Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

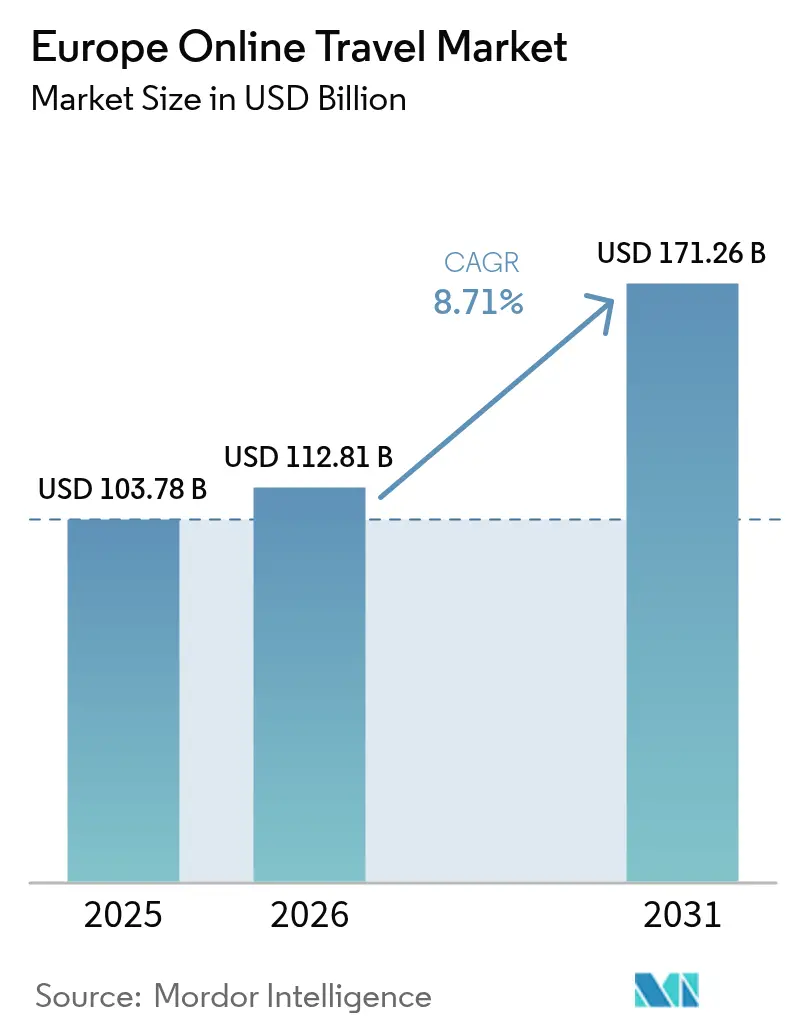

| Base Year Market Size (2025) | USD 103.78 Billion |

| Market Size (2026) | USD 112.81 Billion |

| Market Size (2031) | USD 171.26 Billion |

| Growth Rate (2026 - 2031) | 8.71% CAGR |

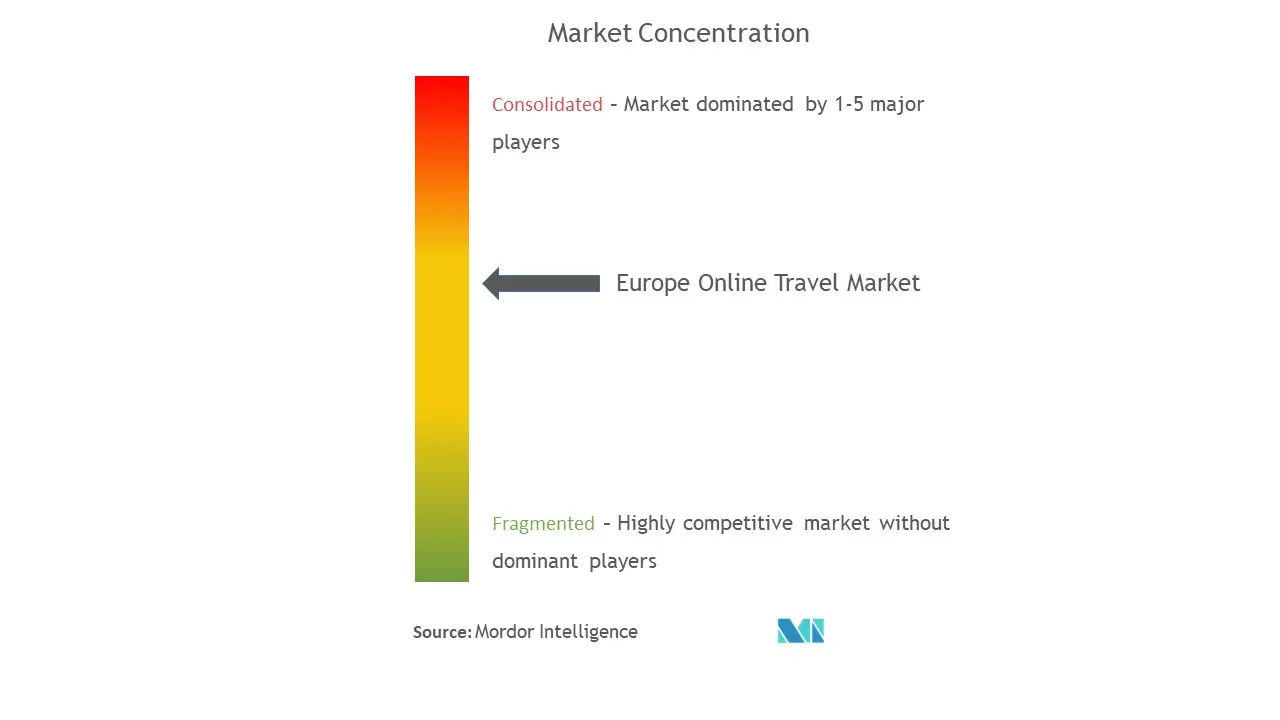

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Online Travel Market Analysis by Mordor Intelligence

The Europe online travel market size was valued at USD 103.78 billion in 2025 and estimated to grow from USD 112.81 billion in 2026 to reach USD 171.26 billion by 2031, at a CAGR of 8.71% during the forecast period (2026-2031). This expansion is powered by post-pandemic rebound in intra-European and long-haul tourism, intensifying mobile-first booking behaviours, and regulatory catalysts such as the forthcoming EU Digital Identity Wallet that promises one-click authentication across borders. Heightened airline adoption of New Distribution Capability (NDC) protocols is redistributing pricing power toward carriers, while generative-AI trip-planning tools funnel search intent directly into bookable inventory, shortening the booking funnel for both consumers and suppliers. Competitive dynamics remain moderate because the top five companies hold just 48.9% of revenue, leaving ample space for differentiated entrants specializing in sustainable travel, multimodal transport, and hyper-localized experiences. Meanwhile, spiralling traffic-acquisition costs driven by the Digital Markets Act force leading OTAs to rethink marketing mixes, emphasizing loyalty ecosystems and subscription programs over purely search-driven growth. Taken together, these macro forces establish a resilient demand base for the Europe online travel market despite regulatory headwinds and intensifying supplier-direct campaigns.

Key Report Takeaways

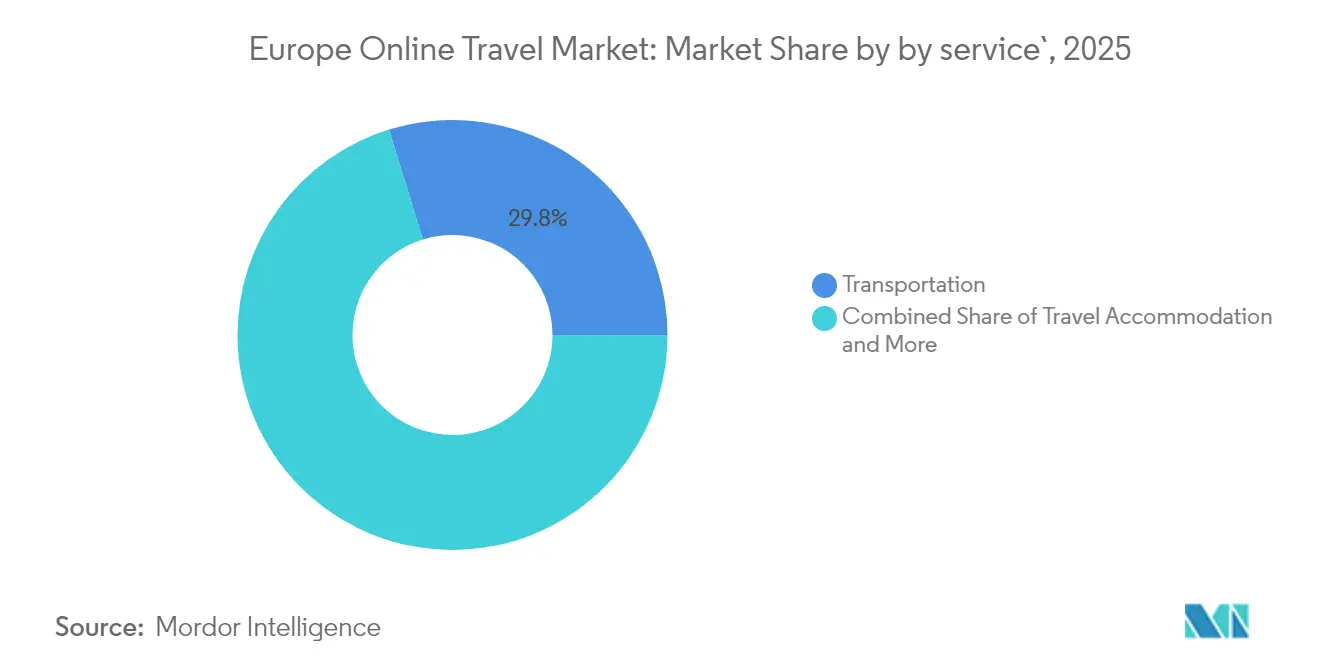

- By service type, transportation captured 29.78% of Europe online travel market share in 2025, whereas vacation packages are on track for the fastest 11.86% CAGR through 2031.

- By booking type, direct suppliers commanded 54.02% share of the Europe online travel market size in 2025, but OTAs are forecast to expand at a 9.05% CAGR between 2026 and 2031.

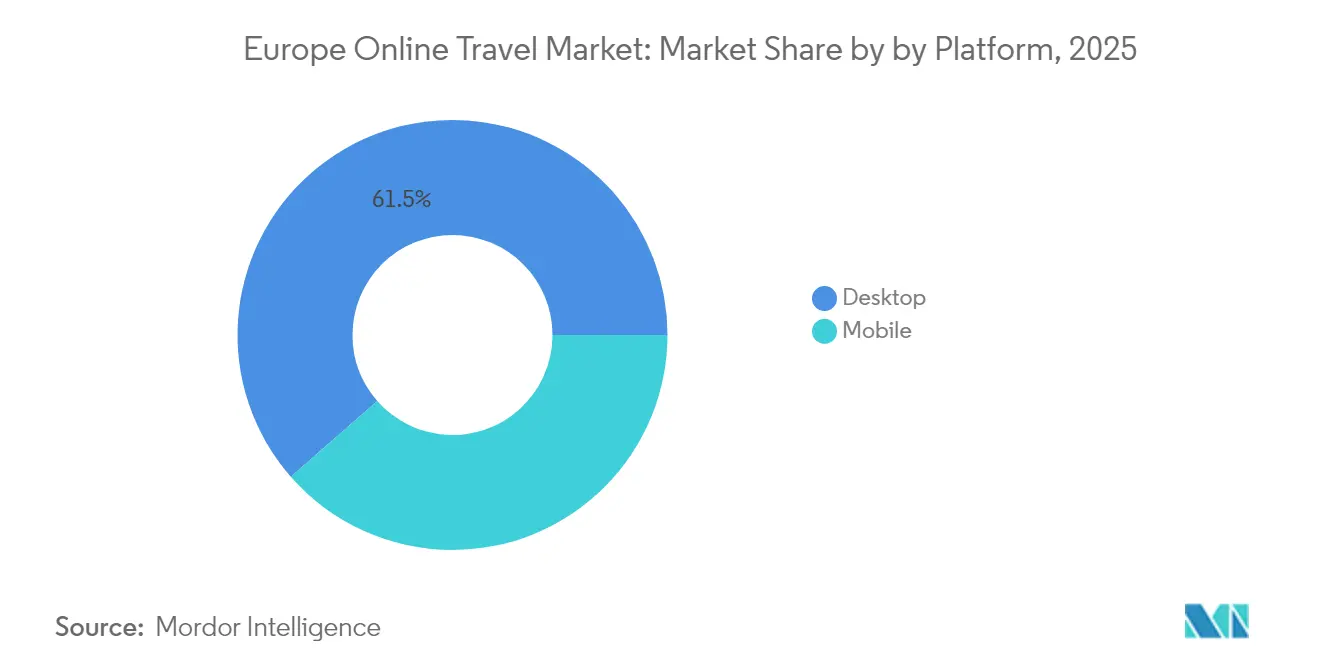

- By platform, desktop bookings led with 61.45% share of the Europe online travel market size in 2025, while mobile is projected to post the highest 13.12% CAGR through 2031.

- By geography, the United Kingdom held the largest 21.05% contribution to the Europe online travel market in 2025, whereas Spain is primed for the strongest 11.58% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Online Travel Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-pandemic rebound in intra-European and long-haul tourism | +2.1% | UK, Germany, France, Spain | Short term (≤ 2 years) |

| Surge in mobile booking penetration and in-app payments | +1.8% | Europe-wide; Nordic and BENELUX hot spots | Medium term (2 – 4 years) |

| EU Digital Identity Wallet enabling one-click checkout | +1.2% | EU-27 pilot markets first | Medium term (2 – 4 years) |

| Generative-AI trip-planning bots accelerating conversion | +1.5% | Germany, UK, Netherlands | Long term (≥ 4 years) |

| Liberalised high-speed rail & multimodal ticketing APIs widen online transport inventory | +1.3% | France, Germany, Spain, cross-border EU | Medium to Long term (2–5 years) |

| Lifestyle & hybrid hotel formats using API-first distribution | +1.0% | Urban hubs across Western & Central Europe | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Post-pandemic tourism rebound

France welcomed more than 100 million international visitors in 2024, surpassing pre-crisis highs and setting a benchmark for the Europe online travel market[1]Source: Campus France, “2024, a Record Year for International Tourism in France,” campusfrance.org. Spain followed suit with 94 million foreign arrivals, a surge that lifted travel receipts and fueled online booking demand, particularly for higher-yield long-haul segments originating in North America. UK-bound inbound tourism reached record spending levels, reinforcing demand for dynamic packaging services that combine flights, hotels, and rail. Long-haul markets such as China demonstrated 40% growth in nights spent in France, signalling renewed appetite for European itineraries despite revenue remaining below 2019 benchmarks. Business travel remains subdued, but hybrid leisure-business (bleisure) itineraries are rising, causing suppliers to revamp loyalty programs around extended-stay rewards. The rebound underscores a structural pivot toward flexible digital channels as travelers prioritize real-time availability over traditional agency visits.

Mobile booking penetration

Mobile devices manage a growing share of transactions as European consumers integrate digital wallets and contactless payments into everyday life. Nordic countries, where mobile wallet usage exceeds 75%, illustrate how seamless payments accelerate app conversion rates. Booking Holdings reported double-digit mobile booking growth after deploying micro-personalization features that adjust inventory display to user context. Rail-first app Trainline now accounts for most European rail bookings, demonstrating how frictionless mobile UX can unlock highly fragmented transport markets. App-first challenger Omio launched Flex across continental markets, allowing travelers to change itineraries post-purchase, reinforcing the appeal of mobile-centric flexibility. Payment-method diversity from Apple Pay in Germany to Bizum in Spain compels platforms to localize checkout, driving further investment into payment orchestration middleware.

EU Digital Identity Wallet

The EU Digital Identity Wallet scheduled for 2026 rollout will store government-verified credentials, enabling instant passenger identity verification during booking and check-in[2]Source: European Commission, “European Digital Identity,” commission.europa.eu. Early pilots in Belgium and Estonia reduced check-in times by 35%, illustrating clear value in complex cross-border travel. OTAs integrating the wallet can skip repetitive KYC checks, lowering abandonment rates and fraud costs. Hotels expect smoother compliance with Schengen guest registration laws once digital IDs replace manual passport scans. Large tech suppliers, notably Amadeus, already invest in single-API frameworks for wallet integration, signalling industry-wide readiness. Over time, one-click identity is likely to become table stakes for the Europe online travel market, resetting customer expectations around speed and privacy.

Generative-AI trip-planning bots

Conversational AI systems that transform open-ended inspiration into bookable itineraries shorten the discovery funnel and may reorganize search economics. Google’s AI Overviews now surface fully priced itineraries in SERPs, reducing traffic volume to traditional comparison sites. Leading OTAs respond by deploying proprietary large-language models to personalize suggestions and auto-bundle ancillaries that push average booking value upward. Airlines feed real-time fares and seat-map APIs into chatbots to upsell preferred seating and carbon-offset options, proving AI’s monetization potential on supplier-direct channels. Early adopters in Germany and the Netherlands witness higher cross-sell rates for rail-hotel combos generated by AI. While data privacy regulation remains stringent, clear commercial upside is accelerating investment in generative-AI through 2030.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital Markets Act inflates OTA traffic-acquisition costs | –1.4% | EU-27 | Short term (≤ 2 years) |

| Supplier-direct campaigns compress OTA commission rates | –0.9% | Europe-wide | Medium term (2 – 4 years) |

| Consumer privacy push limits personalization and retargeting effectiveness | –0.8% | Europe-wide, especially Germany & France | Medium term (2–4 years) |

| Slow adoption of NDC standards delays flight content parity | –0.6% | EU major airline markets | Short to Medium term (1–3 years) |

| Source: Mordor Intelligence | |||

Digital Markets Act costs

The Digital Markets Act designates major OTAs as “gatekeepers,” subjecting them to new self-preferencing and data-sharing rules that diminish organic search visibility and raise paid marketing costs [3]Source: Phocuswire Staff, “Phocuswright Analyst Travel Predictions 2025,” phocuswire.com. Booking.com’s removal of rate-parity clauses exemplifies shifts hitting commission models and net margins. Meta-search engines like Skyscanner gain short-term advantage because diversified traffic sources dilute dependence on Google. Yet compliance complexity may entrench larger incumbents that can absorb additional legal and technical overhead, raising barriers for smaller rivals. Across Europe, class-action litigation against OTA pricing practices intensifies, adding incremental risk. Higher CAC pressures force OTAs to deepen loyalty programs, invest in brand media, and experiment with membership plans to stabilize repeat bookings.

Supplier-direct campaigns

Airlines and hotel chains leverage NDC plumbing to enforce content differentiation in their own channels, often adding GDS surcharges that push corporate buyers toward direct booking. Lufthansa Group, British Airways, and Air France-KLM now reserve key ancillaries such as seat selection and free rebooking for direct customers, cutting OTA attach-rate potential. Hotel majors expand “book direct” campaigns that bundle Wi-Fi upgrades and member-only rates unavailable in public feeds. The net effect compresses OTA commission pools, prompting them to diversify into fintech products like deferred payment and dynamic currency conversion. At the same time, suppliers face higher technology costs to maintain modern e-commerce stacks, prompting selective partnerships with tech-savvy aggregators. Direct-vs-indirect channel tension will stay central to competitive strategy in the Europe online travel market through the next five years.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Transportation Dominance Faces Package Surge

Transportation ranked first with 29.78% Europe online travel market share in 2025 as rail, aviation, and intercity bus operators scaled API connectivity and dynamic pricing engines. Vacation packages, although smaller, are predicted to deliver a 11.86% CAGR, signalling consumer appetite for curated, hassle-free experiences that bundle mobility with lodging and activities. The Europe online travel market size for transportation continues to benefit from continent-wide rail liberalization and highway toll digitization that unlock real-time inventory for third-party platforms. Meanwhile, the package segment attracts funding for software-defined tour operators able to compose flights, hotels, and experiences in milliseconds. Suppliers capitalize on this growth by integrating channel-agnostic APIs, enabling OTAs to sell dynamically priced packages complete with flexible cancellation policies. Overall, service-type diversification mitigates risk against cyclicality in any single travel vertical and encourages cross-sell strategies that boost contribution margins. Over the forecast window, experiences and ancillaries are expected to lift share within “Other Service Types,” leveraging hotel concierges equipped with in-destination activity platforms like Turneo.

The transportation segment’s primacy reflects Europe’s dense multimodal infrastructure, but vacation packages’ superior growth trajectory points to rising demand for convenience amid complex itineraries. Consumers increasingly value one-stop shopping that simplifies visa checks, seat assignments, and travel insurance, propelling conversion rates on OTA “packages tabs.” Airlines partner with rail operators through initiatives like Eurostar’s SkyTeam membership to extend network breadth without fleet expansion, thus supporting seamless ground-air itineraries. API-first property managers such as limehome expand across secondary cities, supplying inventory that feeds into dynamic packages and increasing geographic coverage for non-urban tourism. Technology vendors upgrade orchestration layers to assemble multi-sector bookings in real time, lowering package creation time from minutes to milliseconds. Consequently, platforms that master automated bundling gain a defensible moat as they cut complexity for both traveler and supplier. These shifts collectively reinforce the package category’s rapid expansion in the Europe online travel market.

By Booking Type: Direct Suppliers Lead but OTA Growth Accelerates

Direct travel suppliers held 54.02% of revenue in 2025, underscoring their success in steering customers toward proprietary channels with tailored rewards and exclusive fare classes. The Europe online travel market size for direct channels is projected to rise steadily but at a slower pace than OTA revenue, which will log the fastest 9.05% CAGR to 2031. Suppliers maintain the edge by integrating loyalty points, wallet credits, and personalized offers visible only within logged-in ecosystems. Airlines deepen NDC distribution, highlighting richer content such as bundled carbon offsets and ancillary seat packages unavailable through global distribution systems. Major hotel chains invest in mobile apps that serve as in-stay companions, further anchoring the direct relationship. Despite these tactics, OTAs leverage breadth of choice, price transparency, and multilanguage customer support to poach undecided travelers. Over time, the interplay between channel control and consumer convenience will dictate share shifts across the Europe online travel market.

Competition between channels catalyzes technological arms races as each side seeks differentiation. OTAs push deeper personalization through AI-driven recommendations that stitch together disparate inventory sources into coherent trips. Suppliers, in turn, harness first-party data to deliver contextual offers like seat upgrades at check-in nudges. Commission compression pressures OTAs to launch fintech-adjacent products such as “book now, pay later,” mitigating sticker shock and stalling direct defection. Corporates increasingly adopt direct-booking tools embedded with duty-of-care features, dragging managed travel away from legacy TMCs and into supplier ecosystems. Regulators scrutinize parity clauses, potentially leveling the playing field between direct and indirect options. The outcome will be a coexistence where suppliers dominate repeat, identity-attached travelers, while OTAs remain gateways for discovery and complex multi-provider itineraries across the Europe online travel market.

By Platform: Desktop Resilience Meets Mobile Momentum

Desktop retained 61.45% of bookings in 2025, reflecting the complexity of multi-component trips that drive travelers to larger screens for research and price comparison. Still, mobile channels are set to achieve a 13.12% CAGR, outpacing every other platform thanks to improving UX and digital wallet penetration. Younger cohorts born into smartphone ecosystems convert at higher rates on apps featuring biometric logins and one-tap payments. The Europe online travel market size derived from mobile will surpass desktop for last-minute and low-consideration purchases such as single-city hotel nights and intercity bus tickets within the forecast period. Desktop will remain relevant for lengthy itineraries where multiple tabs and advanced fare calendars aid decision making. However, cross-device journeys blur traditional boundaries as users begin research on a laptop and finish purchases on a phone after price alerts trigger push notifications.

App-first companies demonstrate how native mobile can outperform responsive web builds by embedding device features like GPS and push messaging into the booking flow. Flix SE leverages real-time location data to suggest the nearest bus stop, elevating user satisfaction. Meanwhile, established OTAs rebuild their web stacks into progressive web apps offering near-native performance on mobile browsers, closing the experience gap. As Apple Pay and Google Pay enrolments climb across Europe, payment friction further declines, benefitting impulse bookings. The rise of camera-enabled passport scanning and forthcoming digital identity wallets will eliminate form-fill friction, leading to higher funnel throughput on smartphones. Collectively, these advances ensure mobile’s share will steadily erode desktop dominance in the Europe online travel market.

Geography Analysis

The United Kingdom contributed 21.05% of revenue in 2025, reinforcing its status as the largest national slice of the Europe online travel market. British consumers embrace online booking across flights, rail, and short-term rentals, aided by widespread card-payment acceptance and a mature fintech landscape. UK-based suppliers capitalize on post-Brexit demand for mainland Europe leisure travel by bundling eSIMs and insurance into packages to offset passport-control uncertainty. Regulatory separation compels UK OTAs to manage duplicate compliance frameworks, raising operating costs but also fostering innovation in flexible ticketing and dynamic currency conversion. Domestic tourism rebounds as weak sterling makes staycations cost-competitive, leading to robust performance among cottage-rental platforms. Investment into sustainable rail infrastructure increases share of rail bookings to continental Europe, supporting Eurostar’s network expansion.

Spain, while smaller in absolute size, posts the fastest 11.58% CAGR to 2031 owing to record inbound tourism, rising household e-commerce adoption, and a strategic pivot toward digital nomads via new visa categories. The Europe online travel market size tied to Spanish travelers is set to grow as digital wallet usage tops 60% and broadband penetration deepen. Andalusia, Catalonia, and Madrid capture the bulk of spending, but secondary regions leverage EU recovery funds to digitalize tourism SMEs, widening geographic dispersion of online bookings. Robust collaboration between airports and low-cost carriers powers direct connectivity to tier-2 European cities, diversifying inbound profiles. Spanish OTA startups innovate with bilingual interfaces targeting Latin-American visitors, further reinforcing growth.

Germany and France round out the top tier, each contributing sizable, stable volumes driven by strong middle-class travel demand and advanced payment ecosystems. Germans display a cultural preference for rail and road transport, benefitting platforms that aggregate intermodal itineraries. France’s push for USD 108 billion (EUR 100 billion) in tourism receipts by 2030 stimulates hotel upgrade programs that rely heavily on digital distribution. Nordic and BENELUX markets provide early-adopter sandboxes for sustainable travel and identity wallet pilots, often exporting best practices continent-wide. Rest-of-Europe markets from Portugal to the Balkans offer green-field opportunities for specialized platforms that localize language, currency, and payment methods to capture first-time online bookers. Taken together, geographic variance underlines the need for flexible, localized strategies within the Europe online travel market.

Competitive Landscape

The Europe online travel market is moderately concentrated, with the top five players Booking Holdings, Expedia Group, Trip.com Group, Trivago, and Lastminute.com controlling a massive portion of overall revenue. This concentration still leaves considerable room for regional specialists and emerging platforms to gain traction. The market leader, Booking Holdings, maintains its position through Booking.com’s extensive hotel inventory and global reach. Expedia Group follows, leveraging a diverse brand ecosystem that includes vacation rentals via Vrbo. Despite the dominance of these key players, the market remains open to innovation and disruption, particularly from agile local operators and tech-enabled newcomers. Market leaders are investing in AI-powered personalization, loyalty subscriptions, and fintech add-ons to elevate customer lifetime value. Meanwhile, supplier-owned platforms like Ryanair.com and Hilton.com gain traction by funnelling exclusive content through loyalty ecosystems, demonstrating channel contestation in the Europe online travel market. Regulatory scrutiny under the Digital Markets Act forces gatekeepers to share data and cease self-preferencing, potentially redistributing traffic toward smaller entrants that excel in niche verticals such as wellness retreats or adventure travel. Intermodal aggregators, namely Trainline and Omio, expand across borders, capturing travelers seeking sustainable alternatives to short-haul flights.

Strategic partnerships and M&A shape competitive positioning. Air France-KLM’s planned 60.5% stake in SAS extends SkyTeam reach into Scandinavia, promising bundled air-rail itineraries once Eurostar’s SkyTeam partnership becomes operational. TUI Group’s equity swap with Bentour Reisen underscores a hybrid strategy: leveraging OTA reach while strengthening direct supplier relationships in the Nordics. Trip.com Group’s elevation of Skyscanner’s leadership aims to cross-pollinate metasearch capabilities with OTA full-stack services, intensifying competition for European traffic. Technology giants Amadeus and Sabre partner with Google Cloud and hotel groups to embed AI into core reservation systems, raising the table stakes for smaller technology vendors.

Barriers to entry hinge on data scale, brand trust, supplier relations, payment orchestration, and regulatory compliance. OTAs with global footprints possess marketing scale to navigate rising customer-acquisition costs, yet their need to show incremental value over supplier direct channels becomes more acute. Niche entrants position themselves on sustainability filters, flexible subscription travel passes, or localized payment methods that incumbents may overlook. Startups exploiting narrow but deep verticals such as luxury rail excursions or digital nomad housing often win through superior UX and curated inventory rather than pricing alone. Competitive intensity will spur further consolidation, especially among midsize OTAs pressured by margin squeeze from both supplier surcharges and regulatory compliance. Overall, flexibility, technological agility, and regulatory foresight will define winning playbooks across the Europe online travel market.

Europe Online Travel Industry Leaders

Booking Holdings Inc.

Expedia Group Inc.

Trip.com Group Ltd.

eDreams ODIGEO

lastminute.com Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: TUI Group acquired a 20% stake in Bentour Reisen while Bentour Reisen received a reciprocal 20% stake in Nazar Nordic AB, creating a strategic partnership that enhances TUI's Nordic market presence and demonstrates the company's expansion strategy through equity partnerships.

- May 2025: Amadeus IT Group announced a strategic partnership with Google Cloud to enhance its travel technology platform capabilities, focusing on AI-driven personalization and cloud infrastructure optimization to support growing demand for real-time travel booking services.

- April 2025: Omio expanded its Flex product across European markets, enabling travelers to make last-minute changes to train and bus bookings through mobile interfaces, addressing the growing demand for flexible travel options in post-pandemic booking behaviours.

- March 2025: Sabre Corporation announced a partnership with Ensana Hotels to enhance distribution capabilities across European wellness and spa destinations, demonstrating the growing importance of specialized travel segments in online distribution strategies.

Europe Online Travel Market Report Scope

Online travel is the type of travel that is booked online through a website or a mobile application that has a specialty in making the travel arrangements, such as flight tickets, car rentals, and packages. A complete background analysis of the market, including the analysis of market size and forecast, industry trends, growth drivers, and leading players, is provided in the report. Additionally, the report features qualitative and quantitative assessments by analyzing the data gathered from industry analysts and market participants across key stakeholders in the industry's value chain.

The market is segmented by service type, by booking type, by platform, and by country. By service type, the market is segmented into transportation, travel accommodations, vacation packages, and others. By booking type, the market is segmented into online travel agencies, direct travel suppliers. By platform, the market is segmented into desktop, mobile, and by country, the market is segmented into United Kingdom, Germany, France, Italy, and Rest of Europe. The report offers market size and forecast values for the European Online Travel Market in USD for the above segments.

By Service Type

| Transportation |

| Travel Accommodation |

| Vacation Packages |

| Other Service Types |

By Booking Type

| Online Travel Agencies |

| Direct Travel Suppliers |

By Platform

| Desktop |

| Mobile |

By Geography

| United Kingdom |

| Germany |

| France |

| Spain |

| Italy |

| BENELUX (Belgium, Netherlands, Luxembourg) |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) |

| Rest of Europe |

| By Service Type | Transportation |

| Travel Accommodation | |

| Vacation Packages | |

| Other Service Types | |

| By Booking Type | Online Travel Agencies |

| Direct Travel Suppliers | |

| By Platform | Desktop |

| Mobile | |

| By Geography | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | |

| Rest of Europe |

Key Questions Answered in the Report

How large is the Europe online travel market in 2026?

It is valued at USD 112.81 billion, with a forecast to hit USD 171.26 billion by 2031 at an 8.71% CAGR.

Which segment grows fastest by 2031?

Vacation packages lead growth, posting a 11.86% CAGR through 2031.

Why does mobile booking matter for European travel firms?

Mobile is forecast to grow 13.12% annually, propelled by digital wallets and app-centric loyalty features, steadily shifting share from desktop.

How will the EU Digital Identity Wallet influence bookings?

It will allow one-click ID verification, reduce checkout friction, and boost cross-border sales once launched in 2026.

What regulatory headwinds impact OTAs most?

The Digital Markets Act raises customer-acquisition costs and imposes data-sharing rules, pressing OTAs to diversify marketing and deepen loyalty programs.

Page last updated on: