Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

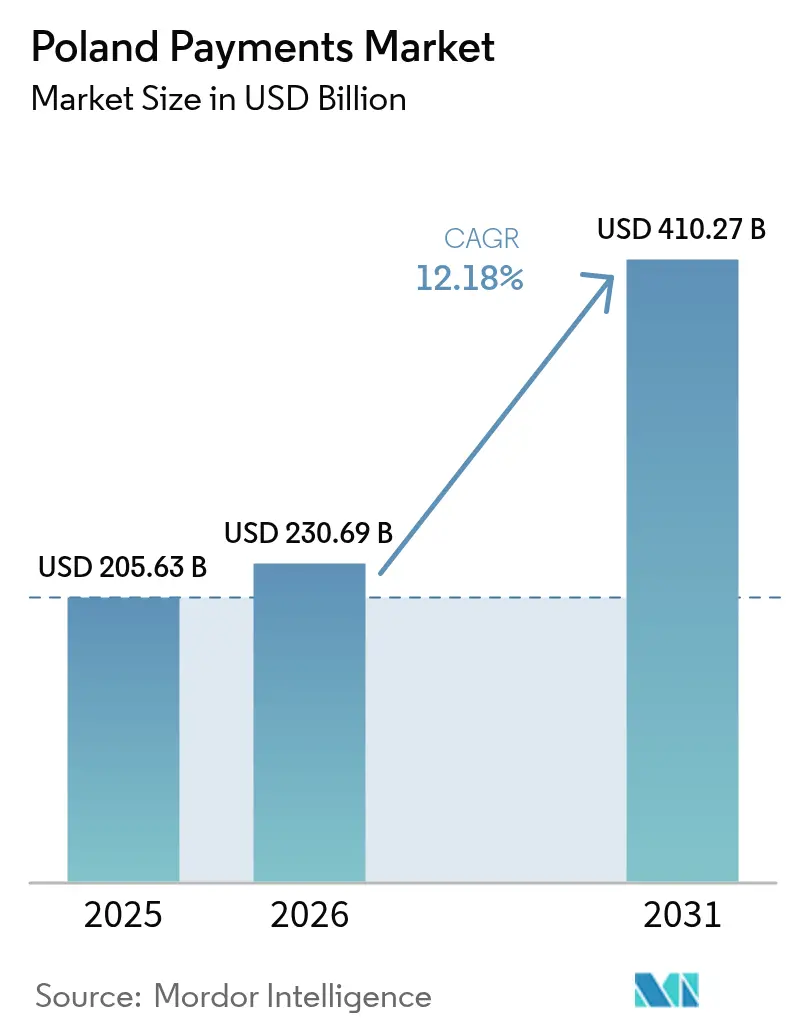

| Base Year Market Size (2025) | USD 205.63 Billion |

| Market Size (2026) | USD 230.69 Billion |

| Market Size (2031) | USD 410.27 Billion |

| Growth Rate (2026 - 2031) | 12.18% CAGR |

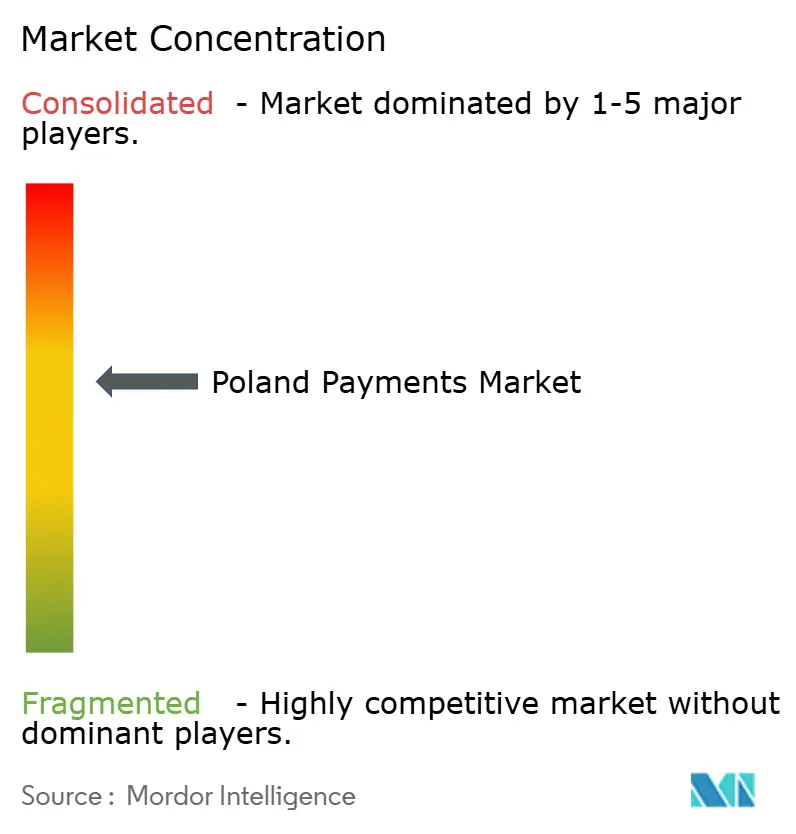

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Poland Payments Market Analysis by Mordor Intelligence

The Poland payments market size is expected to grow from USD 205.63 billion in 2025 to USD 230.69 billion in 2026 and is forecast to reach USD 410.27 billion by 2031 at 12.18% CAGR over 2026-2031. The expansion reflects a decisive migration from cash to digital payments, amplified by the Cashless Poland Program, government tax incentives for terminal deployment and the ubiquity of domestic instant-payment rails. BLIK’s contribution of 1.2% to national GDP in 2024 underscores the economic weight of locally engineered solutions.[1]BLIK, “BLIK as a Growth Driver for the Economy – Payments Made with BLIK Supported the Generation of Around 1.2% of Poland's GDP in 2024,” blik.com Competitive intensity remains high as banks, fintechs and global processors contest share across point-of-sale, e-commerce and mobile channels. Rising interchange fees, broader AML requirements and rural cash affinity temper growth, yet improving broadband coverage and PSD2-enabled open banking keep the long-term outlook compelling.

Key Report Takeaways

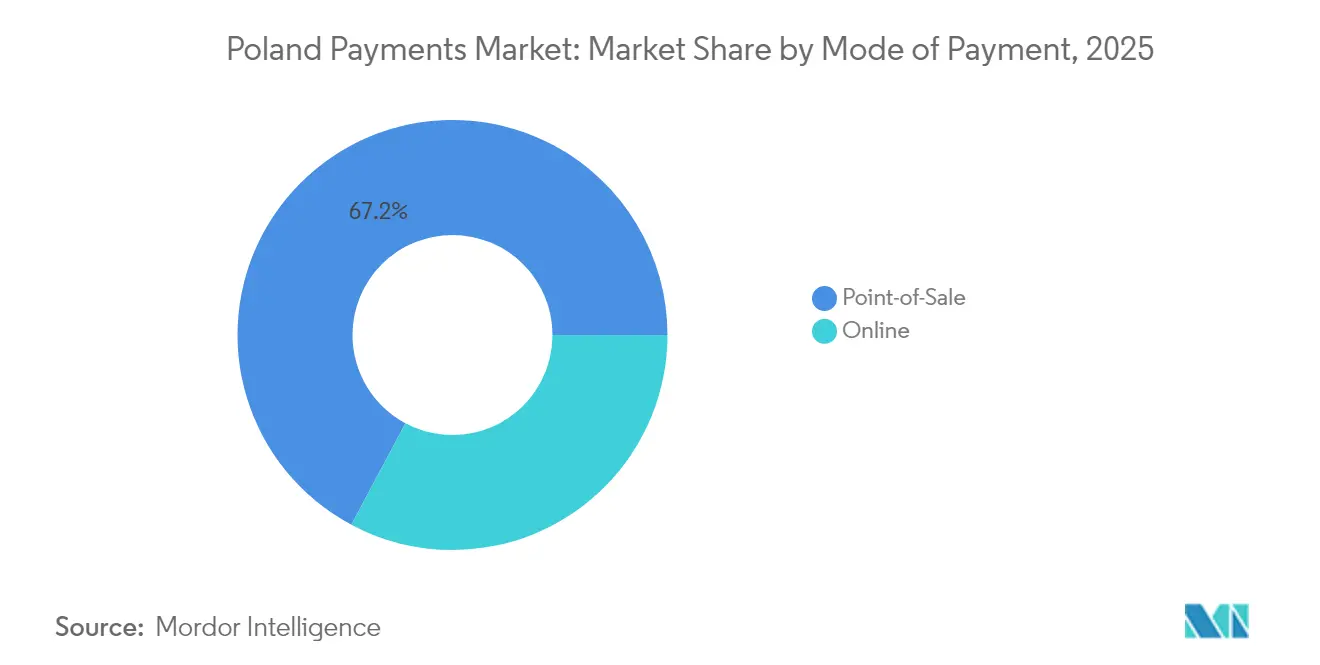

- By interaction channel, point-of-sale captured 57.20% Poland payments market share in 2025; e-commerce and m-commerce are forecast to expand at a 15.52% CAGR to 2031.

- By mode of payment, card-based POS held 37.25% Poland payments market share in 2025, while digital wallet and account-to-account options are scaling at a 13.98% CAGR. Overall Point-of-sale accounts for 67.20% of the share.

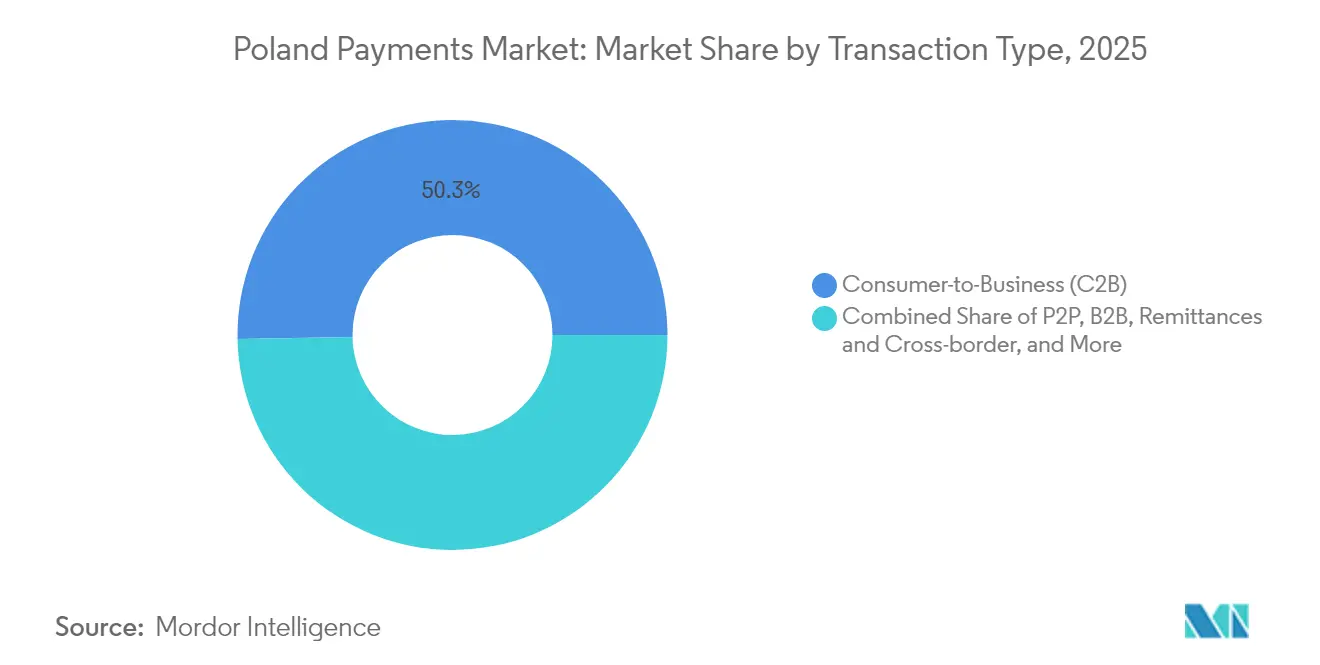

- By transaction type, consumer-to-business flows accounted for 50.30% of the Poland payments market size in 2025; remittances and cross-border payments are forecast to rise at a 15.79% CAGR.

- By end-user industry, retail commanded 38.40% of the Poland payments market size in 2025; healthcare payments are advancing at a 13.18% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Poland Payments Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government-led Cashless Poland Program & Tax Incentives for POS Adoption | +2.1% | National, with early gains in Warsaw, Krakow, Gdansk | Medium term (2-4 years) |

| Rapid Uptake of BLIK & Domestic Instant-Payment Infrastructure | +2.8% | National, strongest in urban centers | Short term (≤ 2 years) |

| E-commerce Boom Among Polish SMEs Leveraging Omnichannel Gateways | +1.9% | National, concentrated in major metropolitan areas | Medium term (2-4 years) |

| NFC-Enabled Mobile-Wallet Penetration Driven by High Android Share | +1.4% | National, with rural lag | Short term (≤ 2 years) |

| PSD2 Open-Banking APIs Fueling Embedded Payments in Polish Super-apps | +1.2% | EU-wide, Poland as early adopter | Long term (≥ 4 years) |

| Contactless Public-Transport Ticketing Roll-outs in Major Cities | +0.8% | Urban centers: Warsaw, Krakow, Wroclaw, Gdansk | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government-led Cashless Poland Program & Tax Incentives for POS Adoption

The state programme links fiscal incentives with infrastructure expansion, allowing merchants that process predominantly cashless sales to accelerate VAT refunds and claim specific tax deductions. More than 586,000 terminals had been deployed by mid-2023, substantially widening acceptance in micro-merchant segments that historically lacked point-of-sale capacity.[2]Visa, “Promoting Financial Inclusion and Minimising Cash Usage,” bqk-kos.org Educational campaigns paired with fiscal relief encourage merchants to actively steer consumers toward electronic payment, forming a self-reinforcing demand loop. The scheme also increases data visibility for revenue authorities, which in turn motivates further policy support.

Rapid Uptake of BLIK & Domestic Instant-Payment Infrastructure

BLIK processed 2.4 billion transactions in 2024, half occurring online, as its single-interface design removed friction across retail, ATM and peer-to-peer contexts. Full integration with 19 banks and a widening footprint on iOS devices extend reach beyond its Android origin. Partnerships with Google Play have moved BLIK from utility use cases into digital content commerce, illustrating its versatility. Because framework ownership sits with Polish banks, sovereignty concerns are mitigated while interoperability with SEPA Instant facilitates cross-border euro transfers.

E-commerce Boom Among Polish SMEs Leveraging Omnichannel Gateways

Online retail is set to double from PLN 94 billion (USD 25.32 billion) in 2022 to PLN 190 billion (USD 51.19 billion) by 2027, intensifying the need for gateways that aggregate cards, BLIK and alternative methods.[3]Neopay, “Why Every Percent Counts for Polish Retailers,” neopay.online Checkout optimisation drives value given local cart-abandonment rates near 75%. Providers differentiate through Polish-specific payment coverage, mobile-first UX and analytics that translate payment data into conversion insights. SMEs adopt subscription pricing for gateways to circumvent heavy capex, aligning costs with revenue seasonality.

NFC-Enabled Mobile-Wallet Penetration Driven by High Android Share

Contactless volumes exceeded PLN 300 billion (USD 76 billion) in H2 2024 as smartphones and wearables displaced plastic for low-value spends. Leading banks bundle tokenised credentials into core apps, prioritising biometric sign-on and single-click checkout. The coexistence of 51 million physical cards with rising wallet tokens indicates a transition phase where consumers hedge payment options rather than fully abandoning cards. Youth segments anchor wallet growth, pushing issuers to embed loyalty, transit and insurance features within payment apps.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented Bank-led Schemes Creating Merchant Interoperability Friction | -1.3% | National, affecting smaller merchants disproportionately | Medium term (2-4 years) |

| Aging Rural Demographics Maintaining Cash Preference | -0.9% | Rural areas, particularly eastern and southern regions | Long term (≥ 4 years) |

| Rising Card Interchange Fees Post-2019 Cap Expiry | -0.7% | National, impacting merchant adoption costs | Short term (≤ 2 years) |

| Heightened AML/KYC Scrutiny after Wirecard Scandal | -0.5% | EU-wide, affecting payment institutions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented Bank-Led Schemes Creating Merchant Interoperability Friction

Individual banks continue to layer proprietary features atop BLIK or card rails, forcing merchants to support multiple SDKs, dashboards and settlement cycles. This fragmentation elevates integration costs and complicates reconciliation. SMEs in particular confront varying fee matrices and chargeback processes, eroding net margins and discouraging full digital transitions. Industry bodies are now exploring unified routing protocols to streamline payout timetables and security standards.

Aging Rural Demographics Maintaining Cash Preference

A digital divide persists as only 45% of rural households enjoy very-high-capacity broadband versus 81.1% nationally. Older residents equate physical currency with security and budget control, a perception reinforced during periods of economic uncertainty. Cash dominance rises for low-ticket items where digital fees outweigh margins. While financial-literacy drives have expanded, behavioural change remains gradual and will likely follow infrastructure upgrades.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mode of Payment: Digital Wallets Extend Reach Beyond Cards

POS card payments retained a 37.25% Poland payments market share in 2025; yet digital wallets and account-to-account options are advancing at a 13.98% CAGR, steadily narrowing the gap. Overall Point-of-Sale accounts for around 67.20% of the share. This migration stems from BLIK’s bank-agnostic QR and code-based authorisation, NFC tokenisation and simplified consumer authentication. The Poland payments market size for digital wallets is projected to outpace cards beyond 2028 as smartphone penetration nears saturation. Physical cards persist in higher-age cohorts and remain essential backups when connectivity falters. Issuers respond by blending card credentials into wallets, thereby prolonging card relevance while meeting mobile demand.

Cash still anchors small rural transactions but declines each year as terminal density rises. Emerging alternatives such as wearables and QR-based closed-loop systems address niche contexts like campus payments and micro-mobility rentals. Online, card-not-present volumes compete with wallet-based push payments, especially where merchants promote BLIK to sidestep interchange. Buy-now-pay-later add-ons and instant bank transfers further diversify the modality landscape, compelling acquirers to emphasise orchestration over single-rail dominance.

By Interaction Channel: E-commerce Growth Redefines Transaction Mix

Point-of-sale activity represented 57.20% of all processed value in 2025, but the Poland payments market is witnessing a channel inversion as e-commerce and mobile commerce expand at 15.52% CAGR. Smartphones account for most incremental online traffic, driven by frictionless in-app payments and social-commerce integration. Payment service providers invest in adaptive checkout APIs that route across wallets, cards and bank transfers without altering front-end design.

High average ticket values in e-commerce necessitate robust risk scoring, 3-D Secure 2.2 compliance and token-based credential storage. In-store environments still capture large spontaneous purchases, yet even here QR links, pay-by-link receipts and scan-to-pay codes blend digital elements into face-to-face shopping. Value-added services such as real-time inventory displays or loyalty redemption provide additional revenue levers for processors serving omnichannel merchants.

By Transaction Type: Cross-Border Flows Accelerate

Consumer-to-business transactions accounted for 50.30% of 2025 volumes, underpinning stable retail dynamics. Remittances and cross-border flows, however, are forecast to outpace all other types at 15.79% CAGR, supported by Poland’s sizeable diaspora working across Western Europe and tightening EU instant-payment mandates. Providers with direct clearing connectivity and competitive FX mark-ups capture wallet share from correspondent banks.

Person-to-person transfers thrive on BLIK’s six-digit code model that posts within seconds, supporting gig-economy payouts and social-commerce settlements. Business-to-business payments, historically manual and invoice-driven, are digitising as corporates seek working-capital efficiencies. Embedded finance platforms now integrate invoice issuance, approval workflows and same-day settlement, linking payment directly to ERP records to cut reconciliation time.

By End-User Industry: Healthcare Digitalisation Emerges

Retail maintained 38.40% Poland payments market share in 2025, reflecting entrenched terminal networks and everyday transaction frequency. Yet healthcare is expanding fastest at 13.18% CAGR, propelled by e-prescriptions, telemedicine and digital patient journeys championed by the National Health Fund. The Poland payments market size for healthcare services is poised to grow further as insurers adopt instant co-pay settlement and pharmacies integrate QR prescription fulfilment.

Government services, utilities and municipal ticketing follow close behind, leveraging mObywatel and ePUAP to unify identity, documentation and payment in one interface. Hospitality, travel and entertainment sectors seize mobile wallets to streamline guest check-in and ticket redemption. Education, professional services and creative industries demand bespoke billing cycles and split-payment capabilities, allowing payment firms to monetise vertical-specific modules.

Geography Analysis

Urban centres drive heaviest digital payment penetration, with Warsaw, Krakow, Wroclaw and the Tri-City area benefitting from near-universal 4G/5G coverage and dense POS acceptance networks. These regions account for the majority of BLIK transactions and host the country’s highest ratios of wallet-enabled cards. Western and northern voivodeships, buoyed by strong manufacturing and foreign direct investment, exhibit higher e-commerce order values and cross-border trade volumes than eastern counterparts.

Rural districts lag due to limited high-speed broadband and pronounced cash culture among older demographics. Nonetheless, postal banking agents and mobile-enabled micro-acquirers are helping to bridge acceptance gaps, especially in agribusiness settlements and seasonal markets. Municipal contactless transit in Warsaw and Krakow fosters habitual wallet use that spills over to retail and food services. Success in these pilot cities serves as a template for mid-sized towns rolling out similar projects over the next three years.

Poland’s EU membership ensures technical alignment with SEPA Instant and forthcoming digital-euro initiatives, positioning domestic processors to service intra-EU merchant needs. Proximity to Ukraine and the Baltics also elevates regional remittance corridors, leading PSPs to integrate multi-currency wallets and dynamic FX engines. The strategic location of logistics parks along the A2 and S3 highways intensifies B2B payment velocity, underscoring geographic interplay between infrastructure and payment adoption.

Competitive Landscape

The Poland payments market features a moderately concentrated yet fiercely contested arena where local banks, global schemes and fintech specialists coexist. PKO Bank Polski, Santander Bank Polska and Bank Pekao S.A. command substantive customer bases and regulatory capital advantages, yet rely on continuous digital upgrades to defend share. BLIK’s consortium model empowers banks to own a domestically controlled rail, limiting dependence on international card networks.

International brands such as Mastercard and Visa enhance acceptance ubiquity and cross-border capability, often through co-branded initiatives with local issuers. Fintech entrants including PayPro’s Przelewy24, Klarna and Revolut exploit niche propositions such as e-commerce orchestration, pay-later installments or multi-currency wallets. Strategic alliances proliferate: PKO Bank Polski partnered with Mastercard to pilot tokenised open-loop transit, while foreign PSPs integrate BLIK to localise checkout.

Regulation both intensifies and shapes rivalry. PSD2 spawns open-banking aggregation platforms that blur lines between account information and payment initiation. The Digital Operational Resilience Act (DORA) raises compliance costs, favouring scale players able to amortise cybersecurity investments. Meanwhile, rising interchange ceilings since 2019 encourage merchants to steer volumes toward lower-cost account-to-account options, altering pricing levers across the value chain.

Poland Payments Industry Leaders

Apple Inc. (Apple Pay)

PayU

Santander Bank Polska

PKO Bank Polski

PayPal Holdings Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: The Polish Bank Association’s Forum Usług Płatniczych 2025 spotlighted PSD3 and DORA timelines, prompting providers to recalibrate roadmaps toward unified customer authentication and resilience testing.

- April 2025: EU Instant Payments Regulation came into force, mandating euro-denominated transfer availability across Polish banks, which pivot to fee-based value-adds such as liquidity analytics.

- March 2025: Payment-orchestration provider Solidgate integrated BLIK, giving merchants a single API for local wallet access and signalling rising demand for orchestration layers that abstract country-specific methods.

- October 2024: Mastercard unveiled a cross-border optimisation suite promising lower rejection rates and faster settlement for Polish banks, aimed at safeguarding scheme volumes amid surging account-to-account alternatives.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Polish payments market as every consumer or business transaction settled inside Poland through cards, digital wallets, account-to-account rails, or cash at a merchant point-of-sale and across online checkouts. Values are recorded at full face value in U.S. dollars, covering retail, services, and bill-payment flows. We also count cross-border e-commerce payments booked on Polish instruments that clear domestically, since they shape local acquiring volumes and fee structures. According to Mordor Intelligence, the market was worth USD 205.63 billion in 2025 and will reach USD 368.82 billion by 2030, expanding at 12.39 percent.

Scope Exclusions: Cryptocurrency peer-to-peer swaps, ATM cash withdrawals, wholesale interbank transfers, and provider fee revenues are not included in this valuation.

Segmentation Overview

- Segmentation by Mode of Payment

- Point-of-Sale

- Card (Debit, Credit, Pre-paid)

- Digital Wallets (Apple Pay, Google Pay, Interac Flash)

- Cash

- Other POS (Gift-cards, QR, Wearables)

- Online

- Card (Card-Not-Present)

- Digital Wallet and Account-to-Account (Interac e-Transfer, PayPal)

- Other Online (COD, BNPL, Bank Transfer)

- Point-of-Sale

- Segmentation by Interaction Channel

- Point-of-Sale

- E-commerce/M-commerce

- Segmentation by Transaction Type

- Person-to-Person (P2P)

- Consumer-to-Business (C2B)

- Business-to-Business (B2B)

- Remittances and Cross-border

- Segmentation by End-user Industry

- Retail

- Entertainment and Digital Content

- Healthcare

- Hospitality and Travel

- Government and Utilities

- Other End-user Industries

Detailed Research Methodology and Data Validation

Primary Research

Interviews and structured surveys with bankers, processors, fintech founders, regulators, and large merchants across Warsaw, Krakow, Wroclaw, and Gdansk let us test desk-based findings, gauge wallet uptake, and refine blended average ticket values. Feedback further anchors scenario weights within our forecast horizon.

Desk Research

We mine authoritative, non-paywalled sources such as Narodowy Bank Polski's payment statistics, Eurostat household-consumption tables, Polish Central Statistical Office retail indices, ECB card datasets, and Polish Financial Supervision Authority disclosures. Company filings, acquirer presentations, and trade association releases supplement channel splits and adoption trends. Commercial intelligence from D&B Hoovers and news flows on Dow Jones Factiva help our team verify participant revenues, merger events, and terminal rollouts. These references establish historic baselines, highlight anomalies, and guide assumption setting. Many other sources are also consulted along the way.

Market-Sizing & Forecasting

A top-down build anchored on National Bank spend totals and e-commerce GMV is reconciled with sampled bottom-up checks, POS terminal density × average ticket, BLIK transaction counts × median value, and card issuance × usage frequency to validate and adjust totals. Core variables modeled include GDP per capita, smartphone penetration, interchange caps, POS estate growth, and cash-to-card substitution velocity. Multivariate regression on these drivers, fine-tuned through expert consensus, underpins year-by-year estimates. Residual gaps are proportionally allocated to preserve internal consistency.

Data Validation & Update Cycle

Outputs clear automated variance screens, peer review, and senior sign-off. Mordor analysts revisit the model each year, triggering interim updates when major regulatory or macro shifts occur, and every refresh is preceded by fresh callbacks to our primary panel.

Why Mordor's Poland Payments Baseline Earns Trust

Published estimates often diverge because firms apply different scopes, metrics, and currency treatments. By selecting a transaction-value lens and blending top-down and bottom-up evidence, Mordor Intelligence provides a balanced yardstick that decision makers can trace back to transparent inputs.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 205.63 B (2025) | Mordor Intelligence | - |

| USD 165.3 B (2023) | Global Consultancy A | Excludes cross-border e-commerce and uses constant ticket values |

| USD 5.5 B (2025) | Industry Data Firm B | Tracks embedded finance segment only |

| USD 150.62 M (2024) | Regional Analyst C | Measures processor fee revenue, not gross payment turnover |

Differences show that when scope, metric, and currency are harmonized, Mordor's disciplined approach delivers the most dependable, repeatable baseline for Poland's payments market.

Key Questions Answered in the Report

How large is the Poland payments market in 2026?

The Poland payments market is valued at USD 230.69 billion in 2026 and is projected to grow to USD 410.27 billion by 2031.

Which interaction channel is expanding fastest?

E-commerce and mobile commerce channels are advancing at a 15.52% CAGR, overtaking point-of-sale growth momentum.

What role does BLIK play in the market?

BLIK handled 2.4 billion transactions in 2024 and contributed 1.2% to national GDP, positioning it as a critical domestic rail.

Why is healthcare a high-growth end-user segment?

National Health Fund digitalisation of prescriptions and patient records is driving a 13.18% CAGR in healthcare payment value through 2031.

How will the EU Instant Payments Regulation influence Poland?

The regulation obliges banks to offer round-the-clock euro instant transfers, enhancing cross-border speed and supporting remittance growth at a 15.79% CAGR.

What are key restraints on digital payment growth?

Scheme fragmentation that complicates merchant integration and rural cash preference among aging demographics modestly slow overall CAGR by 2.2 percentage points combined.

Page last updated on: