Flooring Resins Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.64 Billion |

| Market Size (2031) | USD 4.49 Billion |

| Growth Rate (2026 - 2031) | 4.29% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

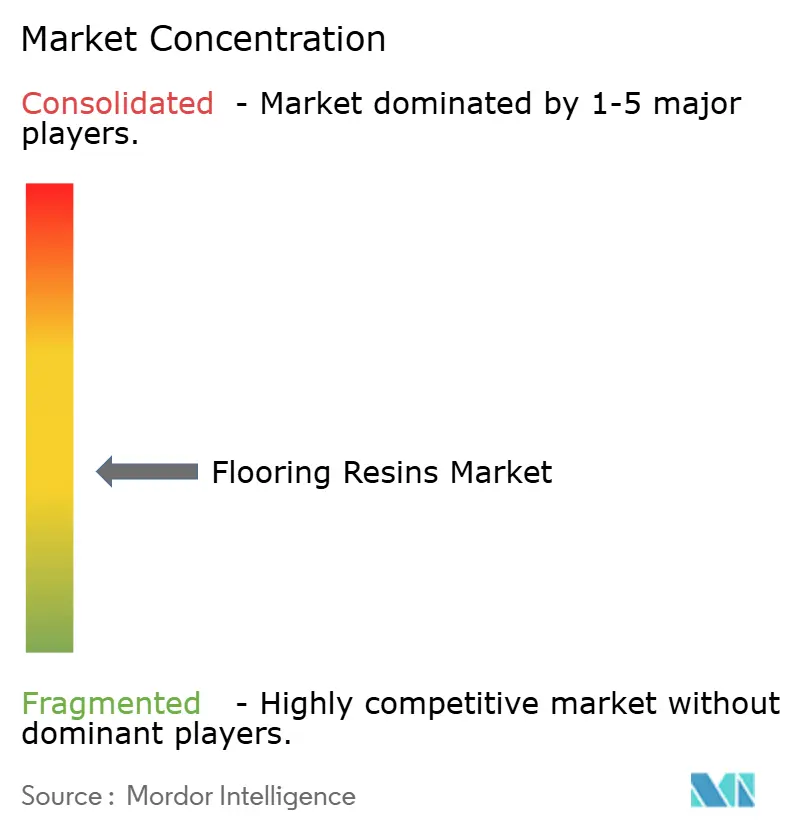

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Flooring Resins Market Analysis by Mordor Intelligence

The Flooring Resins Market size was valued at USD 3.49 billion in 2025 and estimated to grow from USD 3.64 billion in 2026 to reach USD 4.49 billion by 2031, at a CAGR of 4.29% during the forecast period (2026-2031). Rising industrial construction across emerging economies, together with mounting hygiene and chemical-resistance requirements, underpins this expansion. Accelerated green-field plant construction in Asia–Pacific and the Middle East keeps demand buoyant, while facility retrofits in North America and Europe favor high-performance, low-VOC systems. Corporate sustainability targets are pushing manufacturers toward bio-based or water-borne chemistries that meet tightening regulations without sacrificing durability. At the same time, fast-curing technologies that shorten shutdown windows are becoming decisive differentiators in procurement decisions. Supply-chain localization strategies are also shaping competitive positioning as anti-dumping measures and feedstock swings expose import-reliant companies to cost volatility.

Key Report Takeaways

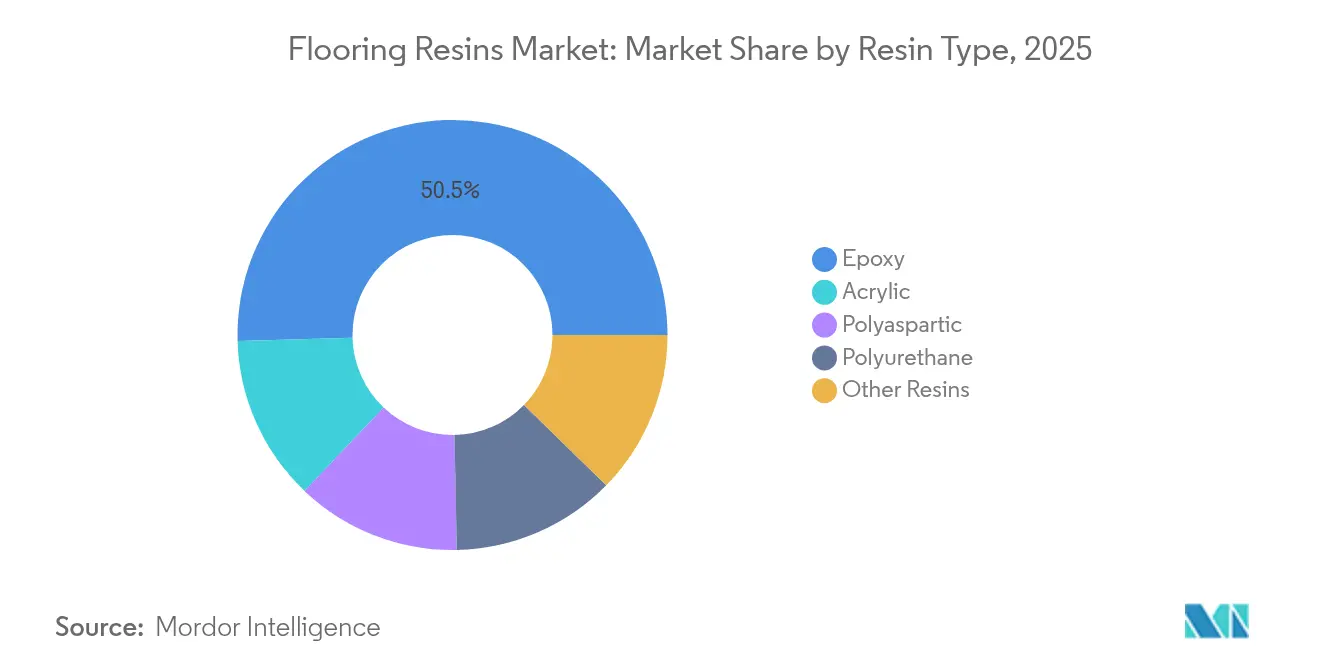

- By resin type, epoxy led with 50.45% revenue share in 2025; acrylic is forecast to expand at a 6.38% CAGR to 2031.

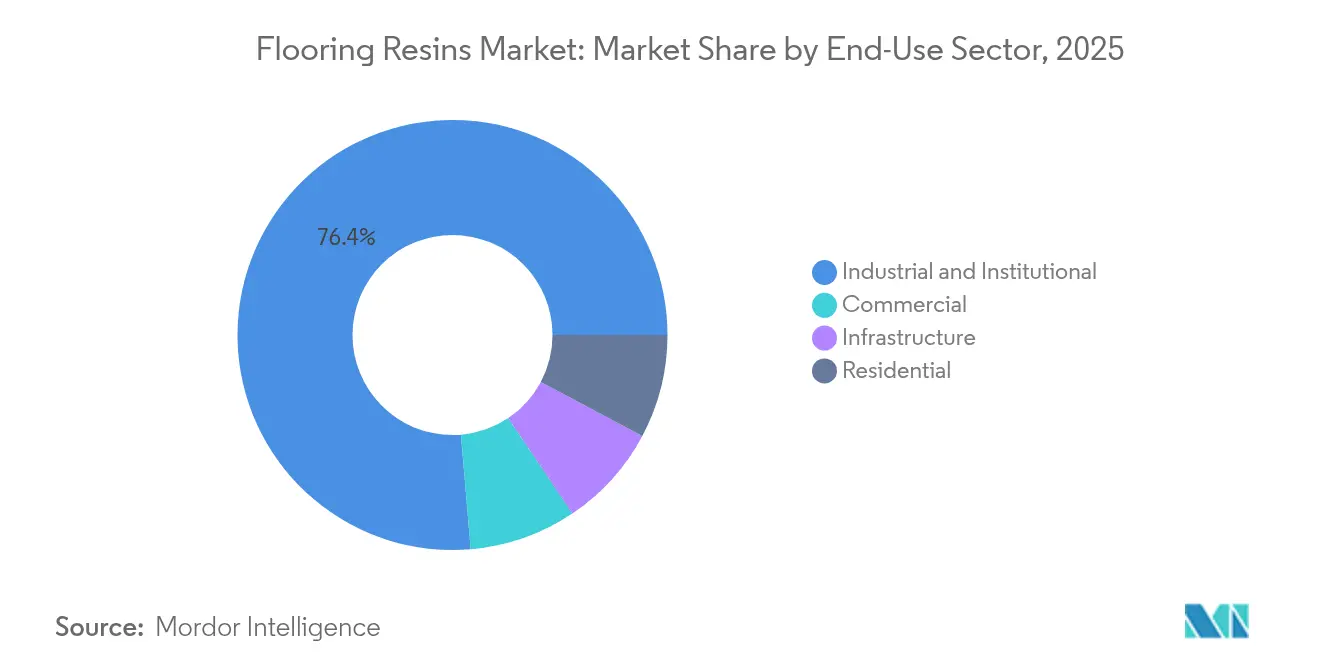

- By end-use sector, industrial and institutional held 76.35% of the flooring resins market share in 2025, while commercial applications record the highest projected CAGR at 4.88% through 2031.

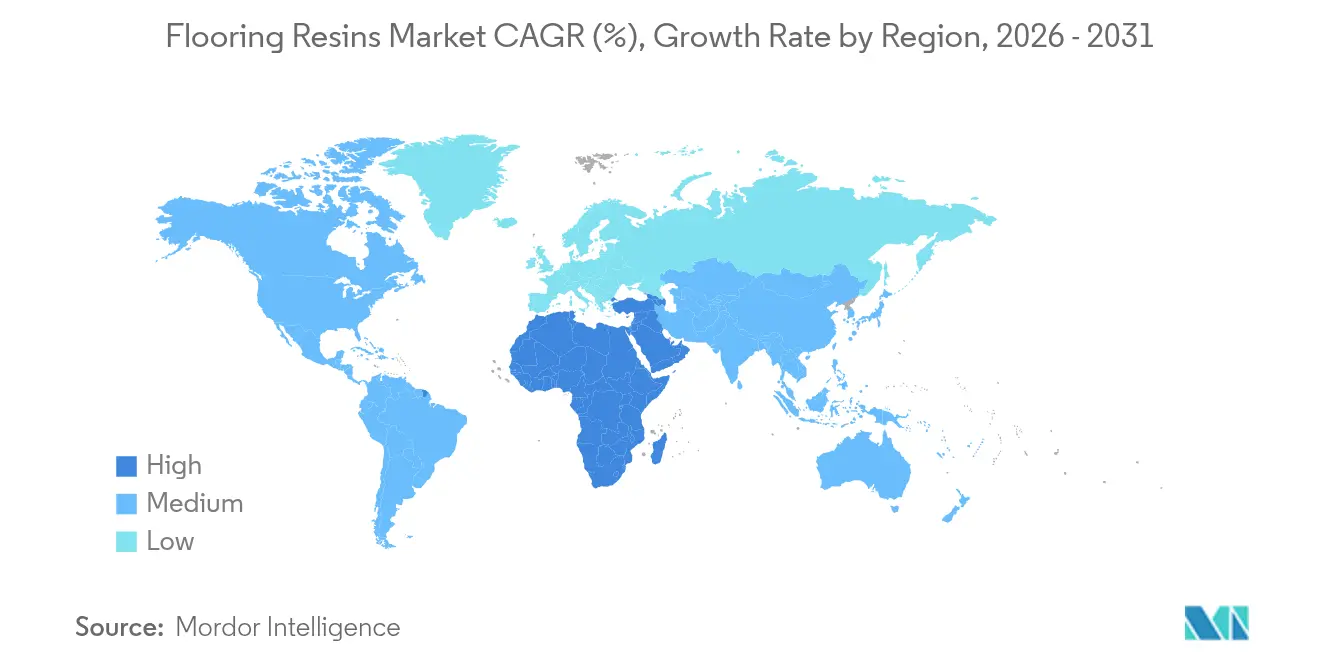

- By geography, Asia-Pacific commanded 40.21% share of the flooring resins market size in 2025 and the Middle-East and Africa is advancing at 5.42% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Flooring Resins Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating industrial and commercial construction in emerging economies | +1.8% | Asia–Pacific, Middle East and Africa | Medium term (2-4 years) |

| Surging demand for chemical-resistant industrial floors | +1.2% | Global, APAC hubs | Long term (≥4 years) |

| Rapid shift to low-VOC epoxy and polyurethane technologies | +0.9% | North America and EU expanding to APAC | Short term (≤2 years) |

| Tightening hygiene standards in clean-production zones | +0.6% | Global pharma and food sectors | Medium term (2-4 years) |

| Adoption of fast-curing polyaspartic/PUMMA retrofit systems | +0.4% | North America and Europe expanding to APAC | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Accelerating Industrial and Commercial Construction in Emerging Economies

Manufacturing facility build-outs across China, India, and Southeast Asia continue to propel the flooring resins market as investors demand robust surfaces capable of supporting heavy machinery and resisting chemical splash-and-spill events. Saudi Arabia’s NEOM megaproject and similar diversification programs in the Gulf further amplify regional demand for flooring systems that can tolerate thermal extremes and corrosive agents while aligning with international safety codes. India’s construction-chemicals segment shows rising uptake of resin-modified concrete toppings that cut lifecycle costs. The resulting project pipeline cements emerging markets as principal growth engines over the medium term.

Surging Demand for Chemical-Resistant Industrial Floors

Pharmaceutical and specialty-chemical producers specify seamless, antimicrobial floors that withstand acids, solvents, and aggressive wash-downs necessary for ISO-3 or GMP Class A environments. USDA-approved resin systems now dominate food-processing sites where hot-steam sanitation creates repeated thermal shock. In Asia–Pacific, expanding dairy and ready-meal capacity accelerates the shift from conventional concrete to epoxy toppings, securing a pivotal market driver through 2030.

Rapid Shift to Low-VOC Epoxy and Polyurethane Technologies

REACH in Europe and analogous rules in North America are phasing out solvent-rich chemistries, pushing the flooring resins industry to re-engineer formulations that balance performance with environmental compliance. Polyaspartic, water-borne epoxy, and bio-based hardeners already command premium pricing yet unlock lower facility downtime and worker-safety benefits, gaining traction among retrofit projects in hospitals and food plants.

Tightening Hygiene Standards in Clean-Production Zones

Pharmaceutical, biotech, and advanced electronic manufacturers increasingly view flooring systems as integral components of contamination control. Seamless coving, antimicrobial additives, and static-dissipative finishes are now baseline specifications for new builds, supporting steady demand for high-value resin solutions.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Feedstock price volatility | -0.8% | Global, import-dependent regions | Short term (≤2 years) |

| Stricter BPA/VOC regulations on legacy epoxy chemistries | -0.5% | North America and EU | Medium term (2-4 years) |

| Anti-dumping trade actions disrupting Asian epoxy supply | -0.3% | Global supply chains | Short term (≤2 years) |

| Shortage of certified resin-floor installers | -0.2% | North America and Europe, emerging APAC zones | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Feedstock Price Volatility

Ethylene and propylene swings directly affect epoxy and polyurethane costs, compelling manufacturers to issue frequent price adjustments that strain project budgets in price-sensitive installations[1]Asian Chemical Connections, “Petrochemical Capacity Additions and Price Volatility,” asianchemicalconnections.com. Integrated producers with captive feedstock streams gain margin insulation, while smaller converters face working-capital pressures that can delay expansions.

Stricter BPA/VOC Regulations on Legacy Epoxy Chemistries

Ongoing regulatory review of bisphenol-A and VOC thresholds forces expensive reformulations. Although non-BPA alternatives appeal to environmentally focused clients, they often require process requalification, creating market hesitation and incremental research and development expenditure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Epoxy Dominance Faces Acrylic Innovation Challenge

Epoxy resins retained 50.45% share of the flooring resins market in 2025 owing to unmatched chemical resistance and mechanical strength under forklift traffic and wash-downs. Acrylic systems, however, are projected to post a 6.38% CAGR and are gaining favor in sun-exposed settings where UV degradation shortens epoxy lifespan. Polyaspartic hybrids are carving a foothold by combining flexibility with rapid return-to-service, particularly for cold-storage retrofits.

Growing architectural preference for decorative metallic finishes in showrooms and airports further diversifies resin demand. Suppliers that tailor cure kinetics to specific climate conditions are likely to outperform peers. The flooring resins market size for acrylic and polyaspartic variants is set to broaden as building owners weigh lifecycle economics over initial cost, especially in regions with stringent VOC caps.

By End-Use Sector: Industrial Facilities Drive Demand While Commercial Adoption Accelerates

Industrial and institutional customers accounted for 76.35% of revenue in 2025, underscoring the flooring resins market’s dependence on manufacturing hygiene norms. Cleanrooms mandate seamless coves, antimicrobial fillers, and static-control layers that favor premium epoxy and polyurethane systems. Conversely, decorative epoxy terrazzo and metallic polyaspartic toppings are elevating aesthetic standards in offices, hotels, and retail.

Commercial applications’ 4.88% projected CAGR through 2031 reflects facility-management interest in long-wear life and easy maintenance, attributes that lower lifecycle spend despite higher up-front material cost. Infrastructure segments such as airports and hospitals maintain steady demand for skid-resistant, low-odor installations that meet public-occupancy regulations. The flooring resins market share in commercial spaces is therefore expected to continue climbing as architects embed durability metrics into design briefs.

Geography Analysis

Asia-Pacific held 40.21% of global revenue in 2025 as continuous factory build-outs in electronics, automotive, and pharmaceuticals specified high-performance epoxy toppings with ISO cleanroom compliance. India’s construction-chemicals sector accelerates resin uptake as foreign investors seek local production bases. Southeast Asian manufacturing relocations drive orders for UV-stable acrylics and fast-cure polyaspartics, reinforcing regional leadership in the flooring resins market.

The Middle-East and Africa region is forecast to grow at 5.42% CAGR through 2031, buoyed by Saudi Arabia’s Vision 2030 megaprojects and the UAE’s logistics-sector build-outs. Saint-Gobain’s USD 1.025 billion purchase of Dubai-based FOSROC exemplifies scaled entrants positioning to capture this demand surge. Africa’s mining and petrochemical expansions also require chemically robust floors, albeit from a smaller base.

North America and Europe remain technologically influential markets characterized by stringent VOC norms and preference for bio-based chemistries. Facility retrofits fond of water-borne epoxies and polyurethane dispersion topcoats maintain a predictable replacement cycle. Low-odor, overnight-cure solutions are gaining share in hospitals and data centers, underscoring innovation’s role over sheer volume growth in mature regions.

Competitive Landscape

The flooring resins market is moderatly fragmented yet intensifying consolidation. Saint-Gobain deepened regional footholds and acquired complementary chemistries through its FOSROC deal[2]GCP Applied Technologies, “Saint-Gobain Completes the Acquisition of FOSROC,” gcpat.com. Technology leadership now rests on low-VOC innovations, bio-content formulations, and digitally enabled color-matching that shorten decision cycles for architects. Niche entrants focusing on circular-economy materials, such as mycelium-based binders, are carving reputational space among sustainability-led clients. Competitive advantage increasingly hinges on combining technical consultancy with global logistics capabilities that can buffer raw-material shocks.

Flooring Resins Industry Leaders

The Sherwin-Williams Company

Sika AG

Saint-Gobain

RPM International Inc.

Nippon Paint Holdings Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Saint-Gobain has finalized its acquisition of Fosroc, a prominent global player in construction chemicals, significantly enhancing its presence across India, the Middle East, and the Asia-Pacific region. This strategic move, announced in June 2024 and completed in February 2025, marks a pivotal expansion of Saint-Gobain’s construction chemicals portfolio, including Nitoflor FC150, a solvent free, epoxy resin floor coating system.

- October 2024: Atul Ltd. completed a major capacity expansion of its liquid epoxy resin production at one of its manufacturing facilities in India. The expansion increases production capacity from 30,000 tonnes per annum (tpa) to 50,000 tpa, backed by an approved investment of INR 200 crore.

Global Flooring Resins Market Report Scope

Commercial, Industrial and Institutional, Infrastructure, Residential are covered as segments by End Use Sector. Acrylic, Epoxy, Polyaspartic, Polyurethane are covered as segments by Sub Product. Asia-Pacific, Europe, Middle East and Africa, North America, South America are covered as segments by Region.| Epoxy |

| Polyurethane |

| Polyaspartic |

| Acrylic |

| Other Resins |

| Commercial |

| Industrial and Institutional |

| Infrastructure |

| Residential |

| Asia-Pacific | Australia |

| China | |

| India | |

| Indonesia | |

| Japan | |

| Malaysia | |

| South Korea | |

| Thailand | |

| Vietnam | |

| Rest of Asia-Pacific | |

| North America | Canada |

| Mexico | |

| United States | |

| Europe | France |

| Germany | |

| Italy | |

| Russia | |

| Spain | |

| United Kingdom | |

| Rest of Europe | |

| South America | Argentina |

| Brazil | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle-East and Africa |

| By Resin Type | Epoxy | |

| Polyurethane | ||

| Polyaspartic | ||

| Acrylic | ||

| Other Resins | ||

| By End-Use Sector | Commercial | |

| Industrial and Institutional | ||

| Infrastructure | ||

| Residential | ||

| By Geography | Asia-Pacific | Australia |

| China | ||

| India | ||

| Indonesia | ||

| Japan | ||

| Malaysia | ||

| South Korea | ||

| Thailand | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| North America | Canada | |

| Mexico | ||

| United States | ||

| Europe | France | |

| Germany | ||

| Italy | ||

| Russia | ||

| Spain | ||

| United Kingdom | ||

| Rest of Europe | ||

| South America | Argentina | |

| Brazil | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle-East and Africa | ||

Market Definition

- END-USE SECTOR - Flooring resins consumed in the construction sectors such as commercial, residential, industrial, institutional, and infrastructure are considered under the scope of the study.

- PRODUCT/APPLICATION - Under the scope of the study, the consumption of flooring resin products based on epoxy, polyaspartic, polyurethane, acrylic, and other resins are considered.

| Keyword | Definition |

|---|---|

| Accelerator | Accelerators are admixtures used to fasten the setting time of concrete by increasing the initial rate and speeding up the chemical reaction between cement and the mixing water. These are used to harden and increase the strength of concrete quickly. |

| Acrylic | This synthetic resin is a derivative of acrylic acid. It forms a smooth surface and is mainly used for various indoor applications. The material can also be used for outdoor applications with a special formulation. |

| Adhesives | Adhesives are bonding agents used to join materials by gluing. Adhesives can be used in construction for many applications, such as carpet laying, ceramic tiles, countertop lamination, etc. |

| Air Entraining Admixture | Air-entraining admixtures are used to improve the performance and durability of concrete. Once added, they create uniformly distributed small air bubbles to impart enhanced properties to the fresh and hardened concrete. |

| Alkyd | Alkyds are used in solvent-based paints such as construction and automotive paints, traffic paints, flooring resins, protective coatings for concrete, etc. Alkyd resins are formed by the reaction of an oil (fatty acid), a polyunsaturated alcohol (Polyol), and a polyunsaturated acid or anhydride. |

| Anchors and Grouts | Anchors and grouts are construction chemicals that stabilize and improve the strength and durability of foundations and structures like buildings, bridges, dams, etc. |

| Cementitious Fixing | Cementitious fixing is a process in which a cement-based grout is pumped under pressure to fill forms, voids, and cracks. It can be used in several settings, including bridges, marine applications, dams, and rock anchors. |

| Commercial Construction | Commercial construction comprises new construction of warehouses, malls, shops, offices, hotels, restaurants, cinemas, theatres, etc. |

| Concrete Admixtures | Concrete admixtures comprise water reducers, air entrainers, retarders, accelerators, superplasticizers, etc., added to concrete before or during mixing to modify its properties. |

| Concrete Protective Coatings | To provide specific protection, such as anti-carbonation or chemical resistance, a film-forming protective coat can be applied on the surface. Depending on the applications, different resins like epoxy, polyurethane, and acrylic can be used for concrete protective coatings. |

| Curing Compounds | Curing compounds are used to cure the surface of concrete structures, including columns, beams, slabs, and others. These curing compounds keep the moisture inside the concrete to give maximum strength and durability. |

| Epoxy | Epoxy is known for its strong adhesive qualities, making it a versatile product in many industries. It resists heat and chemical applications, making it an ideal product for anyone needing a stronghold under pressure. It is widely used in adhesives, electrical and electronics, paints, etc. |

| Fiber Wrapping Systems | Fiber Wrapping Systems are a part of construction repair and rehabilitation chemicals. It involves the strengthening of existing structures by wrapping structural members like beams and columns with glass or carbon fiber sheets. |

| Flooring Resins | Flooring resins are synthetic materials applied to floors to enhance their appearance, increase their resistance to wear and tear or provide protection from chemicals, moisture, and stains. Depending on the desired properties and the specific application, flooring resins are available in distinct types, such as epoxy, polyurethane, and acrylic. |

| High-Range Water Reducer (Super Plasticizer) | High-range water reducers are a type of concrete admixture that provides enhanced and improved properties when added to concrete. These are also called superplasticizers and are used to decrease the water-to-cement ratio in concrete. |

| Hot Melt Adhesives | Hot-melt adhesives are thermoplastic bonding materials applied as melts that achieve a solid state and resultant strength on cooling. They are commonly used for packaging, coatings, sanitary products, and tapes. |

| Industrial and Institutional Construction | Industrial and institutional construction includes new construction of hospitals, schools, manufacturing units, energy and power plants, etc. |

| Infrastructure Construction | Infrastructure construction includes new construction of railways, roads, seaways, airports, bridges, highways, etc. |

| Injection Grouting | The process of injecting grout into open joints, cracks, voids, or honeycombs in concrete or masonry structural members is known as injection grouting. It offers several benefits, such as strengthening a structure and preventing water infiltration. |

| Liquid-Applied Waterproofing Membranes | Liquid-Applied membrane is a monolithic, fully bonded, liquid-based coating suitable for many waterproofing applications. The coating cures to form a rubber-like elastomeric waterproof membrane and may be applied over many substrates, including asphalt, bitumen, and concrete. |

| Micro-concrete Mortars | Micro-concrete mortar is made up of cement, water-based resin, additives, mineral pigments, and polymers and can be applied on both horizontal and vertical surfaces. It can be used to refurbish residential complexes, commercial spaces, etc. |

| Modified Mortars | Modified Mortars include Portland cement and sand along with latex/polymer additives. The additives increase adhesion, strength, and shock resistance while also reducing water absorption. |

| Mold Release Agents | Mold release agents are sprayed or coated on the surface of molds to prevent a substrate from bonding to a molding surface. Several types of mold release agents, including silicone, lubricant, wax, fluorocarbons, and others, are used based on the type of substrates, including metals, steel, wood, rubber, plastic, and others. |

| Polyaspartic | Polyaspartic is a subset of polyurea. Polyaspartic floor coatings are typically two-part systems that consist of a resin and a catalyst to ease the curing process. It offers high durability and can withstand harsh environments. |

| Polyurethane | Polyurethane is a plastic material that exists in various forms. It can be tailored to be either rigid or flexible and is the material of choice for a broad range of end-user applications, such as adhesives, coatings, building insulation, etc. |

| Reactive Adhesives | A reactive adhesive is made of monomers that react in the adhesive curing process and do not evaporate from the film during use. Instead, these volatile components become chemically incorporated into the adhesive. |

| Rebar Protectors | In concrete structures, rebar is one of the important components, and its deterioration due to corrosion is a major issue that affects the safety, durability, and life span of buildings and structures. For this reason, rebar protectors are used to protect against degrading effects, especially in infrastructure and industrial construction. |

| Repair and Rehabilitation Chemicals | Repair and Rehabilitation Chemicals include repair mortars, injection grouting materials, fiber wrapping systems, micro-concrete mortars, etc., used to repair and restore existing buildings and structures. |

| Residential Construction | Residential construction involves constructing new houses or spaces like condominiums, villas, and landed homes. |

| Resin Fixing | The process of using resins like epoxy and polyurethane for grouting applications is called resin fixing. Resin fixing offers several advantages, such as high compressive and tensile strength, negligible shrinkage, and greater chemical resistance compared to cementitious fixing. |

| Retarder | Retarders are admixtures used to slow down the setting time of concrete. These are usually added with a dosage rate of around 0.2% -0.6% by weight of cement. These admixtures slow down hydration or lower the rate at which water penetrates the cement particles by making concrete workable for a long time. |

| Sealants | A sealant is a viscous material that has little or no flow qualities, which causes it to remain on surfaces where they are applied. Sealants can also be thinner, enabling penetration to a certain substance through capillary action. |

| Sheet Waterproofing Membranes | Sheet membrane systems are reliable and durable thermoplastic waterproofing solutions that are used for waterproofing applications even in the most demanding below-ground structures, including those exposed to highly aggressive ground conditions and stress. |

| Shrinkage Reducing Admixture | Shrinkage-reducing admixtures are used to reduce concrete shrinkage, whether from drying or self-desiccation. |

| Silicone | Silicone is a polymer that contains silicon combined with carbon, hydrogen, oxygen, and, in some cases, other elements. It is an inert synthetic compound that comes in various forms, such as oil, rubber, and resin. Due to its heat-resistant properties, it finds applications in sealants, adhesives, lubricants, etc. |

| Solvent-borne Adhesives | Solvent-borne adhesives are mixtures of solvents and thermoplastic or slightly cross-linked polymers such as polychloroprene, polyurethane, acrylic, silicone, and natural and synthetic rubbers. |

| Surface Treatment Chemicals | Surface treatment chemicals are chemicals used to treat concrete surfaces, including roofs, vertical surfaces, and others. They act as curing compounds, demolding agents, rust removers, and others. They are cost-effective and can be used on roadways, pavements, parking lots, and others. |

| Viscosity Modifier | Viscosity Modifiers are concrete admixtures used to change various properties of admixtures, including viscosity, workability, cohesiveness, and others. These are usually added with a dosage of around 0.01% to 0.1% by weight of cement. |

| Water Reducer | Water reducers, also called plasticizers, are a type of admixture used to decrease the water-to-cement ratio in the concrete, thereby increasing the durability and strength of concrete. Various water reducers include refined lignosulfonates, gluconates, hydroxycarboxylic acids, sugar acids, and others. |

| Water-borne Adhesives | Water-borne adhesives use water as a carrier or diluting medium to disperse resin. They are set by allowing the water to evaporate or be absorbed by the substrate. These adhesives are compounded with water as a dilutant rather than a volatile organic solvent. |

| Waterproofing Chemicals | Waterproofing chemicals are designed to protect a surface from the perils of leakage. A waterproofing chemical is a protective coating or primer applied to a structure's roof, retaining walls, or basement. |

| Waterproofing Membranes | Waterproofing membranes are liquid-applied or self-adhering layers of water-tight materials that prevent water from penetrating or damaging a structure when applied to roofs, walls, foundations, basements, bathrooms, and other areas exposed to moisture or water. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms