Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 7.85 Billion |

| Market Size (2026) | USD 8.19 Billion |

| Market Size (2031) | USD 10.12 Billion |

| Growth Rate (2026 - 2031) | 4.33% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

European Roof Tiles Market Analysis by Mordor Intelligence

European Roof Tiles market size in 2026 is estimated at USD 8.19 billion, growing from 2025 value of USD 7.85 billion with 2031 projections showing USD 10.12 billion, growing at 4.33% CAGR over 2026-2031. Robust regulatory pressure to decarbonize buildings, an aging housing stock that requires systematic renovation, and rising weather-related risks underpin the steady expansion of the European roof tiles market. Demand is buoyed by the cost efficiency of concrete tiles, the longevity of clay tiles, and the accelerating shift toward building-integrated photovoltaic (BIPV) formats that align with mandatory rooftop solar rules. Competitive activity centers on product convergence, where established producers acquire solar-tile specialists to align with EU green-building mandates. At the same time, raw material cost volatility and skilled labor bottlenecks remain immediate headwinds that manufacturers must navigate to protect margins in the European roof tiles market.

Key Report Takeaways

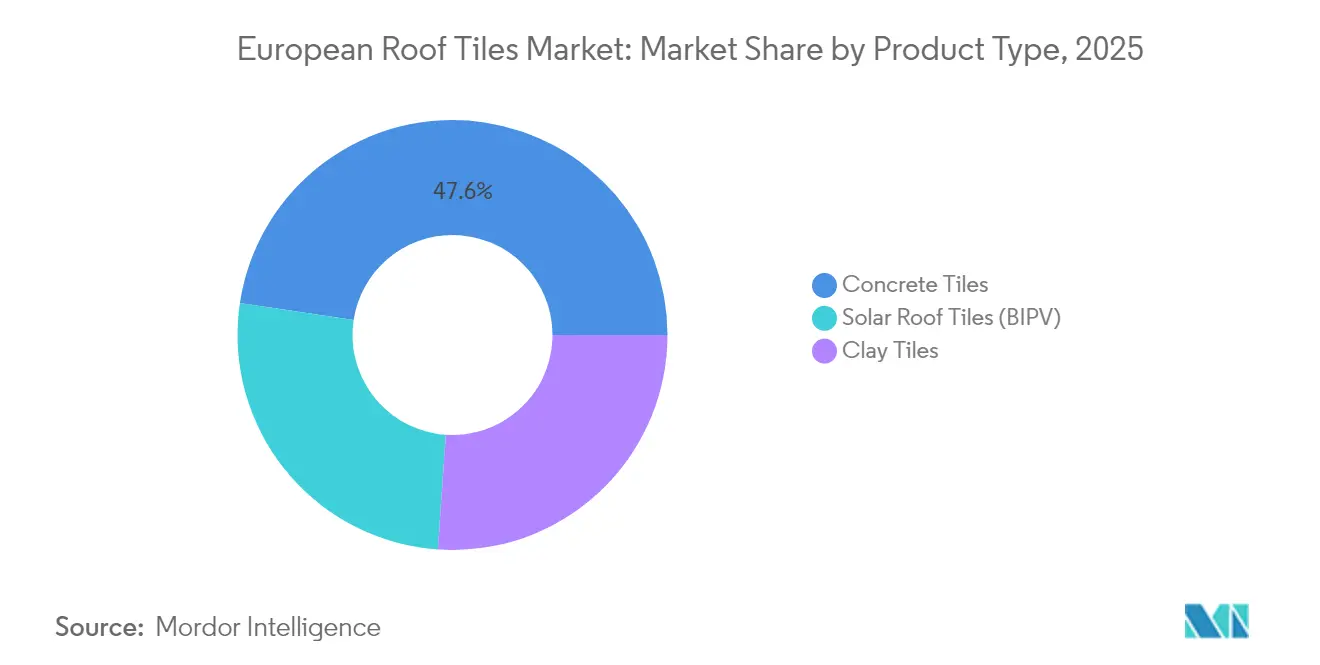

- By product type, concrete tiles led with 47.62% of the European roof tiles market share in 2025, while solar roof tiles recorded the fastest 6.85% CAGR through 2031.

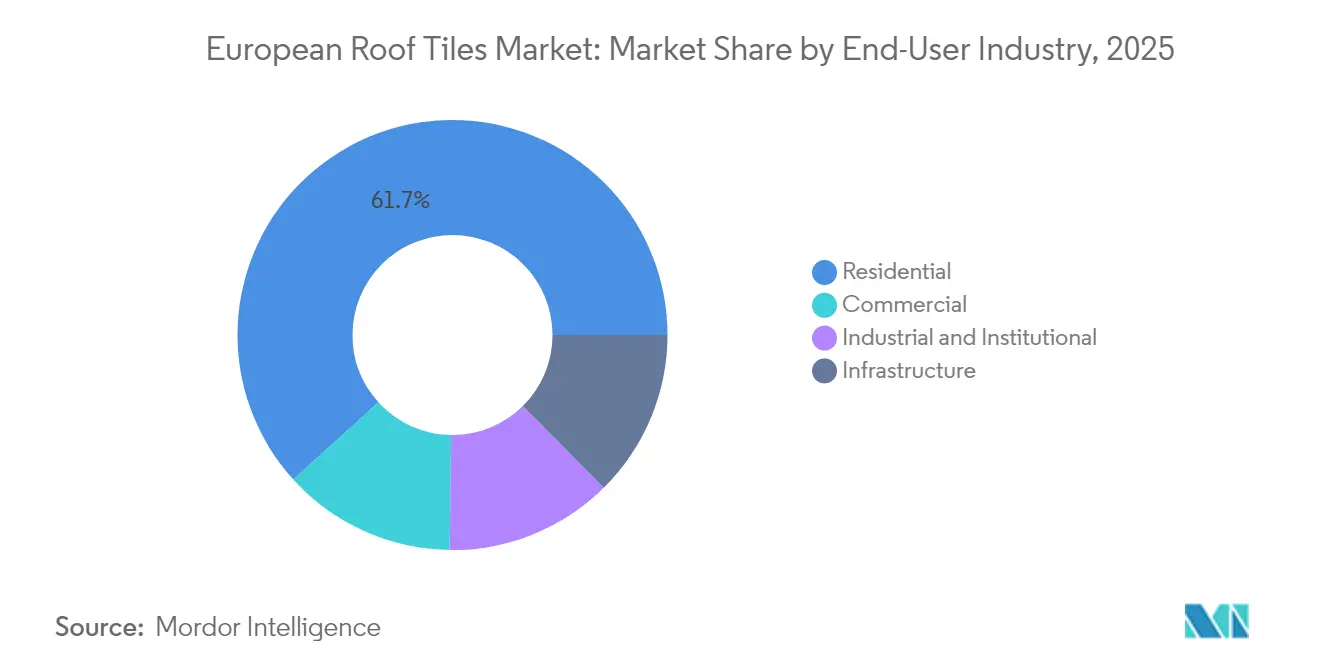

- By end-user industry, residential applications accounted for 61.73% of the European roof tiles market size in 2025; the commercial segment is advancing at a 5.45% CAGR to 2031.

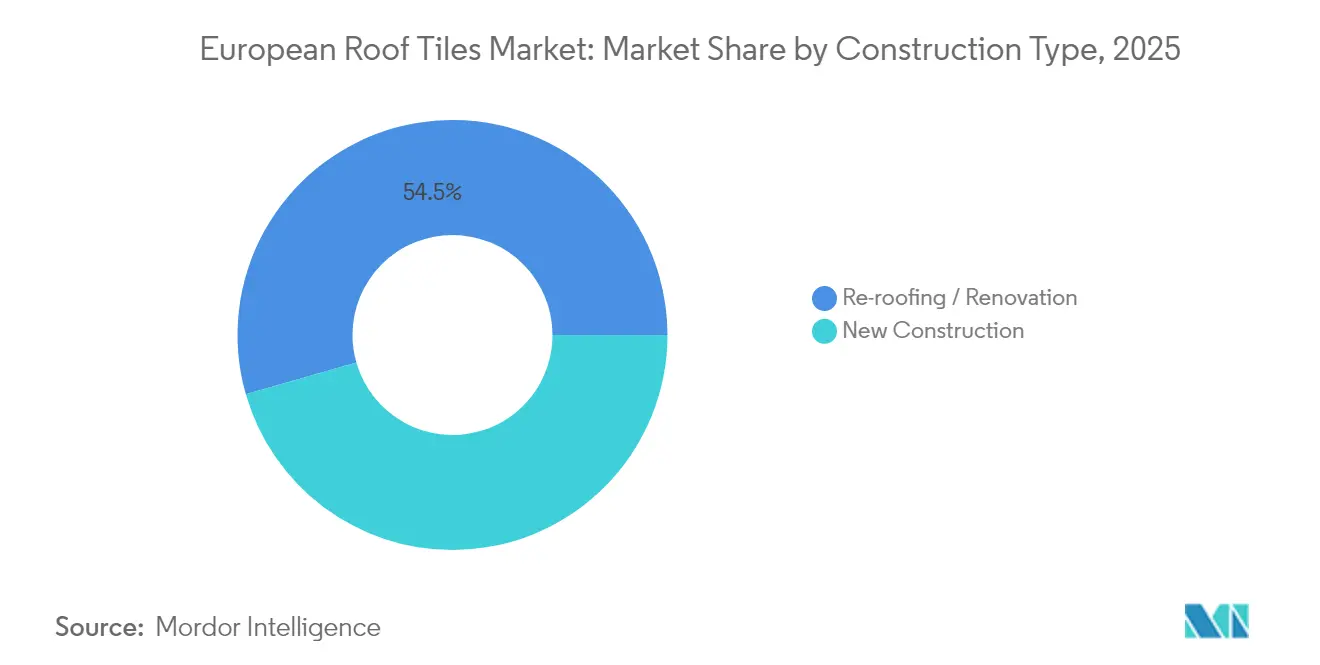

- By construction type, re-roofing and renovation captured 54.45% share of the European roof tiles market size in 2025, whereas new construction is projected to grow at a 5.02% CAGR through 2031.

- By geography, Germany held the largest 18.55% revenue share in 2025, and Turkey is set to expand at a 5.26% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

European Roof Tiles Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU green-building mandates accelerate adoption | +1.20% | EU-wide; strongest in Germany, France, Netherlands | Medium term (2-4 years) |

| Renovation wave across aging housing stock | +1.80% | EU-wide; concentrated in Western Europe | Long term (≥4 years) |

| Durability and life-cycle benefits of clay/concrete | +0.90% | Northern and Central Europe | Long term (≥4 years) |

| Climate-driven re-roofing after extreme weather | +0.70% | Southern Europe; coastal regions | Short term (≤2 years) |

| Mandatory rooftop-PV rules lift solar tiles | +1.10% | Germany, Netherlands, France; expanding EU-wide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

EU Green-Building Mandates Accelerate Tile Adoption

The recast Energy Performance of Buildings Directive compels buildings consuming more than 290 kWh/m² annually to undergo energy renovations by 2030. Consequently, procurement specifications now emphasize roof systems that offer high insulation values and integrate solar generation capacity. Concrete and clay tiles that meet emerging U-value thresholds are becoming default choices in public tenders as local governments align with the Renovation Wave strategy. Early-mover manufacturers roll out tiles pre-certified for BIPV compatibility, positioning themselves ahead of phased compliance deadlines. Late adopters risk exclusion from project shortlists once national transpositions of the directive are fully in force.

Renovation Wave Across Aging European Housing Stock

Three out of every four European dwellings were built before 1990 and fall short of present-day efficiency norms. Brussels targets 35 million renovations by 2030, and roofs top retrofit priority lists because they deliver immediate heat-loss reductions. Concrete tiles remain the default choice for budget-sensitive owners because familiar installation practices limit labor hours and project disruption. Manufacturers leverage predictable replacement cycles to synchronize capacity additions with regional renovation funding programs. Distributors expand just-in-time inventory services, ensuring installers can meet tight subsidy-linked project timelines.

Durability and Life-Cycle Sustainability Advantages of Clay/Concrete Tiles

A 50- to 100-year service life positions clay and concrete products as lower total-cost solutions when labor inflation is factored into replacement scenarios. Independent lifecycle assessments show that the embodied carbon payback of clay tiles occurs within five years, thanks to their superior thermal mass, while concrete tiles require 40% fewer replacements than asphalt shingles over a typical building's life. As climate risk intensifies, insurers are revising premiums in favor of tested products with proven wind-uplift and hail-impact ratings. Producers therefore market durability metrics as both a financial and environmental value proposition.

Integrated Solar Roof Tiles Boosted by Rooftop-PV Rules

Germany’s federal states require solar on new homes as of 2025, while France mandates on-site generation for select commercial roofs. Aesthetic constraints in heritage districts favor BIPV tiles that mimic traditional profiles yet reach 25% cell efficiency. Market entrants partner with conventional roof-tile distributors to capitalize on existing installer relationships, thereby shortening sales cycles. The shift from niche to mainstream has halved system payback periods in high-insolation regions, which drives scale economies and further price reductions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium pricing vs. asphalt and sheet metal | -0.80% | EU-wide; strongest in Eastern Europe | Short term (≤2 years) |

| Skilled-labor shortages in tile installation | -0.60% | EU-wide; acute in Germany and Netherlands | Medium term (2-4 years) |

| Volatile energy and raw-material costs | -0.90% | Manufacturing-intensive regions across the EU | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Premium Pricing Versus Asphalt and Sheet-Metal Roofs

Clay and concrete solutions remain 40-60% pricier than asphalt alternatives, limiting penetration in price-sensitive Eastern European markets. Inflationary spikes in gas and cement during 2024-2025 widened this gap, forcing manufacturers to choose between absorbing costs or raising prices at the risk of volume losses. Nevertheless, where labor costs exceed material costs, owners increasingly value tiles’ extended lifespans, shifting the affordability discussion from upfront expense to lifecycle economics.

Skilled-Labor Shortages in Specialist Tile Installation

Nearly two-thirds of roofing contractors surveyed in 2025 reported project delays due to a lack of trained installers. Tile placement, flashing, and BIPV integration demand precise skill sets that apprenticeship programs are not replenishing fast enough. Wage escalation erodes contractor margins and prompts some to steer clients toward lower-skill alternatives such as bituminous sheets. Manufacturers counter by introducing interlocking designs and augmented-reality training modules, yet a demographic cliff of retiring artisans keeps the constraint acute.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Solar Integration Drives Premium Segment Growth

Solar tiles expanded at a 6.85% CAGR, outpacing all other formats as rooftop-PV obligations proliferated. Concrete maintained a 47.62% share of the European roof tile market in 2025, reflecting its cost advantages and logistical reach into renovation-heavy zones. Clay tiles have captured the heritage restoration market due to their authentic aesthetics and 100-year durability claims. Manufacturers merge traditional lines with BIPV variants to capture adjacency sales, while curved solar formats erase earlier aesthetic objections.

The European roof tiles market increasingly maps to a three-tier value hierarchy: solar tiles at premium price points but limited volume, concrete as a mainstream workhorse, and clay for design-driven or conservation contexts. Plant modernization focuses on digital kiln control to cut gas usage, aligning with corporate net-zero roadmaps. Cross-border acquisitions accelerate, creating platforms that balance commodity concrete capacity with patent-protected solar portfolios, further consolidating the European roof tiles industry.

By End-User Industry: Commercial Acceleration Outpaces Residential Stability

Residential projects accounted for 61.73% of the European roof tiles market share in 2025 as owner-occupied dwellings continued to prioritize curb appeal and durability. Commercial roofs, however, are advancing at a 5.45% CAGR because corporate ESG targets are elevating interest in BIPV solutions that offset energy bills. Industrial and public buildings adopt performance-based procurement, rewarding suppliers who can quantify the total cost of ownership rather than just the headline bid price.

Project financing structures evolve, with roof-lease models bundling installation, maintenance, and energy off-take into a single contract that de-risks capital budgeting for facility managers. Manufacturers respond by building in-house energy services teams or partnering with power purchase agreement aggregators, a shift that blurs the historical lines between construction materials and distributed generation sectors.

By Construction Type: Renovation Dominance Reflects Market Maturity

Re-roofing captured 54.45% of 2025 demand, underscoring the mature profile of European buildings. Predictable replacement cycles ensure stable order intake, even when new housing starts fluctuate, allowing producers to optimize batch runs and raw material purchasing. New construction, forecasted at a 5.02% CAGR, benefits from policy-linked subsidies that require energy-positive envelopes from the outset.

Renovation clients often favor concrete due to familiarity and rapid availability, whereas new-build architects experiment with integrated solar formats that satisfy carbon budgets without compromising design intent. Software-based configurators now allow contractors to assess structural load, wind zone, and electrical output in a single interface, shortening the sales process and increasing specification accuracy.

Geography Analysis

Germany held 18.55% of the European roof tiles market in 2025, supported by stringent energy codes and a dense installer ecosystem that seamlessly handles both traditional and solar formats. Federal state mandates introduced in 2025 require on-site renewables for most residential new builds, effectively guaranteeing baseline demand for BIPV tiles. Automation in German factories raises throughput while maintaining dimensional accuracy, enabling exports that meet diverse European standards.

Turkey is forecast to grow at a 5.26% CAGR through 2031, propelled by rapid urbanization and post-earthquake reconstruction that prioritizes seismic safety and energy efficiency. Local clay deposits reduce input costs, allowing Turkish producers to price competitively within the customs union. Proximity to EU markets offers export optionality, and the government’s housing push sustains domestic volume.

Italy, Spain, and France form a mature yet policy-sensitive triad. Italy’s renovation subsidies spurred a spike in 2025 reroofing permits, but year-to-year volatility persists as fiscal incentives shift. Spain’s tourism-linked construction revival centers on sustainable hotel refurbishments, favoring tiles with Mediterranean aesthetic continuity. France’s 2024 decree mandating solar on large commercial roofs fast-tracks BIPV adoption while strict heritage rules still safeguard clay specifications in protected zones.

Northern Europe exhibits slower but steady adoption, driven by high labor costs that tilt lifecycle economics toward long-lasting tiles. Eastern Europe remains price-constrained, though EU cohesion funds earmarked for energy efficiency could unlock latent demand if subsidy design addresses upfront affordability gaps. Collectively, geographic variations necessitate flexible go-to-market models, from direct sales in Germany to distributor-led approaches in fragmented Mediterranean regions.

Competitive Landscape

The European roof tiles market exhibits consolidated concentration, with Wienerberger, Terreal, and BMI holding a significant share, while dozens of regional specialists cater to localized tastes. Consolidation momentum intensified in 2024-2025 as incumbents acquired solar-tile startups to pre-empt competition from photovoltaic module manufacturers. Private-equity-backed roll-ups target fragmented installer networks, bundling services under unified brands to capture downstream margin.

Technology adoption is a key differentiator. Producers utilize AI-driven kiln optimization to reduce gas usage by up to 8%, thereby meeting their Scope 1 emission goals. Digital specification tools integrate BIM libraries, allowing architects to drag and drop tile styles with embedded performance data. Customer portals now offer order-tracking and remote warranty claims, a service dimension that smaller rivals struggle to replicate.

Strategic thematics revolve around sustainability credentials. EPD-certified products and cradle-to-cradle claims resonate with institutional buyers, while voluntary third-party hail-resistance labels unlock insurance-backed discounts. Companies also pilot recycled-content concrete tiles to mitigate emissions related to cement production. As regulatory bars rise, the cost of compliance escalates, effectively widening the moat for incumbents with ISO-accredited labs and certified quality systems.

European Roof Tiles Industry Leaders

BMI Group

IKO Industries Ltd

Marley

EGGER

Wienerberger AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Sika has finalized the acquisition of Cromar Building Products, one of the leading UK supplier of roofing systems that primarily serves customers through distribution channels. This acquisition presents significant cross-selling opportunities and strengthens Sika's efforts to expand further within the UK's roofing market.

- March 2024: Wienerberger has successfully completed its largest acquisition, encompassing Terreal in France, Italy, Spain, and the USA, as well as Creaton in Germany. This strategic move is expected to significantly influence the European roofing tile market by enhancing Wienerberger's market presence, expanding its product portfolio, and strengthening its competitive position in the region.

European Roof Tiles Market Report Scope

Roof tiles are designed mainly to keep out rain and are traditionally made from locally available materials such as terracotta or slate. Modern materials such as concrete, metal, and plastic are also used, and some clay tiles have a waterproof glaze. Roof tiles provide a barrier between the inside of a structure and the harsh outside elements.

The European roof tiles market is segmented by type, end-user industry, and geography. By type, the market is segmented into clay, concrete, and other types (stone-coated metal, asphalt shingle, etc.). By end-user industry, the market is segmented into residential, commercial, infrastructure, and industrial and institutional. The report also covers the size and forecast for the roofing tiles market in 7 countries across Europe. For each segment, the market sizes and forecasts are provided in terms of revenue (USD).

By Product Type

| Clay Tiles |

| Concrete Tiles |

| Solar Roof Tiles (BIPV) |

By End-user Industry

| Residential |

| Commercial |

| Infrastructure |

| Industrial and Institutional |

By Construction Type

| New Construction |

| Re-roofing / Renovation |

By Geography

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Russia |

| Nordics |

| Turkey |

| Rest of Europe |

| By Product Type | Clay Tiles |

| Concrete Tiles | |

| Solar Roof Tiles (BIPV) | |

| By End-user Industry | Residential |

| Commercial | |

| Infrastructure | |

| Industrial and Institutional | |

| By Construction Type | New Construction |

| Re-roofing / Renovation | |

| By Geography | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Nordics | |

| Turkey | |

| Rest of Europe |

Key Questions Answered in the Report

What is the current value of the European roof tiles market?

The market is valued at USD 8.19 billion in 2026 and is forecast to reach USD 10.12 billion by 2031.

Which product segment leads in market share?

Concrete tiles hold the highest share at 47.62% in 2025.

Which geography shows the fastest growth?

Turkey is projected to grow at a 5.26% CAGR through 2031.

Why are BIPV tiles gaining traction?

Mandatory rooftop-solar rules, improved aesthetics, and 25%+ cell efficiency are driving adoption.

What is the main restraint facing tile installers?

A skilled-labor shortage limits installation capacity across the region.

Page last updated on: