Germany Sextech Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 2.67 Billion |

| Market Size (2026) | USD 3.14 Billion |

| Market Size (2031) | USD 7.15 Billion |

| Growth Rate (2026 - 2031) | 17.85% CAGR |

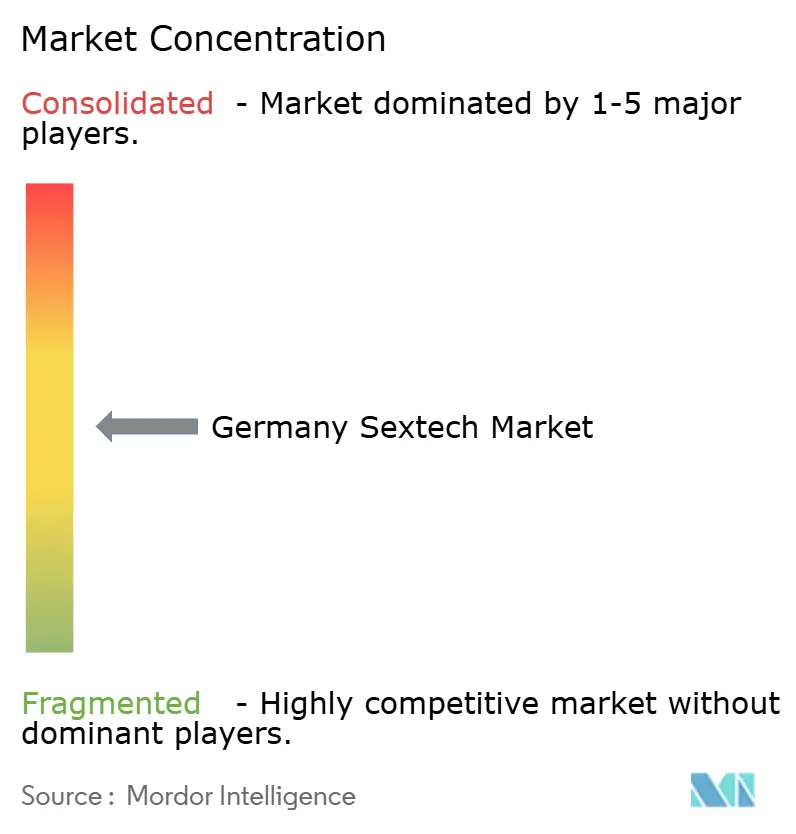

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Sextech Market Analysis by Mordor Intelligence

The Germany Sextech Market size is projected to be USD 2.67 billion in 2025, USD 3.14 billion in 2026, and reach USD 7.15 billion by 2031, growing at a CAGR of 17.85% from 2026 to 2031.

Germany's sextech market benefits from a public health framework that integrates sexual wellness into consumer health, enabling these products to enter mainstream retail and pharmacy channels. With nearly 18,000 pharmacies nationwide, these familiar health access points enhance product visibility, even in areas beyond major cities. The market is further supported by one of Europe’s strongest e-commerce ecosystems, catering to consumer preferences for privacy, discreet delivery, and a broad online product range. This combination of healthcare legitimacy, reliable retail infrastructure, and digital convenience allows local and international brands to compete in premium devices, wellness-focused products, and connected experiences. However, the market operates within a dual regulatory environment. While physical product retail enjoys relative stability, digital content and immersive platforms face stricter compliance requirements, shaping the competitive landscape.

Key Report Takeaways

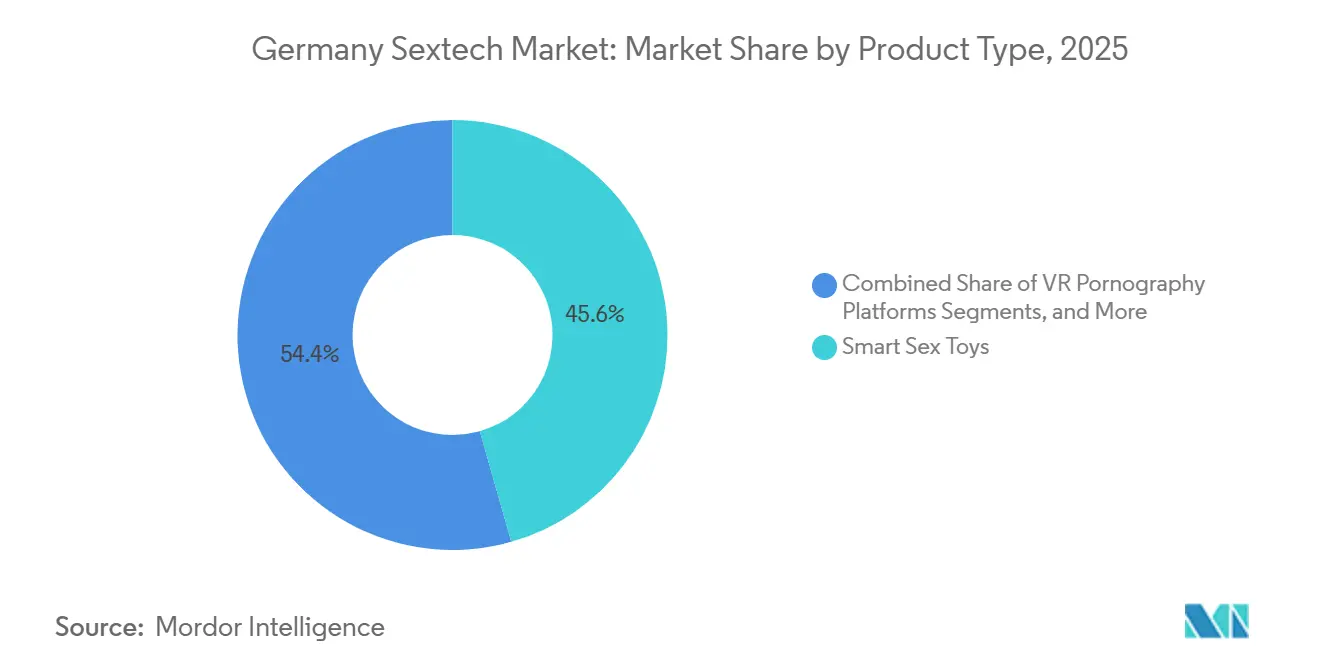

- By product type, smart sex toys held 45.63% share in 2025, while VR pornography platforms are projected to expand at a 18.98% CAGR from 2026 to 2031.

- By distribution channel, online retailers accounted for 40.41% share in 2025 and are also expected to be the fastest-growing channel, at a 19.20% CAGR through 2031.

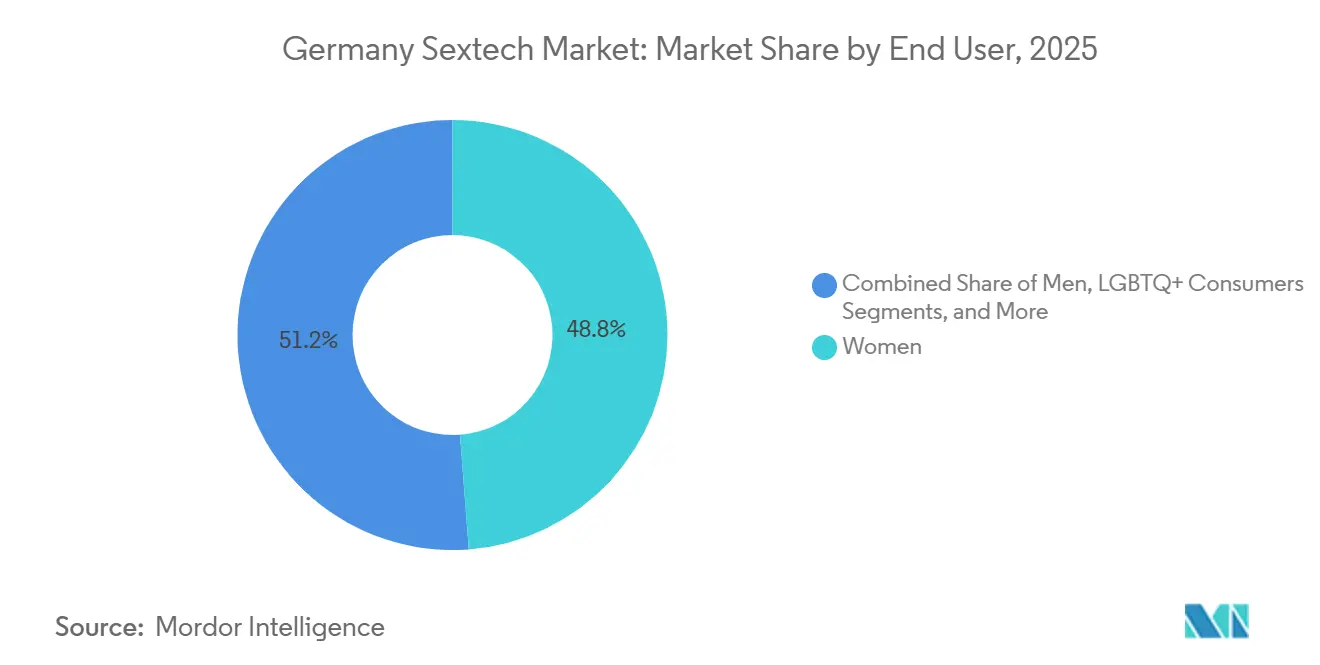

- By end user, women held 48.77% share in 2025, while LGBTQ+ consumers are projected to grow at a 19.67% CAGR from 2026 to 2031.

- By technology, bluetooth-enabled products held 35.88% share in 2025, while virtual reality and immersive content are forecasted to grow at an 20.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Germany Sextech Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Growing mainstream acceptance of sexual wellness as a public health category | +1.5% | National, concentrated in Berlin, Hamburg, Munich | Medium term (2-4 years) |

| Rising demand for discreet direct-to-consumer purchasing | +1.2% | National, strongest in suburban and rural areas | Short term (≤ 2 years) |

| Premiumization of body-safe, app-connected, and design-forward products | +0.9% | Urban centers, Berlin, Munich, Frankfurt | Medium term (2-4 years) |

| Expansion of inclusive sexual health and pleasure education | +0.7% | National, early gains in Berlin, Cologne, Hamburg | Long term (≥ 4 years) |

| Rising adoption among older adults and later-life consumers | +0.5% | National, above average in Baden-Württemberg, Bavaria | Long term (≥ 4 years) |

| Privacy-first payments and anonymous fulfillment improvements | +0.4% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Mainstream Acceptance of Sexual Wellness as a Public Health Category

In Germany, sexual wellness is increasingly recognized as a key component of routine health spending, moving beyond its niche perception. This shift positions sexual wellness products alongside mainstream items like contraceptives and personal care goods, reducing barriers for first-time buyers. Germany's pharmacy infrastructure supports this trend by serving as a trusted channel for health-related purchases, expanding the customer base beyond younger urban buyers. Domestic brands leverage this normalization to market premium devices as wellness products, diversifying the demographic base and reducing reliance on early adopters.

Rising Demand for Discreet Direct-to-Consumer Purchasing

Online purchasing continues to drive Germany's sextech market, with privacy, discreet shipping, and product comparison outweighing promotional discounts. In 2025, Germany's e-commerce sector showed resilience, with Q3 goods spending reaching EUR 17.96 billion, a 2.8% year-on-year increase. This growth highlights the importance of convenience and discretion, especially in areas with limited access to specialized stores. Compliance changes in December 2025 prompted platforms to enhance verification processes and checkout reliability, fostering customer trust and repeat purchases. Discreet direct-to-consumer retail remains a structural growth driver for the market.

Premiumization of Body-Safe, App-Connected, and Design-Forward Products

Premiumization drives Germany's sextech market as consumers prioritize body-safe materials, advanced design, and digital integration. By 2025, smart sex toys led the product mix with a 45.63% share, reflecting demand for connected products as part of a wellness experience. Satisfyer's Connect app, with over 4 million downloads and a 4.8-star rating, exemplifies the value of personalization and partner control. German brands focus on material safety and usability to maintain premium pricing. The 2024 acquisition of FUN FACTORY by EIS, Satisfyer, and Triple A group reinforced this trend, enhancing engineering expertise and product quality.

Expansion of Inclusive Sexual Health and Pleasure Education

Inclusive sexual health education is reshaping Germany's sextech market by broadening consumer entry points and brand communication. Growth is no longer limited to traditional male and female product categories, as brands adopt inclusive language and segmentation. This approach benefits LGBTQ+ consumers, couples, and first-time users, fostering comfort and awareness. Educational partnerships and inclusive messaging build lasting trust, giving established brands a competitive edge. This focus on education supports long-term market expansion as demographic expectations evolve over the forecast period.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Advertising and platform policy restrictions on adult content | -1.5% | National, acute in Bavaria and NRW | Short term (≤ 2 years) |

| Product classification ambiguity across consumer goods categories | -0.8% | National | Medium term (2-4 years) |

| Payment gateway friction and transaction blocking for adult commerce | -1.0% | National | Short term (≤ 2 years) |

| Consumer sensitivity to discretion, storage, and social visibility | -0.6% | National, acute in smaller cities and rural areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Advertising and Platform Policy Restrictions on Adult Content

Germany's sextech market faces significant advertising restrictions, particularly for digital-first operators relying on visibility and efficient customer acquisition. Challenges extend beyond social media moderation, as adult brands encounter barriers in search engines, programmatic advertising, and platform policies, limiting their reach on mainstream channels. Established players like ORION are adapting by investing in community-based acquisition strategies, such as the 2026 "Toy Party" format in Hamburg, to bypass restricted digital channels. These approaches, however, require substantial resources, favoring larger operators and slowing the growth of smaller competitors.

Payment Gateway Friction and Transaction Blocking for Adult Commerce

Payment-related issues present another major obstacle, as consumer trust and privacy are critical for completing sales. A December 2025 amendment to Germany's media regulations allows regulators to instruct banks and payment providers to block transactions with adult platforms lacking approved age verification systems. This creates operational risks for platforms combining physical product sales with digital content or subscriptions. While direct-to-consumer retailers of physical products are somewhat insulated, cautious financial partners and payment processors still pose challenges, particularly for segments relying on recurring digital monetization.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Smart Devices Anchor the Premium Tier

In 2025, Smart Sex Toys accounted for 45.63% of Germany's sextech market, highlighting their role in the premium segment's evolution. This category benefits from Germany's strong manufacturing base, where brands focus on engineering, safety, ergonomic design, and software integration over price competition. The 2024 acquisition of FUN FACTORY further strengthened the domestic market by adding design heritage and intellectual property, making smart devices a key area where brand equity and technical credibility converge.

Vibrators and Dildos continue to generate significant revenue due to their compatibility with mainstream retail formats and accessibility through pharmacies and health channels. Wearables, though smaller, are gaining attention for their discreet, wellness-oriented, and connected functionality. Remote-Controlled Devices are growing in relevance, particularly for long-distance use and couple-focused features. VR Pornography Platforms, projected to grow at an 18.98% CAGR from 2026 to 2031, represent the fastest-growing sub-category despite regulatory challenges. This product mix shows that while tangible device sales dominate today, future growth will rely on integrating devices with software and content ecosystems.

By Distribution Channel: Digital Commerce Leads, Physical Retail Holds Experiential Ground

Online Retailers held a 40.41% share of Germany's sextech market in 2025 and are projected to grow at a 19.20% CAGR through 2031. Consumers prefer online channels for privacy, discreet delivery, and a wider product range, supported by Germany's robust e-commerce environment. This channel's growth reflects its ability to meet consumer demand for convenience and reduced social visibility during purchases.

Specialist Adult Stores remain relevant by offering personalized guidance and product education, with ORION's physical network ensuring visibility across Germany. Drugstores and pharmacies play a strategic role in normalizing products and integrating them into routine shopping. This channel mix highlights a shift from competition to complementarity, where online retail drives scale and physical formats enhance trust and conversion quality.

By End User: Women Remain the Revenue Base While LGBTQ+ Demand Expands Faster

Women represented 48.77% of the market share in 2025, maintaining their position as the largest end-user group in Germany's sextech market. This reflects years of product development focused on female pleasure and intimate wellness. While older female consumers remain underserved, this presents an opportunity for brands to address later-life use cases and expand the market further.

The LGBTQ+ segment is projected to grow at a 19.67% CAGR from 2026 to 2031, making it the fastest-expanding end-user group. This growth reflects a shift toward inclusivity and broader product relevance. Men remain a key segment, particularly in categories like masturbation devices and performance-focused products, while couples drive demand for partner-controlled devices and teledildonics. The market is evolving toward a balanced demand structure shaped by inclusivity and diverse consumer identities.

By Technology: Connectivity Leads Today While Immersive Formats Set the Future Pace

Bluetooth-Enabled Products held 35.88% of Germany's sextech market in 2025, establishing wireless connectivity as a standard feature. This technology supports app-linked features, partner control, and gradual upgrades, enabling consumers to transition to richer ecosystems without changing usage patterns. Bluetooth remains the foundation of connected intimacy products in Germany's sextech market.

Virtual Reality and Immersive Content are projected to grow at a 20.55% CAGR from 2026 to 2031, making them the fastest-growing technology segment. While immersive formats face compliance risks, they cater to the growing demand for enhanced experiences. App-Controlled Products balance personalization and ease of use, aligning with consumer privacy concerns. Teledildonics and remote-control interfaces, though niche, are gaining traction, with innovations like Kiiroo's March 2025 VR compatibility upgrade enhancing cross-device interoperability.

Geography Analysis

Germany's sextech market sees its largest urban centers, particularly Berlin, driving the adoption of premium devices, app-connected services, and VR technologies. Berlin serves as a key hub due to its strong brand presence, active product development, and openness to wellness-focused, tech-enabled sexual health. The city provides access to startup talent, skilled digital teams, and early adopters, making it central to testing and scaling product concepts. Other cities like Hamburg, Munich, and Cologne also contribute significantly, supported by high purchasing power, retail density, and digital convenience.

North Rhine-Westphalia is the largest regional revenue contributor in the Germany sextech market, driven by its consumer scale. However, its strict enforcement against foreign adult content platforms creates challenges for streaming and VR operators, while physical product sellers face fewer hurdles. Bavaria presents a similar dynamic, combining strong purchasing power with conservative regulations on adult content. This results in a more fragmented risk profile for content and platform operators compared to physical wellness product retailers. Overall, the market is more unified for device sales than for immersive and content-driven models.

Hamburg and Frankfurt play distinct roles in the Germany sextech market. Hamburg is a hub for logistics, e-commerce fulfillment, and retail experimentation, which influenced ORION's decision to launch its Toy Party concept there in 2026. Frankfurt's importance lies in its banking and payment infrastructure, which is increasingly critical as compliance and payment enforcement gain prominence in adult commerce. Smaller cities and rural areas remain underpenetrated markets for premium devices and connected formats. Brands focusing on discreet packaging, reliable delivery, and consumer education are better positioned to close this geographic gap during the forecast period.

Competitive Landscape

Germany's sextech market exhibits a dual structure, with moderate concentration in premium devices and fragmentation in the mid-market and digital content segments. Domestic players dominate by leveraging local retail strength, recognized brands, engineering expertise, and direct-to-consumer channels. EIS, Satisfyer, and Triple A group exemplify this synergy, combining e-commerce, connected-device innovation, and manufacturing capabilities, strengthened by the FUN FACTORY acquisition. Satisfyer’s app ecosystem further enhances customer engagement, extending beyond single-device purchases.

Lovehoney, through WOW Tech and its brands Womanizer and We-Vibe, remains a strong competitor in luxury and couples’ devices, keeping the premium segment competitive internationally. ORION plays a dual role as a retailer and wholesale distributor, offering 10,000 SKUs to customers in 57 countries. This makes ORION a key partner for international brands like LELO, Doc Johnson, Pipedream, and California Exotic Novelties, which rely on Germany’s established wholesale and retail infrastructure. Despite local dominance in premium connected devices, the market remains open to global players.

Strategic developments highlight shifting competition. The FUN FACTORY acquisition reflects consolidation around engineering and brand heritage, while ORION’s 2026 Toy Party initiative adapts to advertising restrictions with event-driven customer engagement. Kiiroo’s March 2025 interoperability upgrade emphasizes value through compatibility with immersive and remote-use environments. However, a significant gap persists in addressing the needs of consumers aged 55 and above, whose spending power and preferences remain underrepresented in current market strategies.

Germany Sextech Industry Leaders

WOW Tech Group

FUN FACTORY GmbH

EIS GmbH

Amorelie GmbH

Kessel Medintim GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Berlin's Heeresbäckerei venue reported to host the SX Festival & Expo from June 26–28, 2026, bringing together industry professionals, technology innovators, and kink communities to explore advancements in AI-driven intimacy, sexual wellness, and modern pleasure technology.

- May 2025: ORION Versand deployed the Slim4 AI-driven platform for demand forecasting and inventory automation, optimizing operations across a diverse 10,000-SKU product catalog. This initiative addressed personnel bottlenecks in purchasing workflows and strengthened ORION's parallel B2C e-commerce and global wholesale operations from its Biebertal and Flensburg facilities.

- March 2025: Kiiroo introduced upgraded interactive teledildonics hardware with enhanced compatibility for VR platforms and improved cross-device synchronization. This development reinforces Kiiroo's position in Germany’s growing VR-connected product market and expands its integration with VR content platforms marketed in Germany.

Germany Sextech Market Report Scope

As per the scope of the report, sextech (or sex-tech) refers to technology and software designed to innovate, enhance, and assist in human sexuality, intimate health, and relationships. It encompasses a broad spectrum of products, ranging from connected pleasure devices to sexual education platforms and fertility trackers.

The Germany Sextech Market is segmented by product type, distribution channel, end-user, and technology. By product type, the market includes vibrators, dildos, smart sex toys, wearables, VR pornography platforms, remote-controlled devices, and other sextech products. By distribution channel, the market is segmented into online retailers, specialist adult stores, drugstores and pharmacies, mass merchandisers, and others. By end-user, the market is categorized into men, women, LGBTQ+ consumers, and couples. By technology, the market is segmented into non-connected products, Bluetooth-enabled products, app-controlled products, virtual reality and immersive content, and teledildonics and remote-control interfaces. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Vibrators |

| Dildos |

| Smart Sex Toys |

| Wearables |

| VR Pornography Platforms |

| Remote-controlled Devices |

| Other Sextech Products |

| Online Retailers |

| Specialist Adult Stores |

| Drugstores and Pharmacies |

| Mass Merchandisers |

| Others |

| Men |

| Women |

| LGBTQ+ Consumers |

| Couples |

| Non-Connected Products |

| Bluetooth-Enabled Products |

| App-Controlled Products |

| Virtual Reality and Immersive Content |

| Teledildonics and Remote-Control Interfaces |

| By Product Type | Vibrators |

| Dildos | |

| Smart Sex Toys | |

| Wearables | |

| VR Pornography Platforms | |

| Remote-controlled Devices | |

| Other Sextech Products | |

| By Distribution Channel | Online Retailers |

| Specialist Adult Stores | |

| Drugstores and Pharmacies | |

| Mass Merchandisers | |

| Others | |

| By End User | Men |

| Women | |

| LGBTQ+ Consumers | |

| Couples | |

| By Technology | Non-Connected Products |

| Bluetooth-Enabled Products | |

| App-Controlled Products | |

| Virtual Reality and Immersive Content | |

| Teledildonics and Remote-Control Interfaces |

Key Questions Answered in the Report

How large is Germany's sextech space in 2026 and where is it heading by 2031?

It is valued at USD 3.14 billion in 2026 and is projected to reach USD 7.15 billion by 2031, growing at a 17.85% CAGR during the forecast period.

Which product category leads demand in Germany?

Smart Sex Toys lead the product mix with 45.63% share in 2025, supported by Germany's strong domestic manufacturing base, premium product design, and connected app ecosystems.

What is the fastest-growing technology area in Germany?

Virtual Reality and Immersive Content is the fastest-growing technology segment, with an 20.55% CAGR projected from 2026 to 2031.

Why are online retailers so important in Germany?

Online Retailers held 40.41% share in 2025 and are projected to grow at a 19.20% CAGR, largely because German consumers value privacy, discreet delivery, and broad online assortment.

Which consumer group is expanding fastest?

LGBTQ+ Consumers are the fastest-growing end-user group, with a projected 19.67% CAGR from 2026 to 2031, reflecting rising demand for more inclusive products and brand communication.

What is the biggest near-term challenge for companies operating in Germany?

Regulatory and payment compliance is the main near-term challenge, especially for platforms linked to digital content, streaming, and VR, where age verification and payment blocking risks are more significant than for physical product sellers.

Page last updated on: