Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 112.98 Billion |

| Market Size (2026) | USD 116.23 Billion |

| Market Size (2031) | USD 133.88 Billion |

| Growth Rate (2026 - 2031) | 2.88% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Office Real Estate Market Analysis by Mordor Intelligence

The Germany office real estate market size was valued at USD 112.98 billion in 2025 and estimated to grow from USD 116.23 billion in 2026 to reach USD 133.88 billion by 2031, at a CAGR of 2.88% during the forecast period (2026-2031). The European Central Bank (ECB) kept its main rate at 4.5% for most of 2024, tightening loan supply and reshaping investment criteria across commercial property segments. Germany’s economy inched forward, posting 0.2% GDP growth in Q1 2025, yet corporate insolvencies touched a 10-year peak, underscoring latent stress in the business base. Construction output, measured by gross value added, rose 0.9% over the same period despite material-cost inflation running above 15% year on year. The ECB further warns that 72% of euro-area firms, property companies included, are highly exposed to ecosystem-degradation risks, accelerating the push toward sustainable buildings.

Key Report Takeaways

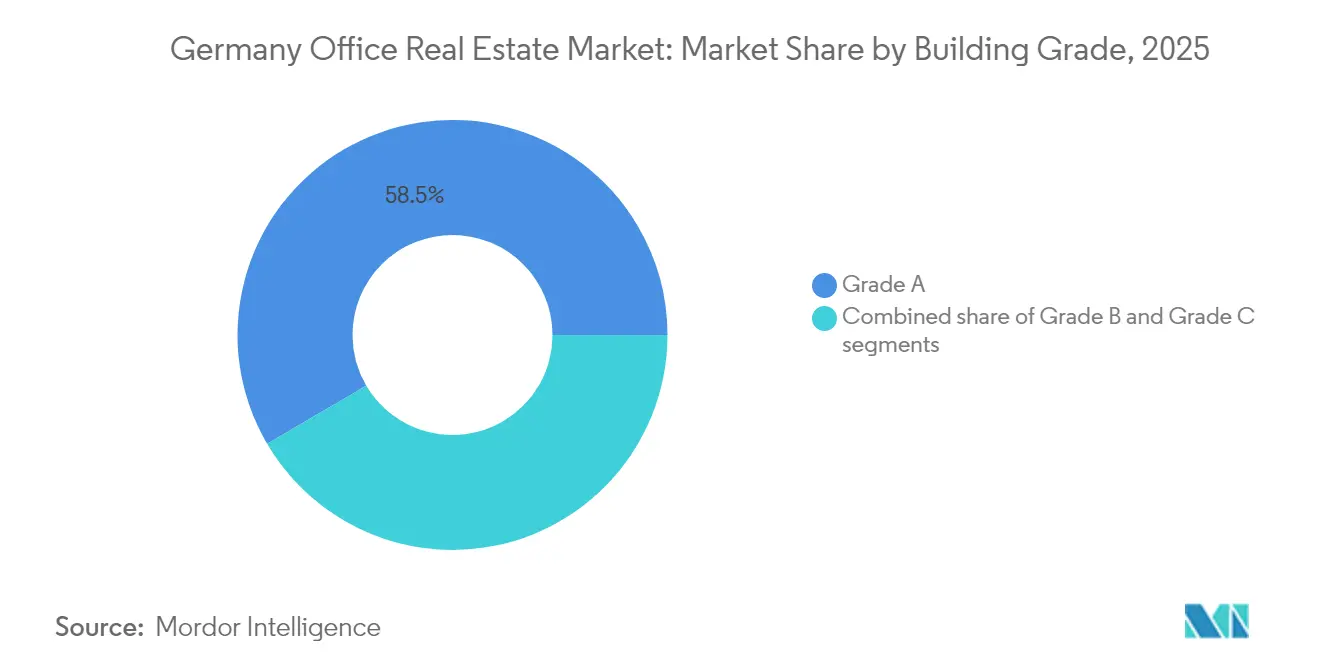

- By building grade, Grade A stock captured 58.45% of Germany office real estate market share in 2025; Grade A is also the fastest-growing grade at a 3.08% CAGR to 2031.

- By transaction type: Rental deals controlled 73.40% of the Germany office real estate market size in 2025, while sales transactions are expanding at a 3.32% CAGR through 2031.

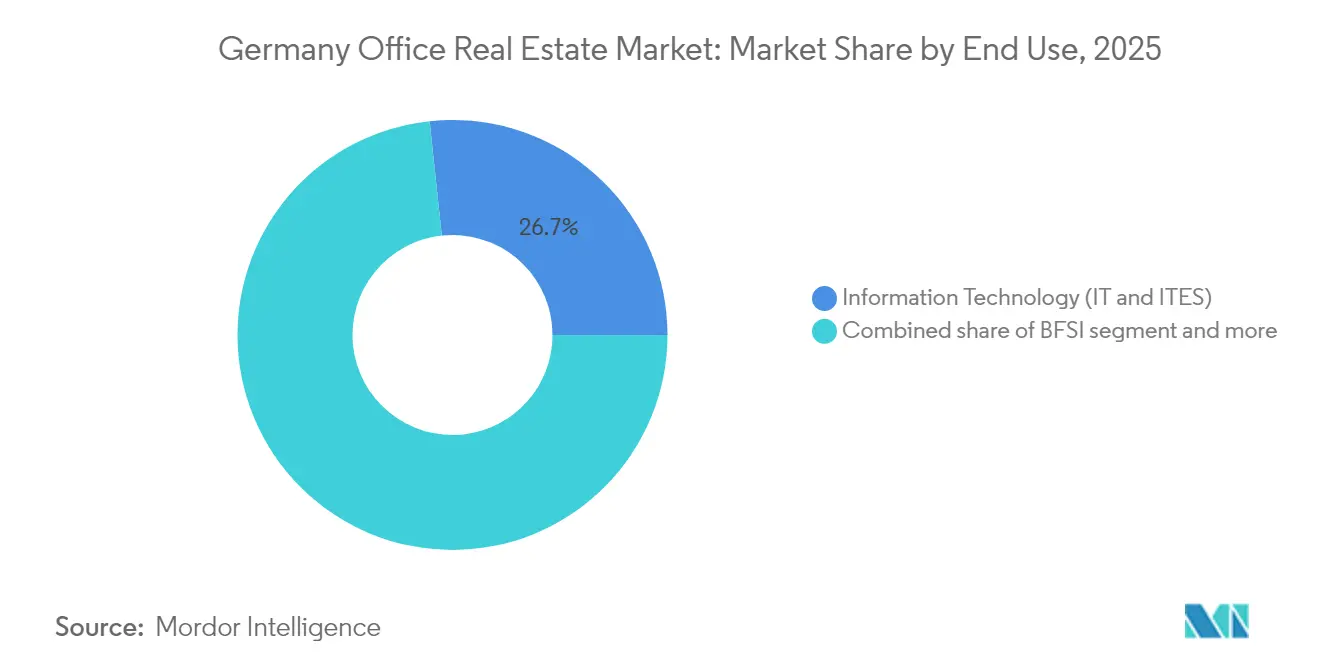

- By end use: Information Technology and IT-enabled services accounted for 26.70% of total demand in 2025 and are advancing at a 3.45% CAGR to 2031.

- By city: Berlin held a leading 22.70% share of the Germany office real estate market size in 2025 and is projected to expand at a 3.25% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Germany Office Real Estate Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Corporate preference for ESG-certified Grade A space | +0.8% | Berlin, Munich, Frankfurt | Medium term (2-4 years) |

| Expansion into secondary business districts | +0.4% | Bonn, Offenbach, Gießen | Long term (≥ 4 years) |

| Government incentives for energy-efficient upgrades | +0.6% | Nationwide | Medium term (2-4 years) |

| Tech-sector absorption in urban hubs | +0.7% | Berlin, Munich, Hamburg | Short term (≤ 2 years) |

| Flexible workspace adoption | +0.3% | Startup-dense cities | Short term (≤ 2 years) |

| Smart-building technology integration | +0.2% | Tier-1 CBDs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing preference for ESG-compliant, high-quality office spaces

As ESG expectations become a cornerstone of corporate occupancy strategy, certified office assets are capturing a growing share of tenant demand. Certified buildings represented 33% of total big-seven city take-up in H1 2024, double the share recorded five years prior. Frankfurt now counts 27% of its inventory as certified, while Munich has grown its certified footprint by 122% since 2019. Banking and financial services groups pursue these assets to satisfy tightening disclosure norms, supporting measurable rent premiums and shorter vacancy cycles. The Germany office real estate market therefore rewards landlords that can prove energy-use transparency and deliver IoT-backed operational metrics. This shift positions ESG-certified buildings as both compliance enablers and high-performance investment assets in the evolving office landscape.

Expansion of office development in emerging urban and secondary business districts

Secondary cities are emerging as strategic destinations for value-seeking office investors and tenants alike. Vacancy in B-cities averages 5.0%, markedly below the 7.1% recorded across A-tier locations. Long-lease public institutions in Bonn and Gießen offer defensive cash flows that offset cyclical stress in CBD portfolios. Cost-conscious corporates increasingly relocate support functions to these cities, while remote work tools reduce the dependency on top-tier addresses. Investors targeting the German office real estate market thus unlock yield premiums without over-exposure to volatile prime rents. This trend marks a decisive broadening of the investment map, driven by structural shifts in workplace location flexibility and financial resilience.

Government-backed incentives promoting energy-efficient building upgrades

Robust policy frameworks are accelerating the decarbonization of Germany’s office inventory through targeted funding mechanisms. Germany’s Federal Funding for Efficient Buildings has mobilized up to USD 86 billion of potential capital since launch, covering as much as 40% of retrofit costs via KfW loans and grants.[1]Federal Ministry for Economic Affairs and Energy, “Federal Funding for Efficient Buildings,” Resulting refurbishments already cut 7.7 million tonnes of CO₂ annually. For the Germany office real estate market, subsidies de-risk deep-green capex, strengthening landlord returns even as EU emission ceilings tighten. As a result, energy efficiency is no longer just a regulatory goal—it’s a viable path to investment-grade returns.[2]Federal Ministry for Economic Affairs and Climate Action, “Efficient Buildings – KfW Subsidy Overview,”

Rising demand from tech and digital-services sectors supporting urban office absorption

Tech-driven occupiers are redefining spatial demand patterns in Germany’s urban office hubs. IT occupiers held 27% of end-user demand in 2024 and continue to outpace traditional finance tenants. Berlin’s start-up scene and Munich’s tech corridor demand scalable, collaboration-ready floors that fuse wired and wireless connectivity. The European Central Bank’s 34,800 m² lease executed in Frankfurt during 2024 underlines how tech-enabled space also appeals to policy institutions seeking hybrid-work compatibility. This growing segment reinforces the value of smart, flexible office formats that support innovation, scalability, and hybrid operations.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher interest rates curbing investment activity | -0.9% | Nationwide, severe in high-value CBDs | Short term (≤ 2 years) |

| Office downsizing in banking and insurance | -0.6% | Frankfurt, Hamburg, Düsseldorf | Medium term (2-4 years) |

| Construction and material cost inflation | -0.5% | Nationwide | Medium term (2-4 years) |

| Rising compliance costs under EU regulation | -0.3% | Older stock nationwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Higher interest rates reducing commercial real estate investment activity

The ECB lifted key rates to 4.5% before a 25 basis-point cut in June 2025, tightening debt terms and weighing on deal flow. Federal Reserve research shows Germany’s manufacturing-heavy economy contracts more sharply than service-centric peers when ECB rates rise, intensifying pressure on office demand. Heightened scrutiny after the Signa collapse forces banks to revalue collateral and build reserves for USD 1.1 trillion in property loans. Insolvency filings climbed 3.3% year on year in April 2025, with creditor claims of USD 9.9 billion in February, further limiting real-estate risk appetite. Office assets appear most vulnerable as values adjust to shifting work patterns and tighter credit.

Office space downsizing in traditional sectors like banking and insurance

Consolidation in legacy sectors is triggering a structural reduction in office space requirements across major German cities. Deutsche Bank’s 3,500-staff reduction in 2024 exemplifies sectoral optimisation. Banks extend leases in situ to avoid relocation expenditure, but they typically sublet or surrender excess area. Insurance carriers mirror the trend, as muted premium growth lowers support-function headcounts. Consequently, landlords in Frankfurt must compete against a rising sub-lease pool, while flex-space providers capture short-cycle overflow. This shift intensifies competition for tenants and undermines long-term absorption in core financial districts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Building Grade: Premium assets set the standard

Grade A captured 58.45% of the Germany office real estate market share in 2025, dwarfing secondary grades. Tenants will continue favouring these assets, propelling the segment at a 3.08% CAGR through 2031. ESG scoring, advanced HVAC automation, and centralised location secure double-digit rent premiums over Grade B stock. Investors unable to finance deep-retrofits on Grade B and Grade C buildings face liquidity risk as regulation accelerates obsolescence.

Flight-to-quality gathered pace in 2024 when corporations linked workspace standards to retention and productivity goals. Smart-building retrofits, ranging from IoT-enabled lighting to AI-driven energy management, now differentiate best-in-class offerings. The Germany office real estate market size for Grade A assets therefore grows both by new construction and by up-cycled conversions, whereas structurally obsolete Grade C floors increasingly pivot toward alternative uses.

By Transaction Type: Rentals dominate while sales gain momentum

Rental contracts represented 73.40% of 2025 transaction value, confirming occupiers’ preference for flexibility in uncertain macro conditions. Yet resurgent investor interest pushes capital-market trades along a 3.32% CAGR path to 2031 as repriced yields lure opportunistic funds. Owner-occupier acquisitions rose to 15% of total deal flow in 2024, signaling corporates’ desire for long-term cost containment.

Distressed disposals and value-add plays form the core of private-equity pipelines, with specialist managers leveraging design-build expertise to harvest green premiums on hand-back. The Germany office real estate market size linked to outright sales will advance as refinancing gaps widen, while the rental sub-market remains the cornerstone of day-to-day occupancy.

By End Use: Technology reshapes demand patterns

Information Technology and IT-enabled services controlled 26.70% of leasing in 2025, the highest single-sector share across the Germany office real estate market. Fast-evolving project cycles and hybrid workflows require adaptable floor plates and robust digital infrastructure. The segment is also the fastest grower at 3.45% CAGR to 2031.

Traditional banking and insurance occupiers downsize core footprints yet intensify demand for smart conference and client-facing zones, blurring boundary lines with flexible-workspace operators. Industrial, life-science, and legal firms now adopt similar agile designs, expanding the total addressable pool for tech-ready stock. Hence, cross-sector competition escalates for prime, digitally-secure, carbon-efficient building.

Geography Analysis

Berlin’s 22.70% share and 3.25% projected CAGR rest on a dual engine of public-sector presence and Europe-leading start-up formation. Major floor plates taken by federal ministries underpin multi-cycle lease stability, while early-stage ventures covet flexible sub-2,000 m² clusters that can scale inside tech-friendly micro corridors. Landlords accelerate mixed-use conversions-PGIM’s 2025 purchase of a mid-rise office for 300 micro-living units is a prime illustration-to integrate residential density within transit nodes.

Munich and Frankfurt remain premium-priced. Munich posted a 29% surge in take-up through 2024, fuelled by global tech firms co-locating R&D and HQ functions in the city’s established innovation spine. Frankfurt’s financial district is navigating rationalised bank footprints against ECB expansion; near-term vacancy spikes foster landlord concessions, but the core bank cluster sustains prime-rent benchmarks. Hamburg’s diversified tenant mix, media, trade logistics, maritime services, keeps vacancy lowest among the big seven, buffering cyclical shocks with sectoral heterogeneity.

Beyond tier-one markets, Düsseldorf, Stuttgart, Cologne, and Hannover capitalise on lower occupancy costs and strong university pipelines. Average purchase prices in these B-cities trail prime CBD deals by 30% yet provide yield premiums of 80–120 bpst. Remote work adoption reduces geographic lock-in, emboldening corporates to pursue distributed-hub real-estate strategies. Consequently, the Germany office real estate market is evolving into a mesh network of specialised city sub-clusters that collectively absorb national demand growth.

Competitive Landscape

The Germany office real estate market displays moderate concentration. International advisers—CBRE, JLL, Cushman & Wakefield—command sizeable advisory mandates by integrating valuation, capital markets, and ESG consulting expertise. Domestic heavyweights such as Union Investment and alstria exploit deep local intel and long-standing municipal ties to lock in early pipeline access. Technology now trumps sheer square-meter control; firms that embed AI-powered asset optimization or blockchain-based lease administration secure strategic advantage.

Consolidation is accelerating. Brookfield’s 2024 buy-out of Alstria and the target’s subsequent REIT delisting highlights how private capital seeks operational turnarounds free from public-market scrutiny. Likewise, Partners Group’s pending takeover of Empira’s USD 15.4 billion project pipeline amplifies institutional appetite for vertically-integrated development capacity. White-space opportunities include office-to-residential conversions; PwC flags 75 million m² of potential stranded office stock primed for mixed-use repositioning.

PropTech alliances proliferate. Siemens teamed with Enlighted and Zumtobel in 2024 to deploy IoT lighting that cuts energy intensity while feeding live data into landlord dashboards. Advisory groups bundle these solutions within end-to-end retrofit offerings, differentiating their German portfolios in tender bids. The German office real estate market, therefore, rewards operators that fuse physical asset control with data-rich, service-oriented platforms.

Germany Office Real Estate Industry Leaders

CBRE

Jones Lang LaSalle IP

Cushman & Wakefield

Savills

Knight Frank

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: The ECB trimmed policy rates by 25 basis points and forecast 0.9% GDP growth for 2025, signalling a modest easing in financing costs for office investors

- May 2025: Alstria Office REIT leased 35,300 m² of new space and renewed 31,000 m² in Q1, keeping its 106-asset portfolio valued at USD 4.62 billion and generating USD 53.9 million in revenue.

- May 2025: Corporate insolvency applications climbed 3.3% year on year in April, with creditor claims of USD 9.9 billion, underscoring financial stress.

- January 2025: Germany logged USD 5.64 billion in 2024 office deals, with USD 1.63 billion closed in Q4, marking a clear uptick in investor appetite for core assets.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

According to Mordor Intelligence, we view the Germany office real estate market as the cumulative value of Grade A, B, and C office buildings that are newly built, refurbished, traded, or leased to corporate, professional-services, public-sector, and technology tenants across all German cities. The valuation reflects asset prices transacted or appraised during the base year rather than annual rental turnover.

Scope exclusion: coworking operator service revenues and mixed-use schemes in which office space accounts for less than half of the gross floor area are left outside the model.

Segmentation Overview

- By Building Grade

- Grade A

- Grade B

- Grade C

- By Transaction Type

- Rental

- Sales

- By End Use

- Information Technology (IT & ITES)

- BFSI (Banking, Financial Services and Insurance)

- Business Consulting & Professional Services

- Other Services (Retail, Lifesciences, Energy, Legal)

- By City

- Berlin

- Munich

- Frankfurt

- Hamburg

- Rest of Germany

Detailed Research Methodology and Data Validation

Primary Research

Interviews were held with valuation surveyors, fund managers, municipal planners, and tenant-representation brokers in Berlin, Munich, Frankfurt, and secondary hubs. These conversations clarified achievable prime yields, energy-efficiency premiums, and likely refurbishment pipelines, letting us refine cost and absorption assumptions that can otherwise drift in desk research.

Desk Research

Our analysts first mapped the market using open datasets such as Destatis construction permits, Deutsche Bundesbank mortgage flows, the European Public Real-Estate Association's capital-value indices, and city-level take-up reports released by IVD and IZ Research. Company filings, listed REIT fact-sheets, and press releases on prime deals helped us gauge prevailing asset prices. We also tapped paid platforms, notably D&B Hoovers for developer financials and Dow Jones Factiva for deal news. These inputs built the foundational supply, demand, and pricing grid; many other public and subscription sources were reviewed for cross-checks.

Market-Sizing & Forecasting

A top-down stock-value reconstruction anchored the model: total completed office stock by city multiplied by average capital value per square meter, adjusted for vacancy and grade mix. Bottom-up sense checks, including developer pipeline roll-ups and sampled prime-rent multiplied by yield back-calculations, tempered any overreach. Key variables include GDP growth, office-using employment, ECB policy rates, prime yield shifts, and ESG retrofit cost trajectories. Forecasts to 2030 rely on multivariate regression, stress-tested through scenario analysis agreed upon with our primary research panel. Data gaps where municipal statistics lag were filled by short-run linear projections that are subsequently overwritten once fresh figures release.

Data Validation & Update Cycle

Before sign-off, senior analysts rerun variance tests against JLL and Cushman vacancy data, ensure currency conversions at the annual average EUR-USD rate, and reconcile any ±5% anomaly. The report is refreshed yearly, with interim updates triggered by rate shocks, tax code changes, or transactions exceeding 2% of baseline value.

Why Mordor's Germany Office Real Estate Baseline Earns Trust

Published estimates often differ; scope, pricing metrics, and refresh cadence rarely align.

Key gap drivers include competitors valuing only rental cash flows, using 2023 exchange rates, or omitting Grade C stock, whereas Mordor chooses full asset value, constant 2024 euros, and a visible grade split.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 112.98 B (2025) | Mordor Intelligence | - |

| USD 27.4 B (2024) | Global Consultancy A | Rental-income lens, excludes owner-occupiers |

| €150 B (2025) | Industry Association B | Includes corporate headquarters yet omits secondary-city stock |

These contrasts show that Mordor's blended stock-plus-transaction approach, city granularity, and annual data sweep provide a balanced, repeatable baseline that decision-makers can rely on.

Key Questions Answered in the Report

What is the current size of the Germany office real estate market?

The market is valued at USD 116.23 billion in 2026 and is projected to rise to USD 133.88 billion by 2031.

Which building grade commands the highest share?

Grade A assets control 58.45% of market share and are growing at a 3.08% CAGR as firms chase ESG compliance and premium amenities.

How have higher ECB interest rates affected investment activity?

Financing costs spiked, flattening prime yields at 4.91% and holding 2024 transaction volume to USD 5.64 billion, but repricing is creating attractive value-add opportunities.

Which sector is driving new leasing demand?

Information Technology and IT-enabled services represent 26.70% of end-user demand and are forecast to grow leasing needs at a 3.45% CAGR.

Why are secondary German cities gaining investor attention?

B-cities offer lower purchase costs, average vacancy of 5.0%, and yield premiums of up to 120 bps compared with A-tier CBDs, making them attractive for diversification.

What role do government incentives play in refurbishment economics?

KfW loans and grants cover up to 40% of retrofit costs, lowering payback periods and driving nationwide upgrades that cut 7.7 million tonnes of CO₂ annually.

Page last updated on: