Glass Fiber Reinforced Concrete (GFRC) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

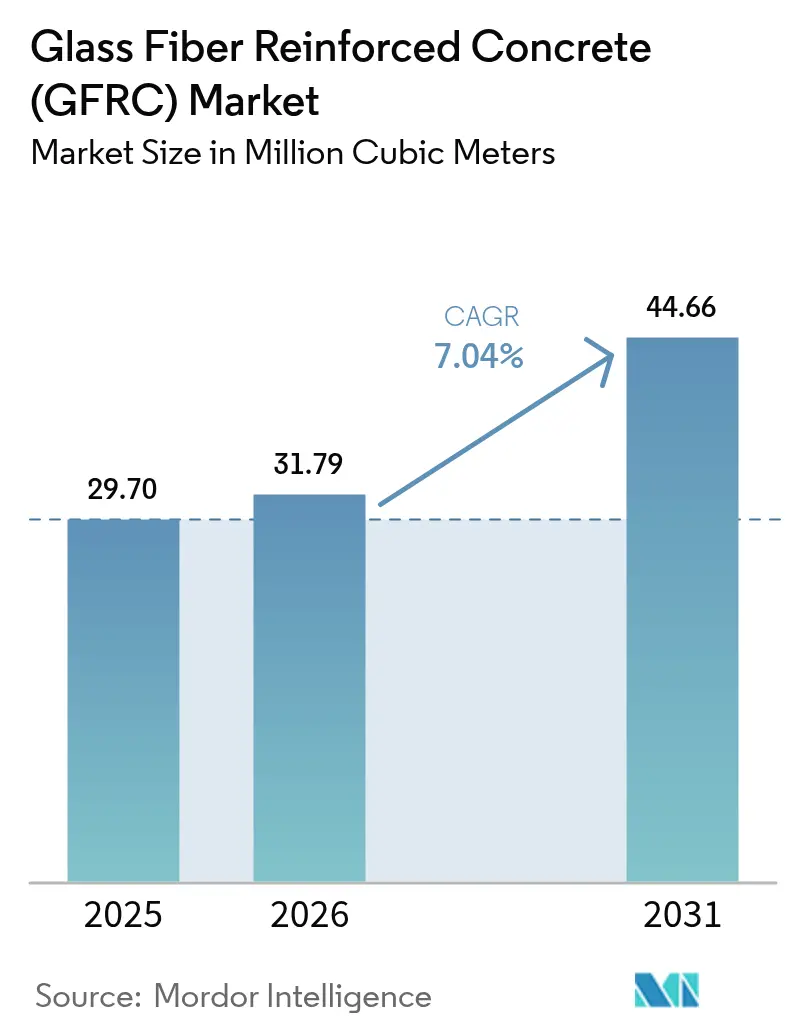

| Market Volume (2026) | 31.79 Million cubic meters |

| Market Volume (2031) | 44.66 Million cubic meters |

| Growth Rate (2026 - 2031) | 7.04% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Glass Fiber Reinforced Concrete (GFRC) Market Analysis by Mordor Intelligence

Glass Fiber Reinforced Concrete Market size in 2026 is estimated at 31.79 million cubic meters, growing from 2025 value of 29.70 million cubic meters with 2031 projections showing 44.66 million cubic meters, growing at 7.04% CAGR over 2026-2031. This expansion is fueled by the material’s higher strength-to-weight ratio, growing green-building mandates, and rapid adoption of digital manufacturing. Infrastructure owners are retrofitting assets with slender GFRC panels to reduce seismic loads, while architects exploit CNC-machined molds to deliver intricate façades at lower cost. Expanded supply of alkali-resistant (AR) fibers stabilizes raw-material pricing, making long-run production planning easier for both regional and global suppliers. However, the pace of growth still hinges on faster code development, as engineers remain cautious where ductility rules favor steel reinforcement.

Key Report Takeaways

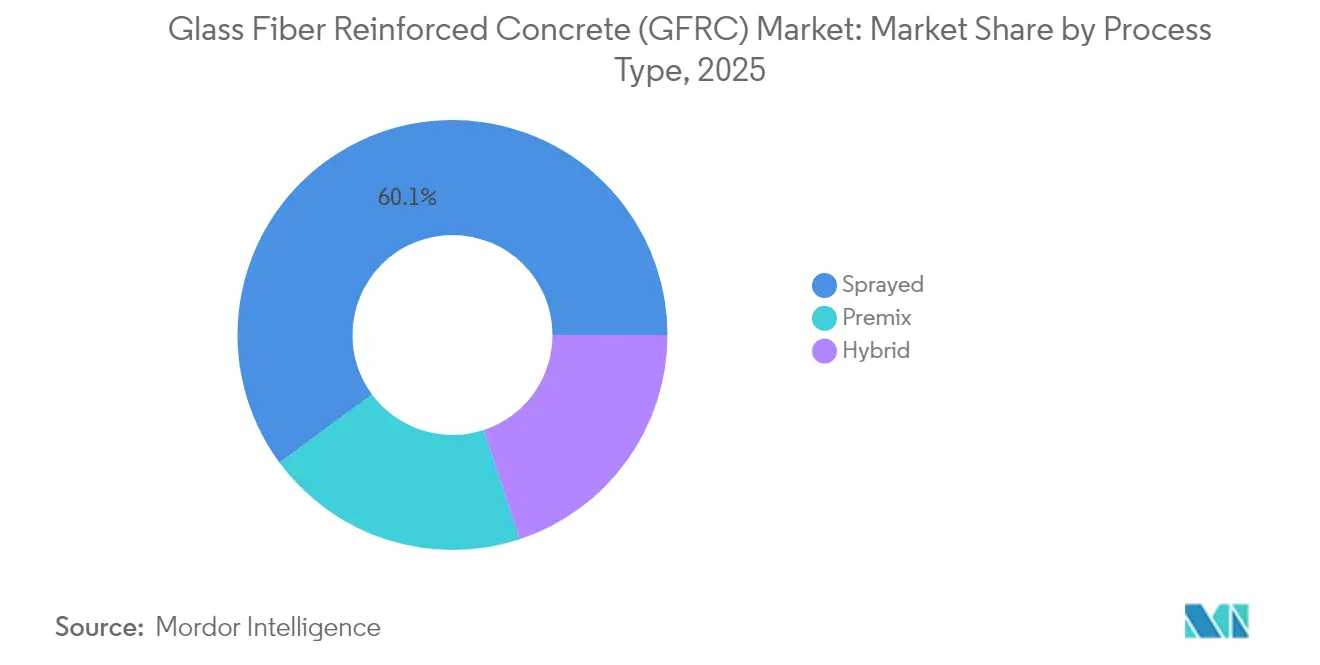

- By process type, the sprayed method captured 60.12% of the glass fiber reinforced concrete market share in 2025 and is growing at a 7.21% CAGR through 2031.

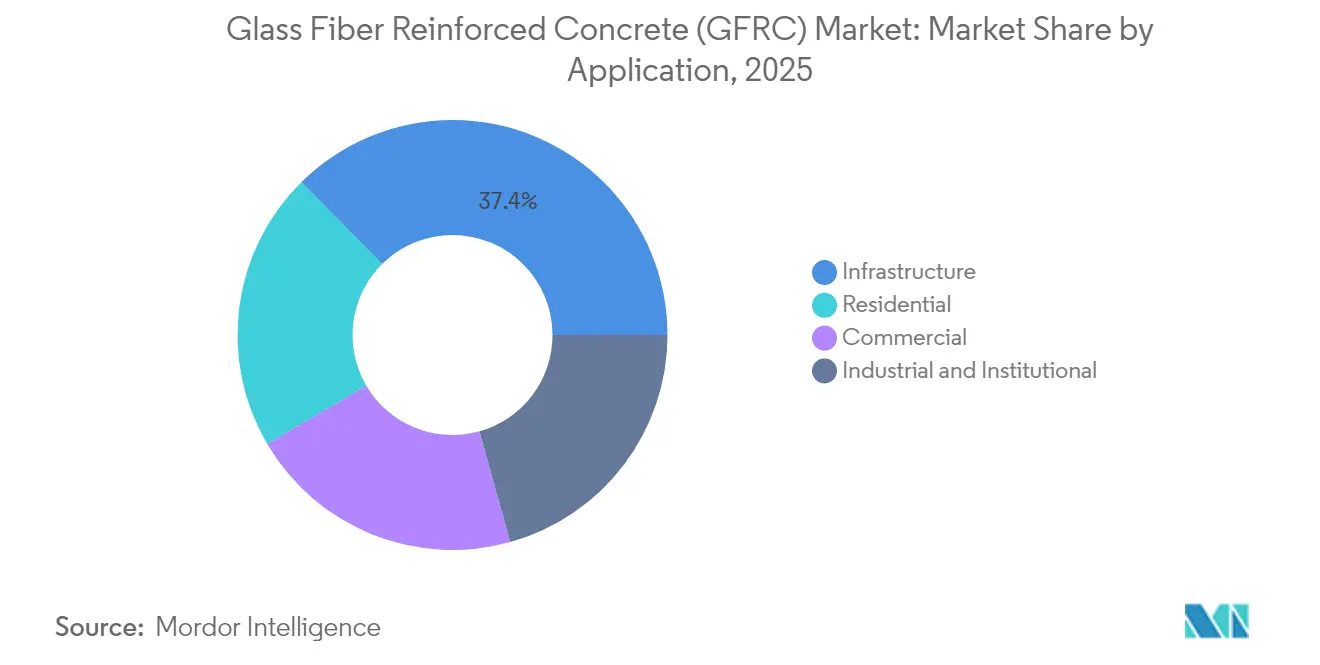

- By application, infrastructure accounted for 37.42% of the glass fiber reinforced concrete market size in 2025, while residential is advancing at a 7.63% CAGR through 2031.

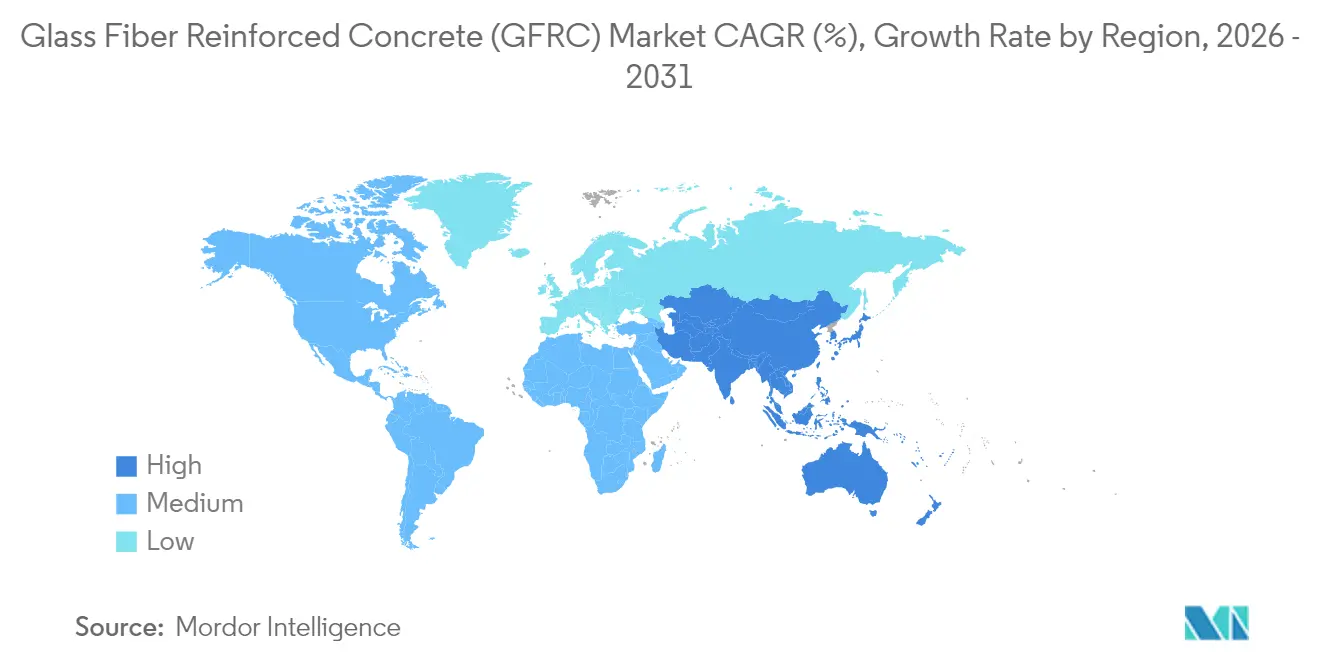

- By geography, Asia-Pacific held 53.58% revenue share of the glass fiber reinforced concrete market in 2025; the region is set to expand at a 7.29% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Glass Fiber Reinforced Concrete (GFRC) Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increased emphasis on green buildings (LEED ratings) | +1.8% | Global, led by North America and EU | Medium term (2-4 years) |

| Superior strength-to-weight ratio reduces structural and logistics cost | +2.1% | Global, especially APAC mega-projects | Long term (≥ 4 years) |

| Precast adoption to cut on-site labor and cycle time | +1.5% | APAC core, rising in North America | Short term (≤ 2 years) |

| Growing availability of alkali-resistant glass fiber supply | +0.9% | Global | Medium term (2-4 years) |

| Digital manufacturing enables complex façades | +0.8% | North America and EU first movers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increased Emphasis on Green Buildings (LEED Ratings)

GFRC reduces cement clinker volume and supports thinner cross-sections, both of which lower embodied carbon. The resulting credits help commercial buildings meet LEED v4 material and resource benchmarks. Developers also gain operational savings because lighter panels permit smaller foundations and less steel framing[1]Chalmers University of Technology, “New Model Makes It Easier to Build Sustainable Structures of Textile-Reinforced Concrete,” techxplore.com . Pilot studies show up to 65% CO₂ savings in floor slabs that combine GFRC skins with recycled aggregates, a result now cited in voluntary disclosure statements across Europe. Structure owners increasingly demand environmental product declarations, and GFRC makers have begun publishing cradle-to-gate data that compares favorably with masonry and precast concrete. These disclosures accelerate specification rates in both public and private tenders.

Superior Strength-to-Weight Ratio Reduces Structural and Logistics Cost

GFRC panels weigh roughly 20% less than comparable reinforced-concrete elements while delivering 25-35% higher ultimate tensile capacity[2]Yaqin Chen et al., “Performance Evaluation of Indented Macro Synthetic Polypropylene Fibers in High Strength Self-Compacting Concrete,” nature.com. Infrastructure teams deploying tunnel liners in China’s Dalian Bay shaved 15 days off crane work after switching to thin GFRC segments. Lower dead load also improves seismic resilience by cutting base shear forces, a concern in Japan and California. Transportation cost drops become notable on long-haul routes where weight-based freight tariffs dominate. These economic gains strengthen the business case despite fiber and polymer premiums relative to ordinary concrete.

Precast Adoption to Cut On-Site Labor and Cycle Time

Chronic craft-labor shortages intensify pressure on contractors to prefabricate structural elements. Controlled factory conditions cut rework and shorten pour-to-install cycles by 20-30%. GFRC offers crisp finishes without external cladding, eliminating multiple job-site trades. Automation readiness adds further value: palletizing robots can place sprayed panels directly onto curing racks, while bar-coding systems track mix designs in real time. The result is predictable throughput that aligns with just-in-time site logistics, giving developers confidence to lock in accelerated delivery milestones.

Growing Availability of Alkali-Resistant Glass Fiber Supply

Regional AR-fiber plants in China and India now serve 80% of Asia-Pacific demand, slashing import lead times and buffering price shocks. Advanced sizings improve bond durability under high-pH pore solutions, extending fatigue life projections beyond 50 years. The tighter supply chain allows mid-tier manufacturers to secure multi-year contracts at indexed rates, a hedge against volatility during construction booms. As fiber suppliers scale, minimum-order volumes drop, bringing smaller mold shops into the market and broadening geographic reach.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack of ductility vs. steel-reinforced concrete | -1.2% | Global, seismic zones | Long term (≥ 4 years) |

| Limited design codes and certification standards | -0.8% | North America and EU | Medium term (2-4 years) |

| High initial cost of proprietary premix/polymer systems | -0.6% | Price-sensitive economies | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Lack of Ductility vs. Steel-Reinforced Concrete

Fiber bridging narrows but does not close the gap between GFRC and steel in post-yield behavior, a property enshrined in seismic-resistance provisions worldwide. Engineers remain uneasy specifying GFRC for plastic hinge regions, particularly in high-rise cores that carry life-safety loads. Hybrid reinforcement trials mixing GFRC panels with internal steel cages show promise, yet add back both weight and corrosion risk, dulling two core advantages. Structural adoption will lag until national codes formally recognize design equations for displacement-based checks.

Limited Design Codes and Certification Standards

The building-code vacuum forces project teams into costly mock-up testing or special-inspection regimes that stretch schedules. While the PCI and GRCA publish best-practice manuals, municipal authorities seldom grant blanket approvals, so every load-bearing use still goes through alternate-means submittals. Divergent acceptance criteria among the International Building Code, Eurocode, and local Asian standards further complicate multinational rollouts. Harmonized test methods under ISO or ASTM banners would streamline compliance, but committee processes move slower than product innovation, stranding new mixtures in regulatory limbo.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Process Type: Versatility of the Sprayed Method

The sprayed route led the glass fiber reinforced concrete market with 60.12% volume in 2025 and is on track for a 7.21% CAGR through 2031. Real-time deposition control and higher fiber alignment deliver reliable tensile capacity, letting producers mold ultra-thin panels that match 1.6 kN/m² wind-load targets. Automated spray guns cut labor hours by 30%, pushing per-panel cost down even on low-volume runs. Hybrid plants overlay premix backing onto sprayed face coats, marrying cosmetic quality with structural heft in one pass. Field adoption rises fastest in stadium roofs and transit hubs that require graceful curves and rapid erection.

Growing penetration of six-axis robots expands the sprayed method beyond premium façade work. Continuous-measurement nozzles now adjust slurry flow for ambient humidity, reducing rebound to under 5% and costing less than manual cleanup. The process remains sensitive to curing-room climate, but sensor-driven HVAC mitigates shrinkage cracking in temperate and tropical zones. Premix-only lines still rule when compressive-strength targets top 100 MPa, yet their slower cycle time limits appeal for mass-produced cladding.

By Application: Infrastructure Momentum and Residential Upswing

Infrastructure owned 37.42% of 2025 shipments, translating to the largest slice of the glass fiber reinforced concrete market size and reflecting public-works demand across tunnels, bridges, and wastewater tanks. Weight savings trim crane capacity and allow prefabricated arch segments that speed nightly bridge-deck replacements. Meanwhile, residential demand climbs at 7.63% CAGR as modular developers in Japan and Australia select GFRC skin-plus-core panels to solve labor gaps and deliver net-zero energy walls.

Commercial towers prefer GFRC curtain walls over aluminum where local codes impose strict fire-spread limits. Institutional campuses—especially hospitals—specify GFRC for interior cladding in MRI suites due to its non-magnetic character. Industrial wastewater operators choose the material for secondary containment basins because chloride resistance exceeds that of epoxy-coated conventional concrete. Each niche adoption feeds a flywheel: higher production volume lowers average cost, prompting architects to expand specification breadth.

Geography Analysis

Asia-Pacific generated 53.58% of global volume in 2025 and carries the highest growth outlook at 7.29% CAGR to 2031. China’s Belt and Road megaprojects demand GFRC, and localized AR-fiber production shortens supply chains. India’s Smart Cities Mission budgets USD 165 billion for transit-oriented hubs, many in corrosive coastal zones perfectly suited to GFRC façades. Japan and South Korea refine seismic-grade mix designs, targeting 1.2 GPa flexural capacity while keeping density below 2,200 kg/m³. Government-backed lab programs certify these formulations, slashing approval hurdles.

North America ranks second in volume and leads in green-building adoption. LEED-linked mandates across California and New York add specification pull, while U.S. federal infrastructure funds channel USD 24 billion toward bridge replacement projects that can benefit from weight-saving GFRC decks. Canada’s cold-climate trials confirm freeze-thaw durability, a prerequisite for Highway 11 viaduct retrofits. Mexico explores GFRC crash-barrier applications on its expanding toll-road network, where lighter panels simplify overnight lane closures.

Europe focuses on retrofit markets, using GFRC to relieve overstressed masonry foundations in historic districts. Germany pilots large-format rainscreen panels integrated with vacuum insulation, meeting near-zero energy targets under the updated EPBD. The United Kingdom reshapes the office refurb sector after whole-life carbon criteria entered planning guidance in 2025. France courts heritage-preservation specialists by coloring GFRC with iron oxide pigments that mimic sandstone while resisting acid rain. Italy deploys slender vault shells inside basilica restorations, exploiting the material’s high impact resilience.

Competitive Landscape

Global supply is fragmented, yet regional oligopolies form around fiber, binder, and panel capacity. Innovation strategy now tilts toward Industry 4.0. European suppliers deploy digital twins to predict panel distortion during cure, while U.S. startups fit machine-vision cameras that scan fiber distribution. Asia-Pacific giants couple proprietary AR-fiber plants with captive panel shops, allowing cost-plus pricing that undercuts independent molders. Yet capital intensity—robotic arms, curing kilns, real-time analytics—raises financial barriers for new entrants. Consolidation is expected as middle-tier firms lacking scale share transfer to investors eager for environmental-tech exposure. Over the horizon, recycled carbon fiber fillers loom as a disruptive option, promising higher strength-to-weight ratios at modest carbon impact.

Glass Fiber Reinforced Concrete (GFRC) Industry Leaders

Formglas Products Ltd

Ultratech Cement Ltd

Clark Pacific

Fibrex Construction Group

Betofiber

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: PORAVER gmbh announced to provide expanded glass to improve the properties of glass fiber-reinforced concrete. By incorporating PORAVER, manufacturers can significantly lower the weight of GFRC components.

- February 2025: Ibstock plc. announced its exit from the Glass Fiber Reinforced Concrete (GFRC) division, following sustained financial underperformance. The company ceased production after its GFRC division reported a trading loss of GBP 3 million in 2024, driven by intense margin pressure and subcontractor failures.

Global Glass Fiber Reinforced Concrete (GFRC) Market Report Scope

The glass fiber reinforced concrete (GFRC) market is segmented by type, application, and geography. By type, the market is segmented into sprayed, premix, and hybrids. By application, the market is segmented into architecture, engineering, defense, and other applications. The report also covers the market sizes of and forecasts for the glass fiber reinforced concrete (GFRC) market in 15 countries across the major regions. For each segment, the market sizing and forecasts have been done on the basis of revenue (USD million).

| Sprayed |

| Premix |

| Hybrid |

| Commercial |

| Residential |

| Infrastructure |

| Industrial and Institutional |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Process Type | Sprayed | |

| Premix | ||

| Hybrid | ||

| By Application | Commercial | |

| Residential | ||

| Infrastructure | ||

| Industrial and Institutional | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large will the glass fiber reinforced concrete market be by 2031?

Volume is forecast to reach 44.66 million cubic meters by 2031, reflecting a 7.04% CAGR from 31.79 million cubic meters in 2026.

Which region leads the current demand for GFRC?

Asia-Pacific commands 53.58% of global volume thanks to large infrastructure programs and local fiber production advantages.

What application segment shows the fastest growth?

Residential construction is expanding at a 7.63% CAGR as developers adopt precast GFRC panels to reduce labor and accelerate schedules.

Why are architects choosing GFRC over aluminum curtain walls?

GFRC offers lighter weight, superior fire resistance, and the ability to deliver complex shapes at lower embodied carbon.

What limits structural adoption of GFRC today?

Engineers remain cautious due to limited ductility relative to steel reinforcement and the lack of comprehensive design codes.

Page last updated on: