Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

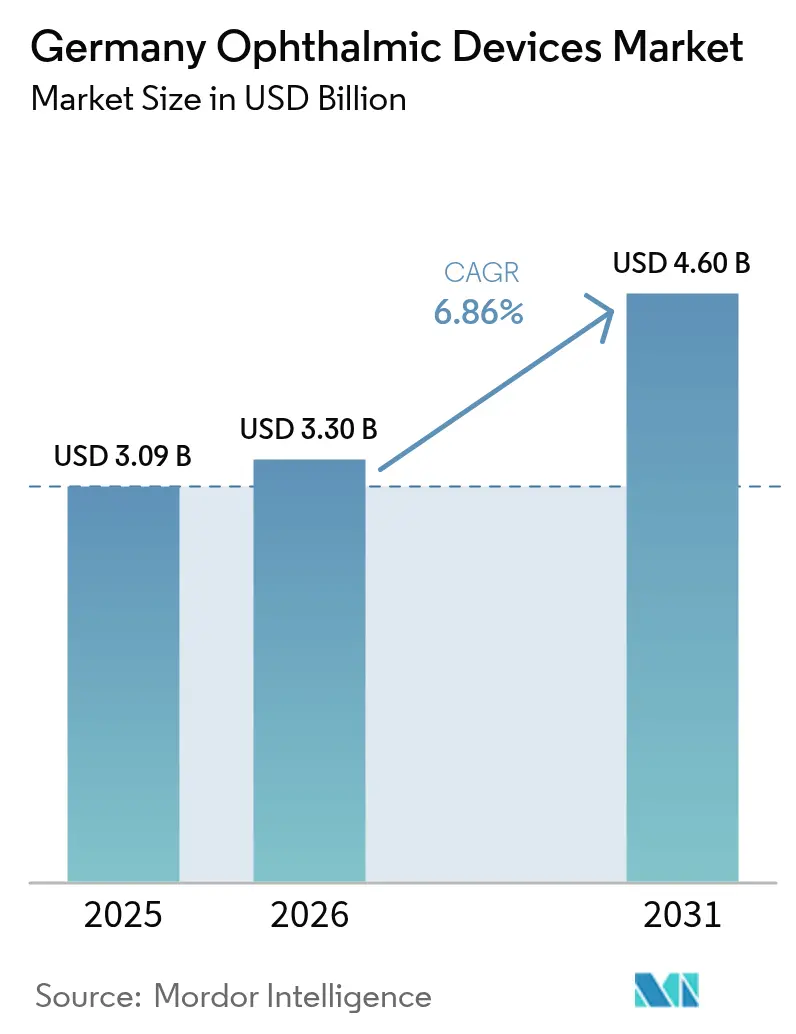

| Base Year Market Size (2025) | USD 3.09 Billion |

| Market Size (2026) | USD 3.3 Billion |

| Market Size (2031) | USD 4.6 Billion |

| Growth Rate (2026 - 2031) | 6.86% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Ophthalmic Devices Market Analysis by Mordor Intelligence

The Germany ophthalmology devices market size is expected to grow from USD 3.09 billion in 2025 to USD 3.3 billion in 2026 and is forecast to reach USD 4.6 billion by 2031 at 6.86% CAGR over 2026-2031. A rapidly ageing population, high digital literacy among clinicians, and the migration of cataract and refractive surgery to ambulatory settings collectively underpin sustained demand across diagnostic, vision-care, and surgical product lines. Device makers are pouring capital into data-enabled platforms that compress diagnostic pathways and into minimally invasive tools that trim operating-room time, insulating order volumes even during macro-economic slow-downs. Payer alignment around DRG incentives and clearer reimbursement for technology add-ons is shortening payback horizons, which attracts small innovators seeking niche opportunities. Although the Germany ophthalmology devices market remains fragmented, suppliers that can bundle consumables, capital equipment, and software are positioned to capture superior margins.

Key Report Takeaways

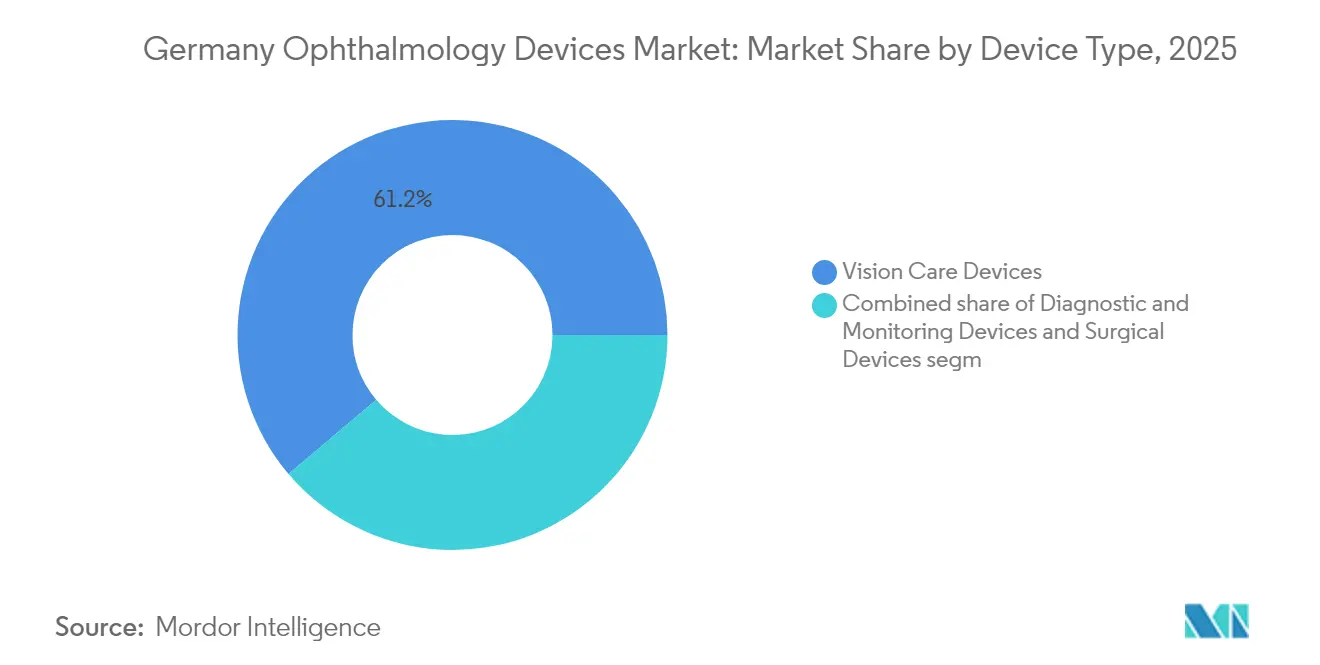

- By device type, vision-care products led with 61.20% Germany ophthalmology devices market share in 2025, while diagnostic platforms registered the highest projected CAGR at 8.2% through 2031.

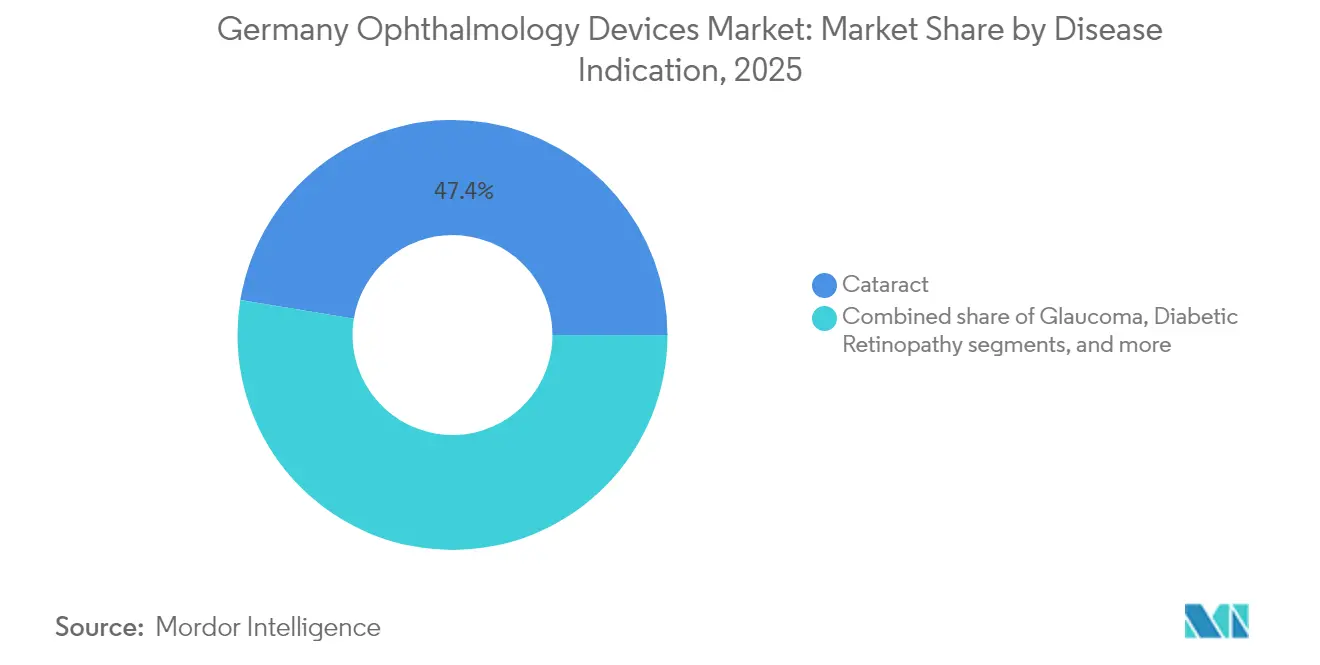

- By disease indication, cataract solutions accounted for 47.40% share of the Germany ophthalmology devices market size in 2025, whereas retinal-disorder devices are forecast to advance at a 8.85% CAGR between 2026-2031.

- By end-user, hospitals held 44.30% of Germany ophthalmology devices market share in 2025, yet ambulatory surgery centres are on track for an 7.95% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Germany Ophthalmic Devices Market Trends and Insights

Driver Impact Analysis*

| Drivers Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising myopia and hyperopia prevalence | +1.9% | Nationwide | Long term (≥ 4 years) |

| DRG expansion for premium IOLs | +1.4% | Nationwide | Medium term (2-4 years) |

| AI-enabled diagnostic accuracy | +1.3% | Urban centres | Short term (≤ 2 years) |

| Shift to ambulatory ophthalmic surgery | +1.1% | Nationwide | Medium term (2-4 years) |

| Germany’s photonics manufacturing cluster accelerating innovation | +0.9% | Berlin-Brandenburg | Medium term (2-4 years) |

| Post-COVID backlog of cataract procedures | +1.2% | Nationwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Demographic Shift – Rising Myopia and Hyperopia Patterns

Studies tracking refractive errors show prevalence rates rising sharply from primary-school age to young adulthood, while hyperopia accelerates in older cohorts. Retailers respond with gender-specific frames and ortho-k lenses that increase repeat purchases without aggressive price hikes. Screen-time proliferation and reduced outdoor activity amplify demand for spectacles, contact lenses, and emerging myopia-control solutions. Vision-care vendors that pair product launches with mobile apps monitoring wear-time see stronger brand loyalty, validating a data-driven upsell strategy. The Germany ophthalmology devices market consequently enjoys a broad, resilient consumer base.

Statutory Health Insurance Reimbursement for Premium IOLs

The October 2024 DRG update added three ophthalmology codes that broaden coverage for advanced IOLs. While monofocal models remain fully reimbursed, multifocal and toric lenses still entail co-payments, tempering immediate uptake. Hospitals therefore pilot adjustable IOLs that can be fine-tuned post-operatively, demonstrating cost-effective visual outcomes. Early adopters report lower re-operation rates, a metric expected to influence future tariff negotiations. Manufacturers using real-world evidence to prove these benefits reinforce the Germany ophthalmology devices market narrative that premium technology aligns with payer value frameworks.

Rapid Uptake of AI-Enabled Diagnostic Platforms

Peer-reviewed data confirm that AI algorithms now achieve perfect sensitivity in diabetic-retinopathy screening and near-perfect accuracy in detecting age-related macular degeneration and glaucoma[1]Skevas C. et al., “Implementing and evaluating a fully functional AI-enabled model for chronic eye disease screening in a real clinical environment,” BMC Ophthalmology, biomedcentral.com. Clinics integrating cloud-based image-analysis suites report shorter patient throughput times, freeing capacity for high-margin vitrectomy and cataract cases. Direct integration with electronic health records simplifies reimbursement audits, nudging insurers toward favourable coverage decisions. The digital maturity of German eye-care therefore fuels recurring software revenues within the Germany ophthalmology devices market.

Expansion of Ambulatory Ophthalmic Surgery Centers

Policy makers are moving cataract and refractive surgery from inpatient wards to accredited ambulatory surgery centres (ASCs), mirroring an EU-wide trend[2]Organisation for Economic Co-operation and Development, “Health at a Glance: Europe 2024,” oecd.org. Surgeons cite reduced anaesthesia needs and smaller incision sizes as enablers of same-day discharge, while private-equity investors scale national ASC networks that co-locate optical retail stores. Competitive pressure prompts hospitals to install compact phaco consoles and single-use packs, lifting order books for suppliers that tailor equipment to lean workflows. This shift helps the Germany ophthalmology devices market capture procedure growth without straining hospital budgets.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Public-fund price ceilings on refractive devices | −1.0% | Nationwide | Medium term (2-4 years) |

| Rural shortage of ophthalmologists | −0.8% | Eastern & Southern Länder | Long term (≥ 4 years) |

| High out-of-pocket cost for premium contact lenses | −0.7% | Nationwide | Short term (≤ 2 years) |

| MDR 2017/745 certification delays for SMEs | −0.9% | Nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Price Pressure from Public Sickness Funds on Refractive Devices

Statutory sickness funds apply tight reference pricing to premium spectacles and accommodative IOLs, compressing manufacturer margins. The looming EU Health Technology Assessment regulation, mandating joint clinical evaluations for high-risk devices from 2025, could elongate market-entry timelines for small firms. Companies equipped with robust real-world evidence may convert the regulatory hurdle into a competitive moat. Nonetheless, persistent cost caps weigh on ASPs, limiting the pricing latitude of the Germany ophthalmology devices market.

Shortage of Ophthalmologists in Rural Bundesländer

OECD data show Germany sharing Europe’s broader healthcare workforce deficit, with rural districts hardest hit. Mobile programmes such as the Eye Van deliver outreach services, yet patchy broadband connectivity hampers tele-ophthalmology deployment. Device makers are therefore re-engineering diagnostic units into ruggedised, portable formats to suit mobile clinics. Until workforce imbalances recede, this gap constrains procedure volumes in underserved areas, capping growth for portions of the Germany ophthalmology devices market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Diagnostic Growth Outpaces, Vision-Care Dominates

Vision-care products accounted for the largest slice of Germany ophthalmology devices market size in 2025, reflecting entrenched purchasing habits and the steady introduction of higher-margin continuous-wear lenses. Retail chains integrating on-site refraction services increase store traffic and boost ancillary accessory sales, further protecting the segment’s 61.20% share. Suppliers deploying myopia-management lenses accompanied by mobile-app compliance trackers raise replacement frequency and reinforce brand stickiness. The coexistence of high-volume spectacles and premium contact-lens materials underscores a dual-track opportunity: volume stability alongside ASP expansion.

Diagnostic and monitoring equipment, though smaller in absolute terms, is forecast to post a high single-digit CAGR from 2026-2031, making it the fastest-growing category. Hospital administrators cite preventive-care guidelines and chronic-disease surveillance targets as drivers for OCT and fundus-camera purchases. A leading lens maker’s acquisition of a Heidelberg-based imaging specialist illustrates how vertical integration pairs screening hardware with personalised lens solutions, enabling seamless data flow from scan to prescription. By closing this loop, vendors sharpen competitive moats and lift wallet share within the Germany ophthalmology devices market.

By Disease Indication: Cataract Still Leads, Retina Surges

Cataract solutions retained the largest Germany ophthalmology devices market share at 47.40% in 2025, mirroring cataract’s status as Europe’s most common surgical intervention. Adjustable IOLs designed to fine-tune refractive outcomes reduce spectacle dependency and elevate patient-reported satisfaction, aligning with payer mandates for measurable benefits. Public tenders increasingly request lens-coating innovations that lower posterior capsule opacification rates, rewarding suppliers able to document long-term efficacy.

Devices addressing diabetic retinopathy and broader retinal disorders are set to deliver the fastest indication-level CAGR at 8.85%, buoyed by Germany’s rising diabetes prevalence. AI-guided imaging catches micro-vascular changes earlier than slit-lamp exams, enabling treatment well before irreversible damage. Pharmaceutical-device combination products, such as sustained-release implants, necessitate handheld scanners to verify placement during follow-ups, thereby selling diagnostics alongside therapeutics. Integration of longitudinal data with reimbursement-linked outcome tracking positions suppliers to capitalise on bundled payments in the Germany ophthalmology devices market.

By End-User: Hospitals Anchor Volume, ASCs Accelerate

Hospitals controlled 44.30% of Germany ophthalmology devices market share in 2025, leveraging large operating budgets to adopt 3D heads-up microscopes and digitally networked phaco consoles. Administrators emphasise cybersecurity-certified platforms that simplify audit trails under Germany’s evolving hospital-financing rules. Service contracts bundling predictive maintenance and on-site staff training provide incremental value, strengthening vendor-hospital relationships.

Ambulatory surgery centres are projected to clock an 7.95% CAGR through 2031, outstripping other facility types. Private-equity investments accelerate ASC roll-outs, and ophthalmology’s predictable cash flows appeal to diversified healthcare portfolios. Laser-vision networks benefit from region-wide marketing campaigns promising transparent pricing and convenient scheduling, enticing younger cohorts who prefer outpatient care. Suppliers offering consumables-leasing models lower upfront costs, rapidly expanding installed bases within the Germany ophthalmology devices market.

Geography Analysis

Southern Bundesländer such as Baden-Württemberg and Bavaria capture a disproportionate share of cataract and refractive surgeries, reflecting higher household incomes and dense provider networks. These regions also host the Berlin-Brandenburg photonics cluster, where over 400 enterprises collaborate with university labs, accelerating prototype-to-trial timelines for corneal lasers and high-resolution imaging systems. Proximity between optics engineers and clinicians allows suppliers to iterate devices quickly, a competitive edge that reverberates across national procurement channels.

Germany’s northern states, including Lower Saxony and Schleswig-Holstein, increasingly channel diabetic-retinopathy screening into mobile outreach programmes run by public insurers. Portable OCT and fundus-camera units designed for rugged conditions witness stronger order volumes in these regions, compensating partially for lower surgical throughput. Insurers stationed here favour AI-enabled triage platforms that reduce unnecessary specialist visits, nudging adoption curves upward within the Germany ophthalmology devices market.

Eastern federal states face pronounced ophthalmologist shortages, as clinician density lags national averages. Tele-ophthalmology pilots show promise yet remain limited by inconsistent broadband, prompting reliance on mobile vans equipped with satellite connectivity. Device manufacturers that tailor compact, battery-operated diagnostic systems gain early-mover advantage. Although procedure counts per capita remain subdued, latent demand suggests a long-term expansion runway once digital infrastructure catches up, offering geographic diversification for participants in the Germany ophthalmology devices market.

Competitive Landscape

Competitive Landscape

Consolidation reshapes the Germany ophthalmology devices industry as multinationals acquire niche imaging and surgical firms to offer end-to-end eye-care pathways. EssilorLuxottica’s 80% stake in Heidelberg Engineering folds diagnostics into its retail empire, capturing recurring revenue streams from screening through spectacle sales. Market observers expect this blueprint to spur similar moves, compelling rivals to forge partnerships or risk ceding integrated-care territory.

Private-equity entry into ASC networks injects operational rigor, emphasising lean workflows and cost discipline. Equipment vendors differentiate by demonstrating measurable efficiency gains, such as reduced phaco-tip energy consumption and auto-calibrated sterile fields. Those who validate claims in real-world settings negotiate multi-year supply deals across growing ASC footprints, stabilising unit demand even as public-tender cycles elongate.

Innovation remains a pillar: ZEISS devotes a notable share of revenue to R&D and expanded its Dresden hub to co-locate optics, software, and data-science teams. Collaboration with pharmaceutical majors links imaging outputs directly to therapeutic decision support, creating platform value that pure-play device firms struggle to replicate. Concurrently, life-science conglomerates dip into device territory—Boehringer Ingelheim’s data partnership with ZEISS exemplifies convergence—as they seek to couple drugs with monitoring hardware. Companies that cultivate data-rich ecosystems thus occupy strategically defensible space in the Germany ophthalmology devices market.

Germany Ophthalmic Devices Industry Leaders

Alcon Inc.

Carl Zeiss Meditec AG

Johnson & Johnson Vision Care

Bausch + Lomb Corp.

Ziemer Ophthalmic Systems AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: ZEISS introduced its artificial-intelligence Research Data Platform, rolling out across selected markets, and emphasised personalised care for chronic retinal diseases. The phased launch includes integration with Boehringer Ingelheim’s clinical data to enhance real-world evidence generation.

- April 2025: Nordic Pharma secured CE Mark for Lacrifill canalicular gel aimed at dry-eye therapy, with German commercial release planned for later in the year. Management anticipates that ophthalmologists will adopt the gel as a non-surgical option before punctal plug placement.

- March 2025: Heidelberg Engineering and DeepEye Medical formed a collaboration to embed advanced artificial-intelligence analysis into diagnostic workflows. The partners expect the joint solution to shorten reading times for high-volume screening programmes.

- October 2024: ZEISS expanded its digital product line with the VisioGen patient-communication tool and the MICOR 700 hand-held lens-removal device. Early hospital feedback highlights user-interface simplicity as a differentiator in crowded tool categories.

- July 2024: EssilorLuxottica signed a definitive agreement to acquire an 80 % stake in Heidelberg Engineering, adding imaging expertise to its portfolio. The move strengthens the group’s end-to-end strategy from diagnosis through eyewear dispensing.

- April 2024: Carl Zeiss Meditec finalised the acquisition of Dutch Ophthalmic Research Center (DORC), enhancing capabilities in vitreoretinal surgery solutions. The integration includes digital workflow tools designed to streamline surgical planning.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Germany ophthalmic devices market as the annual sales value of new diagnostic and monitoring systems, surgical platforms, and vision-care products (frames, lenses, and contact lenses) supplied to hospitals, specialty clinics, optical retailers, and ambulatory surgery centers within Germany. According to Mordor Intelligence, refurbs, rental fleets, drugs, and post-sales consumables are out of scope.

Scope exclusion: Used and refurbished equipment, bare ophthalmic software modules sold without hardware, and pharmaceutical eye-care products remain outside this valuation.

Segmentation Overview

- By Device Type

- Diagnostic & Monitoring Devices

- OCT Scanners

- Fundus & Retinal Cameras

- Autorefractors & Keratometers

- Corneal Topography Systems

- Ultrasound Imaging Systems

- Perimeters & Tonometers

- Other Diagnostic & Monitoring Devices

- Surgical Devices

- Cataract Surgical Devices

- Vitreoretinal Surgical Devices

- Refreactive Surgical Devices

- Glaucoma Surgical Devices

- Other Surgical Devices

- Vision Care Devices

- Spectacles Frames & Lenses

- Contact Lenses

- Diagnostic & Monitoring Devices

- By Disease Indication

- Cataract

- Glaucoma

- Diabetic Retinopathy

- Other Disease Indications

- By End-user

- Hospitals

- Specialty Ophthalmic Clinics

- Ambulatory Surgery Centers (ASCs)

- Other End-users

Detailed Research Methodology and Data Validation

Primary Research

Our analysts interviewed cataract surgeons, clinic procurement heads, optical-chain buyers, and notified-body consultants across Bavaria, North Rhine-Westphalia, and Saxony. The conversations validated prevalence estimates, purchasing cycles, and typical device mark-ups, while short online surveys of contact-lens retailers quantified consumer side volumes.

Desk Research

We began with open datasets, Statistisches Bundesamt procedure counts, the Federal Joint Committee reimbursement schedules, and import codes 9018.50 and 9027.50 from Eurostat customs databases, because they show unit flows and price corridors. Supplementary context came from the German Ophthalmological Society white papers, peer-reviewed studies in Graefe's Archive, and press releases in Dow Jones Factiva. Company 10-Ks and CE-mark certificates helped us map competitive footprints. D&B Hoovers was tapped for revenue splits. These sources illustrate the demand pool, average selling prices, and technology refresh timelines; many other references supported narrower clarification needs.

Market-Sizing and Forecasting

A top-down construct links cataract and refractive-surgery volumes, spectacle penetration, contact-lens adoption, and average device ASPs to derive demand; selective bottom-up roll-ups of leading suppliers and channel checks adjust anomalies before lock-in. Key variables monitored include cataract procedure growth, diabetic-retinopathy screening rates, premium intra-ocular-lens mix, reimbursement tariff shifts, exchange-rate movements, and clinic capacity additions. Multivariate regression with scenario analysis captures how these drivers shape revenues; gaps in sampled ASPs are bridged using hospital tender data and Marklines-style channel intelligence.

Data Validation and Update Cycle

Outputs undergo variance checks against historical import trends and independent prevalence surveys, followed by a multi-analyst review. Reports refresh every twelve months, with interim updates when regulatory or macro events materially alter the baseline; a final pre-publication sweep ensures clients receive the latest vetted view.

Why Our Germany Ophthalmic Devices Baseline Commands Reliability

Published estimates often diverge because firms choose distinct device baskets, currency years, and update rhythms.

Key gap drivers include some publishers capturing only surgical or diagnostic gear, others freezing 2024 prices without adjusting for 2025 tariff uplifts, and several extrapolating EU averages instead of Germany-specific procedure data. Mordor analysts, by contrast, anchor values on verified domestic surgery counts, retailer sell-through volumes, and live ASP tracking, then revisit the file annually.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.09 Bn (2025) | Mordor Intelligence | - |

| USD 1.90 Bn (2024) | Global Consultancy A | Excludes vision-care products and uses static 2024 price deck |

| USD 0.86 Bn (2024) | Trade Journal B | Counts only diagnostic devices; relies on regional sample extrapolation |

Collectively, the comparison shows that when scope breadth, Germany-specific inputs, and annual refresh cadence are harmonized, as in Mordor's approach, the resulting baseline offers decision-makers a balanced, transparent floor for strategic planning.

Key Questions Answered in the Report

What is the current value of the Germany ophthalmology devices market?

The market stands at USD 3.3 billion in 2026 and is forecast to reach USD 4.6 billion by 2031, growing at a 6.86% CAGR.

Which device category leads in unit sales?

Vision-care products, notably spectacles and contact lenses, command 61.20% of market share due to entrenched purchasing habits.

Why are AI-enabled diagnostics gaining traction in Germany?

Peer-reviewed studies show perfect sensitivity for diabetic-retinopathy screening, and clinics adopting these tools shorten patient throughput times, boosting profitability.

How is ambulatory surgery influencing device demand?

The migration of cataract and refractive procedures to ASCs drives demand for compact phaco consoles and single-use packs tailored to lean workflows.

What are the main restraints on market growth?

Price ceilings imposed by public sickness funds on premium refractive devices and a shortage of ophthalmologists in rural regions both exert downward pressure on growth.

Page last updated on: