Sex Dolls Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 0.61 Billion |

| Market Size (2031) | USD 1.02 Billion |

| Growth Rate (2026 - 2031) | 10.78% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sex Dolls Market Analysis by Mordor Intelligence

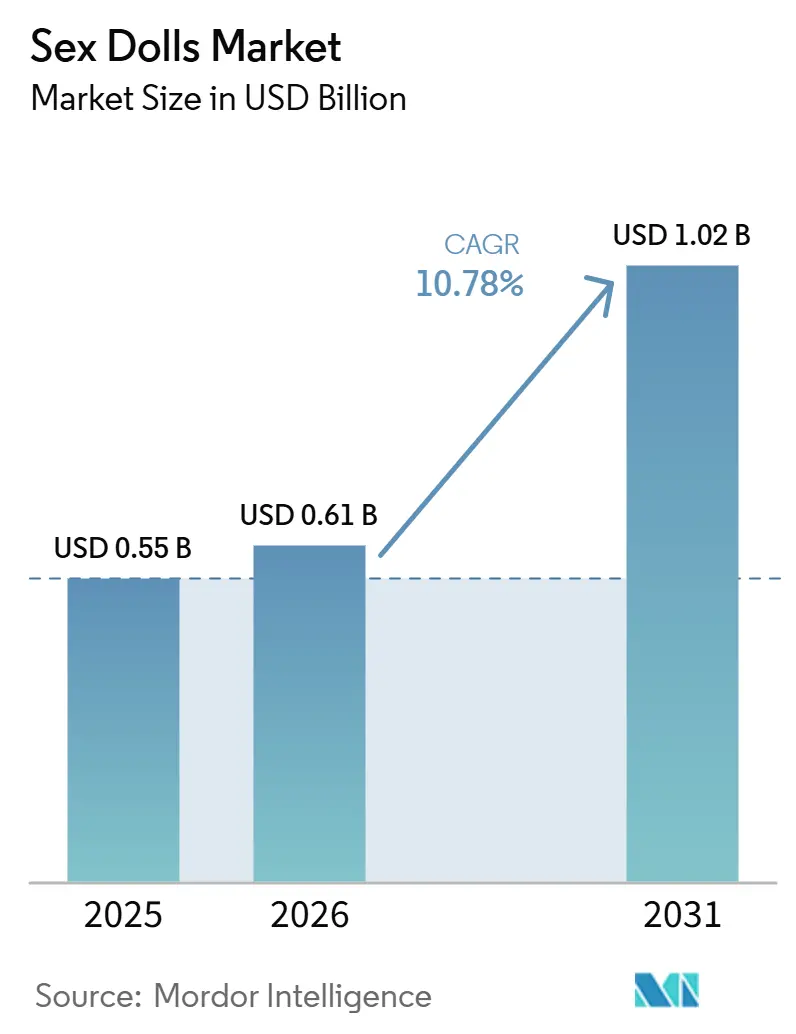

The Sex Dolls Market size is projected to expand from USD 0.55 billion in 2025 and USD 0.61 billion in 2026 to USD 1.02 billion by 2031, registering a CAGR of 10.78% between 2026 to 2031.

The sex dolls market is benefiting from a clear shift in consumer attitudes, as intimacy products are moving closer to broader self-care and personal wellness spending. Better materials, more realistic product design, and wider use of direct online sales are helping the sex dolls market reach buyers who previously stayed outside the category. The sex dolls market is also being shaped by a move from one-time hardware purchases toward products that support longer engagement through customization, maintenance services, and companion features. Competitive positioning is becoming more defined, with premium brands focusing on craft and realism, while larger volume players expand access through scale, pricing flexibility, and broader digital distribution. This combination of wider social acceptance, product improvement, and more discreet fulfillment continues to support the sex dolls market through 2031.

Key Report Takeaways

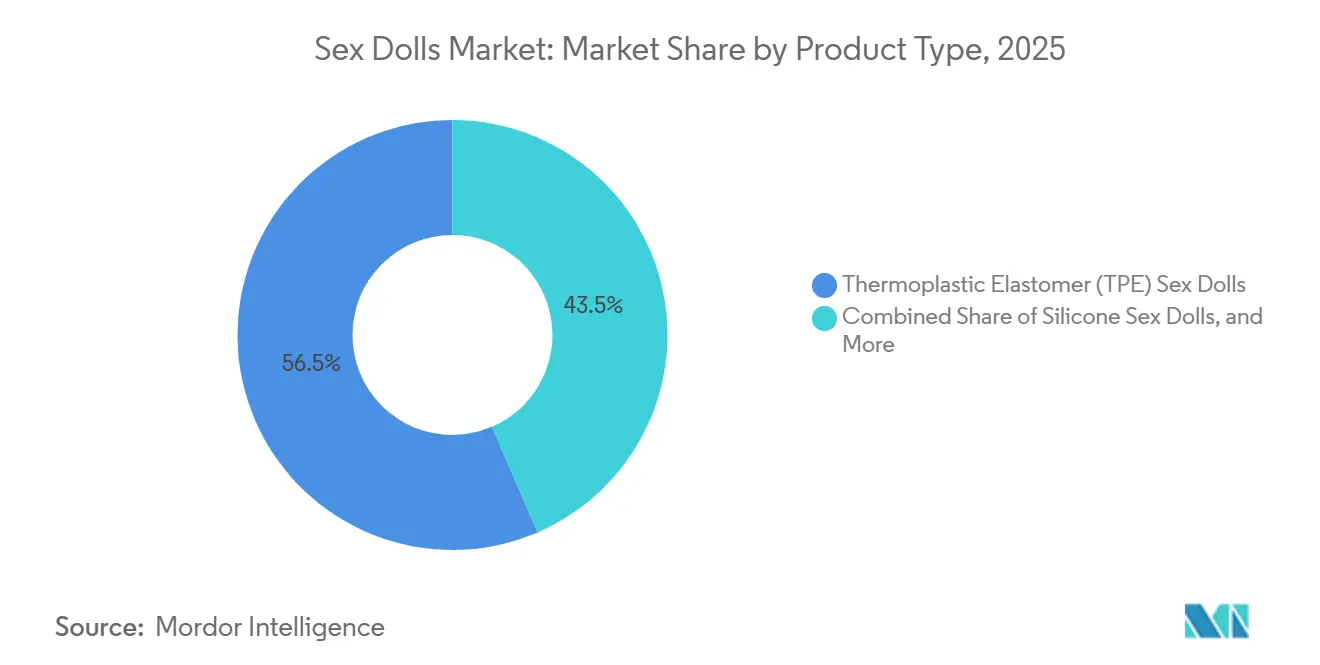

- By product type, TPE dolls led with 56.48% of revenue in 2025, while silicone sex dolls are projected to expand at an 11.65% CAGR through 2031.

- By technology, non-AI or traditional sex dolls held 68.25% of revenue in 2025, while AI-enabled sex dolls are forecast to grow at a 12.43% CAGR through 2031.

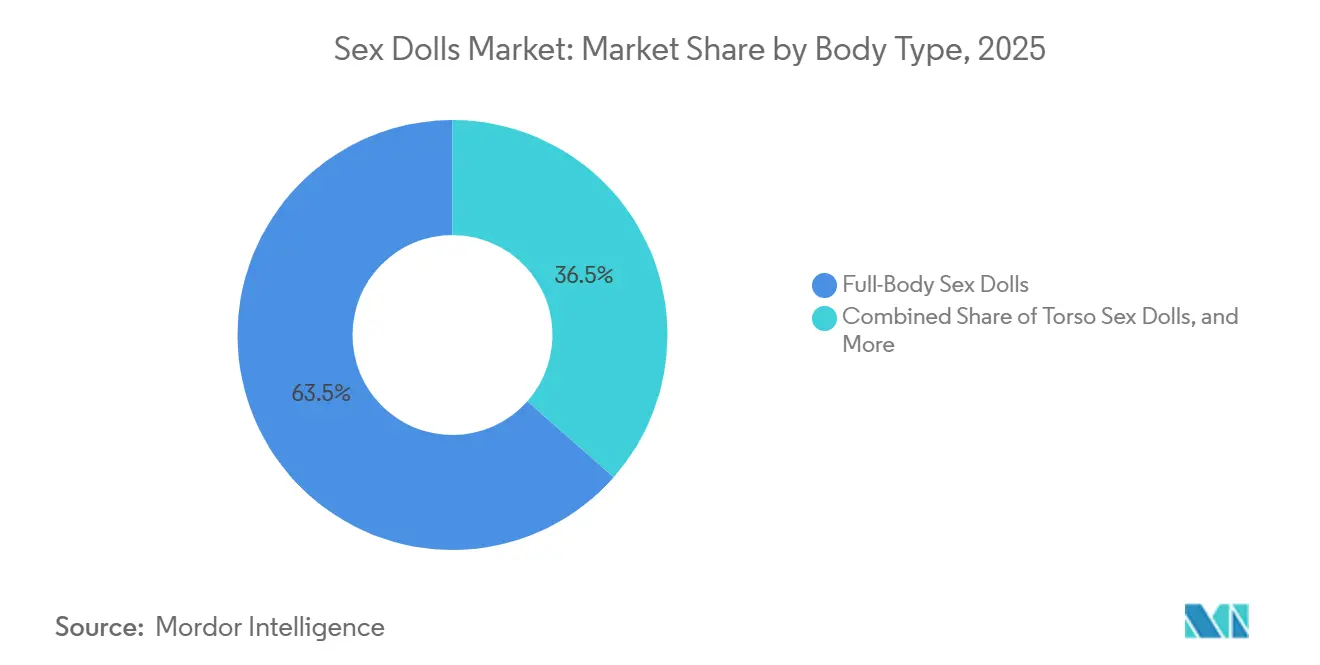

- By body type, full-body sex dolls accounted for 63.49% of revenue in 2025, while torso sex dolls are projected to rise at a 12.89% CAGR through 2031.

- By distribution channel, online retail or e-commerce represented 58.71% of revenue in 2025, while direct-to-consumer manufacturer websites are expected to grow at a 13.58% CAGR through 2031.

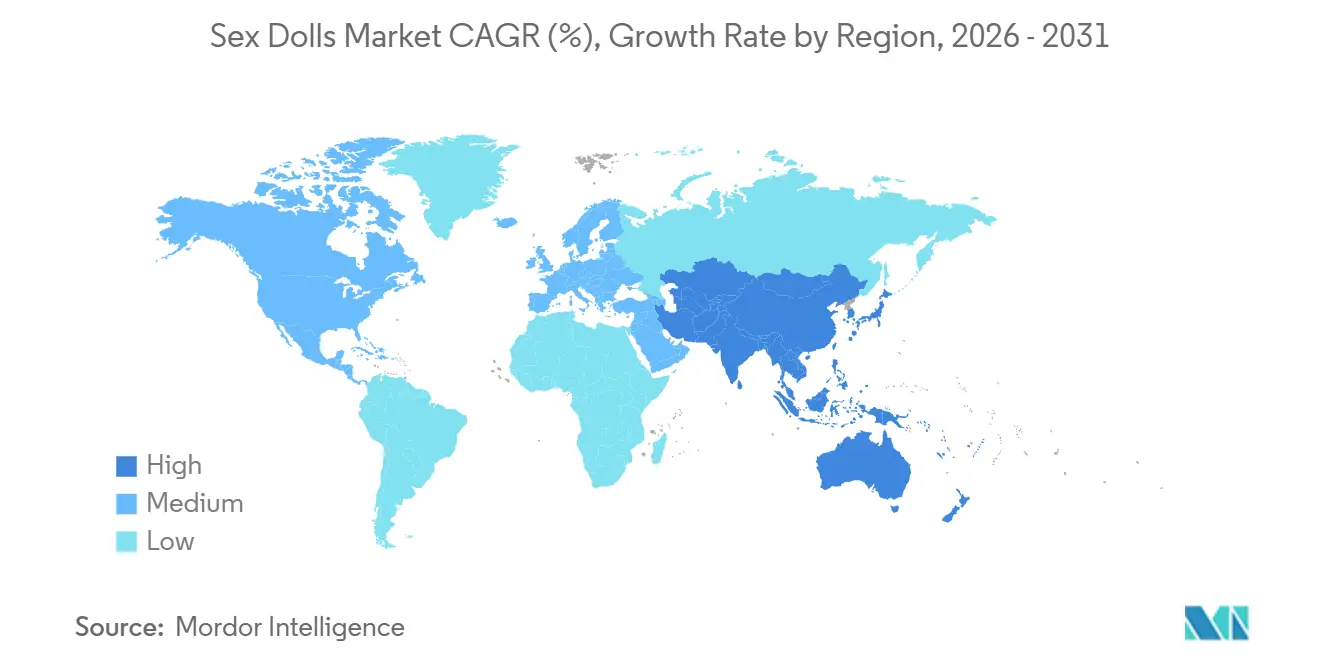

- By geography, the Asia-Pacific accounted for 41.37% of the revenue share in 2025. The Asia-Pacific is set to expand at a 14.53% CAGR, the quickest among all regions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Sex Dolls Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Acceptance of Sexual Wellness Products and Shifting Consumer Attitudes | +2.3% | Global, most pronounced in North America and Western Europe | Medium term (2-4 years) |

| Growth of E-Commerce and Direct-To-Consumer Sales Channels | +2.8% | North America, Europe, APAC core | Short term (≤ 2 years) |

| Increasing Demand for AI-Enabled Companion and Robotic Sex Dolls | +2.1% | North America, China, Japan, spillover to South Korea and Australia | Medium term (2-4 years) |

| Rising Demand For Personalization, Customization, and Premium Features | +1.8% | North America, Western Europe, Australia | Long term (≥ 4 years) |

| Expansion of Private-Label and Discreet Fulfillment Models | +1.4% | North America, UK, Germany, early gains in Brazil and India | Short term (≤ 2 years) |

| Social Normalization Through Digital Communities and Creator-Led Marketing | +1.2% | APAC, North America, social-commerce-led spillover to MEA | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Acceptance of Sexual Wellness Products and Shifting Consumer Attitudes

The sex dolls market is gaining from a broader change in how adult wellness products are discussed in public and private settings. Products that once sat at the edge of discretionary spending are now being considered alongside emotional comfort, companionship, and self-care in several consumer groups. The Japan Love Doll White Paper 2026 reported that many owners associated doll ownership with mental stability and hobby enrichment, which supports the view that buyer motivation is widening beyond physical use alone.[1]Japan Love Doll White Paper 2026,” Kuma Trading Co., Ltd That shift matters for the sex dolls market because it reduces the role of stigma as the main filter on purchase intent. It also suggests that brands able to support ongoing engagement after purchase may hold stronger loyalty than brands that compete only on product appearance or entry price.

Growth of E-Commerce and Direct-to-Consumer Sales Channels

The sex dolls market continues to expand through online channels because privacy remains a central condition for conversion in many countries. E-commerce allows buyers in less accessible or more socially conservative areas to research, configure, and purchase products without entering a physical store. Direct manufacturer websites are especially important in the sex dolls market because they move customization decisions closer to the factory, which broadens product choice while reducing reliance on intermediaries. This shift also gives manufacturers direct access to buyer preferences, delivery behavior, and configuration patterns that can shape faster product updates. As a result, the sex dolls market is seeing digital channels function as both a sales route and a product development tool.

Increasing Demand for AI-Enabled Companion and Robotic Sex Dolls

The sex dolls market is being reshaped by products that add voice interaction, memory, and responsive behavior to a traditionally static product category. These features change the value proposition from physical ownership alone to a more sustained companionship experience. Realbotix used CES 2026 to showcase AI-powered humanoid robots with on-device conversational capability in multiple languages, which signaled that embedded interaction is moving closer to commercial practicality.[2]Realbotix to Exhibit at CES 2026 with Expanded Lineup of AI-Powered Humanoid Robots For the sex dolls market, this matters because AI can support recurring revenue models and create a stronger reason for buyers to remain engaged after purchase. It also raises the competitive ceiling, since product differentiation will rely more on software performance, responsiveness, and system integration.

Rising Demand for Personalization, Customization, and Premium Features

The sex dolls market is also moving upward through a strong preference for customization in materials, body format, facial design, and added features. Buyers in premium tiers are showing a willingness to accept longer delivery windows when the end product reflects specific personal preferences. This is helping the sex dolls market support higher average selling prices without relying only on scale. The trend is particularly visible in silicone products, where realism, color stability, and dimensional precision support premium positioning, and silicone sex dolls are forecast to grow at an 11.65% CAGR through 2031. Over time, manufacturers that can manage bespoke orders with steady quality control are likely to hold a stronger position than sellers that compete only through lower prices.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Product Cost and Limited Affordability | -1.4% | MEA, South America, South and Southeast Asia | Short term (≤ 2 years) |

| Social Stigma, Ethical Concerns, and Regulatory Challenges | -1.2% | MEA, conservative markets in APAC and South America, EU compliance escalation | Long term (≥ 4 years) |

| Cross-Border Compliance Risk for Materials, Content, and Shipping | -0.9% | Global, EU, Australia, and New Zealand most exposed | Medium term (2-4 years) |

| Product Durability, Hygiene, and Maintenance Complexity | -0.7% | Global, most acute in markets lacking established post-sale infrastructure | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Product Cost and Limited Affordability

The sex dolls market still faces a clear affordability ceiling, especially outside higher-income buyer groups. Premium silicone products and AI-linked full-body models remain expensive relative to discretionary spending capacity in many emerging markets. Even mid-tier options can limit adoption where household budgets are tighter and digital financing tools are less mature. This matters for the sex dolls market because demographic conditions may support demand in those countries, yet pricing still constrains actual conversion. The result is a slower volume build in regions where interest may exist, but feature-rich products remain difficult to afford.

Social Stigma, Ethical Concerns, and Regulatory Challenges

Social stigma continues to limit visibility, category trust, and purchase willingness in many parts of the sex dolls market. Regulatory pressure is also becoming more direct, especially around product compliance, platform responsibility, and child-like designs. In November 2025, the European Parliament called for stronger Digital Services Act enforcement, customs reform, and tighter accountability for platforms selling non-compliant goods.[3]Resolution 2025/2971(RSP) on Protecting EU Consumers Against the Practices of Certain E-Commerce Platforms, The Case of Child-Like Sex Dolls, Weapons and Other Illegal Products and Materials In Germany, the Federal Constitutional Court upheld criminal liability tied to child-like sex dolls in a May 2026 ruling that was published in July 2026.[4]“Beschluss Vom 21. Mai 2026, Az. 2 BvR 1096/22, 2 BvR 1097/22,” Bundesverfassungsgericht For the sex dolls market, these developments increase compliance costs, raise reputational exposure for marketplaces, and favor manufacturers whose adult-focused documentation and product design are clearly defensible.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: TPE Dominates, Silicone Grows Through Premiumization

TPE dolls held 56.48% of the market in 2025, which kept them in the leading position by product type. That share reflects a price-to-quality range that reaches a much larger buyer base than full silicone alternatives. TPE is easier to mold, more elastic, and lower in raw material cost, which makes it well suited to mid-market production runs. Those features help the sex dolls market maintain accessibility in a category where affordability still shapes first-time purchase behavior. TPE also aligns well with online buying patterns, since buyers can obtain life-size products with broad visual customization at a lower entry cost.

Silicone sex dolls are projected to expand at an 11.65% CAGR through 2031, making this the fastest-growing material category in the sex dolls market size. Growth in silicone reflects rising buyer interest in tactile realism, stronger long-term color retention, and better compatibility with premium features. This trend also supports the view that a growing part of the sex dolls market is trading up rather than staying fixed at entry-level price points. Latex and other smaller material variants remain niche because allergy concerns and durability limits keep them behind TPE and silicone in wider adoption. Hybrid constructions that combine silicone-focused facial presentation with lower-cost body materials are also gaining attention because they narrow the price gap while preserving a premium appearance.

TPE keeps its lead because it offers a workable balance between realism and affordability for a broad buyer group. Manufacturers also benefit from faster scaling when they use TPE in standard and semi-custom models. In practical terms, that keeps replacement cycles, catalog breadth, and online assortment expansion moving in the right direction for the sex dolls market. Silicone, however, is gaining faster because premium buyers place more value on finish quality and long-term presentation. This split means the sex dolls market is likely to hold a dual-material structure rather than converge around a single dominant material tier.

The product mix also shows that pricing and aspiration are working side by side. Buyers entering the category still lean toward lower-cost formats, while experienced or higher-income buyers move toward higher-spec products. This creates room for manufacturers to operate at several price bands without leaving the broader sex dolls market. It also explains why leading suppliers continue to carry both TPE and silicone programs instead of focusing on only one material. Over the forecast period, product type competition is likely to center on how well brands manage this balance across margin, realism, and fulfillment speed.

By Technology: Non-AI Holds Share, AI Redraws the Competitive Ceiling

Non-AI or traditional sex dolls accounted for 68.25% of the market in 2025, which made them the largest technology segment. The installed buyer base still treats the purchase as a physical product decision first, with realism and customization outweighing software functionality. That pattern keeps conventional products commercially important across much of the sex dolls market. It also shows that the sex doll industry remains heavily tied to form, material quality, and buyer comfort with a one-time purchase model. For many consumers, tactile realism and visual specification still matter more than advanced interaction.

AI-enabled sex dolls are projected to grow at a 12.43% CAGR through 2031, which places them at the front of the technology curve. That pace reflects improving feasibility for voice interaction, memory tools, and adaptive response systems. Realbotix highlighted this direction through its CES 2026 exhibition of AI-powered humanoid robots with multilingual on-device interaction. The importance of the sex dolls market is not only product novelty, but also the possibility of recurring engagement and higher buyer retention. As interaction quality improves, AI becomes a stronger reason for brands to position themselves as platform providers rather than simple hardware sellers.

Robotic sex dolls remain the highest technical frontier, but they are still early in unit terms. Full articulation and autonomous movement raise engineering complexity, durability demands, and service expectations. That keeps the sex dolls market from reaching mass robotic adoption in the near term, even though the concept is drawing attention. The technology path still matters because it shapes buyer expectations for what premium products may offer in future cycles. In that sense, robotic formats influence competitive direction even before they become a large revenue base.

The technology split also reveals a layered market rather than a sudden shift from old to new. Traditional models continue to provide the revenue foundation, while AI-led formats define the next premium ceiling. This gives manufacturers room to stage upgrades instead of forcing a complete technology reset across the full catalog. For the sex dolls market, that staged pattern lowers transition risk and supports broader product laddering. Over time, the strongest brands are likely to be those that can connect physical realism with credible software performance.

By Body Type: Full-Body Leads, Torso Gains on Value

Full-body sex dolls captured 63.49% of the market in 2025, which kept them in the lead by body type. This format supports the highest degree of customization and usually carries the strongest premium pricing. It also matches the buying behavior seen in bespoke online orders, where buyers spend more time on configuration and accept longer delivery windows. For the sex dolls market, full-body products remain the aspirational anchor of the category because they combine realism, scale, and personalization in a single purchase. That makes them central to both premium branding and revenue generation.

Torso sex dolls are projected to grow at a 12.89% CAGR through 2031, which makes them the fastest-growing body type. The appeal comes from lower entry pricing, easier storage, and better handling for buyers in smaller living spaces. This growth pattern shows that the sex dolls market is not only expanding through premiumization but also through formats that reduce ownership friction. Torso products are especially relevant in single-occupancy urban settings where space, portability, and discretion matter as much as physical design. Partial body dolls continue to serve smaller entry and specialty niches, but they remain behind both full-body and torso formats in broader momentum.

The body type mix points to two distinct forms of value creation. Full-body formats drive higher ticket size and deeper customization, while torso formats improve reach by lowering commitment on price and storage. That balance helps the sex dolls market serve both advanced buyers and first-time users without forcing a single ownership model. It also gives manufacturers a practical way to broaden assortment without diluting category identity. As the market grows, brands that present torso products as a deliberate format, rather than a compromise, are likely to gain more traction.

This segment also reflects how privacy shapes product choice. A buyer who wants realism may still choose a smaller format if daily storage and shipping concerns are significant. That means the sex dolls market is responding not only to desire for features, but also to practical ownership conditions. Full-body products should keep their lead because they remain the category benchmark. Torso products, however, are likely to keep growing faster because they solve cost and convenience barriers that still limit wider adoption.

By Distribution Channel: E-Commerce Leads, DTC Websites Redefine Margins

Online retail or e-commerce held 58.71% of distribution revenue in 2025, which made it the largest sales channel. That lead reflects the strong role of privacy in purchase behavior and the ability of digital platforms to reach buyers beyond major urban centers. In the sex dolls market, online access is often a precondition for transaction completion rather than a simple convenience feature. It allows buyers to compare formats, materials, and body types in a controlled setting with greater anonymity. This keeps e-commerce central to both category discovery and repeat demand.

Direct-to-consumer manufacturer websites are projected to grow at a 13.58% CAGR through 2031, which makes them the fastest-growing distribution channel. Their advantage lies in direct configuration, stronger margin capture, and better access to buyer preference data. That makes the sex dolls market more responsive, because product teams can learn from real order behavior without waiting on distributor feedback. Specialty adult stores remain relevant for first-time buyers who want reassurance before purchase, but their reach stays limited to concentrated urban demand pockets. Over time, direct channels are also likely to gain importance in compliance-heavy markets because manufacturers can control documentation, disclosure, and shipment protocols more closely.

The channel mix shows that anonymity and customization now work together. Marketplace-style online retail still supports broad traffic and entry-level access. Manufacturer-owned websites, however, are becoming more important where buyers want premium specification or tailored builds. This creates a two-layer digital structure inside the sex dolls market rather than a simple shift from stores to websites. Brands that understand the difference between discovery channels and decision channels are better positioned to grow efficiently.

Distribution also has a clear effect on margins and brand power. Sellers that rely mostly on third-party marketplaces may reach buyers faster, but they give up control over data and part of the customer relationship. Brands with strong direct sites can shape the full purchase path from configuration to after-sales contact. That matters in the sex dolls industry because repeat engagement, maintenance support, and future upgrades can influence lifetime value. As a result, distribution channel strategy is becoming a core part of competition rather than a back-end sales decision.

Geography Analysis

North America held 41.37% of the sex dolls market share in 2025, which made it the largest regional market. The region benefits from mature direct-to-consumer logistics, broad online purchasing comfort, and a higher willingness to pay for premium configurations. The United States drives most regional demand, supported by well-known domestic manufacturers and a strong base of buyers comfortable with factory-direct customization. Canada and Mexico are smaller markets, but cross-border fulfillment is helping demand broaden beyond the United States. North America also stands out as an early proving ground for companion features because buyers in this region are more likely to accept subscription-style digital interaction layered onto a hardware purchase.

Europe was the second-largest regional cluster in 2025, with Germany, the United Kingdom, and France serving as the main demand centers. Product demand in Germany has moved beyond a narrow niche, supported by better material quality and more sophisticated product design. At the same time, the regulatory picture in Europe is becoming stricter around compliance, platform responsibility, and prohibited child-like designs. The European Parliament called for stronger action against non-compliant goods in November 2025, which increases the operating advantage of manufacturers that can support solid documentation and age-verification processes. Germany added another clear signal in 2026 when its Federal Constitutional Court upheld the legal ban tied to child-like sex dolls.

Asia-Pacific is projected to grow at a 14.53% CAGR through 2031, making it the fastest-growing regional block in the sex dolls market size. China remains central because its manufacturing clusters support much of global production volume and product variety. Japan adds a different source of demand, with local ownership patterns increasingly linked to companionship, hobby value, and emotional comfort rather than only physical use. South Korea and Australia are emerging demand markets, though Australia presents stricter border enforcement conditions for non-compliant imports. Middle East and Africa, along with South America, remain earlier-stage markets because affordability limits, stronger stigma, and weaker discreet logistics still slow wider uptake. Even so, expanding mobile commerce and cross-border e-commerce are gradually lowering access barriers in urban pockets across those regions.

Competitive Landscape

The sex dolls market remains moderately fragmented, with Chinese manufacturers leading production scale while a smaller set of U.S. and Japanese companies holds stronger premium recognition. This creates a market structure where scale leadership and brand prestige do not always sit with the same companies. In practice, the sex dolls market is forming around two broad strategies: higher-volume makers that broaden access through scale and feature expansion, and premium specialists that focus on material quality, realism, and bespoke design. That split helps explain why price ladders in the sex dolls market remain wide even when products look similar at a distance. It also shows why buyer trust, product finish, and delivery experience matter as much as catalog breadth.

One important strategic move came from Realbotix, which used CES 2026 to showcase a broader lineup of AI-powered humanoid robots and highlight multilingual on-device conversation capability. That move matters because it pushes competition toward embedded intelligence rather than static hardware alone. A second strategic pattern is the continued use of factory-direct configuration portals by premium brands, which helps preserve margin while giving buyers more control over design choices. A third pattern is dual-material product planning, where manufacturers keep both TPE and silicone lines to serve separate price bands without leaving the broader sex dolls market. Together, these moves show that competition is no longer only about realism, but also about how effectively a company manages channel control, feature depth, and buyer segmentation.

The sex dolls market still has clear white space in gender diversity, therapeutic use cases, and more accessible AI-linked products at lower price points. Male and gender-diverse products remain underrepresented relative to the attention they are beginning to receive from buyers. The sex dolls market may also open further if companies can position select products around loneliness support, social comfort, or assistive use without losing regulatory clarity. Compliance quality is becoming another real differentiator, especially in Europe and Australia, where documentation standards and enforcement pressure are rising. As regulation tightens and product technology advances, competitive advantage in the sex dolls market is likely to depend on a mix of product credibility, direct customer access, and the ability to support evolving legal requirements.

Sex Dolls Industry Leaders

Abyss Creations (ReaDoll)

Aibei Doll

DS Doll

Elsa Babe

Irontech Doll

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2026: Germany's Bundesverfassungsgericht (Federal Constitutional Court) upheld the constitutionality of §184l StGB (ruling dated May 21, 2026, published July 2, 2026) in a 6-2 majority decision, confirming criminal prohibitions on the manufacture, sale, and possession of child-like sex dolls. The ruling signals durable enforcement in Germany and sets a persuasive precedent for interpretation across EU member states.

- January 2026: Realbotix Corp. (TSX-V: XBOT; OTC: XBOTF) demonstrated the first public autonomous, unscripted AI conversation between two humanoid robots (Aria and David) at CES 2026, running proprietary on-device AI in English, Spanish, French, and German for over two hours. The demonstration validated on-device embedded AI as a commercially credible capability path, independent of cloud connectivity.

- November 2025: The European Parliament adopted Resolution 2025/2971(RSP) on November 26, 2025, calling for enforcement of the EU Digital Services Act against platforms selling non-compliant sex dolls, reform of the Union Customs Code to introduce a "deemed importer" concept, and direct Commission sanctioning powers. The resolution accelerates regulatory pressure on marketplace operators and cross-border distributors across the EU single market.

Global Sex Dolls Market Report Scope

As per the scope of the report, sex dolls are life‑sized silicone or TPE companions designed to resemble human anatomy for intimate, personal, or companionship use. They feature realistic body sculpting, articulated skeletons, and customizable faces or body types. Modern manufacturers also integrate soft‑touch materials and optional robotic/AI features to enhance realism. They are produced by specialized sex‑doll manufacturers using proprietary molding and finishing techniques.

The sex dolls market is segmented by product type, technology, body type, distribution channel, and geography. By product type, the market is segmented into silicone sex dolls, thermoplastic elastomer (TPE) sex dolls, latex sex dolls, and others. By technology, the market is segmented into non-AI / traditional sex dolls, AI-enabled sex dolls, and robotic sex dolls. By body type, the market is segmented into full-body sex dolls, torso sex dolls, and partial body dolls. By distribution channel, the market is segmented into online retail / E-commerce, specialty adult stores, and others. The geography segment is further divided into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market size and forecasts in value (USD) for the above segments.

| Silicone Sex Dolls |

| Thermoplastic Elastomer (TPE) Sex Dolls |

| Latex Sex Dolls |

| Others |

| Non-AI / Traditional Sex Dolls |

| AI-Enabled Sex Dolls |

| Robotic Sex Dolls |

| Full-Body Sex Dolls |

| Torso Sex Dolls |

| Partial Body Dolls |

| Online Retail / E-Commerce |

| Specialty Adult Stores |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Silicone Sex Dolls | |

| Thermoplastic Elastomer (TPE) Sex Dolls | ||

| Latex Sex Dolls | ||

| Others | ||

| By Technology | Non-AI / Traditional Sex Dolls | |

| AI-Enabled Sex Dolls | ||

| Robotic Sex Dolls | ||

| By Body Type | Full-Body Sex Dolls | |

| Torso Sex Dolls | ||

| Partial Body Dolls | ||

| By Distribution Channel | Online Retail / E-Commerce | |

| Specialty Adult Stores | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the 2031 outlook for the sex dolls market?

The sex dolls market is projected to reach USD 1.02 billion by 2031 from USD 0.61 billion in 2026, which reflects a 10.78% CAGR over 2026-2031.

Which product type leads revenue today?

TPE dolls led product revenue with 56.48% in 2025 because they offer a wider affordability range than full silicone products.

Which material category is growing the fastest?

Silicone sex dolls are the fastest-growing product type, with an 11.65% CAGR through 2031, supported by premiumization and stronger realism.

Why are AI-enabled products getting more attention?

AI-enabled formats are forecast to grow at a 12.43% CAGR through 2031 because buyers are showing stronger interest in memory, interaction, and companion-style features.

Which sales channel matters most for future growth?

Online retail led with 58.71% of revenue in 2025, but direct-to-consumer manufacturer websites are growing faster at a 13.58% CAGR because they support customization, better margins, and stronger buyer data capture.

Which region is growing the fastest through 2031?

Asia-Pacific is the fastest-growing region at a 14.53% CAGR, supported by China’s manufacturing base and Japan’s growing companionship and well-being use case.

Page last updated on: