Glamping Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

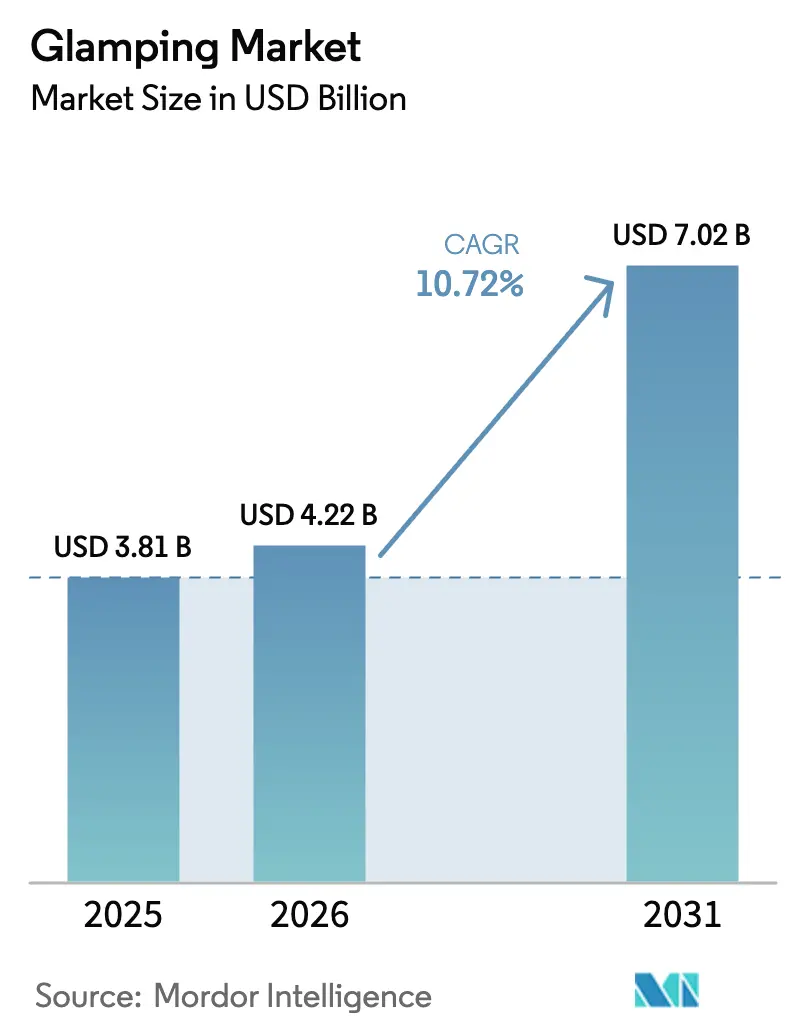

| Market Size (2026) | USD 4.22 Billion |

| Market Size (2031) | USD 7.02 Billion |

| Growth Rate (2026 - 2031) | 10.72% CAGR |

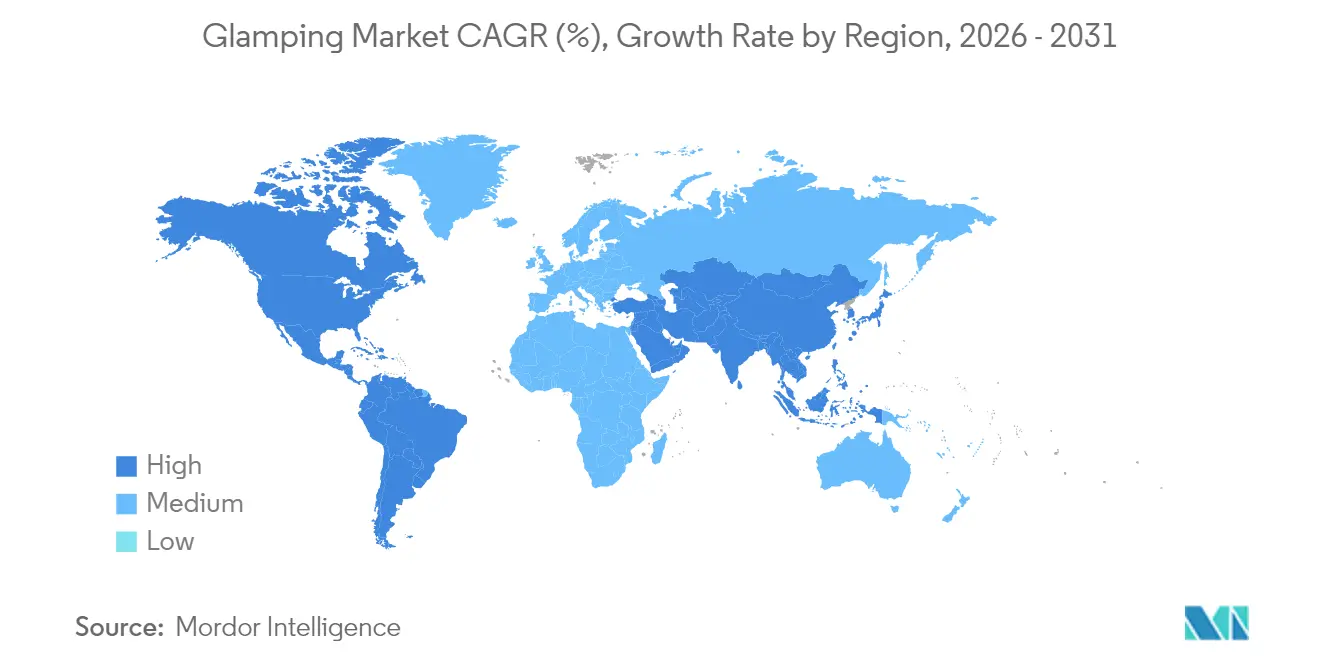

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Glamping Market Analysis by Mordor Intelligence

The glamping market size is expected to grow from USD 3.81 billion in 2025 to USD 4.22 billion in 2026 and is forecast to reach USD 7.02 billion by 2031 at 10.72% CAGR over 2026-2031. Rising disposable incomes, a growing preference for nature-immersive trips that do not sacrifice comfort, and the integration of loyalty programs by global hotel chains are accelerating demand. Partnerships such as Hyatt–Under Canvas and Hilton–AutoCamp broaden the customer base beyond traditional campers toward mainstream luxury travelers. Investors also signal confidence by channeling capital into purpose-built sites, and regulatory clarity in mature tourism markets reduces development risk. On the supply side, operators that control and upgrade physical assets deliver consistent quality and justify premium pricing, pushing the glamping market toward a distinct hospitality tier rather than a subset of camping.

Key Report Takeaways

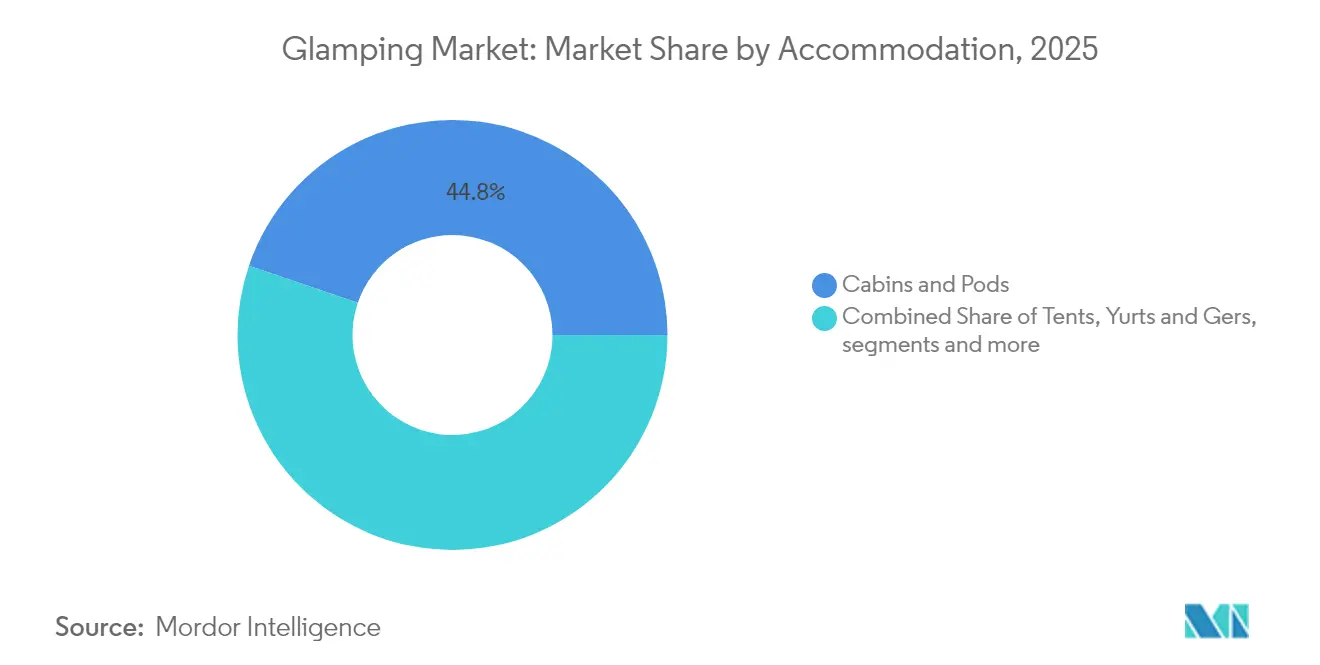

- By accommodation type, Cabins & Pods led with 44.78% of the glamping market share in 2025, while Treehouses & Canopy Suites posted the fastest growth at 11.36% CAGR to 2031.

- By age group, the 18-32 cohort captured 38.92% revenue share in 2025; the 33-50 segment is projected to expand at a 9.86% CAGR in the glamping market.

- By booking mode, Online Booking Platforms accounted for 56.94% of the glamping market size in 2025 and are advancing at an 11.12% CAGR.

- By application, Family Travel represented 49.55% of the glamping market size in 2025, whereas Wellness & Retreats is forecast to grow at 11.47% CAGR.

- By geography, North America held 38.96% of the glamping market share in 2025; Asia-Pacific records the highest projected CAGR at 12.58% through 2031.

- Top 5 players such as Canvas, AutoCamp, Huttopia, Collective Retreats, and Getaway hold significant market share in 2024.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Glamping Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for unique travel experiences | +2.8% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Growing interest in eco-friendly and sustainable tourism | +2.1% | Europe & North America core, expanding to APAC | Long term (≥ 4 years) |

| Influence of social media and digital marketing | +1.9% | Global, strongest in APAC and North America | Short term (≤ 2 years) |

| Popularity of staycations and local travel | +1.6% | Global, particularly post-pandemic recovery regions | Short term (≤ 2 years) |

| Technological advancements in glamping accommodation | +1.4% | North America & Europe, selective APAC adoption | Medium term (2-4 years) |

| Diverse accommodation options | +1.2% | Global, with regional preferences varying | Medium term (2-4 years) |

| Supportive government initiatives | +0.8% | APAC core, selective adoption in other regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Unique Travel Experiences

Fifty-eight percent of couples cite uniqueness as their top selection criterion for glamping stays, often reserving them for celebrations. Luxury chains respond by opening tented resorts with rates starting at USD 4,000 per night, a sign that affluent travelers will pay premium prices for curated outdoor experiences. Operators that weave local culture into design and activities capture this premium, elevating the glamping market above commodity lodging. Pricing power is reinforced by limited-inventory, location-specific structures that cannot be replicated in urban hotels. As these differentiated stays proliferate, the glamping market deepens its status as an experience-economy offering.

Influence of Social Media and Digital Marketing

Online booking already represents 57.61% of revenue and grows the fastest among all channels. Eye-catching visuals of domes, treehouses, and safari tents encourage user-generated content that lowers acquisition costs while amplifying brand reach. Social platforms, therefore, level the playing field by giving smaller operators access to global audiences, although dependence on algorithms also introduces exposure to sudden policy shifts. The glamping market benefits from this digital virality, but operators hedge risk by developing direct-to-consumer capabilities.

Growing Interest in Eco-Friendly and Sustainable Tourism

Sustainability now influences the choices of 59% of travelers. Operators emphasize low-impact construction, water-saving fixtures, and renewable-energy solutions that meet both guest expectations and regulatory demands. For instance, Under Canvas uses rechargeable power packs and low-flow plumbing across its American portfolio. In Europe, investors back projects that pair environmental stewardship with local community engagement, signaling that green credentials are evolving from differentiation to requirement. These factors together funnel growth toward operators, able to verify eco-standards, reinforcing the upward trajectory of the glamping market.

Technological Advancements in Glamping Accommodation

Smart-site design reconciles guest comfort with wilderness settings. Many sites restrict Wi-Fi to encourage digital detox yet install solar systems, IoT climate control, and app-based check-ins to streamline operations. The paradox of high-touch service in an off-grid environment requires precise infrastructure planning. It also links directly to sustainability goals by moderating energy use and enabling real-time monitoring of resource consumption, a core expectation among environmentally conscious guests.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High up-front site infrastructure CAPEX | -1.8% | Global, particularly acute in remote locations | Short term (≤ 2 years) |

| Zoning / land-use restrictions | -1.4% | North America & Europe, emerging in APAC | Long term (≥ 4 years) |

| Seasonality and weather-related occupancy risk | -1.2% | Temperature-sensitive regions, Northern climates | Medium term (2-4 years) |

| Rural hospitality labour shortages | -0.9% | Global, most acute in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Up-Front Site Infrastructure CAPEX

Bringing utilities, access roads, and waste treatment to remote plots pushes initial project cost above typical hotel renovations. Asset-light franchisors once sidestepped these hurdles, yet Tentrr’s Chapter 7 filing after managing 1,000 locations exposed the limits of low-control models. Larger players counter with vertical integration that safeguards quality and unlocks economies of scale, but high capital needs still deter many entrepreneurs from entering the glamping market.

Seasonality and Weather-Related Occupancy Risk

Severe winters can force multi-month closures or require insulated structures that inflate operating budgets. Single-site operators are most vulnerable, as revenue swings complicate debt schedules and staffing plans. Diversifying across climates eases the strain yet demands further capital, reinforcing consolidation dynamics as only well-funded brands can smooth seasonal volatility across a balanced portfolio.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Accommodation: Customer comfort drives cabin dominance

Cabins & Pods secured 44.78% of revenue in 2025, translating into the largest slice of the glamping market. The format delivers weather protection, private bathrooms, and climate control, matching family expectations for safety and convenience. The segment’s scale also lets operators amortize investment in year-round insulation, reducing downtime linked to cold seasons. Treehouses & Canopy Suites stage the fastest rise at 11.36% CAGR thanks to striking designs that command daily rates above comparable cabins. These experiential builds resonate with social-media-driven demand, adding fresh momentum to the glamping market.

Yurts and gers cater to culture-seeking guests, while domes, bubbles, and igloos serve sky-gazing travelers willing to pay for unobstructed night-viewing. Boats and houseboats remain niche because marina leases cap expansion, yet they expand the total addressable glamping market by tapping waterfront demand. The breadth of structures positions the market to meet diverse traveler motivations, which supports growth in both mature and emerging tourism regions.

By Age Group: Widening appeal beyond early adopters

The 18-32 segment captured 38.92% of sales in 2025, underscoring millennials’ preference for experience over asset accumulation. As this cohort ages, family formation lifts demand for multi-room units and kid-friendly programming. The 33-50 segment’s 9.86% CAGR confirms that trend, showing the glamping market is maturing from novelty to mainstream vacation option.

Japanese surveys report that couples in their 30s represent the highest intent to glamp at 29.6%, illustrating the demographic shift. Operators, therefore, invest in flexible layouts and group amenities. Meanwhile, empty nesters sit at the fringe, constrained by mobility concerns that the glamping industry addresses through accessible boardwalks and on-site medical support.

By Booking Mode: Digital reach underpins volume growth

Online platforms contributed 56.94% of 2025 revenue and are expanding at 11.12% CAGR, anchoring the largest slice of the glamping market size for distribution channels. Aggregators aggregate limited inventory, simplify price comparisons, and reduce marketing spend for smaller brands. Yet the fee structure pressures margins, prompting larger operators to funnel repeat guests into direct booking portals to capture data and control brand narrative.

Traditional travel agents retain relevance for cross-border packages that weave glamping with cultural tours or adventure sports. Direct-to-site phone reservations persist among older travelers and in regions with patchy internet, but their share continues to erode. This channel mix indicates that digital competence is no longer optional in the glamping market.

By Application: Families shape core use cases

Family Travel represented 49.55% of the glamping market size in 2025. Parents value safe, controlled interaction with nature, pushing operators to install playgrounds, supervision services, and allergy-aware menus. Wellness & Retreats, growing at 11.47% CAGR, answers rising mental-health awareness with yoga decks and mindfulness trails.

Couples’ Getaways remain vital during shoulder seasons because romantic escapes fill mid-week slots. Digital-nomad packages merge high-speed internet with scenic workspaces, quelling seasonality dips. Festivals and corporate gatherings leverage temporary tent villages but planning complexity and insurance requirements constrain their share despite high spend per attendee.

Geography Analysis

North America’s 38.96% revenue share in 2025 owes much to vast public lands, matured outdoor culture, and clear permitting. Strategic alliances, such as Hyatt’s linkage of 13 Under Canvas sites to its loyalty scheme, funnel city-hotel guests toward tents and safari-style suites. The United States further lowers operator barriers through state frameworks such as Utah’s glamping ordinance that codifies health and safety rules. Canada mirrors the trend by pairing wilderness reserves with eco-certified lodging, while Mexico demonstrates premium potential with tent resorts priced from USD 4,000 nightly.

Asia-Pacific delivers the fastest growth at 12.58% CAGR. Japanese consumer research shows 43.1% have already experienced glamping and 32.7% intend to do so, putting total addressable interest above 75% of leisure travelers. India’s Ministry of Tourism guidelines for tented accommodations accelerate site approvals, particularly near heritage zones and tiger reserves. China’s domestic tourism rise and Australia’s long-standing eco-tour circuits add additional tailwinds. Year-round warm climates in Southeast Asia also mitigate seasonality risks that plague temperate markets.

Europe blends regulatory maturity with strong demand. The EUR 120 million (USD 130 million) investment from Hines and Clessidra into Human Company underscores institutional appetite for scalable, sustainable outdoor hospitality. Scotland’s licensing regime for pods establishes fire-safety and community-impact thresholds, likely informing future EU standards. Germany, France, and the United Kingdom channel their rich camping heritage into higher-spend glamping stays, while Mediterranean coasts see luxury tents complementing resort inventory. Together these factors anchor Europe as a benchmark for sustainability and compliance within the global glamping market.

Competitive Landscape

The glamping market remains moderately fragmented, yet the collapse of Tentrr after operating 1,000 franchised locations signals mounting consolidation pressure. Under Canvas, AutoCamp, Huttopia, Collective Retreats, and Getaway differentiate through full property control, assuring consistency that asset-light models struggle to match. Their vertical integration allows bespoke design, strict maintenance, and seamless brand storytelling important to loyalty-program travelers.

Strategic hotel alliances widen distribution and lower customer-acquisition costs. Hilton’s deal with AutoCamp lets Honors members redeem points for Airstream stays, while Hyatt expands its luxury footprint via Under Canvas. Capital channels follow, with Human Company drawing EUR 120 million to build eco-certified Italian sites and Huttopia adding EUR 13 million for European growth. Private-equity buyers such as DLP Capital group multiple RV resorts under unified management, blending campground experience with glamping amenities.

Emerging entrants pursue micromarkets like wellness sanctuaries, corporate retreats, and nomad hubs. Competitive edges arise from technology overlays such as contactless check-in, remote monitoring, and solar-powered climate control. Brands also experiment with floating domes and subterranean lodges that stretch conventional definitions, expanding the ceiling for the glamping market. Overall, success hinges on marrying scale economics with authentic, site-specific storytelling—an equation favoring players who own or long-lease their land assets.

Glamping Industry Leaders

Under Canvas

AutoCamp

Huttopia

Collective Retreats

Getaway

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Under Canvas unveiled plans for its first Pacific Northwest site in Washington’s White Salmon River Valley with safari-inspired tents, low-flow toilets, and rechargeable power packs.

- January 2025: Human Company secured EUR 120 million (USD 130 million) from Hines and Clessidra to expand open-air hospitality in Italy.

- July 2024: Hyatt Hotels integrated 13 Under Canvas properties into World of Hyatt loyalty program.

- February 2024: Hilton enabled Honors members to book stays at AutoCamp Airstream and cabin sites.

Global Glamping Market Report Scope

Glamping, a blend of "glamorous" and "camping," offers luxury in outdoor experiences. From canvas tents to treehouses, glamping destinations span the globe. Its visual appeal gained traction on social media, with platforms like Instagram and Pinterest driving its popularity. The term combines glamour and camping, signifying an upscale alternative to traditional camping. Glamping experiences vary, from basic safari tents to extravagant treehouses, catering to different luxury levels. Unlike traditional camping, glamping eliminates the need for gear like tents or firewood. Guests arrive to ready-made setups, such as roaring campfires, enhancing convenience. Social media showcased glamping as more than a trend, portraying it as an accessible luxury experience that redefined outdoor recreation for a broader audience.

The glamping market is segmented by accommodation (tents, yurts, treehouses, boats & houseboats, cabins & pods, others), by age group (18 - 32 years, 33 - 50 years, 51 - 65 years, above 65 years), by booking mode (direct booking, travel agents, online booking platforms), by application (family travel, couples getaways, solo travel, wellness & retreats, others), by Geography (North America, Europe, Asia Pacific, Latin America, Middle East and Africa). The report offers the market size and forecasts in value (USD) for all the above segments.

| Tents |

| Yurts and Gers |

| By Accommodation |

| Cabins and Pods |

| Domes, Bubbles and Igloos |

| Boats and Houseboats |

| Other Concepts |

| 18 - 32 years |

| 33 - 50 years |

| 51 - 65 years |

| Above 65 years |

| Direct-to-Site |

| Travel Agents |

| Online Booking Platforms |

| Family Travel |

| Couples Getaways |

| Solo and Digital-Nomad Travel |

| Wellness and Retreats |

| Festivals and Corporate Events |

| Other |

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | |

| Rest of Asia-Pacific | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Accommodation | Tents | |

| Yurts and Gers | ||

| By Accommodation | ||

| Cabins and Pods | ||

| Domes, Bubbles and Igloos | ||

| Boats and Houseboats | ||

| Other Concepts | ||

| By Age Group | 18 - 32 years | |

| 33 - 50 years | ||

| 51 - 65 years | ||

| Above 65 years | ||

| By Booking Mode | Direct-to-Site | |

| Travel Agents | ||

| Online Booking Platforms | ||

| By Application | Family Travel | |

| Couples Getaways | ||

| Solo and Digital-Nomad Travel | ||

| Wellness and Retreats | ||

| Festivals and Corporate Events | ||

| Other | ||

| By Geography | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | ||

| Rest of Asia-Pacific | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the glamping market?

The glamping market stands at USD 4.22 billion in 2026 and is on track to reach USD 7.02 billion by 2031.

What is the current Glamping Market size?

In 2026, the Glamping Market size is expected to reach USD 4.22 billion.

Which accommodation type contributes most to revenue?

Cabins & Pods lead with a 44.78% share thanks to their weather resilience and family-friendly amenities.

Which region is growing fastest?

Asia-Pacific records the highest CAGR at 12.58% between 2026 and 2031, driven by rising middle-class spending and urban stress relief.

How are hotel chains influencing the sector?

Partnerships such as Hyatt–Under Canvas and Hilton–AutoCamp integrate glamping sites into global loyalty programs, broadening reach and elevating service standards.

What role does sustainability play in guest choice?

Fifty-nine percent of travelers prefer eco-friendly options, prompting operators to adopt low-impact construction, renewable energy, and resource-efficient operations.

Page last updated on: