Glass Fiber Reinforced Gypsum Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

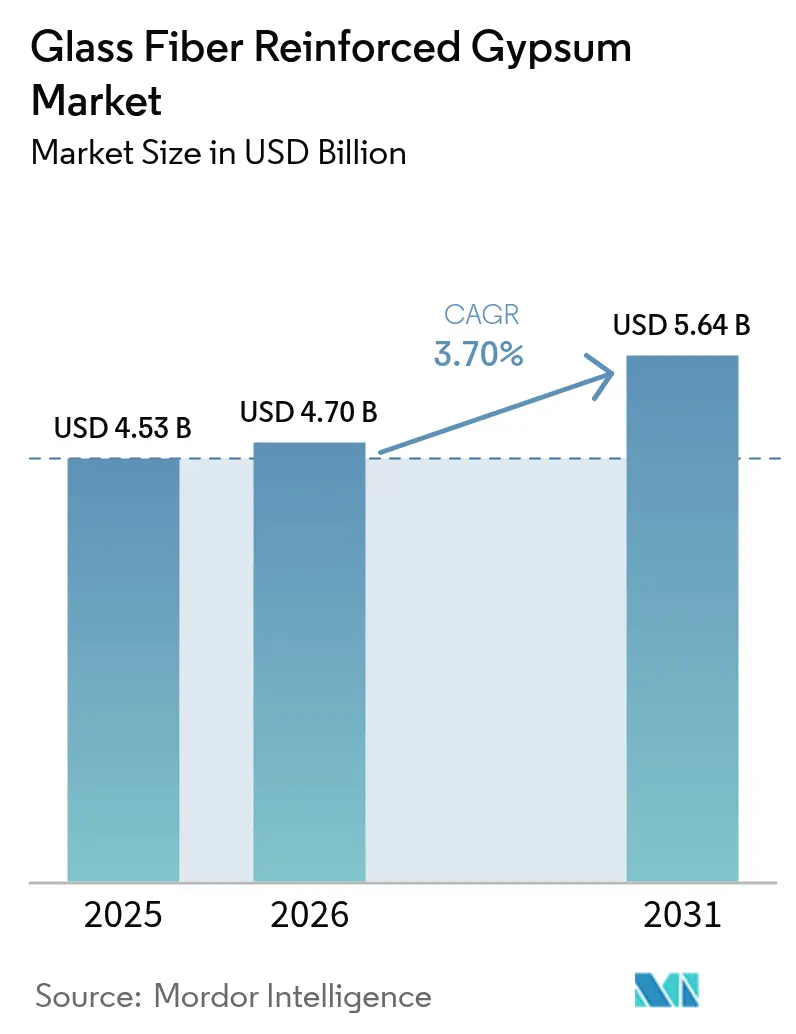

| Market Size (2026) | USD 4.7 Billion |

| Market Size (2031) | USD 5.64 Billion |

| Growth Rate (2026 - 2031) | 3.70% CAGR |

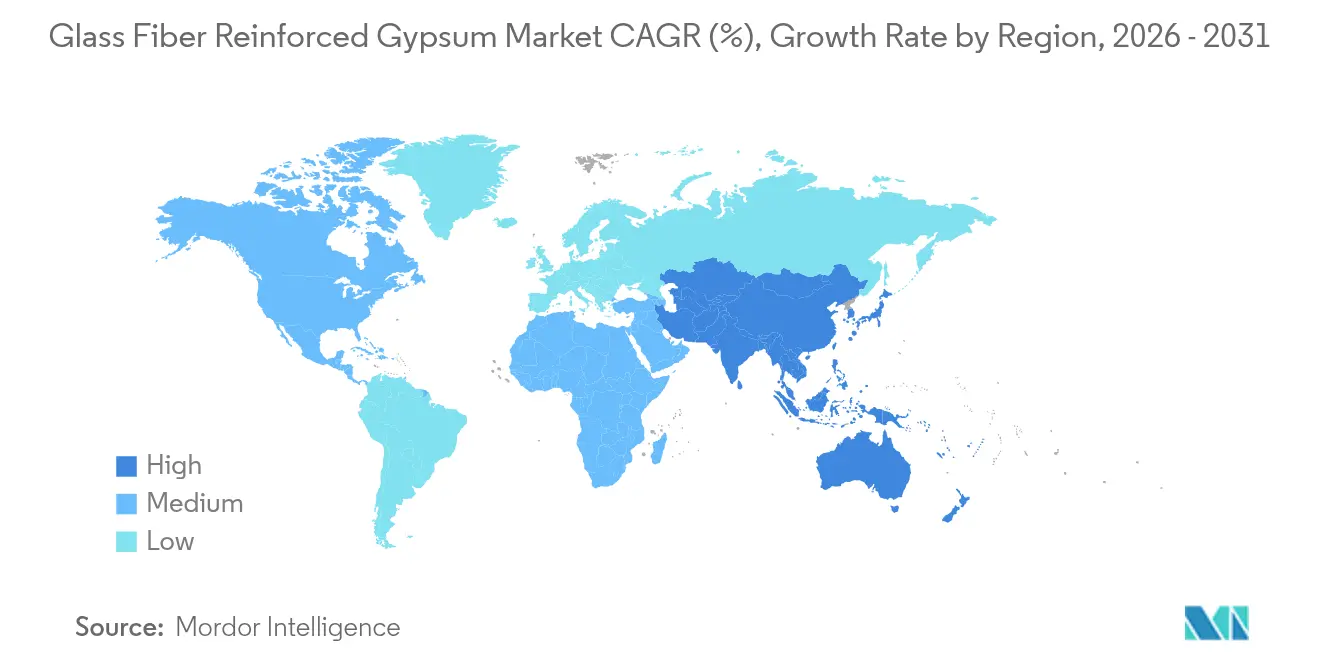

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

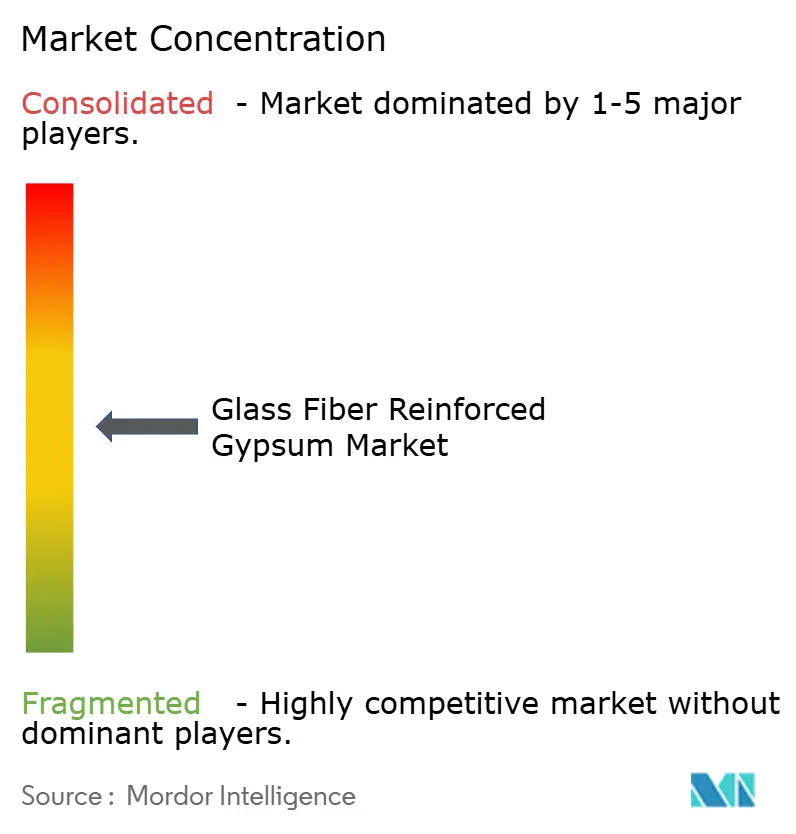

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Glass Fiber Reinforced Gypsum Market Analysis by Mordor Intelligence

The Glass Fiber Reinforced Gypsum Market size was valued at USD 4.53 billion in 2025 and estimated to grow from USD 4.70 billion in 2026 to reach USD 5.64 billion by 2031, at a CAGR of 3.70% during the forecast period (2026-2031). Momentum comes from stricter fire-safety rules, corporate sustainability targets, and the material’s lower installed cost compared with conventional drywall. Non-residential demand is recovering faster than broader construction output, while premium interior aesthetics and wellness-oriented design continue to lift specification rates. Supply diversification into natural gypsum quarries mitigates the decline of synthetic gypsum sourced from coal power plants, and product innovation in ultra-lightweight and moisture-resistant boards is broadening the application envelope. Asia-Pacific remains the primary growth engine, benefiting from urbanization, infrastructure investment, and government-sponsored affordable-housing programs.

Key Report Takeaways

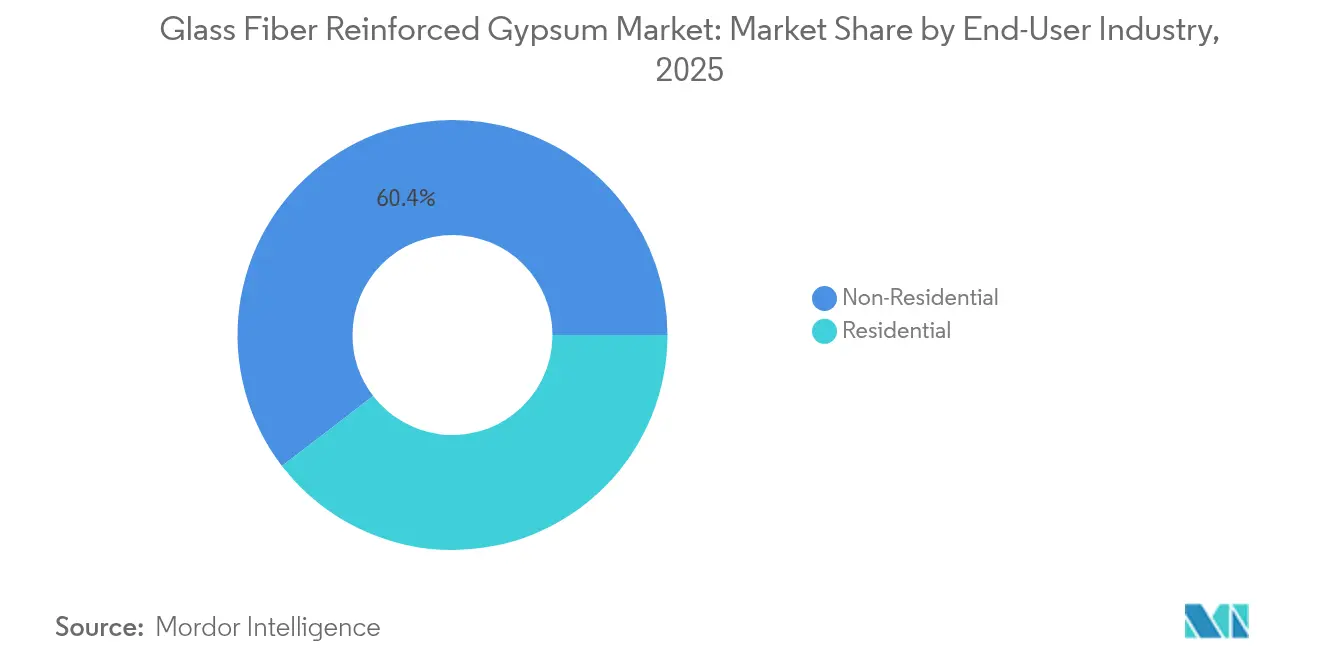

- By end-user industry, non-residential construction accounted for 60.42% of the glass fiber reinforced gypsum market share in 2025 and is expanding at 4.26% CAGR through 2031.

- By application, interior installations held 54.67% of the glass fiber reinforced gypsum market size in 2025, whereas exterior applications are projected to grow at 4.32% CAGR to 2031.

- By product type, fire-rated boards led with 36.74% revenue share in 2025; ultra-lightweight and specialty grades post the fastest 4.55% CAGR forecast.

- By geography, Asia-Pacific dominated with 43.86% revenue share in 2025 and is paced to grow at 3.86% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Glass Fiber Reinforced Gypsum Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lower installation & life-cycle cost advantage | +0.80% | Global, with stronger impact in Asia-Pacific and emerging markets | Medium term (2-4 years) |

| Rising demand for premium interior aesthetics | +0.60% | North America & Europe core, expanding to Asia-Pacific urban centers | Short term (≤ 2 years) |

| Stringent fire-safety building codes | +0.40% | Global, with accelerated adoption in North America and Europe | Long term (≥ 4 years) |

| Valorization of flue-gas-desulfurization (FGD) gypsum waste | +0.30% | North America & Europe, with emerging applications in Asia-Pacific | Medium term (2-4 years) |

| Government-led affordable-housing pilots adopting GFRG | +0.20% | Asia-Pacific core, with spillover to Latin America and MEA | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Lower Installation & Life-Cycle Cost Advantage

Glass fiber reinforced gypsum weighs less than traditional gypsum board, trims structural loads, and accelerates installation, thereby cutting labor outlays and project schedules. Retrofit projects benefit most because lighter panels allow direct attachment over existing substrates without extensive reinforcement. The boards also resist impact, abrasion, and mold growth, reducing maintenance frequency and extending refurbishment cycles. Developer focus on total cost of ownership in Asia-Pacific, where labor costs are rising, is intensifying interest in the material. Manufacturers highlight additional savings tied to lower embodied carbon, which can help building owners meet green-building certification thresholds. These combined advantages lift specification rates in both new-build and renovation markets.

Rising Demand for Premium Interior Aesthetics

High-end residential towers, hospitality venues, and corporate offices increasingly specify intricate ceiling coffers, curved walls, and monolithic column enclosures that conventional gypsum cannot deliver economically. GFRG enables such complex geometries while maintaining a smooth finish suitable for direct decoration. The boards achieve low formaldehyde and VOC emissions, aligning with WELL and LEED interior air-quality credits, a priority in healthcare and education facilities. Armstrong World Industries reported a 40.8% year-on-year jump in architectural specialties revenue in 2024, illustrating fast adoption of premium gypsum solutions. Design-laden urban markets such as New York, London, Shanghai, and Dubai are fueling the trend, and the aesthetic pull-through accelerates as digital fabrication techniques make custom molds more economical.

Valorization of Flue-Gas-Desulfurization (FGD) Gypsum Waste

Coal-fired utilities historically supplied synthetic gypsum captured from SO₂ scrubber systems, diverting millions of tons from landfill into wallboard production. Pilot studies show mineralization efficiencies exceeding 92% when ionic strength is optimized, underscoring the technical viability of the waste-to-resource route[1]Tan Wenyi, “Flue Gas Desulfurization Gypsum Mineralization in Waste Lye,” nature.com . As coal plants retire, supply tightens, prompting producers to diversify toward natural deposits. USG’s new Avery Quarry in Michigan is slated to yield 550,000 tons in 2025, safeguarding raw-material continuity for Mid-western plants[2]Saint-Gobain Canada, “CarbonLow Wallboard Line Press Release,” saint-gobain.com Source: USG, “Avery Quarry Opening,” usg.com . The valorization narrative remains powerful in jurisdictions where industrial waste regulation and circular-economy incentives overlap, chiefly North America and Europe.

Government-Led Affordable-Housing Pilots Adopting GFRG

In India, multi-story social-housing schemes have started specifying GFRG sandwich panels for load-bearing walls, reducing build times and embodied carbon compared with brick-and-mortar solutions. Similar pilot projects are underway in Indonesia and Brazil, supported by grants that reward innovative, cost-effective materials. Asian and Latin American ministries view the panels as an avenue to accelerate delivery of durable, fire-safe residences while uplifting construction productivity. Long-term impact is significant because positive pilot results often translate into prescriptive inclusion in national housing codes or public-procurement guidelines.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Low consumer & installer awareness in emerging regions | -0.40% | Asia-Pacific emerging markets, Latin America, MEA | Medium term (2-4 years) |

| Moisture-susceptibility concerns in high-humidity climates | -0.30% | Southeast Asia, tropical regions, coastal areas globally | Short term (≤ 2 years) |

| Shortage of skilled labour for complex GFRG mouldings | -0.50% | Global, with acute impact in North America and Europe, emerging challenges in Asia-Pacific urban centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Low Consumer & Installer Awareness in Emerging Regions

Carpenters and drywall crews in secondary Chinese cities, rural India, and sub-Saharan Africa often default to wood or masonry because training materials for GFRG are scarce. Misapplication—such as omitting sealant on panel joints—can lead to cracking, reinforcing negative perceptions. Manufacturers sponsor on-site clinics and digital modules to bridge the skills gap, yet uptake outside capital cities is gradual. The knowledge deficit limits order volumes in small-scale residential projects that dominate emerging-market construction, tempering growth despite favorable cost and performance metrics.

Moisture-Susceptibility Concerns in High-Humidity Climates

Relative humidity above 80% and prolonged wet seasons in Indonesia, the Philippines, and coastal Brazil heighten fears of board sagging and microbial growth. Though fiberglass-faced variants resist moisture better than paper-faced products, the gypsum core remains susceptible if improperly sealed. Builders sometimes over-specify cement board or autoclaved fiber cement for wet areas, eroding potential GFRG share. Product advances—such as hydrophobic additives and factory-applied primers—are narrowing the perception gap, yet installers still require robust detailing guidance to ensure long-term performance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User Industry: Non-Residential Dominance Drives Growth

Non-residential projects captured 60.42% of the glass fiber reinforced gypsum market share in 2025, and the segment is forecast to advance at 4.26% CAGR through 2031. Commercial towers, hospitals, airports, and schools increasingly specify GFRG for its fire-rating compliance and design freedom, strengthening the segment’s lead. Renovation programs across North American healthcare facilities emphasize low-emission interiors, favoring GREENGUARD Gold-certified boards. Institutional demand also benefits from government stimulus allocations focused on resilient infrastructure. The residential slice remains smaller but is gathering pace as affordable-housing agencies in India and Malaysia pilot load-bearing GFRG wall panels, highlighting cost advantages. DIY adoption in the United States is rising as big-box retailers stock lightweight panels that can be handled by two workers without lifting equipment. Industrial applications remain niche—predominantly chemical plants and data centers where fire and chemical stability are paramount—but serve as proof points for the material’s technical ceiling. Overall, non-residential leadership is likely to persist given the backlog of global infrastructure projects and stricter building-performance mandates.

Commercial interiors in particular drive repeat volume because partition walls and ceilings undergo more frequent reconfiguration than structural elements, opening recurring opportunities for premium products. Educational facilities specify impact-resistant faces to withstand high foot traffic, expanding the value mix. In contrast, the residential segment prioritizes cost, but rising middle-class incomes in China and Vietnam are unlocking demand for decorative ceiling roses and recessed lighting niches made from GFRG. Cross-selling opportunities emerge as contractors accustomed to classical plaster ornaments pivot toward factory-finished GFRG, shortening on-site schedules. The segment split underscores the versatility of the material across divergent performance thresholds and budget constraints.

By Application: Interior Focus with Exterior Potential

Interior uses contributed 54.67% of the glass fiber reinforced gypsum market size in 2025, leveraging the board’s acoustic dampening, fire resistance, and freedom to form compound curves. Wall linings in high-rise apartments use the panels to offset concrete thermal mass, improving room comfort without adding significant weight. Multi-family builders in Canada specify moisture-resistant grades for unit bathrooms, cutting mold remediation claims. Retail chains choose pre-finished GFRG bulkheads to slip consumer-facing areas into service faster, limiting downtime during store refurbishments. While interior leadership is entrenched, exterior grade panels featuring UV-stable coatings and fibrous mesh reinforcement are accelerating at 4.32% CAGR, propelled by Florida’s hurricane-zonal standards and Japan’s typhoon codes. National Gypsum’s PURPLE eXP line illustrates how formulations tailor water resistance and dimensional stability for façade sheathing.

Exterior uptake is further encouraged by architects seeking continuous insulation solutions that dovetail with energy-stringent envelopes. Combining GFRG sheathing with mineral wool delivers both fire and thermal performance, which is important for mid-rise wood-frame apartments in British Columbia. Builders in the Gulf Cooperation Council adopt GFRG cladding to achieve sculpted façades without heavy stone, trimming foundation loads. That said, long-term field data on UV durability in equatorial markets remains limited, so conservative specifiers may still favor fiber cement or EIFS in searing climates. Manufacturers respond by extending warranties and publishing accelerated-weathering test results to build confidence. As research institutions gather real-world exposure data, uptake in tropical belts will gradually climb, reinforcing the exterior segment’s double-digit share aspirations.

By Product Type: Fire-Rated Leadership with Specialty Innovation

Fire-rated boards held the largest 36.74% slice of the glass fiber reinforced gypsum market share in 2025 because code officials now reference prescriptive 1-hour and 2-hour performance benchmarks for most occupancies. Hospitals and data centers rarely accept substitutions, cementing baseline demand. Type C boards enriched with vermiculite and glass fiber maintain structural integrity even after gypsum dehydration, satisfying stringent criteria for shaft walls and protected steel columns. However, the ultra-lightweight and specialty cohort expands at a brisk 4.55% CAGR as builders chase ergonomic advantages and carbon-reduction credits. Weight reductions of 25% translate into fewer material handling injuries and quicker floor-to-floor cycles on high-rise jobsites. Specialty acoustical panels integrate viscoelastic damping layers, serving premium cinema and recording-studio projects that pay price premiums for decibel performance.

Standard Type S boards remain relevant in cost-sensitive emerging markets, but producers upsell towards mid-tier moisture-resistant SKUs by bundling extended warranties against mold! Architectural kits—complete with pre-formed coffers, column casings, and cornices—open a new revenue channel, especially in luxury hospitality refurbishments. Digital twin workflows allow contractors to extract mold files directly from BIM models, cutting pattern-making labor. As additive-manufacturing of molds becomes commonplace, custom work that once required artisan plaster labor now scales commercially. The product typology is therefore shifting from commodity sheets into solutions packages, raising average selling prices and cementing brand differentiation.

Geography Analysis

Asia-Pacific’s leadership rests on government infrastructure pipelines, rapid urban migration, and an evolving preference for lightweight, high-performance materials. China’s stimulus-backed rail, airport, and social-housing projects keep wallboard lines busy despite real-estate softness, while India’s smart-city initiatives integrate GFRG into multi-modal transit hubs. Southeast Asian nations, notably Thailand and the Philippines, intensify port and logistics-park construction, creating pockets of premium board demand to satisfy NFPA-aligned fire codes. Manufacturers deploy mobile training units to raise installer proficiency, thereby easing one of the region’s principal adoption constraints. Exchange-rate stability and competitive labor costs permit aggressive pricing strategies that undercut imported cement panels, preserving share gains.

North America follows with strong fundamentals rooted in renovation spending, data-center proliferation, and federal incentives for low-carbon materials. The U.S. General Services Administration’s low embodied-carbon procurement program unlocks federal project demand for advanced GFRG formulations, while the EPA’s USD 18 million clean-manufacturing grants catalyze factory upgrades to lower Scope 1 emissions. Border tariffs reshape supply chains, prompting distributors to secure alternate sources within the Midwest and Appalachia. Canadian provinces update building codes to allow taller wood-frame structures, indirectly increasing demand for fire-barrier layers such as Type X GFRG.

Europe centers its strategy on decarbonization. Developers routinely request Environmental Product Declarations, rewarding suppliers that can document lower embodied energy. Energy-retrofit subsidies in Germany and France push demand for interior board overlays that improve thermal resistance without sacrificing space, an ideal fit for ultra-lightweight GFRG. Emerging European economies—Poland, Romania—also climb as nearshoring expands warehousing and light-industrial stock, each requiring code-compliant fire partitions. In South America, Brazil’s Minha Casa Minha Vida subsidized-housing program begins to accept GFRG sandwich wall panels as a substitute for masonry, and Chilean coastal resorts use weather-resistant boards to withstand saline air. The Middle East leans on GFRG ornamentation to replicate traditional Islamic motifs quickly, trimming artisan labor while hitting tight project timelines ahead of international events. Collectively, these nuances illustrate that regional dynamics intertwine policy, macroeconomic shifts, and localized climatic demands.

Competitive Landscape

The industry exhibits moderately fragmented concentration. Saint-Gobain’s USD 400 million multi-state expansion will add 900 million ft² of annual capacity to its CertainTeed network, signalling confidence in sustained demand. Etex’s acquisition of BGC’s plasterboard assets scales its footprint in Australia and New Zealand, securing closer access to the buoyant Asia-Pacific trade. USG pursues raw-material self-sufficiency through the Avery Quarry, reflecting a defensive posture against synthetic gypsum shrinkage. National Gypsum differentiates with patented PURPLE moisture-resistant technology, while Armstrong focuses on designer-grade ceiling systems bundled with GFRG components.

Strategic playbooks now converge on three vectors. First, sustainability: firms publish carbon-reduction roadmaps, adopt biomass or solar for kiln heating, and develop lower-calcination-temperature chemistries. Second, product diversification: ultra-lightweight cores, impact-resistant faces, and acoustical laminates multiply SKUs, capturing niche margins and protecting against price compression on commodity boards. Third, geographic rebalancing: capacity moves closer to demand centers to mitigate freight costs and tariff risks. Digital customer portals enable order tracking and installation guidance, fostering loyalty among contractors.

Innovation pipelines increasingly rely on partnerships with chemical companies and universities exploring nanoparticle reinforcement, phase-change-material integration for thermal regulation, and 3D printing of molds. Competitive intensity is moderate; price wars do occur in commoditized Type S boards, yet differentiation on carbon footprint and performance specifications provides shelter for premium pricing. Start-ups remain rare due to capital-intensive production lines, but niche mold-fabrication firms capture value in architectural specialties. Scale producers hedge against cyclical downturns by servicing adjacent segments such as cementitious panels and insulation, smoothing revenue volatility.

Glass Fiber Reinforced Gypsum Industry Leaders

China National Building Material Group Corporation

Formglas Products Ltd.

Saint-Gobain

Etex Group

USG Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Saint-Gobain Canada plans to launch its CarbonLow gypsum wallboard line in 2025, featuring up to 60% less embodied carbon. This initiative is expected to drive sustainability advancements in the glass fiber reinforced gypsum market by reducing carbon emissions and promoting eco-friendly construction materials.

- June 2024: USG Corporation has initiated gypsum production at its new Avery Quarry in Michigan, targeting 300,000 tons by the end of 2024 and 550,000 tons in 2025. This increased supply is expected to support the growing demand in the glass fiber reinforced gypsum market, ensuring a steady availability of raw materials.

Global Glass Fiber Reinforced Gypsum Market Report Scope

The Glass Fiber Reinforced Gypsum market report include:

| Residential | |

| Non-Residential | Commercial |

| Institutional | |

| Industrial |

| Interior |

| Exterior |

| Standard (Type S) |

| Fire-Rated (Type X) |

| High-Strength (Type C) |

| Ultra-Lightweight/Specialty |

| Custom Architectural Elements and Kits |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By End-user Industry | Residential | |

| Non-Residential | Commercial | |

| Institutional | ||

| Industrial | ||

| By Application | Interior | |

| Exterior | ||

| By Product Type | Standard (Type S) | |

| Fire-Rated (Type X) | ||

| High-Strength (Type C) | ||

| Ultra-Lightweight/Specialty | ||

| Custom Architectural Elements and Kits | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the glass fiber reinforced gypsum market?

The glass fiber reinforced gypsum market size is valued at USD 4.70 billion in 2026 and is projected to reach USD 5.64 billion by 2031, growing at a 3.70% CAGR.

Which segment holds the largest share in the glass fiber reinforced gypsum market?

Non-residential construction leads with 60.42% share in 2025 due to strict fire-safety requirements and design flexibility needs.

Why is Asia-Pacific the dominant region for glass fiber reinforced gypsum demand?

Rapid urbanization, infrastructure spending, and affordable-housing programs position Asia-Pacific at 43.86% of global revenue and the fastest 3.86% CAGR through 2031.

How do fire-safety regulations influence market growth?

Stringent building codes worldwide mandate higher fire-performance levels, driving consistent demand for fire-rated GFRG boards.

What are the main barriers to adoption in emerging markets?

Limited installer awareness and concerns over moisture susceptibility in tropical climates slow uptake, though manufacturer training and product innovation are addressing these issues.

Which product type is growing the fastest?

Ultra-lightweight and specialty variants are forecast to expand at 4.55% CAGR as builders prioritize ease of handling and advanced performance attributes.

Page last updated on: