Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

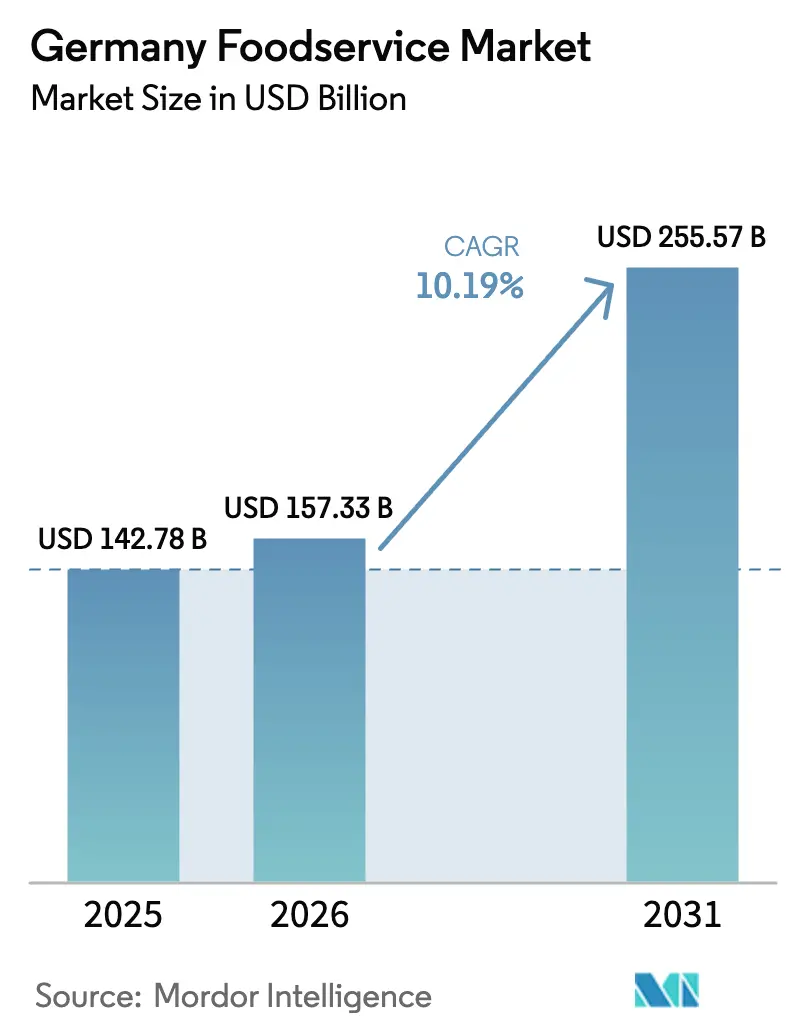

| Base Year Market Size (2025) | USD 142.78 Billion |

| Market Size (2026) | USD 157.33 Billion |

| Market Size (2031) | USD 255.57 Billion |

| Growth Rate (2026 - 2031) | 10.19% CAGR |

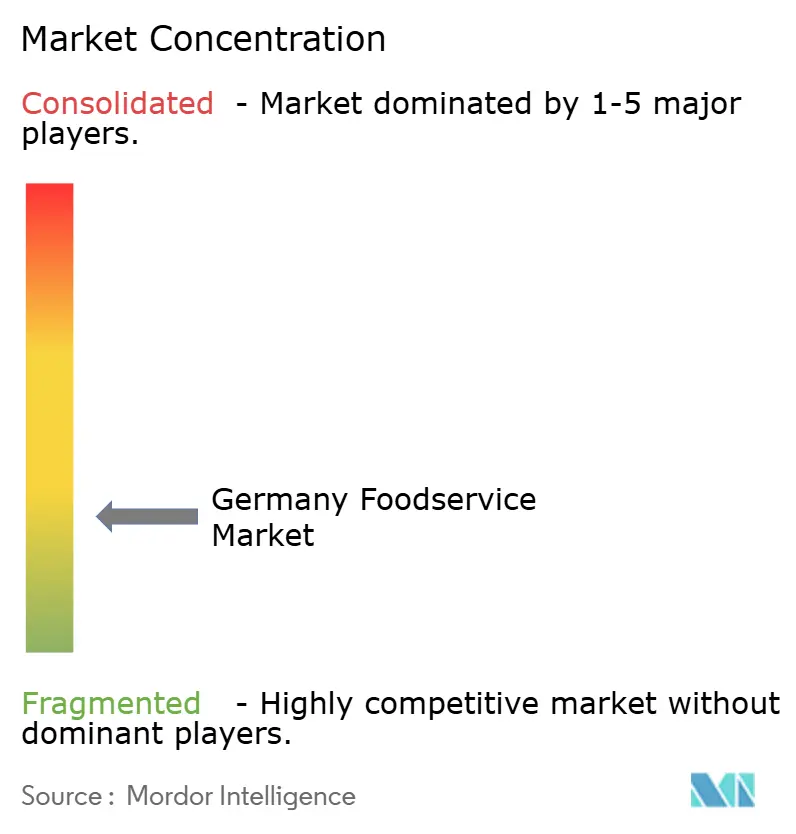

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Germany Foodservice Market Analysis by Mordor Intelligence

The German foodservice market size was valued at USD 142.78 billion in 2025 and estimated to grow from USD 157.33 billion in 2026 to reach USD 255.57 billion by 2031, at a CAGR of 10.19% during the forecast period (2026-2031). This acceleration reflects a structural shift from pandemic-era contraction to sustained recovery, driven by record tourism inflows, rapid digitalization of ordering and payment systems, and evolving consumer preferences toward plant-based and experiential dining formats. Germany recorded 433 million overnight stays between January and October 2024, signaling robust demand for out-of-home consumption[1]Source: Statistics Germany, "Genesis online", destatis.de. Meanwhile, international visitor spending is forecast to reach EUR 57.0 billion in 2025, amplifying foot traffic across cafés, full-service restaurants, and quick-service outlets[2]Source: World Travel & Tourism Council, "Travel and Tourism Economic Impact Research", wttc.org. Structural recovery from pandemic-era contraction, coupled with accelerating digital adoption, record inbound tourism, and rising demand for plant-based and experiential dining, underpins this trajectory.

Key Report Takeaways

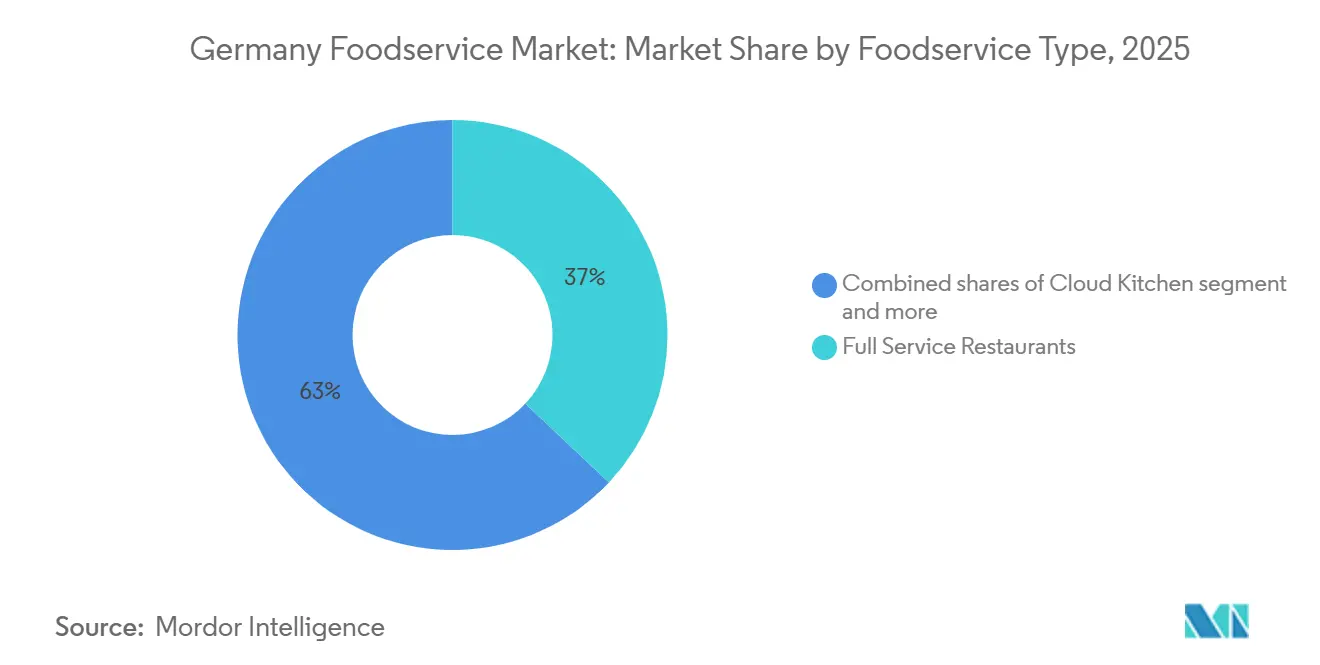

- By foodservice type, full-service restaurants led with 37.03% of Germany foodservice market share in 2025, while cloud kitchens are projected to expand at a 10.71% CAGR through 2031.

- By outlet, independent operators captured 66.25% share of the Germany foodservice market in 2025; chained formats are forecast to grow at a 10.56% CAGR to 2031.

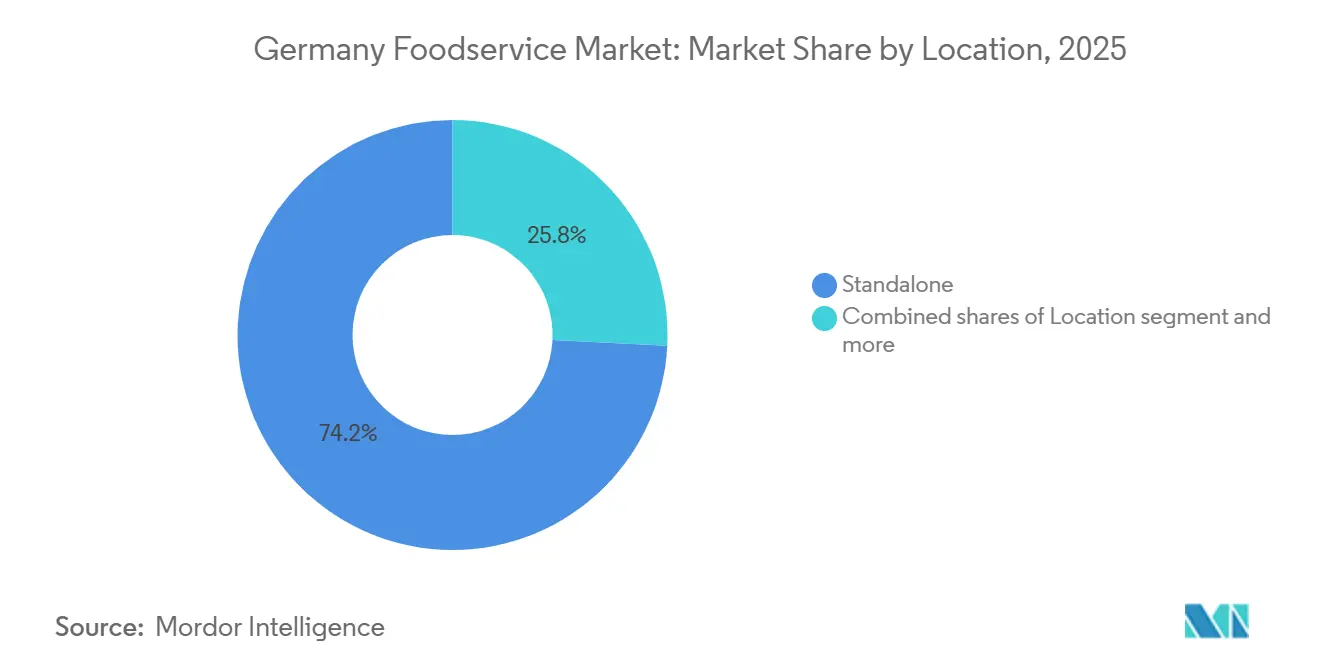

- By locations, standalone venues accounted for 74.21% share of the Germany foodservice market in 2025, whereas travel hubs are set to advance at an 11.05% CAGR.

- By service type, dine-in commanded 54.17% of the Germany foodservice market size in 2025; takeaway is expected to post an 11.33% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Germany Foodservice Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of fast casual and quick-service formats | +1.8% | National, concentrated in urban centers | Medium term (2-4 years) |

| Growth in online food delivery services adoption | +2.1% | National, highest in Berlin, Hamburg, Munich | Short term (≤ 2 years) |

| Strong tourism driving restaurant foot traffic demand | +1.5% | National, peaks in Bavaria, Berlin, Rhine Valley | Short term (≤ 2 years) |

| Technological integration enhancing ordering and service efficiency | +1.3% | National, early adoption in metro areas | Medium term (2-4 years) |

| Social dining experiences boosting out-of-home eating | +1.2% | National, urban millennials and Gen Z | Long term (≥ 4 years) |

| Greater focus on plant-based and wellness menus | +1.4% | National, strongest in Berlin, Stuttgart, Frankfurt | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion of Fast Casual and Quick-Service Formats

Quick-service and fast-casual chains are deploying capital-efficient formats (drive-thrus, kiosks, and modular units) to capture convenience-driven demand without the overhead of full-service real estate. McDonald's Deutschland opened 25 new outlets in 2024 and plans to add 75 restaurants annually from 2025 through 2027, targeting a total of 500 new locations and creating over 10,000 jobs. Yum! Brands operates 240 restaurants in Germany as of 2024, including 180 KFC, 42 Pizza Hut, and 18 Taco Bell, with KFC Deutschland generating millions in operating profit. The shift toward smaller footprints and digital ordering reduces labor intensity while accelerating table turnover, enabling operators to serve higher transaction volumes per square meter. This format proliferation is particularly pronounced in secondary cities where real estate costs remain lower, yet disposable incomes are rising in tandem with remote-work migration.

Growth in Online Food Delivery Services Adoption

The rapid growth in the adoption of online food delivery services is a key driver of the Germany foodservice market, reshaping how consumers access meals and pushing overall industry expansion. As more Germans prefer ordering meals through apps and platforms like Lieferando, Uber Eats, and others, digital channels are capturing a larger share of foodservice consumption, especially in urban areas where convenience and time savings are prioritized. This shift boosts revenue for delivery platforms and encourages traditional restaurants to partner with or integrate delivery services, expanding their reach and customer base. Strong smartphone and internet penetration, along with user-friendly interfaces, real-time tracking, and contactless payments, have further encouraged consumer adoption and repeat usage. As a result, the online food delivery segment is growing at significant CAGR rates, contributing notable value additions to the broader foodservice market and prompting innovation such as cloud kitchens and AI-enabled logistics to meet demand.

Strong Tourism Driving Restaurant Foot Traffic Demand

Germany's tourism sector rebounded to record levels in 2024, with 433 million overnight stays recorded from January through October, surpassing pre-pandemic benchmarks. The World Travel & Tourism Council forecasts international visitor spending of EUR 57.0 billion in 2025, alongside domestic spending of EUR 425.0 billion, creating sustained demand for cafés, full-service restaurants, and travel-hub outlets. Bavaria, Berlin, and the Rhine Valley capture disproportionate shares of international arrivals, driving occupancy and check sizes in those regions. Notably, tourism's multiplier effect extends beyond hotels: visitors allocate approximately 30% of their trip budgets to food and beverage, amplifying revenue for standalone and leisure-location operators. This dynamic is particularly evident in travel-segment foodservice, where airports and train stations are expanding F&B footprints to monetize dwell time. SSP Group, a travel-concession specialist, opened multiple Starbucks locations at Berlin Brandenburg Airport in 2024, capitalizing on passenger throughput recovery.

Technological Integration Enhancing Ordering and Service Efficiency

Automation and AI are migrating from back-office analytics into customer-facing and kitchen operations, enabling operators to reduce labor dependency while improving throughput. EuroCIS 2025 featured a dedicated Food Service Innovation Hub showcasing AI-driven menu boards, robotic kitchen assistants, and self-ordering terminals. REWE Group announced plans to pilot the CA-1 autonomous kitchen robot in autumn 2025, capable of preparing meals without human intervention, addressing both labor shortages and consistency challenges. German startups such as VisioLab, ventopay, and Smoothr are deploying computer-vision checkout, contactless payment, and AI-powered inventory management, respectively, reducing friction at peak hours. These technologies also generate granular data on customer preferences, enabling dynamic pricing and personalized promotions. The convergence of hardware and software platforms is lowering the total cost of ownership for mid-sized chains, democratizing access to tools previously reserved for multinational franchises.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from packaged and ready-to-eat foods | -1.4% | National, strongest in urban convenience retail | Short term (≤ 2 years) |

| High operational complexity for compliance requirements | -0.9% | National, acute in contract catering | Long term (≥ 4 years) |

| Increasing costs of ingredients and supplies | -1.6% | National, volatile for coffee, cocoa, beef | Short term (≤ 2 years) |

| Persistent labor shortages in foodservice operations | -1.8% | National, severe in Bavaria, Baden-Württemberg | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Competition from Packaged and Ready-to-Eat Foods

Retail gastronomy and frozen convenience meals are capturing share from traditional foodservice by offering speed, price transparency, and portion control. Out-of-home frozen sales alone generated billions, reflecting the penetration of ready-to-heat options in convenience stores and supermarkets. Meal-kit e-Commerce is forecast to grow in 2025, growing at a double-digit CAGR through 2029, as consumers seek restaurant-quality ingredients with at-home preparation flexibility. Retail gastronomy, prepared meals sold in supermarkets, is projected to rise in 2024. This channel offers lower price points and eliminates tipping, service waits, and parking hassles, appealing to budget-conscious and time-starved consumers. Foodservice operators must differentiate through experiential elements, customization, and loyalty programs that packaged goods cannot replicate.

High Operational Complexity for Compliance Requirements

Germany's Food and Nutrition Strategy, published in 2024, imposes sweeping mandates on public-sector catering, requiring adherence to German Nutrition Society standards by 2030, a 30% organic ingredient threshold, and reformulation targets for salt, sugar, and saturated fats [3]Source: Federal Ministry of Agriculture, Food and Regional Identity, "Food and Nutrition Strategy", bmleh.de. Contract catering operators serving schools, hospitals, and government facilities must overhaul procurement, menu engineering, and supplier audits to meet these benchmarks, incurring upfront capital and training costs. The strategy also targets a 50% reduction in food waste by 2030, with out-of-home consumption accounting for 1.9 million tonnes of annual waste, 17% of Germany's total. Operators must invest in demand forecasting, portion optimization, and donation logistics to comply, diverting resources from expansion and innovation. Smaller independent outlets lack the scale to absorb these compliance costs, potentially accelerating consolidation as chains leverage centralized procurement and standardized processes to achieve regulatory efficiency.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Foodservice Type: Cloud Kitchens Outpace Traditional Formats

Full-service restaurants held 37.03% of market share in 2025, anchored by Germany's dining culture that prizes table service, ambiance, and multi-course meals. However, cloud kitchens are expanding at 10.71% CAGR through 2031, the fastest rate among all foodservice types, as operators shed front-of-house real estate to focus on delivery-optimized production. Keatz, a Berlin-based B2B2C cloud kitchen, secured EUR 10 million in Series A funding in June 2024 from Vorwerk Ventures and Cavalry Ventures, targeting corporate catering with scalable meal-prep infrastructure. Delivery Hero operates ghost kitchens across Germany under its Kitchen brand, leveraging its aggregator platform to channel orders directly to production hubs.

Quick-service restaurants, encompassing bakeries, burger chains, pizza outlets, and ice cream parlors, benefit from drive-thru and kiosk formats that reduce labor intensity while maintaining high transaction volumes. Cafés and bars, spanning specialist coffee shops, juice bars, and pubs, cater to social and convenience occasions, with Starbucks expanding in travel hubs and Coffee Fellows maintaining a network of urban locations. Full-service restaurants face margin pressure from ingredient inflation and labor shortages, prompting some operators to introduce hybrid models that combine dine-in with takeaway and delivery to maximize asset utilization.

By Outlet: Chained Formats Gain Ground on Independents

Independent outlets commanded 66.25% of market share in 2025, reflecting Germany's tradition of family-owned restaurants, regional cuisine specialists, and neighborhood cafés. Yet chained outlets are projected to grow at a 10.56% CAGR through 2031, driven by multinational franchises that deploy standardized menus, centralized procurement, and digital ordering systems to achieve economies of scale. Yum! Brands operates 240 restaurants in Germany, including 180 KFC, 42 Pizza Hut, and 18 Taco Bell, with KFC Deutschland generating millions in operating profit in 2024.

AmRest Holdings, which franchises KFC, Pizza Hut, and Starbucks across Central Europe, opened 51 new restaurants in H1 2024 and achieved significant digital sales penetration. Chains leverage brand recognition, loyalty apps, and aggregator partnerships to capture delivery demand, while independents compete on authenticity, localized menus, and personalized service. The labor shortage disproportionately affects independents, which lack the training infrastructure and wage-setting power of chains, accelerating consolidation as smaller operators exit or sell to regional groups. Burger King Deutschland operates over 750 locations, while regional chains such as Hans im Glück and Nordsee maintain 100-plus outlets each, occupying the middle ground between independents and global franchises.

By Locations: Travel Hubs Capture Mobility Recovery

Standalone locations accounted for 74.21% of market share in 2025, encompassing street-front restaurants, suburban outlets, and neighborhood cafés that serve residential and office catchments. Travel locations, airports, train stations, and highway rest stops are growing at 11.05% CAGR through 2031, the fastest rate among location types, as passenger throughput rebounds to pre-pandemic levels and dwell times lengthen due to security protocols and flight delays. SSP Group, a travel-concession specialist, opened multiple Starbucks locations at Berlin Brandenburg Airport in 2024, capitalizing on international and domestic passenger growth.

Germany recorded 433 million overnight stays from January through October 2024, amplifying demand for travel-hub foodservice. Leisure locations, theme parks, museums, and entertainment venues benefit from experiential spending, while lodging-based outlets in hotels and resorts cater to captive audiences. Retail locations, including food courts and in-store cafés, are integrating autonomous kitchen robots and self-checkout systems to reduce labor dependency; REWE Group will pilot the CA-1 robot in autumn 2025. Standalone operators face intensifying competition from delivery aggregators and retail gastronomy, prompting some to adopt hybrid models that combine dine-in, takeaway, and third-party delivery to maximize revenue per square meter.

By Service Type: Takeaway Gains on Dine-In Dominance

Dine-in service represented 54.17% of market share in 2025, anchored by Germany's social dining culture and the experiential premium consumers assign to table service, ambiance, and multi-course meals. Takeaway is projected to grow at 11.33% CAGR through 2031, the fastest rate among service types, as delivery habits formed during lockdowns persist and Gen Z consumers prioritize convenience over sit-down occasions. Delivery, encompassing third-party aggregators and proprietary apps, benefits from Lieferando's dominant market position.

Yum! Brands reported that digital sales accounted for the majority of its international system sales in Q3 2024, reflecting the embedding of aggregator and proprietary apps into consumer routines. Solo dining now accounts for a significant share of full-service restaurant visits, indicating a shift toward individual consumption in public spaces. Operators are optimizing packaging for delivery, negotiating commission structures with aggregators, and deploying ghost kitchens to bypass front-of-house costs. Dine-in remains resilient among affluent and experience-seeking demographics, with fine-dining concepts embedding storytelling, multisensory presentations, and nostalgia-driven plating to justify premium pricing.

Competitive Landscape

Germany's foodservice market remains fragmented, as independent operators and regional chains coexist alongside multinational franchises, creating white space for disruptors targeting niche dietary preferences, hyper-local delivery, and experience-led concepts. Multinational chains such as McDonald's, Yum! Brands, Starbucks, Burger King, and Domino's deploy standardized menus, centralized procurement, and digital ordering systems to achieve economies of scale, while independents compete on authenticity, localized menus, and personalized service. Contract catering operators such as Compass Group, Sodexo, Elior, and Aramark are embedding digital platforms to streamline corporate and institutional feeding.

Keatz, a Berlin-based B2B2C cloud kitchen, secured EUR 10 million in Series A funding in June 2024 from Vorwerk Ventures and Cavalry Ventures, targeting corporate catering with scalable meal-prep infrastructure. This low concentration enables smaller contenders to unsettle incumbents by leveraging technology, localized sourcing, and omnichannel fulfillment. Strategic patterns include the deployment of ghost kitchens to bypass front-of-house costs, the integration of AI-driven menu optimization and robotic kitchen assistants to reduce labor dependency, and the embedding of loyalty apps and aggregator partnerships to capture delivery demand.

REWE Group will pilot the CA-1 autonomous kitchen robot in autumn 2025, capable of preparing meals without human intervention, addressing both labor shortages and consistency challenges. Operators that proactively reformulate menus to meet the Federal Ministry of Agriculture, Food and Regional Identity's 2030 mandates (30% organic ingredients, reduced salt and sugar, and a 50% food-waste reduction) will mitigate compliance risk and appeal to health-conscious demographics. Opportunities include hyper-local delivery networks that bypass aggregator commissions, plant-based quick-service formats targeting flexitarian consumers, and travel-hub concessions that monetize mobility recovery.

Germany Foodservice Industry Leaders

-

AmRest Holdings SE

-

McDonald's

-

Burger King Deutschland GmbH

-

Yum! Brands, Inc.

-

Coop Gruppe Genossenchaft

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Collins Foods announced intentions to expand KFC operations in Germany by opening 40–70 new KFC restaurants over five years (adding to its existing footprint), focusing on under-penetrated urban regions such as North Rhine-Westphalia and Baden-Württemberg.

- May 2024: U.S. doughnut and coffee chain Krispy Kreme signed a franchise agreement with ISH Foods to launch in the traditionally bakery-focused German market, with its first store planned in Berlin in early 2025, marking a notable QSR/retail foodservice expansion.

Germany Foodservice Market Report Scope

Foodservice refers to the business of preparing, serving, and selling ready-to-eat food and drinks for immediate consumption, encompassing diverse establishments like restaurants, cafes, catering, and institutions, focusing on providing meals outside the home for profit or service. The Germany foodservice market is segmented by foodservice type, outlet, service type, and location. By foodservice type, the market is segmented into cafes and bars, cloud kitchen, full-service restaurants, quick service restaurants and more. By outlet, the market is segmented into chained outlets and independent outlets. By location, the market is segmented into leisure, lodging, retail, standalone, and more. By service type, the market is segmented into takeaway, delivery and more. The market forecasts are provided in terms of value (USD).

By Foodservice Type

| Café and Bars | By Cuisine | Bars and Pubs |

| Café | ||

| Juice/Smoothie/Desserts Bars | ||

| Specialist Coffee and Tea Shops | ||

| Cloud Kitchen | ||

| Full Service Restaurants | By Cuisine | Asian |

| European | ||

| Latin American | ||

| Middle Eastern | ||

| North American | ||

| Other FSR Cuisines | ||

| Quick Service Restaurants | By Cuisine | Bakeries |

| Burger | ||

| Ice Cream | ||

| Meat-based Cuisines | ||

| Pizza | ||

| Other QSR Cuisines |

By Outlet

| Chained Outlets |

| Independent Outlets |

By Locations

| Leisure |

| Lodging |

| Retail |

| Sandalone |

| Travel |

By Service Type

| Dine-in |

| Takeaway |

| Delivery |

| By Foodservice Type | Café and Bars | By Cuisine | Bars and Pubs |

| Café | |||

| Juice/Smoothie/Desserts Bars | |||

| Specialist Coffee and Tea Shops | |||

| Cloud Kitchen | |||

| Full Service Restaurants | By Cuisine | Asian | |

| European | |||

| Latin American | |||

| Middle Eastern | |||

| North American | |||

| Other FSR Cuisines | |||

| Quick Service Restaurants | By Cuisine | Bakeries | |

| Burger | |||

| Ice Cream | |||

| Meat-based Cuisines | |||

| Pizza | |||

| Other QSR Cuisines | |||

| By Outlet | Chained Outlets | ||

| Independent Outlets | |||

| By Locations | Leisure | ||

| Lodging | |||

| Retail | |||

| Sandalone | |||

| Travel | |||

| By Service Type | Dine-in | ||

| Takeaway | |||

| Delivery | |||

Market Definition

- FULL-SERVICE RESTAURANTS - A foodservice establishment where customers are seated at a table, give their order to a server and are served food at a table.

- QUICK SERVICE RESTAURANTS - A foodservice establishment that provides customers convenience, speed, and food offerings at lower prices. Customers usually help themselves and carry their own food to their tables.

- CAFES & BARS - A type of foodservice business that include bars and pubs that are licensed to serve alcoholic drinks for consumption, cafes that serve refreshments and light food items, as well as specialty tea and coffee shops, dessert bars, smoothie bars, and juice bars.

- CLOUD KITCHEN - A foodservice business that utilizes a commercial kitchen for the purpose of preparing food for delivery or takeout only, with no dine-in customers.

| Keyword | Definition |

|---|---|

| Albacore Tuna | It is one of the smallest species of tuna found in the six distinct stocks known globally in the Atlantic, Pacific, and Indian oceans, as well as the Mediterranean Sea. |

| Angus beef | It is beef derived from a specific breed of cattle indigenous to Scotland. It requires certification from the American Angus Association to receive the "Certified Angus Beef" quality mark. |

| Asian cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Chinese, Indian, Korean, Japanese, Bengali, Southeast Asian, etc. |

| Average Order Value | It is the average value of all orders made by the customers at a foodservice establishment. |

| Bacon | It is salted or smoked meat that comes from the back or sides of a pig. |

| Bars & Pubs | It is a drinking establishment that is licensed to serve alcoholic drinks for consumption on the premises. |

| Black Angus | It is beef derived from a black-hided breed of cows that don't have horns. |

| BRC | British Retail Consortium |

| Burger | It is a sandwich consisting of one or more cooked beef patties, placed inside a sliced bread roll or bun roll. |

| Café | It is a foodservice establishment serving various refreshments (mainly coffee) and light meals. |

| Cafes & Bars | It is a type of foodservice business that include bars and pubs that are licensed to serve alcoholic drinks for consumption, cafes that serve refreshments and light food items, as well as specialty tea and coffee shops, dessert bars, smoothie bars, and juice bars. |

| Cappuccino | It is an Italian coffee drink that is traditionally prepared with equal parts double espresso, steamed milk, and steamed milk foam. |

| CFIA | Canadian Food Inspection Agency |

| Chained Outlet | It refers to a foodservice establishment that shares brands, operates in several locations, has central management, and standardized business practices. |

| Chicken Tender | It refers to chicken meat prepared from the pectoralis minor muscles of a chicken bird. |

| Cloud Kitchen | It is a foodservice business that utilizes a commercial kitchen for the purpose of preparing food for delivery or takeout only, with no dine-in customers. |

| Cocktail | It is an alcoholic mixed drink made with either a single spirit or a combination of spirits, mixed with other ingredients such as juices, flavored syrups, tonic water, shrubs, and bitters. |

| Edamame | It is a Japanese dish prepared with soybeans (harvested before they ripen or harden) and cooked in its pod. |

| EFSA | European Food Safety Authority |

| ERS | Economic Research Service of the USDA |

| Espresso | It is a concentrated form of coffee, served in shots. |

| European cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Italian, French, German, English, Dutch, Danish, etc. |

| FDA | Food and Drug Administration |

| Fillet Mignon | It is a cut of meat taken from the smaller end of the tenderloin. |

| Flank Steak | It is a cut of beef steak taken from the flank, which lies forward of the rear quarter of a cow. |

| Foodservice | It refers to the part of the food industry which includes businesses, institutions, and companies which prepare meals outside the home. It includes restaurants, school and hospital cafeterias, catering operations, and many other formats. |

| Franks | Also known as frankfurter or Würstchen, it is a type of highly seasoned smoked sausage popular in Austria and Germany. |

| FSANZ | Food Standards Australia New Zealand |

| FSIS | Food Safety and Inspection Service |

| FSSAI | Food Safety and Standards Authority of India |

| Full service restaurant | It refers to a foodservice establishment where customers are seated at a table, give their order to a server, and are served food at a table. |

| Ghost Kitchen | It refers to a cloud kitchen. |

| GLA | Gross Leasable Area |

| Gluten | It is a family of proteins found in grains, including wheat, rye, spelt, and barley. |

| Grain-fed beef | It is beef derived from cattle that have been fed a diet supplemented with soy and corn and other additives. Grain-fed cows can also be given antibiotics and growth hormones to fatten them up more quickly. |

| Grass-fed beef | It is beef derived from cattle that have only been fed grass as feed. |

| Ham | It refers to the pork meat taken from the leg of a pig. |

| HoReCa | Hotels, Restaurants and Cafes |

| Independent Outlet | It refers to a foodservice establishment that operates with a single outlet or is structured as a small chain with no more than three locations. |

| Juice | It is a drink made from the extraction or pressing of the natural liquid contained in fruit and vegetables. |

| Latin American | It includes full-service offerings in restaurants that serve cuisines from cultures such as Mexican, Brazilian, Argentinian, Colombian, etc. |

| Latte | It is a milk-based coffee that is made up of one or two shots of espresso, steamed milk, and a thin layer of frothed milk. |

| Leisure | It refers to foodservice offered as a part of a recreation business, such as sports arenas, zoos, movie theaters, and museums. |

| Lodging | It refers to foodservice offerings at hotels, motels, guesthouses, holiday homes, etc. |

| Macchiato | It is an espresso coffee drink with a small amount of milk, usually foamed. |

| Meat-based cuisines | This inlcudes food items like fried chicken, steak, ribs, etc. where meat is the primary ingredient for the dish. |

| Middle Eastern cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Arabic, Lebanese, Iranian, Israeli, etc. |

| Mocktail | It is an non-alcoholic mixed drink. |

| Mortadella | It is a large Italian sausage or luncheon meat made of finely hashed or ground heat-cured pork, which incorporates at least 15% small cubes of pork fat. |

| North American | It includes full-service offerings in restaurants that serve cuisines from cultures such as American, Canadian, Caribbean, etc. |

| Pastrami | It refers to a highly seasoned smoked beef, typically served in thin slices. |

| PDO | Protected Designation of Origin: It is the name of a geographical region or specific area that is recognized by official rules to produce certain foods with special characteristics related to location. |

| Pepperoni | It is an American variety of spicy salami made from cured meat. |

| Pizza | It is a dish made typically of flattened bread dough spread with a savory mixture usually including tomatoes and cheese and often other toppings and baked. |

| Primal cuts | It refers to the major sections of the carcass. |

| Quick service restaurant | It refers to a foodservice establishment that provides customers convenience, speed, and food offerings at lower prices. Customers usually help themselves and carry their own food to their tables. |

| Retail | It refers to a foodservice outlet inside a mall. shopping complex or a commercial real estate building, where there are other businesses operating as well. |

| Salami | It is a cured sausage consisting of fermented and air-dried meat. |

| Saturated fat | It is a type of fat in which the fatty acid chains have all single bonds. It is generally considered unhealthy. |

| Sausage | It is a meat product made of finely chopped and seasoned meat, which may be fresh, smoked, or pickled and which is then usually stuffed into a casing. |

| Scallop | It is an edible shellfish that is a mollusk with a ribbed shell in two parts. |

| Seitan | It is a plant-based meat substitute made out of wheat gluten. |

| Self-service kiosk | It refers to a self-order point-of-sale (POS) system through which customers place and pay for their own orders at kiosks, enabling totally contactless and frictionless service. |

| Smoothie | It is a beverage made by placing all the ingredients in a container and processing them together, without removing the pulp. |

| Specialty coffee & tea shops | It refers to a foodservice establishment that serves only various types of tea or coffee. |

| Standalone | It refers to a restaurants that have an independent infrastructure setup and not connected to any other business. |

| Sushi | It is a Japanese dish of prepared vinegared rice, usually with some sugar and salt, accompanied by a variety of ingredients, such as seafood—often raw—and vegetables. |

| Travel | It refers to foodservice offerings such as airplane food, dining on long-distance trains, and foodservice on cruise ships. |

| Virtual Kitchen | It refers to a cloud kitchen. |

| Wagyu Beef | It is beef derived from any of four strains of a breed of black or red Japanese cattle that are valued for their highly marbled meat. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for the market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market size estimations for the forecast years are in nominal terms. Inflation is considered for average order value, and it is forecasted as per predicted inflation rates in the countries.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms