Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

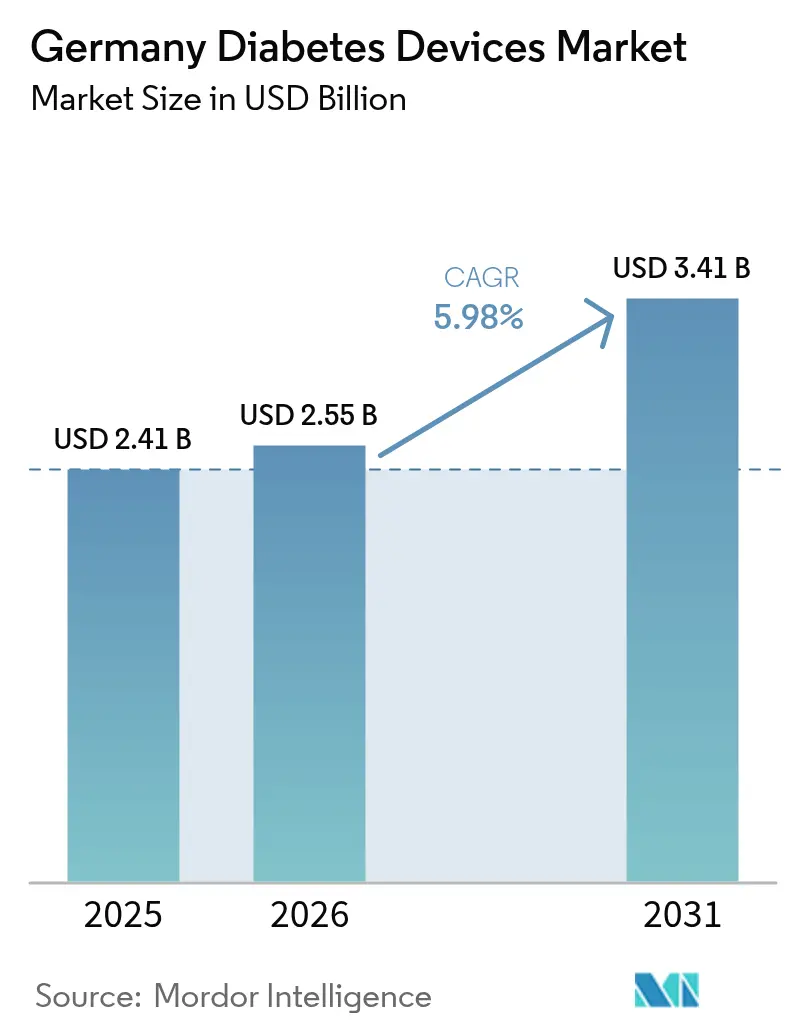

| Base Year Market Size (2025) | USD 2.41 Billion |

| Market Size (2026) | USD 2.55 Billion |

| Market Size (2031) | USD 3.41 Billion |

| Growth Rate (2026 - 2031) | 5.98% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Diabetes Devices Market Analysis by Mordor Intelligence

The Germany diabetes devices market size is expected to grow from USD 2.41 billion in 2025 to USD 2.55 billion in 2026 and is forecast to reach USD 3.41 billion by 2031 at 5.98% CAGR over 2026-2031. Growth is underpinned by statutory health insurance reimbursement for flash and real-time continuous glucose monitoring, wider coverage for hybrid closed-loop pumps, and sustained public funding for AI-enabled insulin titration. A rapidly ageing, insulin-intensive population, coupled with the Digital Healthcare Act’s fast-track pathway for reimbursable health apps, is steering demand toward connected, home-based solutions. Manufacturers are concentrating on integrated ecosystems that pair sensors, pumps and cloud software, a strategy that helps defend margins while test-strip prices fall under tendering pressure. The Baden-Württemberg med-tech cluster adds resilience by localising R&D and production, reducing exposure to global supply-chain shocks.

Key Report Takeaways

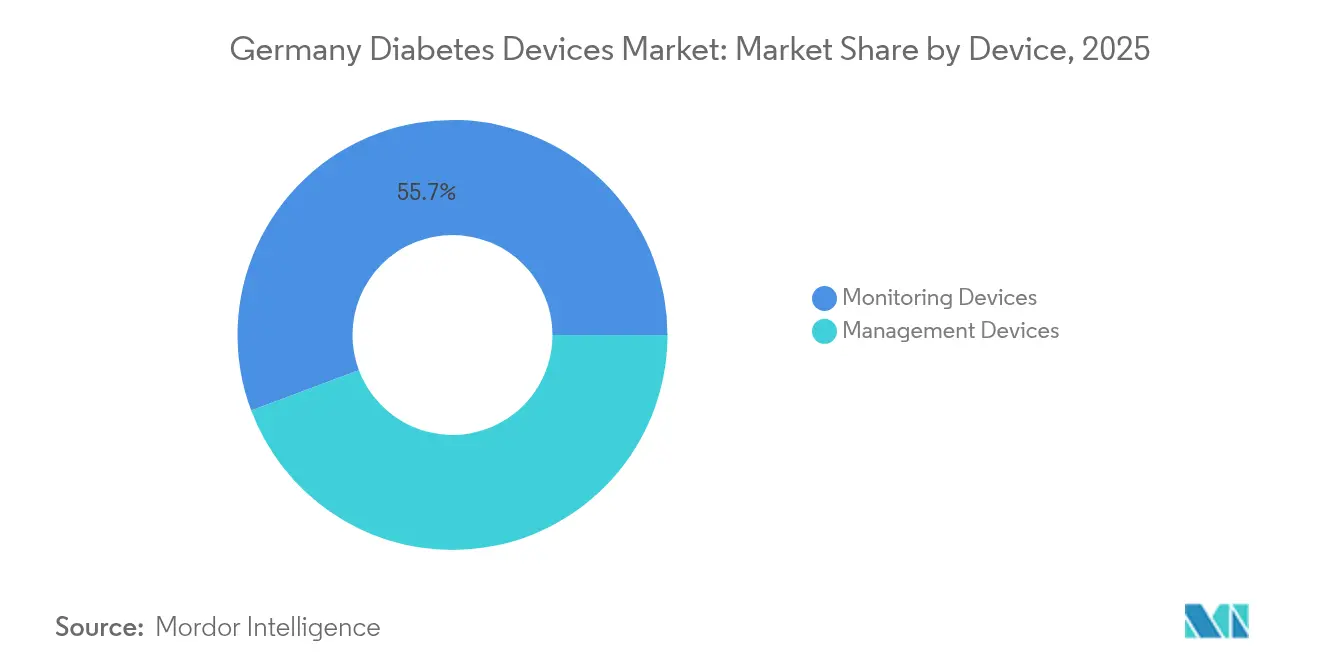

- By device type, Monitoring Devices led with 55.72% revenue share in 2025, while continuous glucose monitoring is projected to expand at a 7.41% CAGR through 2031.

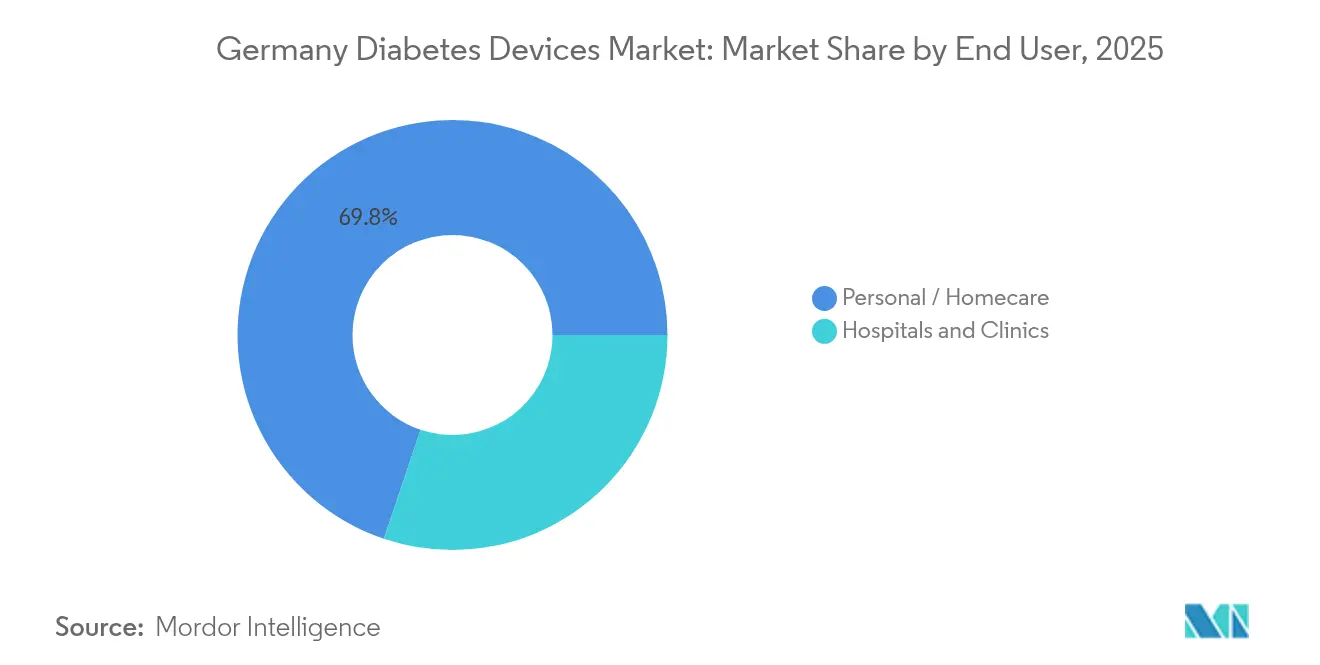

- By end user, the Personal/Homecare segment held 69.83% of the Germany diabetes devices market share in 2025 and is advancing at a 6.39% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Germany Diabetes Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| National Diabetes Strategy-driven SHI Reimbursement for Flash-CGM | +1.5% | National | Medium term (2-4 years) |

| Hybrid Closed-Loop Pump Reimbursement Accelerating Adoption | +1.2% | National | Medium term (2-4 years) |

| Ageing, High-Insulin-Utilisation Population Base in Germany | +0.9% | National, with higher impact in regions with older demographics | Long term (≥ 4 years) |

| Digital-Health-App (DiGA) Law Boosting Connected Home Monitoring | +0.7% | National | Short term (≤ 2 years) |

| Baden-Württemberg Med-Tech Cluster Securing Local Supply | +0.6% | Regional, with national impact | Medium term (2-4 years) |

| Bund-funded AI Projects for Automated Insulin Titration | +0.4% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

National Diabetes Strategy-driven SHI Reimbursement for Flash-CGM

Expanded reimbursement now covers type 2 patients needing ≥ 3 insulin injections daily, insulin-treated gestational diabetes, and all minors under 18. Usage among adults with type 1 diabetes jumped from 31.1% in 2017 to 75.4% in 2021/2022 [1]Yong Du, “Use of Glucose Monitoring Devices Among Adults With Diabetes in Germany,” Diabetes Technology & Therapeutics, liebertpub.com. The policy emphasises access rather than price reduction, enabling firms to sustain R&D while broadening reach. Higher penetration lifts demand for sensors, transmitters and data platforms, reinforcing the Germany diabetes devices market’s technology-led expansion.

Hybrid Closed-Loop Pump Reimbursement Accelerating Adoption

Statutory coverage for automated insulin delivery creates a clear upgrade path from multiple daily injections. Ypsomed’s mylife Loop drove 80.8% sales growth in 2024/25 in Germany [2]Ypsomed AG, “Ypsomed Sells Its Diabetes Business and Grows by Over 35%,” ypsomed.com. Clinical studies record a 76% drop in severe hypoglycaemia for users with impaired awareness [3]Roman Hovorka, “Closed-Loop Insulin Delivery: Update on the State of the Field,” tandfonline.com. Competition is intensifying as incumbents and newcomers race to refine algorithms, extend sensor wear time and simplify onboarding, adding depth to the Germany diabetes devices market.

Ageing, High-Insulin-Utilisation Population Base

About 7 million Germans live with diabetes, with projections of 10.7–12.3 million by 2040 [4]Diabinfo, “How Many People Have Diabetes?,” diabinfo.de. Older adults often struggle with dexterity and vision, prompting demand for devices featuring larger displays and ergonomic designs. This demographic shift anchors long-run volume growth for pumps, pen injectors and connected monitors, strengthening the Germany diabetes devices market across all channels.

Digital-Health-App (DiGA) Law Boosting Connected Home Monitoring

Germany’s Digital Healthcare Act enables prescription-based reimbursement of certified apps within a 12-month fast track. Fifty-six apps now qualify, giving 73 million insured citizens access to guided monitoring, dose calculators and coaching tools. Seamless data flow from sensors to cloud platforms underpins proactive care, reduces clinic visits and raises stickiness for device vendors within the Germany diabetes devices market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| MDR Recertification Backlog Slowing New Device Launches | -0.8% | National, with EU-wide implications | Short term (≤ 2 years) |

| SHI Tendering Driving Test-Strip Price Compression | -0.5% | National | Medium term (2-4 years) |

| GDPR-linked Cloud-Data Privacy Concerns | -0.3% | National, with EU-wide implications | Medium term (2-4 years) |

| Shortage of Diabetes Educators for Advanced Pump Training | -0.4% | National, with regional variations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

MDR Recertification Backlog Slowing New Device Launches

Fewer than 10% of legacy devices have transitioned to the new EU regulation, and 83% of companies have postponed certification for new products. Lengthy audits restrict pipeline flow, dulling innovation momentum in the Germany diabetes devices market until notified-body capacity expands.

SHI Tendering Driving Test-Strip Price Compression

Aggressive reference pricing shrinks margins on blood-glucose strips. As manufacturers redirect capital toward sensor-based monitoring, the self-monitoring blood glucose segment commoditises. The shift accelerates CGM uptake, but revenue erosion in consumables trims overall growth for the Germany diabetes devices market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device: CGM Paces Monitoring Segment Growth

Monitoring Devices captured 55.72% of device revenues in 2025 and is rising at a 7.41% CAGR, faster than the Germany diabetes devices market size overall. Expanded reimbursement for flash systems and paediatric coverage sustains volume gains, while platforms such as Abbott’s forthcoming continuous ketone sensor hint at adjacent profit pools (lovemylibre.com). Self-monitoring blood glucose remains an entry point for newly diagnosed patients but endures compressing prices under SHI tenders. The Germany diabetes devices market share for management devices sits at 44.28%; hybrid closed-loop pumps are lifting this portion through double-digit unit growth.

Predictive insights increasingly inform therapy: time-in-range metrics correlate with lower retinopathy and cardiovascular risks. Sales of the mylife YpsoPump exemplify convergence of monitors and pumps into near-autonomous loops. As sensor accuracy, algorithm sophistication and smartphone integration improve, the Germany diabetes devices market is migrating from episodic testing toward continuous, closed-loop control.

By End User: Home-Care Dominance Reflects Policy Success

Personal/Homecare users accounted for 69.83% of the Germany diabetes devices market in 2025 and will grow at 6.39% CAGR to 2031. DiGA-enabled apps and remote pump starts prove clinical equivalence to in-office training. Smartphones now serve as hubs for sensor data, bolstering adherence and reducing hospital visits. Hospitals & Clinics, with 30.17% share, focus on complex cases and technology initiation, mandating electronic quality measures for in-patient glycaemic control.

Cross-setting collaboration tightens the care continuum: clinics launch structured pump education such as GoPump, then hand patients to community providers. This division of labour reinforces volume in home channels while ensuring safe scale-up of advanced tools, sustaining the Germany diabetes devices market size across user groups.

Geography Analysis

Southern Germany, led by Baden-Württemberg, functions as an innovation engine. Headquarters and production sites of Roche Diagnostics and a dense network of academic partners incubate sensor chemistry, low-power electronics and AI algorithms. The cluster employs about 20,000 med-tech specialists and supports a resilient domestic supply chain, buffering the Germany diabetes devices market against external volatility.

Northern federal states leverage strong digital infrastructure to scale connected care. Ypsomed’s investment in Schwerin broadens capacity for autoinjectors and pens, anchoring export-oriented growth while distributing jobs beyond the traditional south-west base. Policymakers in Hamburg and Schleswig-Holstein run telemedicine pilots that bundle DiGA apps with CGM, increasing penetration especially among working-age users.

Eastern regions, facing faster population ageing, drive demand for geriatric-friendly devices. Uptake of large-display pumps and vibration-alert sensors is higher where prevalence of visual impairment complicates self-care. Uniform SHI benefits ensure national reimbursement consistency, yet disparities in specialist educator availability persist; rural Saxony reports longer wait times for advanced pump training than urban Berlin. Continued federal grants for digital clinics are expected to level service gaps, reinforcing the Germany diabetes devices market across Länder.

Regulatory Landscape

Germany diabetes devices are governed by the EU Medical Device Regulation (MDR, Regulation (EU) 2017/745), requiring CE marking and ongoing post-market surveillance to place products on the German market. In Germany, BfArM is a central authority here, covering medical-device vigilance and administering the DiGA fast-track pathway under the Digital Health Applications Ordinance (DiGAV) for reimbursable digital medical devices, including diabetes-relevant applications.

Manufacturers also face an operational shift toward EUDAMED. As of May 28, 2026, EUDAMED use is mandatory for registration of new medical devices in the EU, with Germany transitioning away from reliance on the national DMIDS route for new notifications. This raises the bar on compliance and data submission readiness (UDI and device master data) as a gating item for launches and line extensions, alongside continued evidence requirements to secure and defend statutory health insurance reimbursement for connected diabetes ecosystems (CGM, pumps, and associated software).

Value Chain Analysis

The value chain runs from sensor and electronics inputs, through device design and manufacturing (often supported by German med-tech clusters such as Baden-Wuerttemberg for R&D and high-value components), to conformity assessment and CE marking under MDR. Market access in Germany then depends on reimbursement pathways, tendering, and channel build-out. For diabetes devices, connected-care software adds a parallel value-chain layer, where DiGA listing managed by BfArM under DiGAV operates as a formal market-access step for eligible digital medical devices that complement monitoring and insulin-delivery hardware.

Commercial distribution in Germany is carried out through a mix of direct sales by local subsidiaries and specialized medtech distributors, along with wholesale and homecare-focused providers for ongoing consumables and patient support. Hospital purchasing dynamics often incorporate tendering and purchasing networks, which can drive price pressure in commoditized categories (for example, strips), while logistics and compliance service partners (including 3PL and importer-of-record providers) support EU importation, warehousing, and documentation to maintain continuity of supply for high-velocity sensors and pump consumables.

Competitive Landscape

Market concentration is moderate, with Abbott, Roche, Dexcom and Medtronic dominating sensors, while Novo Nordisk, Eli Lilly and Sanofi command pen and vial insulin channels. Strategic alliances are redrawing boundaries: Abbott and Medtronic will co-develop a dual-branded sensor-pump combinatio. Roche’s 2024 debut of a CGM challenges the historical duopoly and signals escalating R&D bets.

Start-ups target white spaces: Diafyt MedTech applies machine-learning to automated titration, winning Bund grants and fast-track Class IIb approval zefyron.com. Senseonics’ implantable sensor gains traction among patients wanting quarterly insertions instead of fortnightly replacements, although surgical workflow limits volume. Incumbents counter with sensor-wear-time extensions and app personalisation features such as Medtronic’s My Insights, which emails behavioural nudges to MiniMed users.

Regulation shapes rivalry. Firms that clear MDR audits early secure uninterrupted sales and marketing bandwidth; laggards risk stock-outs and lost tenders. IQWiG’s health economic dossiers influence reimbursement ceilings, nudging suppliers to link device data to measurable outcome gains. As digital ecosystems mature, lock-in hinges on cloud interoperability and clinician workflow integration, deepening competitive moats within the Germany diabetes devices market.

Germany Diabetes Devices Industry Leaders

Abbott Diabetes Care

Roche Diabetes Care

DexCom Inc.

Medtronic PLC

Insulet Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

CGM expansion into broader type 2 diabetes use cases is widening the addressable segment beyond intensive insulin therapy. Product design and positioning increasingly target basal-insulin and non-intensive regimens, and this shows up in go-to-market choices. A clear anchor is Dexcoms May 2026 announcement of Dexcom Flex for Germany, aimed at adults with type 2 diabetes on basal insulin, oral therapies, or GLP-1 receptor agonists, which intensifies competition around simplified onboarding, affordability levers, and homecare channel execution.

Innovation whitespace is also building at the overlap of new biosensing modalities and automated insulin delivery (AID) ecosystems. Abbott secured CE Mark in May 2026 for Libre Duo and Libre Duo 10 Day (dual glucose-ketone sensing), while June 2026 CE marking for FiberSense AGs reusable CGM (Class IIb) indicates scope for differentiated form factors and reusability concepts under MDR. On the management side, July 2026 saw Diabeloop launch DBLG2 AID in Germany with ViCentra Kaleido and Dexcom G7 integration, running the algorithm via an Android smartphone as the control interface, reinforcing ecosystem competition around interoperability, patient experience, and software-driven therapy differentiation within Germanys reimbursement-led market structure.

Recent Industry Developments

- July 2026: Diabeloop launched the DBLG2 automated insulin delivery system in Germany, integrating the ViCentra Kaleido patch pump with Dexcom G7 CGM and running the algorithm on a compatible Android smartphone. This adds another commercially available AID ecosystem option and raises the importance of smartphone-centric workflows, partner compatibility, and training support for scaling advanced pump therapy.

- May 2026: Dexcom announced Dexcom Flex in Germany, a CGM system designed for adults with type 2 diabetes who do not use intensive insulin therapy, including users on basal insulin, oral therapies, or GLP-1 receptor agonists. The launch broadens the competitive battleground from insulin-intensive populations to higher-volume type 2 cohorts, pushing suppliers to optimize cost-to-serve and consumer-style onboarding in the home channel.

- August 2024: Dexcom Deutschland enabled the Direct-to-Watch feature for Dexcom G7 in Germany, allowing CGM readings to be viewed on Apple Watch without a nearby smartphone. This strengthens wearable-centric adherence and positions smartwatch connectivity as a differentiator for CGM brands competing on convenience and engagement features.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this report, the Germany diabetes devices market is defined as the value of diabetes monitoring and insulin administration devices sold in Germany, including the main device hardware and routine consumables used by patients and care settings.

Scope exclusions: We exclude devices used only for laboratory diagnostics and devices used only for gestational diabetes screening.

Segmentation Overview

- By Device

- Monitoring Devices

- Self-Monitoring Blood Glucose

- Glucometers

- Blood-Glucose Test Strips

- Lancets

- Continuous Glucose Monitoring

- Sensors

- Durables/Transmitters

- By CGM Type

- Self-Monitoring Blood Glucose

- Management Devices

- Insulin Pumps

- Tethered Pumps

- Patch Pumps

- Insulin Pens

- Disposable Pens

- Re-usable Pens & Cartridges

- Insulin Syringes

- Jet Injectors

- Insulin Pumps

- Monitoring Devices

- By End User

- Hospitals & Clinics

- Personal / Homecare

Data Sources, Market Sizing, and Validation

Desk Research

Desk research started with public health and reimbursement signals that shape diabetes device uptake in Germany, then we checked the size and direction of the treated population and the testing intensity reported for diabetes care. We referenced sources such as the Robert Koch Institute (RKI), the Federal Statistical Office of Germany (Destatis), the Federal Joint Committee (G-BA), the German Federal Institute for Drugs and Medical Devices (BfArM), and OECD health statistics to build consistent inputs.

To translate these signals into a market model, we also used company annual reports and investor presentations for product mix context, and we cross-checked policy timing and adoption milestones using association websites and reputable press. Where public disclosures were not detailed enough, paid subscriptions supporting company financials and news screening, patent intelligence, and selective import and export shipment views were used to support directionality checks. The desk sources listed here are illustrative, and many other public and paid references were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to pressure-test utilization and pricing logic, especially for CGM, pump therapy, and insulin pen intensification where reimbursement rules and patient adherence can shift assumptions quickly. We spoke with clinicians, diabetes educators, and stakeholders across distributor, pharmacy, and homecare channels, including device-focused managers. Their input helped fill gaps from desk research and allowed key assumptions to be cross-checked across Germany.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 15% | |

| Mid tier: 45% | Functional/Unit leaders: 38% | |

| Smaller Players: 20% | Managers: 47% |

Market-Sizing & Forecasting

The sizing logic was built using a top-down approach where diabetes prevalence and treated cohorts are converted into device demand through monitoring frequency, therapy mix, and reimbursement-driven adoption, then valued using typical price points for devices and consumables. We corroborated the totals with selective bottom-up approximations, such as sampled average selling price times estimated unit volumes for key categories, and we ran channel checks on mix shifts between SMBG and CGM.

A few inputs were treated as the main market fingerprints because they move the total in a visible and repeatable way, including CGM penetration in insulin-treated and non-insulin cohorts, sensor replacement cycles, strip consumption per patient for SMBG, pump user base growth and infusion set change frequency, and the split between reusable hardware and recurring consumables. When a device subcategory had limited visibility, we used bounded ranges from interviews and reconciled them against Germany-level diabetes population signals before selecting a final midpoint.

For forecasting, we used scenario analysis and then blended into a base case, since reimbursement expansion and technology switching can create step-changes rather than smooth lines. Assumptions for adoption rates, price progression, and consumable intensity were refreshed with primary inputs, and the resulting trajectory was checked against observed policy timing and care pathway changes.

Data Validation & Update Cycle

Validation was handled through triangulation across independent signals, where utilization, patient pool, and price logic had to point in the same direction before results were finalized. Outliers were flagged when growth implied unrealistic jumps in device users or consumable intensity, then we rechecked the underlying drivers, followed by a second analyst review before sign-off.

The report is refreshed annually, and interim updates are made when material events occur, such as reimbursement changes, major guideline shifts, or product transitions that alter the mix between SMBG, CGM, pens, and pumps. Before delivery, a fresh update pass is completed so clients receive an up-to-date view aligned to the latest available public data and field feedback.

Mordor Intelligence's Germany Diabetes Devices Market Size Measured Against Other Published Estimates

Published market sizes for Germany diabetes devices can vary even when the topic label looks the same, since the counted products, the year used as the starting point, and the pricing logic are often not aligned. Differences also show up when some studies mix in adjacent healthcare items, or when they value only device hardware and not the recurring consumables that typically drive the larger share.

By tracking key demand drivers and refresh points, Mordor Intelligence keeps the estimate tied to Germany-only device and consumables revenue for diabetes monitoring and insulin administration, with lab-only diagnostics and gestational screening devices left out, which changes totals when broader definitions are used elsewhere.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.41 B (2025) | |

| Industry Platform A | USD 2.27 B (2024) | Uses an earlier base year and does not clearly state whether recurring consumables and all channels are valued consistently, which can pull the market value down even if the device list is similar. |

| Publisher B | USD 1.71 B (2023) | Anchored to a different year and appears to apply a narrower device boundary and pricing build, which can undercount ongoing sensor and strip revenue when conversion to value is simplified. |

The comparison shows that year selection and what gets counted as device revenue usually explain most of the spread. When scope is kept tight to diabetes monitoring and insulin administration devices sold in Germany, and pricing is tied back to consumable replacement behavior, the final number becomes easier to reproduce and defend in planning discussions.

Key Questions Answered in the Report

How big is the Germany Diabetes Care Devices Market?

The Germany Diabetes Care Devices Market size is expected to reach USD 2.55 billion in 2026 and grow at a CAGR of 5.98% to reach USD 3.41 billion by 2031.

What technologies are likely to shape the next wave of growth?

Hybrid closed-loop pumps, AI-driven insulin titration apps, and integrated sensor-pump platforms are expected to deepen the shift toward automated, connected diabetes management through 2030.

Who are the key players in Germany Diabetes Devices Market?

Abbott Diabetes Care, Roche Diabetes Care, DexCom Inc., Medtronic PLC and Insulet Corporation are the major companies operating in the Germany Diabetes Devices Market.

Which product type is expanding the fastest?

Continuous glucose monitoring systems lead growth with a 7.41% CAGR, driven by broadened statutory insurance reimbursement and strong patient demand for sensor-based tracking.

Page last updated on: