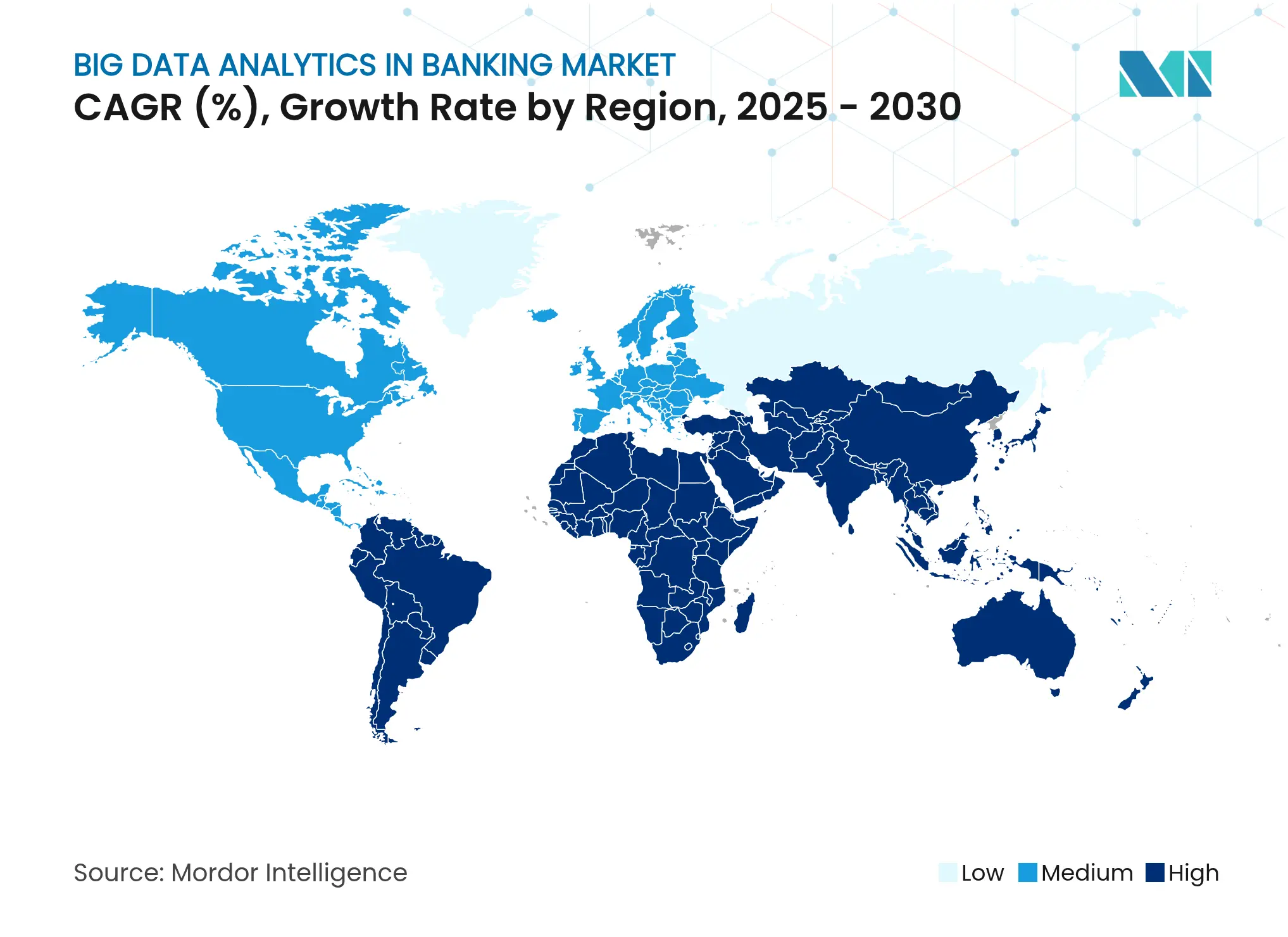

North America retained 40.32% of 2024 revenue, driven by FedNow’s launch and stringent OCC model-risk guidelines that force banks to invest USD 5 million to USD 15 million annually in validation tooling. Canadian regulators are finalizing an open-banking framework, prompting banks to build API gateways and consent dashboards ahead of a 2025 deadline. Mexico’s sandbox for AI credit scoring encourages the use of graph analytics that leverage mobile-phone and utility data to underwrite borrowers from underserved communities.

Asia-Pacific is the fastest-growing geography at 25.98% CAGR. India’s UPI generates monthly datasets of 2.1 petabytes that feed real-time fraud engines and merchant-risk scorers. The Account Aggregator network covers 1.4 billion accounts, obliging lenders to ingest consented cash-flow histories within seconds. China mandates streaming anti-money laundering analytics on digital yuan wallets, while Japan’s sandbox accelerates AI wealth advisory pilots. ASEAN payment-rail interoperability further increases demand for cross-border fraud and FX risk dashboards.

Europe’s growth is anchored in DORA and the forthcoming Financial Data Access framework, which will force banks to share enriched transaction feeds by 2026. The United Kingdom’s digital sandbox lets firms validate compliance models on synthetic data, slashing validation cycles from six months to six weeks. South America benefits from Brazil’s PIX rule that mandates pre-settlement fraud checks, pushing local banks toward ensemble analytics while Middle East growth is propelled by Saudi Arabia’s Cloud First policy requiring new workloads to run on public or hybrid cloud. Africa remains nascent, with South Africa piloting AI credit-scoring sandboxes.

Market Concentration

The big data in banking market is fragmented. Hyperscalers such as AWS, Microsoft, and Google Cloud dominate infrastructure, embedding generative AI services like Amazon Q, Azure OpenAI, and Anti-Money Laundering AI that enable banks to deploy sophisticated models without building in-house engines. Legacy vendors, including IBM, Oracle, and SAP, defend their installed bases with containerized, hybrid offerings that maintain on-premises data sovereignty. Niche fintechs, including ThetaRay, DataRobot, and Alteryx, target high-growth subsegments such as synthetic-fraud detection, automated machine learning, and no-code workflow orchestration.

White space remains in prescriptive treasury analytics, where 70% of liquidity decisions still rely on manual processes, despite having access to real-time collateral data. Vendors providing optimization engines that automate intraday funding and collateral swaps stand to gain. Explainable AI is another growth pocket as EBA guidelines mandate transparency, spurring demand for SHAP-based visualizations and counterfactual generators. Competitive intensity is high, but the market’s rapid expansion leaves room for both incumbents and disruptors.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

Big data analytics can help banks understand customer behavior based on the inputs received from various insights, including investment patterns, shopping trends, motivation to invest, and personal or financial background. With the advancement in big data analytics, banks can analyze market trends and make informed decisions related to adjusting interest rates for individuals across various regions. With the help of big data analytics, financial services are actively utilizing it to store data, derive business insights, and enhance scalability as the volume of electronic records increases.

The Big Data in Banking Market Report is Segmented by Solution Type (Data Discovery and Visualization, Advanced Analytics, Data Management, Fraud Detection and Compliance Analytics), Deployment Mode (On-Premise, Cloud, Hybrid), Application (Risk Management, Customer Analytics, Fraud Detection and Compliance, Wealth Management and Advisory), Organization Size (Large Banks, Mid-Sized Banks, Community/Small Banks), Analytics Technique (Descriptive, Diagnostic, Predictive, Prescriptive), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

Unlocking Saudi Arabia’s Regional Tourism Growth Potential

5 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.