Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

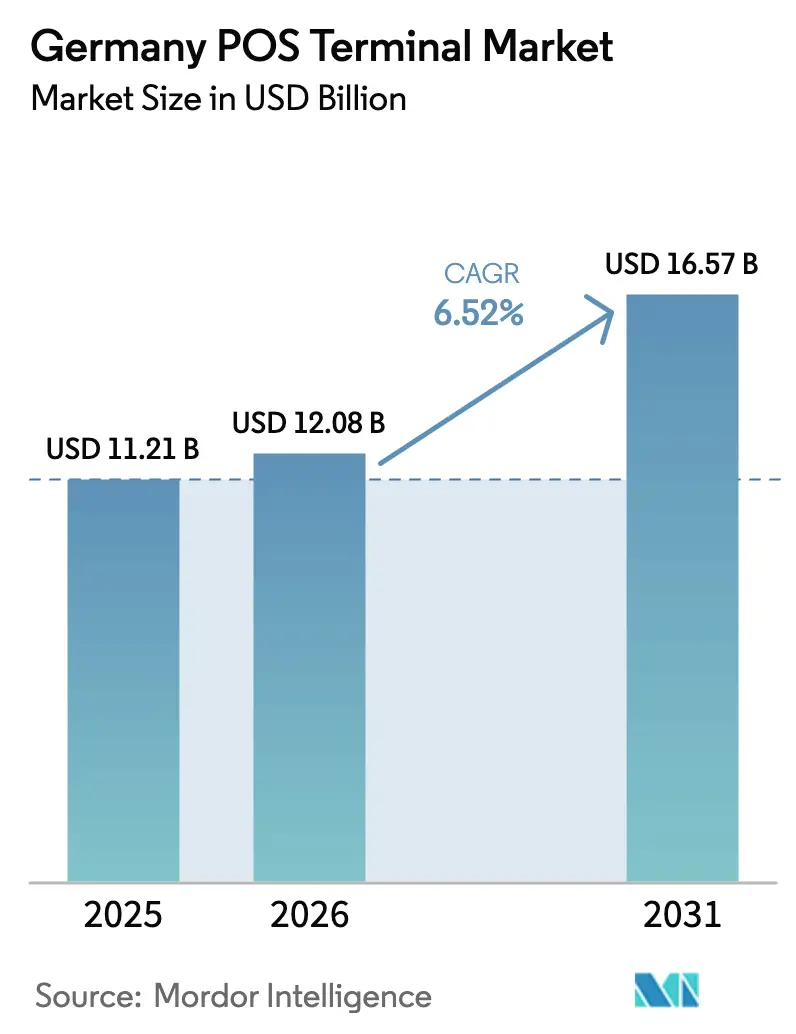

| Base Year Market Size (2025) | USD 11.21 Billion |

| Market Size (2026) | USD 12.08 Billion |

| Market Size (2031) | USD 16.57 Billion |

| Growth Rate (2026 - 2031) | 6.52% CAGR |

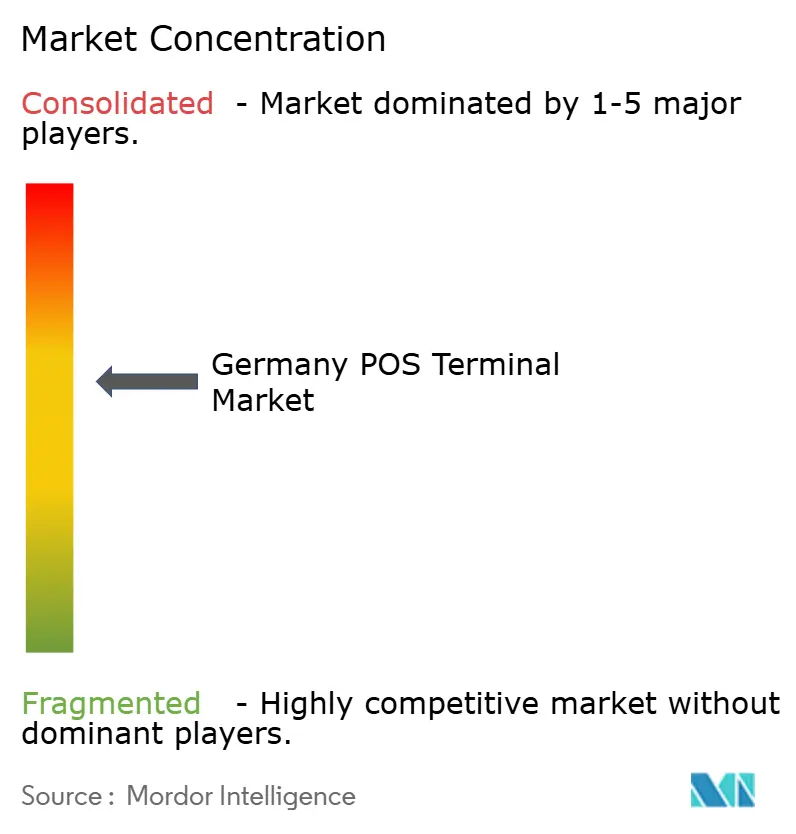

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany POS Terminal Market Analysis by Mordor Intelligence

The Germany POS terminal market size is projected to expand from USD 11.21 billion in 2025 and USD 12.08 billion in 2026 to USD 16.57 billion by 2031, registering a CAGR of 6.52% between 2026 and 2031. Robust adoption of contactless payment rails, an accelerated mobile-POS (mPOS) rollout, and fiscal-compliance mandates have synchronized to shorten terminal-replacement cycles and lift total shipment value. Cloud-based software refreshes, triggered by end-of-life announcements for legacy on-premise applications, are redirecting capital toward smart, Android-powered devices that monetize recurring software revenue instead of pure hardware margin. Fintech bundles that blend payment acceptance with working-capital loans are smoothing the upfront cost curve for small retailers, while healthcare digitalization is opening a fresh growth corridor as electronic patient records demand integrated billing and payment capability. Supply-chain exposure to Chinese Android original-design manufacturers remains a structural vulnerability, yet local certification hurdles lock in incumbents with deep BaFin and Bundesbank expertise, allowing them to pass through incremental compliance costs.

Key Report Takeaways

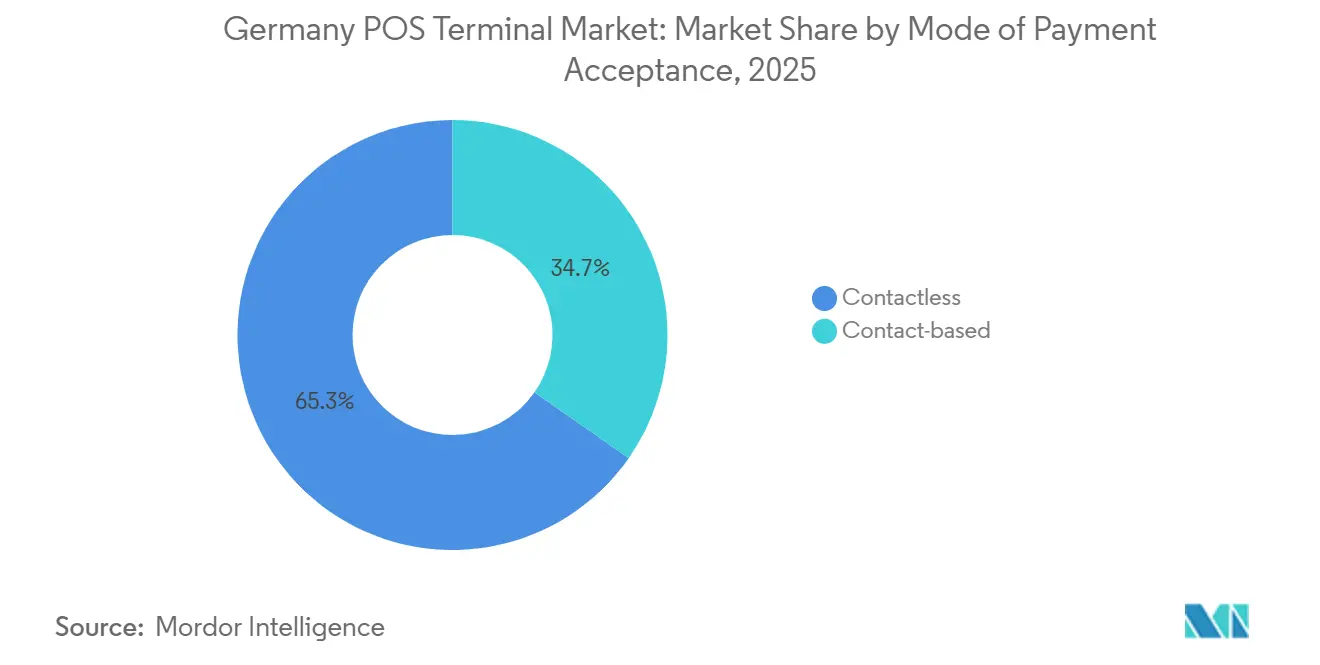

- By mode of payment acceptance, contactless terminals commanded 65.29% share of the Germany POS terminal market in 2025 and are forecast to expand at a 6.98% CAGR through 2031.

- By POS type, mobile and portable devices represented 40.03% of the Germany POS terminal market size in 2025 and are advancing at a 7.54% CAGR over the forecast horizon.

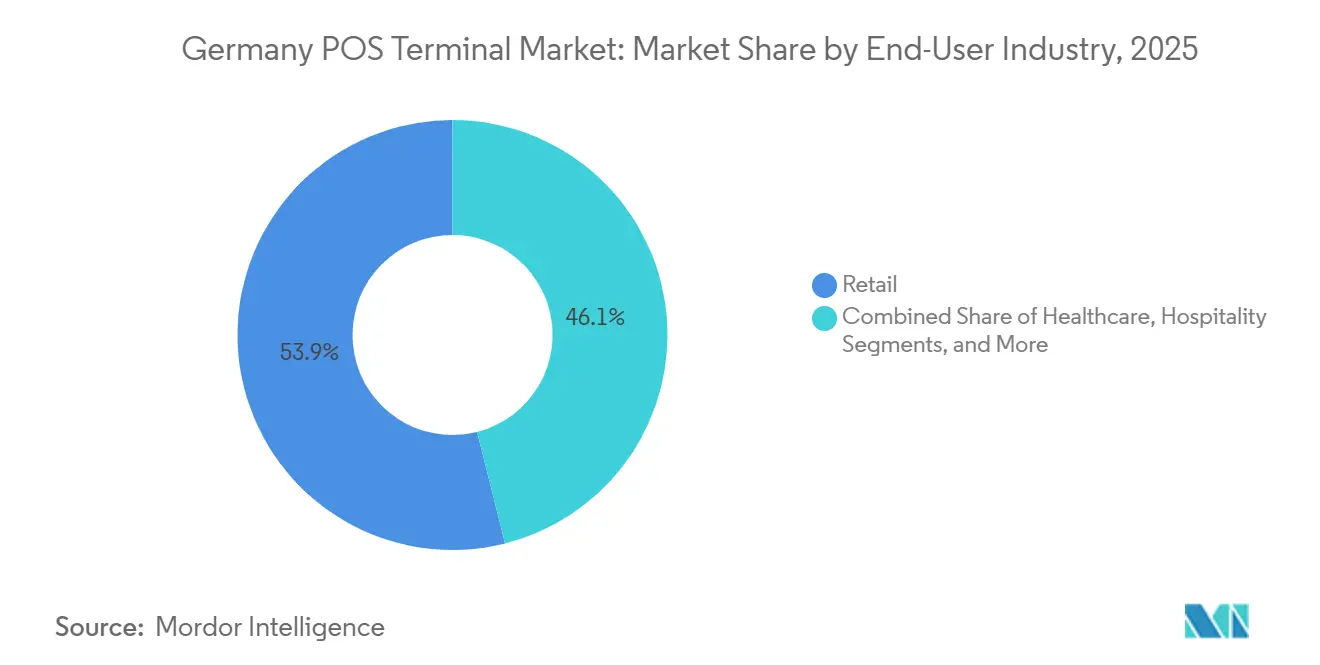

- By end-user industry, retail led with 53.92% revenue share in 2025, while healthcare is projected to post the fastest CAGR at 7.27% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Germany POS Terminal Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Contactless Payment Penetration Exceeding 65% of In-Store Card Spend | +1.8% | National, higher in urban grocery chains | Short term (≤ 2 years) |

| Rapid mPOS Adoption Among SMEs Via Fintech Bundles | +1.5% | National, services and hospitality focused | Medium term (2-4 years) |

| Retail Cloud-POS Refresh Cycle Driven by Software End-of-Life | +1.3% | National, multi-location retailers | Short term (≤ 2 years) |

| Growing Debit Card Transaction Volumes and Girocard Tokenization | +1.0% | National | Medium term (2-4 years) |

| Android Smart POS App Stores Unlocking Value-Added Services | +0.5% | National, early hospitality and transport | Medium term (2-4 years) |

| Digital Euro Readiness Clauses in Retailer RFPs | +0.4% | National, large retail and public sector | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Contactless Payment Penetration Exceeding 65% Of In-Store Card Spend

Contactless transactions made up 87% of girocard payments by December 2024, up from 74% two years earlier, forcing merchants to retire contact-only hardware or risk checkout friction as tap-to-pay becomes the default experience.[1]Deutsche Bundesbank, “Payment Behaviour in Germany in 2024,” bundesbank.de The speed differential, with NFC taps clearing about 30% faster than chip-and-PIN, improves throughput and queue management during peak trading hours. Tokenization upgrades tied to the girocard roadmap demand secure-element support that most pre-2022 devices lack, creating a technical obsolescence cliff. Retailers in grocery, quick-service restaurants, and public transportation therefore front-load capital expenditure to secure BaFin-certified replacements. City-center merchants have reacted quickest, but rural operators are now following as mobile-wallet usage jumped from 5% of card transactions in 2022 to 16% in 2024.[2]European Central Bank, “Study on the Payment Attitudes of Consumers in the Euro Area,” ecb.europa.eu

Rapid mPOS Adoption Among SMEs Via Fintech Bundles

Fintech challengers have bundled card acceptance with invoicing, bookkeeping, and instant cash advances, collapsing perceived hardware cost to zero for micro-businesses. SumUp alone processed more than 1 billion transactions in 2024, proof that penetration has shifted from early adopters to the SME mainstream. Working-capital advances underwritten on payment flow data remove collateral barriers that previously discouraged small retailers from adopting electronic payments. KassenSichV allows cloud-based technical security systems for mobile devices, trimming recertification overhead for itinerant merchants and food-truck operators. The combination of regulatory latitude and bundled finance sharply tilts preference toward portable devices, accelerating the mPOS share-take from fixed lanes.

Retail Cloud-POS Refresh Cycle Driven By Software End-Of-Life

SAP will cease on-premise Commerce support in July 2026, obliging thousands of mid-market retailers to re-platform to cloud environments.[3]PCI Security Standards Council, “PCI DSS v4.0 Requirements and Testing Procedures,” pcisecuritystandards.org Cloud migration necessitates terminals capable of containerized apps, OAuth 2.0 authentication, and remote key injection, none of which legacy devices support. Concurrently, five-year validity windows for TSS certifications issued between 2020 and 2023 expire from 2025 onward, giving retailers limited incentive to extend the life of older hardware. Snabble and other microservices-based providers showcase the economics of decoupling front-end devices from back-office logic, a model that justifies up-front hardware swaps with lower lifetime support spend.

Growing Debit Card Transaction Volumes And Girocard Tokenization

Girocard handled 7.9 billion transactions in 2024, adding 800 million incremental payments year over year. The tokenization program replaces static primary account numbers with single-use tokens, raising cryptographic requirements beyond the capability of many pre-2022 terminals. Cash’s share of point-of-sale transactions slid to 51% in 2023, pushing absolute card volumes higher even as retail sales stayed flat. Co-badged girocard-Visa and girocard-Mastercard products require terminals to juggle multiple authentication protocols, hastening retirement of single-application devices.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cyber-Resilience Costs for PCI DSS v4.0 and NIS2 Compliance | -0.9% | National, heavy on mid-tier acquirers | Short term (≤ 2 years) |

| Rising Scheme Fees on International Debit | -0.6% | National, tourism hubs | Medium term (2-4 years) |

| Shrinking High-Street Footprint Reduces Absolute Terminal Growth | -0.7% | National, department stores | Medium term (2-4 years) |

| Supply-Chain Dependency on Chinese Android ODMs | -0.4% | National, all Android deployments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cyber-Resilience Costs For PCI DSS v4.0 And NIS2 Compliance

Mandatory migration to PCI DSS v4.0 in March 2025 introduced 53 new controls, including continuous vulnerability scanning and encrypted east-west network traffic, driving one-off remediation bills that can surpass USD 500,000 for large payment providers. NIS2, transposed into German law four months earlier, compounds the burden with 24-hour incident reporting, board-level accountability, and potential fines of 2% of global revenue. Mid-market acquirers face a fixed-cost wedge that erodes pricing flexibility, postponing terminal-upgrade budgets and nudging smaller independent sales organizations toward consolidation.

Rising Scheme Fees On International Debit

Although EU interchange caps freeze acquirer-to-issuer fees at 0.2% for debit, they leave scheme fees untouched. Visa and Mastercard have lifted those network charges in several categories by 20-30 basis points since 2020. German merchants in tourism-centric regions like Munich airports and Berlin duty-free shops face margin compression because EU rules bar cardholder surcharging. Retailers delay high-spec terminal rollouts while they lobby for fee transparency or switch traffic to girocard wherever possible.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mode of Payment Acceptance: Contactless Devices Widen Their Lead

Contactless hardware captured 65.29% of the Germany POS terminal market share in 2025 and will outpace contact-based systems at a 6.98% CAGR to 2031. Merchant preference has tilted decisively toward NFC because customer dwell time falls and girocard mandates demand it. The Germany POS terminal market size for contact-based devices is stagnating as their embedded cryptographic modules cannot support token-based authentication.

Capital allocation follows transaction density; grocery chains and urban quick-service restaurants are bulk-ordering Android NFC countertop units, while pop-up retailers deploy Bluetooth-enabled card readers tethered to tablets. Firmware-level tokenization and certified remote key injection insulate contactless devices from compliance obsolescence, ensuring that residual values stay higher at buyback. Consequently, secondary leasing firms are shifting portfolios toward these upgraded assets.

By POS Type: Mobile Form Factors Narrow The Gap With Fixed Lanes

Fixed countertop units still accounted for 59.97% of Germany POS terminal market size in 2025 thanks to entrenched deployments in multi-lane grocery and pharmacy chains. However, the mobile cohort is compounding at 7.54% annually, swelling its share as fintech lenders cover the cost of the reader in return for payment-data underwriting. That economics reshuffle has made portable devices the entry point for many first-time card-accepting merchants.

Hospitality and home-repair services value the all-day battery life and built-in receipt printers of new Android handhelds, while multi-location retailers treat dockable tablets as dual-use inventory-control and checkout stations. The Germany POS terminal market share of fixed hardware will therefore erode gradually, although it will remain critical where cash drawers, barcode scanners, and weigh-scales must be hard-wired.

By End-User Industry: Healthcare Emerges As The Fastest-Rising Vertical

Retail retained 53.92% of market revenue in 2025, but hospitals, clinics, and pharmacies are growing fastest at 7.27% CAGR through 2031 as electronic patient records go live nationwide. Reimbursement workflows now begin chair-side, compelling care providers to embed certified payment modules within electronic medical records.

Telematics infrastructure rules under the German Social Code Book V oblige every healthcare entity to install secure endpoints, for which Android smart-POS offers ready integration. Retail chains, on the other hand, are cycling through third-generation PCI-PTS devices but at a slower unit-growth pace because their square-meter footprint is shrinking even as ticket sizes rise.

Geography Analysis

Germany holds a 1.2 million-unit girocard-compliant terminal base inside a wider euro-area installed count of 20.8 million. BaFin certification layers and Bundesbank scheme oversight raise the entry bar for foreign acquirers, giving established processors pricing latitude in large metropolitan districts where card usage already surpasses 70% of checkout spend.

Regional divergence aligns with tourism intensity and retail density. Bavaria, Berlin, and Hamburg log the highest Visa and Mastercard debit throughput, pushing merchants to adopt multi-scheme devices that interoperate with girocard rails. Rural Saxony and Thuringia lag, retaining elevated cash usage; nonetheless, mobile-wallet acceptance initiatives by regional savings banks are nudging small stores toward low-cost mPOS kits.

Healthcare infrastructure mandates apply uniformly nationwide, but uptake is quickest in North Rhine-Westphalia, which hosts Germany’s largest clinical network. Meanwhile, the looming Digital Euro pilot, slated for 2027, has already appeared as a readiness clause in tender documents from two national retailers headquartered in Hesse. NIS2 and DORA drive acquirer consolidation, with smaller ISOs exiting high-compliance overhead states such as Baden-Württemberg.

Competitive Landscape

Market power is shifting from hardware vendors to vertically integrated payment platforms. Worldline’s February 2026 Ingenico 360 launch bundled fraud scoring, loyalty engines, and dynamic currency conversion in a single subscription, crystallizing the pivot toward recurring software revenue. SumUp’s EUR 285 million (USD 302 million) raise and EUR 1.5 billion (USD 1.59 billion) private-credit facility signaled investor appetite for mPOS models where payments yield ancillary lending and invoicing cash flows.

Verifone and PAX Technology defend share through Android smart-POS app stores that court independent software vendors, although dependency on Chinese ODM firmware exposes them to DORA concentration-risk audits. European makers such as AURES Technologies and Vectron Systems exploit that gap to pitch sovereign-controlled supply chains despite higher unit prices.

Diebold Nixdorf’s 2024 restructuring underscores the peril of hardware-only strategies, prompting a rash of M&A among mid-tier processors seeking scale. As of 2026, the top four suppliers collectively occupy roughly 60% of the installed base, characterizing the Germany POS terminal market as moderately concentrated but primed for further platform-centric consolidation.

Germany POS Terminal Industry Leaders

Verifone Systems Inc.

PAX Technology Limited

NCR Voyix Corporation

Diebold Nixdorf AG

DATECS Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Worldline launched the Ingenico 360 cloud platform and AXIUM device family, embedding real-time fraud scoring and loyalty modules inside Android 12 countertop and portable units.

- December 2025: Worldline agreed to divest its PaymentIQ platform to Incore Invest for about EUR 160 million (USD 170 million) to streamline European acquiring operations.

- December 2024: SumUp raised EUR 285 million (USD 302 million) in a round led by Sixth Street Growth to fund geographic expansion and embedded-finance products.

- December 2024: Vectron Systems and Shift4 rolled out a bundled cloud POS and payment solution for hospitality operators following Shift4’s takeover.

Germany POS Terminal Market Report Scope

Point-of-Sale or POS terminal is a fixed or mobile device that facilitates payments through several modes, including cards with a magnetic stripe (credit, debit, or any other compatible card), near field communication (NFC) technology, or QR codes and other media for mobile and internet banking.

The German POS terminal market is segmented by type (fixed point-of-sale and mobile/portable point-of-sale systems) and end-user (retail, hospitality, and healthcare).

The report includes fixed/EPOS terminals comprising PC-based workstations, namely LAN-available terminals and PC-class Processors that are fully programmable and can transmit data to other devices unrestrictedly.

Further, mobile Terminals include electronic funds terminals such as the countertop, multilane, tablet, handheld terminals, PCI-DSS approved chip & PIN devices, approved chip and signature devices, and mPOS devices. All other systems, such as PC-based systems, PIN pads, etc., are excluded from the scope.

By Mode of Payment Acceptance

| Contact-Based |

| Contactless |

By POS Type

| Fixed Point-of-Sale Systems |

| Mobile and Portable Point-of-Sale Systems |

By End-User Industry

| Retail |

| Hospitality |

| Healthcare |

| Transportation and Logistics |

| Other End-User Industries |

| By Mode of Payment Acceptance | Contact-Based |

| Contactless | |

| By POS Type | Fixed Point-of-Sale Systems |

| Mobile and Portable Point-of-Sale Systems | |

| By End-User Industry | Retail |

| Hospitality | |

| Healthcare | |

| Transportation and Logistics | |

| Other End-User Industries |

Key Questions Answered in the Report

How large is the Germany POS terminal market today?

It reached USD 12.08 billion in 2026 and is on track to hit USD 16.57 billion by 2031.

What is driving the rapid shift to contactless payments in Germany?

Girocard mandates, faster checkout speed, and rising mobile-wallet use pushed contactless penetration to 87% of girocard transactions by end-2024.

Which POS device category is growing fastest?

Mobile and portable terminals are advancing at a 7.54% CAGR through 2031, fueled by fintech-embedded financing.

Why is healthcare becoming an important buyer of POS terminals?

The January 2025 nationwide rollout of electronic patient records requires integrated payment and billing at the point of care.

How do PCI DSS v4.0 and NIS2 affect acquirers?

The two regimes add heavy cyber-resilience costs and continuous monitoring duties, squeezing margins for mid-tier processors.

Who are the leading vendors?

Worldline, Verifone, PAX Technology, and SumUp collectively control about 60% of Germany's installed terminal base.

Page last updated on: