Advanced Airport Technologies Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

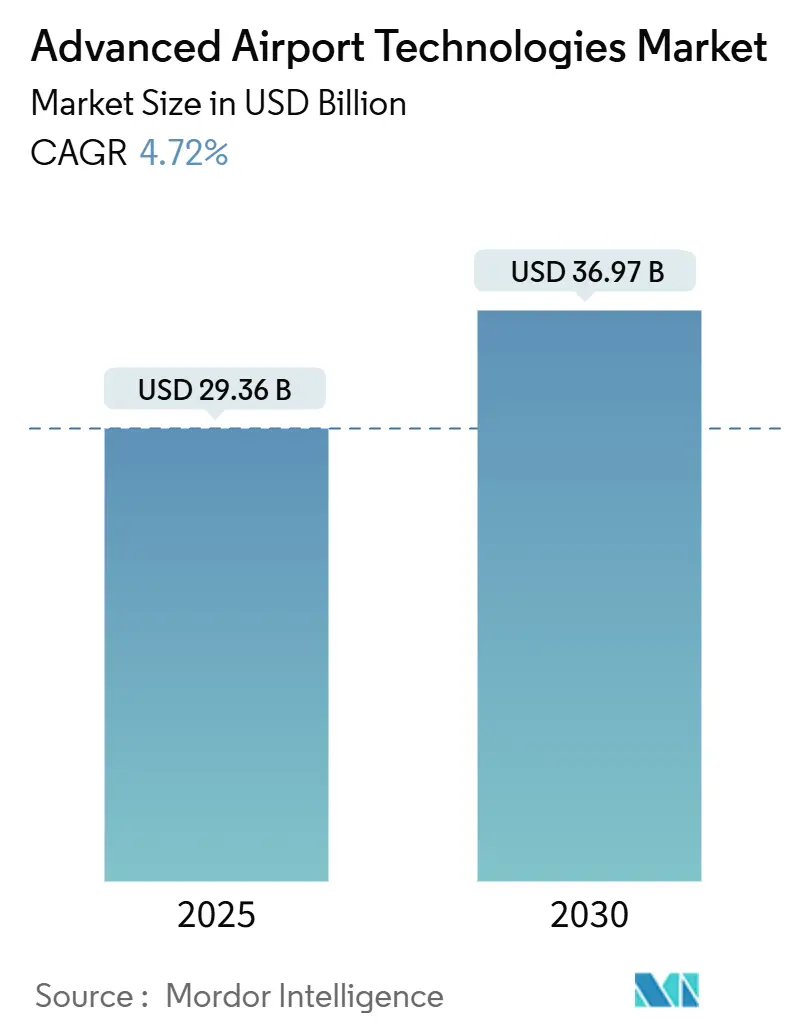

| Market Size (2025) | USD 29.36 Billion |

| Market Size (2030) | USD 36.97 Billion |

| Growth Rate (2025 - 2030) | 4.72% CAGR |

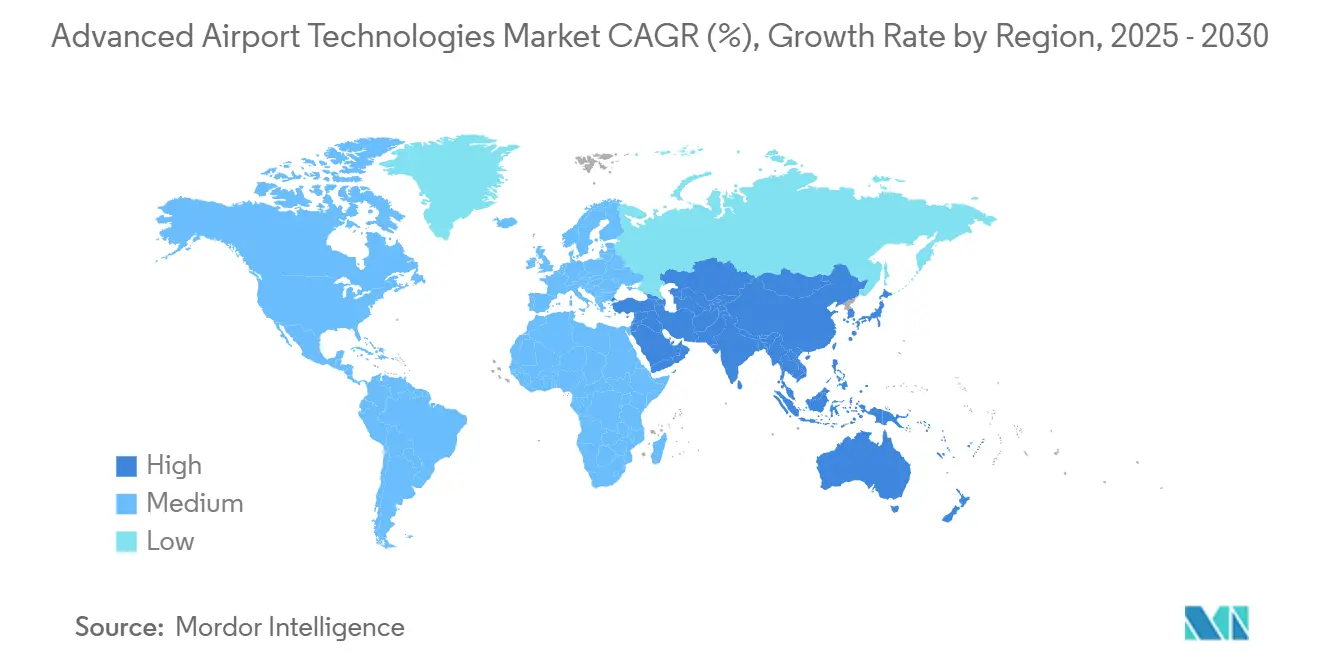

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Advanced Airport Technologies Market Analysis by Mordor Intelligence

The advanced airport technologies market stands at USD 29.36 billion in 2025, and forecasts indicate expansion to USD 36.97 billion by 2030 at a 4.72% CAGR. Robust passenger-traffic recovery, mandatory security upgrades, and digital transformation spending continue to anchor purchasing decisions. Airports favor deployments that raise throughput and cut operating costs, giving security and screening platforms a stable revenue base, while cloud platforms and biometrics generate the steepest growth curves. Budget-constrained regional facilities lean on SaaS models and vendor financing, whereas hub airports refresh legacy systems to satisfy sustainability and resilience targets. Competitive dynamics remain moderate, with diversified conglomerates acquiring niche innovators to secure AI and automation expertise.

Key Report Takeaways

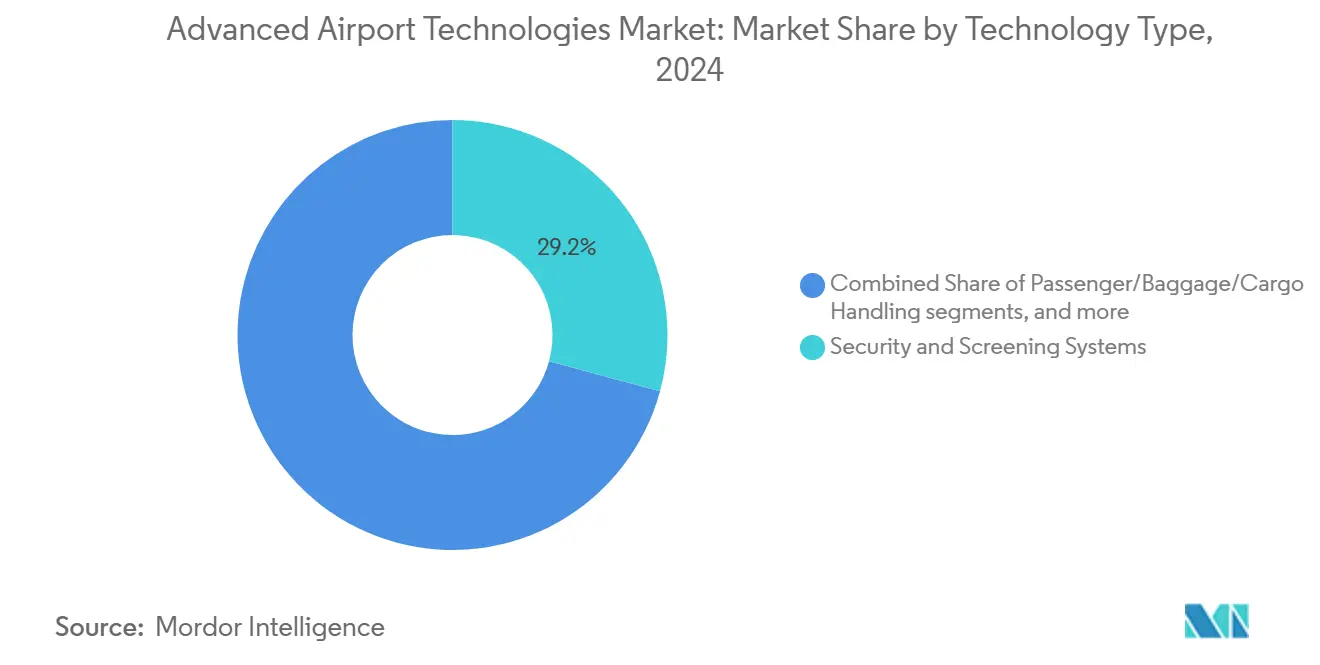

- By technology type, security and screening systems led with 29.21% of the advanced airport technologies market share in 2024; biometric passenger identification is projected to record a 6.25% CAGR through 2030.

- By operation area, terminal-side systems controlled 44.19% revenue in 2024, while air-side solutions are advancing at a 5.84% CAGR to 2030.

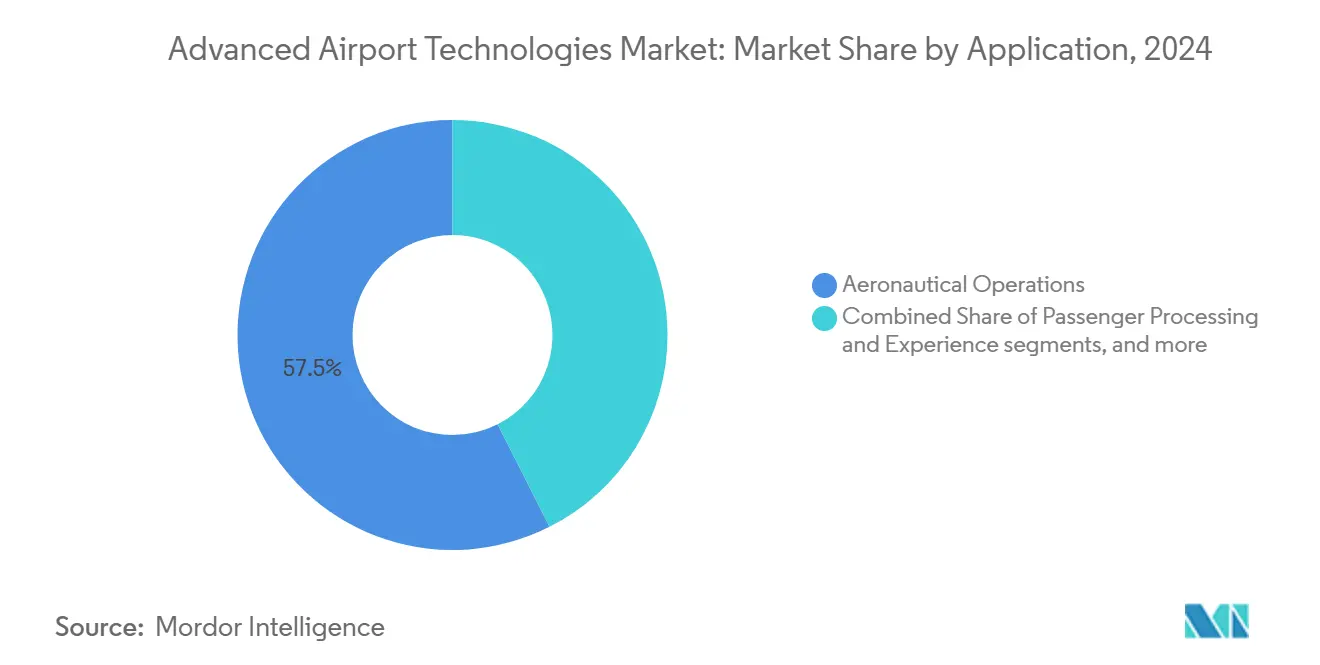

- By application, aeronautical operations held a 57.45% share of the advanced airport technologies market in 2024; smart retail and non-aeronautical platforms will accelerate at a 6.12% CAGR to 2030.

- By airport size, Class A hubs (greater than 25 million passengers per annum (mppa)) captured 35.79% of the advanced airport technologies market size in 2024; small and regional airports (less than 5 mppa) are expanding at a 6.33% CAGR through 2030.

- By deployment mode, on-premise systems retained 57.32% of spending in 2024, yet cloud and SaaS offerings are growing at a 5.88% CAGR to 2030.

- By geography, North America commanded 34.58% market share in 2024, yet Asia-Pacific exhibits the fastest growth at 7.15% CAGR to 2030.

Global Advanced Airport Technologies Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing air-passenger volumes and green-field airport projects | +1.2% | Global, strongest impact in Asia-Pacific and Middle East | Medium term (2-4 years) |

| Stringent global aviation-security mandates (ICAO, TSA, EASA) | +0.9% | Global, immediate impact in North America and Europe | Short term (≤ 2 years) |

| Rapid biometrics roll-outs for seamless passenger journey | +0.8% | North America and EU leading, Asia-Pacific accelerating | Medium term (2-4 years) |

| Demand for real-time data to cut turnaround-times | +0.6% | Global, early adoption in major hub airports | Short term (≤ 2 years) |

| Digital-twin adoption for remote ops and predictive maintenance | +0.4% | North America and EU core, spill-over to Asia-Pacific | Long term (≥ 4 years) |

| ESG-linked airport-financing favoring low-carbon tech | +0.3% | Europe leading, North America and Asia-Pacific following | Long term (≥ 4 years) |

Source: Mordor Intelligence

Growing Air-Passenger Volumes and Green-Field Airport Projects

According to ACI-World, global passenger traffic surpassed pre-pandemic levels in 2024 and reached 9.4 billion journeys, generating urgent capacity needs. Mega projects such as Singapore’s Changi Terminal 5, launched in May 2025, embed automated baggage flows, smart building controls, and solar power from day one.[1]Singapore Press Holdings, “Changi Terminal 5 Ground-breaking,” straitstimes.com This design-phase integration lets operators bypass costly retrofits and elevates baseline technology expectations for every subsequent expansion. Emerging-market governments fund similar builds, driving the advanced airport technologies market toward integrated, cloud-ready platforms that scale with traffic.

Stringent Global Aviation-Security Mandates (ICAO, TSA, EASA)

The European Union's (EU's) computed-tomography deadline and TSA's capital plan through 2029 lock in the procurement of advanced screening equipment. ICAO's 2024 Security Week endorsed AI-enhanced threat detection, creating a common playbook across jurisdictions. Harmonized rules lower customization costs, enlarge addressable volumes, and encourage bulk purchasing, lifting the advanced airport technologies market in every region. Smaller airports, however, face timetable pressure, accelerating partnerships with equipment vendors that offer pay-as-you-go models.

Rapid Biometrics Roll-Outs for Seamless Passenger Journey

Facial-recognition lanes operate at more than 400 US airports, and 79% of travelers endorse their use.[2]Phocuswire, “Traveler Attitudes Toward Biometric ID,” phocuswire.com Airports link biometric checkpoints to retail-loyalty platforms, converting shorter queues into incremental spend. BigBear.ai’s veriScan pilot at Denver and Delta’s digital-ID rollout in Salt Lake City demonstrate dwell-time drops and higher concession yields. With over 50% of airports planning deployments by 2026, the advanced airport technologies market anticipates biometrics shifting from pilot status to baseline requirement.

Demand for Real-Time Data to Cut Turnaround Times

Copenhagen Airports’ Total Airport Management suite trimmed average departure delays by 6.5 minutes, saving USD 540,582 in six months.[3]Regional Gateway, “Copenhagen Airport and Assaia Launch TAM Solution,” regionalgateway.netAI-driven ApronAI delivers predictive alerts that permit an extra aircraft turn per gate daily, translating to revenue and carbon reductions. Private 5G networks enhance spatial efficiency by up to 50%, while autonomous pushback vehicles lower taxi delays by 70%. Such quantifiable returns underpin capital cases, propelling the advanced airport technologies market toward data-centric investments.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX and long payback periods | -0.8% | Global, strongest impact on smaller airports | Medium term (2-4 years) |

| Escalating cybersecurity and data-privacy risks | -0.6% | Global, heightened concern in North America and Europe | Short term (≤ 2 years) |

| Legacy-IT integration complexity | -0.4% | North America and Europe primarily, limited impact in green-field markets | Medium term (2-4 years) |

| Passenger-consent bottlenecks for biometrics | -0.2% | Europe and privacy-conscious markets | Short term (≤ 2 years) |

Source: Mordor Intelligence

High CAPEX and Long Payback Periods

Revenues at many airports remain below 2019 peaks, tightening discretionary budgets. Class C facilities struggle to finance CT scanners that exceed USD 3 million per lane, slowing penetration. ESG-linked bonds and airport-as-a-service contracts soften upfront outlays, illustrated by Vienna Airport’s CO₂-neutral financing pathway. Nevertheless, extended payback horizons temper the advanced airport technologies market, especially where service fees cannot be raised.

Escalating Cybersecurity and Data-Privacy Risks

Airports ranked cybersecurity as the top IT focus for 73% of respondents in 2025, yet skill shortages stretch deployment timelines.[4]SITA, “SITA Acquires CCM to Integrate Technology with Design,” airport-technology.com Ransomware attacks on baggage-handling control systems highlight operational exposure. Privacy rules like the US Traveler Privacy Protection Act impose opt-in and deletion mandates, adding integration complexity. Compliance costs shave growth from the advanced airport technologies industry until standardized frameworks mature.

Segment Analysis

By Technology Type: Security Dominance Amid Biometric Disruption

Security and screening systems accounted for 29.21% of the advanced airport technologies market share in 2024, underpinned by EU-wide CT mandates that guarantee equipment placement. This segment supplies reliable recurring service revenues and replacement cycles that stabilize vendor pipelines. The advanced airport technologies market size for security and screening reached USD 8.8 billion in 2025 and is forecast to post mid-single-digit gains through 2030.

Though smaller in 2025, biometric passenger identification platforms expanded at a 6.25% CAGR as airports link seamless ID to duty-free conversion rates. Hybrid solutions that fuse biometrics with threat-detection analytics attract bundled contracts, edging incumbent X-ray suppliers toward software partnerships. Baggage, cargo, and passenger-flow management software, embedding analytics into formerly hardware-only workflows, rides the same adoption wave. Ground-handling electrification also reshapes procurement; Shenzhen Airport’s 100% new-energy vehicle goal signals that environmental targets now influence specification sheets.

Note: Segment shares of all individual segments available upon report purchase

By Operation Area: Terminal Efficiency Versus Airside Innovation

Terminal-side systems represented 44.19% of the advanced airport technologies market size in 2024, reflecting concentrated passenger touchpoints. Checkpoint biometrics, digital signage, and smart retail software deliver throughput and ancillary revenue, making terminals the first investment priority.

Air-side applications, while smaller, recorded a 5.84% CAGR and increasingly integrate with terminal platforms via digital twins. Saab’s cloud-based runway-safety system at Nashville provides real-time alerts in line with FAA surface-awareness goals.[5]Saab AB, “Cloud-Based Runway Safety System Operational at Nashville,” saab.com Air-side gains are amplified by AI-driven gate allocation that trims taxi times, lowering Scope 1 emissions. Landside mobility systems, including smart parking PARCS installed at Charleston, unlock last-mile monetization and data capture, rounding out holistic airport-wide platforms.

By Application: Aeronautical Operations Lead Smart Retail Surge

Aeronautical operations and ATC/ATM commands a 57.45% share, reflecting mandatory safety spending and NextGen program rollouts. The advanced airport technologies market size for this application segment is projected to reach USD 22 billion by 2030, growing with the US FAA’s USD 16.5 billion budget for system modernization.

Smart retail and non-aeronautical platforms posted a 6.12% CAGR as airports pivot toward diversified income. Real-time location analytics allow concessionaires to tailor offerings, boosting per-passenger spend. Passenger-processing tools piggyback on biometric corridors, and asset-management software exploits IoT sensors to predict maintenance needs, aligning with lean staffing.

Note: Segment shares of all individual segments available upon report purchase

By Airport Size/Class: Hub Spending Versus Regional Growth

Class A hubs (greater than 25 mppa) represented 35.79% of the advanced airport technologies market size in 2024, leveraging cash flows to adopt AI orchestration platforms. These airports act as proving grounds for biometrics and digital twins before scaling downstream.

Small and Regional airports (less than 5 mppa) deliver 6.33% CAGR through 2030, propelled by government grants and cloud subscriptions that bypass on-site IT investment. McGhee Tyson’s smart parking system, live within three days, typifies quick-turn projects that enhance service without extensive capital. Medium airports balance constraints by prioritizing single-pane dashboards over siloed point solutions.

By Deployment Mode: Cloud Transformation Accelerates

On-premise architectures held 57.32% of spending in 2024, driven by stringent control requirements. Yet cloud and SaaS solutions grow at 5.88% CAGR, aided by aviation-focused compliance frameworks. The advanced airport technologies market share for cloud models rises sharply in regions building green-field terminals free of legacy stacks.

Hybrid models will gain favor as airports shift analytics and passenger interfaces off-site while retaining critical command functions on-premise. SITA’s acquisition of CCM to blend design and cloud technology underscores vendor convergence toward “airport-in-a-box” offerings.

Geography Analysis

North America retained 34.58% of 2024 revenue, supported by TSA’s multiyear capital plan prioritizing biometrics and vetting systems. US hub airports pioneer frictionless ID pilots, and Vancouver’s digital-innovation push shows similar momentum. However, saturation tempers growth to low single digits. Canada’s airports leverage climate-resilience funds for energy-efficient retrofits, accelerating LED lighting and electrified ground fleets.

Europe sustains sizable demand through harmonized regulation and ESG imperatives. The EU CT scanner mandate secures new installs, while Vienna Airport’s net-zero roadmap channels spending into photovoltaic and electric ground service equipment. Passenger traffic rose 9% year-on-year in the first half of 2024, yet 47% of airports remain below 2019 levels, highlighting uneven recovery. Sustainability-linked financing and Fit-for-55 infrastructure rules drive conversion to smart-grid-ready assets.

Asia-Pacific is the fastest-growing theater at 7.15% CAGR, energized by India’s 174 million travelers in 2024 and a massive portfolio of new airports. Changi Terminal 5’s USD 3.5 billion build embeds robotics and AI, setting a regional benchmark. Incheon aims for 100% renewable electricity by 2040, boosting orders for smart-energy management systems. China’s multi-city expansions and South Korea’s RE100 commitments amplify opportunity, making the region the fulcrum of the advanced airport technologies market through 2030.

Competitive Landscape

Established multi-industry players such as Honeywell International, Inc., Cisco Systems, Inc., Thales Group, Amadeus IT Group SA, Siemens AG, and SITA command gateway relationships and broad portfolios, allowing cross-selling across security, communications, and building-automation layers. 2025 witnessed consolidation: Vanderlande moved to acquire Siemens Logistics to secure baggage-handling automation, and Toyota Industries invested USD 1.5 trillion (FY 2025-2027) in airport-linked logistics technologies, reflecting scale-driven competition.

Disruptors concentrate on narrow, high-value niches. Assaia captured visibility with ApronAI deployments, cutting delays by 6% and increasing turns by 4%. BigBear.ai leverages computer vision for biometric boarding that speeds gates without hardware overhauls. These firms win by proving ROI within six-month cycles, an attractive proposition for CFO-led procurement committees.

Cloud platform convergence reshapes vendor roles. SITA’s April 2025 acquisition of CCM integrates design, interiors, and IT into turnkey packages, signaling a shift from standalone software toward holistic delivery. Market barriers remain moderate; switching costs favor incumbents, yet airports demand open APIs, enabling specialists to interoperate. Competitive intensity focuses on AI capability, cybersecurity certifications, and sustainability credentials, factors that now differentiate bids as much as price.

Advanced Airport Technologies Industry Leaders

-

Thales Group

-

SITA

-

Siemens AG

-

Amadeus IT Group, S.A.

-

Honeywell International, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: SITA acquired CCM to enhance integrated airport design and cloud platforms.

- April 2025: IP Parking delivered a plug-and-play PARCS at Charleston International Airport, operational in three days .

- December 2024: GMR Airports launched an AI-powered digital twin at Rajiv Gandhi International Airport.

Global Advanced Airport Technologies Market Report Scope

Advanced airport technologies refer to cutting-edge innovations and systems designed to enhance efficiency, safety, and passenger experience at airports. These technologies may include biometric authentication, autonomous vehicles, smart baggage handling, AI-powered security screening, and advanced air traffic management solutions, revolutionizing the way airports operate and deliver services.

The advanced airport technologies market is segmented by type and by geography. By type, the market is segmented into airport communications, airport management software, car parking systems, passenger, baggage, and cargo handling control systems, airport digital signage systems, and landing aids, guidance, and lighting. By geography, the market is segmented into North America, Europe, Asia-Pacific, Latin America, and Middle-East and Africa.

The report offers market size and forecasts for all the above segments in value (USD)

| By Technology Type | Airport Communications Systems | |||

| Airport Management Software | ||||

| Passenger/Baggage/Cargo Handling | ||||

| Security and Screening Systems | ||||

| Ground and Airside Handling Equipment | ||||

| Landing Aids, Guidance and Lighting | ||||

| Airport Digital Signage Systems | ||||

| Smart Parking and Landside Mobility Solutions | ||||

| By Operation Area | Terminal-side | |||

| Air-side | ||||

| Land-side | ||||

| By Application | Passenger Processing and Experience | |||

| Aeronautical Operations and ATC/ATM | ||||

| Asset and Facility Management | ||||

| Smart Retail and Non-Aeronautical Revenue Solutions | ||||

| By Airport Size/Class | Class A (Greater than 25 mppa) Large Hubs | |||

| Class B (5 to 25 mppa) Medium Airports | ||||

| Class C (Less than 5 mppa) Small and Regional Airports | ||||

| By Deployment Mode | On-premise/Proprietary | |||

| Cloud and SaaS | ||||

| By Geography | North America | United States | ||

| Canada | ||||

| Mexico | ||||

| Europe | Germany | |||

| United Kingdom | ||||

| France | ||||

| Italy | ||||

| Rest of Europe | ||||

| Asia-Pacific | China | |||

| Japan | ||||

| India | ||||

| South Korea | ||||

| Rest of Asia-Pacific | ||||

| South America | Brazil | |||

| Rest of South America | ||||

| Middle East and Africa | Middle East | United Arab Emirates | ||

| Saudi Arabia | ||||

| Rest of Middle East | ||||

| Africa | South Africa | |||

| Egypt | ||||

| Rest of Africa | ||||

| Airport Communications Systems |

| Airport Management Software |

| Passenger/Baggage/Cargo Handling |

| Security and Screening Systems |

| Ground and Airside Handling Equipment |

| Landing Aids, Guidance and Lighting |

| Airport Digital Signage Systems |

| Smart Parking and Landside Mobility Solutions |

| Terminal-side |

| Air-side |

| Land-side |

| Passenger Processing and Experience |

| Aeronautical Operations and ATC/ATM |

| Asset and Facility Management |

| Smart Retail and Non-Aeronautical Revenue Solutions |

| Class A (Greater than 25 mppa) Large Hubs |

| Class B (5 to 25 mppa) Medium Airports |

| Class C (Less than 5 mppa) Small and Regional Airports |

| On-premise/Proprietary |

| Cloud and SaaS |

| North America | United States | ||

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the 2025 value of the advanced airport technologies market?

The market is valued at USD 29.36 billion in 2025 and is forecast to reach USD 36.97 billion by 2030, reflecting a 4.72% CAGR.

Which segment grows the fastest within the advanced airport technologies market?

Biometric Passenger Identification leads with a 6.25% CAGR through 2030 as airports pursue seamless passenger journeys.

Why are cloud deployments accelerating at airports?

Cloud platforms cut upfront costs, offer scalability, and meet new compliance frameworks, driving an 5.88% CAGR to 2030.

Which region offers the strongest growth prospects?

Asia-Pacific posts a 7.15% CAGR, supported by large-scale green-field construction and rapid passenger recovery.

How are cybersecurity concerns influencing technology buying?

With 73% of airports ranking cybersecurity as a priority, solutions that meet stringent data-protection rules gain procurement preference.