Germany FMCG B2B E-Commerce Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

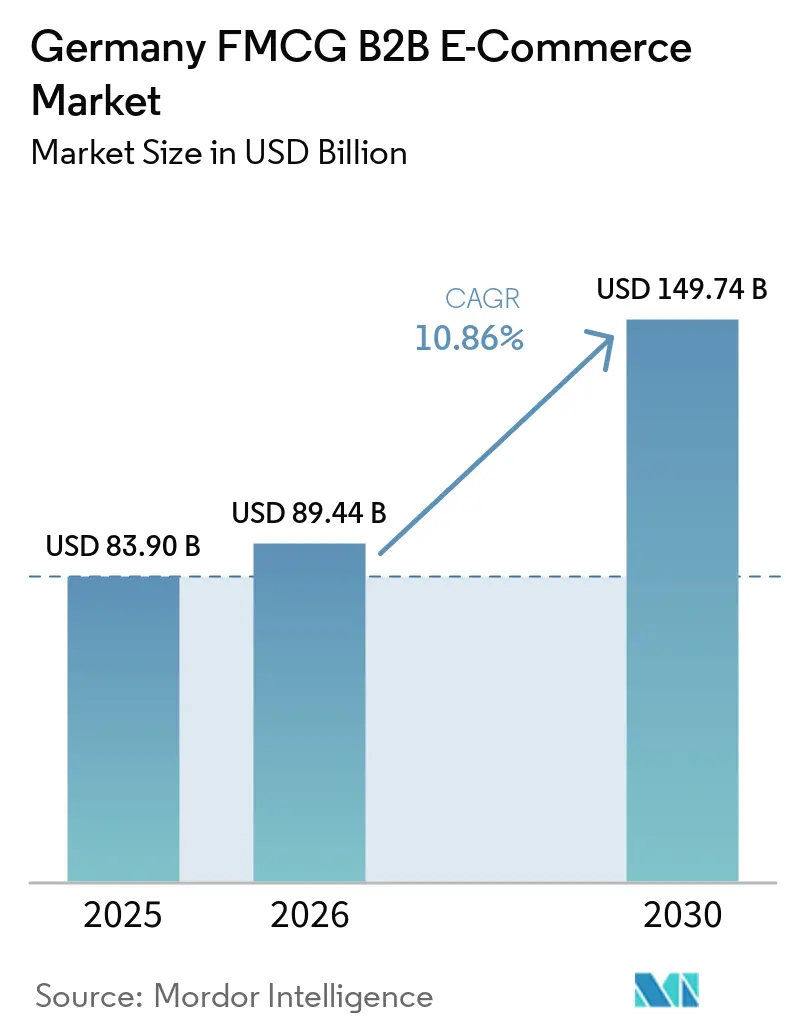

| Base Year Market Size (2025) | USD 83.90 Billion |

| Market Size (2026) | USD 89.44 Billion |

| Market Size (2030) | USD 149.74 Billion |

| Growth Rate (2026 - 2030) | 10.86% CAGR |

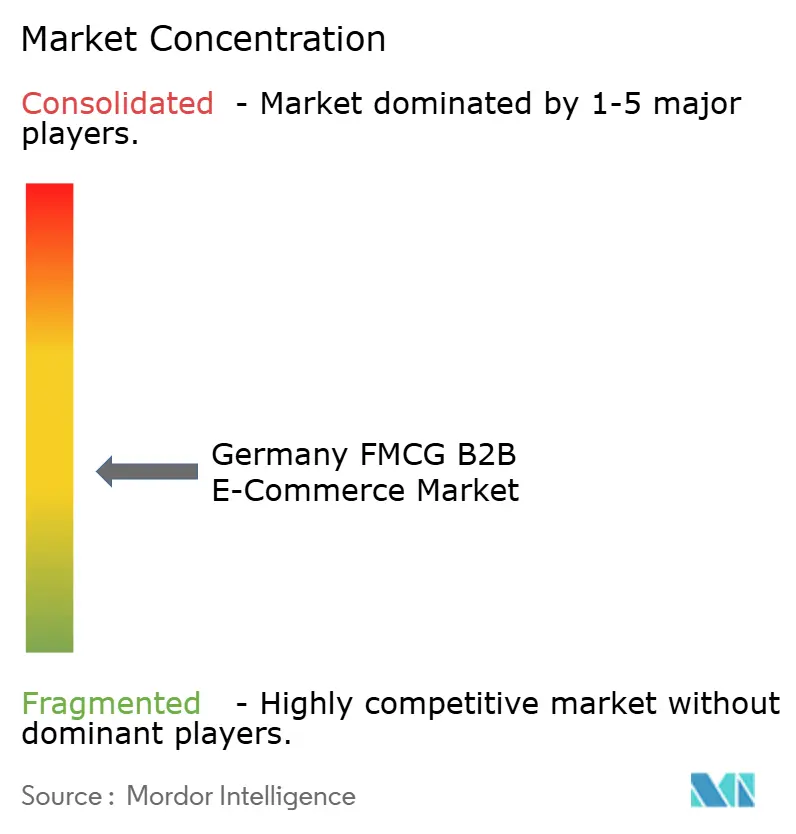

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany FMCG B2B E-Commerce Market Analysis by Mordor Intelligence

The Germany FMCG B2B E-Commerce Market size was valued at USD 83.90 billion in 2025 and is estimated to grow from USD 89.44 billion in 2026 to reach USD 149.74 billion by 2030, at a CAGR of 10.86% during the forecast period (2026-2030).

Momentum in the Germany FMCG B2B e-commerce market is reinforced by the phased rollout of mandatory B2B e-invoicing and the rapid expansion of the Peppol network, which together simplify onboarding and payment cycles across buyer and supplier ERPs. Product master data enforcement through GS1 Germany’s DQX program is elevating catalog quality, improving B2B search precision, and reducing order disputes as distributors upgrade API-first portals. Pharmacy e-prescription mainstreaming has digitized replenishment in OTC-adjacent categories and sharpened wholesale demand forecasting by enabling the lawful use of aggregated signals. As buyers adopt API, EDI, and Peppol workflows, procurement teams consolidate spend on platforms that can validate invoices in real time and reconcile VAT data with minimal manual intervention, further shifting volumes to the Germany FMCG B2B e-commerce market.

Key Report Takeaways

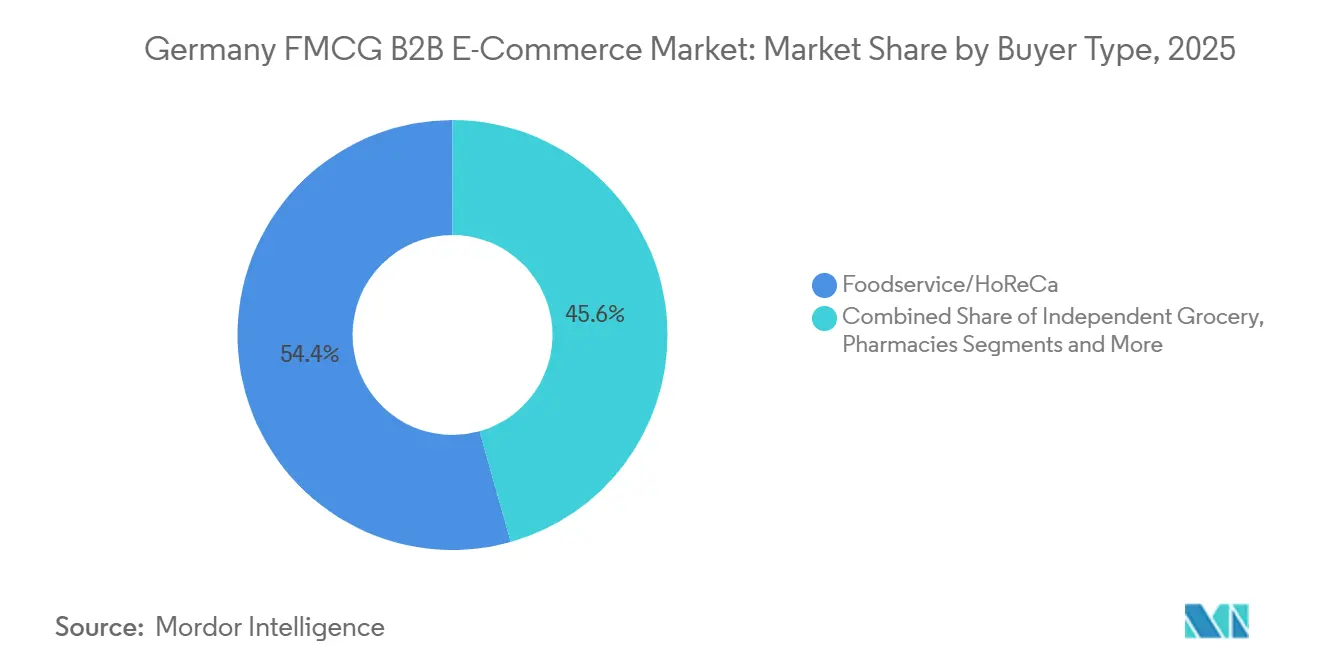

- By buyer type, Foodservice and HoReCa led the Germany FMCG B2B e-commerce market with a 54.37% revenue share in 2025, while Online-only and quick-commerce resellers are projected to expand at a 11.55% CAGR through 2031.

- By product category, Food & Beverage held 74.39% share of the Germany FMCG B2B e-commerce market in 2025, and OTC Health & Wellness is projected to grow at a 10.39% CAGR to 2031.

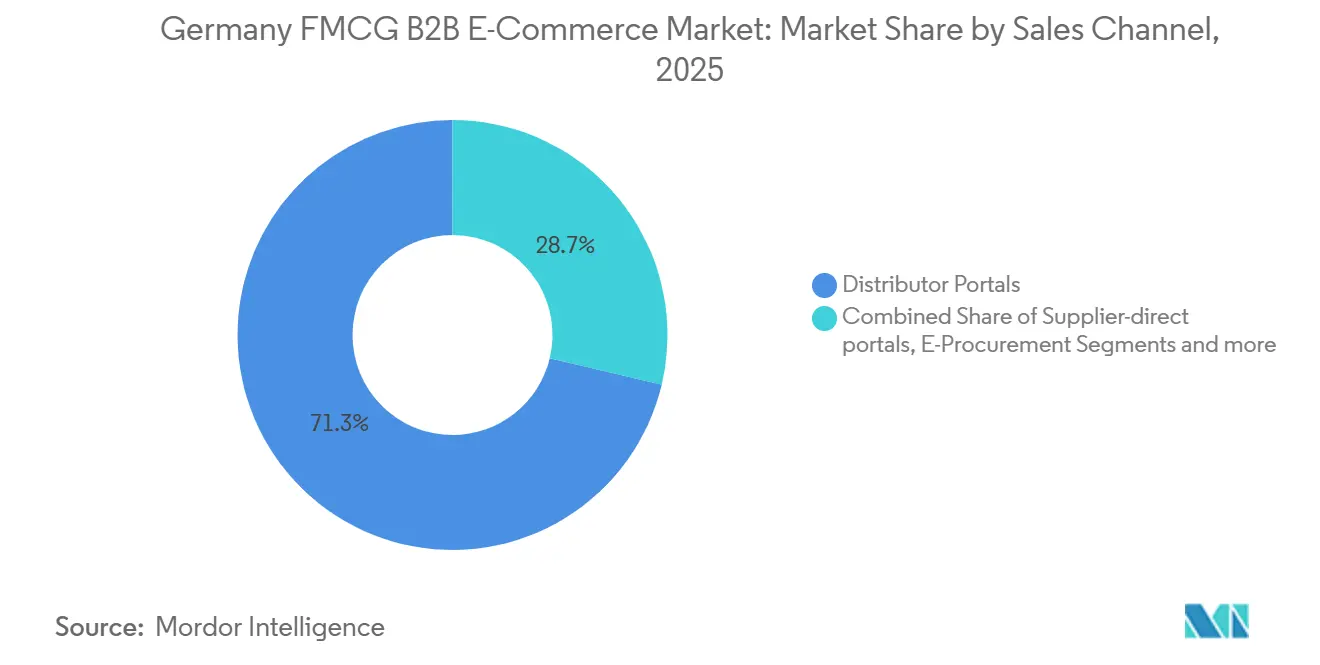

- By sales channel, company-owned distributor portals captured 71.28% share of the Germany FMCG B2B e-commerce market in 2025, and Third-party B2B marketplaces are projected to grow at a 12.58% CAGR through 2031.

- By geography, North Rhine-Westphalia accounted for 28.38% of the Germany FMCG B2B e-commerce market in 2025, while Berlin is projected to grow at a 9.40% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Germany FMCG B2B E-Commerce Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mandatory B2B e-invoicing (2025–2028) accelerates digitized ordering-to-cash and e-procurement integration | +1.8% | National and cross-border within the EU | Short term (≤ 2 years) |

| GS1 Germany DQX/GDSN enforcement raises product data quality, enabling API catalogs and richer B2B search/conversion | +1.2% | National, with early gains in North Rhine-Westphalia and Baden-Württemberg | Medium term (2-4 years) |

| Pharmacy e-prescription (E-Rezept) mainstreaming increases digital OTC/near-pharmacy B2B replenishment | +1.5% | National, strongest in dense urban markets | Short term (≤ 2 years) |

| Distributor portals’ dominance and marketplace expansion in B2B internet trade lift FMCG e-commerce penetration | +2.1% | Europe-wide, strength in NRW, Hamburg, and Berlin | Medium term (2-4 years) |

| API/EDI/Peppol readiness among larger buyers reduces onboarding frictions and shifts spend to digital channels | +1.4% | National, with strong adoption in Germany and the Nordics | Short term (≤ 2 years) |

| Supplier-direct professional portals widen SKUs and promotions for B2B buyers | +1.3% | National, with early gains in Bayern and Hesse | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Mandatory B2B E-invoicing Accelerates Digitized Ordering-to-Cash and E-Procurement Integration

Germany’s phased B2B e-invoicing mandate is anchoring the shift from email-PDF to structured, machine-readable formats and harmonizing invoice data quality across buyers and suppliers[1]European Commission, “eInvoicing in Germany - Country Factsheet,” European Commission, ec.europa.eu. The Peppol network’s rapid growth, as measured by KoSIT, confirms mainstream adoption, with monthly transmissions exceeding 300,000 in early 2026, tightening validation workflows and payment approvals across large buyer ERPs. As more enterprises standardize on EN 16931-conformant formats, dispute rates fall, and receivables cycles compress, enabling suppliers to convert working capital faster while procurement gains transaction-level transparency. Momentum is reinforced by the EU’s VAT in the Digital Age program, which promotes cross-border interoperability and supports transactional reporting foundations that Germany is preparing to leverage. The net effect for the Germany FMCG B2B e-commerce market is a lower-friction onboarding environment where Peppol-ready suppliers and API-first portals see higher RFP conversion and share-of-wallet wins among enterprise buyers. Early movers that invested in scalable invoice validation and metadata routing are positioned to gain recurring compliance advantages as more buyers mandate Peppol connectivity in 2026 sourcing cycles.

GS1 Germany DQX/GDSN Enforcement Raises Product Data Quality, Enabling API Catalogs and Richer B2B Search/Conversion

GS1 Germany’s Data Quality Excellence (DQX) service has become a de facto gatekeeper for new consumer units syndicated via GDSN in Food and Near-Food, with broad supplier adoption and a large base of validated GTINs by mid-2025. Category coverage levels signal where distributors can expect clean, API-ready attributes, with strong penetration in detergents and confectionery and more room to grow in meat, sausage, and poultry[2]GS1 Germany, “Datenqualität von FMCG-Segmenten nach Prüfvorgaben gemäß GS1 DQX,” GS1 Germany, gs1-germany.de. Release updates to the DQX Kompendium broaden visual validation and enforce mandatory communication-channel attributes in select categories, reducing manual audits and mismatches between product images and structured metadata. As distributors and marketplaces programmatically filter by certified attributes, including allergen declarations and packaging marks within GDSN payloads, B2B search relevance improves, and return rates decrease as product misunderstandings decline. Large catalogs require automated mapping to GS1 standards, as shown by AI-led attribute normalization that reconciles thousands of supplier-specific terms into target schemas at scale. For the Germany FMCG B2B e-commerce market, this codifies a quality-data premium where DQX-cleared SKUs surface higher in portal search and gain distributor preference within curated assortments.

Pharmacy E-Prescription (E-Rezept) Mainstreaming Increases Digital OTC/Near-Pharmacy B2B Replenishment

E-Rezept adoption has scaled nationwide, with redemptions crossing 1 billion by October 2025 and steady monthly volumes supporting pharmacy-side digital workflows. The predominant redemption pathway uses the electronic health card, placing the operational load on pharmacy infrastructure rather than on patient-facing apps, and aligning replenishment cycles with pharmacy ERP and wholesale interfaces. Early integration with pharmacy platforms has let leading wholesalers connect demand signals to forecasting tools and tighten inventory turns for OTC-adjacent categories in a legally compliant manner. As e-prescription data flows populate the electronic patient file, aggregated and anonymized trends help regionalize stocking strategies without breaching privacy, reinforcing the shift of replenishment orders to digital channels. Over 70 million electronic patient files were created by late 2025, expanding the available signal base for lawful, aggregated analytics and improving planning precision for pharmacy-linked assortments. The cumulative effect for the Germany FMCG B2B e-commerce market is a durable uplift in digital order penetration among pharmacies and drugstores, especially for fast-moving OTC and personal care items.

API/EDI/Peppol Readiness Among Larger Buyers Reduces Onboarding Frictions and Shifts Spend to Digital Channels

Active end users and monthly transmissions on Germany’s Peppol network grew sharply into early 2026, reducing manual invoice-processing frictions and establishing interoperability norms that larger buyers now expect. Enterprise procurement suites and custom buyer ERPs route transactions through EDI, APIs, or Peppol with automated validation, lowering order error rates and accelerating invoice approval cycles. Suppliers that expose real-time SKU availability and pricing through machine-readable endpoints meet enterprise RFP criteria more consistently, which advantages distributors with API-first architectures. Some wholesalers have paired data hubs with warehouse systems to consolidate retail and wholesale signals, improving predictive replenishment across multi-country networks and supporting faster fulfillment. Pharmacy cooperatives have also implemented AI-supported prognosis tools that link prescription workflows to inventory adjustments, a capability that enhances digital order reliability and reduces stockout risk. These technology contours are pushing more spend to digital channels in the Germany FMCG B2B e-commerce market as compliance-ready suppliers and platform intermediaries compress the cost of trading at scale.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| CO2-based Lkw-Maut and broader toll scope increase delivery costs, pushing MOQs and delivery-fee thresholds | -0.9% | National | Short term (≤ 2 years) |

| SME digitization gaps (structured e-invoice reception, clean master data) slow long-tail digital uptake | -0.7% | National, with rural concentrations | Medium term (2-4 years) |

| Reverse logistics and compliance complexity for DPG deposit handling in beverages strain small buyers | -0.5% | National | Medium term (2-4 years) |

| Cold-chain/HACCP operational constraints limit delivery windows and same-day expansion for perishables | -0.6% | National, uneven infrastructure across regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

CO2-Based Lkw-Maut and Broader Toll Scope Increase Delivery Costs, Pushing MOQs and Delivery-Fee Thresholds

Adjustments to Germany’s truck toll regime and the extension to lighter commercial vehicles have raised route costs, pushing distributors to raise minimum order quantities or introduce delivery-fee thresholds to protect margins. CO2 pricing adds to fuel costs and creates additional volatility that is difficult to hedge under fixed buyer contracts, increasing the need for dynamic pricing and careful route optimization[3]BHS Spedition und Logistik GmbH, “Road Tolls and CO2 Emissions Costs – 2023/2024/2025,” BHS Spedition, bhs-spedition.com. Urban cores can absorb these costs more efficiently due to higher route density. Still, smaller cities and rural areas face longer lead times or higher delivery thresholds as runs are consolidated. Distributors have responded by embedding backhaul optimization and, where feasible, centralized pickup of deposit-bearing beverage containers, though additional toll costs can limit the economic payoff of longer detours. In practice, this has driven buyers in lower-density zones to batch orders, which impacts replenishment cycles for fast-moving perishables and requires more precise inventory planning. The short-term effect on the Germany FMCG B2B e-commerce market is a redistribution of delivery services toward dense areas, while distributors recalibrate price floors and delivery windows.

SME Digitization Gaps (Structured E-Invoice Reception, Clean Master Data) Slow Long-Tail Digital Uptake

The new e-invoicing rules require the ability to receive structured invoices. However, many smaller buyers still rely on email-PDF workflows and struggle with validator requirements, which increases exception handling and slows payments. On the product-data side, GS1 DQX adoption is high among large brands but lags in some fresh-food categories and among smaller producers, who face the cost of PIM tooling and GDSN data-pool subscriptions. This widens the catalog-quality gap between enterprise suppliers and craft producers and increases the onboarding burden on distributors seeking to preserve long-tail assortments online. Marketplaces and procurement orchestration platforms are absorbing some of this complexity by issuing consolidated invoices and normalizing attributes at the platform level. However, suppliers still bear connection and data-prep costs. Over time, as validator adoption, GDSN compliance, and API-based catalogs become standard for SME cohorts, order accuracy will rise, and manual touchpoints will fall. Until then, these digitization gaps temper the speed at which the Germany FMCG B2B e-commerce market can bring the long tail fully online.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Buyer Type: Foodservice & HoReCa Lead Digital Procurement

Foodservice and HoReCa buyers accounted for 54.37% of the 2025 value, reflecting the scale and order frequency that restaurants, hotels, and caterers drive in B2B replenishment across ambient, chilled, and frozen staples. This buyer set also uses structured e-invoicing and portal-based ordering more often than the long tail, which increases order accuracy and compresses receivables cycles for distributors that can expose real-time inventory and pricing via APIs. In parallel, online-only and quick-commerce resellers are projected to post an 11.55% CAGR through 2031 as dark-store networks originally built for consumer grocery expand their professional-buyer assortments and delivery time windows. Pharmacies and drugstores benefit from E-Rezept adoption and associated platform integrations, which improve signal fidelity for OTC replenishment and drive higher digital order shares across adjacent personal care and wellness categories[4]PHOENIX Pharmahandel GmbH & Co KG, “Annual Report 2024/25,” PHOENIX Group, phoenixgroup.eu. Larger retail chains standardize purchasing through API, EDI, or Peppol connections and expect machine-readable endpoints, while independent stores and kiosks adopt at a slower pace, which sustains the need for hybrid, phone-to-portal workflows during the transition. These patterns combine to deepen the Germany FMCG B2B e-commerce market’s reliance on digital-first buyer cohorts, even as distributors maintain analog order capture for late adopters.

The Germany FMCG B2B e-commerce market share held by Foodservice and HoReCa in 2025 underscores how route density, product breadth, and portal adoption reinforce one another in this buyer group. For quick-commerce operators, the Germany FMCG B2B e-commerce market size for professional buyers is set to rise alongside new buyer services, such as consolidated invoicing and curated wholesale packs, which improve economics at case and pallet quantities. Pharmacy cooperatives and larger drugstore formats are using e-prescription volumes to tune demand models and raise the productivity of wholesale interfaces, with evidence from national platforms that aggregate e-prescriptions and integrate with medication lists. Across buyer types, Peppol-connected procurement and API catalogs reduce onboarding friction and error rates, encouraging buyers to consolidate suppliers onto a smaller set of compliant portals and marketplaces. As coverage expands, distributors that can validate invoices, surface certified attributes, and align delivery promises by buyer segment will capture a greater share of wallet in the Germany FMCG B2B e-commerce market.

By Product Category: Food & Beverage Dominates, OTC Health Gains Digital Traction

Food & Beverage accounted for 74.39% of the 2025 value, driven by SKU breadth and delivery cadence in HoReCa and proximity retail. OTC Health & Wellness is projected to grow at a 10.39% CAGR through 2031 as E-Rezept adoption synchronizes pharmacy workflows with wholesaler systems and accelerates same-day or next-day replenishment for fast-turn OTC categories. Household & Cleaning contributes a solid share and benefits from high DQX penetration that elevates attribute completeness for GDSN-syndicated SKUs, including eco-labels and safety data that B2B buyers filter in procurement portals. Personal Care & Beauty uptake follows similar patterns, with DQX validation lifting data quality and decreasing returns caused by inadequate or inconsistent product descriptions. In Pet Care, new DQX checks that require communication-channel attributes strengthen SKU discoverability and reduce customer-service friction post-purchase, helping portals increase conversion. Together, these category-level changes reinforce the role of mandated data standards and pharmacy digitization in shaping the growth trajectory of the Germany FMCG B2B e-commerce market.

The Germany FMCG B2B e-commerce market size is also influenced by the balance between breadth and compliance depth within category portfolios, where GS1 DQX-certified SKUs receive preferred placement and fewer returns in distributor catalogs. For OTC Health & Wellness, e-prescription data aggregated on pharmacy platforms supports more accurate, privacy-compliant forecasting, reducing out-of-stocks and improving turnover rates. Household & Cleaning and Personal Care & Beauty gain from attribute-driven search improvements as procurement platforms filter by allergen-free claims, certifications, and usage instructions embedded in GDSN payloads. Food & Beverage remains structurally advantaged through route density and portal penetration in HoReCa, although cold-chain constraints and toll-driven delivery costs shape service-level offerings by region. Across all categories, the interplay of DQX enforcement and e-invoicing compliance is tilting buyers toward platforms that package validation, certified data, and reliable delivery into a single interface across the Germany FMCG B2B e-commerce market.

By Sales Channel/Platform Type: Distributor Portals Dominate, Marketplaces Surge

Company-owned distributor portals captured 71.28% of 2025 value, reflecting the advantage of integrated inventory, credit, and delivery orchestration within established wholesale networks. Third-party B2B marketplaces are projected to grow at a 12.58% CAGR through 2031 as multi-vendor catalogs, unified invoicing, and API-first integration reduce procurement frictions for professional buyers that need breadth and compliance in a single workflow. Platforms that issue consolidated invoices and connect supplier catalogs through PunchOut or APIs can help buyers enforce account-wide procurement policies while enabling suppliers to meet structured-invoice and metadata requirements. AI-driven mapping that reconciles supplier taxonomies with standardized attributes has become the backbone of marketplace catalog onboarding, ensuring consistent search and comparison experiences across millions of SKUs. E-procurement integrations that route POs via Peppol or EDI and validate structured invoices upstream now differentiate portals and marketplaces in enterprise RFPs, improving win rates among buyers with strict compliance policies. This blend of catalog science and compliance plumbing is key to sustaining share gains across the Germany FMCG B2B e-commerce market.

For portals, scale economics in warehousing and delivery enable competitive fees and tighter service levels, while marketplaces add value by simplifying onboarding, validating supplier data, and consolidating billing for buyers. Supplier-direct portals from major CPG firms complement both models by offering category depth, IoT-linked replenishment in selective segments, and access to branded content, then stitching fulfillment through wholesale logistics when needed. As Peppol adoption spreads and DQX validation becomes the norm, both distributors and marketplaces continue to converge on API-first architectures that move buyers toward a single source of truth for pricing, availability, and invoicing. The Germany FMCG B2B e-commerce market will likely see continued shifts in share between large distributor portals and compliance-capable marketplaces as buyers optimize for data quality, invoice automation, and delivery reliability.

Geography Analysis

North Rhine-Westphalia accounted for 28.38% of the 2025 value, supported by population scale, dense HoReCa networks, and proximity to major freight corridors that reinforce route efficiency for frequent replenishment. Berlin is projected to grow at a 9.40% CAGR through 2031, driven by a concentration of digitally native operators, high foodservice density, and platform adoption that capitalizes on short-haul delivery radius economics. Pharmacy digitization deepens urban digital order penetration and gives wholesalers more reliable planning inputs through e-prescription signals and lawful, anonymized patient-file aggregation. Peppol growth, as tracked by KoSIT, is reinforcing a nationwide baseline for structured invoicing, which eases cross-Land procurement, invoice validation, and payment automation for multi-site buyers. These elements, when combined, improve the addressable reach of compliant portals and marketplaces across leading urban and peri-urban clusters in the Germany FMCG B2B e-commerce market.

Hamburg’s freight and logistics digitization supports faster truck processing and improved supply chain visibility, benefiting FMCG distributors that rely on the port for inbound flows. City-driven initiatives to scale AI across logistics improve routing, simulation, and resource allocation, which aligns with distributor needs to optimize multi-stop, temperature-controlled runs within tight time windows. As Hamburg deploys digital identity and slot-booking tools for container movements, dwell times fall, which reduces variability in replenishment turns for wholesale networks that feed nearby states. This infrastructure backdrop helps portals maintain predictable availability and delivery SLAs for high-volume urban accounts, thereby strengthening the share of digital channels in the Germany FMCG B2B e-commerce market.

Across the Rest of Germany, category-level GS1 DQX penetration shows where attribute quality supports richer B2B search and lower return rates, with detergents and confectionery leading and select fresh-food segments trailing. Local digitization programs also matter, as seen in Düsseldorf’s Retail+ DUS initiative that gives smaller retailers and gastronomy operators a path to test new tools and workflows. Combined with structured e-invoicing and growing Peppol reach, these state and city programs reduce the practical barriers to onboarding and shift more of the long tail into compliant digital channels. While toll and CO2 cost pressures remain higher outside dense cores, the balance of digitized ordering, validated catalog data, and unified invoicing supports steady expansion of the Germany FMCG B2B e-commerce market beyond top metros.

Competitive Landscape

The Germany FMCG B2B e-commerce market remains moderately fragmented, with the top five players together accounting for roughly 48% of the 2025 value and no single operator above 15%. Competitive intensity is defined by three core capabilities: omnichannel infrastructure spanning self-service cash-and-carry, delivery fleets, and digital order capture. The second is compliance-grade plumbing that validates structured invoices and synchronizes master data, improving buyer confidence and cash cycle predictability. The third is data science that forecasts demand and optimizes replenishment using aggregated, lawful signals, reducing out-of-stocks and maintaining consistent service levels. Operators that can package these capabilities into API-first portals gain advantages in RFPs and enterprise integrations. At the same time, marketplaces win by bundling data quality, invoicing, and catalog normalization into a single workflow.

Strategic moves by leading wholesalers demonstrate a clear focus on pharmacy platform integration, data hubs, and compliant digital flows. PHOENIX has scaled a national digital health platform that unites pharmacies, patients, and service providers, enabling e-prescription integration and registered orders at meaningful volume by FY 2024/25. The group also built a centralized data hub to integrate wholesale and retail signals across countries, which feeds predictive replenishment and improves localization of assortments. NOWEDA enhanced its pharmacy platform with e-prescription capabilities and implemented an AI-supported prognosis tool to model supply bottlenecks and adjust purchasing directly. These moves position both firms to capture more OTC-adjacent flow as pharmacy orders digitize and as buyers prefer portals with verified catalog data and fast validation across invoices and receipts.

On the platform side, procurement networks are competing on standards alignment, onboarding speed, and attribute consistency. Unite’s model consolidates invoicing, documents competition for buyers, and exposes catalog integrations that reduce manual steps, which helps capture spend from enterprises that require uniform policy enforcement. AI-based mapping, highlighted by technology partners, shows how marketplaces can reconcile tens of thousands of supplier source attributes into target schemas, thereby improving discoverability and comparability across long-tail assortments. As GS1 DQX releases extend visual validations and enforce new attribute checks, distributors and marketplaces that operationalize these standards will lower return rates and raise buyer trust. With Peppol usage still rising, compliance-grade invoice validation and data governance will remain decisive in share shifts across the Germany FMCG B2B e-commerce market.

Germany FMCG B2B E-Commerce Industry Leaders

METRO Deutschland

Transgourmet Deutschland

EDEKA Foodservice / EDEKA Convenience

CHEFS CULINAR

Lekkerland (REWE)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: GS1 Germany released DQX Kompendium v1.9.3, adding new product-data validation codes and stricter image compliance checks, reinforcing digital catalog quality standards for suppliers and distributors.

- March 2025: Düsseldorf opened the Retail+ DUS showroom, showcasing AI, robotics, smart POS, and energy management tools to accelerate digitalization in SME retail and gastronomy.

- February 2026: GS1 Germany published a new Category Vision whitepaper focused on future-ready assortment planning and shopper-centric category management. The initiative supports FMCG suppliers and distributors by improving digital data standards and providing collaborative planning tools.

- January 2025: CHEFS CULINAR expanded its nationwide digital foodservice ordering capabilities, including online procurement tools for horeca and institutional buyers, strengthening Germany’s fast-growing professional FMCG e-commerce segment.

Germany FMCG B2B E-Commerce Market Report Scope

The Germany FMCG B2B E-Commerce Market involves the online trade of fast-moving consumer goods, including food, beverages, household products, personal care items, and convenience goods, between businesses such as wholesalers, manufacturers, retailers, restaurants, hotels, pharmacies, and other commercial buyers through digital platforms, marketplaces, and direct ordering portals.

The Germany FMCG B2B E-commerce Market Report is Segmented by Buyer Type (Independent Grocery & Specialty Retailers, Chain Supermarkets & Mass Merchandisers, Convenience Stores & Gas Stations, Foodservice/HoReCa, Pharmacies & Drugstores, Online-only and Quick-commerce Resellers, Institutional, Office & Janitorial Buyers), Product Category (Food & Beverage, Household & Cleaning, Personal Care & Beauty, OTC Health & Wellness, Pet Care, Baby & Family Care), Sales Channel/Platform Type (Distributor-managed Portals, CPG/Supplier-direct Portals, Third-party B2B Marketplaces, E-procurement/API/EDI-integrated), and Geography (Berlin, Hamburg, Nordrhein-Westfalen, Rest of Germany). The Market Forecasts are Provided in Terms of Value (USD).

| Independent grocery & specialty retailers |

| Chain supermarkets & mass merchandisers |

| Convenience stores & gas stations |

| Foodservice/HoReCa (restaurants, cafes, catering) |

| Pharmacies & drugstores |

| Online-only and quick-commerce resellers |

| Institutional, office & janitorial buyers |

| Other Products |

| Food & beverage |

| Household & cleaning |

| Personal care & beauty |

| OTC health & wellness |

| Pet care |

| Baby & family care |

| Other Products |

| Distributor-managed portals |

| CPG/supplier-direct portals |

| Third-party B2B marketplaces |

| E-procurement/API/EDI-integrated |

| Berlin |

| Hamburg |

| Nordrhein-Westfalen |

| Rest of Germany |

| By Buyer Type | Independent grocery & specialty retailers |

| Chain supermarkets & mass merchandisers | |

| Convenience stores & gas stations | |

| Foodservice/HoReCa (restaurants, cafes, catering) | |

| Pharmacies & drugstores | |

| Online-only and quick-commerce resellers | |

| Institutional, office & janitorial buyers | |

| Other Products | |

| By Product Category | Food & beverage |

| Household & cleaning | |

| Personal care & beauty | |

| OTC health & wellness | |

| Pet care | |

| Baby & family care | |

| Other Products | |

| By Sales Channel/Platform Type | Distributor-managed portals |

| CPG/supplier-direct portals | |

| Third-party B2B marketplaces | |

| E-procurement/API/EDI-integrated | |

| By Geography | Berlin |

| Hamburg | |

| Nordrhein-Westfalen | |

| Rest of Germany |

Key Questions Answered in the Report

What is the current size and expected growth of the Germany FMCG B2B e-commerce market?

The Germany FMCG B2B e-commerce market size is USD 83.90 billion in 2025, projected to reach USD 149.74 billion by 2031 at a 10.86% CAGR.

Which buyer segment leads and which is growing fastest in Germany?

Foodservice and HoReCa lead with 54.37% of value in 2025, while online-only and quick-commerce resellers are projected to grow the fastest at 11.55% CAGR to 2031.

Which product category dominates and which will expand the most?

Food & Beverage dominates at 74.39% of value in 2025, and OTC Health & Wellness is projected to post the highest growth at 10.39% CAGR through 2031.

Which sales channel is largest and which is set to scale fastest?

Company-owned distributor portals hold 71.28% of value in 2025, while third-party B2B marketplaces are projected to grow at 12.58% CAGR through 2031.

How do e-invoicing and Peppol adoption affect procurement cycles?

Phased e-invoicing and rising Peppol usage reduce invoice errors, shorten approvals, and improve compliance, which shifts more enterprise spend to integrated portals and marketplaces.

Which region in Germany is projected to grow quickest?

Berlin is projected to grow at 9.40% CAGR through 2031, aided by high digital adoption and dense foodservice demand.

Page last updated on: